38

1 © K.Cuthbertson, D. Nitzsche Lecture Mergers and Acquisitions, M&A 11/9/2001

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | hope-hampton |

| View: | 219 times |

| Download: | 0 times |

1

© K.Cuthbertson, D. Nitzsche

Lecture

Mergers and Acquisitions, M&A

11/9/2001

© K.Cuthbertson, D. Nitzsche

2

Topics

Types of Merger/ M&A Activity

Good/Bad Economic Motives

Economic Gains and Distribution of Gains

~ Cash Offer/ Share Offer

Financing of Mergers and Defence Tactics

Who Benefits/Loses: Empirics

Self Study: Regulation of Mergers: UK

© K.Cuthbertson, D. Nitzsche

3

Types of Merger/ M&A Activity

© K.Cuthbertson, D. Nitzsche

4

Types of Merger

Merger

Combining of two business under common ownership (over 95% are friendly, 5% hostile takeovers)

Horizontal

Banks and Building Societies

Glaxo-Welcome, Nestle-Rowntree, Granada-Forte(1996)

Vertical

Oil drilling, refinery and petrol stations

Car manufacturer and retail

AOL (America Online) and Time Warner (2000), Yahoo and others(1996-)

Conglomerate: Hanson Trust

© K.Cuthbertson, D. Nitzsche

5

Disbursement/Disinvestment/Downsizing

- we will not discuss this

Strategic Alliances

- BA, Quantas, Air Liberte etc

Types of Merger

© K.Cuthbertson, D. Nitzsche

6

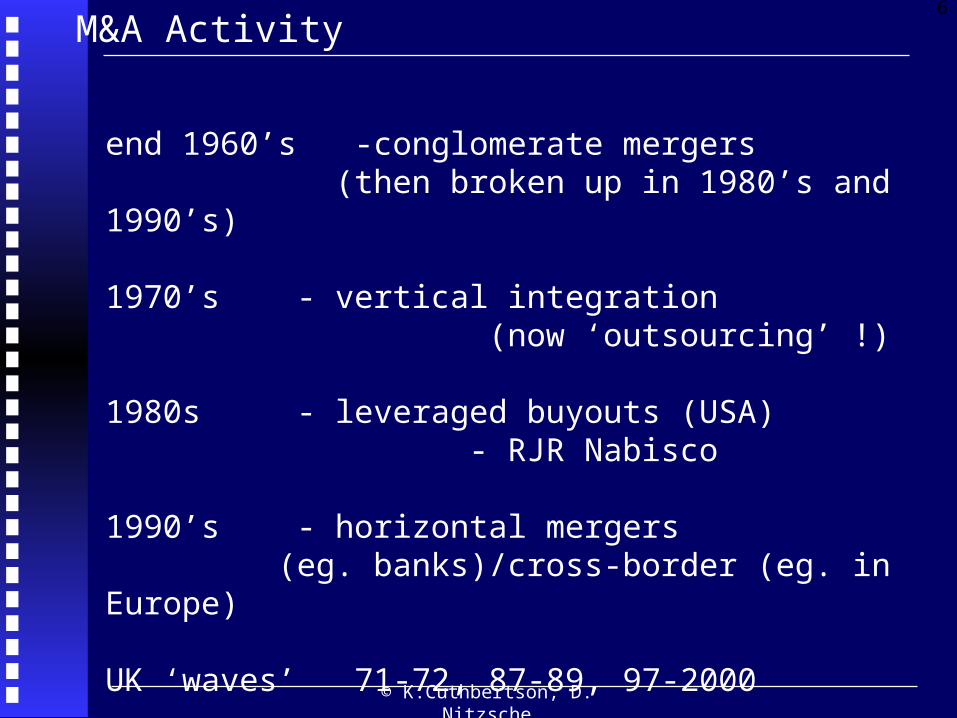

M&A Activity

end 1960’s -conglomerate mergers (then broken up in 1980’s and 1990’s)

1970’s- vertical integration (now ‘outsourcing’ !)

1980s - leveraged buyouts (USA) - RJR Nabisco

1990’s- horizontal mergers (eg. banks)/cross-border (eg. in Europe)

UK ‘waves’ 71-72, 87-89, 97-2000

© K.Cuthbertson, D. Nitzsche

7

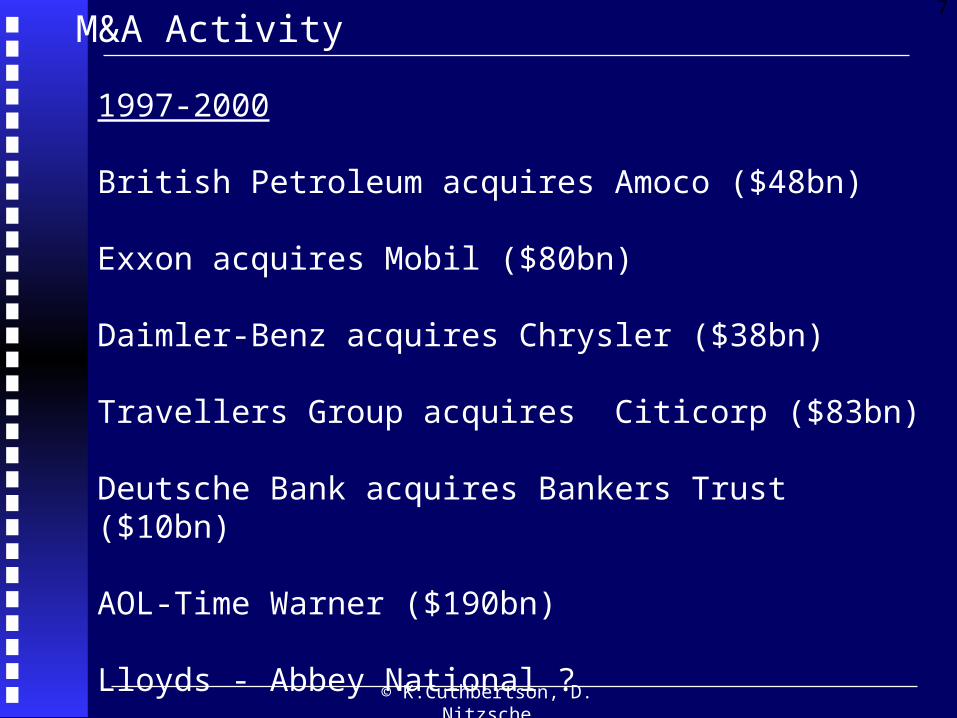

1997-2000

British Petroleum acquires Amoco ($48bn)

Exxon acquires Mobil ($80bn)

Daimler-Benz acquires Chrysler ($38bn)

Travellers Group acquires Citicorp ($83bn)

Deutsche Bank acquires Bankers Trust ($10bn)

AOL-Time Warner ($190bn)

Lloyds - Abbey National ?

M&A Activity

© K.Cuthbertson, D. Nitzsche

8

Good/Bad Economic Motives

© K.Cuthbertson, D. Nitzsche

9

Good Economic Motives

More Efficient Use of Resources

Better management in merged firm (e.g. Marriott takeover of Renaissance hotel grp, Dec 1996)

Cost savings (e.g. close bank branches)

Additional revenue generation (e.g. AOL-Time Warner)

Technology transfer/know-how (e.g. Glaxo-Welcome)

Strategic objectives (‘option’ to do something in the future e.g. AOL-Time Warner)

© K.Cuthbertson, D. Nitzsche

10

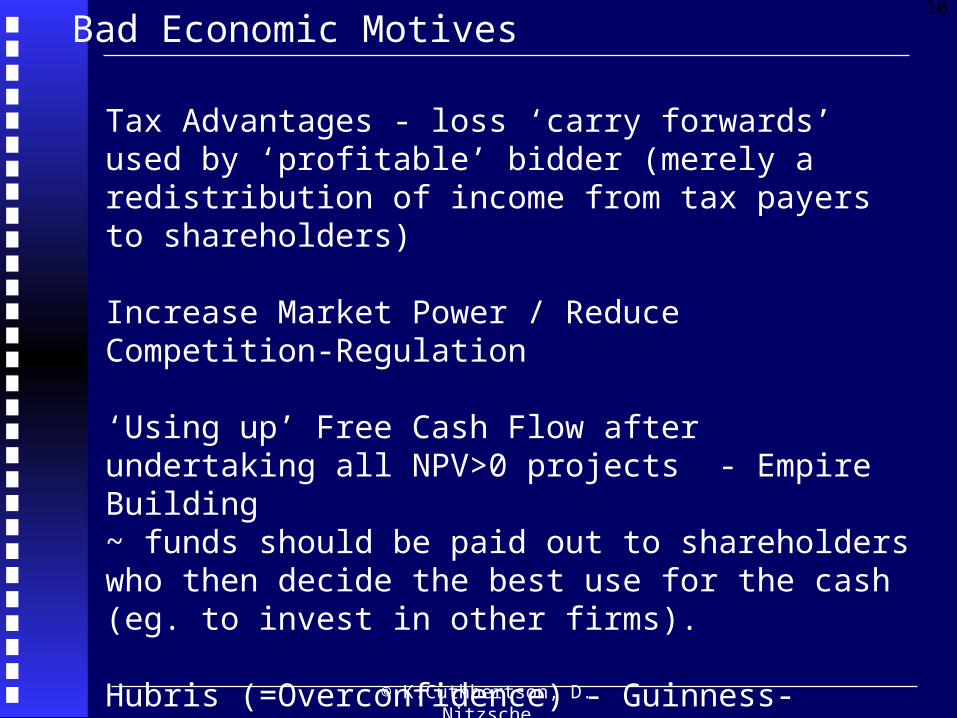

Tax Advantages - loss ‘carry forwards’ used by ‘profitable’ bidder (merely a redistribution of income from tax payers to shareholders)

Increase Market Power / Reduce Competition-Regulation

‘Using up’ Free Cash Flow after undertaking all NPV>0 projects - Empire Building~ funds should be paid out to shareholders who then decide the best use for the cash (eg. to invest in other firms).

Hubris (=Overconfidence) - Guinness-Distillers

Generate fees for Corporate Bankers/Lawyers !

Bad Economic Motives

© K.Cuthbertson, D. Nitzsche

11

Economic Gains

and

Distribution of Gains

© K.Cuthbertson, D. Nitzsche

12

Economic Gains and Distribution of Gains

1) Economic Gains

2) Distribution of Gains - cash offer- cash offer and underpriced

3) Distribution of Gains - share offer

© K.Cuthbertson, D. Nitzsche

13

Economic Gains

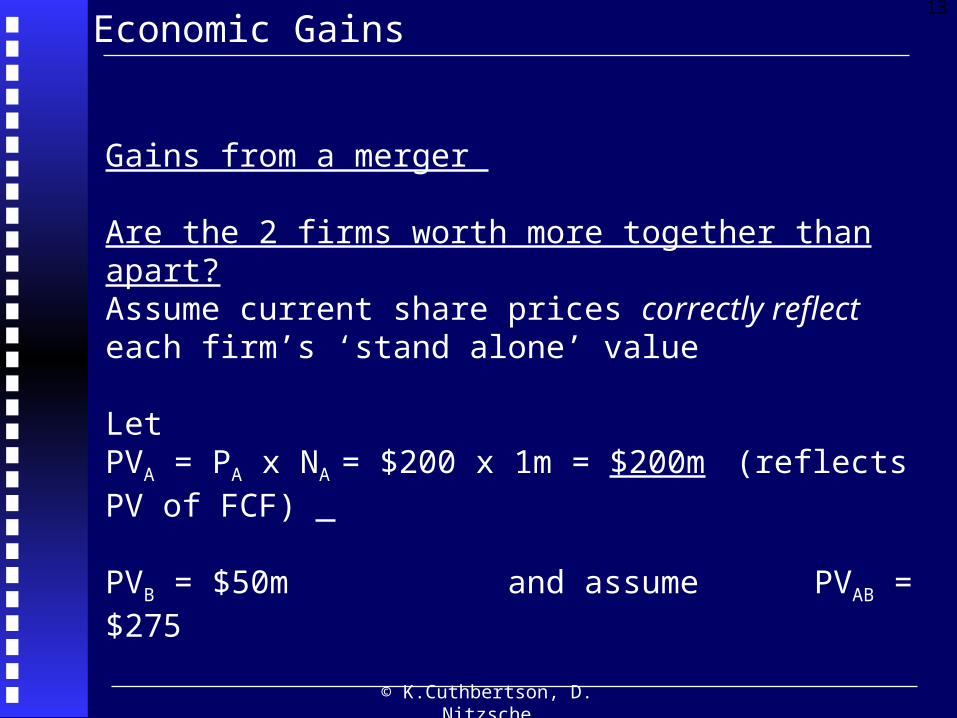

Gains from a merger

Are the 2 firms worth more together than apart?Assume current share prices correctly reflect each firm’s ‘stand alone’ value

LetPVA = PA x NA = $200 x 1m = $200m (reflects PV of FCF)

PVB = $50m and assume PVAB = $275

© K.Cuthbertson, D. Nitzsche

14

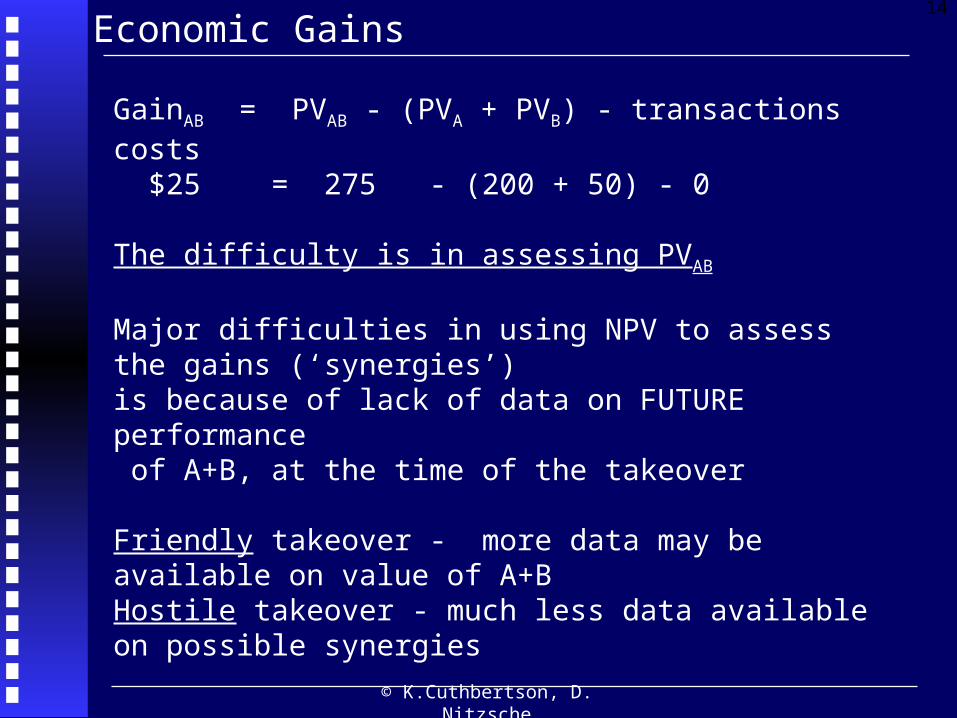

GainAB = PVAB - (PVA + PVB) - transactions costs $25 = 275 - (200 + 50) - 0

The difficulty is in assessing PVAB

Major difficulties in using NPV to assess the gains (‘synergies’) is because of lack of data on FUTURE performance of A+B, at the time of the takeover

Friendly takeover - more data may be available on value of A+BHostile takeover - much less data available on possible synergies

Scenario/sensitivity analysis will be used to estimate PVAB

Economic Gains

© K.Cuthbertson, D. Nitzsche

15

‘REAL OPTIONS THEORY’ ~ is now being used to value the merged company (when involving ‘young’ dot.coms)

Value of merged company = ‘conventional’ estimate of PVAB + value of ‘new’ options

e.g.‘New options’ = option to expand into new markets~ -if these ‘take-off’, then large profits (e.g. AOL-Time Warner with Disney films down the internet ?)

Economic Gains

© K.Cuthbertson, D. Nitzsche

16

Distribution of Gains: Cash Offer

Target ‘Correctly’ Priced in the market

‘A’ takeover of ‘B’: Gain for B= Cost for A

CostA = (cash paid - PVB ) = 65 - 50 = $15mThis is the ‘bid premium’This is a gain to B’s shareholders

Gain for A’s shareholdersGainA = GainAB - CostA = 25 - 15 = $10m

Return to B’s shareholders = 15/50 = 30%Return to A’s shareholders = 10/200 = 5%

© K.Cuthbertson, D. Nitzsche

17

Note:

If GainAB had been 10 (rather than 25) then A’s shareholders would loose from the merger:

GainA = GainAB - CostA = 10 - 15 = -$5m

and PA would fall on announcement of merger terms

Distribution of Gains: Cash Offer

© K.Cuthbertson, D. Nitzsche

18

Cash Offer: Target Underpriced

If PB << PVB : ie. B is underpriced

Then (for a given bid premium) more of the gains go to A. ‘A’ can gain, even if there are no synergies

(In this case there is not a gain for ‘society’, but a redistribution from B’s shareholders to A’s )

~ but note that A could ‘realise’ this gain by simply buying B’s shares (and not merging) and merely waiting for the ‘market correction’ that increases B’s price.

© K.Cuthbertson, D. Nitzsche

19

Share Offer

Assume A pays $65m for B (as with the cash offer) We also have PVAB = $275m, PVA = $200m, NA =1m and PA= $200

If B’s shareholders are to receive the equivalent of $65mthenNumber of (A’s) shares to be issued to B-shareholders

NB = PVB / PA (before merger) = $65m /$200 = 0.325m

This is announced BEFORE the actual merger takes place

© K.Cuthbertson, D. Nitzsche

20

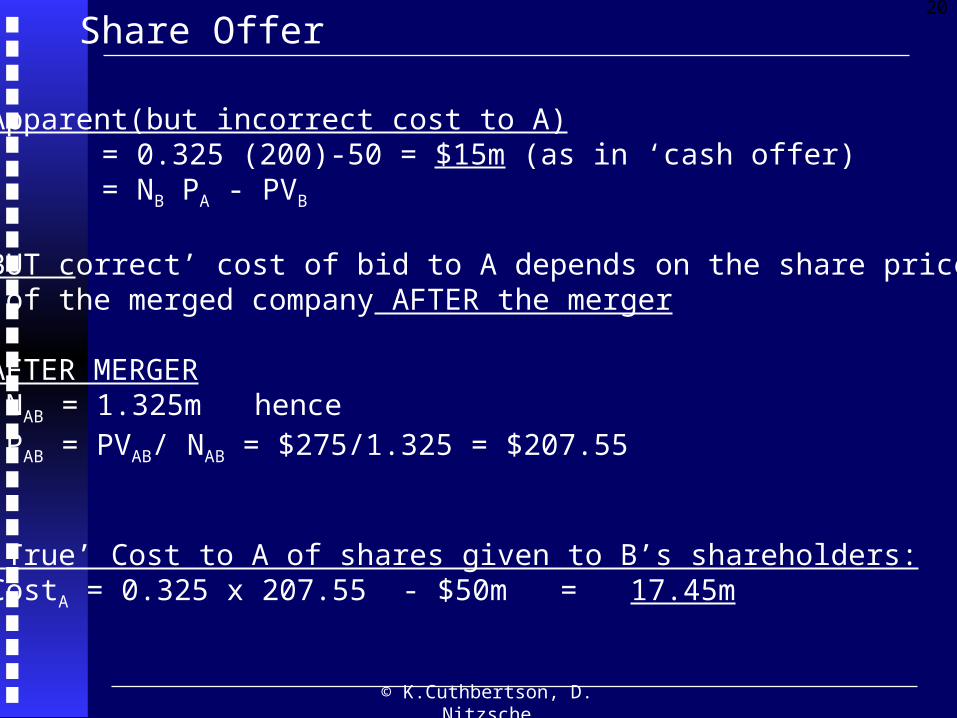

Apparent(but incorrect cost to A) = 0.325 (200)-50 = $15m (as in ‘cash offer) = NB PA - PVB

BUT correct’ cost of bid to A depends on the share price of the merged company AFTER the merger

AFTER MERGER NAB = 1.325m hence PAB = PVAB/ NAB = $275/1.325 = $207.55

‘True’ Cost to A of shares given to B’s shareholders:CostA = 0.325 x 207.55 - $50m = 17.45m

Share Offer

© K.Cuthbertson, D. Nitzsche

21

Cash versus Share Offer

CASH: cost to A of the merger is unaffected by the post-merger gains.

SHARESCost to A depends on the merger gains PVAB , which show up in the post merger price, PAB

© K.Cuthbertson, D. Nitzsche

22

Financing of Mergers

and

Defence Tactics

© K.Cuthbertson, D. Nitzsche

23

Financing of Mergers

CASH (TENDER) OFFER

Source of cash can be provided by the acquirer undertaking a ‘rights issue’ or, by bank borrowing or, issuing debt(e.g. LBO) or by using retained profits (‘free cash flows’)

- advantage to target shareholders is ‘precision’, and free to re-invest the cash in any other company

- disadvantage is cash paid out may be treated as realised capital gain and taxed.

- advantage for acquirer is that it retains total control of the new merged firm (ie no ‘dilution’ for its shareholders

© K.Cuthbertson, D. Nitzsche

24

SHARE OFFER- advantage to target shareholders is that any capital gain on ‘new’ shares are not realised and hence not subject to immediate capital gains tax

- advantage is target shareholder have (voting) shares in the new company

-disadvantage to acquirer, if target (B) is overvalued by stock market or bid premium is ‘too high’

MIXED OFFERs ARE ALSO USED: Cash, shares, preference shares, share options

Financing of Mergers

© K.Cuthbertson, D. Nitzsche

25

Defence Tactics

PAC MAN- mount a counter bid against the predator

WHITE KNIGHT- arrange another bid from a friendly company

POISON PILL- make bid costly (e.g. your shareholders can buy shares of new company at v. large discount. Rights issue to dilute predators holdings )

POISON PUT (in bond covenants)- bondholders of target can demand immediate repayment in full, if there is a change in ownershipCROWN JEWELS- sell off bits the acquirer is most interested in

© K.Cuthbertson, D. Nitzsche

26

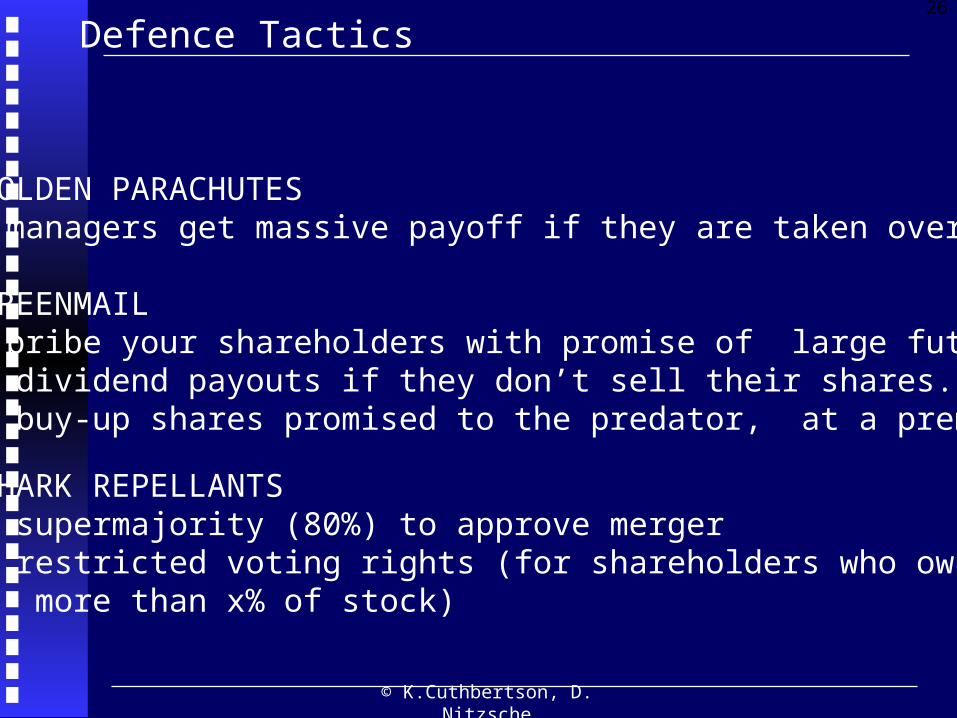

GOLDEN PARACHUTES- managers get massive payoff if they are taken over

GREENMAIL- bribe your shareholders with promise of large future dividend payouts if they don’t sell their shares.- buy-up shares promised to the predator, at a premium.

SHARK REPELLANTS- supermajority (80%) to approve merger- restricted voting rights (for shareholders who own more than x% of stock)

Defence Tactics

© K.Cuthbertson, D. Nitzsche

27

Who Benefits/Loses:

Empirics

© K.Cuthbertson, D. Nitzsche

28

Who Benefits/Loses: Empirics

MANAGEMENT- acquiring management gain control and $’s - 4 directors of RBS shared £2.5 for successful takeover of Nat West- Vodaphone CE Chris Gent £10m for takeover of Mannesmann

- acquired managers(‘golden parachutes’ or redundancy)

EMPLOYEES- usually redundancies for some employees of target

© K.Cuthbertson, D. Nitzsche

29

SHAREHOLDERS- TARGET SHAREHOLDERS gain - ACQUIRING SHAREHOLDERS - lose or break even,

THE ECONOMY- v. mixed (see CAR and Post merger performance - below)

Who Benefits/Loses: Empirics

© K.Cuthbertson, D. Nitzsche

30

The markets reaction/interpretation- Abnormal Return and Cumulative Abnormal Return

1) Use data from -70days to -10 days before announcementNormal Return = a + (beta) Rm

2) Data -10 days to +10 days after announcement

AR = Actual R - Normal ReturnCAR = sum of AR (from -10 to +10 or longer)

Markets are forward looking so change in price reflects the PV of all future prospects/profits

Who Benefits/Loses: Empirics

© K.Cuthbertson, D. Nitzsche

31

Bid announced by Doubletree 31/12/96

Doubletree drops out as Marriott announces agreement to acquire 18/2/97

13/12/96

12/3/97

AR (Daily) and CAR

CARAR

60%

40%

80

20%

-20%

0%

AR and CAR: Target = Renaissance Hotel Grp

© K.Cuthbertson, D. Nitzsche

32

The markets reaction/interpretation

RESULT (Average of US mergers)Acquired/Target firm’s shares have CAR of around +30%

Acquirer, CAR of -3.2% (stock offer)and -0.8% (cash offer)

For acquirer, over 2-years after merger, CAR is -17% (US)

SIZE MATTERSPVB=$10m and CAR = +100%, $-gain = $20mPVA =$1000m and CAR is -2% $-loss = $20m

Who Benefits/Loses: Empirics

© K.Cuthbertson, D. Nitzsche

33

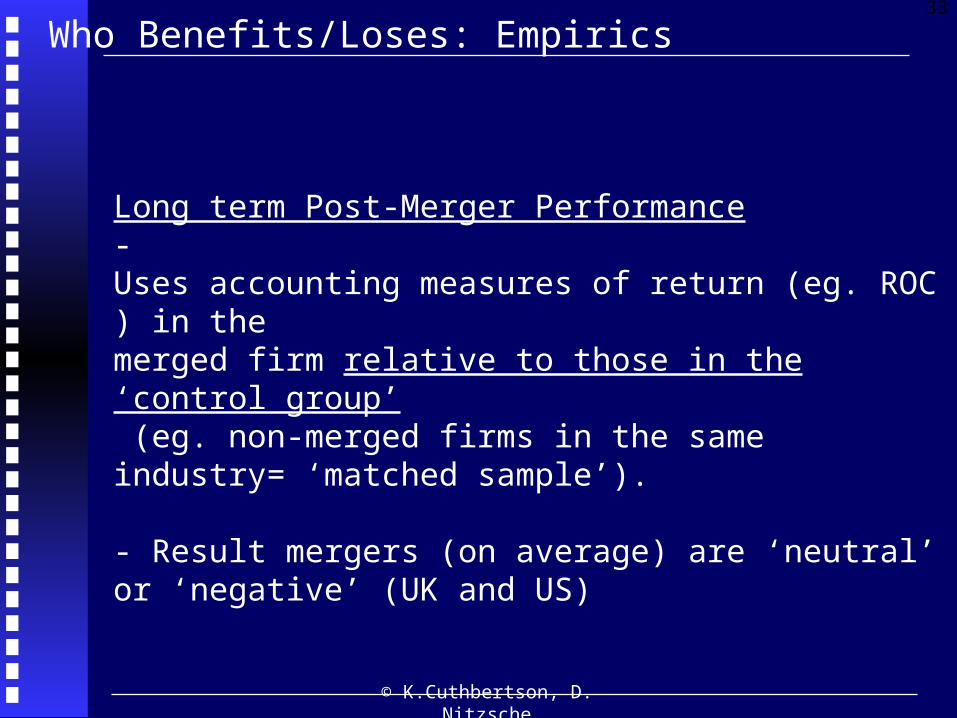

Long term Post-Merger Performance- Uses accounting measures of return (eg. ROC ) in the merged firm relative to those in the ‘control group’ (eg. non-merged firms in the same industry= ‘matched sample’).

- Result mergers (on average) are ‘neutral’ or ‘negative’ (UK and US)

Who Benefits/Loses: Empirics

© K.Cuthbertson, D. Nitzsche

34

End of Lecture

© K.Cuthbertson, D. Nitzsche

35

Self Study

Regulation of Mergers

© K.Cuthbertson, D. Nitzsche

36

Regulation of Mergers: UK

Takeover Panel - to ensure fairness for all shareholders

- In UK when ‘one firm’ holds 3% of the total shares outstanding of B, then you must make this public.

- Purchase of more than 10% of shares in B within 7 days is not allowed if this takes total shareholding to over 15%

- to prevent purchases from ‘professionals’ rather than general shareholders

© K.Cuthbertson, D. Nitzsche

37

- over 30% holding then T.P usually insists on a bid for all of B’s remaining shares. B comes ‘into play’ as a takeover target (observable by all).

Office of Fair Trading (OFT) - ensures competition

Monopolies and Mergers Commission- investigates M&A referred to it by OFT.

Regulation of Mergers: UK

© K.Cuthbertson, D. Nitzsche

38

End of Slides