36

Alexandria, 18th of March 2019 Alessandro Panaro Head of Maritime Dept. SRM Intesa Sanpaolo Banking Group The new maritime phenomena

Alexandria, 18th of March 2019

Alessandro Panaro Head of Maritime Dept. SRM

Intesa Sanpaolo Banking Group

The new maritime phenomena

www.srm-maritimeconomy.com

The main phenomena that will shape the future of the maritime sector

The Mediterranean Economic Scenario and competitiveness indicators

The growing role of Mediterranean

The most important data on the shipping sector in the Med

Source: SRM on Eurostat, Suez Canal Authority, ISTAT, Port Authorities

25% WORLD’S

CONTAINER LINER SERVICES

20% GLOBAL SHIPPING TRAFFIC

19 PORTS THROUGHPUT >1 MLN TEUs

83% SHARE OF SEA TRADE ITALY-MED

+500% OF CONTAINER

TRAFFIC SINCE 1995

611 mln tonnes SHORT SEA SHIPPING

983 mln tonnes SUEZ CARGO

TRAFFIC

4% annual growth 10,7 bn tons Global volumes gathered momentum

and reached Fastest growth in five years

Containerized trade accounted for

17.1% of total seaborne trade

+6.4%

Major dry bulk commodities accounted for

29.9% of total seaborne trade

+5.1%

Crude oil shipments rose by

2.4% down from

4% in 2016

Combined volumes of refined petroleum products and gas went up by

3.9%

World Seaborne Trade in 2017

Source: SRM on UNCTAD, 2018

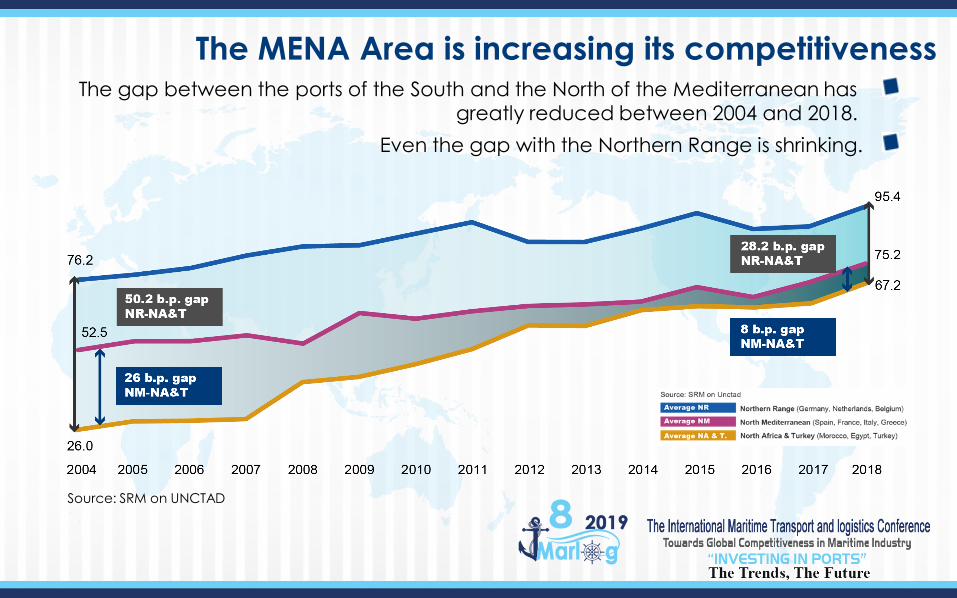

The MENA Area is increasing its competitiveness The gap between the ports of the South and the North of the Mediterranean has

greatly reduced between 2004 and 2018. Even the gap with the Northern Range is shrinking.

Source: SRM on UNCTAD

Liner Shipping Connectivity Index (LSCI): analysis of the MENA Area

Source: SRM on UNCTAD

Egypt gained 30 b.p. in the span analysed (2004-2018)

2004 2010 2015 2018

1° Egypt 42.9 UAE 63.4 UAE 70.4 UAE 83.91 2° UAE 38.1 Saudi Arabia 50.4 Morocco 68.3 Morocco 71.5

3° Saudi Arabia 35.8 Morocco 49.4 Saudi

Arabia 64.8 Egypt 70.28

4° Turkey 25.6 Oman 48.5 Egypt 61.5 Saudi Arabia 66.62

5° Oman 23.3 Egypt 47.6 Turkey 52 Oman 62.97

Logistic Performance Index

4,2 4,05 4,04 4,03 4,03 4,02 4,00 3,99 3,99 3,97

3,74

2016 2018

26th 19th

Italy Ranks 19th

China hold the 26th place in the world

Source: SRM on World Bank

3,61

In this scenario logistic efficiency and connectivity are the new challenges in international maritime competitiveness

The top 5 countries of the world in terms of

shipping competitiveness are in ASIA

Source: SRM on Unctad and World Bank

The top 4 countries of the world in terms of Logistic connectivity

are in EUROPE

Source: SRM on Unctad and World Bank

In this scenario logistic efficiency and connectivity are the new challenges in international maritime competitiveness

The top 5 countries of the world in terms of

shipping competitiveness are in ASIA

46%

8% 12%

8%

8%

6% 7%

2% 3% Northern Range

40%

South Med 9%

West Med 13%

Italy 6%

East Med 13%

Black Sea 6%

UK 7%

Atlantic 3%

Baltic Sea 3%

2008

2017

The analysis of container ports by geographic area: the new role of Med

Northern Range market share (40%) is decreased between 2008 and 2017.

The MED Area can be a great opportunity; between 2008 and 2017 the ports of MED Area increased their market share from 36% to 41%.

Market Share - TEU

MED AREA IS

GROWING

NORTHERN RANGE IS

SLOWING DOWN

Source: SRM on Port Authorities

Suez Canal: the new records

container ships 4,724

oil tankers

+2.5%

+4.1% 18,174 Ships

983,4 million tonnes of goods

+3.6%

+8.2%

+4.2%

491 mln tonn 235.5

mln tonn

+7%

5,706

Source: SRM on Suez Canal Authority, 2019

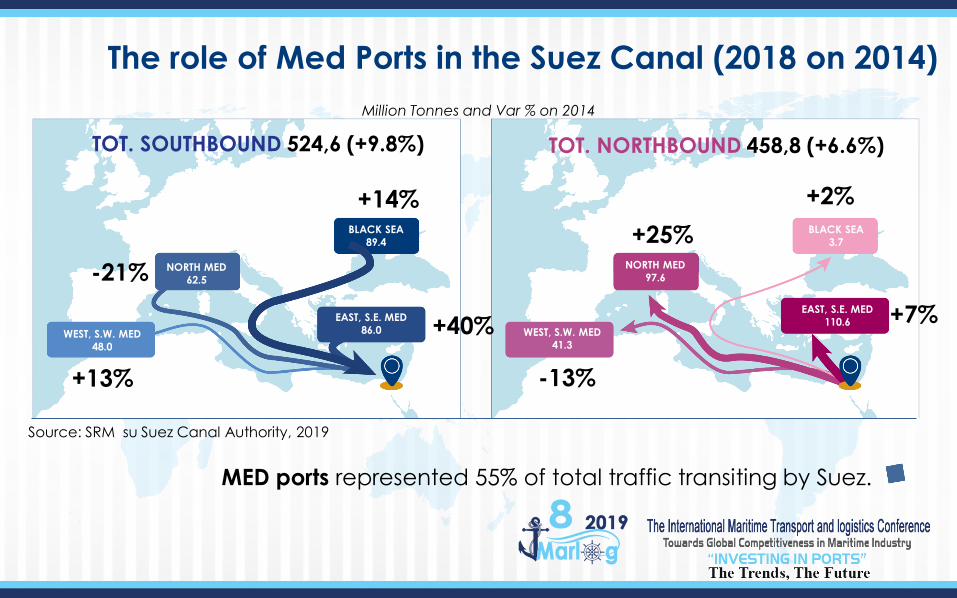

WEST, S.W. MED 48.0

EAST, S.E. MED 86.0

NORTH MED 62.5

BLACK SEA 89.4

WEST, S.W. MED 41.3

EAST, S.E. MED 110.6

BLACK SEA 3.7

NORTH MED 97.6

TOT. SOUTHBOUND 524,6 (+9.8%) TOT. NORTHBOUND 458,8 (+6.6%)

The role of Med Ports in the Suez Canal (2018 on 2014)

MED ports represented 55% of total traffic transiting by Suez.

Source: SRM su Suez Canal Authority, 2019

+40%

-21%

+14%

+13%

+7%

+25%

-13%

+2%

Million Tonnes and Var % on 2014

Suez (and the Sumed pipeline) is the 3rd busiest transit chokepoint in the world with a total oil flow (crude oil and refined products) of 5.5 million b/d transited in both

directions

It holds 9% of global seaborne oil trade and

9% of LNG

Mains oil global chokepoints

Source: SRM on U.S. Energy Information Administration (EIA)

Petroleum transit volumes through select maritime routes|2016 - Million barrels per day

…the naval gigantism…

Source: ITF (2015)

The ship size increased 7 times in a period of 40 years

133 new ships of the 10-23,000 TEUS category will be launched by 2022

(45 of which in the 18-23,000 TEUS)

Growth of Containership size, period 1970-2017

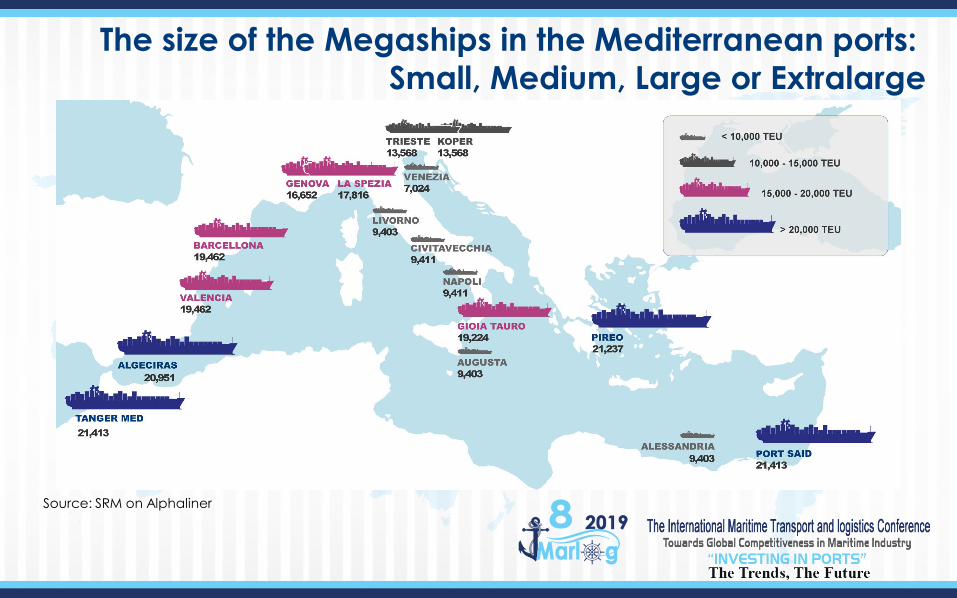

The size of the Megaships in the Mediterranean ports: Small, Medium, Large or Extralarge

Source: SRM on Alphaliner

MSC 30%

MAERSK 16% CMA CGM

11%

COSCO 7% EVERGREEN

1%

YM 2%

NYC 2%

AL 2%

ZIM 1%

MOL 1%

OTHERS 27%

Carriers' fleet market share in the Med Ports Total TEUs - 2018

In 2018, the market share of the container fleet

managed by 2M was 46%. The market share held by

Ocean Alliance was almost 20%

Source: SRM on Alphaliner

2012 2017

2017 2012

The Mediterranean routes of the Ocean Alliance

2012 2017

2017 2012

+27 OCEAN

ALLIANCE Traffic

+10 COSCO

Presence

2017

The Mediterranean routes of the Ocean Alliance

The Short Sea Shipping map

42

72

74 60 123

84

60 50 56

51

46

41 52

43

Source: SRM on Eurostat

542 46

70 450

261

611

131

From - To Cargo Transited (Million tons)

Main Short Sea Shipping

Corridor

Cargo Carried (Million tons)

* CEU (car equivalent unit) * Source: SRM on WWL, BRS Group, ANFIA, Fearnleys

The connection between the growth of Ro-Ro and the increase of the automotive

Ro-Ro traffic in the Mediterranean Sea-density map

2012-2017 comparison

Source: SRM

Arab Middle East and

North Africa 6%

East Asia 51%

Europe 10%

North America

1%

Sub-Saharan Africa

3%

West Asia 29%

$146 bn

INVESTMENT VALUE BY GEOGRAPHIC AREA

The role of BRI in the Mediterranean

Source: SRM on China Global Investment Tracker database Investment until June 2018

No financial investment

40.6

87.2 99.6

19.1

269.4

319.0

71.4

167.8 185.8

36.2

103.1 108.8

0

50

100

150

200

250

300

350

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

*

2019

*

2020

*

Italy China USA Germany

$ bn

Italy

Germany USA

China

A steady increase in trade relation towards the MENA area China is the largest partner

Source: SRM on UNCTAD

Italy’s trade with MENA Area: $87 bn (+70.4% on 2001). According to SRM forecast, this

trade will reach

$99.6 bn in 2020

China is the largest trade partner of MENA countries

$269.4 bn import-export

VALENCIA PIRAEUS

Source: SRM

The Chinese chessboard

VALENCIA PIRAEUS

ROTTERDAM

ABU DHABI

AMBARLI

SUEZ CANAL ASHDOD

HAIFA

MARSEILLE

MALTA

ANTWERP

ZEEBRUGGE

HAMBURG

BILBAO

Source: SRM

The Chinese chessboard

Total traffic of Cosco Container terminal is increasing in the Med

Source: SRM on COSCO

In 2018 total traffic of Cosco container terminal in the Med ports was almost 12 million TEUs.

Chinese terminals dominate 22% of the traffic in the Med ports.

Cosco Cargo in Med terminal 2018

Terminal Throughput (TEU ‘000)

Piraeus 4,409.2

Noatum 3,622.2

Suez Canal 1,258.3

Kumport 1,258.3

Vado Reefer 66.6

22% of Med ports

Total throughput Med Ports 11,966,100

The growth of the free zones in the world

1975 1986 1997 2002 2006 2014

79 176

845

3,000 3,500 4,500

N F

ree

Zone

s In

n. C

ount

ries

in 25 in 47

in 93

in 116 in 130

in 135

There are about 4,500 Free zones all over the world. These zones have created 68 million direct jobs and over $ 500 billion of direct

trade-related value added.

Source: SRM on Trade Performance Of Free Trade Zones, 2014 and others

Italian Free Zones: SEZ basic criteria

Source: SRM

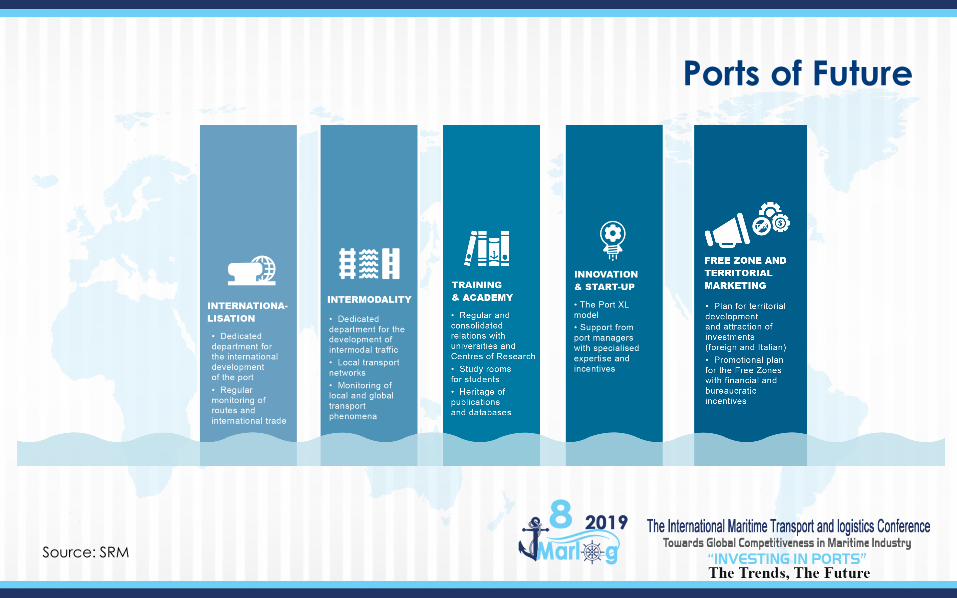

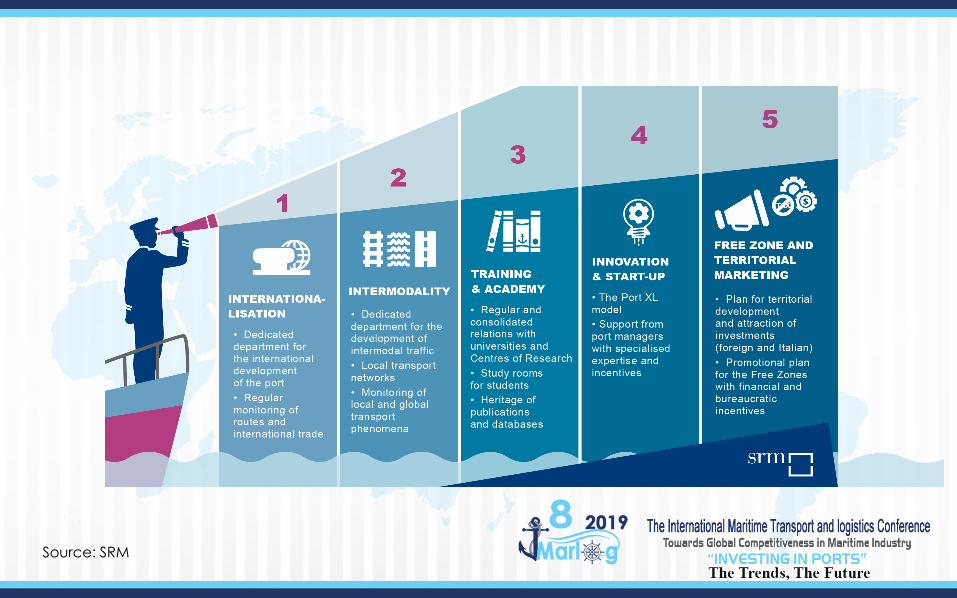

Ports of Future

Source: SRM

Ports of Future

Source: SRM

Ports of Future

Source: SRM

Ports of Future

Source: SRM

Ports of Future

Source: SRM

Source: SRM

Alessandro Panaro Head of Maritime & Energy Dept. SRM

www.srm-maritimeconomy.com

srmezzogiorno

SRM

SRM Studi Ricerche Mezzogiorno

Thank you for your attention SRM