1 Controllership: Addressing Financial Management Challenges and Transformation Opportunities Financial Management Institute Presented by: Murray Lindo, Director, Financial Management and Control Branch Ministry of Finance, Ontario Government February 25, 2009

Transcript

1

Controllership:

Addressing Financial Management Challenges and Transformation Opportunities

Financial Management Institute

Presented by: Murray Lindo, Director, Financial Management and Control Branch

Ministry of Finance, Ontario Government

February 25, 2009

2

Today’s Discussion

Outline the key public sector financial management issues, especially during a global economic slow-down.

Describe the leadership role that the controllership function and the financial community must play in supporting the decision-makers through this challenging time.

Provide some thoughts on how the financial function may need to transform to support the emerging economic and public sector environment.

3

Key Messages

An effective controllership function is forward looking, acting as the business’s “head lights”: scanning the environment, anticipating issues and seeking effective resolutions.

Controllership must be involved in the front-end of the decision-making process helping to assess options and thereby contribute to successful implementation.

Controllership function must balance a professional understanding with practical skills in advanced management accounting, risk management, process and structure cost control, and revenue management.

4

Section 1:

What is Controllership and

Why is it Challenging?

5

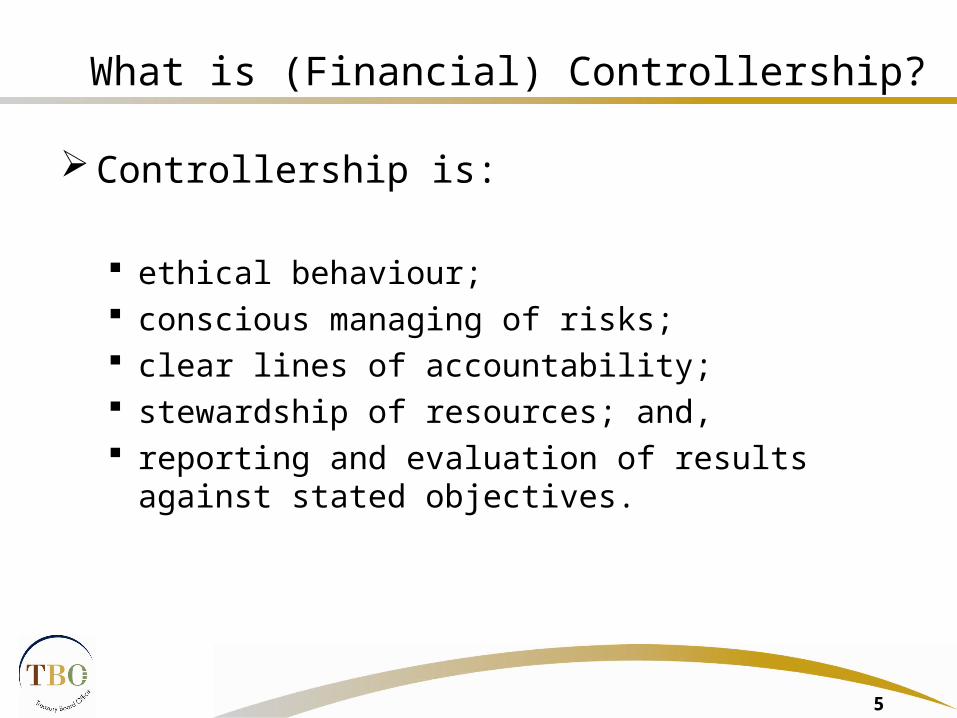

What is (Financial) Controllership?

Controllership is:

ethical behaviour; conscious managing of risks; clear lines of accountability; stewardship of resources; and, reporting and evaluation of results against stated objectives.

6

Why Controllership is important?

Accountability to the public Stability and transparency Ensures compliance against stated standards Enables efficient and effective use of public resources Defines roles and responsibilities

Enables performance measurement against agreed expectations Fulfills legal obligations and mandate

7

Why is Controllership Challenging?

Equal Footing: financial/controllership analysis not always on an equal footing to policy, operational and communication considerations, in the decision-making process.

Management Perceptions: controllership seen by management as “end state” technical process rather being critical to transparency and accountability.

Credible Information: ability to produce timely, reliable, usable and accurate financial and risk information to decision-makers.

Communication: providing clear and accessible financial/controllership information to line-management

Capacity: revitalizing financial capacity by attracting, retaining and developing financial/controllership talent.

8

Key Principles in the Controllership’s Evolution

Supporting the evolution of the Controllership function are four key principles:

Credibility – a trusted business advisor, providing accurate, timely and reliable financial information and advice;

Competence – combine business knowledge with financial expertise to optimize value added;

Commitment – a shared commitment to the goals of financial management and effective program service and delivery; and

Communication – open communication across government, with external professional organizations and counterparts in other jurisdictions.

9

Section 2:

“Think globally, act locally”

Controllership’s Transformation

in Challenging Economic Times

10

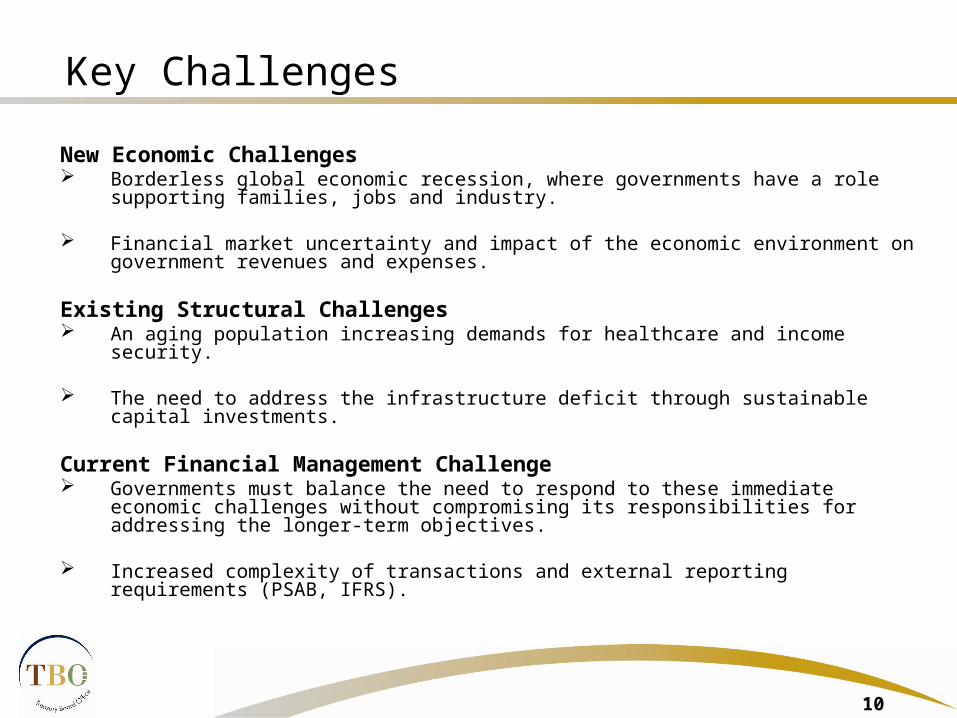

Key Challenges

New Economic Challenges Borderless global economic recession, where governments have a role supporting families,

jobs and industry.

Financial market uncertainty and impact of the economic environment on government revenues and expenses.

Existing Structural Challenges An aging population increasing demands for healthcare and income security.

The need to address the infrastructure deficit through sustainable capital investments.

Current Financial Management Challenge Governments must balance the need to respond to these immediate economic challenges

without compromising its responsibilities for addressing the longer-term objectives.

Increased complexity of transactions and external reporting requirements (PSAB, IFRS).

11

Today’s Operating Environment

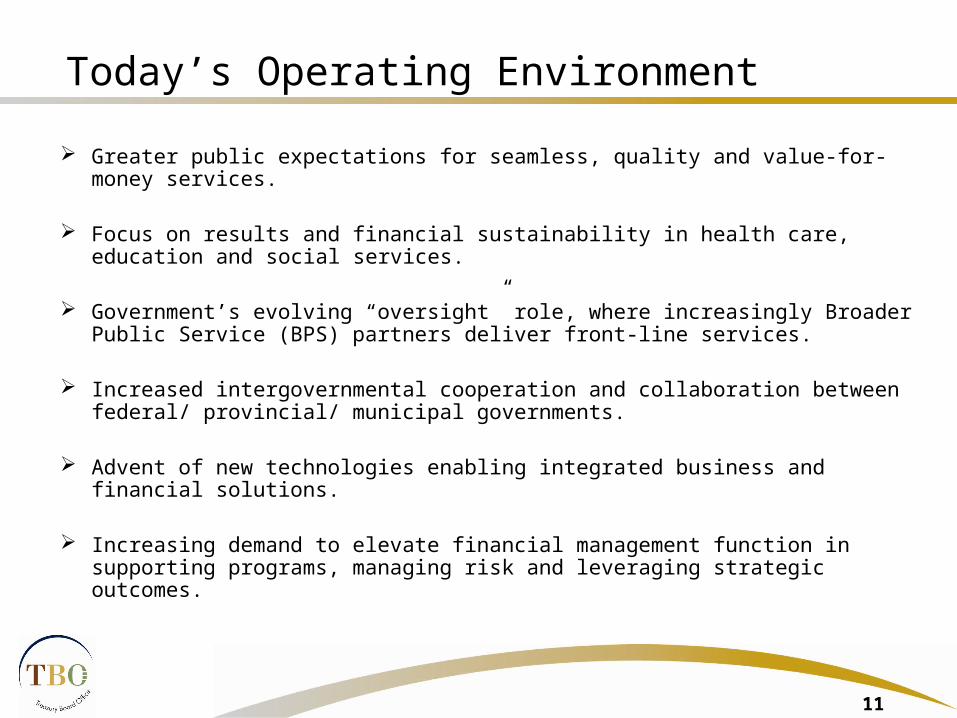

Greater public expectations for seamless, quality and value-for-money services.

Focus on results and financial sustainability in health care, education and social services.

Government’s evolving “oversight” role, where increasingly Broader Public Service (BPS) partners deliver front-line services.

Increased intergovernmental cooperation and collaboration between federal/ provincial/ municipal governments.

Advent of new technologies enabling integrated business and financial solutions.

Increasing demand to elevate financial management function in supporting programs, managing risk and leveraging strategic outcomes.

12

Controllership must exercise Financial Leadership

During economic downturns, the role of the public sector financial community is even more critical.

Our role is to provide government decision-makers with the best financial information possible, so that they can make well informed decisions amongst the competing public policy demands.

To be successful in this role, in supporting financial decision-making, we must:

• establish a robust financial management framework;• emphasize value for money and fiscal accountability;• balance immediate fiscal impacts with longer-term stewardship;• ensure appropriate controls are in place and functioning;• apply financial risk management principles; and• ensure transparency in financial reporting through public disclosure.

13

Controllership’s role in financial management

The controller/controllership function plays a key financial management role in making the government’s business objectives achievable.

Controllership adds to the financial management discipline by providing assurance of compliance with financial reporting and controls.

However, the controllership function’s “value” is fully realized by supporting decision-makers with financial analyses that identifies: links between costs and performance; opportunities to reduce direct and indirect costs; and opportunities to increase delivery efficiency in meeting public policy goals.

Realizing this contribution can only happen when we fully apply advanced management accounting, risk management, effective costing and revenue management.

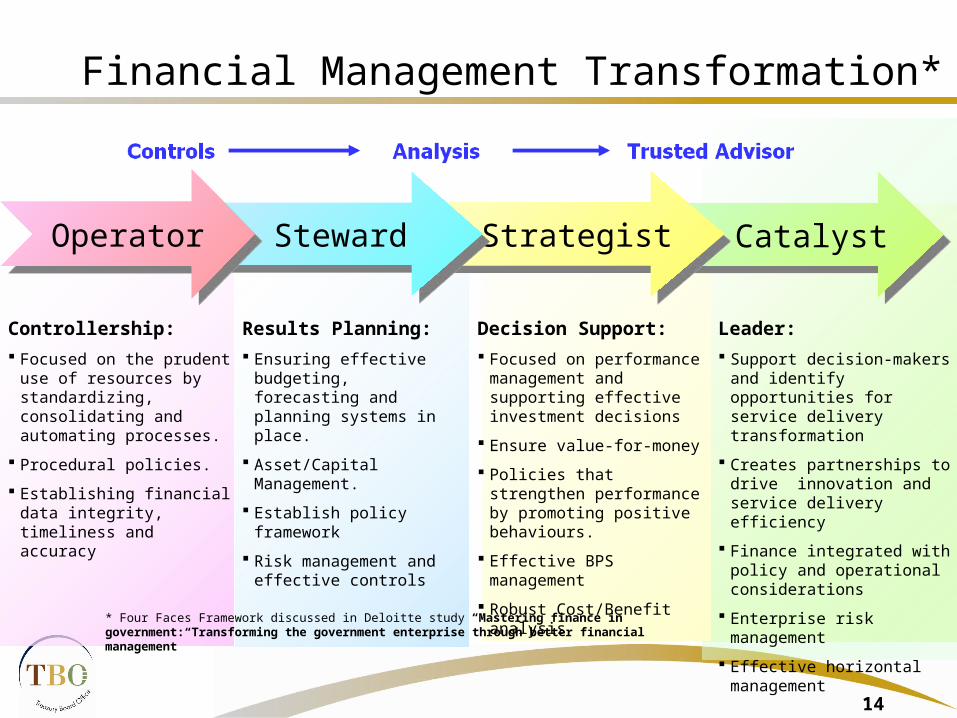

use of resources by standardizing, consolidating and automating processes.

Procedural policies.

Establishing financial data integrity, timeliness and accuracy

Results Planning: Ensuring effective

budgeting, forecasting and planning systems in place.

Asset/Capital Management.

Establish policy framework

Risk management and effective controls

Decision Support: Focused on performance

management and supporting effective investment decisions

Ensure value-for-money

Policies that strengthen performance by promoting positive behaviours.

Effective BPS management

Robust Cost/Benefit analysis

Leader: Support decision-makers

and identify opportunities for service delivery transformation

Creates partnerships to drive innovation and service delivery efficiency

Finance integrated with policy and operational considerations

Enterprise risk management

Effective horizontal management

* Four Faces Framework discussed in Deloitte study “Mastering finance in government: Transforming the government enterprise through better financial management”

15

Required Financial Management Elements

Management Decision Support Financial evaluation expertise Business risk management expertise Capital investment analysis expertise Financial performance management

expertise

Business Planning, Fiscal Planning and Budgeting Strategic business planning expertise Risk-based Fiscal planning expertise Capital planning expertise Integrated capital, operating and cash-flow

Accounting, Appropriations and Financial Reporting Accounting policy application and control

expertise Appropriation compliance and control

expertise Costing and pricing expertise Financial reporting expertise Financial information analysis and integrity

assurance expertise

Risk Management, Accountability and Control Program risk management and control

expertise Project risk management and control

expertise Asset and Liability risk management and

control expertise Transfer Payment, Agency and Trust risk

management and control expertise.

16

Financial Competencies needed

Business Knowledge

Effective Costing, Planning & Evaluation

Risk Management

Standards Compliance

Effective Communication

Performance Management

Forecasting, Planning and Budgeting

Accounting/ Financial Knowledge

Valued-added Advice

Value-for-

Money

StrategicFocus

Competencies

17

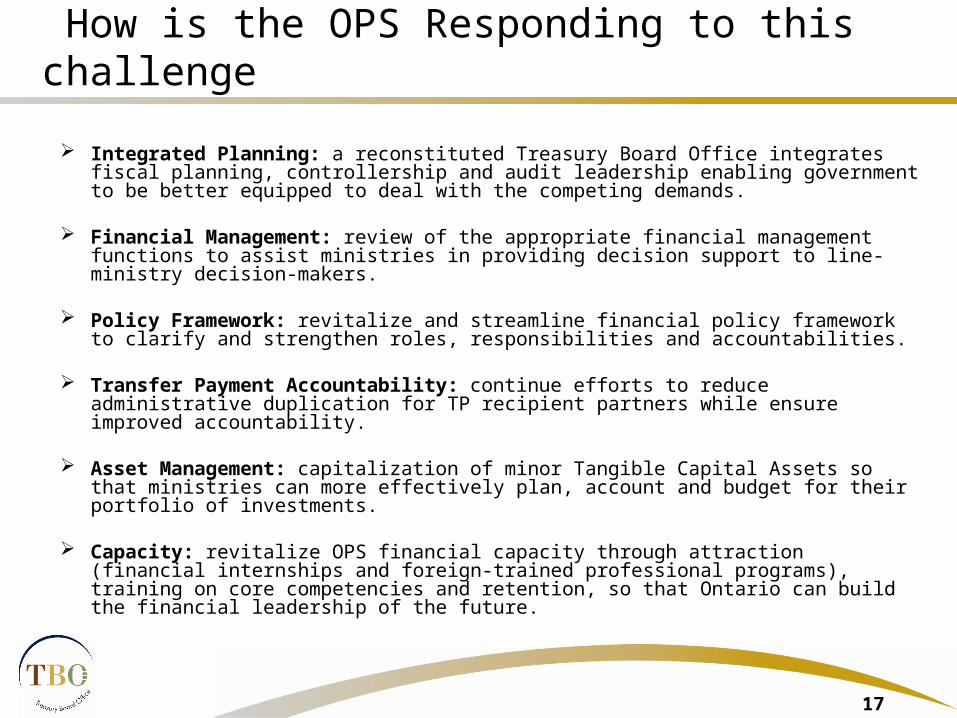

How is the OPS Responding to this challenge

Integrated Planning: a reconstituted Treasury Board Office integrates fiscal planning, controllership and audit leadership enabling government to be better equipped to deal with the competing demands.

Financial Management: review of the appropriate financial management functions to assist ministries in providing decision support to line-ministry decision-makers.

Policy Framework: revitalize and streamline financial policy framework to clarify and strengthen roles, responsibilities and accountabilities.

Transfer Payment Accountability: continue efforts to reduce administrative duplication for TP recipient partners while ensure improved accountability.

Asset Management: capitalization of minor Tangible Capital Assets so that ministries can more effectively plan, account and budget for their portfolio of investments.

Capacity: revitalize OPS financial capacity through attraction (financial internships and foreign-trained professional programs), training on core competencies and retention, so that Ontario can build the financial leadership of the future.

18

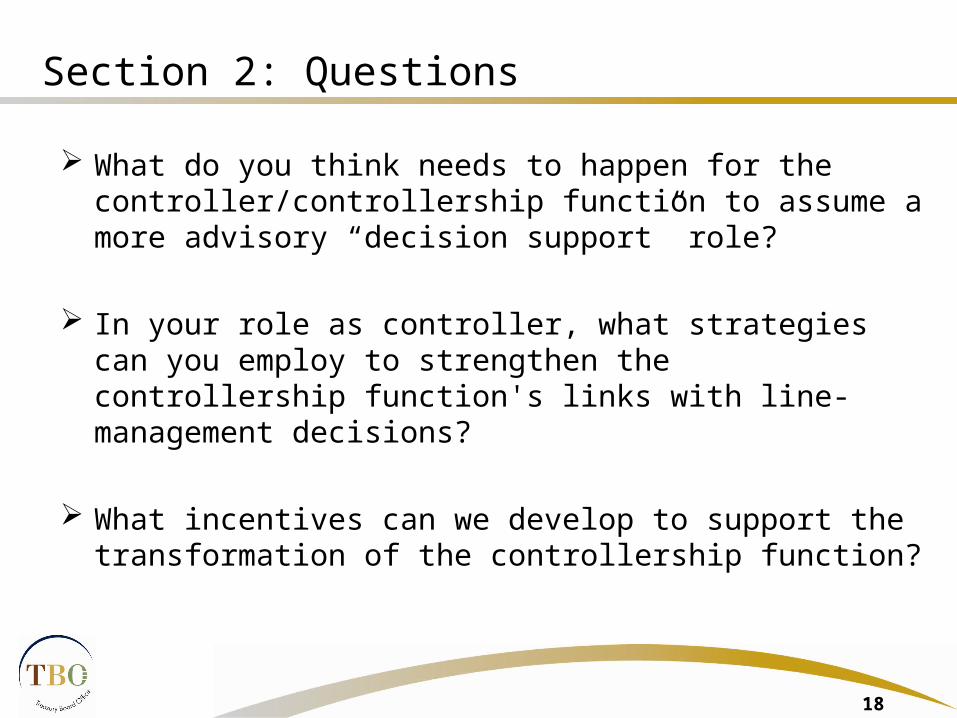

Section 2: Questions

What do you think needs to happen for the controller/controllership function to assume a more advisory “decision support” role?

In your role as controller, what strategies can you employ to strengthen the controllership function's links with line-management decisions?

What incentives can we develop to support the transformation of the controllership function?

19

Section 3:

Case Studies

20

Case Study 1: Government support for the Auto Sector

Challenge: Balancing socio-economic imperative to save manufacturing jobs against the public policy and accountability requirements.

Objective: Provide ailing automobile companies a credit bridge through difficult times.

Key Issues: Supporting the auto sector is multi-jurisdictional issue. Loan agreements cannot be made in

vacuum and must take into account all aspects of the various governments’ initiatives. Managing the risk of longer-term investments in an industry with weak consumer demand

and volatile stock markets. Ensuring public money is spent appropriately and contributes to wider public policy goals,

such as more environmentally friendly cars. Making sure public loans are repaid and that government exposure is based on the

associated risks.

21

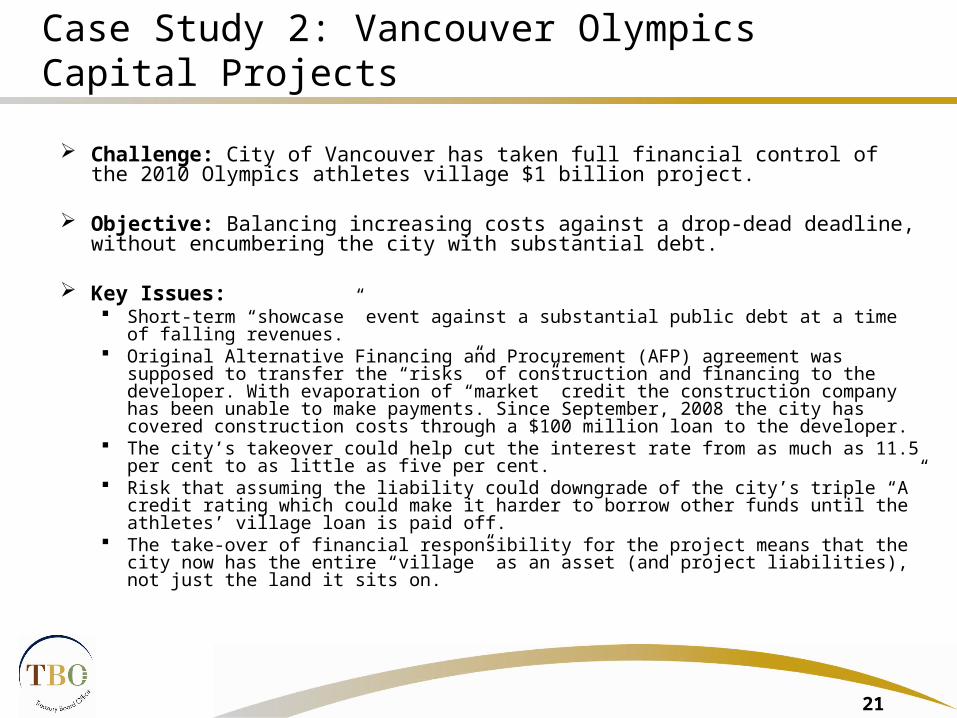

Case Study 2: Vancouver Olympics Capital Projects

Challenge: City of Vancouver has taken full financial control of the 2010 Olympics athletes village $1 billion project.

Objective: Balancing increasing costs against a drop-dead deadline, without encumbering the city with substantial debt.

Key Issues: Short-term “showcase” event against a substantial public debt at a time of falling revenues. Original Alternative Financing and Procurement (AFP) agreement was supposed to transfer

the “risks” of construction and financing to the developer. With evaporation of “market” credit the construction company has been unable to make payments. Since September, 2008 the city has covered construction costs through a $100 million loan to the developer.

The city’s takeover could help cut the interest rate from as much as 11.5 per cent to as little as five per cent.

Risk that assuming the liability could downgrade of the city’s triple “A” credit rating which could make it harder to borrow other funds until the athletes’ village loan is paid off.

The take-over of financial responsibility for the project means that the city now has the entire “village” as an asset (and project liabilities), not just the land it sits on.

22

Case Study 3: Alternative Financing Arrangements

Challenge: Ontario has an infrastructure deficit estimated at more than $100 billion.

Objective: Alternative Financing and Procurement (AFP) represents an opportunity to leverage private-sector project management expertise and financing to help bridge the infrastructural deficit.

Key Issues: Public policy considerations in the government’s construction, management and ownership

of assets. The higher private-sector financing rates must be balanced against construction risks (i.e.

cost overruns) transferred to the private partners. Long-term AFPs that include design, build and asset management components, require

performance criteria to ensure value-for-money throughout the asset’s life-cycle. The openness and transparency of the alternative financing process are critical to ensure the

highest return on investments and public accountability. Differing financing rates methodologies impact the recognised value of the assets. Using a

project costing model will increase financing costs, while a internal discounted rate will decrease financing costs and change the asset’s value.

23

From a Controllership Perspective

We need to ensure: solid financial management information is provided to support an effective balance between

the need to stimulate the economy against the stewardship role of asset management for the longer-term;

a strong and transparent decision-making framework is in place that provides value-for-money to taxpayers;

public resources are effectively controlled in accordance with legislative and public sector accountability standards;

a strong understanding and independent assessment of AFP rival bids based on robust and reasonable costing/financing assumptions; and,

transactions are accurately accounted for and represented in the province’s Public Accounts.

Overall, we need to put this in a language that helps the decision makers make informed investment choices.

24

Section 4:

Looking Forward

25

Key Requirements for Success

Informed Decisions: Further integration of risk and performance management into the fabric of financial decision-making.

Effective Governance: establishing clear roles and accountabilities, linked to decision-making structure and supported by a robust policy framework.

Financial Leadership: to set priorities, support capacity improvements and provide a strategic financial “voice” at the decision-making table.

Financial transformation: continue to migrate the financial function away from a transaction-rules focus to an “advisory” decision support and oversight role.

Business “ownership” of Finance: progressively, delegate financial management to program managers and other government organizations, while maintaining accountability and oversight.

Measuring Progress: establish clear performance measures, evaluate progress toward achieving the desired goals and taking remedial action when necessary.

Communications: open and transparent communications to allow knowledge of risks, challenges and solutions to flow throughout the organization(s).

Financial Capacity: attract, retain and develop financial capacity that is aligned to future needs.

26

Looking Ahead

Controllership closes the financial management “accountability loop”.

Effective controllership provides the front-end financial information to make informed business decisions but also ensures controls are met in the achievement of results.

As the demands of controllership function increase, it is critical to integrate risk management, process and structure cost control, and revenue management into the fabric of decisions.

Ultimately, our success depends upon the professional knowledge we bring to the decision-making table. Only up-to-date, strategic competencies and a robust financial community can ensure we provide value-added expertise needed to achieve public policy goals.