27

© 2004 by Nelson, a division of Thomson Canada Limited Contemporary Financial Management Chapter 14: Dividend Policy

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | marian-cole |

| View: | 218 times |

| Download: | 2 times |

© 2004 by Nelson, a division of Thomson Canada Limited

Contemporary Financial Management

Chapter 14:Dividend Policy

© 2004 by Nelson, a division of Thomson Canada Limited2

Introduction

This chapter examines the factors that influence a company’s choice of dividend policy

The pros and cons of dividend policies

The mechanics of dividend payments

Stock dividends

Share repurchase plans

© 2004 by Nelson, a division of Thomson Canada Limited3

Dividends

When a company earns a profit, there are only two things it can do with the earnings: Pay a dividend to the shareholders Retain the earnings in the form of Retained

Earnings

The choice as to how to divide firm earnings between Retained Earnings and Dividends and the implications of the choice made is the subject of this chapter.

© 2004 by Nelson, a division of Thomson Canada Limited4

Influencing the Value of the Firm

Investment Decisions Determine the level of future earnings and future

potential dividends

Financing Decisions Influence the cost of capital, which can determine

the number of acceptable investment opportunities

Dividend Decisions Influence the amount of equity in a firm’s capital

structure and the cost of capital

© 2004 by Nelson, a division of Thomson Canada Limited5

Determinants of Dividend Policy

Legal Constraints A firm’s capital cannot be used to pay dividends

(capital impairment restriction) Dividends can only be paid out of past & present

net earnings (net earnings restriction) Dividends cannot be paid when a firm is insolvent

(insolvency restriction)

Restrictive Covenants & Sinking Funds Usually imposed by creditors to prevent excessive

withdrawals by owners

© 2004 by Nelson, a division of Thomson Canada Limited6

Determinants of Dividend Policy

Tax considerations Investment income can be received as a capital

gain or as a dividend The marginal tax rate will determine which form of

income is preferred by investors

Liquidity and Cash Flow Considerations Dividends represent an outflow of cash

Access to New Equity and Debt Capital A firm may decide to pay dividends and

simultaneously issue new equity or borrow

© 2004 by Nelson, a division of Thomson Canada Limited7

Determinants of Dividend Policy

Variability of Earnings (stable vs. growth) The more stable the earnings pattern, the

greater the percentage of earnings the firm can safely pay out as a dividend

Inflation During periods of high inflation, the firm may

need to retain more earnings to fund the replacement of fixed assets

© 2004 by Nelson, a division of Thomson Canada Limited8

Determinants of Dividend Policy

Shareholder Preference Firms often develop “clienteles” that are

attracted to the firm’s stated dividend policy

Protection Against Dilution If the firm pays dividends and issues new

equity, existing shareholders will be diluted if they do not purchase a portion of the new equity sold

© 2004 by Nelson, a division of Thomson Canada Limited9

Dividend Irrelevance

Miller & Modigliani (MM) argue that dividends are irrelevant (under certain assumptions)

MM argue that firm value is determined by the firm’s investment policy, not dividend policy

MM’s assumptions for dividend irrelevance No taxes No transaction costs No issuance costs (for selling new equity) Existence of a fixed investment policy

© 2004 by Nelson, a division of Thomson Canada Limited10

Dividend Irrelevance

MM recognize that changes in dividend policy affect share prices They argue this is due to the informational content

conveyed by the change, not the change itself

Changes in dividend policy have a signaling effect – it signals management beliefs about future firm prospects

The existence of clienteles should not affect share price, since one clientele is as good as another clientele

© 2004 by Nelson, a division of Thomson Canada Limited11

Are Dividends Relevant?

?What happens when the assumptions are relaxed?

MM probably correct, given their restrictive

assumptions.

© 2004 by Nelson, a division of Thomson Canada Limited12

Are Dividends Relevant?

Risk aversion (Bird in the Hand Theory) Dividends represent a regular, certain return,

thereby lowering risk and increasing firm value

Transaction costs With no transaction costs, investors can sell a portion

of their shares to “create” a dividend In reality, transactions costs are real and significant

Taxes Investors care only about their after-tax return Thus taxes affect the preferred form of income

© 2004 by Nelson, a division of Thomson Canada Limited13

Relevance of Dividends

Issuance (Flotation) costs The existence of issuance costs reduces the

attractiveness of paying dividends and issuing equity

Agency costs are reduced when management is subjected to market scrutiny

© 2004 by Nelson, a division of Thomson Canada Limited14

Conclusions Regarding Dividend Policy

Empirical evidence is mixed Some studies found that, due to tax effects,

investors require a higher pretax return on high-dividend shares

Other studies found no difference

Many practitioners believe that dividends are important due to: Their informational content External equity is expensive

© 2004 by Nelson, a division of Thomson Canada Limited15

Passive Residual Policy

Suggests that a firm should retain its earnings as long as it has investment opportunities that promise higher rates of return than the shareholder’s required return

Would imply that dividends fluctuate significantly, based on earnings & investment opportunities

In practice, firms can smooth their dividends payments by using debt and varying their earnings retention policy

© 2004 by Nelson, a division of Thomson Canada Limited16

Stable Dollar Dividend Policies

Firms are reluctant to reduce dividends; shareholders like a stable dividend stream

Increases in dividends tend to lag earnings

Investors prefer stable dividends because: Dividend changes convey information Many shareholders depend on dividend income Stability tends to reduce uncertainty, thereby

lowering the firm’s cost of capital Certain institutions can only hold the shares of firms

with a record of continuous and stable dividends

© 2004 by Nelson, a division of Thomson Canada Limited17

Other Dividend Payment Policies

Constant Payout Ratio Pays a constant percent of earnings as

dividends Causes the dividend to fluctuate

© 2004 by Nelson, a division of Thomson Canada Limited18

Other Dividend Payment Policies

Small Regular Dividends Plus Extras Shareholders can depend on regular payout Accommodates changing earnings and

investment requirements

© 2004 by Nelson, a division of Thomson Canada Limited19

Other Dividend Payment Policies

Small Firms and Dividends Tend to pay out a smaller percent of earnings Rapid growth requires capital; small firms retain

more of their income to fund growth Small firms have limited access to capital

markets

© 2004 by Nelson, a division of Thomson Canada Limited20

Multinational Firms & Dividends

Primary means of transferring funds to parent company

Important issues to consider include:

Tax Foreign Exchange Political risk Funds availability Financing needs

© 2004 by Nelson, a division of Thomson Canada Limited21

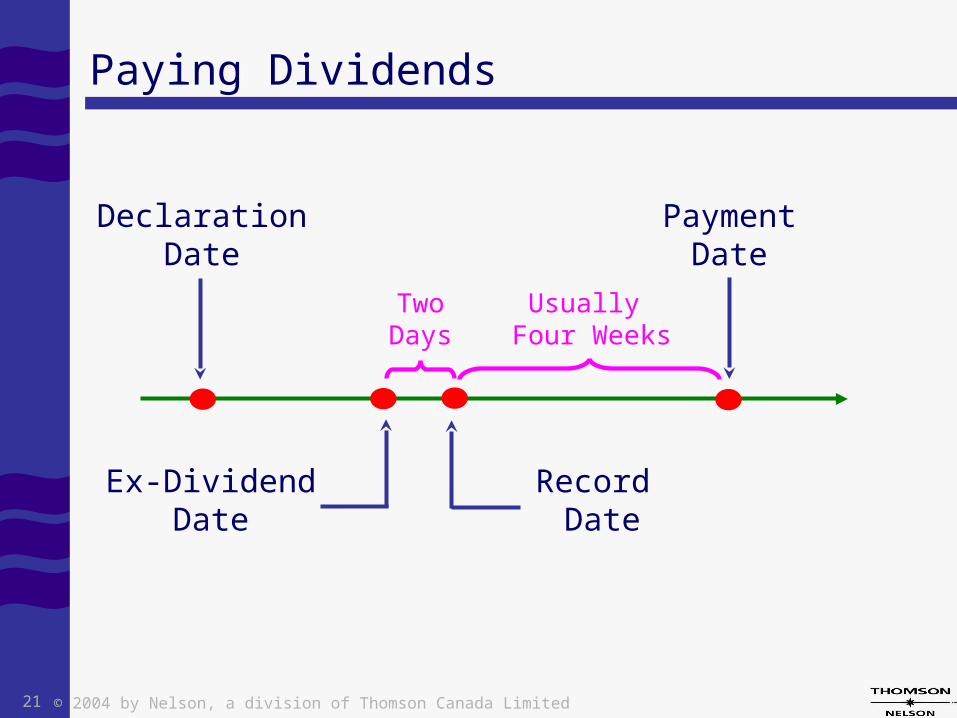

Paying Dividends

DeclarationDate

Ex-DividendDate

Record Date

PaymentDate

TwoDays

Usually Four Weeks

© 2004 by Nelson, a division of Thomson Canada Limited22

Dividend Reinvestment Plan

Cash dividends reinvested automatically into additional shares

Purchase new or existing shares Purchasing new shares raises new equity capital

for the firm

No brokerage commissions

Income tax liability

© 2004 by Nelson, a division of Thomson Canada Limited23

Stock Dividends

Stock dividends are similar to stock splits

Both increase the number of shares outstanding

Accounting transaction Transfer pre-dividend market value from

retained earnings to other stockholder’s equity

Market price of common shares should decline in proportion to the number of new shares issued

© 2004 by Nelson, a division of Thomson Canada Limited24

Reasons for Stock Dividends

Broaden the ownership of the firm’s shares

May result in an effective increase in cash dividends, provided the level of cash dividends per share is not reduced

Reduction in share price may broaden the appeal of the stock to investors Thus may result in a real increase in market

value

© 2004 by Nelson, a division of Thomson Canada Limited25

Share Repurchase

By Tender Offer in the open market or by negotiation with large holders

Acquired shares may be cancelled or held as Treasury stock

Reduces the number of shares outstanding Increases EPS for the remaining shareholders

Stock repurchase programs are usually publicly announced

© 2004 by Nelson, a division of Thomson Canada Limited26

Share Repurchase

Advantages Converts dividend income into capital gains Greater financial flexibility Greater control over timing Signaling effect

Disadvantages Company may overpay for the stock Tax avoidance Some current shareholders may be unaware

© 2004 by Nelson, a division of Thomson Canada Limited27

Major Points

Firm profits are split into Retained Earnings and Dividends. Dividend policy explicitly states how the firm intends to make this split.

In a perfect world, it would not matter whether the firm paid dividends or not.

In the real world, where taxes and transaction costs exist, dividends probably do matter.

Dividends can be paid in cash or stock. In both cases, stock price declines on ex-dividend date

Share repurchases reduce shares outstanding, thereby pushing up the future price of the stock.