16

· 1 Dilutive Securities and EPS CORPORATE FINANCIAL REPORTING 2 19 - Financial Reporting Of Income Taxes

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 221 times |

| Download: | 0 times |

· 1Dilutive Securities and EPS

CORPORATE FINANCIAL REPORTING 2

19 - Financial Reporting Of Income Taxes

Financial Reporting of Income Taxes· 2

ACCOUNTING FOR INCOME TAXES

I. Tax loss carryback & carryforwardII. Tax allocation because of differences between public reporting and tax returns: A. Differences either called:

1. temporary differences (create

“deferred income taxes”) 2. permanent differences

B. Accounting for differences

Financial Reporting of Income Taxes · 3

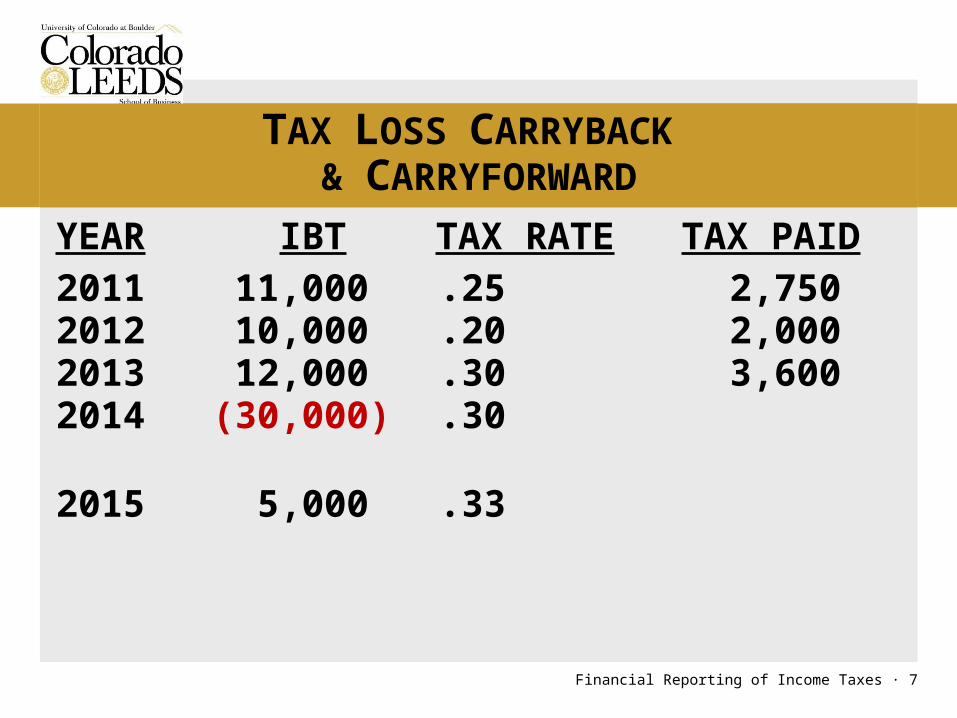

TAX LOSS CARRYBACK & CARRYFORWARD

YEAR IBT TAX RATE TAX PAID2011 11,000 .25 2,7502012 10,000 .20 2,0002013 12,000 .30 3,6002014 (30,000) .30

Tax journal entries for 2011, 2012 and 2013 are straight forward.

Financial Reporting of Income Taxes · 4

TAX LOSS CARRYBACK & CARRYFORWARD

IRS says we can do one of two things with our loss.

Financial Reporting of Income Taxes · 5

TAX LOSS CARRYBACK & CARRYFORWARD

We choose to carryback the loss, what will our accountant do?

Financial Reporting of Income Taxes · 6

TAX LOSS CARRYBACK & CARRYFORWARD

We still have some loss we couldn’t carryback – what will we do with that remaining loss if management says: “It is more likely than not that we will have at least $8,000 of income in the next 20 years.”?

Financial Reporting of Income Taxes · 7

TAX LOSS CARRYBACK & CARRYFORWARD

YEAR IBT TAX RATE TAX PAID2011 11,000 .25 2,7502012 10,000 .20 2,0002013 12,000 .30 3,6002014 (30,000) .30

2015 5,000 .33

Financial Reporting of Income Taxes · 8

TAX LOSS CARRYBACK & CARRYFORWARD

YEAR IBT TAX RATE TAX PAID2011 11,000 .25 2,7502012 10,000 .20 2,0002013 12,000 .30 3,6002014 (30,000) .30

2015 5,000 .332016 9,000 .34

Financial Reporting of Income Taxes · 9

TAX LOSS CARRYBACK & CARRYFORWARD

“It is more likely than not that we will not have sufficient income in the future to use all of the loss carryforward. We estimate that we will only have $2,000 of future income in the next 20 years.”?

Financial Reporting of Income Taxes · 10

TAX LOSS CARRYBACK & CARRYFORWARD

QUESTIONSabout loss carryback/carryforward?

Financial Reporting of Income Taxes · 11

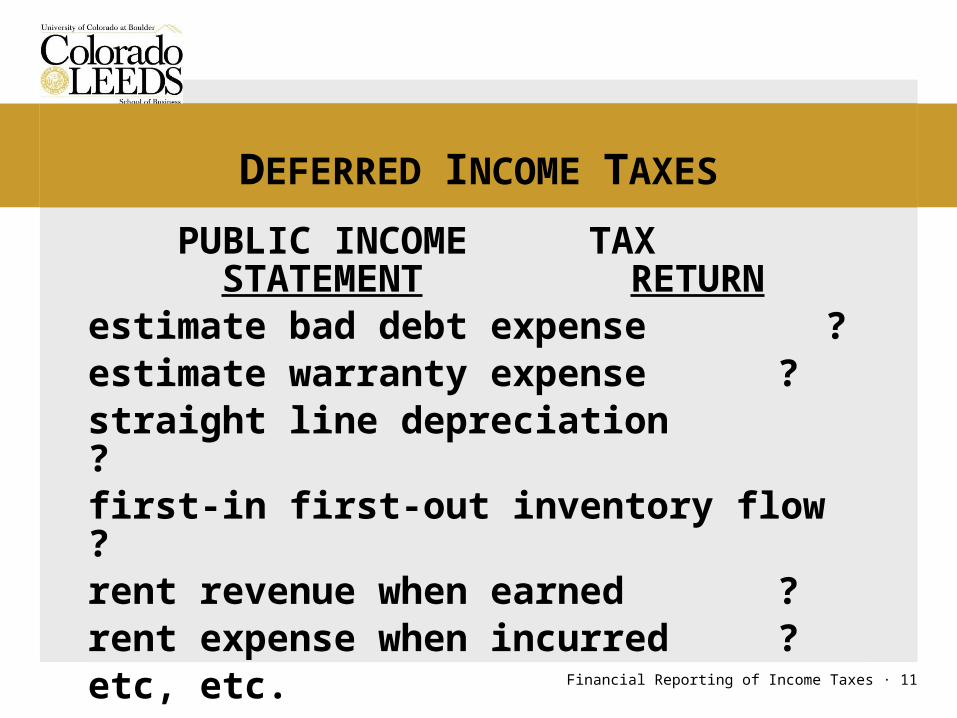

DEFERRED INCOME TAXES

PUBLIC INCOME TAX STATEMENT RETURNestimate bad debt expense ?estimate warranty expense ?straight line depreciation ?first-in first-out inventory flow ?rent revenue when earned ?rent expense when incurred ?etc, etc.

Financial Reporting of Income Taxes · 12

DEFERRED INCOME TAXES

The point is, all publicly traded companies have at least two sets of books – one for the IRS and one for their stockholders (and if they are in a regulated industry, like the banking industry, they have a third set of books).

Financial Reporting of Income Taxes · 13

DEFERRED INCOME TAXES

That poses a problem – what should the company report as income tax expense on their public income statement? What they really owe the IRS or something else.The FASB answer (in FAS 109/ASC 740) is “something else.”

Financial Reporting of Income Taxes · 14

DEFERRED INCOME TAXES

The FASB approach is best illustrated by two examples we will discuss in class.

But first, to use the FASB (or “asset and liability”) approach you need to understand the difference between “temporary” and “permanent” differences between public income and tax income.

Financial Reporting of Income Taxes · 15

DEFERRED INCOME TAXES

Temporary (or timing) differences are things like we discussed earlier (depreciation, bad debts, rent, etc.) – they are differences that, over time, “balance out” (or “reverse”).

Temporary differences require the use of deferred tax assets or liabilities.

Financial Reporting of Income Taxes · 16

DEFERRED INCOME TAXES

Permanent differences are things that never reverse, such as: municipal interest fines the company pays life insurance premiums paid on key employee insurance policies