22

> Market Update February 2015 Michael Fazzini Multi Asset Group

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | clarence-craig |

| View: | 217 times |

| Download: | 1 times |

> Market Update

February 2015

Michael FazziniMulti Asset Group

// 2

Economic and investment outlook

> Okay but uneven global growth – 2013: 3.0%, 2014: 3.5%, 2015: 3.5%

> Australian growth to pick up on a more sustainable basis over the year ahead

> Interest rates to remain low, with the RBA cutting rates again

> The $A is headed towards $US0.75, with the risk of an undershoot

> Bonds and term deposits offer low returns

> Cyclical bull market in shares is likely to continue, but expect more volatility

> Key risks: the first Fed rate hike; problems with energy producers; Greece;

China

Source: AMP Capital

// 3

// 4

4

2014 saw another year of solid returns

Source: Thomson Reuters, AMP Capital

0

5

10

15

20

25

30

35

40

45

50

Austequities

Int'l equities($A)

Int'l equities(local)

Aust bonds Globalbonds

Aust listedproperty

Global listedproperty

Directproperty

Cash

Percent return *

* pre fees and taxes.

2013

2014

6%

15%

10% 10% 10%

27% 28%

2.7%

9%

// 5

Global business conditions point to okay global growth, but no boom

Source: Bloomberg, AMP Capital

Global Manufacturing PMI averageManufacturing PMI’s

-1%

0%

1%

2%

3%

4%

5%

6%

35

40

45

50

55

60

05 06 07 08 09 10 11 12 13 14

Global Manufacturing PMI (LHS)

World GDP growth (RHS)

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

70

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

US PMI (LHS)

Japan PMI (LHS)

European PMI(LHS)

China PMI (RHS)

India PMI (RHS)

Brazil PMI (RHS)

// 6

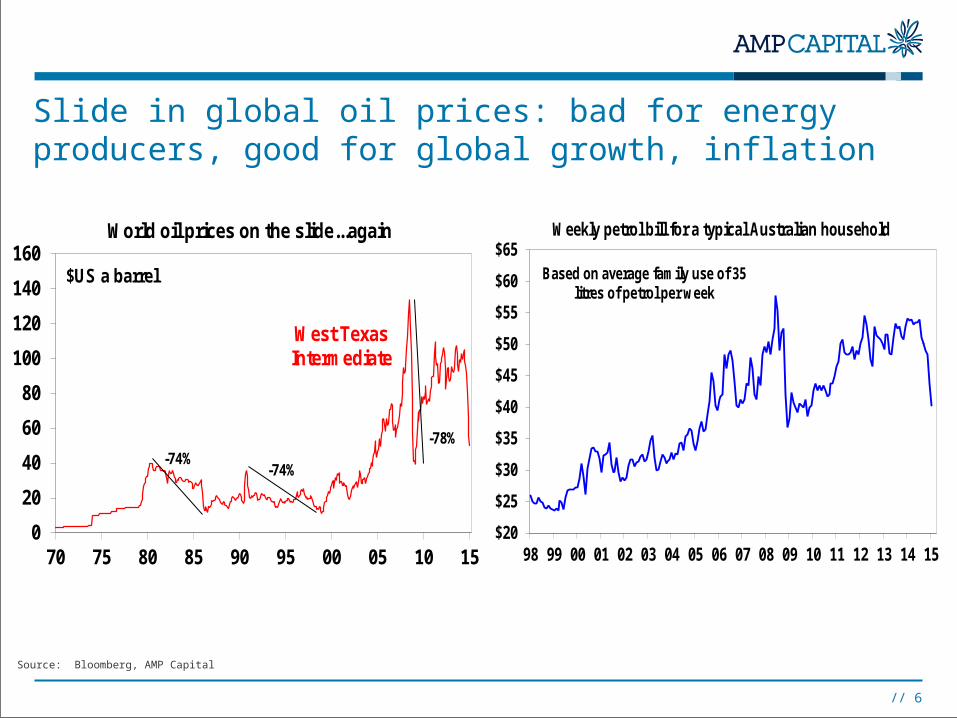

Slide in global oil prices: bad for energy producers, good for global growth, inflation

Source: Bloomberg, AMP Capital

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Based on average family use of 35 litres of petrol per week

Weekly petrol bill for a typical Australian household

0

20

40

60

80

100

120

140

160

70 75 80 85 90 95 00 05 10 15

World oil prices on the slide...again

West Texas Intermediate

$US a barrel

-78%

-74%-74%

US economic growth is good

Source: Thomson Reuters, AMP Capital

// 7

-5

-3

-1

1

3

5

7

30

40

50

60

70

00 02 04 06 08 10 12 14

Manufacturing conditions PMI (LHS)

US GDP growth (RHS)

Annual % change

// 8

Source: The Economist, AMP Capital

The Eurozone recovery has faltered – but the ECB is providing more support

Source: Bloomberg, AMP Capital

// 9

30

35

40

45

50

55

60

65

-6

-4

-2

0

2

4

6

00 02 04 06 08 10 12 14

Manufacturing conditions PMI (RHS)

European GDP growth (LHS)

Annual % change

The Japanese economy should bounce back, helped by even more aggressive BoJ stimulus

Source: Bloomberg, AMP Capital

// 10

30

35

40

45

50

55

60

65

-7

-5

-3

-1

1

3

5

7

04 06 08 10 12 14

Annual % change

Manufacturing conditions PMI (RHS)

Japan GDP growth (LHS)

Chinese data is running “hot and cold”, but consistent with growth “around 7.5%”. The main risk is the property downturn

Source: Thomson Reuters, AMP Capital

// 11

38

42

46

50

54

58

62

66

5

6

7

8

9

10

11

12

13

14

05 06 07 08 09 10 11 12 13 14

Chinese real GDP growth (LHS)

Chinese PMI manufacturing

conditions indexes,

smoothed (RHS)

Annual % change

Chinese growth down from last decade

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

-6

-4

-2

0

2

4

6

8

10

12

14

05 06 07 08 09 10 11 12 13 14

Property price falls sharper than 2008 and 2011

new data

Monthly % [RHS]

Annual % change [LHS]

70 city property prices

Interest rates likely to remain low, with another RBA rate cut likely and the Fed unlikely to start tightening till mid year

Source: Thomson Reuters, AMP Capital

// 12

0

1

2

3

4

5

6

7

8

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Australia

Europe

Japan

US

Interest Rates %

// 13

Fed monetary tightening is not always bad for shares – US shares before and after first Fed rate hikes, %

Hike -6 mths -3mths +3mths +6mths +12mths +24mths*

Oct 80 19.9 4.8 1.6 4.2 -4.4 2.4

Mar 84 -4.1 -3.5 -3.8 4.3 13.5 22.5

Nov 86 0.8 -1.5 14.0 16.4 -7.6 4.8

Mar 88 -19.6 4.8 5.6 5.0 13.9 14.6

Feb 94 7.5 2.9 -6.4 -4.9 -2.3 14.9

Mar 97 10.2 2.2 16.9 25.1 45.5 30.3

Jun 99 11.7 6.7 -6.6 7.0 6.0 -5.6

June 04 2.6 1.3 -2.3 6.2 4.4 5.5

Average 3.6 2.2 2.4 7.9 8.6 11.2

* % pa

Source: Thomson Reuters, AMP Capital

// 14

Source: Thomson Financial, AMP Capital

The Australian economy – mining investment slowing but there are signs of life elsewhere in the economy

Mining investment looks to have peaked

…which should help boost retail sales… …and then eventually non-mining investment

But dwelling construction is looking up…

0

1

2

3

4

5

6

7

8

9

10

49/50 59/60 69/70 79/80 89/90 99/00 09/10

Non -Mining investment as % GDP

Forecast

0

1

2

3

4

5

6

7

8

49/50 59/60 69/70 79/80 89/90 99/00 09/10

Mining investment as % GDP

Forecast

8

10

12

14

16

18

20

90 92 94 96 98 00 02 04 06 08 10 12 14

(dwelling approvals, monthly '000s)

-5%

0%

5%

10%

15%

90 92 94 96 98 00 02 04 06 08 10 12 14

Retail Sales % yoy

Share markets are generally cheapShare market valuation indicators

Source: Thomson Reuters, AMP Capital

// 15

-4

-3

-2

-1

0

1

2

3

489 91 93 95 97 99 01 03 05 07 09 11 13

Australia

Expensive

Cheap

-4

-3

-2

-1

0

1

2

3

491 93 95 97 99 01 03 05 07 09 11 13

Europe

Expensive

Cheap

-4

-3

-2

-1

0

1

2

3

495 97 99 01 03 05 07 09 11 13

USA

Expensive

Cheap

-4

-3

-2

-1

0

1

2

3

489 91 93 95 97 99 01 03 05 07 09 11 13

Japan

Expensive

Cheap

US shares are at record highs, but underpinned by record profits – much more than just quantitative easing

// 16

Source: Bloomberg, AMP Capital

0

20

40

60

80

100

120

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

90 92 94 96 98 00 02 04 06 08 10 12 14

US S&P 500 (LHS)

US earnings per share (RHS)

The challenge for investors – how to find better yield and returns as bank deposit rates stay low

Source: RBA, Bloomberg, AMP Capital

// 17

2

3

4

5

6

7

8

9

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Percent

Average bank 1 yr term deposit rate

Average bank 3 yr term

deposit rate

Official cash rate

// 18

With interest rates & bond yields remaining very low the “search for yield” is likely to go further

Source: Thomson Reuters, AMP Capital

// 18

0

2

4

6

8

10

12

14

16

18

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14

10 year bond yield

Avg yield on office, industrial and retail

property

Australian property yields v bond yield

Avg residential property yield

The $A is likely to fall to around $US0.75, with the risk of an undershoot

Source: Bloomberg, AMP Capital

// 19

The $A remains high compared to levels suggested by relative prices

Short positions in the $A are building suggesting the risk of a short term bounce

-100,000

-80,000

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Net speculative positions in AUD

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

$US per $A, at June each year

Purchasing power parity implied level (based on relative consumer prices)

Latest

Page 20 |

“Bull markets are born

on pessimism, grow on

scepticism, mature on

optimism and die of

euphoria”.

John Templeton

// 21

Important note

While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts.

Past performance is not a reliable indicator of future performance.

This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs.

This document is solely for the use of the party to whom it is provided.

// 21

// 22

The power of compound interest

Bought for 10 cents in 1938 and sold for $3.2m in 2014…a compound return of 25.5% pa!

Source: AMP Capital Investors