Page 1

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

1

USA-MaltaDouble Tax Treaty

Dr Juanita BrockdorffTax Partner

16 February 2011

Page 2

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

2

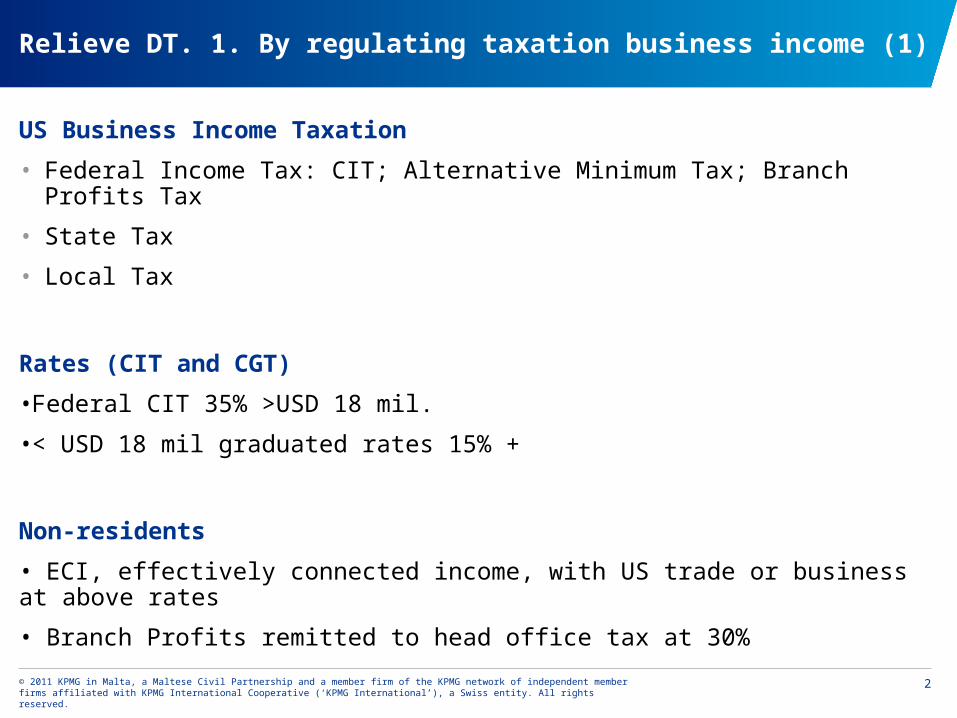

Relieve DT. 1. By regulating taxation business income (1)

US Business Income Taxation

• Federal Income Tax: CIT; Alternative Minimum Tax; Branch Profits Tax

• State Tax

• Local Tax

Rates (CIT and CGT)

•Federal CIT 35% >USD 18 mil.

•< USD 18 mil graduated rates 15% +

Non-residents

• ECI, effectively connected income, with US trade or business at above rates

• Branch Profits remitted to head office tax at 30%

Page 3

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

3

Relieve DT. 1. By regulating taxation business income (2)

•Treaty covers federal taxes; excludes local, state, social security and unemployment taxes

•Treaty protection for business income, including professional/personal services:

PE threshold

• Physical PE: fixed place of business through which business of enterprise is wholly or partially carried out

• Project PE: OECD 12-month threshold (oil rig/ship)

• Agency PE: dependant with mandate to bind principal and habitually does so

Net basis of taxation (similar to election for net taxation available for immovable property income where PE not necessary for situs tax)

Page 4

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

4

Relief DT: 2. Reduce WHT (1)

On US Source Portfolio Income

•WHT 30% Dividends, Interest, Royalties, Rents which not ECI

•Malta: higher than general. Why? vs Treaty Shopping

•15% Dividends. WHT usually 15%; but 10% Japan, Russia, Mexico

•5% Intercompany Dividends for 10% shareholders. Typical, but EU trend parent-sub 0% France, Germany, NL, UK etc. for 80% voting stock

•5% Branch Profits WHT Dividend equivalent, for neutrality with Subs. Italy 2010

•15% Dividends paid by US RIC (Registered Investment Companies)/ US REIT (Real Estate Investment Trusts). Prevents treaty circumvention by using, so higher WHT exception for RICS and REITS Italy; Protocol France 2010; in some treaties domestic rate WHT

•0% Dividend payments to pension funds.

Page 5

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

5

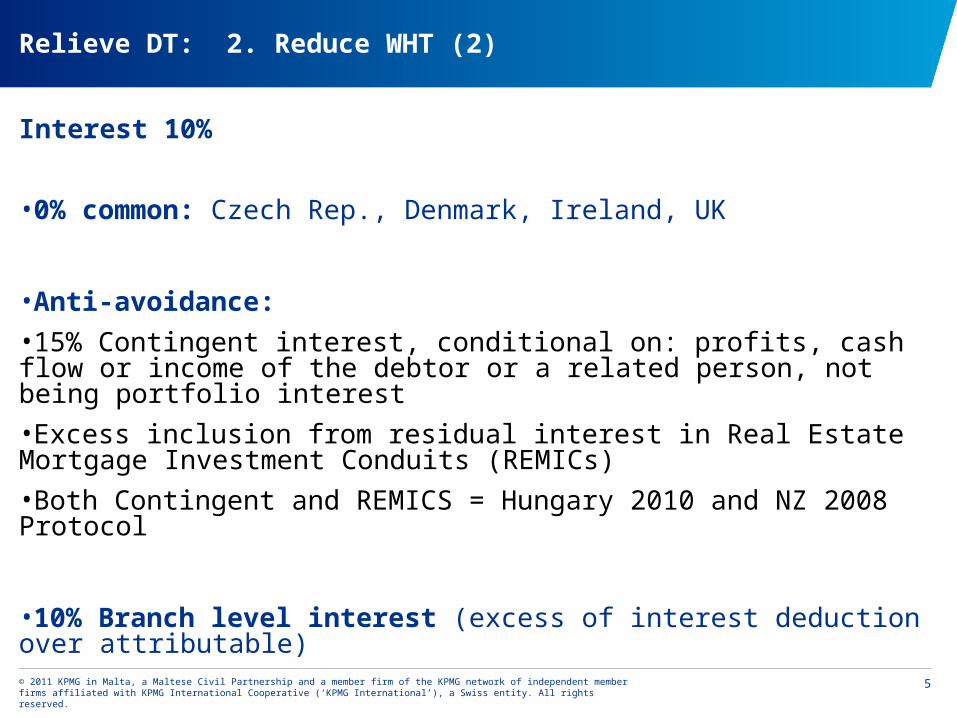

Relieve DT: 2. Reduce WHT (2)

Interest 10%

•0% common: Czech Rep., Denmark, Ireland, UK

•Anti-avoidance:

•15% Contingent interest, conditional on: profits, cash flow or income of the debtor or a related person, not being portfolio interest

•Excess inclusion from residual interest in Real Estate Mortgage Investment Conduits (REMICs)

•Both Contingent and REMICS = Hungary 2010 and NZ 2008 Protocol

•10% Branch level interest (excess of interest deduction over attributable)

Page 6

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

6

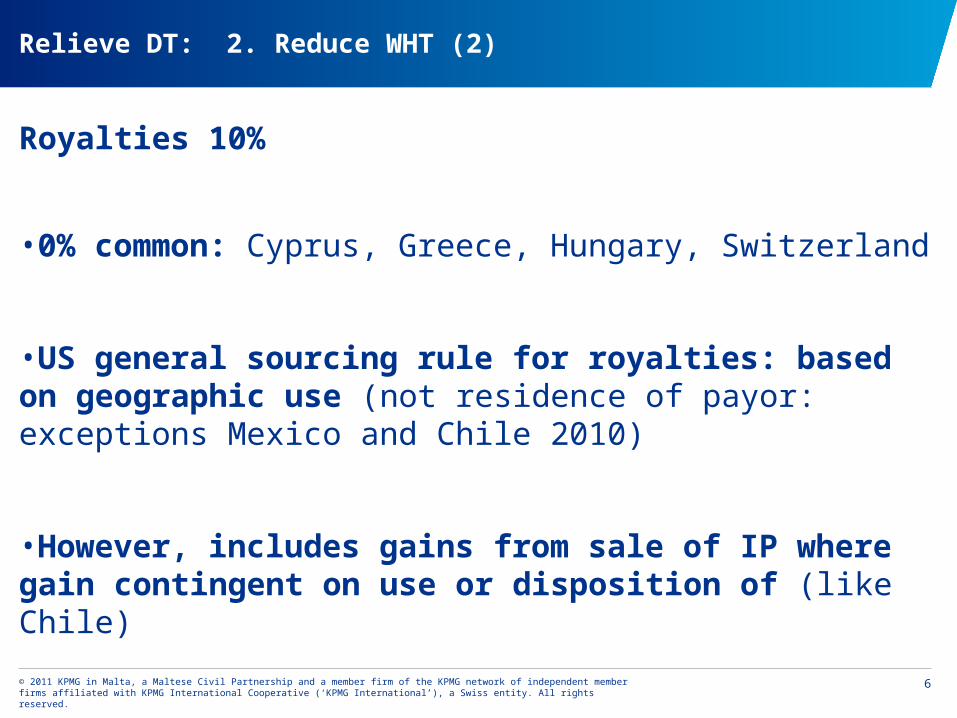

Relieve DT: 2. Reduce WHT (2)

Royalties 10%

•0% common: Cyprus, Greece, Hungary, Switzerland

•US general sourcing rule for royalties: based on geographic use (not residence of payor: exceptions Mexico and Chile 2010)

•However, includes gains from sale of IP where gain contingent on use or disposition of (like Chile)

Page 7

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

7

Relieve DT: 3. By allocating exclusive taxing rights

CG:

Residence country exclusive entitlement to tax gains on alienation of property

Special rules on certain transfers:

■ Immovable property (property-rich clause: US real property interest; MT assets principally immovable)

■ Business property of a PE

Pensions:

Only residence state

State pensions , or social security benefits pension only source state

Annuities / Alimony:

Residence state has exclusive taxing rights

Page 8

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

8

Relieve DT: 4. Credit Method

Credit for foreign taxes

US, Without Treaty:

• Ordinary FTC, and

• Indirect FTC (underlying tax credit) US Co deemed paid credit 10% voting Malta Co

US Treaty:

• Same as domestic

• Remittance Provision

Page 9

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

9

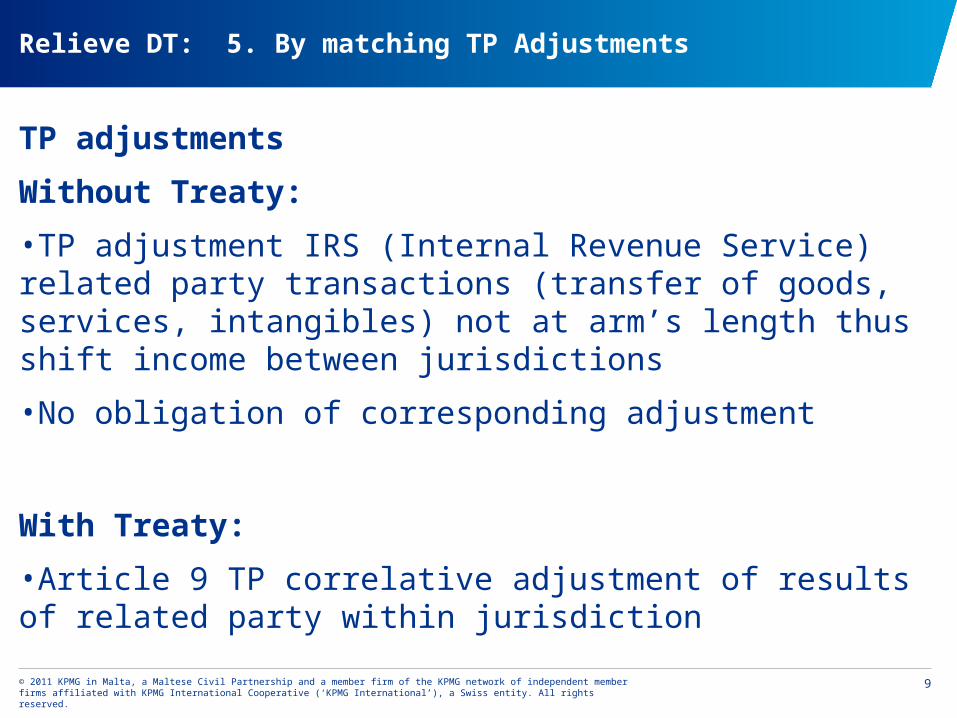

Relieve DT: 5. By matching TP Adjustments

TP adjustments

Without Treaty:

•TP adjustment IRS (Internal Revenue Service) related party transactions (transfer of goods, services, intangibles) not at arm’s length thus shift income between jurisdictions

•No obligation of corresponding adjustment

With Treaty:

•Article 9 TP correlative adjustment of results of related party within jurisdiction

Page 10

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

10

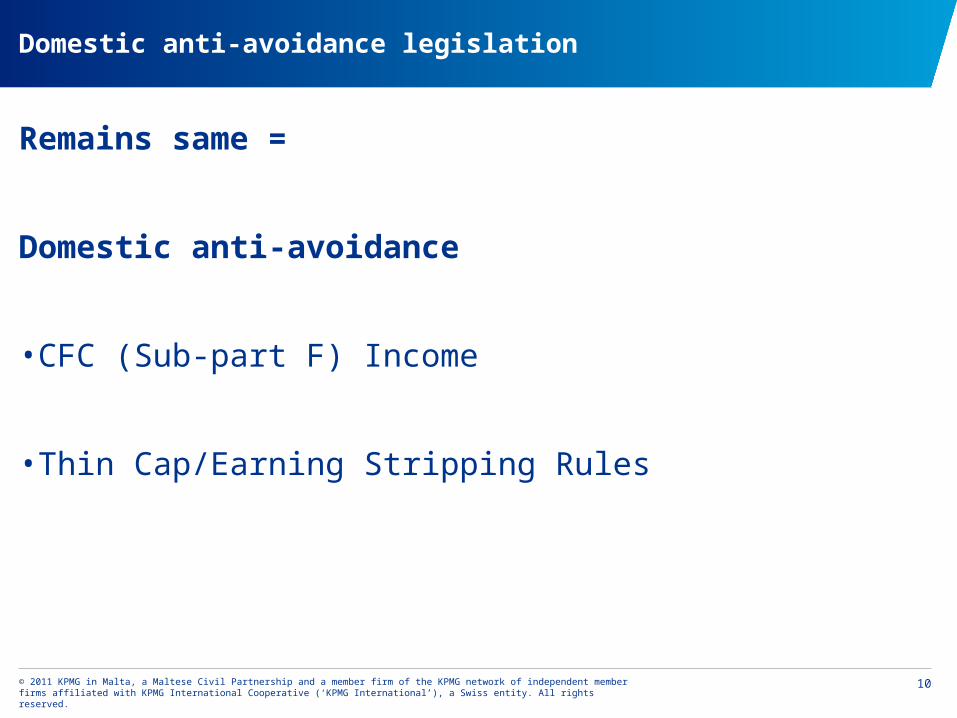

Domestic anti-avoidance legislation

Remains same =

Domestic anti-avoidance

•CFC (Sub-part F) Income

•Thin Cap/Earning Stripping Rules

Page 11

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

11

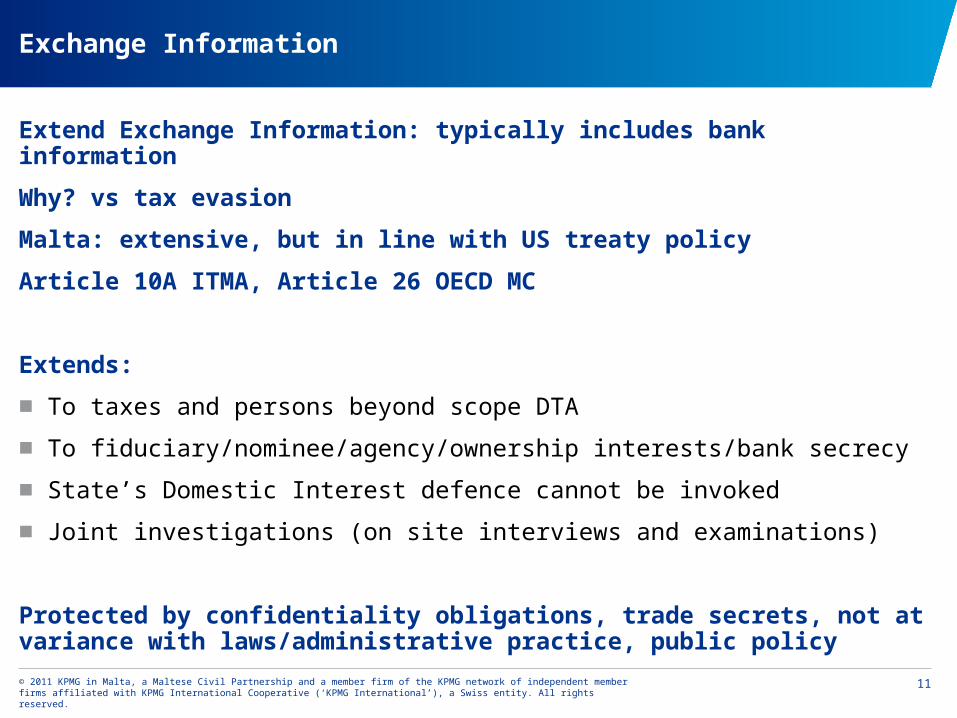

Exchange Information

Extend Exchange Information: typically includes bank information

Why? vs tax evasion

Malta: extensive, but in line with US treaty policy

Article 10A ITMA, Article 26 OECD MC

Extends:

■ To taxes and persons beyond scope DTA

■ To fiduciary/nominee/agency/ownership interests/bank secrecy

■ State’s Domestic Interest defence cannot be invoked

■ Joint investigations (on site interviews and examinations)

Protected by confidentiality obligations, trade secrets, not at variance with laws/administrative practice, public policy

Page 12

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

12

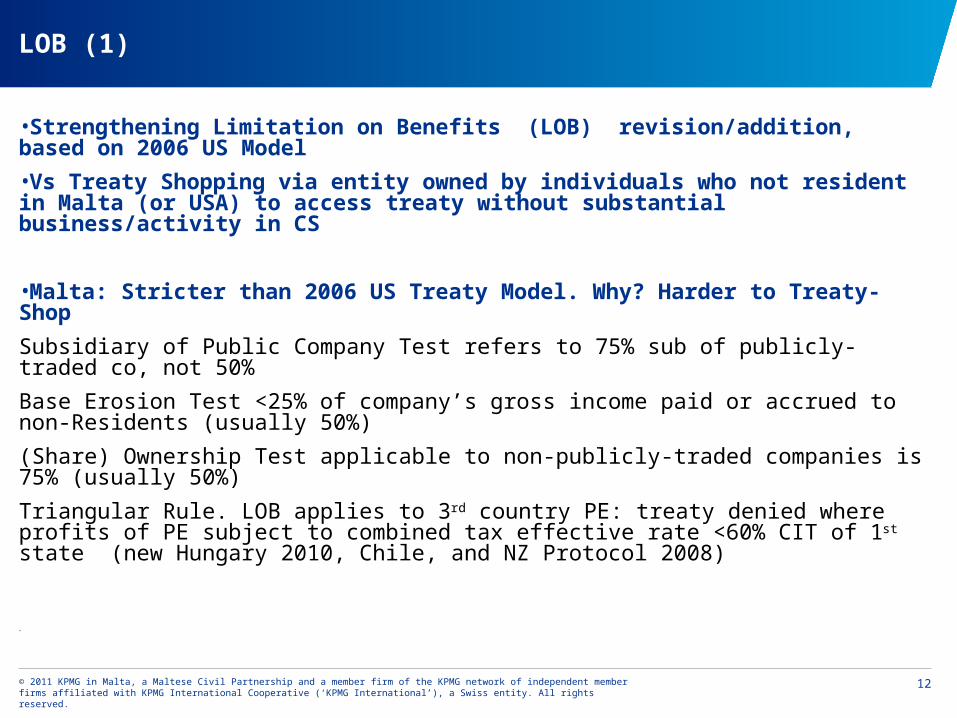

LOB (1)

•Strengthening Limitation on Benefits (LOB) revision/addition, based on 2006 US Model

•Vs Treaty Shopping via entity owned by individuals who not resident in Malta (or USA) to access treaty without substantial business/activity in CS

•Malta: Stricter than 2006 US Treaty Model. Why? Harder to Treaty-Shop

Subsidiary of Public Company Test refers to 75% sub of publicly-traded co, not 50%

Base Erosion Test <25% of company’s gross income paid or accrued to non-Residents (usually 50%)

(Share) Ownership Test applicable to non-publicly-traded companies is 75% (usually 50%)

Triangular Rule. LOB applies to 3rd country PE: treaty denied where profits of PE subject to combined tax effective rate <60% CIT of 1st state (new Hungary 2010, Chile, and NZ Protocol 2008)

•

Page 13

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

13

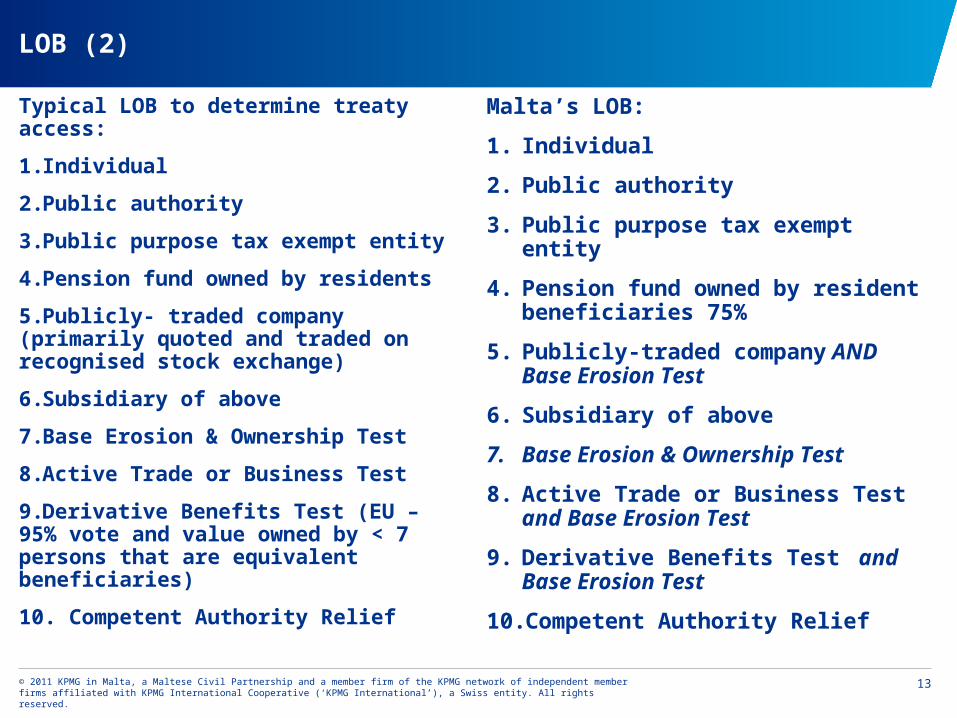

LOB (2)

Typical LOB to determine treaty access:

1.Individual

2.Public authority

3.Public purpose tax exempt entity

4.Pension fund owned by residents

5.Publicly- traded company (primarily quoted and traded on recognised stock exchange)

6.Subsidiary of above

7.Base Erosion & Ownership Test

8.Active Trade or Business Test

9.Derivative Benefits Test (EU – 95% vote and value owned by < 7 persons that are equivalent beneficiaries)

10. Competent Authority Relief

Malta’s LOB:

1. Individual

2. Public authority

3. Public purpose tax exempt entity

4. Pension fund owned by resident beneficiaries 75%

5. Publicly-traded company AND Base Erosion Test

6. Subsidiary of above

7. Base Erosion & Ownership Test

8. Active Trade or Business Test and Base Erosion Test

9. Derivative Benefits Test and Base Erosion Test

10. Competent Authority Relief

Page 14

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

14

Bottom-line

Treaty:

•MT – was only remaining EU MS without

•Status – shedding tax haven/offshore

•Certainty – coordinates and improves relief double taxation

Aims:

•Attract

• High-value added manufacturing

• Services, especially Financial Services

• ICT

•Facilitate mutual cross-border trade and investment.

Page 15

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

15

Thank you

Dr Juanita Brockdorff

Tax Partner

Tel. +356 2563 1148

Fax. + 356 2566 1000

Email. [email protected]

Page 16

© 2011 KPMG in Malta, a Maltese Civil Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

16

© 2011 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and ‘cutting through complexity’ are registered trademarks or trademarks of KPMG International Cooperative (KPMG International).