February 13 th 2015 Credicorp Capital Research Andean Daily Report CREDICORP CAPITAL RESEARCH Chile: +(562) 2450 1600 Colombia: +(571) 339 4400 Ext. 1505 Peru: +(511) 205 9190 Ext. 36070 CHILE The Central Bank maintained the monetary policy rate at 3.0% Company Update: Sigdo Koppers – HOLD. Not the right moment yet; downgrading from Buy to Hold COLOMBIA EEB was awarded a new transmission project in south-west Colombia Canacol reported financials for fiscal 2Q15; results were negative in our view Shareholder of Sociedades Bolívar approve capital increase BoD of Banco de Bogota proposes a monthly dividend distribution of COP 210/share PERU The Central Bank kept its rate unchanged at 3.25% The Ministry of Energy and Mines (MINEM) presented projects Communities call for dialogue regarding the Bambas project Cerro Verde posted a 72% (y/y) drop in net income - 4Q14 results This report is property of IM Trust S.A. and/or Credicorp Capital Colombia S.A Sociedad Comisionista de Bolsa and/or Credicorp Capital S.A.A. and/or its subsidiaries (hereinafter jointly called “Credicorp Capital”), therefore, no part of this the material or its content, nor any copy of it may altered in any way, transmitted, copied or distributed to any third party without prior and express written consent of Credicorp Capital. In making this report, Credicorp Capital has relied on information from public sources. Credicorp Capital has not verified the truthfulness, completeness or accuracy of the information accessed, nor has audit the information in any way. Accordingly, this report does not constitute a statement, assertion or guarantee (express or implied) as to the truth, accuracy or completeness of the information contained herein or any other written or oral information furnished to any person and/or their advisors. Local USD Local USD S&P MILA 40 611 1.5% 1.5% -4.0% -4.0% S&P INDEX 2,088 1.0% 1.0% 1.4% 1.4% Chile 3,964 1.1% 2.3% 2.9% 0.3% Colombia 1,381 0.0% 1.5% -8.7% -9.1% Peru 13,679 1.3% 1.8% -7.5% -10.4% Mexico 43,046 2.7% 4.1% -0.2% -1.3% Brazil 49,533 2.7% 4.6% -0.9% -7.2% Equities Latam 2,595 3.2% 3.2% -4.8% -4.8% CLP / US$ 622 UF / CLP 24,531 Peru / US$ 3.07 Colombia / US$ 2,389 Brazil / US$ 2.82 CLP / Euro 709 Euro / US$ 1.14 Local USD Local USD Copper (US$/lb) 260 Gold (US$/oz) 1,221 Silv er (US$/oz) 16.8 Brent (US$/bbl) 57 Pulp (US$/MT) 903 WTI (US$/bbl) 51 Index Last D/D % YTD% Fx Rates Last D/D % YTD% -1.3% 2.5% 0.0% -0.4% -0.5% 3.0% -1.5% 0.5% -1.7% 6.6% -0.7% -3.2% 0.6% -5.7% Commodities Last D/D % YTD% 2.4% -7.9% -1.5% -3.1% 4.9% -3.9% 0.1% 3.0% 0.2% 7.7% 5.2% 2.3% P/BV 2 0 14 E 2 0 15 E 2 0 14 E 2 0 15 E LTM Chile 20.4x 16.9x 9.0x 8.3x 1.7x Colombia 18.9x 22.0x 8.0x 8.3x 1.3x Peru 14.7x 13.4x 7.8x 7.1x 1.3x Valuations Country P / E EV / EBITDA

Transcript

February 13th 2015

Credicorp Capital Research

Andean Daily Report

CREDICORP CAPITAL RESEARCH

Chile: +(562) 2450 1600

Colombia: +(571) 339 4400 Ext. 1505

Peru: +(511) 205 9190 Ext. 36070

CHILE

The Central Bank maintained the monetary policy rate at 3.0%

Company Update: Sigdo Koppers – HOLD. Not the right moment yet;

downgrading from Buy to Hold

COLOMBIA

EEB was awarded a new transmission project in south-west Colombia

Canacol reported financials for fiscal 2Q15; results were negative in

our view

Shareholder of Sociedades Bolívar approve capital increase

BoD of Banco de Bogota proposes a monthly dividend distribution of

COP 210/share

PERU

The Central Bank kept its rate unchanged at 3.25%

The Ministry of Energy and Mines (MINEM) presented projects

Communities call for dialogue regarding the Bambas project

Cerro Verde posted a 72% (y/y) drop in net income - 4Q14 results

This report is property of IM Trust S.A. and/or Credicorp Capital Colombia S.A Sociedad Comisionista de Bolsa and/or Credicorp Capital S.A.A. and/or its subsidiaries (hereinafter jointly called “Credicorp Capital”), therefore, no part of this the material or its content, nor any copy of it may altered in any way, transmitted, copied or distributed to any third party without prior and express written consent of Credicorp Capital. In making this report, Credicorp Capital has relied on information from public sources. Credicorp Capital has not verified the truthfulness, completeness or accuracy of the information accessed, nor has audit the information in any way. Accordingly, this report does not constitute a statement, assertion or guarantee (express or implied) as to the truth, accuracy or completeness of the information contained herein or any other written or oral information furnished to any person and/or their advisors.

Local USD Local USD

S&P MILA 40 611 1.5% 1.5% -4.0% -4.0%

S&P INDEX 2,088 1.0% 1.0% 1.4% 1.4%

Chile 3,964 1.1% 2.3% 2.9% 0.3%

Colombia 1,381 0.0% 1.5% -8.7% -9.1%

Peru 13,679 1.3% 1.8% -7.5% -10.4%

Mex ico 43,046 2.7% 4.1% -0.2% -1.3%

Brazil 49,533 2.7% 4.6% -0.9% -7.2%

Equities Latam 2,595 3.2% 3.2% -4.8% -4.8%

CLP / US$ 622

UF / CLP 24,531

Peru / US$ 3.07

Colombia / US$ 2,389

Brazil / US$ 2.82

CLP / Euro 709

Euro / US$ 1.14

Local USD Local USD

Copper (US$/lb) 260

Gold (US$/oz) 1,221

Silv er (US$/oz) 16.8

Brent (US$/bbl) 57

Pulp (US$/MT) 903

WTI (US$/bbl) 51

Index LastD/D % YTD%

Fx Rates LastD/D % YTD%

-1.3% 2.5%

0.0% -0.4%

-0.5% 3.0%

-1.5% 0.5%

-1.7% 6.6%

-0.7% -3.2%

0.6% -5.7%

Commodities LastD/D % YTD%

2.4% -7.9%

-1.5% -3.1%

4.9% -3.9%

0.1% 3.0%

0.2% 7.7%

5.2% 2.3%

P/BV

2 0 14 E 2 0 15 E 2 0 14 E 2 0 15 E LTM

Chile 20.4x 16.9x 9.0x 8.3x 1.7x

Colombia 18.9x 22.0x 8.0x 8.3x 1.3x

Peru 14.7x 13.4x 7.8x 7.1x 1.3x

Va lua tions

CountryP / E EV / EBITDA

2

Chile

Economics and Politics

The Central Bank maintained the monetary policy rate at 3.0%

The Central Bank maintained the policy rate at 3.00% during yesterday’s meeting, in line with the

market’s expectation and our own. While economic activity continues to grow under the potential

trend (2.9% y/y in December), it has shown a rebound in the last month, especially with the

monthly expansion of 1.0% occurred in December, the highest in the last 18 months. On the other

hand, the highest level of current inflation (4.5%) has prevented the possibilities of further

monetary cuts. Annual inflation has slowly decreased to the current level of 4.5% y/y, still above

the upper bound of the target range, but core inflation has been rising, reaching 5.5% y/y (CPIX)

in January. We forecast that the policy rate would remain at 3.00% over the coming months,

unless core inflation returns to the target rate levels or if the economic activity shows growth rates

under 1.0%. The price of copper may condition our base case scenario.

Company News

Company Update: Sigdo Koppers – HOLD

Not the right moment yet; downgrading from Buy to Hold

(SK; HOLD; T.P.: CLP 950)

We are updating our coverage of SK, downgrading our BUY recommendation to HOLD, and

reducing our 2015YE target price from $ 1,150 to $ 950, implying a total return of 14%. Our target

price is based on a 50/50 blended DCF and relative multiple analysis. Despite our confidence in

the strong fundamentals of the company, we hold a cautious view towards the stock in the short

term, reflecting volatility in copper prices, as well as political and economic uncertainty in Chile.

Colombia

Company News

EEB was awarded a new transmission project in south-west Colombia

(EEB: Buy; T.P.: COP 1,930)

EEB was awarded a 500 kV transmission project in the departments of Antioquia, Caldas,

Quindío, Risaralda and Valle del Cauca in Colombia. The total estimated CAPEX of the project is

USD ~350 mn. EEB won the project with a proposal of USD 198 mn in net present value. The

announcement is good news for the company which continues to consolidate its presence in the

transmission segment in Colombia. However, we do not expect a significant impact on the share

price, given the relatively low size of the project, as its NPV represents near 3% of the current

Market Cap of the company.

3

Canacol reported financials for fiscal 2Q15; results were negative in our view

(CANACOL: UNDERPERFORM; TP COP 5,720)

Canacol Energy reported operating & financial results for the second fiscal quarter of 2015.

Although revenues were in line with our expectations, we highlight that EBITDA and net income

showed double-digit downward deviation relative to our estimate. Furthermore, total production in

the quarter reached 11,822 boepd equivalent to a 10.8% q/q decline; average daily production for

2014 (calendar year) was placed at 12,046 boepd, below the company’s revised guidance of

12,500 – 13,000 boepd. We reiterate our UNDERPERFORM on the back of low visibility in terms

of revenue growth before the gas contracts initiate delivery in Dec – 2015 and uncertainty due to

lower oil prices. We expect a negative reaction on shares of Canacol in the absence of a strong

rebound of oil prices during tomorrow’s trading session.

Shareholder of Sociedades Bolívar approve capital increase

The shareholder’s meeting of Sociedades Bolívar approved a Capital increase and the

registration of the shares in the National Register of Securities and Issuers (RNVE in Spanish)

and the Colombia stock exchange (BVC). Sociedades Bolivar, a holding company with

investments in construction, insurance and financial services (controlling shareholder of

Davivienda), approved the issuance of preferred (non-voting) shares and their registration in the

National Register of Securities and Issuers and the Colombia stock exchange. So far, no details

have been provided about the operation but the announcement leads to a potential IPO of one of

Colombia’s largest financial conglomerates.

BoD of Banco de Bogota proposes a monthly dividend distribution of COP 210/share

(BOGOTA: UNDERPERFORM; TP COP 66,100)

The BoD of Banco de Bogota proposed a monthly dividend distribution of COP 210/share

between April and September 2015 on the net income of the 2H14. The distribution represents an

annualized dividend yield of 4% at current share prices.

Canacol Energy

(USD mn)

Rev enues 37.9 43.2 37.4 -12.3% 1.3% P/E 21.3x

EBITDA 6.8 18.7 18.0 -63.9% -62.5% EV/EBITDA 5.6x

Net Income -46.0 -10.4 2.8 NA NA P/BV 0.7x

Div . Yield 0.0%

EBITDA Mg. 17.8% 43.3% 48.2%

Net Mg. -121.3% -24.1% 7.4%

Canacol 2015E2FQ15A 2FQ14A 2FQ15E A/A (%) A/E (%)

4

Peru

Economics and Politics

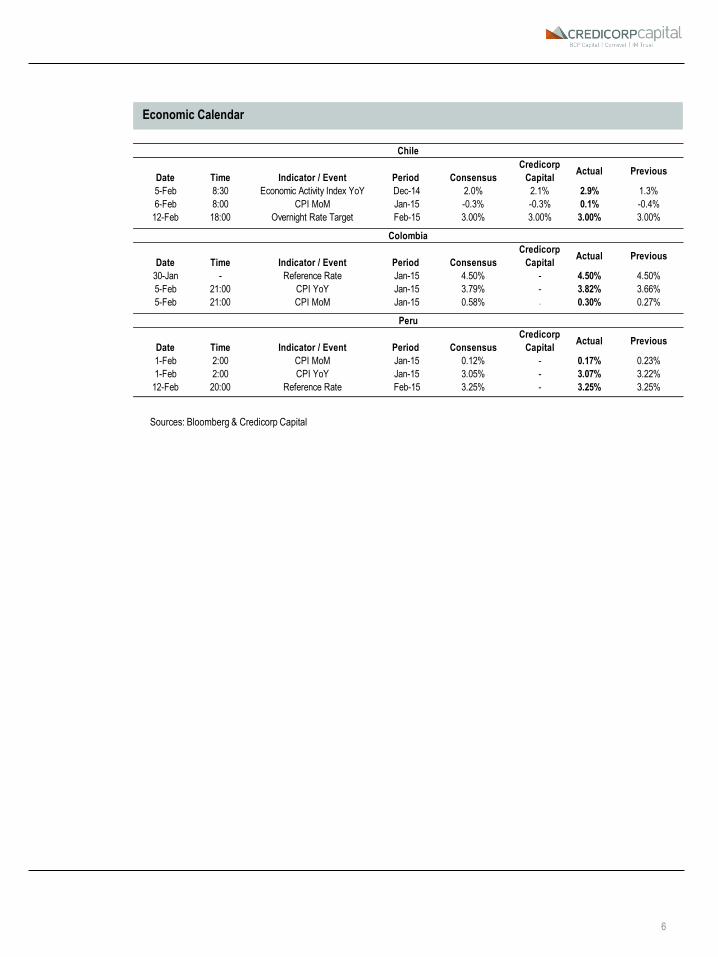

The Central Bank kept its rate unchanged at 3.25%

The monetary authority of Peru said that it kept its main policy instrument unchanged because it

sees it compatible with a 2.0% inflation rate. Its official note highlighted that: i) Economic activity

remains below its potential; ii) inflation expectations seem anchored within the target range; and

iii) international indicators show mixed signs of world economy recovery.

The Ministry of Energy and Mines (MINEM) presented projects

During the Forum organized by the Peruvian Foreign Trade Society, Eleodoro Mayorga, Minister

of Energy and Mines, presented a legislative initiative to allow the entrance of Petroperu into the

oil production segment. According to Mayorga, this proposal would apply to the lots with proven

oil reserves and Petroperu would have a minority stake of 25%. In addition, Mayorga also stated

that it is expected that the southern natural gas pipeline initiates its operations by 2018 and the

construction of a natural gas pipeline to the north should begin during the next ten years.

Communities call for dialogue regarding the Bambas project

The communities and organizations in the Challhuahuacho district in Cotabambas (Apurímac),

demand a dialogue with the authorities of the region and the Presidency of the Minister Council

(PCM in Spanish). They are demanding that the company MMG Limited, owner of Las Bambas

mining project, complies with what was agreed by its predecessor, Xstrata Glencore. It is

important to mention that the mining conflicts observatory reported that those communities have

just completed a 72-hour strike and threaten to extend it indefinitely from February 13th, if their

request is not accepted.

Company News

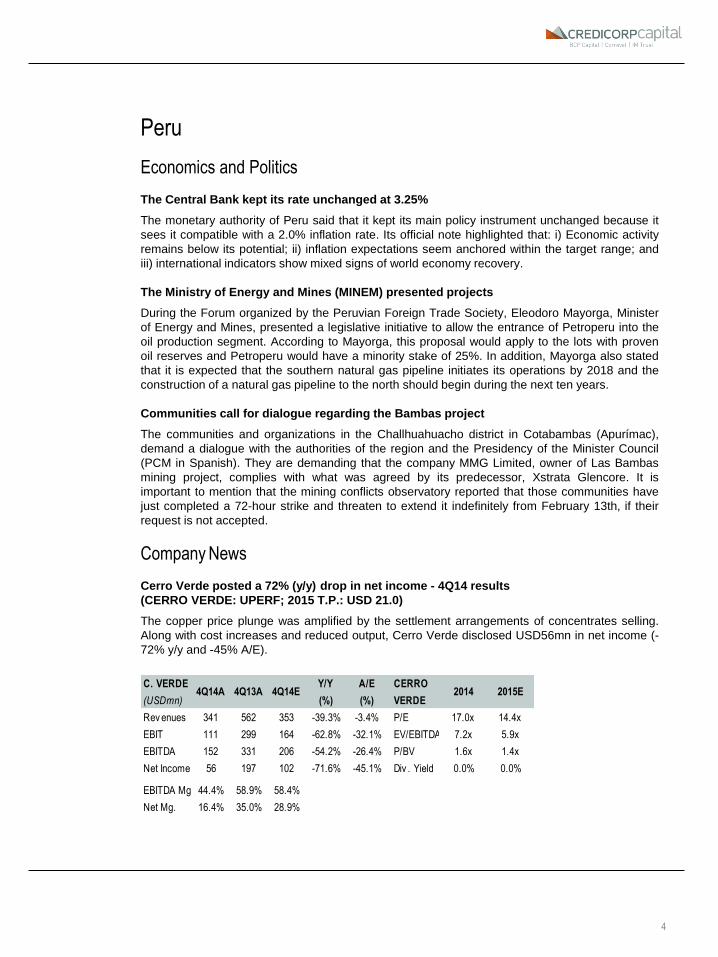

Cerro Verde posted a 72% (y/y) drop in net income - 4Q14 results

(CERRO VERDE: UPERF; 2015 T.P.: USD 21.0)

The copper price plunge was amplified by the settlement arrangements of concentrates selling.

Along with cost increases and reduced output, Cerro Verde disclosed USD56mn in net income (-

Arturo Prado Juan C. Domínguez Iván Bogarín René Ossa Rodrigo Zavala Juan A. Jiménez

Senior Analyst: Natural Resources Senior Analyst: Banks Senior Analyst: Retail & Others International Equity Sales Head of Equity - Peru Head of International Equity Sales

Paulina Yazigi Daniel Velandia Irvin León Guido Riquelme Christian Jarrin Vallerie Yong

Head of Research & Chief Economist Head of Research & Chief Economist Senior Fixed Income Analyst Head of Sales RM Fixed Income Offshore Local FI Senior Trader

Felipe Lubiano Sergio Ferro Alberto Zapata Belén Larraín Andrés Valderrama Evangeline Arapoglou

Senior Fixed Income Analyst Fixed Income Analyst Fixed Income Analyst Head of International FI Sales Fixed Income Trader Senior International FI Trader

![Invariant Shape Features and Relevance Feedback for Weld ... · Sym [0 1] < 0.5 > 0.5 > 0.5 < 0.5 Sig [0 1] < 0.5 < 0.5 → 1 > 0.5 2.2 Generic Fourier descriptor](https://static.documents.pub/doc/80x56/5fb60fbe46489e03c70e3474/invariant-shape-features-and-relevance-feedback-for-weld-sym-0-1-05.jpg)