THE INFLUENCE OF BASEL CAPITAL ACCORD AND GOOD CORPORATE GOVERNANCE IMPLEMENTATION TOWARD CREDIT RISK MANAGEMENT IN INDONESIAN BANKING LISTED ON INDONESIAN STOCK EXCHANGE Ajeng Andriani Hapsari a and John Henry Wijaya b a Faculty of Business and Management, Widyatama University, Indonesia [email protected]b Faculty of Business and Management, Widyatama University, Indonesia [email protected]ABSTRACT The Purpose of this research is to examine the influence of Basel Capital Accord and Good Corporate Governance on Credit Risk. A case study of Indonesian bank period 2011-2016. This research type is a descriptive and verification with purposive sample techniques. Collecting data method used data panel model. The result of this research show that minimum capital ratio, capital need calculation, market risk, credit risk and good corporate governance have positives but not significantly influence. The results find capital adequacy ratio have negative influenced and not significant. In conclusion, operational risk that influence credit risk management in banking industry. Keyword: Basel Capital Accord, Good Corporate Governance, Banking, Credit Risk Management

Transcript

THE INFLUENCE OF BASEL CAPITAL ACCORD AND GOOD CORPORATE GOVERNANCE IMPLEMENTATION TOWARD CREDIT RISK MANAGEMENT

IN INDONESIAN BANKING LISTED ON INDONESIAN STOCK EXCHANGE

Ajeng Andriani Hapsaria and John Henry Wijayab

aFaculty of Business and Management, Widyatama University, [email protected]

bFaculty of Business and Management, Widyatama University, [email protected]

ABSTRACTThe Purpose of this research is to examine the influence of Basel Capital Accord and Good Corporate Governance on Credit Risk. A case study of Indonesian bank period 2011-2016. This research type is a descriptive and verification with purposive sample techniques. Collecting data method used data panel model. The result of this research show that minimum capital ratio, capital need calculation, market risk, credit risk and good corporate governance have positives but not significantly influence. The results find capital adequacy ratio have negative influenced and not significant. In conclusion, operational risk that influence credit risk management in banking industry.

Keyword: Basel Capital Accord, Good Corporate Governance, Banking, Credit Risk Management

I. INTRODUCTION

Bank is a company conducting intermediation function on fund received by clients and then redistribute it in the form of credit or other types of funding. Fund distribution in the form of credit is expected to increase industrial development on real sector, so that it could support the nation’s economic development (Banker Association for Risk Management, 2012). Should a bank failed, the impact it caused will spread and affect many things. One of it is the impact on their clients, and institutions which deposit their fund in such bank, not only where such bank is domiciled but also in the international market. Due to the importance of bank in conducting such function, and to protect clients from occurring problems, a strict regulation must be upholding to supervise the daily operational activities of such bank. One of the basic regulations is regulation regarding bank capital and good corporate governance.

In conducting its business activities, bank faces many risks such as credit risk, market risk, operational risk, liquidity risk, law risk, strategic risk, compliant risk and reputation risk. With many provisions regulating the banking industry to protect public interest, which including provision to regulate that bank must meet the liability of existing minimum capital according to the condition of each bank to make banking sector into a “highly regulated” industrial sector. Considering such importance, in 1988 BIS (Bank for International Settlements) in Switzerland issued a capital framework concept known as “The 1988 Accord” or Basel I and is applied internationally which is only calculating credit risk, so that bank is required to have a minimum capital reserved of 8%. With the passing of time and the development of banking products, BIS issued a new capital framework which is Basel II which is made to be more sensitive toward risk (Risk Sensitive) and provide incentive to the increase of risk management quality in bank consisting of 3 pillars which are Regulatory Capital, Supervisory Review and Disclosure.

Implementation of Basel II is focusing more on the risk management quality improvement on every risk profile considered as banking risk control by the bank (Bank for International Settlement, 2005). However, it does not omit the possibility of obstacles to be faced by Indonesian banks both directly and indirectly shall impact on the effectiveness of risk management implementation.

The banking internal and external environment which rapidly develops and also bank’s complex business activities demand banking to implement adequate risk management and discipline in its implementation (Banker Association for Risk Management, 2012). One real support from Bank of Indonesia on Risk Management is that banking in Indonesia must apply Basel II since 2010 which is expected to increase the process and also supervision especially in seeing the soundness level of bank, financial system stability through risk management as well as such banking capital adequacy, is an absolute requirement for banking industry to be well developed. One of them is to implement Good Corporate Governance.

Implementing Good Corporate Governance is one mean to regain public trust on banking industry by restructuring and recapitulation which will provide a basic long-term effect alongside with three important actions which are compliant to prudence principles, implementation of Good Corporate Governance, effective supervision by Bank Supervisory Authority. So that BIS, as Institution continuously review prudence principles which must be obeyed by banks, also issued Guide of GCG Implementation for International banking. GCG regulation and implementation need commitment of Top Management and organization ranking, which its implementation is start by stipulate Strategic Policy and code of conduct which all parties in a company must obeyed; for Indonesian banking, compliant to the code of conduct which is realized in words and actions, is an important factor as base implementation of GCG.

If the management in a banking company is inadequate, and credit distribution to a group or business group is stimulating high risk of bad credit in a company and also high level of business complexity, this will give rise to the risk faced by bank and capital which are not able to cover the risks faced by such bank, and in turn will reduce the bank’s performance. Credit risk is one of many risks faced by bank. Credit risk is a risk rise due to client’s failure to meet its obligations. Indicator use is NPL (Non-Performing Loan), a comparison between problematic credits with total credit provide by bank to debtor.

Credit risk is a risk which always triggers problems in banks all over the world. Therefore, credit risk must be well managed. Bank must manage the exposure of overall portfolio credit and also risk of each debtor as well as credit transaction. Bank must also pay attention on the relation between credit risk and other risks, and the changes on economic conditions and other environments which may affect the decline of credit quality (Basel committee, 2000)

One effort to minimize risk is that a bank must conduct its function with prudence. Therefore, each bank is obliged to implement Basel Capital Accord and Good Corporate Governance so that it able to control and minimalize arising risk so that it could be anticipated and find its solution.

II. LITERATURE REVIEW AND PREVIOUS STUDIES

A. Basel Capital Accord

Basel Committee for Banking Supervision’s purpose is to strengthen the soundness and stability of international bank’s system, as well as creating a consistent and just basic framework for banks in various countries with different resources actively conducting international banking operational activities. In 1988 Basel Committee issued a capital adequacy framework for G-10 countries with international active business such as Belgium, Canada, France, German, Italy, Japan, Netherlands, Sweden, Switzerland, Luxembourg, England and United States (Frindh, McGregor & Westman, 2006). Such capital adequacy framework is name “Basel Capital Accord” or known as Basel I, which required bank capital adequacy by only calculating credit risk. The goal is to calculate international banking stability and create consistency in its implementation to various countries.

In line with bank’s business development, Basel Committee for Banking Supervision once again perfected bank’s capital adequacy framework. 20 years after the issuance of Basel I, Basel II starts its implementation. Basel II is aiming to improve security and soundness of financial system by focusing on capital calculation with risk base, supervisory review process and market discipline (Frindh, McGregor & Westman, 2006).

B. Good Corporate Governance

Good Corporate Governance is a mechanism used to regulate and manage business, improve company’s performance, and to improve trust of investor (Arafat, 2010). The purpose of GCG implementation in bank is to create added value for stakeholders as form to realize a sound banking (Priambodo and Supriyatno, 2007:89). Assessment of GCG factors is assessment on bank management quality in conducting GCG principles by displaying significance level or materiality of a problem toward GCG implementation according to scale, characteristics and complexity of a bank’s business (SEBI No.15/15/DPNP dated 29 April 2013). Parameter conducted is in accordance with Circular Letter of Bank of Indonesia

No. 15/15/DPNP of 2013 where bank must us self-assessment method as parameter to assess GCG. Below is the classification of composite predicate being use:

Table 1. GCG Self-Assessment Composite ValueComposite Value Composite Predicate

Composite Value < 1,51,5 < Composite Value < 2,52,5 < Composite Value < 3,53,5 < Composite Value < 4,54,5 < Composite Value < 5

Very GoodGood

AdequatePoorBad

Source: SEBI Attachment No.9/12/DPNP (30 May 2007)

Bank with low GCG composite value will display a very good quality of a company’s management (Suciati, 2015). The better the GCG implementation is conducted, the higher the company’s ability to earn profit (Tjondro & Wilopo, 2011).

According to Bank of Indonesia Regulation pursuant to decree No. Kep-117/M-MBU/2002 dated 21 July 2002, Good Corporate Governance is bank’s management conducting the principles of Transparency, Accountability, Responsibility, Independency and Fairness (TARIF).

C. Risk ManagementIn the world of economy, risk is identified as probability of loss. There are two types of

loss potential, which are expected loss and unexpected loss. Expected loss is the base to create loss reserve in a company which may be burdened as one component in stipulating credit risk rate; while unexpected loss is used by bank to determine capital need should such loss potential occurred.

Activity which is the highest source of credit risk is the activity of credit distribution by bank. Meanwhile, credit risk is also found in many activities and other financial instruments such as transaction between bank, trade financing, and currency transaction (Basel Committee, 2000).

Credit risk management implementation is a series of procedure and methods conducted by bank so that it could minimize the occurrence of credit risk. The measurement of bank’s credit risk generally use is the Non-Performing Loan (NPL), credit percentage with performing quality, is doubted and non-performing to the overall bank credit (Bank of Indonesia, Indonesia Banking Statistic). Almost all research on bank failures, find that prior to failure, bank has high level of NPL. Therefore, NPL become the most important parameter to measure bank’s soundness (Bank & DeYoung, 1997). By referring to SEBI No. 5/21/2003, parameter used to measure credit risk management is NPL which shows comparison of number of bad credit on the total credit issued by bank.

Modal Inti & Pelengkap

CAR Risiko Kredit &

Operasional

Market Risk

Credit Risk

Operasional Risk

GCG

CAR

Manajemen Resiko Kredit

BASEL

CAPITAL

ACCORD

H1

H2

H3

H4

H5

H6

H7

H8

Image 1. Framework of Effect between Basel Capital Accord, Good Corporate Governance on the Credit Risk Management

III. RESEARCH METHODS

A. Research Design

This research use hypothesis through data process and test statistically by analysis of descriptive-verificative which the result of this research is useful to find the characteristics of company in the sample so that good bias conclusion shall be achieved. Further, a classic assumption test to find model appropriateness of used regression. Test of multivariate analysis by using multiple regression method to examine the effect of independent variables toward dependent variable. All tests in the research is using significance level of 5%.

B. Data and Sample

The sourced of used data is from secondary data of each bank’s financial statements set by method of purposive sampling which is one non probability sampling method from banking companies listed in Indonesia Stock Exchange in the period of 2011-2016 by using data panel method. The general form of data panel regression model may be formulated in the following equation:

Yit = α + β1 X1it + β2X2it + uit Description:i = 1,2,3…n (amount of observation) cross section dimensiont = 1,2,3…t (time) time series dimensionYit = dependent variable on unit i and time tα = constantβ = constant from independent variable on time t and unit iuit = error

Sample is chosen based on the following criteria:1. Public bank registered in the Indonesia Stock Exchange2. Banking company publishing periodical complete financial statements and annual

reports for period ended on 31 December during observation period of 2011-20163. IPO (initial Public Offering) less than 5 years is not chosenData panel method combining cross section data and time series data resulted in 156

observations which are gained through multiplication result of population number of 26 banks with observation period of 6 years.

C. Operationalization of Research Variable

Dependent Variable

Credit Risk ManagementCredit risk management in this matter is proxied into NPL (Non-Performing Loan) which is the level of credit repayment given by depositor to bank, in general NPL is called bad credit, which is one key indicator to assess bank’s function performance. One of the functions is as intermediary institution or intermediary between party with excess fund and party who needs funding. Bank of Indonesia through its Regulation stipulates that the ratio of non-performing loan is 5%.

x 100%

Independent Variable

Independent variable in the research is Minimum Capital Ratio (X1), CRKO (X2), Market Risk (X3), Credit Risk (X4), Operational Risk (X5), Capital Need Calculation (X6) and GCG (X7).

The first independent variable is Minimum Capital Ratio or Solvency Ratio determined by 2 components which is:

- Risk weigh of Bank Asset is all banks’ exposure changes into assets and then each exposures is multiply by supervisor risk weight based on its risk level.

- 2 minimum ratios or limit related to regulatory capital with risk weight from asset:

o Total regulatory capital is divided with total asset risk weight must be higher or equal to 8%.

o Tier 1 capital or core capital having bigger capacity to absorb loss at any time is divided with total asset risk weight must at least equal to 4%.

The requirements of minimum regulatory capital are created based on 2 components:1. Definition of regulatory capital – list of elements including capital for regulatory capital

and conditions which must be met by such elements to be able to calculated as capital.2. Risk weight from asset is all exposures after converted into asset and has obtained risk

weight from supervisor based on its risk level.

Image 2. Formulation of Minimum Total Capital Ratio and Minimum Tier One RatioSource: www.bi.go.id

Calculation of Capital NeedIn Basel II, it is required that bank must reserve capital of 8% on weighted asset according to risk, which is calculated by using the following formulation:

Market RiskSince 1 January 1998, banking in G 10 countries is required to provide capital to cover

market risk (this matter referred to market risk amendment from Basel Accord). Requirements of bank capital for market risk is stipulated by using two methods: Standardised approach, adopting what is known as “building bock” for transaction related to interest rate and equity instrument which differentiate capital expense for specific risk from general market risk.

Internal model approach enable bank to use self-developed method which must meet the qualitative and quantitative criteria stipulated by Basel Committee and by reference of approval from supervisory authority. Internal model approach specifies capital expense higher than VaR of previous data or average daily VaR during 60 days period multiply with three minimum factors. Bank must calculate VaR value based on daily value with:- One-tailed confidence interval of 99%- Minimum holding period of 10 days- Minimum observation period of one year

Internal model used by bank must accurately cover certain risks related with option and instrument as option.

Based on standardised approach, bank allocated one risk weight for each asset and off-balance sheet posts generating amount of total weight asset according to risk as follow:

ATMR = Amount of exposure x risk weightAllocation of each risk weight based on general category from debtor, be it government, bank or company which then reclassified with rating given by external institution of credit rating.

Operational RiskOperational risk defined by Basel Committee as “direct or indirect risk sourced from

the incapability or failure of internal process, persons and system as well as external event”. There are three approaches in determining capital expense for operational risk:- Basic Indicator Approach determines capital expense for operational risk of certain

percentage (“alpha factor”) from gross income used as estimation on bank risk exposure. In this approach, the capital which must be allocated to loss from operational risk is equal to certain percentage from average annual gross income for three years period.

- Standardise Approach requires an institution to separate its activities into eight line of standard business, for example retail banking, corporate funding and others. Capital expense for each business line is calculated by multiplying gross income for each business line with a number (“beta”) which is determined for each business line. Beta number will be different for each business line.

- Advanced Measurement Approach in this approach the calculation of capital need will be the same with risk measurement resulted from operational risk measurement system which is internally used by bank. Bank must fulfil the qualitative and quantitative criteria as stipulated in Basel II and must be approved by supervisor.

Capital Adequacy Ratio (CAR)Capital Adequacy Ratio is capital adequacy showing bank’s capability in maintaining adequate capital and bank’s management ability to identify, measure, supervise and control risks affecting the amount of capital. CAR ratio also shows how far of all bank’s assets containing risk such as credit, security investments, invoice to other bank, etc, is also funded from bank self-capital fund aside from obtaining funds from external source such as public fund, loan (debt), and other (Dendawijaya, 2003). CAR is calculated through the following formulation:

x 100%Description:Capital = consists of core capital and complementary capitalATMR = risk weighted assets

Good Corporate Governance (GCG) is an independent variable that is composite value or self-assessment which is the assessment of company management implementation based on 7 dimension of GCG: company management commitment, board of commissioners’ management, functional committees, board of directors, treatment to shareholders and other stakeholders, and transparency, independency integrity of other shareholders interest based on equality and fairness principles.

D. Analysis Method

Multiply Linear Regression AnalysisAccording to Ghozali (2005) to test effect model and relation of independent variable

of more than two variables toward dependent variable, multiple liner regression method is used. Test will be executed using multiply regression model as follows:

CRMi,t= α + β1RMMi,t + β2PKMi,t + β3MRi,t + β4CRi,t + β5ORi,t + β6CARi,t + β7GCGi,t + εDescription: CRMi,t = Credit Risk Management of company i on t periodα = Constant coefficientβ1-9 = Regression coefficient variableRMMi,t = i Minimum Capital Ratio on t periodPKMi,t = Perhitungan Kebutuhan Modal perusahaan i pada periode tMRi,t = Market Risk of company i on t periodCRi,t = Credit Risk of company i on t periodORi,t = Operational Risk of company i on t periodCARi,t = Capital Adequacy Ratio of company i on t periodGCGi,t = Good Corporate Governance of company i on t period (self-assessment)ε = error

In the research, CRM variable become dependent variable describing level of Credit Risk Management, meanwhile main independent variable consist of RMM, PKM, MR, CR, OR, CAR and GCG. The above research model will be estimated with help from statistic program of Eviews7. To see ability contribution in describing independent variable collectively toward dependent variable which is observed through R2

determination coefficient, in this matter using Adjusted R2. This is due to Adjusted R2 is better compared to R2. Adjusted R2 which value is getting close to 1 is an indicator which displays stronger ability in describing changes of independent variable toward dependent variable.

IV. FINDINGS AND DISCUSSION

Research object used in the research is banking companies listed in the Indonesia Stock Exchange in the period of 2011-2016. From 43 banking companies, only 26 banks meet the stipulated sampling criteria.

To obtain best and maximum model for research using data panel, a series of test must be conducted through 3 alternatives, which are:

1. Pooled Least Square Method or Common Constant2. Fixed Effect Method (FEM) 3. Random Effect Method (REM)

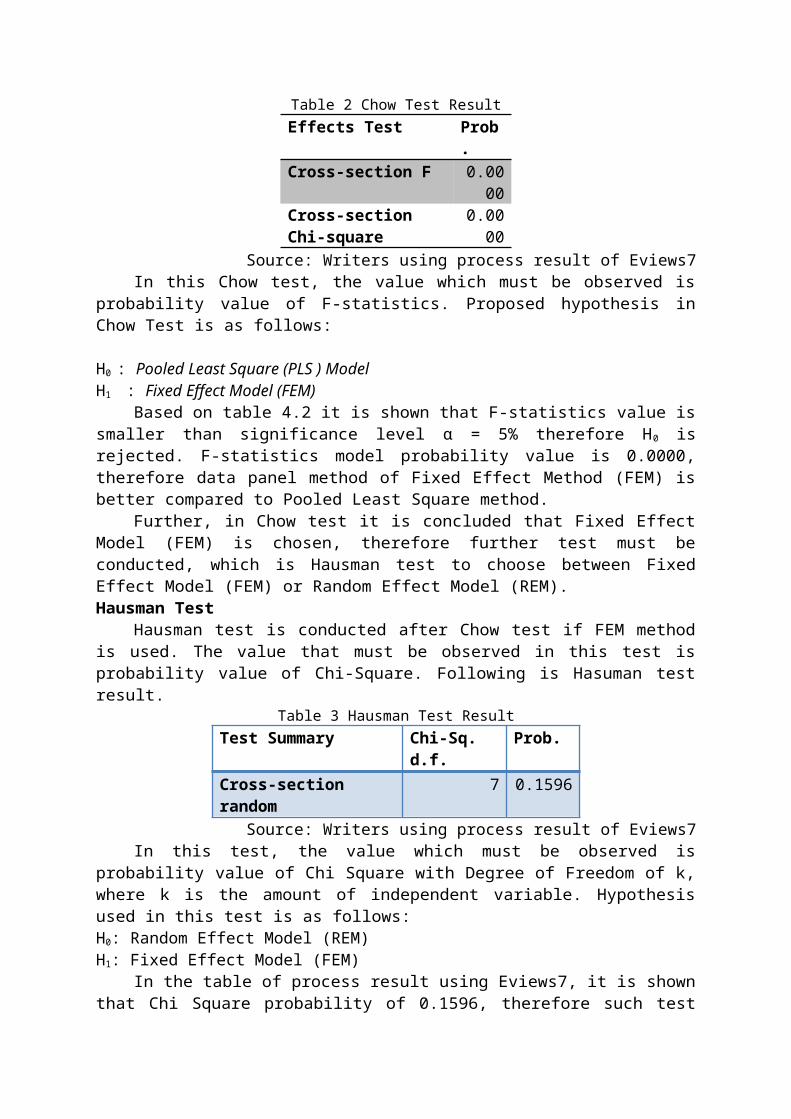

Chow TestChow test is conducted to choose best model between Pooled Least Square (PLS)

and Fixed Effect Method (FEM). The test is conducted by observing F-stat value from Chow test as follows:

Table 2 Chow Test ResultEffects Test Prob. Cross-section F 0.0000Cross-section Chi-square

0.0000

Source: Writers using process result of Eviews7 In this Chow test, the value which must be observed is probability value of F-

statistics. Proposed hypothesis in Chow Test is as follows:

H0 : Pooled Least Square (PLS ) ModelH1 : Fixed Effect Model (FEM)

Based on table 4.2 it is shown that F-statistics value is smaller than significance level α = 5% therefore H0 is rejected. F-statistics model probability value is 0.0000, therefore data panel method of Fixed Effect Method (FEM) is better compared to Pooled Least Square method.

Further, in Chow test it is concluded that Fixed Effect Model (FEM) is chosen, therefore further test must be conducted, which is Hausman test to choose between Fixed Effect Model (FEM) or Random Effect Model (REM).Hausman Test

Hausman test is conducted after Chow test if FEM method is used. The value that must be observed in this test is probability value of Chi-Square. Following is Hasuman test result.

Table 3 Hausman Test ResultTest Summary Chi-Sq. d.f. Prob. Cross-section random 7 0.1596

Source: Writers using process result of Eviews7 In this test, the value which must be observed is probability value of Chi Square with

Degree of Freedom of k, where k is the amount of independent variable. Hypothesis used in this test is as follows:H0: Random Effect Model (REM)H1: Fixed Effect Model (FEM)

In the table of process result using Eviews7, it is shown that Chi Square probability of 0.1596, therefore such test result is not significant due to p-value is higher than 5%, so that H0 is accepted and H1 is rejected. Therefore, the model used in the research is to follow Random Effect. The provision applied to Hausman test is if Hausman statistic value is smaller than its critical value then the accurate model is to use Random Effect Model (REM).

Source: Gujarati, Basic EconometricsImage 2 Summary of Model Choice Result

PLS Method

Chow Test

Fixed Effect Method

Fixed Effect Method

Hausman Test

Random Effect Method

Random Effect Method

Data Panel Regression Model Test ResultTable 4 Data Panel Estimation with Random Effect Model

Variable Coefficient Std. Error t-Statistic Prob.

C 0.731768 0.427210 1.712899 0.0888MIP 1.78E-14 1.01E-14 1.760720 0.0804

CAR -1.230041 2.074839 -0.592837 0.5542GCG 0.121216 0.133866 0.905503 0.3667

Effects SpecificationS.D. Rho

Cross-section random 1.047569 0.6906Idiosyncratic random 0.701204 0.3094

Weighted Statistics

R-squared 0.095064 Mean dependent var 0.223334Adjusted R-squared 0.052263 S.D. dependent var 0.728859S.E. of regression 0.709557 Sum squared resid 74.51371F-statistic 2.221059 Durbin-Watson stat 1.107434Prob(F-statistic) 0.035614

Unweighted Statistics

R-squared 0.070280 Mean dependent var 0.847243Sum squared resid 255.9764 Durbin-Watson stat 0.322370

value shows how big the difference of random error component of a company toward intercept value of all companies (average).

Other information from regression analysis result is: R-squared = 0.731768; shows the model ability, independent variable is able to

describe its effect of 73.71% toward the research dependent variable. Adjusted R-squared = 0.095064; is adjusted R2 value. The more independent variable

included into equation, the smaller the value. S.E. of Regression = 0.709557; is standard error of regression equation. In the

research, the standard error of it regression is relatively low of 7.01%. Sum squared residual = 74.51371; is the amount of residual square value of the

research. Durbin-Watson stat = 1.107434; Durbin-Watson (DW) test value used to find out

whether or not autocorrelation (relation between residual) is exist. Mean dependent var = 0.728859; is standard deviation shows the standard deviation

toward Y variable. F-statistic = 2.221059; simultaneous test the effect of all independent variables

toward dependent variable.

Prob (F-statistic) = 0.035614; probability F statistic test value.

Test Result of Hypothesis and StatisticStatistic model test is related with criteria statistic used to see how good the model or

variable being used in a research. Statistic criteria depend on several value or parameter tested with statistic test. Following is statistic criteria being used:

Determination Coefficient R2 and Adjusted R2

R2 value is the value showing how well regression model used in the research. According to Nachrowi and Usman (2006), R2 is useful to measure the proximity between prediction value and real value of dependent variable. R2 value is between 0< R2<1. If it is near zero (0), then dependent variable cannot be described by independent variable used in the research. Vice versa, if it is close to 1, regression model used is better. Meanwhile Adjusted R2 is aimed to strengthen prediction data of a model.

Table 5 R2 Value and Adjusted R2

R-squared 0.095064Adjusted R-squared 0.052263

Source: Writers using process result of Eviews7 Based on the above table it is shown that R2 is 9.5% which means that risk

management as dependent variable in this research can be explain of 78.03% by model. While 90.5% is explained by other factors outside model. Independent variables in the research is Minimum Capital Ratio, Capital Need Ratio, Market Risk, Credit Risk, Operational Risk, Capital Adequacy Ratio and Good Corporate Governance, are able to describe its effect of 9.5% toward dependent variables.

The remaining of 90.5% is explain by other factor not included in the research regression model. As written by Penza and Bansal, 2001 that credit risk may occurred on unsecured loans, bonds/notes on derivative products which transactions is conducted unorganized (such as swaps, forwards, and derivative products over the counter). Credit risk is more as loss risk due to failure of counterpart in conducting payment according to agreement. While Crouhy, Galai and Mark (2001, pg 35) states that credit risk is risk when changes of counterparty credit quality can affect bank’s position value. In other research, Pagach an Warr (2010) write that risk management is affected by financial performance variable such as leverage, return on equity, financial stack, opacity, market to book ratio, duration ratio and loan loss provision.

Adjusted R2 is adjusted R2 value. As more of independent variable being used in the equation, it will reduce this R2 value (Rohmana, 2010). In the research, Adjusted R2 of 0.052263 may be generally translated that the ability of model to explain variation of Credit Risk Management is 5.22%. To handle R2 weakness, Henry Theil suggested by observing Adjusted R2. In conclusion, the higher Adjusted R2 value, the better the model.

Multiply Linear Significance (F-stat)Nahrowi and Usman (2006) state that F-Test is aimed to conduct coefficient

hypothesis (slope) regression test simultaneously. Following is the summary of F test on table 4.5:

2,221059 0.035614 Significant* H0 rejectedNotes: *shows significance level of 1%

Source: Writers using process result of Eviews7

Based on table 6 it can be explained that F-stat value is 2.221059 with 0 probabilities. This shows that such value is on confidence level of 99% or categorized as highly significant, due to having significance value of 0.035614 < 0.05. If F significance level is smaller than 0.05 then alternative hypothesis is rejected and contrary, if F significance level is bigger than 0.05 then alternative hypothesis cannot be rejected.

In the research, F test purpose if to test the effect of Minimum Capital Ratio, Capital Need Calculation, Market Risk, Credit Risk, Operational Risk, Capital Adequacy Ratio and Good Corporate Governance simultaneously toward Credit Risk Management so that it is proofed that the research model can indeed be applied in the research (model adequacy test). The hypothesis used for F test is the following:

H0 : β1 = β2 = β3 = β4 = β5 = β6 = β7 = β8 = 0Meaning: There are no simultaneously significant effects from independent variables of Minimum Capital Ratio, Capital Need Calculation, Market Risk, Credit Risk, Operational Risk, Capital Adequacy Ratio and Good Corporate Governance, consecutively toward dependent variable of Credit Risk Management of banking companies actively registered in the Indonesia Stock Exchange in the period of 2011-2016.

H1 : β1 = β2 = β3 = β4 = β5 = β6 = β7 = β8 ≠ 0Meaning: There are simultaneous significant effects from independent variables of Minimum Capital Ratio, Capital Need Calculation, Market Risk, Credit Risk, Operational Risk, Capital Adequacy Ratio and Good Corporate Governance consecutively toward dependent variable of Credit Risk Management of banking companies actively registered in the Indonesia Stock Exchange in the period of 2011-2016.

F test result in the research is accepting H1 therefore it show that model created in the research is at least have a coefficient slope equal to zero. In other word, there is at least an independent variables having real effect toward dependent variable.

Partial Significance (T-stat)t Test is use to find out whether individual independent variables (Minimum Capital

Ratio, Capital Need Calculation, Market Risk, Credit Risk, Operational Risk, Capital Adequacy Ratio and Good Corporate Governance) being use is significantly affect its dependent variables of Credit Risk Management. Therefore the hypotheses use in the test is:

H0 = There is no significant effect between i independent variable and dependent variable (βi=0)

H1 = There is significant effect between i independent variable with dependent variable (βi≠0)

Where i consist of number 1, 2, 3, 4, 5, 6, and 7 describing independent variables consist of Minimum Capital Ratio, Capital Need Calculation, Market Risk, Credit Risk, Operational Risk, Capital Adequacy Ratio and Good Corporate Governance consecutively. t test is conducted by comparing t-statistic (p-value) probability value with significance level (α). Decision criteria of reject H0 if p-value < α.

The research finds t table (t critical) with degree of freedom (df) = n-k. With n is the amount of conducted observation and k is the amount of independent variable added with constant so that = 156 – (7+1) = 150. Therefore with df = 150 and α=5% it is acquired t table of 1.65508.

Comparing t calculated value with t table used to make decision in determining test result (reject/accept). H0 or it can also be seen through its significance value through hypothesis test based on t statistic probability with the assumption that residual has normal distribution.

From table 4 it can be concluded that independent variable significantly affecting dependent variable is the Operation Risk and Credit Risk variable due to having t statistic (t calculate) value > than t table value, then its H0 is rejected and accept H1. The same if seen based on statistic t probability value (ρ) operational risk of 0.0018 and 0.0255 or smaller than α = 5% meaning that it is significant due to its error is zero percent below the stipulated 5%.

Meanwhile other variables such are Minimum Capital Ratio, Capital Need Calculation, Market Risk, Capital Adequacy Ratio and Good Corporate Governance are not significantly affecting the research’s dependent variable which is Credit Risk Management. The explanation of t test rest on variables equation affecting Credit Risk Management is in the following:

Test Result of Effect of Minimum Capital Ratio on Credit Risk ManagementThis variable is assumed to have positive relation on company risk management, where

higher minimum capital ratio stipulated by the company will keep bank’s financial stability in existing risk management especially credit risk management. This ratio is risk weighted asset ratio which is one way to measure bank’s capital, aimed as opening of bank’s risk weighted credit. From the research, it is obtained Minimum Capital Ratio coefficient value of 1.78 confirming that Minimum Capital Ratio does has positive effect on company credit risk management, however from such relation probability number it is no significant for its probability > α so that alternative Hypothesis or hypothesis is rejected and accepting null hypothesis.

Test Result of Effect of Capital Need Calculation on Credit Risk ManagementTest result from capital need effect on banking’s credit risk management is positive but

not significant with t significance of 0.64 higher than 0.05. As we know the calculation of the amount of capital need to cover credit risk, market risk and existing operational risk. Capital need is also use to cover risk according to risk position in the company.

Test Result of Market Risk Effect on Credit Risk ManagementMarket risk coefficient of 1.96 shows that market risk has positive effect but not

significant to banking risk management. With changes in the market, it may harm the bank (Hasibuan, 2006). Market risk on balance position and administrative account show derivative transaction result in overall changes of market condition, including risk of option price changes (Bank of Indonesia, 2003). This risk occurred due to market price moving toward loss. It is a combined risk formed due to changes of interest rate, currency and other which affect share market price, equity and commodity. There are two types of market risks which are specific market risk where risk due to price change of a certain monetary instrument (Kasidi, 2010: 66). However, higher market risk does not affecting companies’ credit risk management.

Test Result of Credit Risk Effect on Credit Risk ManagementTest result of credit risk on companies’ credit risk management is both positive and

significant. Credit risk in this matter is credit risk Basel II which stipulated 2 (methods) to measure credit risk, by means of Standard Approach using weighted risk from external rating and Internal Rating Based (IRB) enable bank to determine self-measurement parameter such as probability of default, loss given default, and recovery rate which are adjusted with owned credit portfolio (Bank for International Settlement, 2005), while credit risk management is proxied with NPL. Here we can see the management of credit risk management on banking which cover distribution of credit risk profile with various bank’s activities, among other credit distribution, derivative transaction, other financial instrument trade and other bank

activities recorded in banking book or trading book (Owojori et. al, 2011) is obtained through effect of credit risk in a company.

Test Result of Minimum Operational Risk Effect on Credit Risk ManagementOperational Risk coefficient of -0.65 confirm that risk operational has significant

negative effect on banking company credit risk. This means that high operational risk condition in a company will reduce credit risk management made by the company itself. According to what is written by Crouhy, Galai, and Mark (2001, pg.37) that operational risk potential loss is due to inadequacy of system, management failure, control failure, fraud and human error.

Test Result of Capital Adequacy Ratio (CAR) Effect on Credit Risk ManagementTest result of capital adequacy ratio effect is resulted in test value of -1.23 with t

significance of 0.5542. Higher significance value than 0.05 show that CAR is not significantly affect credit risk management toward negative. This result is contrary to the hypothesis. This is due to CAR condition is higher in a period will provide higher credit distribution from bank resulting into higher credit risk. If CAR positively affect credit risk it is related to its credit distribution, if bank continue is maintained to strengthen its capital, it is likely that the bank will focusing on their assets position to be stable with low risk.

Test Result of Good Corporate Governance Effect on Credit Risk ManagementTest result of GCG effect on credit risk management resulted in significance t test

value of 0.3667. Higher significance value than 0.05 show that GCG does not significantly affecting company credit risk management. This is due to good corporate governance criteria is not only calculated through self-assessment value, but there are also other factors affecting GCG composite value of banking companies.

V. CONCLUSIONS AND SUGGESTIONS

CONCLUSIONSBased on test result using multiply linear analysis, it is found out that credit risk

management of banking companies registered in the Indonesia Stock Exchange in the period of 2011 until 2016 proxied with NPL is simultaneously significantly affected by variables of minimum capital ratio, capital need calculation, market risk, credit risk, operational risk. Capital adequacy ratio and good corporate governance.Meanwhile partially it is obtained:1. Minimum Capital Ratio based on t-test show positive effect and is not significant on

banking Credit Risk Management in the period of 2009-2016.2. Capital Need Calculation based on t-test show positive effect and is not significant

on banking Credit Risk Management in the period of 2009-2016.3. Market Risk based on t-test show positive effect and is not significant on banking

Credit Risk Management in the period of 2009-2016.4. Credit Risk based on t-test show positive effect and is significant on banking Credit

Risk Management in the period of 2009-2016.5. Operational Risk based on t-test show negative effect and is significant on banking

Credit Risk Management in the period of 2009-2016.6. Capital Adequacy Ratio based on t-test show negative effect and is not significant on

banking Credit Risk Management in the period of 2009-2016.7. Good Corporate Governance based on t-test show positive effect and is not

significant on banking Credit Risk Management in the period of 2009-2016.

SUGGESTIONSBased on the discussion and after draw conclusion over the research, the writers

provide several suggestions as follows:1. Use a more representative operationalization variable and is up to date;2. Add new variable on logical research which may affect company risk

management;3. The use of data sample in this research is limited, it is possible to conduct further

research by using wider data;4. The writers suggest academics to use other methods and other statistical tools in

analysing data such as using STATA.

REFERENCEAllen, L. and T.G. Bali. 2007. Cyclicality in Catastrophic and Operational Risk

Measurement. Journal of Banking and Finance. vol. 31 no. 1, pp. 1191-1235. Bank Indonesia. 2006. Implementasi Basel II di Indonesia. Jakarta: Bank Indonesia.Bank for International Settlement. 2005. Basel II: International Convergence of Capital

Measurement and Capital Standards: A Revised Framework. Basel Committee of Banking Supervision, Switzerland.

Bauer, W., and M. Ryser. 2002. Risk Management Strategies for Bank. Journal of Banking and Finance. vol. 28 no. 4, pp. 331-352.

Brown, L.D., and Caylor, M.L. (2006). Corporate Governance and Firm Valuation. Journal of Accounting and Public Policy 25:409-434

Bruno, V.G., and Claessens, S. (2004). Corporate Governance and Regulation:Can There Be Too Much th of a Good Thing?. the 6 Annual Darden Conference on Emerging Markets

Claessens, S. (2006). Corporate Governance and Development. The World Bank Research Observer Advance Access. Published by Oxford University Press

Dendawijaya, Lukman. 2000, Manajemen Perbankan, PT Cholis Indonesia, JakartaFerry N. Idroes, 2008, Manajemen Risiko Perbankan: Pemahaman 3 Pilar Kesepakatan

Basel II Terkait Aplikasi Regulasi dan Pelaksanaannya di Indonesia, Rajawali Pers, Jakarta

Galorath, D. 2006. Risk Management Success Factor. PM world Today. vol. 8 no. 2, pp. 12-23

Goyal, Krishn A. 2010. Risk Management in Indian Banks: Some Emerging Issues. The Indian Economic Journal. vol. 1 no. 1, pp. 102-109.

Indrawati, SM, S.A. Djalil and Taufik Effendi. 2011. Draft Pedoman Penerapan Manajemen Risiko Berbasis Governance. Komite Nasional Kebijakan Governance, Jakarta.

Institute of Risk Management. 2002. A Risk Management Standards. Association of Insurance and Risk Managers, London.

Hasibuan. 2007. Dasar-Dasar Perbankan. Jakarta: Bumi Aksara.. Kasmir. 2008. Manajemen Perbankan Edisi Revisi . Jakarta: PT Raja Grafindo PersadaKuncoro, Mudrajad dan Suhardjono. 2002. Manajemen Perbankan: Teori dan Aplikasi.

Yogyakarta: BPFE..Kasidi. 2010. Manajemen Risiko. Bogor: Penerbit Ghalia Indonesia.Lampiran Surat Edaran Nomor 13/23/DPNP/2011 tentang Pedoman Penerapan

Manajemen Risiko Secara Umum

Laporan Keuangan Bank Indonesia yang dipublikasikan(www.ojk.go.id), diolahKorna Risk Management. 2010. Risk Management in the Ukraine Banking Sector. U.S.A:

A.T. Kearney.Peraturan Bank Indonesia. 2002. SK No. Kep-117/M-MBU/2002 tentang Pelaksanaan

Good Corporate Governance pada Bank UmumPeraturan Nomor 5/8/PBI/2003 tentang Penerapan Manajemen Risiko bagi Bank Umum. Peraturan Bank Indonesia. 2009.Nomor 11/25/PBI2009. tentangPerubahan atas PBI

No.5/8/PBI/ 2003 tentang Penerapan Manajemen Risiko bagi Bank UmumPeraturan Nomor 11/25/PBI/2010 tentang Penerapan Manajemen Risiko bagi Bank

Umum.Peraturan Bank Indonesia. 2011.Nomor 13/1/PBI2011. tentangPenilaian Tingkat

Kesehatan Bank UmumSekaran, U. 2003. Research Methods for Business : A Skill Building Approach 2nd

Edition, John Wiley and Son. New York.Surat Edaran Nomor 5/2/DPNP/2003 tentang Penerapan Manajemen Risiko bagi Bank

Umum. Surat Edaran Bank Indonesia No. 15/15/DPNP/2013, Tentang Self Assesment Penilaian

Kesehatan Bank 13/1/PBI2011, Tentang Penilaian Tingkat Kesehatan Bank Umum Sukamulja, Sukmawati. 2004. "Good corporate governance di Sektor Keuangan:Damapak

GCG terhadap Kinerja Perusahaan (kasus di Bursa Efek Jakarta)". BENEFIT. Sugiyono. 2011. Metode Penelitian Bisnis. Bandung: CV Alvabeta.

Susanti, Angaheni Niken, Rahmawati dan Aryani. 2010. “Analisis Pengaruh Mekanisme Corporate Governance terhadap Nilai Perusahaan dengan Kualitas Laba sebagai variabel Intervening pada Perusahaan Manufaktur yang terdaftar di Bursa Efek Indonesia 2004-2007” Artikel Simposium Nasional Keuangan I.