53

http://www.thaioilgroup.com

http://www.thaioilgroup.com

The information contained in this presentation is intended solely for

your personal reference. Please do not circulate this material. If you

are not an intended recipient, you must not read, disclose, copy,

retain, distribute or take any action in reliance upon it.

2

3

• To be in top quartile on performance and return on investment

• To create a high-performance organization that promotes teamwork, innovation and trust for sustainability

• To emphasis good Corporate Governance and commit to Corporate Social Responsibility

A LEADING FULLY INTEGRATED REFINING & PETROCHEMICAL

COMPANY IN ASIA PACIFICVISION

MISSION

Ownership & Commitment

Social Responsibility Integrity

Vision FocusProfessionalism Excellent Striving

Teamwork & CollaborationInitiative

VALUE

4

Corporate Governance Policy

The board of directors,

management and all staff shall commit to moral principles, equitable treatment to all stakeholders and perform their duties for the company’s interest with dedication, integrity, and transparency.

Roles and Responsibilities for Stakeholders

• Truthfully report company’s situation and future trends to all stakeholders equally on a timely manner.

• Shall not exploit the confidential information for the benefit of related parties or personal gains.

• Shall not disclose any confidential information to external parties.

CG ChannelsShould you discover any ethicalwrongdoing that is notcompliance to CG policies or anyactivity that could harm theCompany’s interest, pleaseinform:

Corporate Management OfficeThai Oil Public Company Limited 555/1 Energy Complex Building A 11F, Vibhavadi Rangsit Road,Chatuchak, Bangkok 10900

[email protected] http://www.thaioilgroup.com

+66-0-2797-2999 ext. 7312-5

+66-0-2797-2973

5

Q1/11 Business Highlights

6

Corporate

• CSR - Building new classroom building for Ban Khun Ya School, Chiang Mai

Utilization

106%Market GRM

6.1 $/bblTPX

2.6 $/bblMarket GIM

9.7 $/bblStock gain

6.2 $/bblTLB

1.3 $/bblAccount GIM

15.6 $/bbl

7

•Global Econ

•Colder than normal

• Japan’s Quake

• Local refineries shutdown for

Euro IV

• LPG Ex-Ref Price Floatation since Jan 2011

•Unrest in ME resulting in a

surge crude oil prices

StrongMarket GIM

HigherDomestic Sales

BetterOptimization

RealizedStock gain

TOP Group Net Profit

3,745 MB

3,483 MB

7,228 MBNP w/o stock gain

Stock gain

Business

• New VLCC – 280,000 DWT• Acquired UBE – Ethanol 400 KLPD• TDAE - additional 50 KTA

Finance

• IFRS Adoption• 200 M$ loan to increase

efficiency of WC management

Performance Analysis

8

44 59 68 75 77 74 75 84 10120

40

60

80

100

120

140

160

9

Dubai Crude Price

Q1/09 Q3/09Q2/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10

62

78

$/bbl

Q1/11

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

106 $/bblas of 20 May

More flow into oil market, WTI net long position hit record high

Colder-than-normal winter to support heating oil & crude prices

Enbridge, Trans-Alaska pipeline shutdown, etc.

Unrests in Middle East & North Africa interrupting crude production

2.7 2.9 3.7 3.6 6.1 1.1 3.3

-3.0-6.7

-4.8-8.2 -8.6

-4.7 -5.7

10

-47.8 -48.5-41.3

-54.5

-24.0-33.8

-48.0

+ Strong demand for bunker grade+ Lower western arbitrage- Singapore supply remained heavy

9.411.7 12.9 14.3

20.2

8.312.1

8.911.3 12.4 13.0

18.2

7.3

11.4

GO - DB

JET - DB

12.69.4 8.6

10.712.6

8.510.3

ULG95 - DB HSFO - DB

LPG - DB

(controlled price)

(Unit: $/bbl)

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

Market GRM

Q1/10 Q2 Q3 Q4 Q1/11 FY/09 FY/10

+ Refinery outage and heavy maintenance + Firm demand from the ME and South Africa

+ Upcoming refinery maintenance to limit supply + Japan’s quake to tighten supply amid low

jet/kerosene inventory

+ Strong heating oil demand in the US & Europe + Japan’s quake to limit exports and even turn

imports for power plants

QTD (Q2)

16.0

21.2

20.6

-9.9

Q1/10 Q2 Q3 Q4 Q1/11 FY/09 FY/10

*(market price announced by Aramco)

*

-26.2

44 59 68 75 77 74 75 84 10120

40

60

80

100

120

140

160

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

2009 2010

Crude Oil Price - Dubai (Unit: $/bbl)

62

111.7 $/bblas of 13 June

3.1 2.5 3.7 7.2 12.3 3.4 4.1

2.7 2.9 3.7 3.6 6.1 1.1 3.3

Market GRM

0.4

-0.4 -0.1

3.6 6.2 2.3 0.8

Stock Gain/Loss

Accounting GRM

(Unit: $/bbl)

(Unit: $/bbl)

(Unit: $/bbl)

11Q1/11

78

Q1/10 Q2 Q3 Q4 Q1/11 FY/09 FY/10

12

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

79% 76%

11%11%

4%4%

6% 9%

10% 10%

37% 38%

20% 20%

16% 15%

14% 14%

3% 4%

FY/10 FY/10 Q1/11 Q1/11

Far East

Local

MiddleEast

Q1/11

Sources of Crude

1.mainly ESPO-USSR2.LPG Market Price – CP Aramco

-24.0

20.6

18.2

-8.6

12.6

2 LPG

Platformate

Gasoline

Jet

Diesel

Fuel oil

Spread over Dubai(US$/bbl)

FY/10

2

Spread over Dubai(US$/bbl)

-14.8

12.1

11.4

-5.7

10.3

• Flexible production by diversifying crude type to seek an opportunity from market for cheaper crude.

• Improve lorry loading facilities and Maximize Gasoil products by adjusting production mode to capture domestic price premium and EURO IV incentive by 1.20 $/bbl

• New LPG Pricing boosted higher LPG production to enhance GIM

Others1

13

80% 92%

20% 8%

FY/10 Q1/11

Export

Domestic

(KBD)Refinery Intake 292

TOP’s Domestic & Export Sales

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

261

45%

13%

13%

5%

17%6%2%

DomesticJobbers

Q1/11

Sales

Breakdown

Export = 8%

147 127 86

335

50

746

185129 95

337

42

788

LPG Gasoline Jet-A1 Diesel/GO FO Total

Q1/10

Q1/11

Domestic Oil Demand / Domestic Refinery Intake Domestic Oil Demand (KBD)

(KBD)

+1%+10%

+0.4%

-16%

+6%

+26%

746 732 722 748 788 711 737

138 155 120 160 80 192 144

89% 89% 90% 90%84% 87% 89%

0%

20%

40%

60%

80%

100%

-

200

400

600

800

1,000

1,200

1,400

Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 FY/09 FY/10

Domestic Demand/Sales Net Export Others Utilization RateLPG Jet/Kero Diesel FOGasoline Total

Demand

Utilization = 106%

0

400

800

1,200

1,600

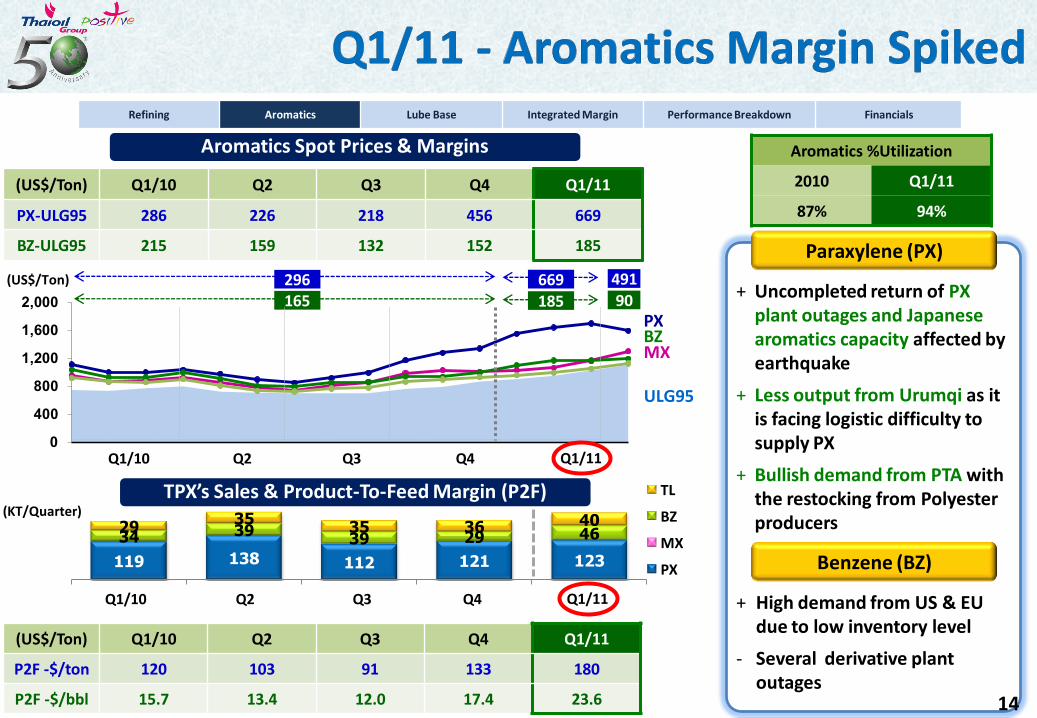

2,000+ Uncompleted return of PX

plant outages and Japanese aromatics capacity affected by earthquake

+ Less output from Urumqi as it is facing logistic difficulty to supply PX

+ Bullish demand from PTA with the restocking from Polyester producers

+ High demand from US & EU due to low inventory level

- Several derivative plant outages

14

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

Aromatics Spot Prices & Margins

PX

ULG95

BZ

(US$/Ton) Q1/10 Q2 Q3 Q4 Q1/11

PX-ULG95 286 226 218 456 669

BZ-ULG95 215 159 132 152 185

MX

119 138 112 121 123

34 3939 29 4629

3535 36 40

Q1/10 Q2 Q3 Q4 Q1/11

TL

BZ

MX

PX

TPX’s Sales & Product-To-Feed Margin (P2F)

(US$/Ton) 296165

Q1/10 Q2 Q3

(KT/Quarter)

49190

Aromatics %Utilization

2010 Q1/11

87% 94%

Paraxylene (PX)

Benzene (BZ)

Q4

669185

(US$/Ton) Q1/10 Q2 Q3 Q4 Q1/11

P2F -$/ton 120 103 91 133 180

P2F -$/bbl 15.7 13.4 12.0 17.4 23.6

Q1/11

Q1/10 Q2 Q3 Q4 Q1/11

0

400

800

1,200

1,600

15

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

64 65 58 44 6936 38 32 25

3687 97 85

60

109

Q1/10 Q2 Q3 Q4 Q1/11

Bitumen

TDAE/Extract/Slack

WaxBase Oil

Base Oil & Bitumen Spot Prices & Margins

BITUMEN

500SN

TLB’s Sales & Product-To-Feed Margin (P2F)(KT/Quarter)

HSFO

629-97

54422

Q1/10 Q2 Q3 Q4

(US$/Ton) Q1/10 Q2 Q3 Q4 Q1/11

500SN-HSFO 435 541 607 593 629

BIT-HSFO 27 38 46 -25 -97

Q1/11

Q1/10 Q2 Q3 Q4 Q1/11

(US$/Ton) Q1/10 Q2 Q3 Q4 Q1/11

P2F -$/ton 115 135 149 179 181

P2F -$/bbl 17.4 20.6 22.6 27.2 27.5

+ Tight supply across Asia Pacific due to several refineries turnaround

+ Chinese demand peak up to building their stock for agriculture sector

+ Producers rose their price follow higher HSFO price

+ Chinese demand remained strong

+ High HSFO prices pressure margin (as bitumen margin decreases QoQ)

+ Spread TDAE 500 $/Ton

Base oil %Production Rate

2010 Q1/11

93% 98%

Lube Base Oil

Bitumen

15

722-117

TDAE

5.4 5.06.1 6.2

9.7

4.35.7

5.7 4.76.0

9.7

15.6

6.1 6.5

16

2.7 2.9 3.7 3.66.1

1.13.3

Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 FY/09 FY/10

15.7 13.412.0

17.4 23.6 20.714.7

Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 FY/09 FY/10

17.4 20.6 22.6 27.2 27.5 15.8 21.5

Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 FY/09 FY/10

Crude

Product toFeed

Product toFeed

(US$/bbl)

Market GRM*

(excluded stock gain / loss)

Q1/10 Q2 Q3 Q4 Q1/11 FY/09 FY/10

(US$/bbl) (US$/bbl)

Market GIM Accounting GIM

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

Q1/10 Q2 Q3 Q4 Q1/11 FY/09 FY/10

4,995 1,407 617 73 92 21 84 (9) 7,228

4,241 540 340 86 13 11 46 (7) 5,25117

.

RefineryUtilization

Aromatic Production

Lube Base Production

Plant Availability

Plant Utilization

SAKC UtilizationShip

Utilization

Q1/10

Q1/11

3.1

12.3

P2F (US$/ton)

Acc GRM(US$/bbl)

P2F (US$/ton)

120

180

115

181

94%84% 92%

65%81%

92% 91%106%

94% 98%84% 87%

97% 96%

AP Rate(Baht/KW hour)

0.30

0.30

Q1/11 Net Profit Breakdown (include stock gain / loss & LCM)

NP

∆YoY

Q1/10 Q1/11

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

(Unit: MB) Conso.56%holding

55%holding

Stock &LCM gain Q1/11 = 3,483 MB

Net Profit excl. stock gain & LCM = 3,745 MB

• TOP: High utilization, More domestic sales, New LPG Pricing

• TLB: Additional 50,000 tons TDAE on commercial

(MB)

Sales Revenue 111,842 81,244 78,957

EBITDA 12,079 6,632 3,715

Financial Charges (543) (451) (424)

FX G/L & CCS 165 433 740

Tax Expense (2,808) (1,402) (451)

Net Profit / (Loss) 7,228 3,579 1,977

EPS (THB/Share) 3.54 1.75 0.97

THB/US$ - ending 30.43 30.30 32.53

Effective Tax Rate (%) 28% 23% 18%

(US$/bbl) Q1/11 Q4/10* Q1/10*

Market GRM 6.1 3.6 3.1

Market GIM 9.7 6.2 5.7

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

18

QoQ+/(-) YoY+/(-)

2.5 3.0

3.5 4.0

30,598 32,885

5,447 8,364

92 (119)

(268) (575)

(1,406) (2,357)

3,649 5,251

1.79 2.57

0.1 (2.1)

5% 10%

Interest Rate Currencies

40% Float 56% THB

60% Fixed 44% USD

Cost of Debt

TOP Group 4.04%19

76,838 82,737

26,20639,136

43,563

47,906

(Unit: MB)

Trade Payable/ Others

LT Debt*

146,607137,745

FY/10

Equities

CurrentAssets

Non-CurrentAssets

Q1/11

Statements of Financial Position

* Including current portion of Long-Term Debt

US$ Bond28%

US$ Loan17%

THB Bond37%

THB Loan18%

89%

5%3%3%

Consolidated Long-Term Debt 1)

1) Including current portion of Long-Term Debt

Q1/11Total LT DebtBt. 47,906 mn.(US$ 1,574 mn.)

Net DebtBt. 28,905 mn.(US$ 950 mn.)

1.6 1.7

0.6

FY09 FY/10 Q1/11

0.5 0.4 0.3

FY/09 FY/10 Q1/11

Financial Ratios

Net Debt / EBITDA Net Debt / Equity

Refining Aromatics Lube Base Integrated Margin Performance Breakdown Financials

Policy ≤ 1.0xPolicy ≤ 2.0x

1) As of 31 Mar 2011 (30.43 THB/US$) 2) EBIDA Q1/54*4

2011 Market Outlook

20

•Macroeconomics & Crude Prices

•Petroleum Market

•Aromatics & Base Oil

•Conclusion

•Q1-2011 Market Highlights

Ave Q1-11 LPG prices @$755/ton compared to previous $333/ton

LPG sales increase from 18,000 ton/month to 40,000 ton/month

TOP GRM increased by $0.6/bbl due to new LPG price

Q1-11 TOP domestic sales increased to 94%

TOP runs at 106% capturing high margins and market shares

Political unrests spreading throughout ME and NA (Tunisia, Egypt, Jordan, Yemen, Iran, Bahrain, Libya) cause investors’ worries on oil supply disruption Unrest in Libya caused a supply

loss by at least 1.3 MBD

30% of Japan’s refinery and 20% of BTX capacity shut down immediately after the quake Support middle distillate cracks to

above $24/bbl early April More fuel oil imports for power

due to nuclear plant outage

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

21

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

Crude surged on supply disruption andfund flows into oil market

Gasoline rose on supply tightness from plant turnaround and stock-rebuilding

Skyrocket aromatics margin on plant outages and strong demand from traders

Steady increase in base oil marginon tight supply

‘10 ‘10 ‘11

Q3 Q4 Q1

Dubai 73.9 84.4 100.9

MO-DB 8.6 10.6 12.6

JET-DB 12.8 14.3 20.3

GO-DB 12.4 13.0 18.4

FO-DB -4.8 -8.2 -8.7

PX-UG95 216 456 669

BZ-UG95 131 152 181

TL-UG95 56 91 39

500SN-FO 607 593 630

Bitumen-FO 46 -25 -97

Extreme cold weather and strong industrial activities pushed up Mid Distillates

GRM* 3.7 3.6 6.1

GIM* 6.1 6.2 9.7Strong GRM and GIM on bullish middle

distillates and PX margins*TOP GRM & GIM excluding stock gain/loss 22

Macroeconomics & Crude Prices

23

Firm fundamentals outlook…

High volatility oil prices

Global Economy to Continue to Grow in 2011

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

2010 2011 *

10.3% 9.6%

10.4% 8.2%

3.9% 1.4%

7.8% 4.0%

2.8% 2.8%

1.7% 1.6%

5.0% 4.4%

2.9%

-0.5%

5.0% 4.4% 4.5%

-9%

-6%

-3%

0%

3%

6%

9%

12%

2008 2009 2010 2011 2012

GDP Growth (%YoY)

China

India

Japan

Thailand

US

EU

World

Source: IMF World Economic Outlook 11 Apr 11

*Change from Jan-11 projection

24

86.8 86.085.1

88.0

1.6-0.6 -1.1

2.9

-8.0

-6.0

-4.0

-2.0

0.0

2.0

83

85

87

89

91

93

Q1 Q2 Q3 Q4

2007 2008 2009 2010 2011

OECD stocks eased from its peak at 63 days of cover to a much comfortable level of 59.2 days of cover

Crude stocks in OECD are below 5 year range if Canada and PADD2 are excluded

Crude exports from Libya is expected to gradually resume as no major facility outage due to the unrest

Demand

YoY Growth

2011 Avg 89.4 MBD

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

25

2011 oil demand is expected to grow by 1.5 MBD, sending the gross number to a record high of 89 MBD Non-OECD countries remain the key driver of growth,

while the US growth to turn flat after a strong rebound last year

MBBL

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

Greece’s 2010 budget deficit overshot the target (-8.1% of GDP) at -10.5% of GDP The cost of insuring Greek 5-yr government bond jump to a record high above 1,400 bps, making it more difficult to finance the debt via the financial market at a reasonable cost. Greece awaits given extra money and EU-IMF bailout package to keep the country from default The absence of Dominique Strauss-Kahn, IMF Chief, cast a cloud over a new plan for Greece as he is a major champion for bailout approach. Portugal became the 3rd euro zone country in a year, after Greece and Ireland, to secure a rescue package.

26

Fund Flows

•More fund flows into commodity market to hedge against inflation amid strong fundamentals

Hurricane Season• NOAA forecasted

2011 Atlantic hurricane season will be above normal with 6-10 hurricanes, around half could become major

OPEC

MENA Unrest to Continue

• Unrests will continue in Libya, Yemen and Syria

• Saudi – Iran development into religion conflict

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

Season: Jun-Nov

•OPEC gets more pressures from IEA and US to boost up output quota to bring price down as OPEC kept oil output quota unchanged sinceDec 2008

27

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

Source : Reuters Polls (20+ companies) as of 21 April 11

What the Others SayCrude prices has risen too fast & too much…. “ EXPECT DOWNWARD CORRECTION”

Oil Price Forecast BRENT

Unit : USD/BBL Q2-11 Q3-11 Q4-11 2011 2012

BofAML 122.0 110.0 95.0 108.0 -

Barclays 120.0 110.0 112.0 112.0 105.0

BNP Paribas 117.0 110.0 115.0 112.0 114.0

CA-CIB 103.0 85.0 86.0 94.9 82.5

Credit Suisse 111.0 107.0 102.0 106.2 101.5

Deutsche 120.0 125.0 120.0 117.5 117.5

First Energy 108.8 111.0 111.0 109.0 107.0

Global Risk - 122.0 119.0 114.0 115.0

Goldman Sachs - 105.0 107.0 - -

JBC Energy 110.7 107.8 102.0 106.4 109.8

Nomura 94.0 95.0 102.0 99.0 110.0

Soc Gen 113.3 110.8 108.7 109.5 110.0

UBS 110.0 105.0 95.0 103.8 95.0

Median from Reuters 113.7 110.0 105.0 109.2 108.0

28

$95$91 $91

$94

$101$106 $106

$109

$62

$68

$94

$62

$78

40

50

60

70

80

90

100

110

120

40

50

60

70

80

90

100

110

120

2006 2007 2008 2009 2010 1Q11 2Q11 3Q11 4Q11

$/BBL$/BBL

Previous Forecast Latest Forecast Actual

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

What We See

We revise up average Dubai to $106, ranging $95-115/barrel on MENA unrest, pick up economic activities and more fund flows

2011 Dubai $106

29

Petroleum Market

30

Optimistic GRM …

On stronger summer demand

Driving season demand and low gasoline inventories in the US to draw Asian supplies

31

Q3-10 Q4-10 Q1-11 Q2-TD Q3-11 Q4-11

LPG ($/t) 613 798 860 923

MO-DB 8.6 10.6 12.6 15.7

JET-DB 12.8 14.3 20.3 21.6

GO-DB 12.4 13 18.4 20.7

FO-DB -4.8 -8.2 -8.7 -10.2

GRM 3.7 3.6 6.1

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

Global industrial & agriculture demand support diesel prices Japan power needs support

Mid distillates and fuel oil price

China suspended diesel export and will expect to import diesel during peak summer demand

Strong heating oil and kerosene demand during winter, supporting Mid distillates cracks in Q4

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

High sugar prices lead to a rally in ethanol prices in Brazil Consumers switched to use more gasoline Brazil imported a lot of gasoline cargoes from the US

US gasoline stocks fell sharply for the 11 straight weeks Arbitrage cargoes from South Korea and India to the US

Healthy regional demand from Indonesia and Vietnam Prompt demand from Malaysia due to refinery outage Limited exports from China and South Korea

Avg.06-09 09 10 11

Anhydrous Ethanol Brazil Price (R$/cbm) US Gasoline Inventory

Following the sell-off in US gasoline futures since May 11 US gasoline stocks rose for the first time in 12 weeks Concerns over US gasoline demand due to high prices

32

1.) Tight local supply as many refineries T/A for Euro IV tight-in

2.) Stabilized Economy & Better Projected Demand as Govt Supports

Growth ( %YoY) 2010 2011F

LPG 11% 15 %

MOGAS (-1.7%) Flat

JET/KERO 6.8% 4 %

GASOIL Flat 1 %

FUEL OIL (-1.8%) 2%

NGV 33.2% 30-35%

GDP Growth Forecast of 4.0 – 5.0 % YoY

Projected strong local investment, consumption and robust agricultural sector

Capped diesel price@30B/L & postponement of B5 enforcement boost further gasoil demand

Q1 Q2 Q3 Q4

33

A

B C,D

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

Aromatics

PARAXYLENE ….

Golden time comes to An End??

34

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

Chinese New Year

Japan Quake

PTA bring forward T/A

Product On Spec

Chinese credit tightening

Kuwait declared FM

A fire @ AMSB Malaysia

New PTAHanbang

35

Source: Consultants and Market

“ YTD 2011 spread is still healthy even it has been softened

currently but still high above 4-year average number.”

PX CFR – Naphtha J

4-year Avg = 412

Company Profile : S-OilLocation : Industrial complex Ulsan, Korea

Capacity Existing Additional -2011

Aromatics(KTPA)

PX-700BZ-100

PX-900BZ-280

“New PX PlantStart up = Apr 11Commercial = May 11”

20 May = 562

36

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

0200400600800

1000120014001600

Yisheng (Zhejiang)

Yisheng (Dahua)

Sanfanxiang

KTPA 2011 New Asian PTA Capacities Company Location PTA When

Yisheng (Zhejiang ) China 1,500 Jul-Aug ‘11

Yisheng (Dahua) China 500 Oct-Nov ‘11

Sanfanxiang China 1,500 Nov-Dec ‘11

Source: Consultants and Market

“Big PTA Plants come into the market. Supply is

expected to be tight in 2H2011 leading to

THE REAL GOLDEN YEAR”

Asia PX Supply / Demand 2011

Source: PCI_Apr 2011

37

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

Q3-10 Q4-10 Q1-11 Q2-TD Q3-11 Q4-11

PX-UG95 216 456 669 467

BZ-UG95 131 152 181 98

TL-UG95 56 91 39 20

S-Oil’s 900kta PX plant is expected to start in May-Jun 2011 Yisheng’s 1500kta PTA plant is expected to start in Jul-Aug 2011

Cut of Automotive production due to Japanese auto-part shortage reducing PS and ABS demand

7.5% polyester global production growth in 2011 (1% higher than 2010) Gasoline blending demand during driving season

Intensive credit tightening policy limits cash availability Power shortage during summer

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

…

38

Lube Base & Bitumen

39

Dearth of spot base oils

Force sellers to push selling prices

…

Thailand automobile producers forecast Q2’11 sales slip Recovery in global car sales remains on track

China plan to open to traffic 9,981 km within this year 30% growth from 2010 construction plan supported bitumen prices

Growing demand in other countries i.e. India, Thailand, Japan Slower demand from China as stimulus faded

Q3-10 Q4-10 Q1-11 Q2-TD Q3-11 Q4-11

500SN-FO 607 593 630 764

Bitumen-FO 46 -25 -97 -91

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

40

Conclusion

41

42

Q1-2011 Market Highlight Macro & Crude Petroleum Market Aromatics & Base Oil Conclusion

“Higher and volatile oil prices due to higher demand, fund flows and MENA unrests”

“Buoyant product spreads on strong regional demand, extra demand from Japan for

reconstruction and additional volumes from domestic market due to refinery shutdown”

“Supportive margin on strong demand from new PTA plants and bullish polyester growth, while

new Aromatics supplies are limited”

“Higher margin from TDAE unit while high base oil spreads support amid soft bitumen spreads”

500SN-FO 544 630 764

Bitumen-FO 21 -97 -91

PX-UG95 311 669 467

BZ-UG95 163 181 98

TL-UG95 86 39 20

MO-DB 10.3 12.6 15.7

JET-DB 12.1 20.3 21.6

GO-DB 11.5 18.4 20.7

FO-DB -5.7 -8.7 -10.2

Dubai 78.1 100.9 113.3

2010 2011

Q1 Q2 Q3 Q4

GRM* 3.3 6.1

GIM* 5.7 9.7

*TOP GRM & GIM excluding stock gain/loss

“ Buoyant GRM and GIM on strong middle distillates , supportive PX and Base Oil margins

and new LPG prices”

TOP Way Forward

43

movingtoward

TOP Group

Branding

44

Aromatics and Solvents:Asia Pacific’s leading

PX Exporter & Regional retailchemical solvent marketer

Lube base oil: Regional producer of high quality base oil

(Group II and III)

Ethanol:ASEAN’s top and

most cost competitive Ethanol player

Marine: PTT Group’s shipping needs provider and

operator

Refining:Asia’s leading

integrated refinery

Solutions:Take leading part in PTT Group’s Energy Solutions roadmapPower:

Shape PTT Group’s Power Portfolio

HRFinance•OperationsExcellence

TQASOURCE: TOP STS discussion

Financing capacity and discipline

CG CSR

HPO

Today

TDAE

GrII/III + Specialty PX Max

LAB / Benzene Derivative

VLCC 1

VLCC 2-3

SPP 2/3

Others UBE

Export Market

PTTES / TES

45

Investment Roadmap

476 M$

890 M$

2010 2011 2012 2013 2014 Total

Ethanol-SAP Ethanol-UBE 45

Fleet Expansion VLCC1 VLCCs 14/10 20

TDAE Specialty-WAX 25 20

Euro IV Gasoline 47

PX Upgrading 45

Refinery Upgrading - HCU Revamp & others 300

Benzene Derivatives: LAB/MDI 300

Lube Base: G. II/III 250

Power expansion 290

• Optimized utilization to achieve maximum profitability and improve margin through dynamic operational excellence and synergy with PTT group

• Refinery industry would be recovery gradually along with global growth, led by China & ME.• Aromatic business will improve especially in H2 when new PTA plants start up.• TOP implements and pursues investment options to grow its revenue as below:

Approved by BoDxxx

xxx Under study

Conclusion

46

47

Thank You

Any queries, please contact:

at email: [email protected]

Tel: 662-797-2999 / 662-797-2961

Fax: 662-797-2976

Appendices

48

49Source : Department of Energy Business, Ministry of Energy

Thailand LPG Demand

LPG Demand by Sector

LPG Demand Highlight

• LPG Demand in Q1 2011 grew 13.0% YoY

driven mainly by industry sector:

Household +8.2% YoY

Transportation +22.1% YoY

Industry +4.8% YoY

Petrochemical +21.8% YoY

Outlook 2011

• Expect 15% LPG demand growth in 2011, largely from petrochemical sector.

• LPG retail price continue to be capped in every sectors except industry sector which will be based on “CP Linked” in July 2011.

ML/Mth

221

7071

142

-

100

200

300

400

500

600

Jan

Mar

May Ju

l

Sep

No

v

Jan

Mar

May Ju

l

Sep

No

v

Jan

Mar

May Ju

l

Sep

No

v

Jan

Mar

May Ju

l

Sep

No

v

2008 2009 2010 2011

Petrochem

Industry

Transportation

Household

KT/Mth

904

816

932

500

600

700

800

900

1,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008

2009

2010

2011

50Source : Department of Energy Business, Ministry of Energy

Thailand Gasoline Demand

Gasoline Demand by Grade

Gasoline Demand Highlight

• Gasoline demand in Q1 2011 expanded 1.4%

YoY though pressured by higher retail price.

• Portion of gasohol & gasoline sales is

relatively maintained at around 60% : 40%

• Average ethanol replacement is 1.31

ML/Day currently

Outlook 2011

• Expects gasoline demand growth 0-1% in

2011 due to:

Higher retail gasoline price will continue

pressuring down demand which trigger

fuel switching

While strong private consumption index

doesn’t help supporting gasoline

demand

ML/Mth

232

205

156 18

-

100

200

300

400

500

600

700

800

JanMarMayJulSepNovJanMarMayJulSepNovJanMarMayJulSepNovJanMarMayJulSepNov

2008 2009 2010 2011

E20

GSH91

GSH95

ULR91

ULG95

ML/Mth

632

596

615

500

550

600

650

700

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008

2009

2010

2011

200

250

300

350

400

450

500

20,000

24,000

28,000

32,000

36,000

40,000

44,000

Jan

Mar

May

Ju

l

Sep

No

v

Jan

Mar

May

Ju

l

Sep

No

v

Jan

Mar

May

Ju

l

Sep

No

v

2009 2010 2011

mm

l /

mo

nth

# o

f a

irc

raft

# of Flights (lhs)

JP 1 Demand

JET Demand Highlight

• Jet consumption, which correlated with

number of flights, has increased

continuously since May 2010. JET fuel in Q1

11 growth was 10.3%YoY.

Outlook 2011

• Expect Jet demand growth in 2011 at 4%

back to normal level which is in align with

Thailand economic growth:

In addition, strong intra-region travelling

figures is another factor that could boost

up Jet fuel demand.

51Source : Department of Energy Business, Ministry of Energy

Thailand JET-A1 Demand

JET-A1 demand and # of flights

ML/Mth

472

425

464

250

300

350

400

450

500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008

2009

2010

2011

259259

290

0

50

100

150

200

250

300

350

Jan Mar May Jul Sep Nov

ML/Mth

2009 2010 2011

Gasoil Demand Highlight

• Gasoil demand in Q1 2011 slightly edged up at 0.4%YoY due to government’s policy to limit diesel price not to exceed 30 Baht/litre. (In March, diesel consumption largely grew 3.2% compared to Feb)

• Current Portion between B3:B5 is 60:40 and B100 replacement is ~ 1.55 ML/Day

Outlook 2011

• Expect modest gasoil demand growth at 1-2%

in 2011 due to:

Capped diesel price (tentatively till Sep

2011) supports demand and also strong

Thai Baht helps cap retail prices.

In addition, strong manufacturing sector

will help limit the loss.

However, if diesel price is floated, fuel

switching to NGV will depress gasoil

consumption.Source : Department of Energy Business, Ministry of Energy

Thailand Gasoil Demand

Rising Trend of NGV Demand

52

ML/Mth

1,624

1,492

1,705

1,200

1,300

1,400

1,500

1,600

1,700

1,800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008

2009

2010

2011

Fuel Oil Demand Highlight

• FO demand in Q1 2011 contracted 16.3%

YoY owing to reduction in every sector

especially electricity area as there were

fewer power plants’ NG disruptions.

Outlook 2011

• Expect better Fuel Oil demand growth 3-5%

in 2011 due to:

Fuel switching from LPG to Fuel Oil

owing to floating LPG retail price of

industrial sector.

Economic growth supported bunker

usage

In addition unexpected natural gas

supply disruption to power, causing

prompt FO demand in power plants

Source : Department of Energy Business, Ministry of Energy

Thailand Fuel Oil Demand

Thailand Fuel Oil Demand by Sector

53

ML/Mth

90 79 15 23

-50

100 150 200 250 300 350 400 450 500

Jan

Mar

May Ju

l

Sep

No

v

Jan

Mar

May Ju

l

Sep

No

v

Jan

Mar

May Ju

l

Sep

No

v

Jan

Mar

May Ju

l

Sep

No

v

2008 2009 2010 2011

Others & Article 10Electricity

Industry

Transportation

ML/Mth

184 210207

100

150

200

250

300

350

400

450

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008

2009

2010

2011