57

© 2012 Rockwell Publishing Financing Residential Real Estate Lesson 12: VA-Guaranteed Loans

© 2012 Rockwell Publishing

Financing Residential Real Estate

Lesson 12:

VA-Guaranteed Loans

© 2012 Rockwell Publishing

Introduction

This lesson will cover:characteristics of VA loanseligibility requirementsVA guarantyVA loan amountsunderwriting guidelines for VA loans

© 2012 Rockwell Publishing

Introduction

VA loan program was established to help veterans finance purchase of their homes.

Affordable loans.Advantages over conventional financing.

© 2012 Rockwell Publishing

Characteristics of VA Loans

VA-guaranteed loan: made by institutional lender, but portion of loan is guaranteed by Department of Veterans Affairs.

Protects lender against losses from default.

© 2012 Rockwell Publishing

Characteristics of VA Loans

VA loans may be used to finance purchase or construction of one- to four-unit residence.

Can’t be used for investor loans.Veteran must occupy home.

© 2012 Rockwell Publishing

Characteristics of VA Loans

No downpayment required (100% financing).

No maximum loan amount set by VA.No maximum income limits.Less stringent qualifying standards.Can be fixed-rate loan or ARM.No mortgage insurance required.No reserves after closing required.

© 2012 Rockwell Publishing

Characteristics of VA Loans

1% of amount financed to cover cost of making loan only; no other origination fees.

No prepayment penalties.Can be assumed by creditworthy buyer,

veteran or non-veteran.Forbearance for veterans in financial

crisis.

© 2012 Rockwell Publishing

Characteristics of VA Loans

Funding fee: amount borrowers must pay VA to defray administrative costs of loan program.

Instead of mortgage insurance premium.Percentage of loan amount.Paid at closing or financed with loan

amount.

Funding fee

© 2012 Rockwell Publishing

Characteristics of VA Loans

Regular military veteran: funding fee is 2.15% of loan amount, unless veteran makes downpayment of 5% of more:

Downpayment > 5% but < 10%: funding fee is 1.5%

Downpayment 10% or more, funding fee is 1.25%

Fees slightly higher for Reserves or National Guard members

Funding fee

© 2012 Rockwell Publishing

Characteristics of VA Loans

Some exempt from funding fee requirement.Veterans entitled to receive VA

compensation for service-related disabilities.

Surviving spouses of veterans who died in service or from service-related disabilities.

Funding fee

© 2012 Rockwell Publishing

Eligibility for VA Loans

Eligibility for VA loans based on length of active duty service in U.S. armed forces.

Minimum requirement: ranges from 90 days to 24 months depends on whether service was

during wartime or peacetime period Check with VA to determine eligibility.

© 2012 Rockwell Publishing

Eligibility for VA Loans

Veterans discharged for service-connected disability: no minimum active duty service.

Disabled veterans

© 2012 Rockwell Publishing

Eligibility for VA Loans

Dishonorable discharge will prevent eligibility.Veterans whose discharge was neither

honorable nor dishonorable are eligible.

Dishonorable discharge

© 2012 Rockwell Publishing

Eligibility for VA Loans

Reserves or National Guard for at least six years:

eligible for VA loanno minimum active duty service

requirement

Reserves or National Guard

© 2012 Rockwell Publishing

Eligibility for VA Loans

Certificate of Eligibility: issued by VA, used by veteran to apply for VA loan.

Veteran must submit most recent discharge/separation papers.

Lender can usually obtain certificate online.

Certificate of Eligibility

© 2012 Rockwell Publishing

Eligibility for VA Loans

Surviving spouse may be eligible if veteran:died on active dutydied of service-related injurieswas listed as missing in actionis prisoner of war

Eligibility of spouse

© 2012 Rockwell Publishing

SummaryCharacteristics and Eligibility

• VA-guaranteed loan

• Owner-occupancy requirement

• Forbearance

• Funding fee

• Minimum service requirement

• Certificate of Eligibility

© 2012 Rockwell Publishing

VA Guaranty

Essential feature of VA loans is that they’re guaranteed by U.S. government.

Significantly reduces lender’s risk of lossif borrower defaults.

© 2012 Rockwell Publishing

VA Guaranty

Guaranty amount: portion of loan covered by VA guaranty.

Guaranty amount for loan depends on:loan amountmaximum guaranty amount in county

where home is located

Guaranty amount

© 2012 Rockwell Publishing

VA Guaranty

Began in World War II: guaranty amount was $4,000.

Over the years: increased periodically to reflect increasing housing costs.

Eventually: guaranty varied with loan amount, up to a specified maximum.

Maximum guaranty amount

© 2012 Rockwell Publishing

Maximum Guaranty Amount

Now: VA maximum guaranty tied to conforming loan limits for conventional loans.

Increases automatically when conforming loan limits increase.

Amount may change each year—check with VA for most current figures.

Tied to conforming loan limits

© 2012 Rockwell Publishing

Maximum Guaranty Amount

Maximum VA guaranty in most areas:25% of Freddie Mac conforming loan limit

for one-unit residence

2011 Freddie Mac’s conforming loan limit for one-unit residence: $417,000.

So 2011 maximum VA guaranty amount in most areas is 25% of $417,000, or $104,250.

$417,000 x .25 = $104,250

Maximum in most areas

© 2012 Rockwell Publishing

VA Guaranty

Guaranty amount available in particular transaction depends on loan amount.

Guaranty based on loan amount

© 2012 Rockwell Publishing

VA Guaranty

Loan amount Guaranty amount

Up to $45,000: 50% of loan amount

$45,001–$56,250: $22,500

$56,251–$144,000: 40% of loan amount, up to $36,000

$144,001–$417,000: 25% of loan amount

Over $417,000: 25% of loan amount, up to county max.

Guaranty based on loan amount

© 2012 Rockwell Publishing

VA Guaranty

Entitlement: guaranty amount available for particular veteran to use.

Doesn’t expire.Available until used by veteran or

eligible surviving spouse.

Guaranty entitlement

© 2012 Rockwell Publishing

VA Guaranty

Restoration of entitlement:restored if veteran sells home and repays

loanavailable again for veteran to userestored if loan paid off when veteran

refinances restored entitlement applied to new

loan

Restoration of entitlement

© 2012 Rockwell Publishing

VA Guaranty

Paying off loan without selling home:can use restored entitlement to purchase

another homeonly allowed to do this oncemust occupy new home (owner-

occupancy requirement)

Restoration of entitlement

© 2012 Rockwell Publishing

VA Guaranty

VA guaranty doesn’t necessarily relieve borrower of personal liability for loan.

Veteran may be liable: after default after loan assumed (for older loans) to VA, to lender, or to both

Veteran’s liability

© 2012 Rockwell Publishing

Veteran’s Liability

Liability to VA:Veteran may have to reimburse VA for

default if foreclosure sale results in loss.For loan closed on or after January 1,

1990: veteran required to repay VA only if guilty of fraud, misrepresentation, or bad faith.

Liability after default

© 2012 Rockwell Publishing

Veteran’s Liability

When veteran is required to repay VA:amount owed is delinquent federal debtfederal income tax refunds can be applied

to itfederal pay can be garnishedveteran not eligible for any federal loans

until arrangements to repay are made

Liability after default

© 2012 Rockwell Publishing

Veteran’s Liability

Even when veteran not required to repay VA (no fraud or bad faith):

no restoration of entitlement unless veteran makes arrangements to repay

Liability after default

© 2012 Rockwell Publishing

Veteran’s Liability

Liability to lender:veteran may be liable for amount of

foreclosure not covered by guarantystate laws restricting deficiency

judgments still apply

Liability after default

© 2012 Rockwell Publishing

Veteran’s Liability

VA loan can be assumed by any creditworthy buyer.

May be veteran or non-veteran. Approval from VA or lender required:

if loan closed on or after March 1, 1988

to release original borrower from liability

Liability after assumption

© 2012 Rockwell Publishing

Veteran’s Liability

Approval and original borrower released from liability if:

buyer meets VA underwriting standardsloan is currentbuyer assumes all of original borrower’s

loan obligations

Liability after assumption

© 2012 Rockwell Publishing

Veteran’s LiabilityLiability after assumption

VA loan originated before March 1, 1988 can be assumed without consent of lender or VA.

Original borrower remains liable unless consent obtained.

© 2012 Rockwell Publishing

VA Guaranty

Veteran’s entitlement not automatically restored after assumption unless assumptor/buyer:

is eligible veteranhas entitlement equal to or greater than

loan’s guaranty amountagrees to substitute own entitlement for

original borrower’s substitution of entitlement requested

from VA

Substitution of entitlement

© 2012 Rockwell Publishing

VA Guaranty

For VA loan assumed by non-veteran: full entitlement can’t be restored.

Veteran may still have remaining entitlement. Also called partial entitlement.Can be used to obtain another VA loan.

Remaining entitlement

© 2012 Rockwell Publishing

VA Guaranty

New loan amount $144,000 or less:subtract entitlement used on old loan from

$36,000

New loan amount over $144,000:subtract entitlement used on old loan from

maximum guaranty amount in county most areas in 2011, usually $104,250

Remaining entitlement

© 2012 Rockwell Publishing

VA Guaranty

Example:Sales price for new home: $210,000Maximum guaranty in county: $104,250Entitlement used on old loan in 1996:

$50,750

$104,250 County maximum guaranty - 50,750 Previously used entitlement

$53,500 Remaining entitlement

Remaining entitlement

© 2012 Rockwell Publishing

VA Guaranty

Co-ownership:if both eligible veterans, maximum

guaranty is not increasedif veteran buys home with non-veteran

other than spouse, guaranty only covers veteran’s half of loan

Entitlement and co-ownership

© 2012 Rockwell Publishing

VA Guaranty

Refinancing with VA loan:VA, conventional, FHA, seller financingother liens such as tax or judgment liensfor non-VA loan, guaranty entitlement is

usedcash from proceeds allowedcannot exceed 100% of appraised valuenormal VA underwriting standards apply

Refinancing with VA loan

© 2012 Rockwell Publishing

VA Guaranty

Streamline refinancing: refinancing existing VA loan just to take advantage of lower interest rates, or replace ARM with fixed-rate loan.

Loan amount limited to old loan balance, closing costs, up to two discount points, funding fee, and cost of energy-efficient improvements.

Underwriting not required.

Refinancing with VA loan

© 2012 Rockwell Publishing

SummaryVA Guaranty

• Guaranty amount

• Maximum guaranty amount

• Entitlement

• Restoration of entitlement

• Remaining entitlement

• Substitution of entitlement

• Refinancing

• Streamline refinancing

© 2012 Rockwell Publishing

VA Loan Amounts

VA doesn’t set maximum loan amount. Loan can’t exceed appraised value of

property.VA-approved appraiser appraises

property, VA issues Notice of Value (NOV).

Sales price exceeds appraised value: borrower must make up difference out of own funds.

Loan amount can’t exceed value

© 2012 Rockwell Publishing

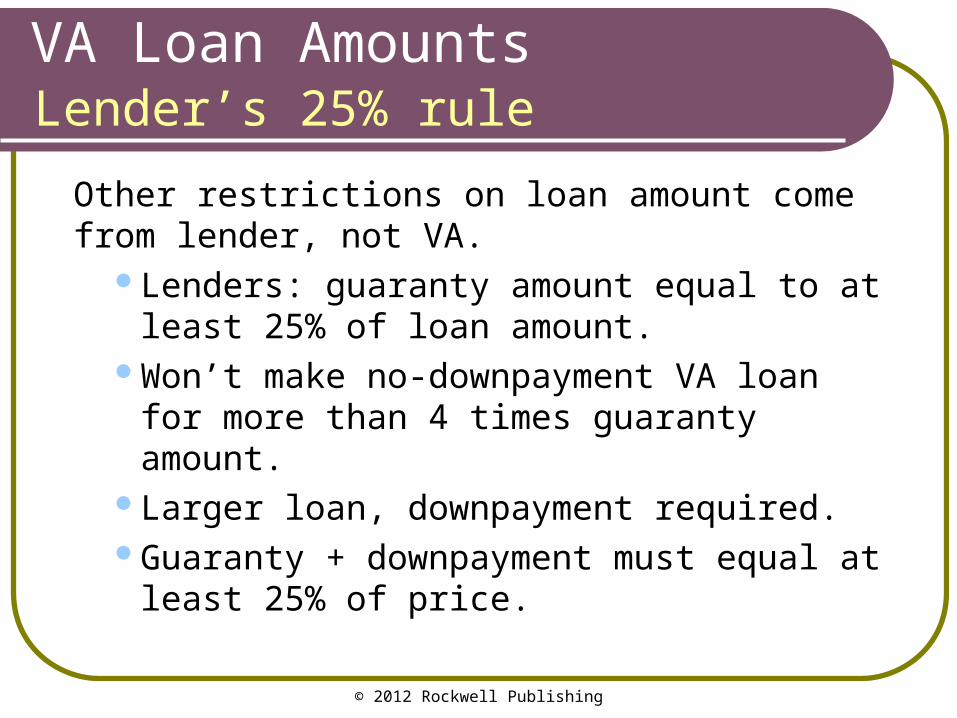

VA Loan Amounts

Other restrictions on loan amount come from lender, not VA.

Lenders: guaranty amount equal to at least 25% of loan amount.

Won’t make no-downpayment VA loan for more than 4 times guaranty amount.

Larger loan, downpayment required.Guaranty + downpayment must equal at

least 25% of price.

Lender’s 25% rule

© 2012 Rockwell Publishing

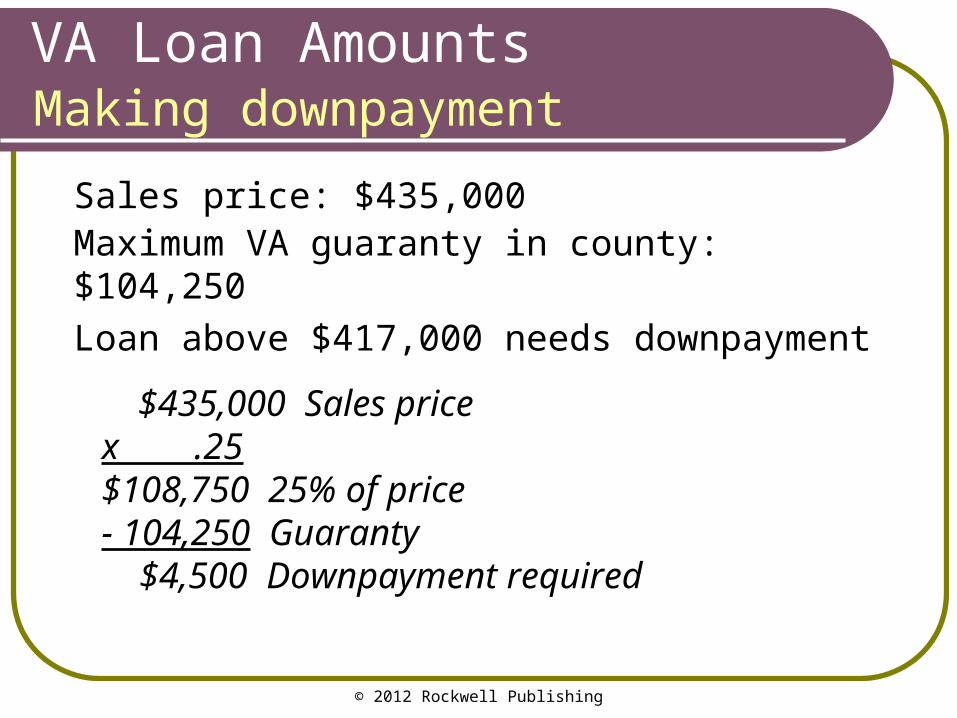

VA Loan Amounts

Sales price: $435,000Maximum VA guaranty in county: $104,250

Loan above $417,000 needs downpayment

$435,000 Sales price x .25 $108,750 25% of price - 104,250 Guaranty $4,500 Downpayment required

Making downpayment

© 2012 Rockwell Publishing

VA Loan Amounts

Example, cont’d:

$435,000 Sales price - 4,500 Downpayment $430,500 Loan amount

Making downpayment

© 2012 Rockwell Publishing

VA Loan Amounts

Veteran can finance part or all of downpayment required by lender if:

combined loans don’t exceed NOVbuyer qualifies for combined paymentssecond loan is assumable by

creditworthy buyer

Secondary financing

© 2012 Rockwell Publishing

Underwriting Guidelines

Two methods of income analysis for VA loans:

income ratio methodresidual income method

© 2012 Rockwell Publishing

Underwriting Guidelines

VA uses debt to income ratio to analyze income of loan applicant.

Ratio generally shouldn’t exceed 41% unless there are compensating factors.

Debts with more than 10 payments left are counted as recurring obligations.

Income ratio analysis

© 2012 Rockwell Publishing

Underwriting Guidelines

Residual income analysis: second method used to qualify loan applicant (also called cash flow analysis).

Gross monthly income− Taxes, recurring obligations, housing expense

Residual income

Residual income analysis

© 2012 Rockwell Publishing

Underwriting Guidelines

Vet’s residual income should be at least one dollar more than VA’s minimum requirement.

Minimum requirement varies according to:region of the countryfamily sizesize of proposed loan

Residual income analysis

© 2012 Rockwell Publishing

Underwriting Guidelines

VA underwriting standards are merely guidelines, not hard and fast rules.

Compensating factors may allow loan approval in spite of weaknesses in application.

Compensating factors must be relevant to weaknesses.

Compensating factors

© 2012 Rockwell Publishing

Underwriting Guidelines

Possible compensating factors:excellent long-term credit historyconservative use of consumer creditminimal consumer debtlong-term employmentsignificant liquid assetssizable downpaymentlittle or no increase in housing expensemilitary benefits

Compensating factors

© 2012 Rockwell Publishing

Underwriting Guidelines

Possible compensating factors, continued:satisfactory previous experience with home

ownershiphigh residual incomelow debt to income ratiotax credits for child caretax benefits of home ownershipsignificant equity in property (for

refinancing)

Compensating factors

© 2012 Rockwell Publishing

Underwriting Guidelines

Special rules for approving applicant whose income ratio is over 41%.

Ordinarily: lender must submit detailed statement to VA, listing compensating factors.

If residual income exceeds minimum by 20% or more: loan can be approved with income ratio over 41% without any compensating factors.

Income ratio exceptions

© 2012 Rockwell Publishing

SummaryLoan Amounts and Underwriting

• Notice of Value

• Downpayment

• Secondary financing

• Income ratio analysis

• Residual income analysis

• Compensating factors