18

Life Insurance in Estate Planning

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | sherman-ezra-strickland |

| View: | 217 times |

| Download: | 1 times |

Life Insurance in

Estate Planning

Life Insuranceo A contract with an insurance company that provides

either a lump sum or annuity at death of insured

• Beneficiaries listed by policy • If no living beneficiaries at death, part of

estate of deceased, and distributed by will or state rules

o Policies can carry riders or features• Cash Surrender Value (Whole Life)• Borrowing rights at “reduced” rates• Ability to increase death benefit over time

Parties to a Life Insurance Contracto The Owner of the Policy --- the one who has title of the

policy and can make future decisions about the policy including• Change beneficiaries of the policy• Borrow from the policy (if borrowing feature part of policy)• Pledge the policy against loan• Change the premium payments (increase or decrease)• Cancel policy

o The Insured of the Policy – Individual’s death that activates payment of death benefit

o The Beneficiary of the Policy – the individuals, charities, or institutions that receive some or all of the death benefit

Why Buy Life Insurance? Or When is Life Insurance necessary?o What asset are you trying to “protect” with proceeds

• Future Income stream for loved ones• Debt retirement for loved ones• Educational costs covered for loved ones• Cover burial, medical, or other expenses of deceased• Other support for loved ones

Change in requirements for Life Insurance over the life of an individual (Life Insurance Matrix)o Height of needed insurance and point where not neededo When to start (when to buy first policy)

Worksheet on Life Insurance Proceeds to Replace Spouse Income o Example on Page 451 to 452 – Jack and Jill

• Determine the annual income to replace• Determine the annuity present value (for a perpetuity)• Perpetuity is the Life Insurance lump sum payout at death• Determine annual withdrawals adjusted for inflation• Forty year income stream

o Spreadsheet for Client – explains the withdrawals and reinvestment

Does paying off mortgage with death benefit (policy on outstanding balance of mortgage paid at death) reduce monthly expenses by size of mortgage? Not really, Why?

Types of Life Insuranceo Term Life Insurance

• Policy is for specific time period – the term of the contract• Policy pays a “death benefit” if and only if the insured dies

prior to the end of the term• Policy is usually paid for with annual, semi-annual, quarterly or

monthly payments to insurance company• Policy payments stop at death of insured or if policy is

cancelledo From the Insurance Company’s Perspective

• Policy premium is a put option on the insured• Value of contract is determined by factors (interest, expected

life of insured, interest rates, and payout (strike price of contract))

• Option because strike price paid if and only if death occurs

Types of Life Insurance -- continuedo Universal Life Insurance

• Two Parts – Term Insurance and Cash Accumulation Account• Policy Premium is cost of term plus and investment election• Total premium is paid to cash accumulation account and

insurance company “pays” annual premium from cash accumulation account

• Cash accumulation account is “invested” asset for policy and earns income (can be set rate or variable)

• Individual can “withdraw” from cash accumulation account• Policy is cancelled if cash accumulation account is insufficient to

pay annual premiumo Insurance Company provides two simultaneous services

• Risk coverage• Investment

Types of Life Insurance -- continuedo Variable Universal Life Insurance

• Two Parts – Term Insurance and Cash Accumulation Account• Policy Premium is cost of term plus and investment election• Total premium is paid to cash accumulation account and

insurance company “pays” annual premium from cash accumulation account

• Cash accumulation account is “invested” at the direction of the policy holder – usually options provided by insurance company

• Individual can “withdraw” from cash accumulation account• Policy is cancelled if cash accumulation account is insufficient to

pay annual premiumo Insurance Company provides two simultaneous services

• Risk coverage• Investment

Types of Life Insurance -- continuedo Whole Life Insurance

• Two Parts – Permanent Insurance and Cash Accumulation Account• Permanent insurance for life of insured (does not have a preset

end or term)• Policy Premium is cost of permanent plus and investment account• Total premium is paid to cash savings account and insurance

company “pays” annual premium from cash accumulation account

• Individual can “withdraw” from cash accumulation account• Policy is cancelled if cash accumulation account is insufficient to

pay annual premiumo Insurance Company provides two simultaneous services

• Risk coverage with guaranteed payment whenever death occurs• Investment

Types of Life Insurance -- continuedo Second-to-Die Insurance

• Two Individuals insured but payment at second death• Can be Term, Universal, Variable, Whole Life Insurance• Policy Premium is cost of insurance choice and if elected,

investment• Typically Policy is part of an Irrevocable Life Insurance Trust• Often used when one spouse is uninsurable (probably will die

first)• Policy is cancelled if premiums not paid

o Insurance Company provides two simultaneous services• Risk coverage with payment whenever second in death occurs• Investment – option to add this based on type of policy

selected

Life Insurance and Taxeso In general, the death benefit proceeds from a life

insurance policy are not taxed• You can think of the policy premiums as the expense

of the asset and death benefit is return of the principal

o Transfer for Value• If the life insurance policy is transferred to

another individual, the proceeds can be taxed• If the transfer is gratuitous – no tax• If transfer provides benefit to original policy holder

– death benefit minus consideration is taxable

Exceptions to the Transfer for Value Ruleo Transferred to the insured (Policy holder

transfers policy to the insured individual)o Transferred to business partner of insuredo Transferred to partnership of insuredo Transferred to corporation where insured is a

shareholder or officero Transferred to policy holder that takes the basis

of the original policy holder Future cancellation of transfer does not

avoid taxes

Settlement of Life Insurance Proceedso Death Benefit Paid at death of insured

• Lump Sum at death (typically as close to death as possible)• Benefit left with Insurance Company and interest from

benefit paid to beneficiary – income is taxed as ordinary income and benefit paid out at later date

• Annuity paid to beneficiary – portion of annuity is principal of benefit and portion is income and taxed as ordinary income (amortization of the benefit)

o Early Payout – Cash Surrender• Election to receive benefit prior to death (only for whole life

policies)• Surrender value is percent of death benefit minus

administrative costs of the surrender

Modified Endowment Contractso Contracts set up to look life a variable life insurance contract

but…• Set up to avoid taxes• Cannot qualify for tax relief if the policy payments are front loaded• Rule is if policy is essentially paid up before seven years it is a MEC

not a life insurance policy• Earnings (interest income) is taxable as ordinary income• Death benefit – when paid – is still free of tax

Exchangeso Typically free of tax and basis is original basis plus cost of

exchange Early pay-off for terminally or chronically ill insured

o Payment to chronically ill for actual out of pocket medical expenses

Gift Tax Treatment of Life Insuranceo In general, if the beneficiary is not the policy holder, the

proceeds at death of the insured are a gift from the policy holder to the beneficiary• Example, Hillary owns a life insurance policy on Bill. At Bill’s

death the policy has Chelsea as the beneficiary and a $2,000,000 benefit is paid to Chelsea• Hillary has made a $2,000,000 gift to Chelsea (and may need

to pay a gift tax depending on unused one-time exemption)• Chelsea receives a tax free income of $2,000,000

o If beneficiary is a charity, payout is to a charitable gift and may be gift tax free (some special considerations need to be met for gift exclusion)

Three year look back applies to insurance payouts

Irrevocable Life Insurance Trust (ILIT)o Insurance Policy purchased on an individual and the trust “owns”

the policy not the insured – trustee has vested title of policyo Since insured is not owner of policy, not part of estate at deatho Trust has beneficiary other than insured (otherwise the death

benefit gets paid to the estate and is part of the estate)o Trust pays policy premiums – Trust maker (the insured) makes

transfers to the trust for premium paymentso Transfers are considered present gift (not future interest) if there

is a Crummey provision – beneficiaries have 30 days to withdraw the transfers to the trust for their personal consumption

o With Crummey provision transfer is gift but eligible for annual exclusion up to the number of beneficiaries in trust

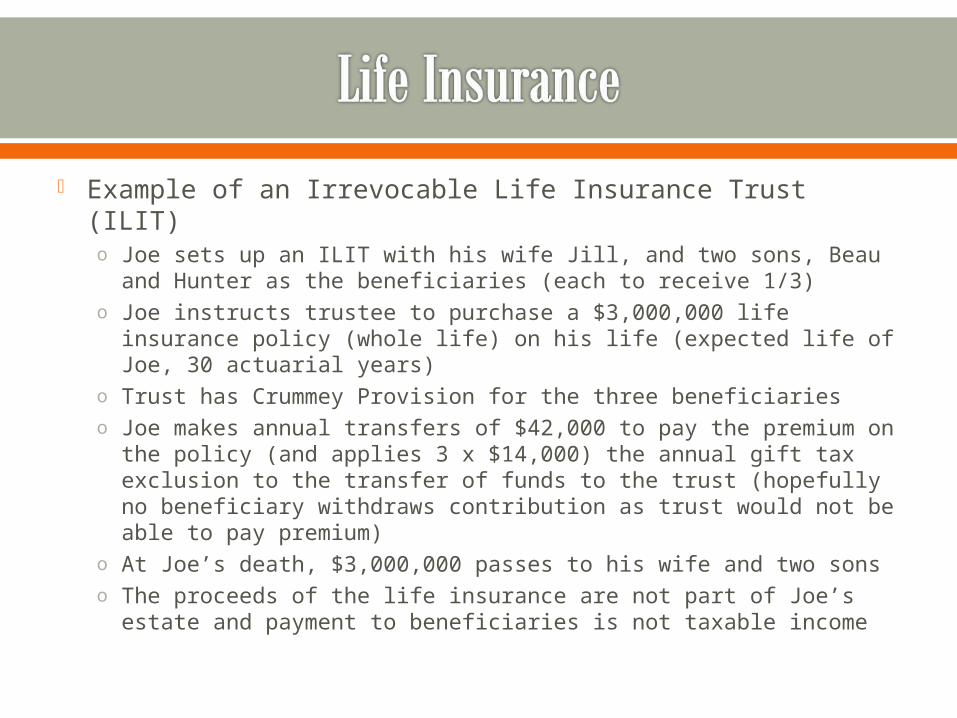

Example of an Irrevocable Life Insurance Trust (ILIT)o Joe sets up an ILIT with his wife Jill, and two sons, Beau and

Hunter as the beneficiaries (each to receive 1/3)o Joe instructs trustee to purchase a $3,000,000 life insurance

policy (whole life) on his life (expected life of Joe, 30 actuarial years)

o Trust has Crummey Provision for the three beneficiarieso Joe makes annual transfers of $42,000 to pay the premium on

the policy (and applies 3 x $14,000) the annual gift tax exclusion to the transfer of funds to the trust (hopefully no beneficiary withdraws contribution as trust would not be able to pay premium)

o At Joe’s death, $3,000,000 passes to his wife and two sonso The proceeds of the life insurance are not part of Joe’s estate

and payment to beneficiaries is not taxable income

What are the implications for Financial Planning?o What options are available to insured?

• Transfers to beneficiaries outside of estate of deceased• Tax free distribution to beneficiaries• Gifts to charities • Payout greater than accrued assets would allow

o How ownership of insurance impact taxes?• Insured is owner and beneficiary, death benefit part of estate• Insured is not owner, can pass payout to beneficiary outside of estate• Can cover partnerships and business agreements at death of partner

o How does payout style impact taxes?• Lump sum payout tax free to beneficiaries• Payout over time can have taxable income consequences to

beneficiary