72

© 2004 Prentice-Hall, Inc. Chap 16-1 Basic Business Statistics (9 th Edition) Chapter 16 Time-Series Forecasting and Index Numbers

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | cecily-cobb |

| View: | 224 times |

| Download: | 3 times |

© 2004 Prentice-Hall, Inc. Chap 16-1

Basic Business Statistics(9th Edition)

Chapter 16Time-Series Forecasting and

Index Numbers

© 2004 Prentice-Hall, Inc. Chap 16-2

Chapter Topics

The Importance of Forecasting Component Factors of the Time-Series

Model Smoothing of Annual Time Series

Moving averages Exponential smoothing

Least-Squares Trend Fitting and Forecasting Linear, quadratic and exponential models

© 2004 Prentice-Hall, Inc. Chap 16-3

Chapter Topics

Holt-Winters Method for Trend Fitting and Forecasting

Autoregressive Models Choosing Appropriate Forecasting Models Time-Series Forecasting of Monthly or

Quarterly Data Pitfalls Concerning Time-Series

Forecasting Index Numbers

(continued)

© 2004 Prentice-Hall, Inc. Chap 16-4

The Importance of Forecasting

Government Needs to Forecast Unemployment, Interest Rates, Expected Revenues from Income Taxes to Formulate Policies

Marketing Executives Need to Forecast Demand, Sales, Consumer Preferences in Strategic Planning

© 2004 Prentice-Hall, Inc. Chap 16-5

The Importance of Forecasting

College Administrators Need to Forecast Enrollments to Plan for Facilities, for Student and Faculty Recruitment

Retail Stores Need to Forecast Demand to Control Inventory Levels, Hire Employees and Provide Training

(continued)

© 2004 Prentice-Hall, Inc. Chap 16-6

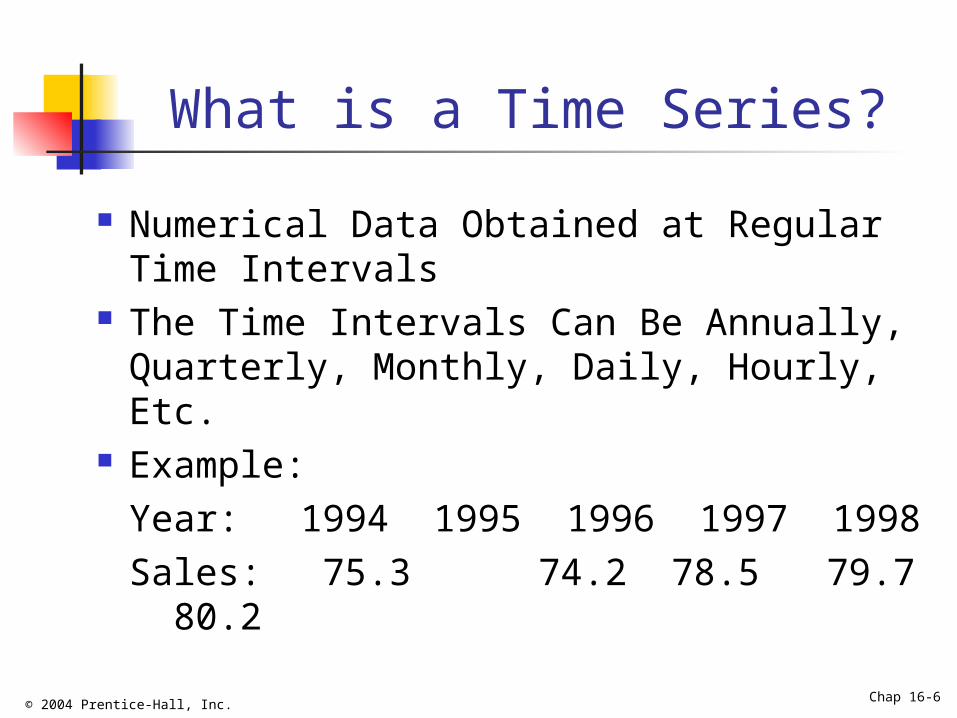

What is a Time Series?

Numerical Data Obtained at Regular Time Intervals

The Time Intervals Can Be Annually, Quarterly, Monthly, Daily, Hourly, Etc.

Example:Year: 1994 1995 1996 1997

1998Sales: 75.3 74.2 78.5

79.7 80.2

© 2004 Prentice-Hall, Inc. Chap 16-7

Time-Series Components

Time-Series

Cyclical

Irregular

Trend

Seasonal

© 2004 Prentice-Hall, Inc. Chap 16-8

Upward trend

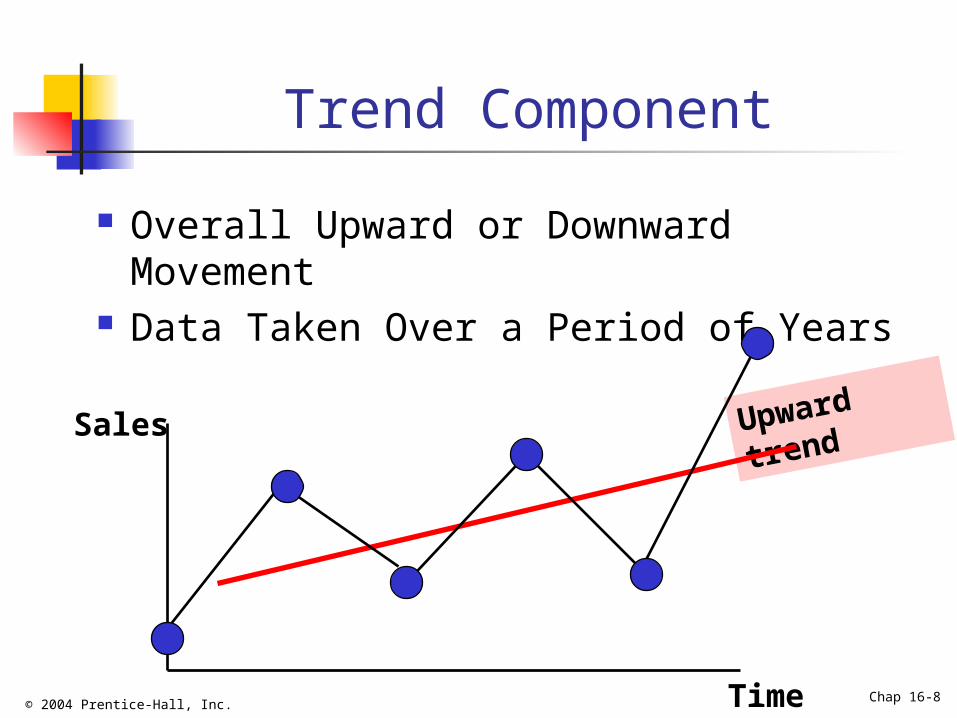

Trend Component

Overall Upward or Downward Movement Data Taken Over a Period of Years

Sales

Time

© 2004 Prentice-Hall, Inc. Chap 16-9

Cyclical Component

Upward or Downward Swings May Vary in Length Usually Lasts 2 - 10 Years

Sales 1 Cycle

© 2004 Prentice-Hall, Inc. Chap 16-10

Seasonal Component

Upward or Downward Swings Regular Patterns Observed Within 1 Year

Sales

Time (Monthly or Quarterly)

WinterSpring

Summer

Fall

© 2004 Prentice-Hall, Inc. Chap 16-11

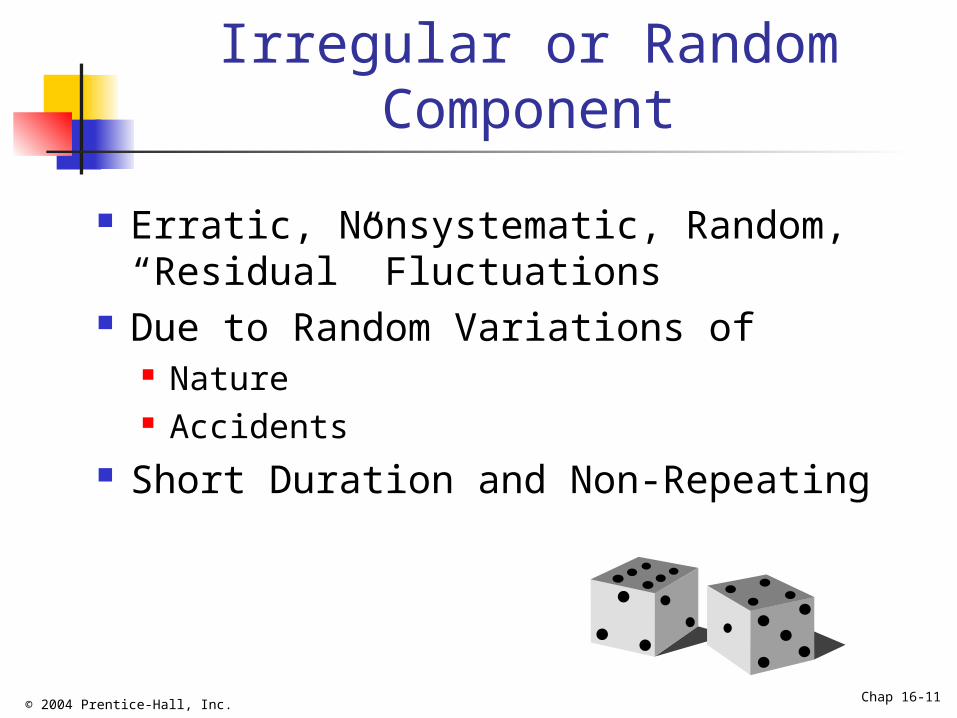

Irregular or Random Component

Erratic, Nonsystematic, Random, “Residual” Fluctuations

Due to Random Variations of Nature Accidents

Short Duration and Non-Repeating

© 2004 Prentice-Hall, Inc. Chap 16-12

Example: Quarterly Retail Sales with Seasonal

Components

Quarterly with Seasonal Components

0

5

10

15

20

25

0 5 10 15 20 25 30 35

Time

Sale

s

© 2004 Prentice-Hall, Inc. Chap 16-13

Example: Quarterly Retail Sales with Seasonal Components

Removed

Quarterly without Seasonal Components

0

5

10

15

20

25

0 5 10 15 20 25 30 35

Time

Sa

les

Y(t)

© 2004 Prentice-Hall, Inc. Chap 16-14

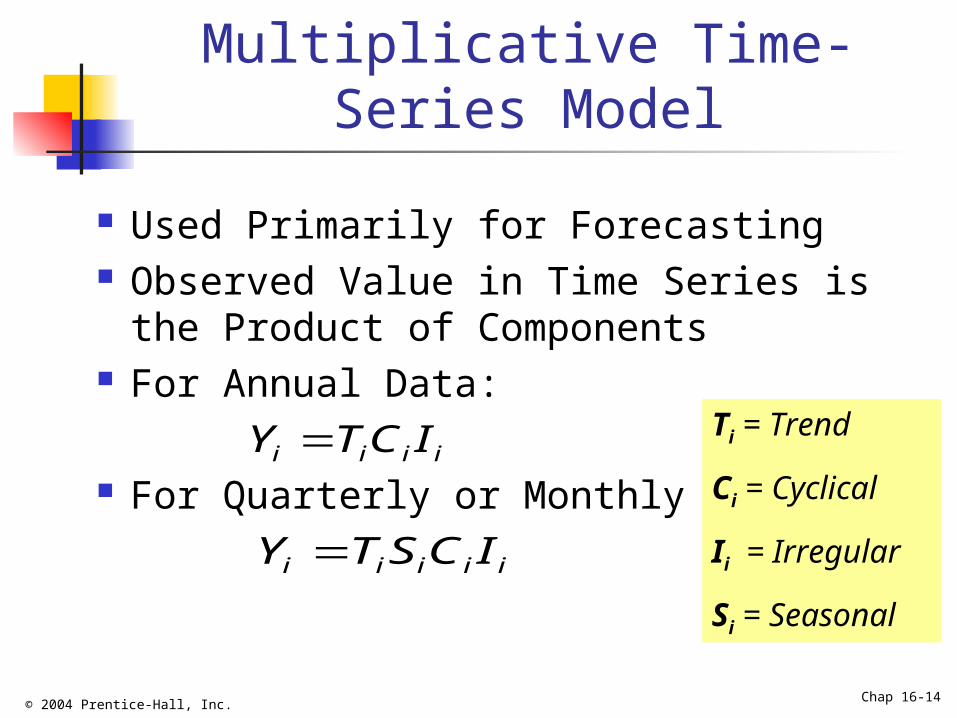

Multiplicative Time-Series Model

Used Primarily for Forecasting Observed Value in Time Series is the

Product of Components For Annual Data:

For Quarterly or Monthly Data:i i i iY TC I

i i i i iY T S C I

Ti = Trend

Ci = Cyclical

Ii = Irregular

Si = Seasonal

© 2004 Prentice-Hall, Inc. Chap 16-15

Moving Averages

Used for Smoothing Series of Arithmetic Means Over Time Result Dependent Upon Choice of L

(Length of Period for Computing Means) To Smooth Out Cyclical Component, L

Should Be Multiple of the Estimated Average Length of the Cycle

For Annual Time Series, L Should Be Odd

© 2004 Prentice-Hall, Inc. Chap 16-16

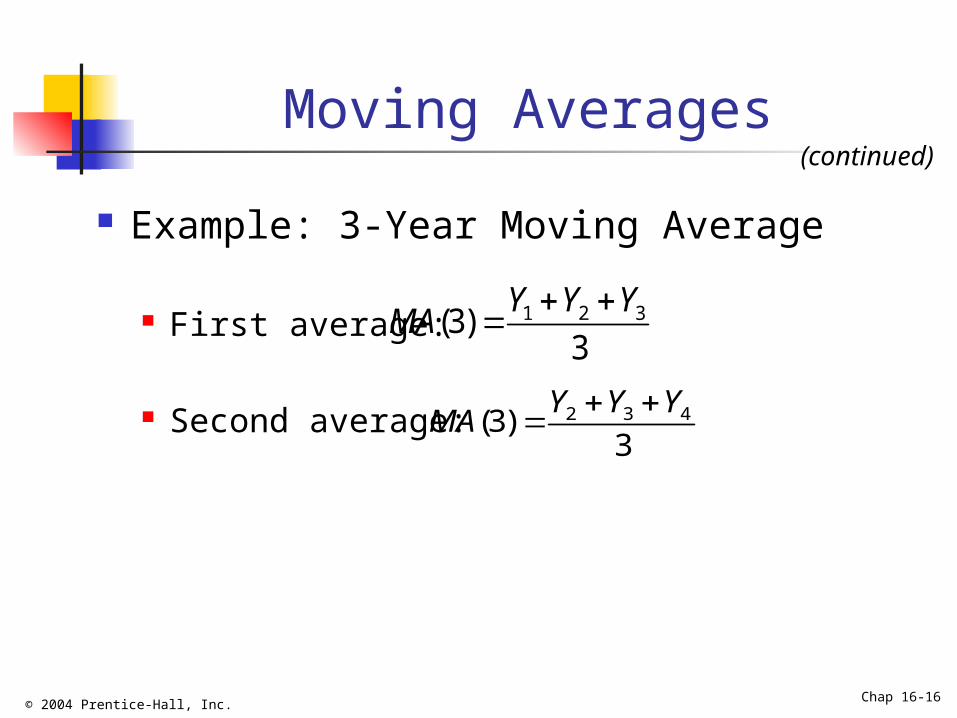

Moving Averages

Example: 3-Year Moving Average

First average:

Second average:

1 2 3(3)3

Y Y YMA

2 3 4(3)3

Y Y YMA

(continued)

© 2004 Prentice-Hall, Inc. Chap 16-17

Moving Average Example

Year Units Moving Ave

1994 2 NA

1995 5 3

1996 2 3

1997 2 3.67

1998 7 5

1999 6 NA

John is a building contractor with a record of a total of 24 single family homes constructed over a 6-year period. Provide John with a 3-year moving average graph.

© 2004 Prentice-Hall, Inc. Chap 16-18

Moving Average Example Solution

Year Response MovingAve

1994 2 NA

1995 5 3

1996 2 3

1997 2 3.67

1998 7 5

1999 6 NA94 95 96 97 98 99

8

6

4

2

0

SalesL = 3

No MA for the first and last (L-1)/2 years

© 2004 Prentice-Hall, Inc. Chap 16-19

Moving Average Example Solution in Excel

Use Excel formula “=average(cell range containing the data for the years to average)”

Excel Spreadsheet for the Single Family Home Sales Example

Microsoft Excel Worksheet

© 2004 Prentice-Hall, Inc. Chap 16-20

Example: 5-Period Moving Averages of Quarterly Retail

Sales

Quarterly 5-Period Moving Averages

0

5

10

15

20

25

0 5 10 15 20 25 30 35

Time

Sa

les

MA(5)

Y(t)

© 2004 Prentice-Hall, Inc. Chap 16-21

Exponential Smoothing Weighted Moving Average

Weights decline exponentially Most recent observation weighted most

Used for Smoothing and Short-Term Forecasting

Weights are: Subjectively chosen Range from 0 to 1

Close to 0 for smoothing out unwanted cyclical and irregular components

Close to 1 for forecasting

© 2004 Prentice-Hall, Inc. Chap 16-22

Exponential Weight: Example

Year Response Smoothing Value Forecast(W = .2, (1-W)=.8)

1994 2 2 NA

1995 5 (.2)(5) + (.8)(2) = 2.6 2

1996 2 (.2)(2) + (.8)(2.6) = 2.48 2.6

1997 2 (.2)(2) + (.8)(2.48) = 2.384 2.48

1998 7 (.2)(7) + (.8)(2.384) = 3.307 2.384

1999 6 (.2)(6) + (.8)(3.307) = 3.846 3.307

1(1 )i i iE WY W E

© 2004 Prentice-Hall, Inc. Chap 16-23

Exponential Weight: Example Graph

94 95 96 97 98 99

8

6

4

2

0

Sales

Year

Data

Smoothed

© 2004 Prentice-Hall, Inc. Chap 16-24

Exponential Smoothing in Excel

Use Tools | Data Analysis | Exponential Smoothing The damping factor is (1-W )

Excel Spreadsheet for the Single Family Home Sales Example

Microsoft Excel Worksheet

© 2004 Prentice-Hall, Inc. Chap 16-25

Example: Exponential Smoothing of Real GNP

The Excel Spreadsheet with the Real GDP Data and the Exponentially Smoothed Series

Microsoft Excel Worksheet

© 2004 Prentice-Hall, Inc. Chap 16-26

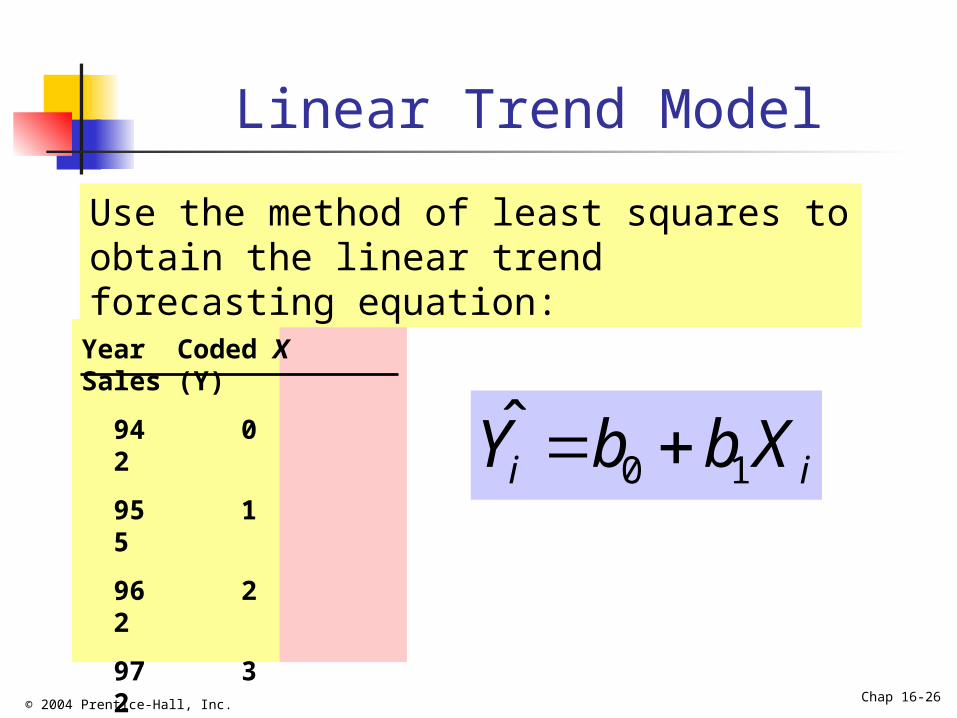

Linear Trend Model

Year Coded X Sales (Y)

94 0 2

95 1 5

96 2 2

97 3 2

98 4 7

99 5 6

0 1i iY b b X

Use the method of least squares to obtain the linear trend forecasting equation:

© 2004 Prentice-Hall, Inc. Chap 16-27

Linear Trend Model(continued)

0 1ˆ 2.143 .743i i iY b b X X

Excel Output

CoefficientsIntercept 2.14285714X Variable 1 0.74285714

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5 6X

Sale

s

Projected to year 2000

Linear trend forecasting equation:

© 2004 Prentice-Hall, Inc. Chap 16-28

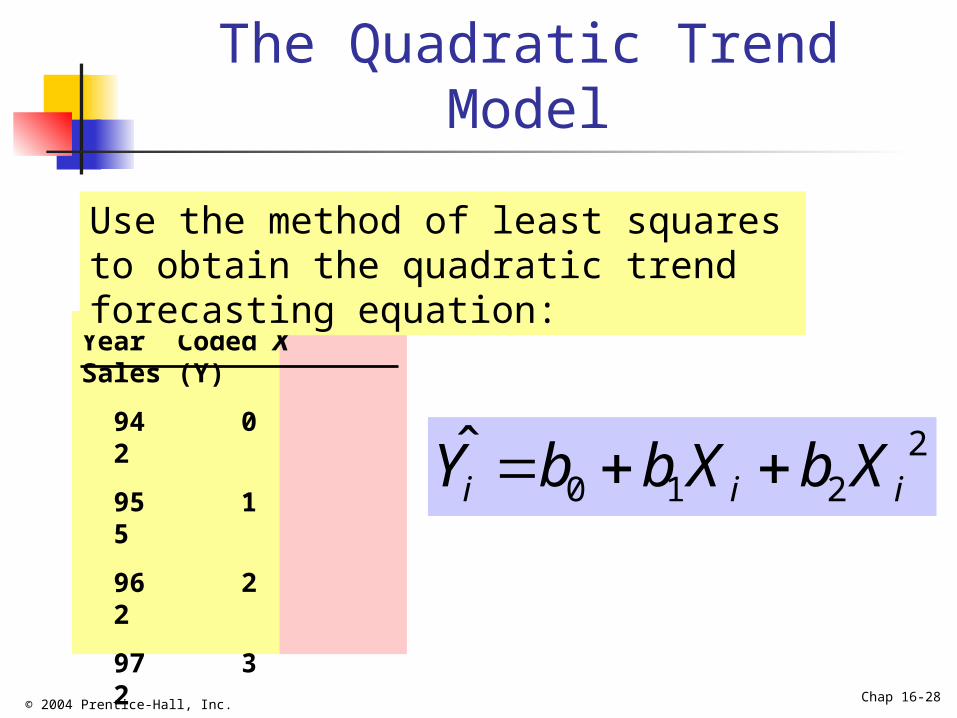

The Quadratic Trend Model

Year Coded X Sales (Y)

94 0 2

95 1 5

96 2 2

97 3 2

98 4 7

99 5 6

20 1 2i i iY b b X b X

Use the method of least squares to obtain the quadratic trend forecasting equation:

© 2004 Prentice-Hall, Inc. Chap 16-29

The Quadratic Trend Model(continued)

2 20 1 2

ˆ 2.857 .33 .214i i i i iY b b X b X X X

CoefficientsIntercept 2.85714286X Variable 1 -0.3285714X Variable 2 0.21428571

Excel Output

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5 6 X

Sale

s Projected to year 2000

© 2004 Prentice-Hall, Inc. Chap 16-30

The Exponential Trend Model

CoefficientsIntercept 0.33583795X Variable 10.08068544

0 1ˆ iXiY b b or

Excel Output of Values in Logs

ˆ (2.17)(1.2) iXiY

antilog(.33583795) = 2.17antilog(.08068544) = 1.2

0 1 1ˆlog log logiY b X b

Year Coded X Sales (Y)

94 0 2

95 1 5

96 2 2

97 3 2

98 4 7

99 5 6

After taking the logarithms, use the method of least squares to get the forecasting equation:

© 2004 Prentice-Hall, Inc. Chap 16-31

The Least-Squares TrendModels in PHStat

Use PHStat | Simple Linear Regression for Linear Trend and Exponential Trend Models and PHStat | Multiple Regression for Quadratic Trend Model

Excel Spreadsheet for the Single Family Home Sales Example

Microsoft Excel Worksheet

© 2004 Prentice-Hall, Inc. Chap 16-32

Model Selection Using Differences

Use a Linear Trend Model If the First Differences are More or Less Constant

Use a Quadratic Trend Model If the Second Differences are More or Less Constant

2 1 3 2 1n nY Y Y Y Y Y

3 2 2 1 1 1 2n n n nY Y Y Y Y Y Y Y

© 2004 Prentice-Hall, Inc. Chap 16-33

Model Selection Using Differences

3 2 12 1

1 2 1

100% 100% 100%n n

n

Y Y Y YY Y

Y Y Y

Use an Exponential Trend Model If the Percentage Differences are More or Less Constant

(continued)

© 2004 Prentice-Hall, Inc. Chap 16-34

The Holt-Winters Method Similar to Exponential Smoothing Advantages Over Exponential Smoothing

Can detect future trend and overall movement Can provide intermediate and/or long-term

forecasting Two Weights 0<U<1 and 0<V<1 are to Be

Chosen Smaller values of U give more weight to the

more recent levels and less weight to earlier levels

Smaller values of V give more weight to the current trends and less weight to past trends

© 2004 Prentice-Hall, Inc. Chap 16-35

The Holt-Winters Method

1 1

1 1

1

1

Level: 1

Trend: 1

: level of smoothed series in time period

: level of smoothed series in time period 1

: value of trend component in time period

: val

i i i i

i i i i

i

i

i

i

E U E T U Y

T VT V E E

E i

E i

T i

T

2 2 2 2 1

ue of trend component in time period 1

: observed value of the time series in period

: smoothing constant (where 0 1)

: smoothing constant (where 0 1)

and

i

i

Y i

U U

V V

E Y T Y Y

© 2004 Prentice-Hall, Inc. Chap 16-36

The Holt-Winters Method: Example

Year

Sales

(Yi )

Level (Ei )U =.2

Trend (Ti )V = .2

94 2 NA NA

95 5 5 5-2=3

96 2 .2(5+3)+.8(2)=3.2 .2(3)+.8(3.2-5)=-.84

97 2 .2(3.2-.84)+.8(2)=2.07 .2(-.84)+.8(2.07-3.2)=-1.07

98 7 .2(2.07-1.07)+.8(7)=5.8

.2(-1.07)+.8(5.8-2.07)=2.77

99 6 .2(5.8+2.77)+.8(6)=6.51

.2(2.77)+.8(6.51-5.8)=1.12

1 1

1 1

Level: 1

Trend: 1

i i i i

i i i i

E U E T U Y

T VT V E E

© 2004 Prentice-Hall, Inc. Chap 16-37

The Holt-Winters Method:Forecasting

ˆ

ˆwhere : forecasted value years into the future

: level of smoothed series in period

: value of trend component in period

: number of years int

n j n n

n j

n

n

Y E j T

Y j

E n

T n

j

o the future

00 99 99

05 99 99

Year 00: 1

ˆ 1 6.51 1 1.12 7.638

Year 05: 6

ˆ 6 6.51 6 1.12 13.26

j

Y E T

j

Y E T

© 2004 Prentice-Hall, Inc. Chap 16-38

Holt-Winters Method:Plot of Series and Forecasts

Excel Spreadsheet with the Computation

0

2

4

6

8

10

12

14

1 2 3 4 5 6 7 8 9 10 11 12

Level (E)

Series (Y)

Forecasts for 2000 to 2005

1994

Microsoft Excel Worksheet

© 2004 Prentice-Hall, Inc. Chap 16-39

Autoregressive Modeling

Used for Forecasting Takes Advantage of Autocorrelation

1st order - correlation between consecutive values

2nd order - correlation between values 2 periods apart

Autoregressive Model for p-th Order:0 1 1 2 2i i i p i p iY A AY A Y A Y

Random Error

© 2004 Prentice-Hall, Inc. Chap 16-40

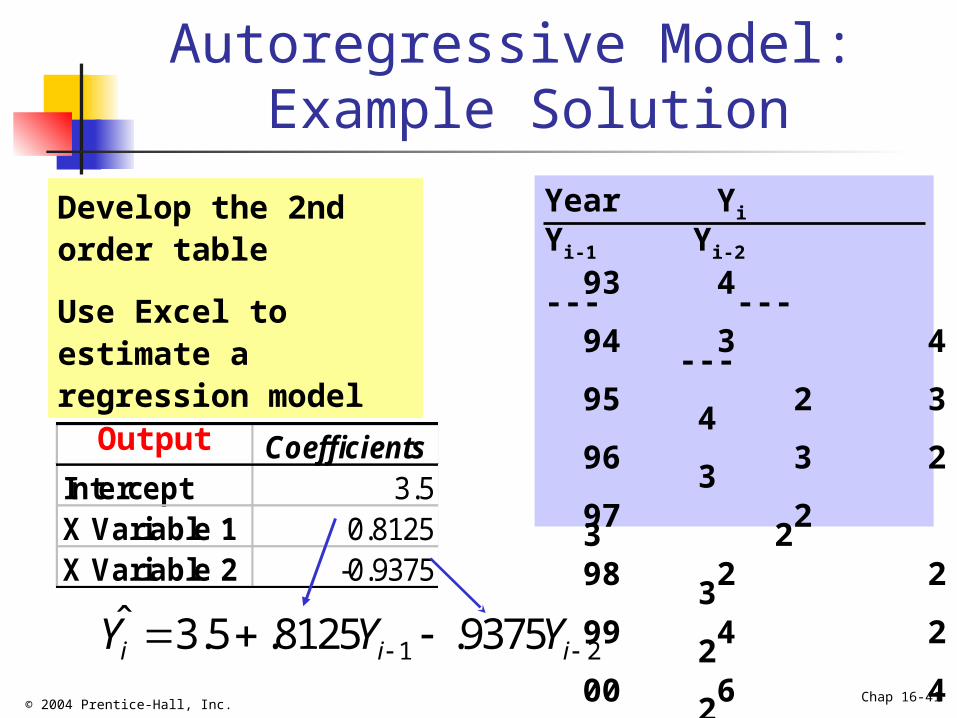

Autoregressive Model: Example

Year Units

93 4 94 3 95 2 96 3 97 2 98 2 99 4 00 6

The Office Concept Corp. has acquired a number of office units (in thousands of square feet) over the last 8 years. Develop the 2nd order autoregressive model.

© 2004 Prentice-Hall, Inc. Chap 16-41

Autoregressive Model: Example Solution

Year Yi Yi-1 Yi-2

93 4 --- --- 94 3 4 --- 95 2 3 4 96 3 2 3 97 2 3 2 98 2 2 3 99 4 2 2 00 6 4 2

CoefficientsIntercept 3.5X Variable 1 0.8125X Variable 2 -0.9375

Excel Output

1 2ˆ 3.5 .8125 .9375i i iY Y Y

Develop the 2nd order table

Use Excel to estimate a regression model

© 2004 Prentice-Hall, Inc. Chap 16-42

Autoregressive Model Example: Forecasting

Use the 2nd order model to forecast number of units for 2001:

1 2

2001 2000 1999

ˆ 3.5 .8125 .9375

ˆ 3.5 .8125 .9375

3.5 .8125 6 .9375 4

4.625

i i iY Y Y

Y Y Y

© 2004 Prentice-Hall, Inc. Chap 16-43

Autoregressive Model in PHStat

PHStat | Multiple Regression

Excel Spreadsheet for the Office Units Example

Microsoft Excel Worksheet

© 2004 Prentice-Hall, Inc. Chap 16-44

Autoregressive Modeling Steps

1. Choose p : Note that df = n - 2p - 12. Form a Series of “Lag Predictor” Variables

Yi-1 , Yi-2 , … ,Yi-p

3. Use Excel to Run Regression Model Using All p Variables

4. Test Significance of Ap

If null hypothesis rejected, this model is selected

If null hypothesis not rejected, decrease p by 1 and repeat

© 2004 Prentice-Hall, Inc. Chap 16-45

Selecting a Forecasting Model

Perform a Residual Analysis Look for pattern or direction

Measure Residual Error Using SSE (Sum of Square Error)

Measure Residual Error Using MAD (Mean Absolute Deviation)

Use Simplest Model Principle of parsimony

© 2004 Prentice-Hall, Inc. Chap 16-46

Residual Analysis

Random errors

Trend not accounted for

Cyclical effects not accounted for

Seasonal effects not accounted for

Time Time

Time Time

e e

e e

0 0

0 0

© 2004 Prentice-Hall, Inc. Chap 16-47

Measuring Errors

Choose a Model that Gives the Smallest Measuring Errors

Sum Square Error (SSE)

Sensitive to outliers

2

1

ˆn

i ii

SSE Y Y

© 2004 Prentice-Hall, Inc. Chap 16-48

Measuring Errors

Mean Absolute Deviation (MAD)

Not sensitive to extreme observations

(continued)

1

ˆn

i ii

Y YMAD

n

© 2004 Prentice-Hall, Inc. Chap 16-49

Principle of Parsimony

Suppose 2 or More Models Provide Good Fit to Data

Select the Simplest Model Simplest model types:

Least-squares linear Least-squares quadratic 1st order autoregressive

More complex types: 2nd and 3rd order autoregressive Least-squares exponential Holt-Winters Model

© 2004 Prentice-Hall, Inc. Chap 16-50

Forecasting with Seasonal Data

Use Categorical Predictor Variables with Least-Squares Trend Fitting

Forecasting Equation (Exponential Model with Quarterly Data):

The bj provides the multiplier for the j -th quarter relative to the 4th quarter

Qj = 1 if j -th quarter and 0 if not Xi = the coded variable denoting the time

period i

1 2 3

0 1 2 3 4ˆ iX Q Q QiY b b b b b

© 2004 Prentice-Hall, Inc. Chap 16-51

Forecasting with QuarterlyData: Example

445.77444.27462.69459.27

500.71544.75584.41615.93

645.5670.63687.31740.74

757.12885.14947.28970.43

I234

Quarter 1994 1995 1996 1997

Standards and Poor’s Composite Stock Price Index:

Excel Output

Appears to be an excellent fit.

r2 is .98

Regression StatisticsMultiple R 0.989936819R Square 0.979974906Adjusted R Square 0.972693054Standard Error 0.019051226Observations 16

© 2004 Prentice-Hall, Inc. Chap 16-52

Forecasting with QuarterlyData: Example

(continued)Excel Output

10 10 0 10 1 1 10 2

1

ˆlog log log log

2.6106 0.02405 0.00453i i

i

Y b X b Q b

X Q

Regression equation for the first quarters:

Coefficients Standard Error t Stat P-valueIntercept 2.610625646 0.013513283 193.1895916 8.96553E-21Coded X 0.024047968 0.001064996 22.58033882 1.44859E-10Q1 0.00452606 0.013844947 0.326910637 0.749871743Q2 0.010373368 0.013638602 0.760588787 0.462894872Q3 0.008400302 0.013513283 0.621632977 0.546850376

1 12.6106 0.02405 0.00453ˆ 10 10 10X Q

iY

© 2004 Prentice-Hall, Inc. Chap 16-53

Forecasting with QuarterlyData: Example

(continued)

1st quarter of 1998:

10 1998,1

2.9999191998,1

16 12.6106 0.02405 0.004531998,1

ˆlog 2.6106 .02405 16 0.00453 1 2.999919

ˆ 10 999.814

ˆor 10 10 10 999.814

Y

Y

Y

1st quarter of 1994:

10 1994,1

2.6151521994,1

0 12.6106 0.02405 0.004531994,1

ˆlog 2.6106 .02405 0 0.00453 1 2.615152

ˆ 10 412.2415

ˆor 10 10 10 412.2415

Y

Y

Y

© 2004 Prentice-Hall, Inc. Chap 16-54

Forecasting with Quarterly Data in PHStat

Use PHStat | Multiple Regression

Excel Spreadsheet for the Stock Price Index Example

Microsoft Excel Worksheet

© 2004 Prentice-Hall, Inc. Chap 16-55

Index Numbers

Measure the Value of an Item (Group of Items) at a Particular Point in Time as a Percentage of the Item’s (Group of Items’) Value at Another Point in Time A price index measures the percentage

change in the price of an item (group of items) in a given period of time over the price paid for the item (group of items) at a particular point of time in the past

Commonly Used in Business and Economics as Indicators of Changing Business or Economic Activity

© 2004 Prentice-Hall, Inc. Chap 16-56

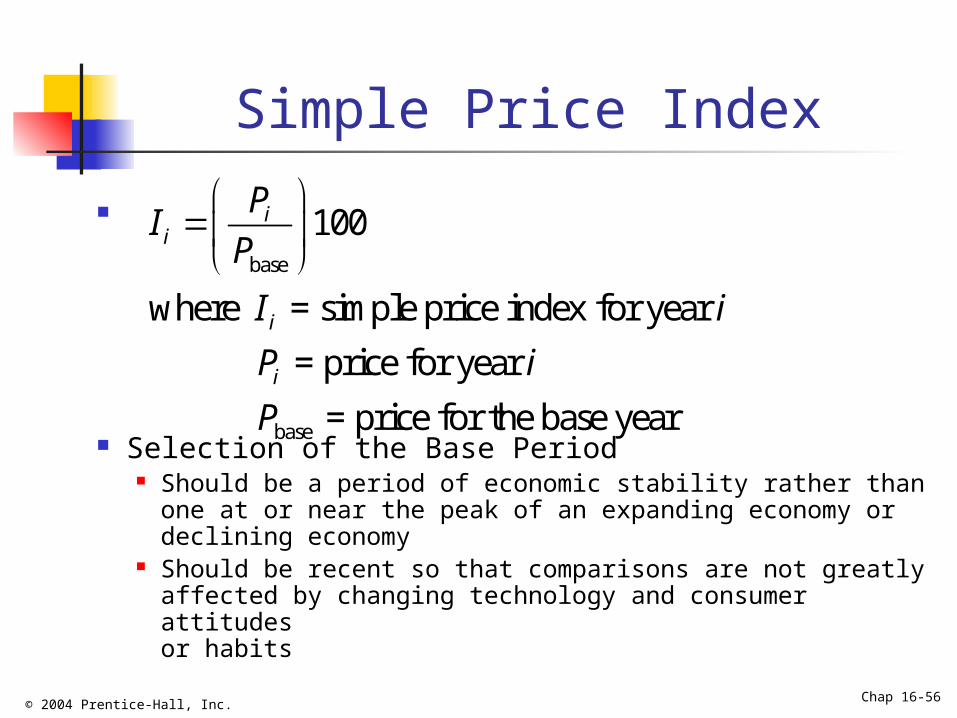

Simple Price Index

Selection of the Base Period Should be a period of economic stability rather than one

at or near the peak of an expanding economy or declining economy

Should be recent so that comparisons are not greatly affected by changing technology and consumer attitudes or habits

base

base

100

where = simple price index for year

= price for year

= price for the base year

ii

i

i

PI

P

I i

P i

P

© 2004 Prentice-Hall, Inc. Chap 16-57

Simple Price Index: Example

Given the prices (in dollars per pound) for apples, construct the simple price index using 1980 as the base year.

Year Price1980 0.692 (0.692/0.692)100 = 100.001985 0.684 (0.684/0.692)100 = 98.841990 0.719 (0.719/0.692)100 = 103.901995 0.835 (0.835/0.692)100 = 120.662000 0.896 (0.896/0.692)100 = 129.48

Simple Price Index

basePBase Year

iP iI

© 2004 Prentice-Hall, Inc. Chap 16-58

Shifting the Base

oldnew

new base

new

old

new base

100

where = new price index

= old price index

= value of the old price index

for the new base year

II

I

I

I

I

© 2004 Prentice-Hall, Inc. Chap 16-59

Shifting the Base: Example

Year Price

1980 0.692 (100.00/129.48)100 = 77.231985 0.684 (98.84/129.48)100 = 76.341990 0.719 (103.90/129.48)100 = 80.251995 0.835 (120.66/129.48)100 = 93.192000 0.896 (129.48/129.48)100 = 100.00

Simple Price Index Simple Price Index

100.0098.84

(base = 2000)

103.90120.66129.48

(base = 1980)

Change the base year of the simple price index of apples from 1980 to 2000:

new baseI newIoldINew Base Year

© 2004 Prentice-Hall, Inc. Chap 16-60

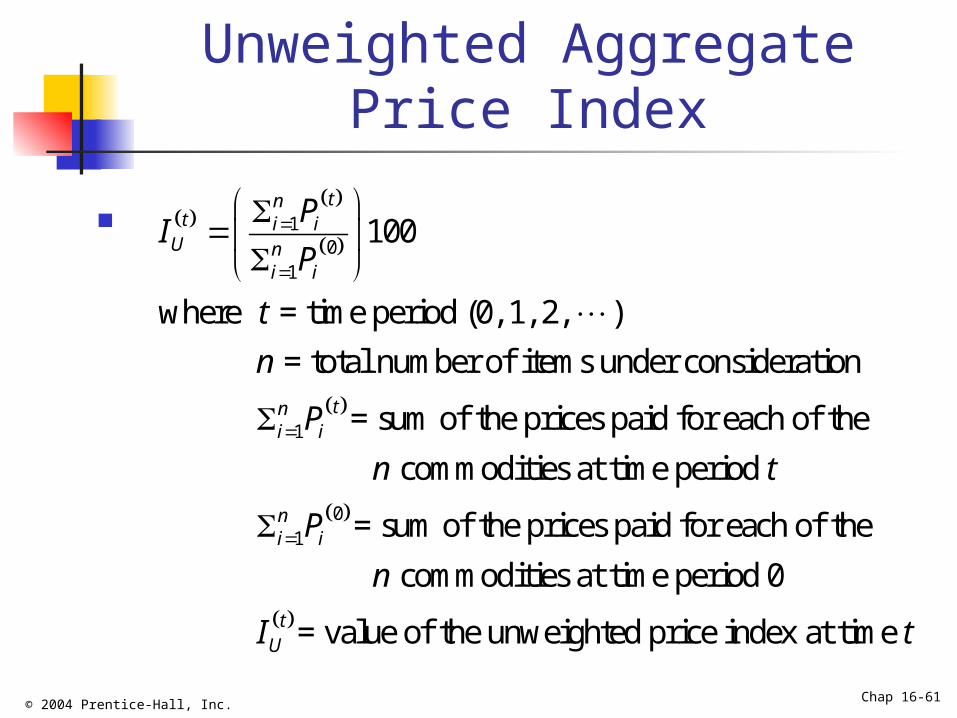

Aggregate Price Index

Reflects the Percentage Change in Price of a Group of Commodities (Market Basket) in a Given Period of Time Over the Price Paid for that Group of Commodities at a Particular Point of Time in the Past

Affects the Cost of Living and/or the Quality of Life for a Large Number of Consumers

Two Basic Types Unweighted aggregate price index Weighted aggregate price index

© 2004 Prentice-Hall, Inc. Chap 16-61

Unweighted Aggregate Price Index

10

1

1

100

where = time period (0, 1, 2, )

= total number of items under consideration

= sum of the prices paid for each of the

comm

tnt i iU n

i i

tni i

PI

P

t

n

P

n

01

odities at time period

= sum of the prices paid for each of the

commodities at time period 0

= value of the unweighted price index at tim

ni i

tU

t

P

n

I

e t

© 2004 Prentice-Hall, Inc. Chap 16-62

Unweighted Aggregate Price Index

Easy to Compute Two Distinct Shortcomings

Each commodity in the group is treated as equally important so that the most expensive commodities per unit can overly influence the index

Not all commodities are consumed at the same rate, but they are treated the same by the index

(continued)

© 2004 Prentice-Hall, Inc. Chap 16-63

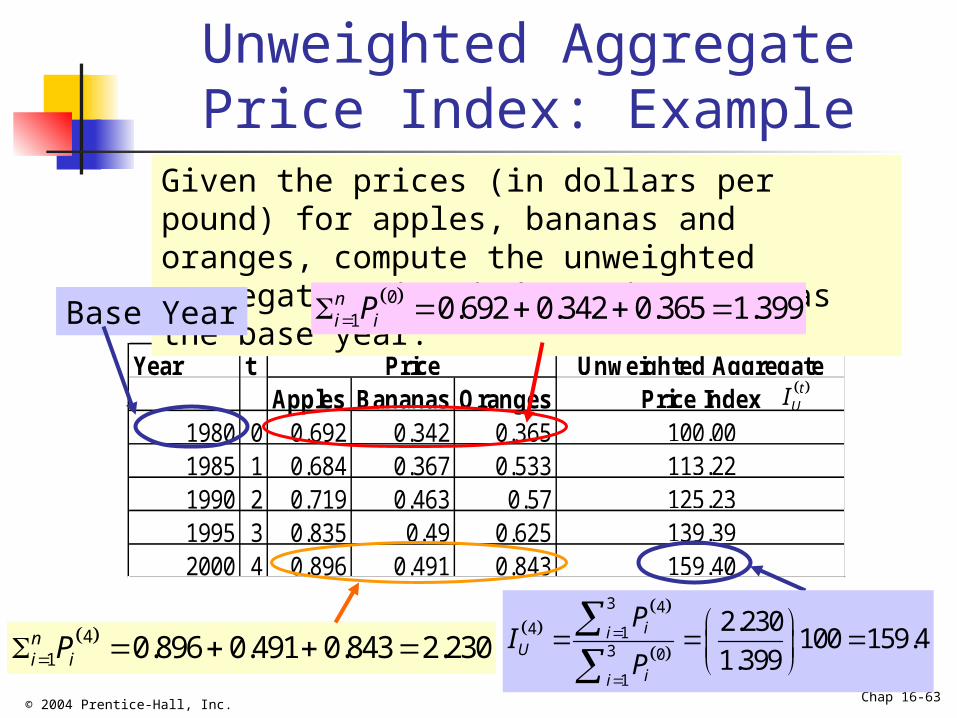

Year tApples Bananas Oranges

1980 0 0.692 0.342 0.3651985 1 0.684 0.367 0.5331990 2 0.719 0.463 0.571995 3 0.835 0.49 0.6252000 4 0.896 0.491 0.843

113.22125.23139.39159.40

Unweighted Aggregate

100.00

PricePrice Index

Unweighted Aggregate Price Index: Example

Given the prices (in dollars per pound) for apples, bananas and oranges, compute the unweighted aggregate price index using 1980 as the base year: 0

1 0.692 0.342 0.365 1.399ni iP

tUI

Base Year

41 0.896 0.491 0.843 2.230n

i iP

3 44 1

3 0

1

2.230100 159.4

1.399ii

U

ii

PI

P

© 2004 Prentice-Hall, Inc. Chap 16-64

Weighted Aggregate Price Indexes

Allow for Differences in the Consumption Levels Associated with the Different Items Comprising the Market Basket by Attaching a Weight to Each Item to Reflect the Consumption Quantity of that Item

Account for Differences in the Magnitude of Prices Per Unit and Differences in the Consumption Levels of the Items

Two Types that are Commonly Used The Laspeyres price index The Paasche price index

© 2004 Prentice-Hall, Inc. Chap 16-65

Laspeyres Price Index

Uses the Consumption Quantities Associated with the Base Year

01

0 01

0

100

where = time period (0, 1, 2, )

= total number of items under consideration

= quantity of item at time period 0

= value of the Laspe

tnt i i iL n

i i i

i

tL

P QI

P Q

t

n

Q i

I

yres price index at time t

© 2004 Prentice-Hall, Inc. Chap 16-66

Laspeyres Price Index: Example

Given the prices (in dollars per pound) and per capita consumption (in pounds) for apples, bananas, and oranges, compute the Laspeyres price index using 1980 as the base year: 3 0 0

10.692 19.2 0.342 20.2 0.365 14.3 25.4143i ii

P Q

3 4 0

10.896 19.2 0.491 20.2 0.843 14.3 39.1763i ii

P Q

Year t Laspeyres P Q P Q P Q Price Index

1980 0 0.692 19.2 0.342 20.2 0.365 14.3 100.001985 1 0.684 17.3 0.367 23.5 0.533 11.6 110.841990 2 0.719 19.6 0.463 24.4 0.57 12.4 123.191995 3 0.835 18.9 0.49 27.4 0.625 12 137.202000 4 0.896 18.8 0.491 31.4 0.843 8.6 154.15

Apple Bananas Oranges

4 39.1763100 154.15

25.4143LI

© 2004 Prentice-Hall, Inc. Chap 16-67

Paasche Price Index

Uses the Consumption Quantities Experienced in the Year of Interest Instead of Using the Initial Quantities

10 0

1

100

where = time period (0, 1, 2, )

= total number of items under consideration

= quantity of item at time period

= value of the Paasc

t tnt i i iP n

i i i

ti

tP

P QI

P Q

t

n

Q i t

I

he price index at time t

© 2004 Prentice-Hall, Inc. Chap 16-68

Paasche Price Index

Advantage A more accurate reflection of total consumption

costs at the point of interest in time Disadvantages

Accurate consumption values for current purchases are often hard to obtain

If a particular product increases greatly in price compared to other items in the market basket, consumers will avoid the high-priced item out of necessity, not because of changes in preferences

(continued)

© 2004 Prentice-Hall, Inc. Chap 16-69

Paasche Price Index: Example

Given the prices (in dollars per pound) and per capita consumption (in pounds) for apples, bananas, and oranges, compute the Paasche price index using 1980 as the base year: 3 0 0

10.692 19.2 0.342 20.2 0.365 14.3 25.4143i ii

P Q

4 39.5120100 155.47

25.4143PI

3 4 4

10.896 18.8 0.491 31.4 0.843 8.6 39.5120i ii

P Q

Year t Laspeyres P Q P Q P Q Price Index

1980 0 0.692 19.2 0.342 20.2 0.365 14.3 100.001985 1 0.684 17.3 0.367 23.5 0.533 11.6 104.821990 2 0.719 19.6 0.463 24.4 0.57 12.4 127.711995 3 0.835 18.9 0.49 27.4 0.625 12 144.442000 4 0.896 18.8 0.491 31.4 0.843 8.6 155.47

Apple Bananas Oranges

© 2004 Prentice-Hall, Inc. Chap 16-70

Pitfalls Concerning Time-Series Forecasting

Taking for Granted the Mechanism that Governs the Time Series Behavior in the Past Will Still Hold in the Future

Using Mechanical Extrapolation of the Trend to Forecast the Future Without Considering Personal Judgments, Business Experiences, Changing Technologies, Habits, Etc.

© 2004 Prentice-Hall, Inc. Chap 16-71

Chapter Summary

Discussed the Importance of Forecasting Addressed Component Factors of the

Time-Series Model Performed Smoothing of Data Series

Moving averages Exponential smoothing

Described Least-Squares Trend Fitting and Forecasting Linear, quadratic and exponential models

© 2004 Prentice-Hall, Inc. Chap 16-72

Chapter Summary

Discussed Holt-Winters Method of Trend Fitting and Forecasting

Addressed Autoregressive Models Described Procedure for Choosing

Appropriate Models Addressed Time-Series Forecasting of

Monthly or Quarterly Data (Use of Dummy-Variables)

Discussed Pitfalls Concerning Time-Series Forecasting

Described Index Numbers

(continued)