41

© 2011 Financial Operations Networks LLC Vendor Master File Strategies to Improve Performance and Reduce Risk Greg Crow Equifax Tuesday, April 12, 2011

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | pamela-hensley |

| View: | 216 times |

| Download: | 1 times |

© 2011 Financial Operations Networks LLC

Vendor Master File Strategiesto Improve Performance

and Reduce Risk Greg CrowEquifax

Tuesday, April 12, 2011

www.TheAPNetwork.com Page 2

THE ACCOUNTS PAYABLE

Leadership ConferenceAgenda

• Identify keys to spotting potential fraud in your vendor master file

• Ensure you are in compliance with U.S. laws and regulations, including IRS and OFAC

• Deploy a process to verify supplier identities and potential for risk before you release funds

• Provide visibility into potential supplier deterioration and failure in your supply base

www.TheAPNetwork.com Page 3

THE ACCOUNTS PAYABLE

Leadership Conference

How can I reduce fraud?

How can I show management

that we have effective compliance to policy?

How can I comply with IRS, OFAC and state-level laws

and regulations?

How can I streamline the supplier

boarding process?

How can I reduce duplicate suppliers and duplicate payments?

There are many questions ...

How does Sarbanes- Oxley impact AP?

How can I do all of this with such a small team?

AccountsPayable Executives

How can I help my firm better manage

cash flow?

www.TheAPNetwork.com Page 4

THE ACCOUNTS PAYABLE

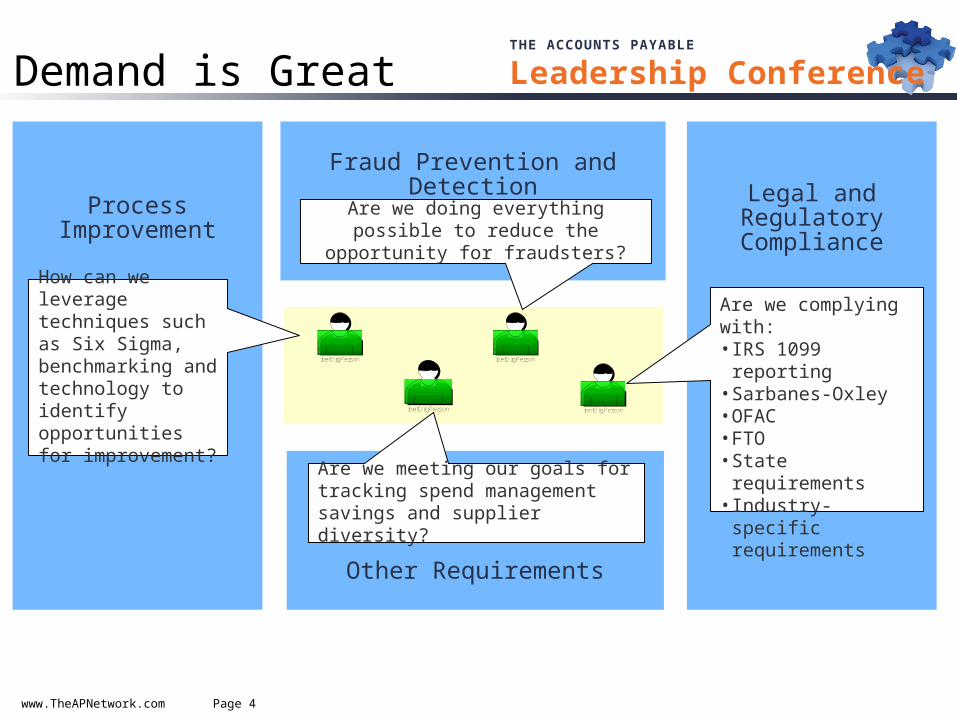

Leadership ConferenceDemand is Great

Other Requirements

Fraud Prevention and DetectionLegal and Regulatory

ComplianceProcess

Improvement

inetOrgPerson

Are we doing everything possible to reduce the opportunity for fraudsters?

Are we complying with:• IRS 1099 reporting• Sarbanes-Oxley• OFAC• FTO• State requirements• Industry-specific

requirements

How can we leverage techniques such as Six Sigma, benchmarking and technology to identify opportunities for improvement?

Are we meeting our goals for tracking spend management savings and supplier diversity?

inetOrgPersoninetOrgPerson

inetOrgPerson

www.TheAPNetwork.com Page 5

THE ACCOUNTS PAYABLE

Leadership ConferenceYour SuppliersAre Changing

Source: http://www.freepress.net/files/att_history.swf

www.TheAPNetwork.com Page 6

THE ACCOUNTS PAYABLE

Leadership ConferenceInternal Obstacles

• Policy does not equal practice

• Technology does not deliver business process improvement

• Outsourcing can reduce accountability

www.TheAPNetwork.com Page 7

THE ACCOUNTS PAYABLE

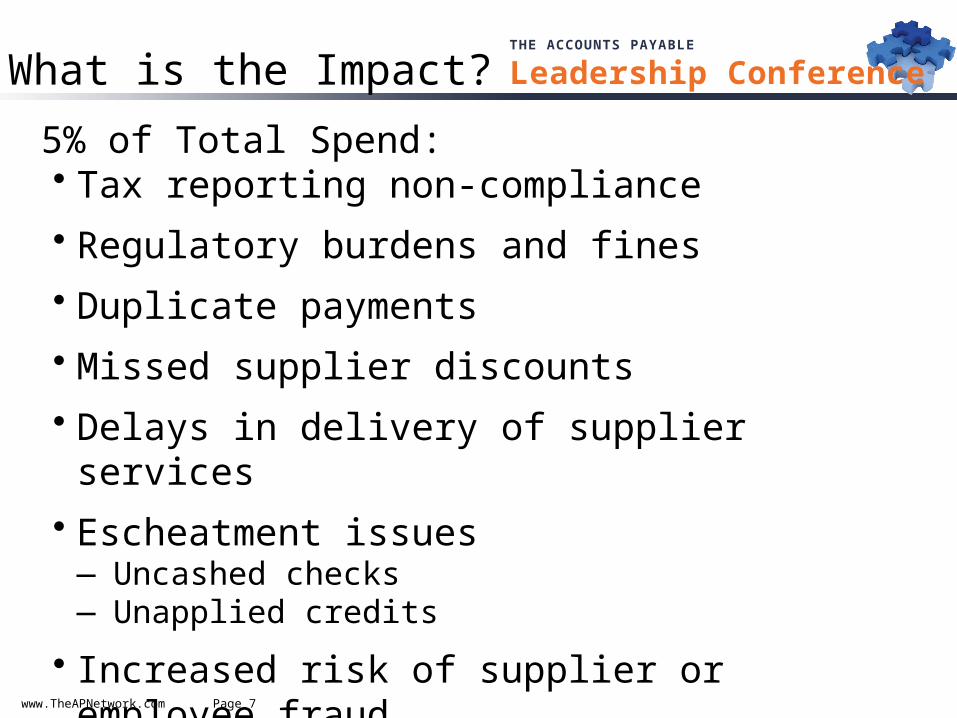

Leadership ConferenceWhat is the Impact?

5% of Total Spend:• Tax reporting non-compliance

• Regulatory burdens and fines

• Duplicate payments

• Missed supplier discounts

• Delays in delivery of supplier services

• Escheatment issues― Uncashed checks― Unapplied credits

• Increased risk of supplier or employee fraud

www.TheAPNetwork.com Page 8

THE ACCOUNTS PAYABLE

Leadership Conference

Assessing Risk in Your Vendor MasterMaking the Case for Change

www.TheAPNetwork.com Page 9

THE ACCOUNTS PAYABLE

Leadership Conference

• Can be done using internal IT resources, consultants or service providers

• Assesses VMF data quality

• Makes specific recommendations on improving overall accuracy of information

• Key deliverables include:―Identifying file duplication―Assessing/improving address quality―Standardizing other elements (country, tax ID, telephone)

Vendor Master Profiling

www.TheAPNetwork.com Page 10

THE ACCOUNTS PAYABLE

Leadership ConferenceSample ReportMetric

SupplierRecords

% of Total Records

ABC Company Spend

% of Total Spend

ABC Company supplier records 17,917 100.0% $1,288M 100.0%ABC Company supplier records matched to Equifax Database 14,832 82.8% $1,191M 92.5%ABC Company supplier records not matched to Equifax Database 3,085 17.2% $97M 7.5%

Non-matched records with primary exceptions 2,160 12.0% $68M 5.2%

Non-matched records without primary exceptions 926 5.2% $29M 2.2%

www.TheAPNetwork.com Page 11

THE ACCOUNTS PAYABLE

Leadership Conference

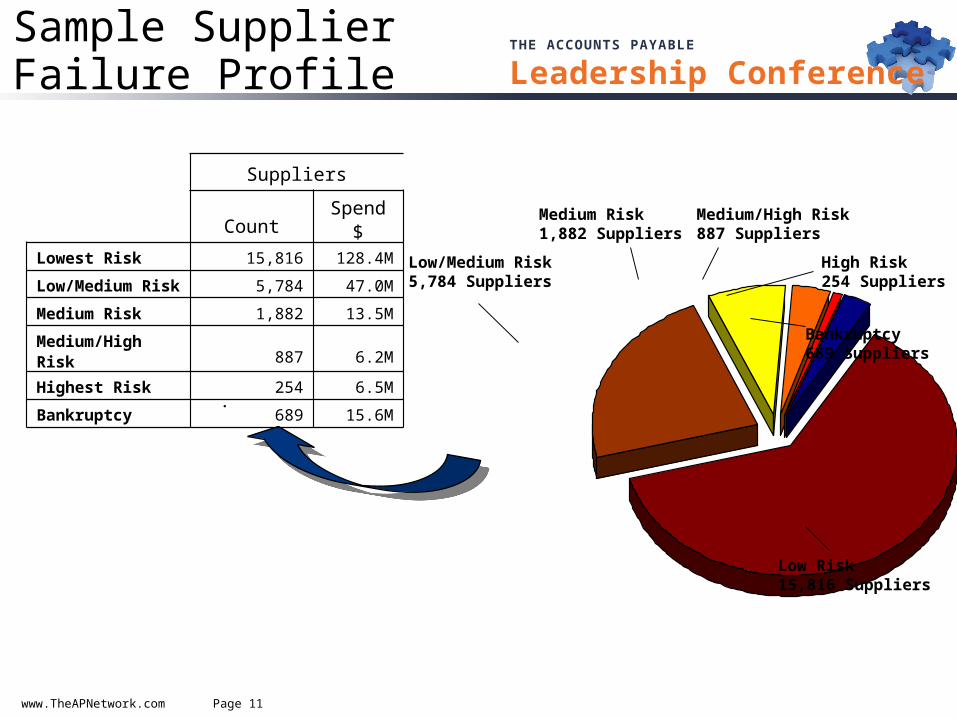

.

Medium Risk1,882 Suppliers

Low/Medium Risk5,784 Suppliers

Low Risk15,816 Suppliers

Medium/High Risk887 Suppliers

Suppliers

Count Spend $

Lowest Risk 15,816 128.4M

Low/Medium Risk 5,784 47.0M

Medium Risk 1,882 13.5M

Medium/High Risk 887 6.2M

Highest Risk 254 6.5M

Bankruptcy 689 15.6M

Bankruptcy689 Suppliers

High Risk254 Suppliers

Sample SupplierFailure Profile

www.TheAPNetwork.com Page 12

THE ACCOUNTS PAYABLE

Leadership Conference

Commercial services rely upon robust reference databases and automated and manual review to identify 75+% of all duplicates

12345AceLoading Dock 12Dallas, TX

75220(214) 555-1234

NCC1701A.C.E. Supply3050 Northwest HwyDallas, TX 75220(214) 555-1234

A-4895John SmithAce Mart3050 NW HwyIrving, TX214.555.123492345

EFX # 112233456Name 1 Ace Mart Supply Inc.Name 2 Ace SupplyStreet 3050 W Northwest HwyCity DallasState TXPostal Code 75220-5941Telephone (214) 555-1234Owner John SmithLegacy Vendor # 1 12345Legacy Vendor # 2 NCC1701Legacy Vendor # 3 A-4895

Vendor Master Records

All represent the same business:

Vendor De-duplication

www.TheAPNetwork.com Page 13

THE ACCOUNTS PAYABLE

Leadership ConferenceManual VMF Cleanup• Take advantage of cleanup opportunities

― Systems upgrades/migrations― Merger/acquisition

• Cutoff by last transaction date, marking the balance of records for archive review

• You can identify 25-40% of supplier duplicates by doing the following:― Step 1: Extract supplier number, supplier name, supplier address,

phone and TIN into an Excel file or Access database. You may also choose a few other attributes such as 1099 status, etc.

― Step 2: Identify exact duplicates on name and address― Step 3: Try the sorts on the following slide, looking for near duplicates

populating one field and leaving the rest as “same”― Step 4: Identify candidates for joint AP and procurement review

www.TheAPNetwork.com Page 14

THE ACCOUNTS PAYABLE

Leadership ConferenceManual Duplicate Review

Supplier #

Supplier Name Address Phone TIN# Category

Different Same Same Same Same Simple Duplicate

Different Similar/DBA vs. Legal Same Same Same

Supplier Name Duplicate*

Different SameSimilar/Physical vs. Mailing

Same SameSupplier Address Duplicate*

Different Same Same Similar/ One Null Same Phone Duplicate

Different Same Same Same Similar/One Null TIN Duplicate*

* Potential indicator of fraud: review is suggested

www.TheAPNetwork.com Page 15

THE ACCOUNTS PAYABLE

Leadership Conference

Legal/Regulatory Compliance What You Need to Know

www.TheAPNetwork.com Page 16

THE ACCOUNTS PAYABLE

Leadership Conference

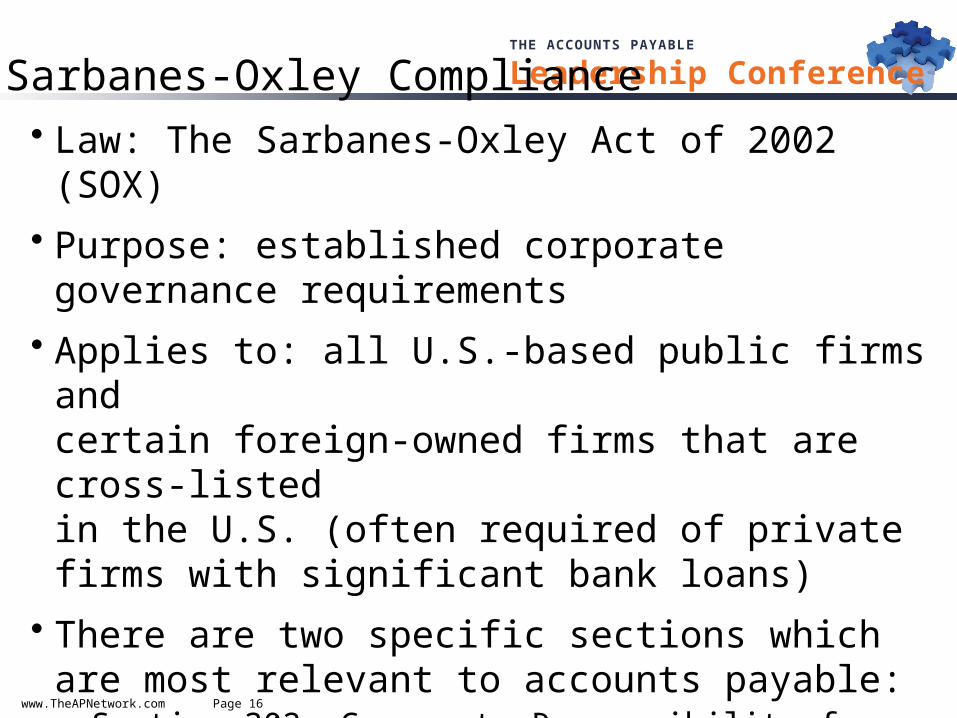

Sarbanes-Oxley Compliance• Law: The Sarbanes-Oxley Act of 2002 (SOX)

• Purpose: established corporate governance requirements

• Applies to: all U.S.-based public firms and certain foreign-owned firms that are cross-listed in the U.S. (often required of private firms with significant bank loans)

• There are two specific sections which are most relevant to accounts payable:― Section 302: Corporate Responsibility for Financial Reports ― Section 404: Management Assessment of Internal Controls

www.TheAPNetwork.com Page 17

THE ACCOUNTS PAYABLE

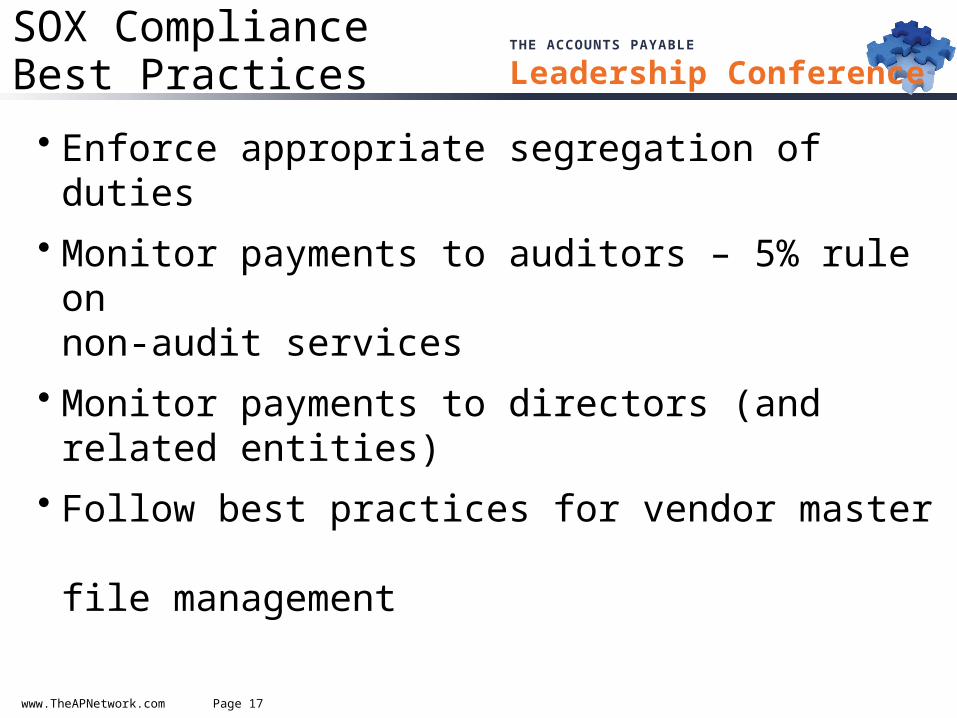

Leadership ConferenceSOX ComplianceBest Practices

• Enforce appropriate segregation of duties

• Monitor payments to auditors – 5% rule on non-audit services

• Monitor payments to directors (and related entities)

• Follow best practices for vendor master file management

www.TheAPNetwork.com Page 18

THE ACCOUNTS PAYABLE

Leadership ConferencePolling Question

How frequently does your firm check suppliers against debarment/denied parties lists?

a) Neverb) Supplier setup onlyc) Regular (monthly or quarterly) vendor

master screens for changesd) Supplier setup and regular vendor

master screens

www.TheAPNetwork.com Page 19

THE ACCOUNTS PAYABLE

Leadership Conference

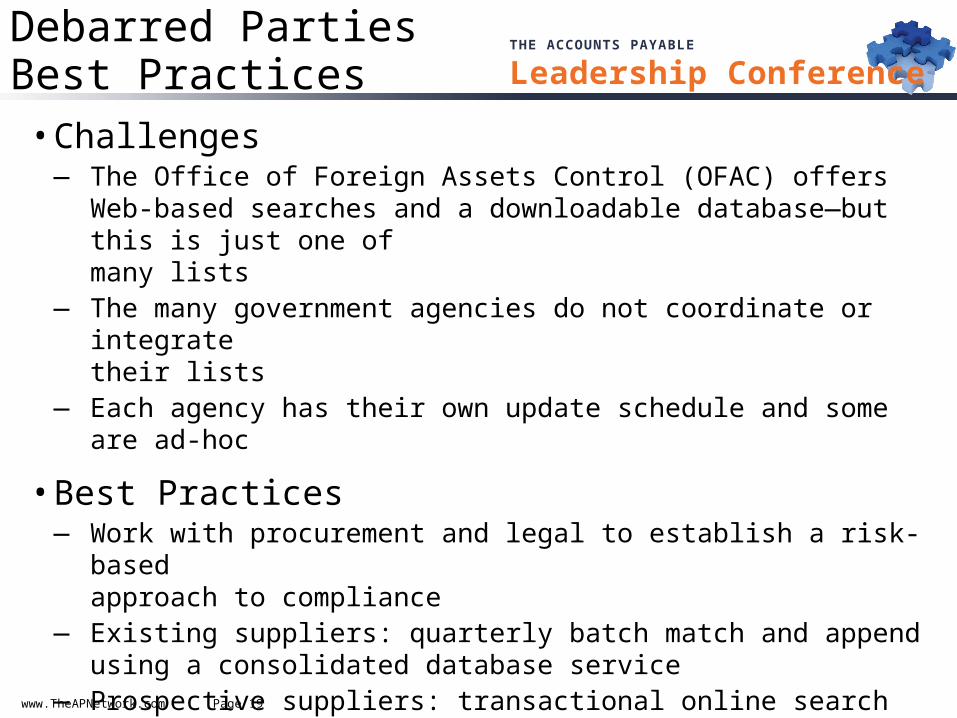

Debarred PartiesBest Practices

• Challenges― The Office of Foreign Assets Control (OFAC) offers Web-based

searches and a downloadable database—but this is just one of many lists

― The many government agencies do not coordinate or integrate their lists

― Each agency has their own update schedule and some are ad-hoc

• Best Practices― Work with procurement and legal to establish a risk-based

approach to compliance― Existing suppliers: quarterly batch match and append using a

consolidated database service― Prospective suppliers: transactional online search against all

required lists or a consolidated database as part of onboarding

www.TheAPNetwork.com Page 20

THE ACCOUNTS PAYABLE

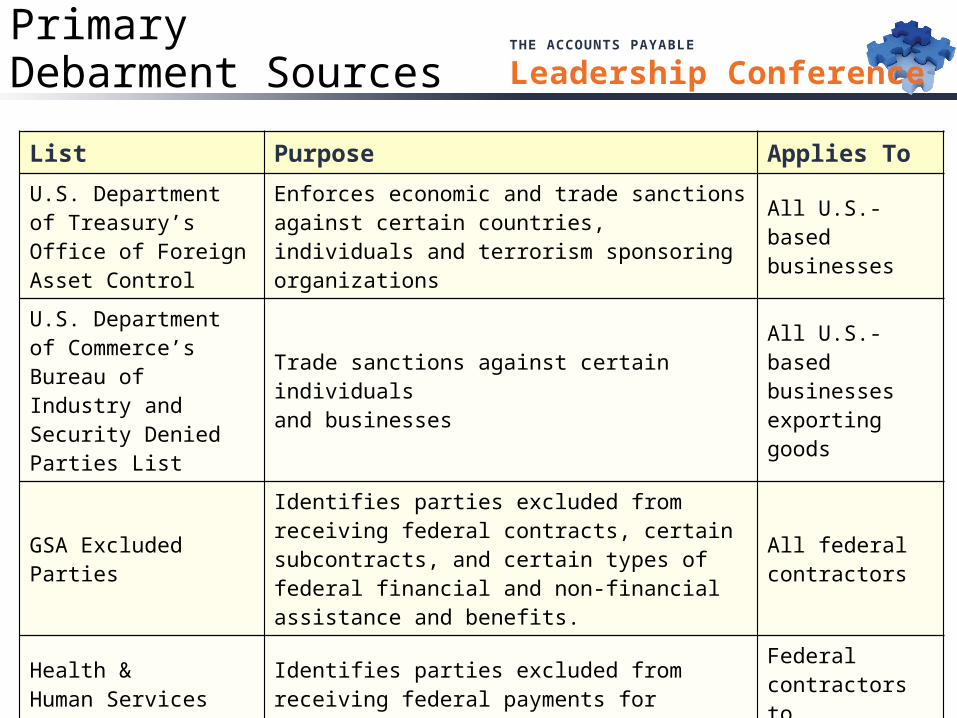

Leadership ConferencePrimaryDebarment Sources

List Purpose Applies To

U.S. Department of Treasury’s Office of Foreign Asset Control

Enforces economic and trade sanctions against certain countries, individuals and terrorism sponsoring organizations

All U.S.-based businesses

U.S. Department of Commerce’s Bureau of Industry and Security Denied Parties List

Trade sanctions against certain individuals and businesses

All U.S.-based businesses exporting goods

GSA Excluded Parties

Identifies parties excluded from receiving federal contracts, certain subcontracts, and certain types of federal financial and non-financial assistance and benefits.

All federal contractors

Health & Human Services Excluded Parties

Identifies parties excluded from receiving federal payments for healthcare services

Federal contractors to the HHS

www.TheAPNetwork.com Page 21

THE ACCOUNTS PAYABLE

Leadership ConferenceThe Costof Non-Compliance

• Portions of Boeing Co. space systems operations remain ineligible to receive government contracts

• Eden Prairie company was fined $400,000 for export violations

• Lloyds TSB expects £180M bill for U.S. blacklist breach• OFAC fines National Australia Bank a $3M for ‘trading

with enemies’• OFAC (Office of Foreign Assets Control) fines more than

100 travelers $1,000 each • OFAC fines 74-year grandmother $8,500 for bicycling

in Cuba

www.TheAPNetwork.com Page 22

THE ACCOUNTS PAYABLE

Leadership Conference

Supplier Data Management Know Your Suppliers, Mitigate Your Risk

www.TheAPNetwork.com Page 23

THE ACCOUNTS PAYABLE

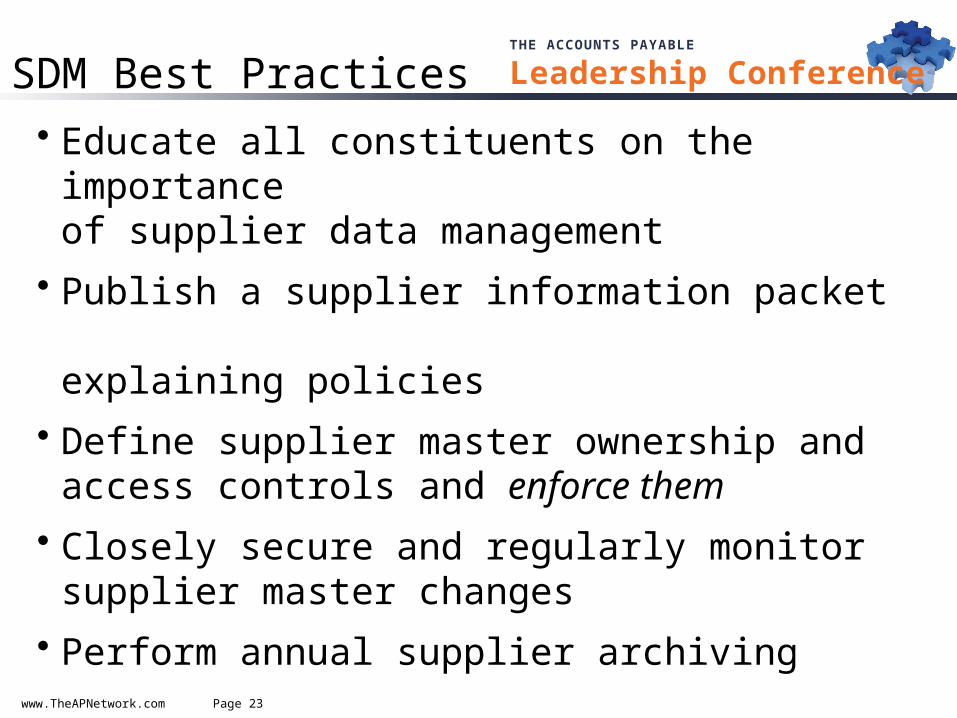

Leadership ConferenceSDM Best Practices

• Educate all constituents on the importance of supplier data management

• Publish a supplier information packet explaining policies

• Define supplier master ownership and access controls and enforce them

• Closely secure and regularly monitor supplier master changes

• Perform annual supplier archiving

www.TheAPNetwork.com Page 24

THE ACCOUNTS PAYABLE

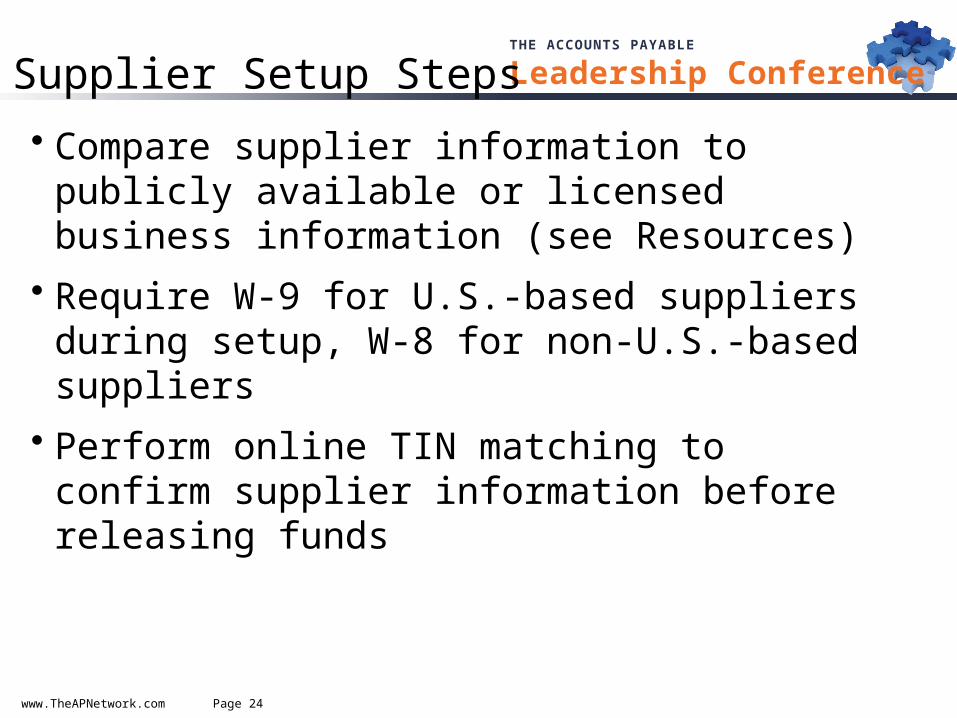

Leadership ConferenceSupplier Setup Steps

• Compare supplier information to publicly available or licensed business information (see Resources)

• Require W-9 for U.S.-based suppliers during setup, W-8 for non-U.S.-based suppliers

• Perform online TIN matching to confirm supplier information before releasing funds

www.TheAPNetwork.com Page 25

THE ACCOUNTS PAYABLE

Leadership ConferenceSupplier Setup Checklist• Develop a scorecard, allocating limited AP review

resources based on level of risk

• A few suggestions for a supplier red-flag checklist― Mail receiving agency addresses/vacant

addresses/prison addresses― Residential addresses with large invoices― No telephone number― Supplier with same address/phone number/SSN/bank

account as employee

www.TheAPNetwork.com Page 26

THE ACCOUNTS PAYABLE

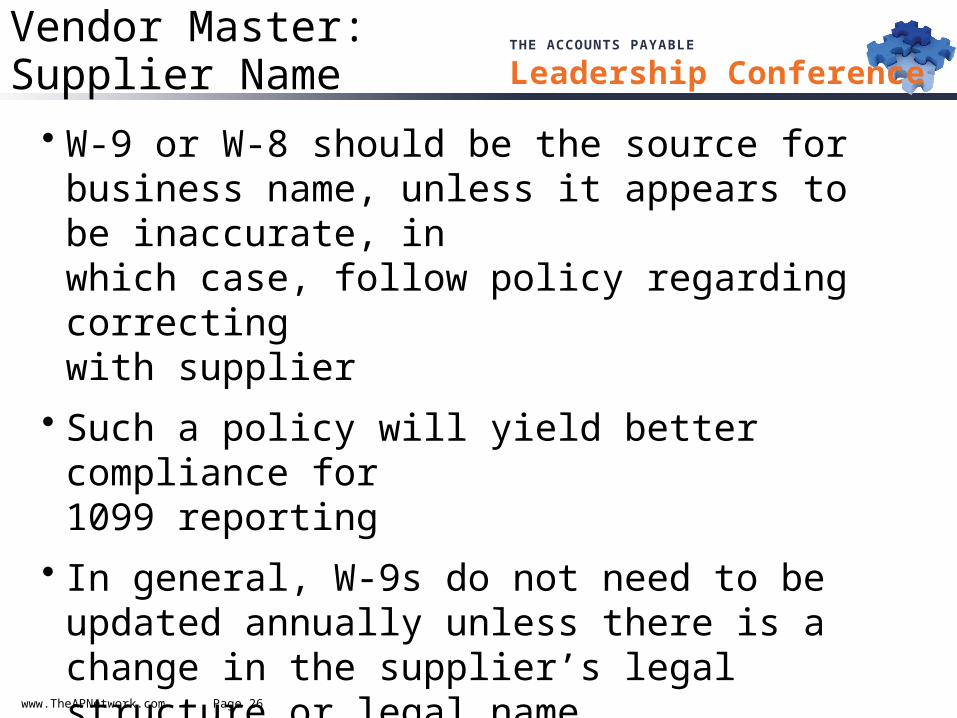

Leadership ConferenceVendor Master:Supplier Name

• W-9 or W-8 should be the source for business name, unless it appears to be inaccurate, in which case, follow policy regarding correcting with supplier

• Such a policy will yield better compliance for 1099 reporting

• In general, W-9s do not need to be updated annually unless there is a change in the supplier’s legal structure or legal name

www.TheAPNetwork.com Page 27

THE ACCOUNTS PAYABLE

Leadership ConferencePolling Question

On what percentage of active U.S. suppliers do you have a W-9 document on file?

a) <10%b) 10%-25%c) 25%-50%d) >50%

www.TheAPNetwork.com Page 28

THE ACCOUNTS PAYABLE

Leadership ConferenceIRS TIN Matching

• TIN Matching is available to any qualified payor to help reduce the number of “B” Notices

• Options include online matching (up to 25 records) and bulk matching (up to 100K records)

• Important: TIN Matching now only compares the EIN/SSN/ITIN and the first 4 characters of the supplier legal name (name control)—poor data quality practices are more likely to cause a mismatch than in the past

• IRS name control may only contain the following characters:― Numeric (0- 9), Alpha (A-Z), Hyphen (-), Ampersand (&)

www.TheAPNetwork.com Page 29

THE ACCOUNTS PAYABLE

Leadership ConferenceVendor Master:Supplier Name

The most important rule is to simply be consistent but there are a few best

practices that practitioners agree on …

www.TheAPNetwork.com Page 30

THE ACCOUNTS PAYABLE

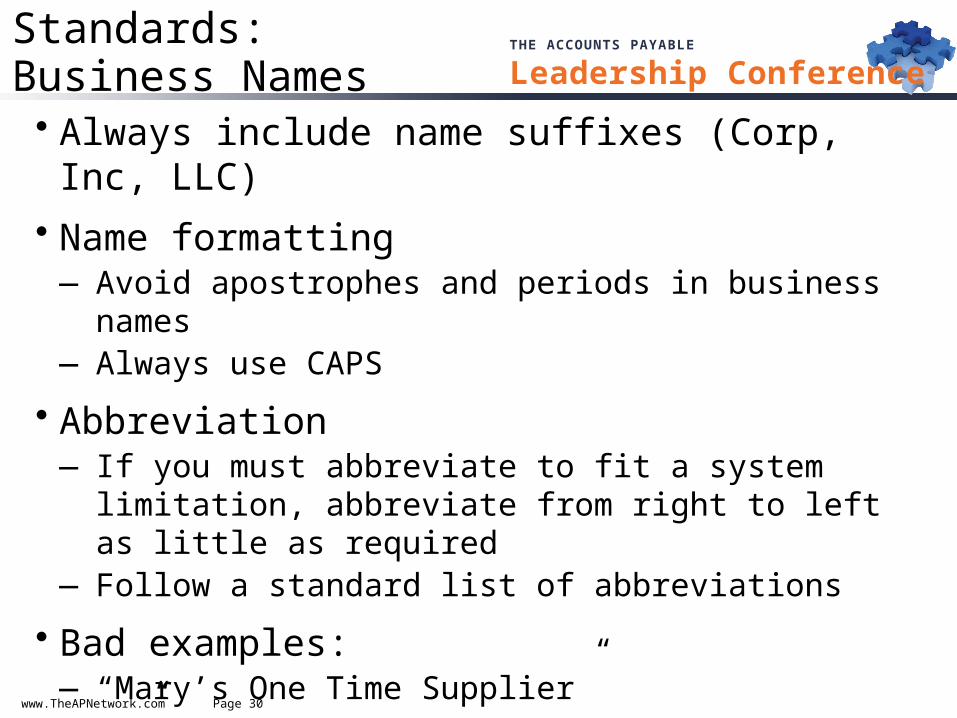

Leadership ConferenceStandards:Business Names• Always include name suffixes (Corp, Inc, LLC)

• Name formatting― Avoid apostrophes and periods in business names― Always use CAPS

• Abbreviation― If you must abbreviate to fit a system limitation, abbreviate

from right to left as little as required― Follow a standard list of abbreviations

• Bad examples: ― “Mary’s One Time Supplier”― “.”― “ ”

www.TheAPNetwork.com Page 31

THE ACCOUNTS PAYABLE

Leadership ConferenceStandards:Individual Names

• Exclude honorifics such as Mr., Mrs., etc.

• Exclude spaces in surnames ― (McDonald, not Mc Donald)

• Apply consistency in last name, first name vs. first name last name standards

• Bad example: employee vendors

www.TheAPNetwork.com Page 32

THE ACCOUNTS PAYABLE

Leadership ConferenceStandards:Government Names

Taxing Authorities• In general, use the same rules as for business name

• Recommended naming convention for government entities:― TEXAS, STATE OF― DALLAS, CITY OF― DALLAS, COUNTY OF

• Put departments in a secondary field if possible

www.TheAPNetwork.com Page 33

THE ACCOUNTS PAYABLE

Leadership ConferenceStandards:Addresses

Online services verify addresses as deliverable and for other suspect conditions (see Resources)• Do not run business name into address line 1

• USPS Publication 28

• Universal Postal Union

www.TheAPNetwork.com Page 34

THE ACCOUNTS PAYABLE

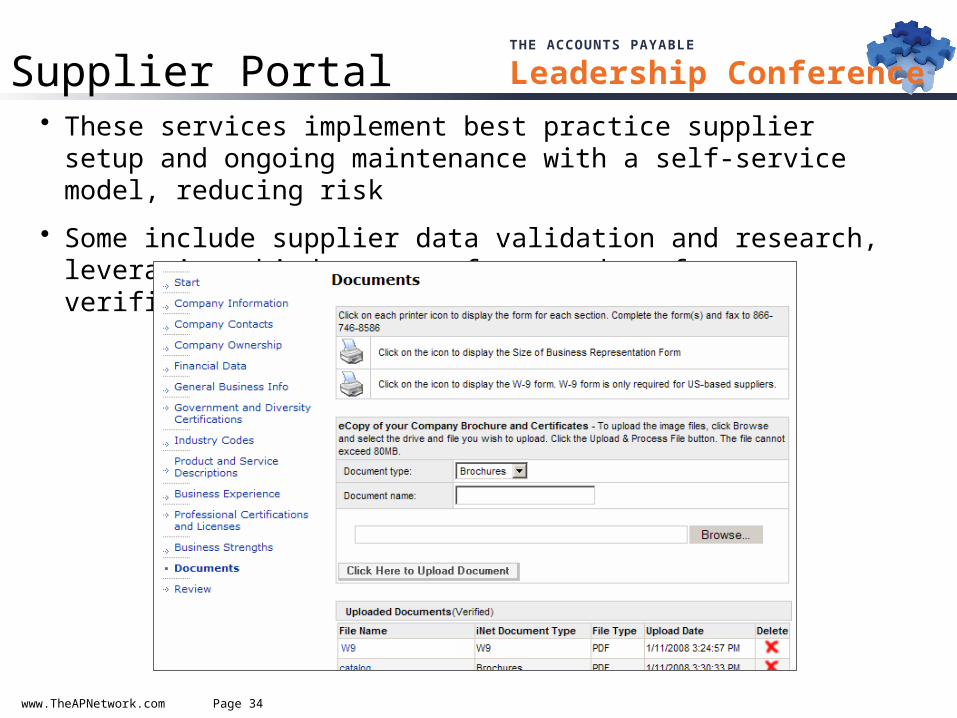

Leadership ConferenceSupplier Portal• These services implement best practice supplier setup and ongoing

maintenance with a self-service model, reducing risk

• Some include supplier data validation and research, leveraging third party reference data for verification

www.TheAPNetwork.com Page 35

THE ACCOUNTS PAYABLE

Leadership ConferenceSupplier Monitoring

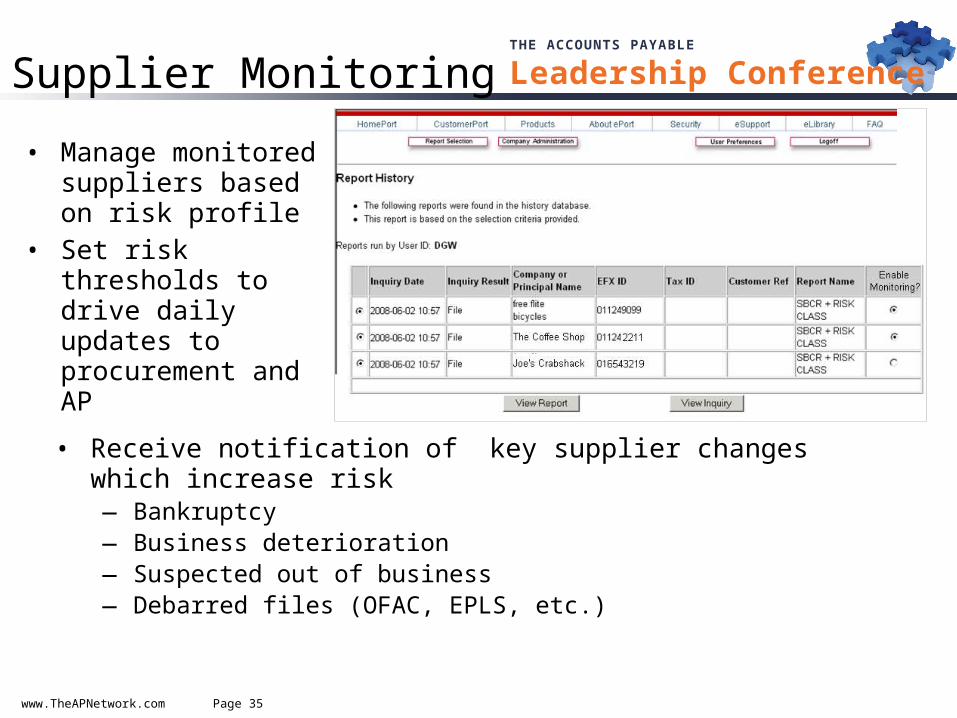

• Manage monitored suppliers based on risk profile

• Set risk thresholds to drive daily updates to procurement and AP

• Receive notification of key supplier changes which increase risk― Bankruptcy― Business deterioration― Suspected out of business― Debarred files (OFAC, EPLS, etc.)

www.TheAPNetwork.com Page 36

THE ACCOUNTS PAYABLE

Leadership ConferenceCase Study• Background

― Global manufacturer with 200K suppliers with a decentralized AP model― Developing a shared service model for consistent best practices

supplier data management approach across multiple divisions and systems and needed technology and verification services

• Solution― Eliminated nearly 25% of vendor master records (duplicates, inactive)― Implemented a streamlined supplier boarding service to support

supplier data verification prior to releasing funds― Developed integration with SAP supplier master using robust business

rules for change management― Improved response SLA to the business by over 50%― Maintains visibility to 99% of total spend, reducing ongoing vendor

master based risk

www.TheAPNetwork.com Page 37

THE ACCOUNTS PAYABLE

Leadership Conference

Resources Where to Go for More

www.TheAPNetwork.com Page 38

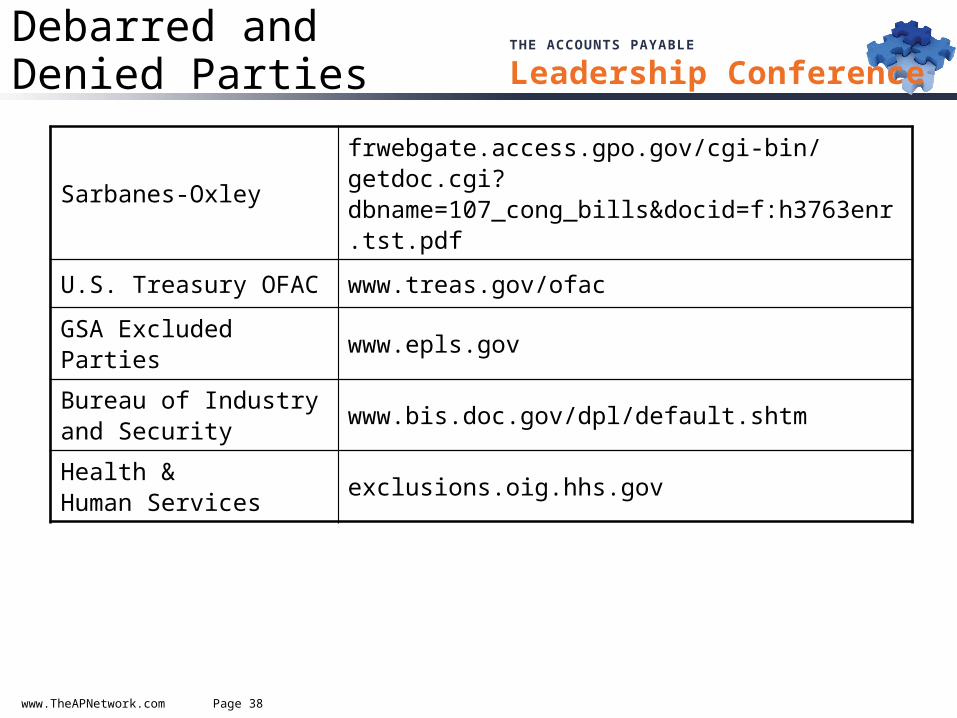

THE ACCOUNTS PAYABLE

Leadership ConferenceDebarred andDenied Parties

Sarbanes-Oxley frwebgate.access.gpo.gov/cgi-bin/getdoc.cgi?dbname=107_cong_bills&docid=f:h3763enr.tst.pdf

U.S. Treasury OFAC www.treas.gov/ofac

GSA Excluded Parties www.epls.gov

Bureau of Industryand Security www.bis.doc.gov/dpl/default.shtm

Health & Human Services exclusions.oig.hhs.gov

www.TheAPNetwork.com Page 39

THE ACCOUNTS PAYABLE

Leadership ConferenceSupplier Verification

State Secretary of States www.secstates.com/

Non-profits www.irs.gov/app/pub-78/

USPS Address Search www.usps/zip4

USPS Publication 28 pe.usps.gov/cpim/ftp/pubs/Pub28/pub28.pdf

Universal Postal Union www.upu.int

IRS TIN Matching www.irs.gov/taxpros/article/0,,id=107478,00.htmlwww.irs.gov/businesses/corporations/article/0,,id=155677,00.html

www.TheAPNetwork.com Page 40

THE ACCOUNTS PAYABLE

Leadership ConferenceYour Questions

© 2011 Financial Operations Networks LLC

Thank You!