30

ffirst.indd 4 11/18/2011 1:34:38 PM

Handbook of BudgetingSixth Edition

WILLIAM R. LALLI

Editor

John Wiley & Sons, Inc.

ffirst.indd 1 11/18/2011 1:34:37 PM

Copyright © 2012 by John Wiley & Sons, Inc. All rights reserved.

The fifth edition of this book, titled Handbook of Budgeting, was published in 2003.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.Published simultaneously in Canada.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without either the prior written permission of the Publisher, or authorization through payment of the appropriate per-copy fee to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, (978) 750-8400, fax (978) 646-8600, or on the web at www.copyright.com. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748-6011, fax (201) 748-6008, or online at www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in preparing this book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this book and specifically disclaim any implied warranties of merchantability or fitness for a particular purpose. No warranty may be created or extended by sales representatives or written sales materials. The advice and strategies contained herein may not be suitable for your situation. You should consult with a professional where appropriate. Neither the publisher nor author shall be liable for any loss of profit or any other commercial damages, including but not limited to special, incidental, consequential, or other damages.

For general information on our other products and services or for technical support, please contact our Customer Care Department within the United States at (800) 762-2974, outside the United States at (317) 572-3993 or fax (317) 572-4002.

Wiley also publishes its books in a variety of electronic formats. Some content that appears in print may not be available in electronic books. For more information about Wiley products, visit our web site at www.wiley.com.

Library of Congress Cataloging-in-Publication Data:

Handbook of budgeting / [edited by] William R. Lalli. — 6th ed. p. cm. Includes index. ISBN 978-0-470-92045-9 (cloth); ISBN 978-1-118-17059-5 (ebk); ISBN 978-1-118-17060-1 (ebk); ISBN 978-1-118-17061-8 (ebk) 1. Budget in business. I. Lalli, William Rea. HG4028.B8H36 2012 658.15′4—dc23 2011029142

Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

ffirst.indd 2 11/18/2011 1:34:37 PM

Founded in 1807, John Wiley & Sons is the oldest independent publishing company in the United States. With offices in North America, Europe, Asia, and Australia, Wiley is globally committed to developing and marketing print and electronic products and services for our customers’ professional and personal knowledge and understanding.

The Wiley Corporate F&A series provides information, tools, and insights to corpo-rate professionals responsible for issues affecting the profitability of their company, from accounting and finance to internal controls and performance management.

ffirst.indd 3 11/18/2011 1:34:38 PM

ffirst.indd 4 11/18/2011 1:34:38 PM

v

Contents

Foreword xv

Preface xvii

PART ONE: INTRODUCTION TO THE BUDGETING PROCESS

Chapter 1: Integrating The Balanced Scorecard for Improved Planning and Performance Management 3

Overview 3Elements of a Balanced Scorecard 5Use of Strategy Maps 11Scorecard Cascading 12Bringing It All Together 13Integrating the Scorecard with Planning and Performance 14Balanced Scorecard and Annual Planning 15Continuous Strategic Management with the Scorecard 22Summary 24

Chapter 2: Strategic Balanced Scorecard–Based Budgeting and Performance Management 25

Introduction: Why Most Companies Fail to Implement Their Strategies 25Why a few Companies Produce Exceptional Results 26Measure your Strategy with Balanced Scorecard 34Balanced Scorecard-Based Budgets 37Performance Management 38Summary 39

Chapter 3: Budgeting and the Strategic Planning Process 41

Defi nition of Strategic Planning 41Planning Cycle 42Strategic Planning Process: A Dynamic Cycle 44Situation Analysis 46Business Direction/Concept 58Alternative Approaches 61Operational Plan 62

ftoc.indd 5 11/18/2011 1:38:14 PM

vi n Contents

Measurement 66Feedback 66Contingency Planning 68Problems in Implementing Formal Strategic Planning Systems 69Summary 70

Chapter 4: Budgeting and Forecasting: Process Tweak or Process Overhaul? 71

Introduction 71Survey Methodology 72Findings: Budgeting Process 72Findings: Forecasting Process 86Report Summary 89Developing a Road Map for Change 90

Chapter 5: The Budget: An Integral Element of Internal Control 93

Introduction 93The Control Environment 94Planning Systems 96Reporting Systems 98Summary 102

Chapter 6: Relationship Between Strategic Planning and the Budgeting Process 103

Introduction 103How to Plan 103The Audience for Whom the Plan Is Designed 104Strategic Business Planning and Its Role in Budgeting 105Planning Differences among Small, Medium, and Large Organizations 106Components of Strategic Planning 107Management and Organization 108Market Analysis 110Formulation of Marketing Strategies 111Operations Analysis 112Summary 114

Chapter 7: The Essentials of Business Valuation 115

Introduction 115Understanding the Valuation Assignment 117Research and Information Gathering 120Adjusting and Analyzing the Financial Statements 123Three Approaches to Valuing a Business 125Income Approach 125Market Approach 132Asset Approach 135Making Adjustments to Value 136

ftoc.indd 6 11/18/2011 1:38:14 PM

Contents n vii

Reaching the Valuation Conclusion 141

Chapter 8: Moving Beyond Budgeting: Integrating Continuous Planning and Adaptive Control 145

Introduction 145Annual Budgeting Trap 146Why Some Organizations Are Going Beyond Budgeting 147Beyond Budgeting: Enabling a More Adaptive Performance

Management Process 148Climbing the Twin Peaks of Beyond Budgeting 152Beyond Budgeting: Enabling Radical Decentralization 153

Chapter 9: Moving Beyond Budgeting: An Update 161

Introduction 161Beyond Budgeting Round Table (BBRT) 162Guardian Industries Corporation 163

PART TWO: TOOLS AND TECHNIQUES

Chapter 10: Implementing Forecasting Best Practices 169

Introduction 169Budgeting versus Forecasting 170Implementing Forecasting Best Practices 170Forecasting Best Practices: Process 171Forecasting Best Practices: Organization 174Forecasting Best Practices: Technology 176Conclusion 178

Chapter 11: Calculations and Modeling in Budgeting Software 181

Introduction 181Why Companies Use Budgeting Software 181Calculations in Accounting Systems and Spreadsheets 183Budgeting Software 184OLAP Databases 186Modeling and Budgeting 188Processes 189More Complex Budgeting Calculations 190Conclusion 192

Chapter 12: Cost-Accounting Systems: Integration with Manufacturing Budgeting 193

Introduction 193Decision Factors in the Selection Process 194Cost-Accounting System Options 195Costs Associated with a Product 195Labor Cost 196

ftoc.indd 7 11/18/2011 1:38:14 PM

viii n Contents

Variable Costing and Budgeting 197Full Costing and Budgeting 217Cost-Accumulation Procedures 219Valuation: Actual versus Standard 221Actual Costing 223Actual Costing, Budgeting, and Cost Control 226Standard Costing 226Variance Reporting 231Variances and Budgeting 236Manufacturing Overhead 236Manufacturing Overhead, Budgeting, and Cost Control 247

Chapter 13: Break-Even and Contribution Analysis as a Tool in Budgeting 249

Introduction 249Break-Even Analysis 249Price/Volume Chart 254Contribution Analysis 255Cost–Volume–Price and the Budgeting Process 261

Chapter 14: Profitability and the Cost of Capital 263

Introduction 263A Market Gauge for Performance 265Coping with the Cost of Equity 266Building Company-Wide Profit Goals 268Building Divisional Profit Goals 270Information Problems and Cost of Capital 276Summary 276

Chapter 15: Budgeting Shareholder Value 279

Introduction 279Long-Term Valuation 281Economic Value Added 285Complementary Measures of Valuation 290Budgeting Shareholder Value 293Summary 296

Chapter 16: Applying the Budget System 297

Introduction 297Initial Budget Department Review of Divisional Budget Packages 299Divisional Review Meetings 302Budget Consolidation and Analysis 303Preliminary Senior Management Review 303Final Revision of Operating Group Plans 304Second Budget Staff Review of Operating Group Plans 304Revised Consolidated Budget Preparations 305

ftoc.indd 8 11/18/2011 1:38:14 PM

Contents n ix

Final Senior Management Budget Review Sessions 305Operating Groups’ Monthly Submissions 306Effective Use of Graphics 306Summary 306

Chapter 17: Budgets and Performance Compensation 307

Introduction 307Measures of Executive Performance 308Structuring Reward Opportunities 316Pitfalls of Linking Incentives to Budgets 317An Optimal Approach 320Adjusting Operating Unit Targets 324Budgets and Long-Term Incentive Plans 326Summary 328

Chapter 18: Predictive Costing, Predictive Accounting 329

Internet Forces the Need for Better Cost Forecasting 329Traditional Budgeting: An Unreliable Compass 330Activity-Based Costing as a Foundation for Activity-Based Planning

and Budgeting 331Budgeting: User Discontent and Rebellion 331Weary Annual Budget Parade 333ABC/M as a Solution for Activity-Based Planning and Budgeting 334Activity-Based Cost Estimating 335Activity-Based Planning and Budgeting Solution 336Early Views of Activity-Based Planning and Budgeting Were

Too Simplistic 337Important Role of Resource Capacity Causes New Thinking 337Major Clue: Capacity Exists Only as a Resource 339Measuring and Using Cost Data 340Usefulness of Historical Financial Data 341Where Does Activity-Based Planning and Budgeting Fit In? 344Activity-Based Planning and Budgeting Solution 345Risk Conditions for Forecasting Expenses and Calculated Costs 350Framework to Compare and Contrast Expense-Estimating Methods 352Economics 101? 355

Chapter 19: Cost Behavior and the Relationship to the Budgeting Process 357

Introduction 357Cost Behavior 357Break-Even Analysis 360Additional Cost Concepts 365Differential Cost Concepts 368Maximizing Resources 370Estimating Costs 373Summary 375

ftoc.indd 9 11/18/2011 1:38:14 PM

x n Contents

PART THREE: PREPARATION OF SPECIFIC BUDGETS

Chapter 20: Sales and Marketing Budget 379

Introduction 379Overview of the Budget Process 379Special Budgeting Problems 384Pertinent Tools 389Unique Aspects of Some Industries 392Summary 394

Chapter 21: Manufacturing Budget 395

IIntroduction 395Concepts 400Changing to a Cost-Management System 402Problems in Preparing the Manufacturing Budget 407Three Solutions 410Technique 410Determining Production Requirements 411Step 1: Developing the Plannable Core 413Step 2: Obtaining Sales History and Forecast 413Step 3: Scheduling New and Revised Product Appearance 415Step 4: Determining Required Inventory Levels 416Step 5: Establishing Real Demonstrated Shop Capacity 418Step 6: Publishing the Master Schedule 424A Total Quality Program—The Other Alternative 425Inventory and Replenishment 431More on the Manufacturing Budget 434Determining Raw-Material Requirements 434Determining Other Indirect-Material Costs 436Determining Direct-Labor Costs 437Establishing the Manufacturing Overhead Functions and Services 440Quality Control Economics Review Questions 447Plant Engineering Buildings and Equipment Maintenance

Review Questions 449Floor and Work-in-Process Control Review Questions 450Summary 451

Chapter 22: Research and Development Budget 455

Relationship of Research and Development and Engineering to the Total Budgeting Process 455

Problems in Establishing Research and Development and Engineering Objectives 459

Developing a Technological Budget 465Preparing a Departmental Budget 481Managing a Budget 484Coordinating Project Budgets 490

ftoc.indd 10 11/18/2011 1:38:14 PM

Contents n xi

Chapter 23: Administrative-Expense Budget 493

Introduction 493Role and Scope of the Administrative-Expense Budget 493Methods Used for Preparing the Administrative-Expense Budget 498Factors that Impact the Administrative-Expense Budget 502Unique Issues Impacting the Administrative-Expense Budget 503Tools and Techniques for Managing the Administrative-Expense Budget 504Summary 506

Chapter 24: Budgeting the Purchasing Department and the Purchasing Process 507

Description and Definition of the Process Approach 507Role of Process Measures 512Process Measures 513Creating the Procurement Process Budget 517

Chapter 25: Capital Investment Review: Toward a New Process 519

Introduction 519Context of the Revised Capital-Investment

Review Process 520Benchmarking Capital-Investment Review Best Practices 523Revised Capital-Investment Review Process: Overview 527Implementation: What Bonneville Learned in the First Three Years 541Summary 544

Chapter 26: Leasing 545

Introduction 545Overview of the Leasing Process 546Possible Advantages of Leasing 549Possible Disadvantages of Leasing 550Types of Lease Sources 550Lease Reporting 552Lease versus Purchase Analysis 560Financial Accounting Standards Board Rule 13 Case Illustration 564Negotiation of Leases 565Selecting a Lessor 566Lease-Analysis Techniques 566Lease Form 572Summary 579

Chapter 27: Balance-Sheet Budget 581

Introduction 581Purpose of the Balance-Sheet Budget 582Definition 582Responsibility for the Budget 583Types of Financial Budgets 587

ftoc.indd 11 11/18/2011 1:38:14 PM

xii n Contents

Preparing Financial Budgets 588Preparing the Balance-Sheet Budget 591Adequate Cash 620Financial Ratios 620Analyzing Changes in the Balance Sheet 628

Chapter 28: Budgeting Property and Liability Insurance Requirements 635

Introduction 635Role Risk Management Plays in the Budgeting Process 637Types of Insurance Mechanisms 638Role of Insurance/Risk Consultants 639Use of Agents/Brokers 639Self-Insurance Alternatives 640Identifying the Need for Insurance 643Key Insurance Coverages 645Identifying Your Own Risks 650How to Budget for Casualty Premiums 653Summary 656

PART FOUR: BUDGETING APPLICATIONS

Chapter 29: Budgeting: Key to Corporate Performance Management 659

Future of Budgeting 659Adding Value to the Organization 660Corporate Performance Management 661Developing a Budget Process Focused on Implementation of Strategy 662Role of Technology 666Overcoming Organizational Resistance 669Planning and Controlling Implementation of a New System 670Conclusion 675

Chapter 30: Zero-Based Budgeting 677

Introduction 677Problems with Traditional Techniques 678Zero-Based Approach 679Zero-Based Budgeting Procedures 680Decision Package 681Ranking Process 687Completing the Profi t and Loss 689Preparing Detailed Budgets 692Summary 695

Chapter 31: Bracket Budgeting 697

Introduction 697Application of Bracket Budgeting 698

ftoc.indd 12 11/18/2011 1:38:14 PM

Contents n xiii

Premises to Profi ts? 699Developing a Tactical Budgeting Model 700Bracket Budgeting in Annual Planning 719Consolidating Income Statements 720Summary of Benefi ts 720Summary 722

Chapter 32: Program Budgeting: Planning, Programming, Budgeting 723

Introduction 723Description of Program Budgeting 724History 728Framework of Program Budgeting 734Program Structuring 747Types of Analysis 751Installation Considerations 759Summary 763

Chapter 33: Activity-Based Budgeting 767

Introduction 767Traditional Budgeting Does Not Support Excellence 768Activity-Based Budgeting Defi nitions 771Activity-Based Budgeting Process 774Linking Strategy and Budgeting 775Translate Strategy to Activities 780Determine Workload 781Create Planning Guidelines 783Identify Interdepartmental Projects 783Improvement Process 787Finalizing the Budget 787Performance Reporting 788Summary 790

PART FIVE: INDUSTRY BUDGETS

Chapter 34: Budgeting For Corporate Taxes 793

Introduction 793Taxation of C Corporations 794Personal Holding Company Tax 799Net Operating Loss Utilization 799Charitable Contributions 800Taxation Budget 802Federal Corporate Tax 803Purposes 804Tax Return 804

ftoc.indd 13 11/18/2011 1:38:14 PM

xiv n Contents

Chapter 35: Budgeting in the Global Internet Communication Technology Industry 805

Overview 805Essentials from Earlier Chapters 806Freemium Strategies 808Volunteer Services 809Enterprise Risk Management 811

About the Editor 813

About the Contributors 815

Index 825

ftoc.indd 14 11/18/2011 1:38:14 PM

xv

Foreword

The idea of budgeting often brings fear, even loathing, to the minds of most persons. Perhaps that is because many of us were fi rst introduced to the term by trying to fi gure out how to spend our seemingly unfairly small “allowances” as children. It was not easy to fi gure out how much candy we could buy and still go to the movies on the weekend. These days our children buy more movies (and video games) than they attend, but the principles (and the sweets) are the same.

In its simplest sense, budgeting is any plan, usually expressed in fi nancial or math-ematical terms. As an expression of expectations, a budget generally aligns resources with needs to accomplish a specifi c goal. As mileposts and measuring sticks, budgets provide invaluable benchmarks that can be used every day in reacting to management challenges.

Some see budgets as a necessary evil, but in reality they are underrated tools that can greatly enhance any business process.

The greatest value of budgets—arming management with key decision-making tools—is often overlooked. To the uninitiated, a budget succeeds or fails based on how close actual results compare to expectations. While it is great fun to predict the future accurately, to win a bet as they say, life’s best lessons are often learned in analyzing why you were wrong.

In reality, analyzing the reasons actual results differ from expected results is a far more useful tool than the often disappointing attempt to accurately predict the future. This cannot be done effectively without a budget to compare things to. Like the weather, fi nancial futures are diffi cult to predict and sometimes correlate only with predictions as result of an accident, good luck or otherwise. Were these assumptions wrong? Were needs incorrectly calculated? Did the business environment change? Did the world change? Was a better method or process discovered? Were there unan-ticipated challenges? By studying what is different and the reasons for differences, we can continually improve both performance and our ability to predict the future. We have certainly come a long way in improving our ability to predict the weather, but expectations for accuracy have also increased. Similarly, the art and science of budget-ing has advanced dramatically over the years since the handbook was fi rst published. Revisions in this edition refl ect alterations and improvements comparing these budgets to older ones.

flast.indd 15 11/18/2011 7:47:46 PM

Budgets are clearly not just for children to manage their allowances and meager earnings. They are not just for big businesses either, as some would incorrectly perceive. Budgets are for everyone.

In modern times, budgets are often (unfortunately) utilized only by midsize busi-nesses when they are in trouble. They would likely be in trouble less frequently if they used budgets more often. Certainly there is less superficial need to manage resources when revenues seem to flow effortlessly well beyond the costs needed to sustain a busi-ness. The lack of need in these cases is invariably only superficial; easy money is a fleet-ing concept. Darwinian pressures on business provide survival only to the fittest and most prepared.

As can be learned by studying the various budgets in this book, time, money, and processes can be budgeted. Planning for the future enhances our understanding of the present. Budgets reduce the chances of repetition of past errors, and while nothing can prevent the commission of new errors or the introduction of new challenges, effective budgeting can lead to the preparedness necessary to deal with adversity and opportu-nity when either is on your doorstep.

This handbook is a resource that will help you identify the right type of budget to use and which tools to implement in actually completing the budget and provide insight into analyzing your budget against actual expectations.

David A. Lifson, CPACrowe Horwath LLP

David Lifson, CPA, is a partner with Crowe Horwath LLP and leads the New York City tax and business consultancy practice, where he develops business strategies and personal financial plans utilizing both his and the firm’s broad range of accounting, audit, tax, and business consulting backgrounds, both domestically and internationally. He specializes in advis-ing clients on managing various types of business change within tax, economic, and other related constraints and dealing with the tax compliance challenges that accompany

change. This includes starting or closing a business; buying, merging, or selling one; or trying to change or value an existing operation.

Mr. Lifson is the recipient of the American Institute of CPAs 2009 Arthur J. Dixon Memorial Award, the accounting profession’s highest award in the area of taxation. He has chaired the Tax Executive Committee, served as a member of the AICPA Board of Directors and on its council, and has chaired or served on various committees, task forces, and technical resource panels over the years. He is also a former president of the New York State Society of CPAs and has served in various capacities on its behalf. Mr Lifson has chaired the Small Business and Self Employed subgroup of the Internal Rev-enue Service’s Advisory Council (IRSAC) while serving on the council. IRSAC meets regularly to advise the Commissioner of the IRS and key IRS group leaders on how to administer the tax system effectively.

xvi n Foreword

flast.indd 16 11/18/2011 7:47:46 PM

xvii

Preface

THE NEED TO IMPROVE YOUR BUDGETING PROCESSES

Despite advances in technology and fi nance, we have not reached the limit of knowl-edge or made the most advanced achievements in reaching our fi nancial goals. That is a defi nition of a frontier that we face in these times.

There are many types of budgeting, and most of them are covered in this book. The need for sound, dependable information as the basis for quality decision making based on reliable budgets, I contend, has never been stronger. That is the reason I proposed revising this book to present this sixth edition of the Handbook of Budgeting.

I could report on the state of the economy and economic trends, citing a variety of sources and experts; however, my only point is that in bad times more than in good times, budgeting can be key to an entity’s survival or prosperity.

This book is intended as a business tool. I shall leave it to the academicians to ana-lyze what might work better. Instead, our authors present 35 chapters of tried-and-true experiences taken from frontline business exposure that will enlighten you as to how you may incorporate real changes in your environment.

I became the second editor of this book after its founding editor died. One reason I was selected to replace him was due to the extensive work I was doing at the time in the budgeting area for delivering continuing professional education to senior fi nancial executives. One day at a conference, an attendee approached me, realized I was the book editor, and paid me the highest compliment I ever received. She told me that she worked with a copy of the book open on her desk.

There is no outer limit in any fi eld of endeavor, especially one in which the oppor-tunities for research and development have not been exploited. This is the new frontier that must be met with technology and information management in fi nance in modern times which companies must master in order to survive and prosper. Use every tool at your disposal.

THE FORECAST ON BUDGETING

The Handbook of Budgeting has been revised in this sixth edition to retain some “ever-green” knowledge from previous contributors, augmented by new experts on new topics.

fpref.indd 17 11/18/2011 7:47:58 PM

More contributions from corporate perspectives translate into more opportunities for you to take this information to your team and to implement the lessons this book contains company-wide.

Chief financial officers, chief information officers, chief operating officers; vice presidents of fnance; controllers and assistant controllers; directors and managers of budgeting, forecasting, financial planning, analysis, business planning, strategic plan-ning, performance measurement, and finance; financial consultants; budget analysts; and financial analysts will all find that this book has been designed with their specific needs in mind.

Our contributors and I believe that budgeting is the most important component of an overall dynamic business planning process. When it is combined with available technology, you may quickly analyze its impact on your business, which will lead you to more effective decisions that improve the profitability of your company.

Please note that the term “budgeting” is used in its broadest context and includes the major process components of strategic planning, target setting, operational plan-ning, financial planning, reporting, and forecasting.

According to research referred to in the pages of this book, forward-looking com-panies spend significantly more time (44 percent of the total time spent in planning) on forecasting and action-planning activities that can actually improve business perfor-mance. They also focus on what is important by implementing best practices through-out the planning process.

You will also find information in the Handbook of Budgeting on the latest business-planning software that allows you to develop budgets quickly by employing Web-based technology to process information over the Internet. Companies that use the latest tech-nology can also quickly assess the impact to their bottom line based on competition, eco-nomic slowdowns, and consumer behavior. Always remember that the consequences of inadequate action planning and forecasting can be severe when a company’s perfor-mance fails to meet Wall Street expectations.

It is the intention of John Wiley & Sons, Inc., that the Handbook of Budgeting will help you to meet the challenges of this new frontier.

William Rea Lalli, EditorJanuary 2012

xviii n Preface

fpref.indd 18 11/18/2011 7:47:58 PM

IPART ONE

introduction to the budgeting Process

ChAPtER 1 integrating the balanced Scorecard for improved Planning and Performance Management 3

ChAPtER 2 Strategic balanced Scorecard–based budgeting and Performance Management 25

ChAPtER 3 budgeting and the Strategic Planning Process 41

ChAPtER 4 budgeting and Forecasting: Process or Process Overhaul? 71

ChAPtER 5 the budget: An integral Element of internal Control 93

ChAPtER 6 the Relationship between Strategic Planning and the budgeting Process 103

ChAPtER 7 the Essentials of business Valuation 115

ChAPtER 8 Moving beyond budgeting: integrating Continuous Planning and Adaptive Control 145

ChAPtER 9 Moving beyond budgeting: An Update 161

ch01.indd 1 11/10/2011 12:19:36 PM

ch01.indd 2 11/10/2011 12:19:36 PM

3

1CHAPTER ONE

integrating the balanced Scorecard for improved Planning and Performance Management

Antosh G. NirmulBalanced Scorecard Collaborative, Inc.

OVERViEW

The balanced scorecard is a management tool developed by Drs. Robert Kaplan and David Norton in the early 1990s. Since that time, the scorecard has become a standard management practice adopted by large and small organizations throughout the world. The balanced scorecard is based on the simple premise that people and organizations respond and perform based on what is measured. Often this is described as “People respond to what is inspected, not expected.” Measurement becomes a language that communicates clear priorities to the organization.

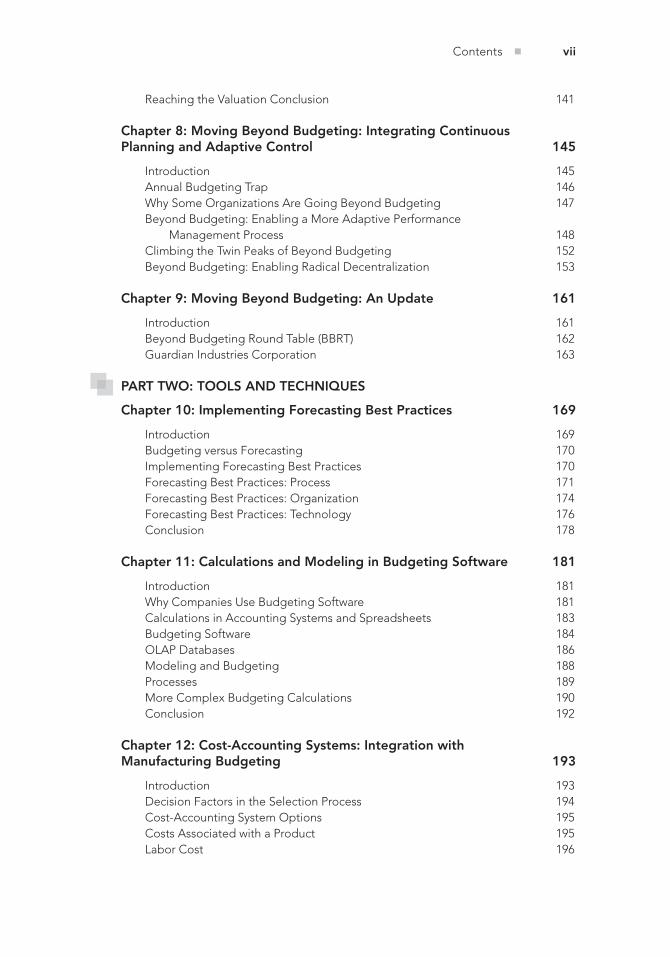

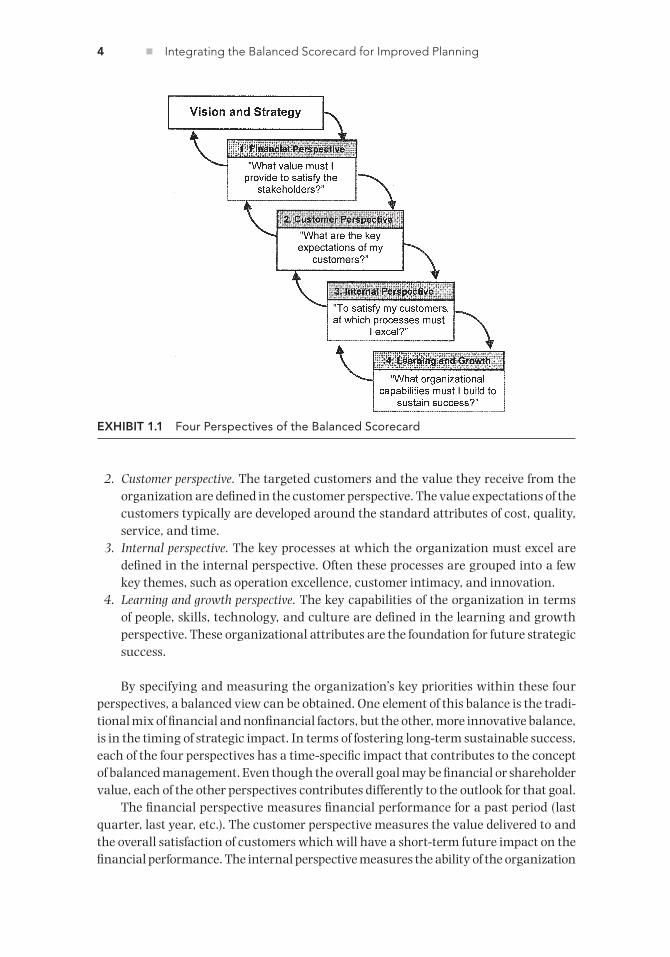

Because the primary goal of any organization (commercial, governmental, or non-profi t) is to create value for its stakeholders and because the strategy is the way the orga-nization intends to create value, the measurement system should be closely linked to the strategy. The balanced scorecard provides a measurement system that translates the strategy into operational terms through a series of causal relationships defi ned around four key perspectives (see Exhibit 1.1):

1. Financial perspective. For commercial organizations, the fi nancial perspective defi nes the value created for the shareholders. For noncommercial organizations, the expectations of the fi nancial stakeholders are defi ned.

ch01.indd 3 11/10/2011 12:19:36 PM

4 n Integrating the Balanced Scorecard for Improved Planning

2. Customer perspective. The targeted customers and the value they receive from the organization are defined in the customer perspective. The value expectations of the customers typically are developed around the standard attributes of cost, quality, service, and time.

3. Internal perspective. The key processes at which the organization must excel are defined in the internal perspective. Often these processes are grouped into a few key themes, such as operation excellence, customer intimacy, and innovation.

4. Learning and growth perspective. The key capabilities of the organization in terms of people, skills, technology, and culture are defined in the learning and growth perspective. These organizational attributes are the foundation for future strategic success.

By specifying and measuring the organization’s key priorities within these four perspectives, a balanced view can be obtained. One element of this balance is the tradi-tional mix of financial and nonfinancial factors, but the other, more innovative balance, is in the timing of strategic impact. In terms of fostering long-term sustainable success, each of the four perspectives has a time-specific impact that contributes to the concept of balanced management. Even though the overall goal may be financial or shareholder value, each of the other perspectives contributes differently to the outlook for that goal.

The financial perspective measures financial performance for a past period (last quarter, last year, etc.). The customer perspective measures the value delivered to and the overall satisfaction of customers which will have a short-term future impact on the financial performance. The internal perspective measures the ability of the organization

Exhibit 1.1 Four Perspectives of the Balanced Scorecard

ch01.indd 4 11/10/2011 12:19:38 PM

Elements of a Balanced Scorecard n 5Elements of a Balanced Scorecard n 5

to execute its processes that will have a short-term future impact on customer value and a medium-term impact on fi nancial performance. The learning and growth perspective measures the development of organizational capabilities that will have a short-term impact on operational execution, a medium-term impact on customer satisfaction, and a long-term impact on fi nancial performance.

By analyzing and measuring the strategy across all four perspectives, organizations achieve balance between the leading and lagging indicators of performance as well as between fi nancial and nonfi nancial factors. The combination of these multiple dimen-sions of balance allows a more holistic understanding of the organization’s strategic execution and ultimate strategic success. Management should be able to use the score-card results to obtain a snapshot of the current performance and a forecast of future strategic performance for the organization. This snapshot should highlight any key issues and be a valuable tool in steering the business through the allocation of resources and prioritization of strategic initiatives.

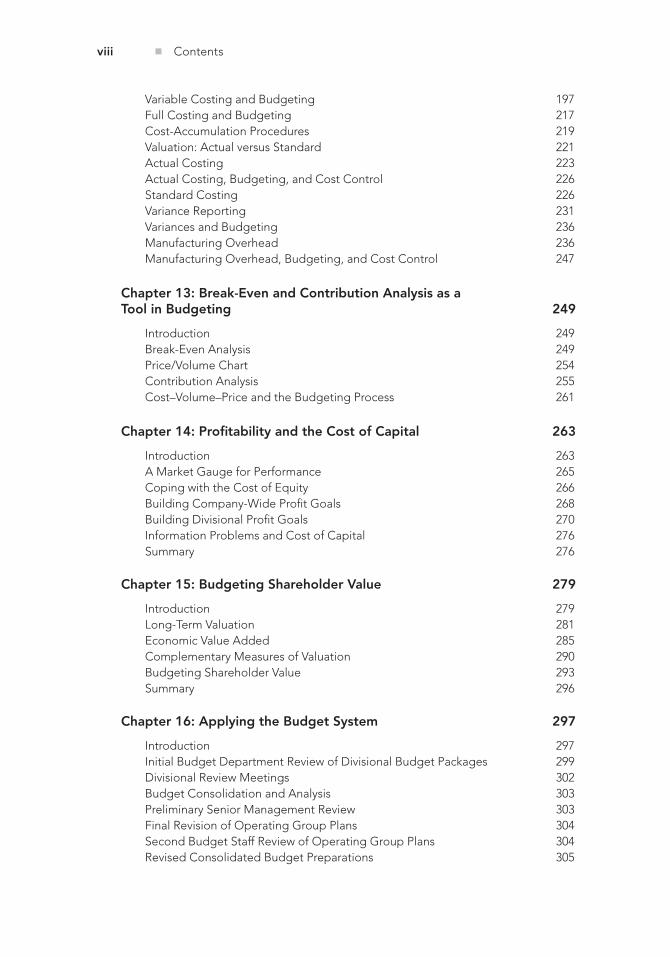

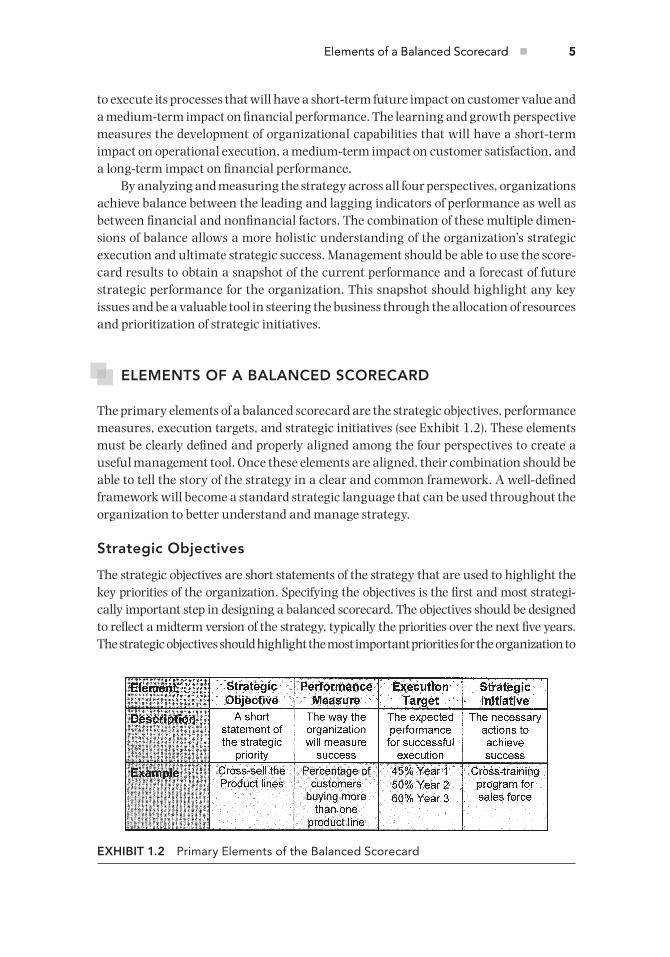

ELEMENtS OF A bALANCED SCORECARD

The primary elements of a balanced scorecard are the strategic objectives, performance measures, execution targets, and strategic initiatives (see Exhibit 1.2). These elements must be clearly defi ned and properly aligned among the four perspectives to create a useful management tool. Once these elements are aligned, their combination should be able to tell the story of the strategy in a clear and common framework. A well-defi ned framework will become a standard strategic language that can be used throughout the organization to better understand and manage strategy.

Strategic Objectives

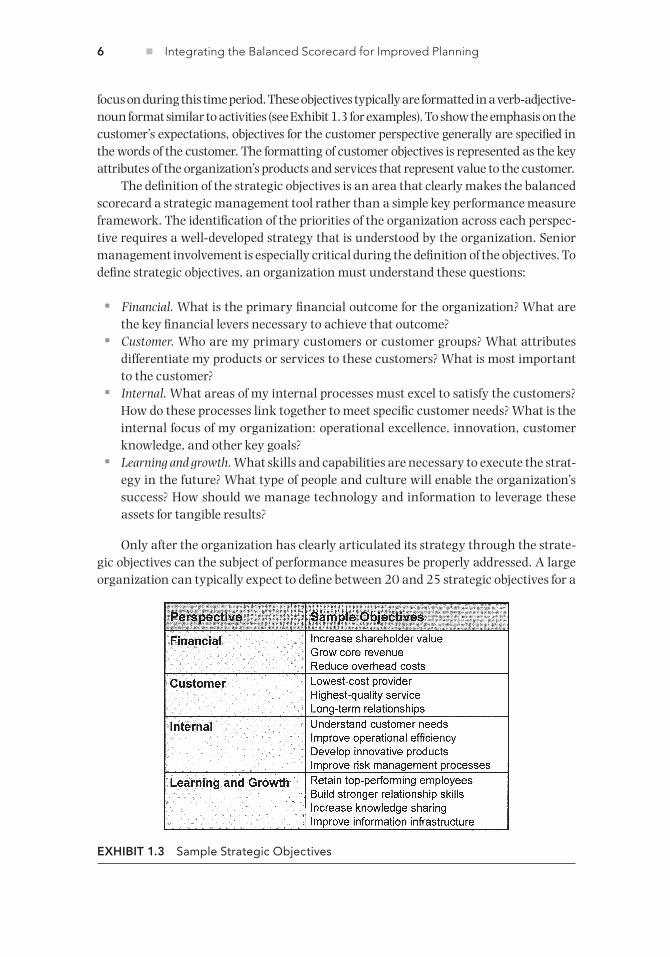

The strategic objectives are short statements of the strategy that are used to highlight the key priorities of the organization. Specifying the objectives is the fi rst and most strategi-cally important step in designing a balanced scorecard. The objectives should be designed to refl ect a midterm version of the strategy, typically the priorities over the next fi ve years. The strategic objectives should highlight the most important priorities for the organization to

Exhibit 1.2 Primary Elements of the Balanced Scorecard

ch01.indd 5 11/10/2011 12:19:39 PM

6 n Integrating the Balanced Scorecard for Improved Planning

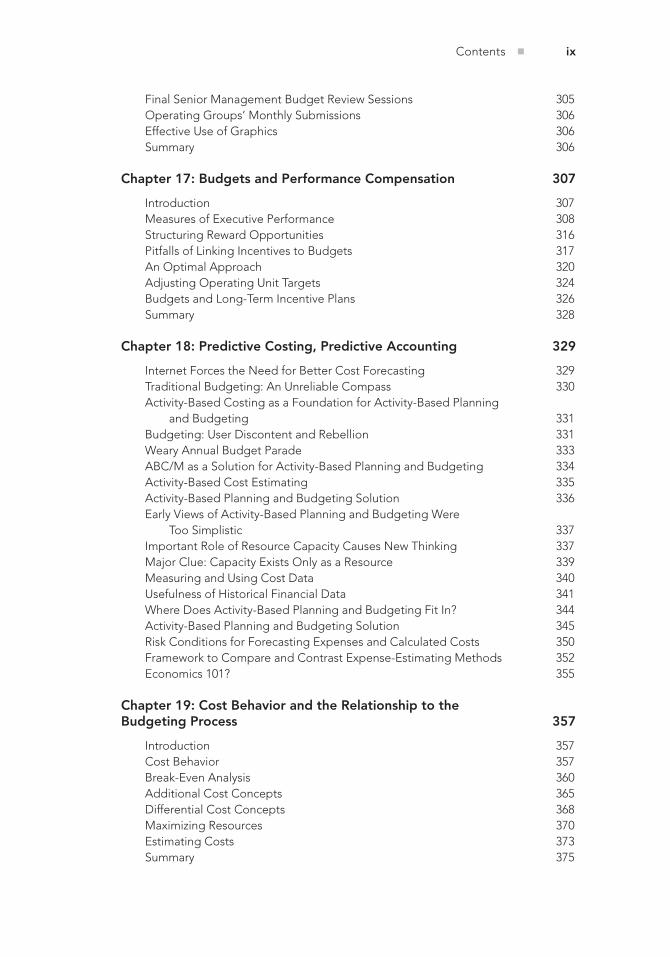

focus on during this time period. These objectives typically are formatted in a verb-adjective-noun format similar to activities (see Exhibit 1.3 for examples). To show the emphasis on the customer’s expectations, objectives for the customer perspective generally are specified in the words of the customer. The formatting of customer objectives is represented as the key attributes of the organization’s products and services that represent value to the customer.

The definition of the strategic objectives is an area that clearly makes the balanced scorecard a strategic management tool rather than a simple key performance measure framework. The identification of the priorities of the organization across each perspec-tive requires a well-developed strategy that is understood by the organization. Senior management involvement is especially critical during the definition of the objectives. To define strategic objectives, an organization must understand these questions:

▪ Financial. What is the primary financial outcome for the organization? What are the key financial levers necessary to achieve that outcome?

▪ Customer. Who are my primary customers or customer groups? What attributes differentiate my products or services to these customers? What is most important to the customer?

▪ Internal. What areas of my internal processes must excel to satisfy the customers? How do these processes link together to meet specific customer needs? What is the internal focus of my organization: operational excellence, innovation, customer knowledge, and other key goals?

▪ Learning and growth. What skills and capabilities are necessary to execute the strat-egy in the future? What type of people and culture will enable the organization’s success? How should we manage technology and information to leverage these assets for tangible results?

Only after the organization has clearly articulated its strategy through the strate-gic objectives can the subject of performance measures be properly addressed. A large organization can typically expect to define between 20 and 25 strategic objectives for a

Exhibit 1.3 Sample Strategic Objectives

ch01.indd 6 11/10/2011 12:19:40 PM

Elements of a Balanced Scorecard n 7

clearly articulated strategy. More than 25 objectives would indicate a lack of clear priori-ties for the organization. Fewer objectives can be sufficient if they are defined specifically enough to communicate the strategy effectively.

The definition of the strategic objectives should highlight areas of inconsistency in the strategy. An organization cannot seek to be all things to all customers. The strategic objective process is designed to highlight the most important outcomes that define value for the shareholders and customers as well as the few key processes and organizational attributes that contribute most to that value. The objectives will not cover every activ-ity performed by the organization but should highlight those that will be most critical over the strategic horizon.

Performance Measures

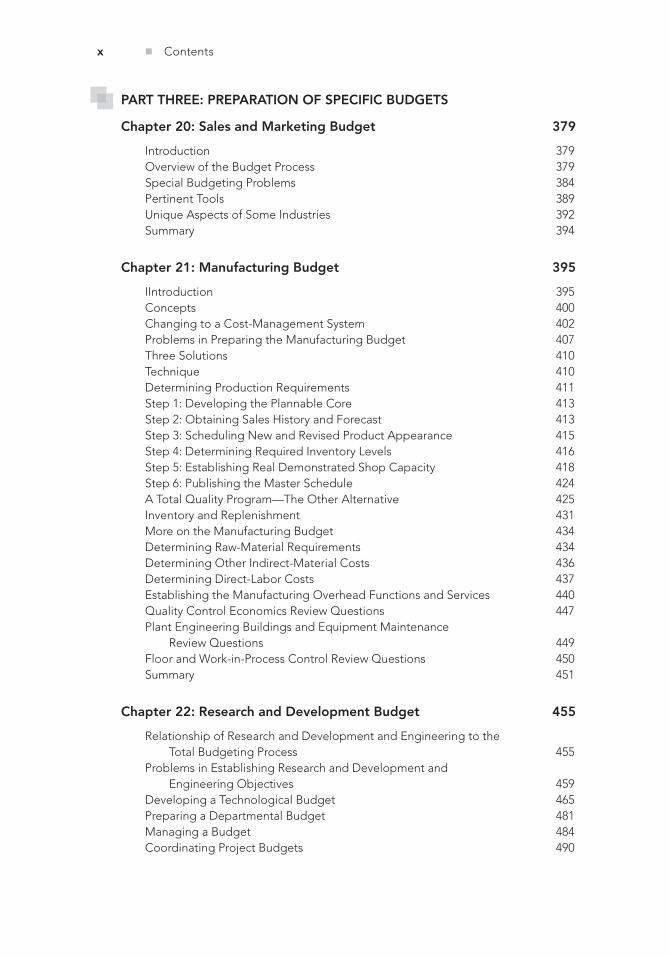

As a measurement framework, the balanced scorecard often is judged by the quality of the performance measures. Performance measures serve to further clarify the priori-ties of an organization by directly identifying the most important priorities for strategic execution. The performance measures identify how the organization will judge success. Most organizations already have some type of indicators defined throughout the various levels of the business. The issue in defining the scorecard is to identify the most impor-tant measures that will reflect the execution of the strategy.

The performance measures on a balanced scorecard often are compared to the dash-board on an automobile. While the driver of the car looks at only a few key metrics (speed, fuel level, etc.), the car itself monitors hundreds of other pieces of information. In our case, the executives of the organization use the scorecard as the key performance information they need to monitor and steer the business while other more operational metrics are looked at within the business. The other operational metrics can be brought forward to the executives only when there is an unusual problem. Major changes (intended or not) in performance and execution should be visible through the scorecard measures.

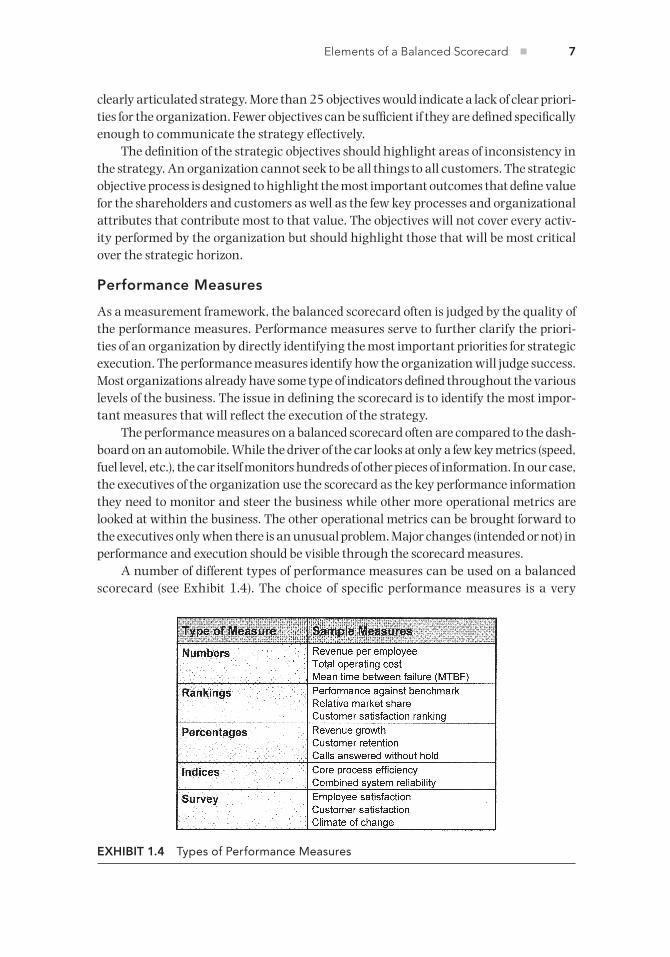

A number of different types of performance measures can be used on a balanced scorecard (see Exhibit 1.4). The choice of specific performance measures is a very

Exhibit 1.4 Types of Performance Measures

ch01.indd 7 11/10/2011 12:19:41 PM

8 n Integrating the Balanced Scorecard for Improved Planning

individual decision for the organization. There is no template set of scorecard measures that will be appropriate for any strategy. There are, however, a few guidelines that can assist an organization in choosing appropriate measures:

▪ Choose at least one measure for each strategic objective. Total measures should be around 25 for a large organization.

▪ Choose quantitative rather than subjective measures where possible.

The goal of these guidelines is to create the most useful set of measures possible. The existence of any strategic objective that cannot be described by a measure should call into question the validity of that strategy. Experience with senior management has shown that using more than 25 indicators makes it very difficult for executives to understand and focus on the results. The clearest measures are those that result in a specific and understandable number (e.g., dollars, number of employees, etc.). Gener-ally, more subjective measures, such as indices and survey results, are more difficult to measure, communicate, and understand. While it is impossible to create a scorecard with only objective measures, the balance should be toward more numerical and less subjective indicators.

Another key factor to consider when choosing measures is the frequency of data reporting. The organization cannot expect to have executive discussions on scorecard results each quarter if its data are available only on an annual basis. The choice of measures should correspond to the frequency of desired reporting. Most organizations review their scorecard performance and strategic focus on a quarterly basis. In this case, at least 75 percent of an organization’s scorecard measures should be available at that frequency.

Execution targets

The setting and communication of targets are key steps necessary to operationalize a scorecard. While the measures communicate where management focus will be, the targets communicate the expected level of performance. For example, a measure such as customer retention shows a strategic focus: The difference between a 90 percent target and a 60 percent target represents a major shift in strategy. The setting of appropriate targets can be a difficult and painful process.

An important distinction in setting targets is the difference between standard per-formance targets and “stretch” targets. Stretch targets typically are used in areas of new or enhanced strategic focus and are meant to move the organization in new directions. Typically these targets are multiyear in nature, and their implementation approach is not fully defined when they are initially set. For an established organization, a target such as doubling revenue in three years would require significant changes. Often the precise steps needed to reach that target are not yet defined. The use of a stretch target forces innovation and change in an organization.

Obviously, an organization cannot set 25 stretch targets and hope to achieve all of them. Most execution targets will be more traditional incremental advances that reflect successful execution of the strategy. The choice of where to use stretch versus

ch01.indd 8 11/10/2011 12:19:41 PM

Elements of a Balanced Scorecard n 9

incremental targets strongly defines the emphasis in the strategy. Stretch targets create inspirational goals for the organization; incremental targets supplement those goals with core areas that need continual focus for sustained success.

The key point in choosing appropriate execution targets, whether stretch or incre-mental, is evaluating the capabilities of an organization and its resources. Incremental targets should be clearly reachable given the available resources and capabilities. The setting of unreasonable targets undermines employee faith and accountability in the performance management process. While the achievement of stretch targets may not be easily envisioned initially, the targets should come into clearer focus as the time period for the stretch goals is crossed. Every stretch target should have a measurable time period attached and should be updated throughout that time frame. Typically, stretch targets would be set at a maximum of 20 percent of the total measures and with 80 percent of targets remaining as incremental improvements.

Strategic initiatives

Strategic initiatives are actions or projects that represent the primary path through which organizations create new skills, capabilities, or infrastructure to achieve strategic goals. In this definition, strategic initiatives are different from projects or actions that simply create incremental improvement over or maintain the existing skills, capabili-ties, or infrastructure of an organization. For example, in a financial organization, a project to build a new online ability to process self-service customer transactions could be a strategic initiative while a project to improve the interface of existing online tools or extend the online services would be considered an incremental upgrade of existing capabilities.

The criteria that an organization uses to define which actions are considered stra-tegic versus basic projects are unique to its strategy and circumstances. Typically, a strategic initiative has a certain strategic importance, size, and breadth of influence that makes it more than an operational project (see Exhibit 1.5). The goal in identifying actions that are strategic initiatives versus operational projects or activities is to be able to allocate resources in a more strategic manner using the scorecard and strategy. This distinction is explored further in the separation of operational versus strategic budgets when the scorecard is integrated into the planning process.

Exhibit 1.5 Key Criteria that Separate Strategic Initiatives

ch01.indd 9 11/10/2011 12:19:42 PM

10 n Integrating the Balanced Scorecard for Improved Planning

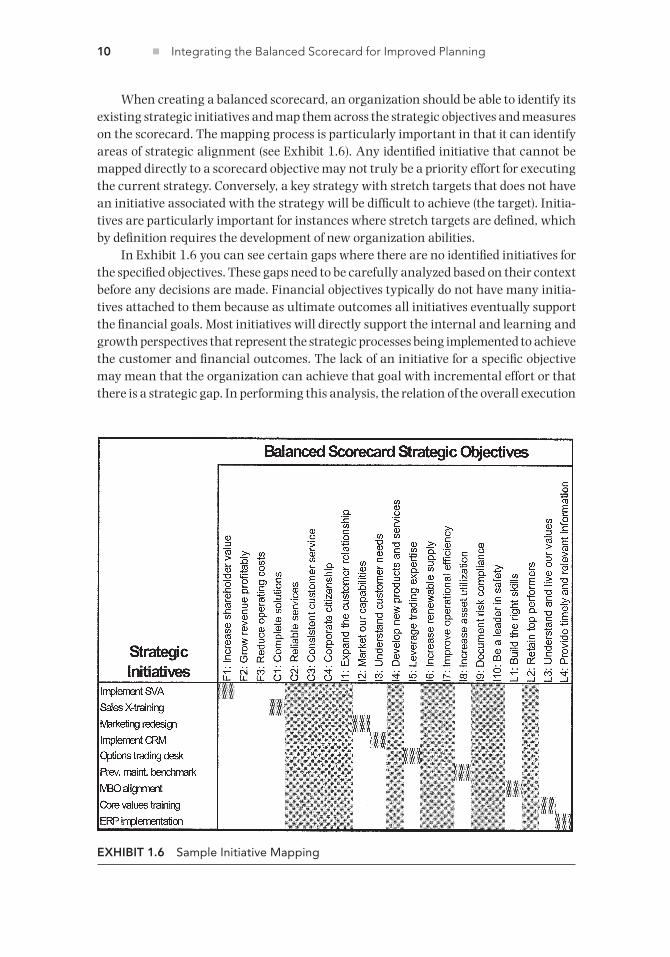

When creating a balanced scorecard, an organization should be able to identify its existing strategic initiatives and map them across the strategic objectives and measures on the scorecard. The mapping process is particularly important in that it can identify areas of strategic alignment (see Exhibit 1.6). Any identified initiative that cannot be mapped directly to a scorecard objective may not truly be a priority effort for executing the current strategy. Conversely, a key strategy with stretch targets that does not have an initiative associated with the strategy will be difficult to achieve (the target). Initia-tives are particularly important for instances where stretch targets are defined, which by definition requires the development of new organization abilities.

In Exhibit 1.6 you can see certain gaps where there are no identified initiatives for the specified objectives. These gaps need to be carefully analyzed based on their context before any decisions are made. Financial objectives typically do not have many initia-tives attached to them because as ultimate outcomes all initiatives eventually support the financial goals. Most initiatives will directly support the internal and learning and growth perspectives that represent the strategic processes being implemented to achieve the customer and financial outcomes. The lack of an initiative for a specific objective may mean that the organization can achieve that goal with incremental effort or that there is a strategic gap. In performing this analysis, the relation of the overall execution

Exhibit 1.6 Sample Initiative Mapping

ch01.indd 10 11/10/2011 12:19:44 PM