Page 1

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 1

Unit 5Accounting for Special Procedures

Chapter 22 Cash Funds

Chapter 23 Plant Assets and Depreciation

Chapter 24 Uncollectible Accounts Receivable

Chapter 25 Inventories

Chapter 26 Notes Payable and Receivable

Page 2

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 2

Chapter 26Notes Payable and Receivable

What You’ll Learn Explain how businesses use promissory notes. Calculate and record notes payable and notes

receivable. Explain the difference between interest-bearing and

non-interest-bearing notes. Journalize transactions involving notes payable. Journalize transactions involving notes receivable. Define the accounting terms introduced in this

chapter.

Page 3

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 3

Chapter 26, Section 1 Promissory Notes

What Do You Think?What does the term interest mean?

Page 4

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 4

Main IdeaThe formula for calculating interest is principal x interest rate x time.

You Will Learn how promissory notes are used. how to calculate the interest on a note.

Promissory NotesSECTION 26.1

Page 5

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 5

Key Terms promissory note note payable note receivable principal face value term issue date payee interest rate maturity date maker

Promissory NotesSECTION 26.1

Page 6

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 6

Key Terms interest maturity value

Promissory NotesSECTION 26.1

Page 7

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 7

A Promise to PayA promissory note is a written promise to pay a certain amount of money at a specific time.

Promissory NotesSECTION 26.1

Page 8

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 8

Notes Payable and Notes ReceivableA note payable is a promissory note that a business issues to a creditor when it borrows or buys on credit. A note receivable is a promissory note that a business accepts from a credit customer.

The parts of a promissory note are: Principal or face value Term Issue date Payee Interest rate Maturity date Maker

Promissory NotesSECTION 26.1

Page 9

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 9

Promissory NotesSECTION 26.1

Page 10

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 10

The Maturity Date of a NoteThe period of time in which a note’s maker agrees to repay the note is the term of the note. The term and the issue date are needed to determine the maturity date.

To calculate a maturity date using a time calendar: Locate the issue date in the Day of month

column. Move across to the issue month to find the day of the year (September 14 is 257).

Add the number of days in the term to the day of the year (90+257=347).

Find this number in the month columns (347 corresponds to December 13).

Promissory NotesSECTION 26.1

Page 11

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 11

The Maturity Date of a Note

Promissory NotesSECTION 26.1

Page 12

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 12

Calculation of Interest on a NoteInterest is the fee charged for the use of money. The interest rate is the interest stated as a percentage of the principal.

Promissory NotesSECTION 26.1

Page 13

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 13

Calculating Interest Using a FormulaUse the following formula to calculate interest:

Interest = Principal x Interest Rate x Time

Interest rates are usually stated on an annual basis. If the term is less than a year, the time in the calculation is expressed as a fraction of a year. Maturity value is the amount due at the due date.

Promissory NotesSECTION 26.1

Page 14

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 14

Calculating Interest Using an Interest TableTo calculate interest using an interest table, follow these steps:

Find the term of the note in the Day column. Follow the row until you reach the column for the

interest rate. Where they intersect is the factor (per $100 of principal).

Divide the principal of the note by 100. Multiply the result by the factor to find the amount

of interest.

Promissory NotesSECTION 26.1

Page 15

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 15

Calculating Interest Using an Interest Table

Promissory NotesSECTION 26.1

Page 16

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 16

Key Terms Review promissory note

A written promise to pay a certain amount of money at a specific time.

note payable

A promissory note issued to a creditor. note receivable

A promissory note that a business accepts from a customer.

principal

The amount of money borrowed on a promissory note.

Promissory NotesSECTION 26.1

Page 17

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 17

Key Terms Review face value

The amount written on the face of a promissory note; also called principal.

term

The length of time the borrower has to repay a promissory note.

issue date

The date on which a promissory note is written. payee

The person or business to whom a check is written or a note is payable.

Promissory NotesSECTION 26.1

Page 18

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 18

Key Terms Review interest rate

The fee charged for the use of money stated as a percentage of the principal.

maturity date

The due date of a promissory note; the date on which the principal and interest must be paid.

maker

The person or business promising to repay the principal and interest when a loan is made.

Promissory NotesSECTION 26.1

Page 19

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 19

Key Terms Review interest

The fee charged for the use of money. maturity value

The principal plus interest that must be paid on a promissory note’s due date.

Promissory NotesSECTION 26.1

Page 20

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 20

Chapter 26, Section 2Notes Payable and Receivable

What Do You Think?What do the terms interest-bearing and non-interest-bearing mean?

Page 21

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 21

Main IdeaBusinesses issue and accept two types of notes: interest-bearing notes and non-interest-bearing notes.

You Will Learn what an interest-bearing promissory note is. why a “non-interest-bearing” note does have

interest expense.

Notes PayableSECTION 26.2

Page 22

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 22

Key Terms long-term liabilities interest-bearing note payable non-interest-bearing note payable bank discount proceeds other expense

Notes PayableSECTION 26.2

Page 23

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 23

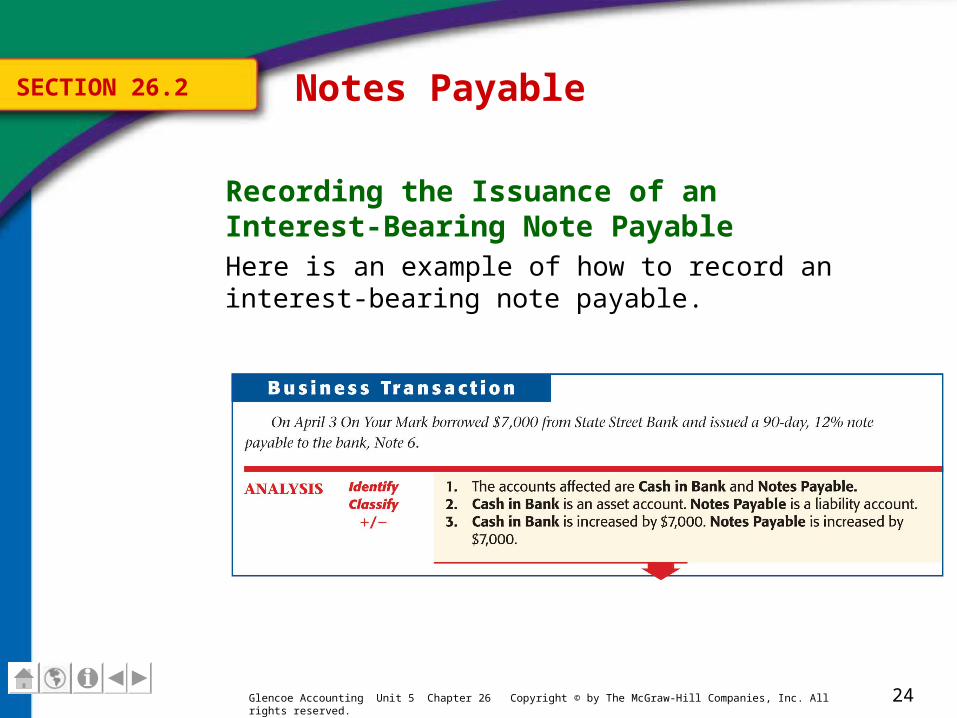

Interest-Bearing Notes PayableNotes issued by a business are recorded in Notes Payable, a liability account. Long-term liabilities are debts that become due after one year. An interest-bearing note payable requires the principle plus interest to be paid on the maturity date.

Notes PayableSECTION 26.2

Page 24

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 24

Recording the Issuance of an Interest-Bearing Note PayableHere is an example of how to record an interest-bearing note payable.

Notes PayableSECTION 26.2

Page 25

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 25

Recording the Issuance of an Interest-Bearing Note Payable

Notes PayableSECTION 26.2

Page 26

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 26

Recording the Issuance of an Interest-Bearing Note Payable

Notes PayableSECTION 26.2

Page 27

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 27

Recording the Issuance of an Interest-Bearing Note Payable

Notes PayableSECTION 26.2

Page 28

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 28

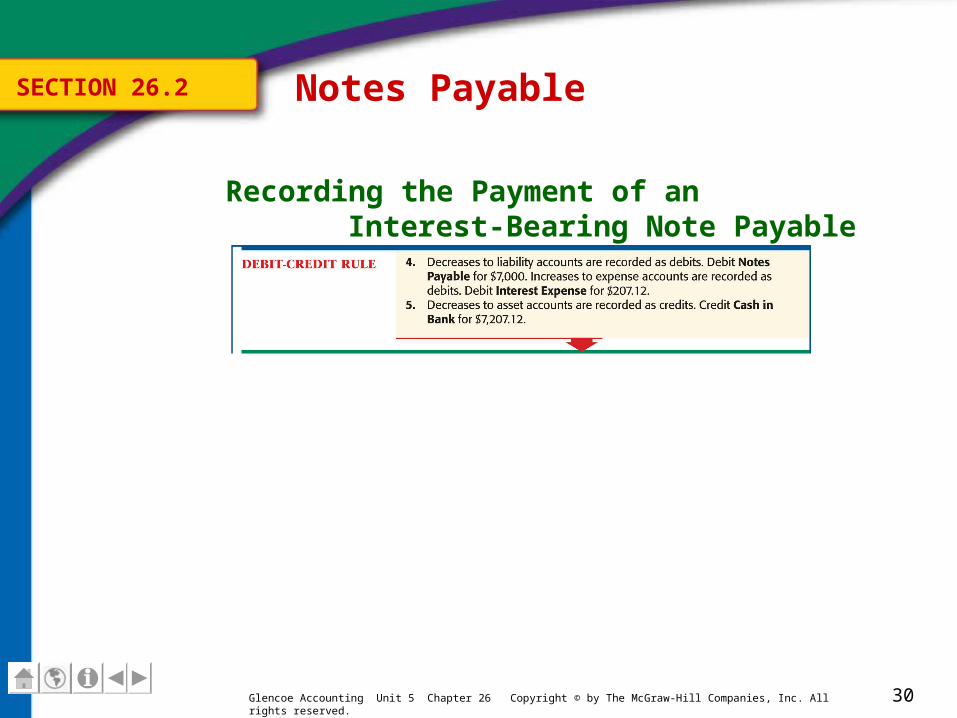

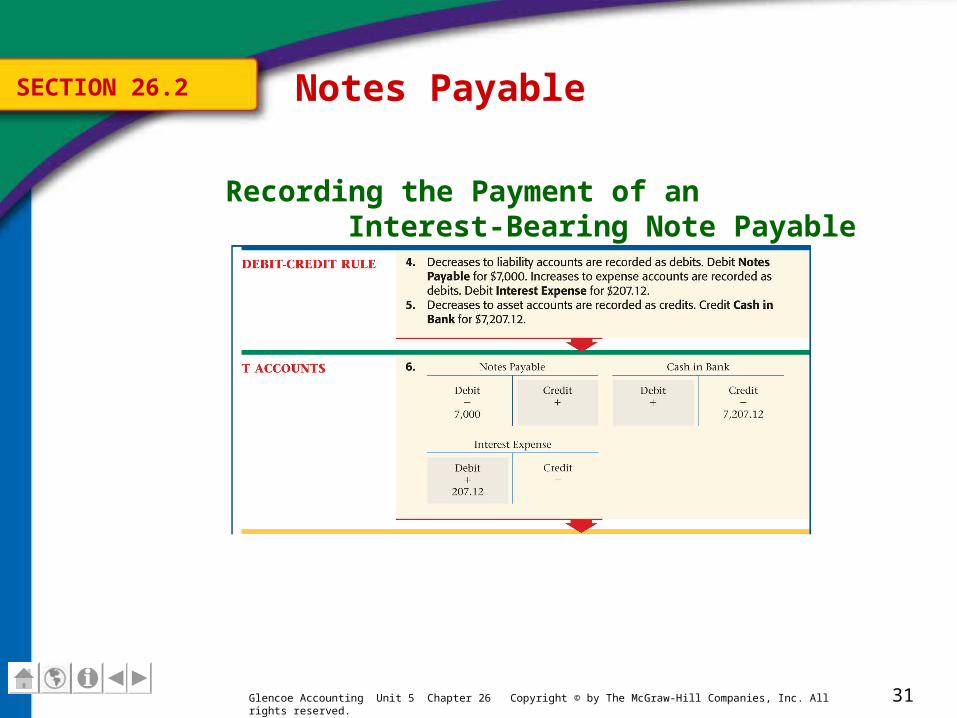

Recording the Payment of an Interest-Bearing Note PayableHere is an example of how to record the payment of an interest-bearing note payable.

Notes PayableSECTION 26.2

Page 29

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 29

Recording the Payment of an Interest-Bearing Note Payable

Notes PayableSECTION 26.2

Page 30

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 30

Recording the Payment of an Interest-Bearing Note Payable

Notes PayableSECTION 26.2

Page 31

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 31

Recording the Payment of an Interest-Bearing Note Payable

Notes PayableSECTION 26.2

Page 32

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 32

Non-Interest-Bearing Notes PayableA non-interest bearing note payable is a note in which the interest is deducted from the face value of the note when it is issued. It is called non-interest bearing because no interest rate is stated on the note.

The interest deducted in advance is the bank discount. The cash received by the borrower is called the proceeds. For this type of note, the maturity value is the same as the face value.

Notes PayableSECTION 26.2

Page 33

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 33

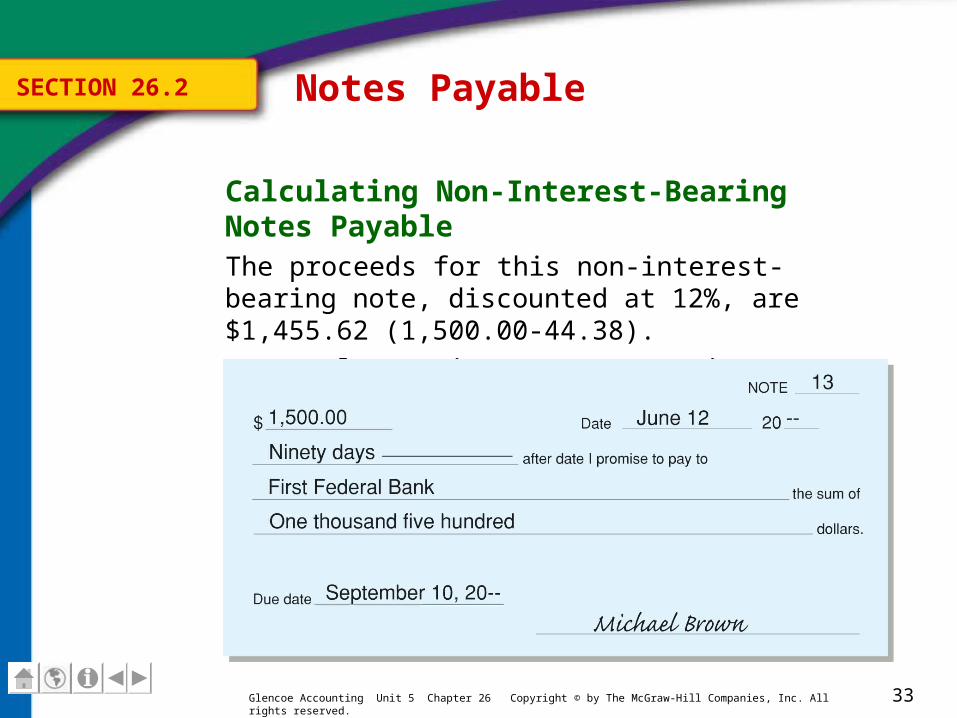

Calculating Non-Interest-Bearing Notes PayableThe proceeds for this non-interest-bearing note, discounted at 12%, are $1,455.62 (1,500.00-44.38).

Face Value x Discount Rate x Time = Bank Discount

$1,500 x 0.12 x 90/365 = $ 44.38

Notes PayableSECTION 26.2

Page 34

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 34

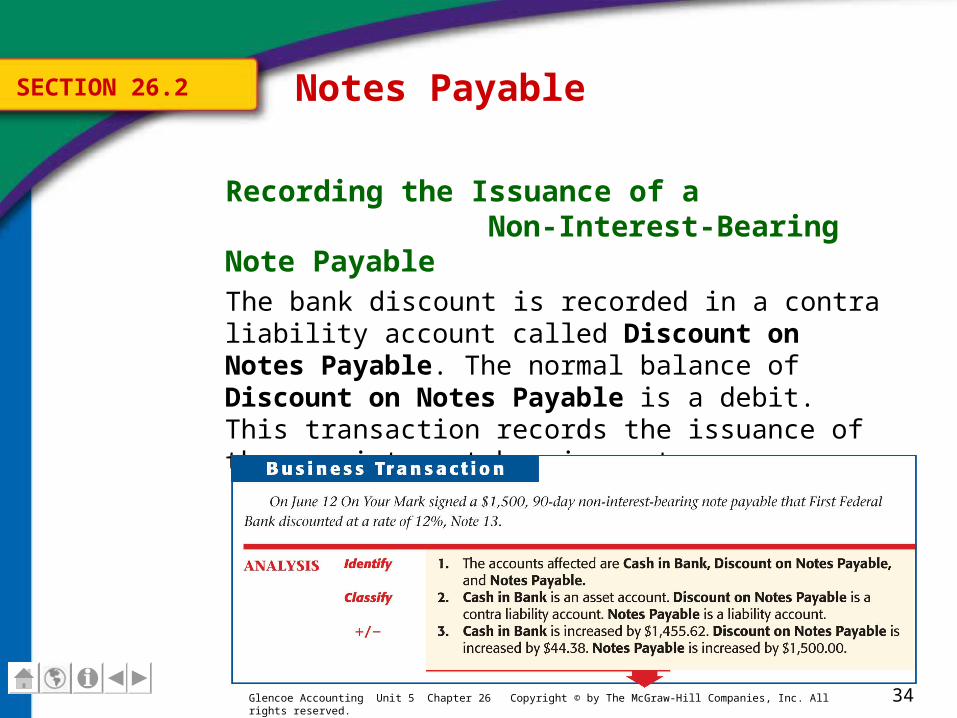

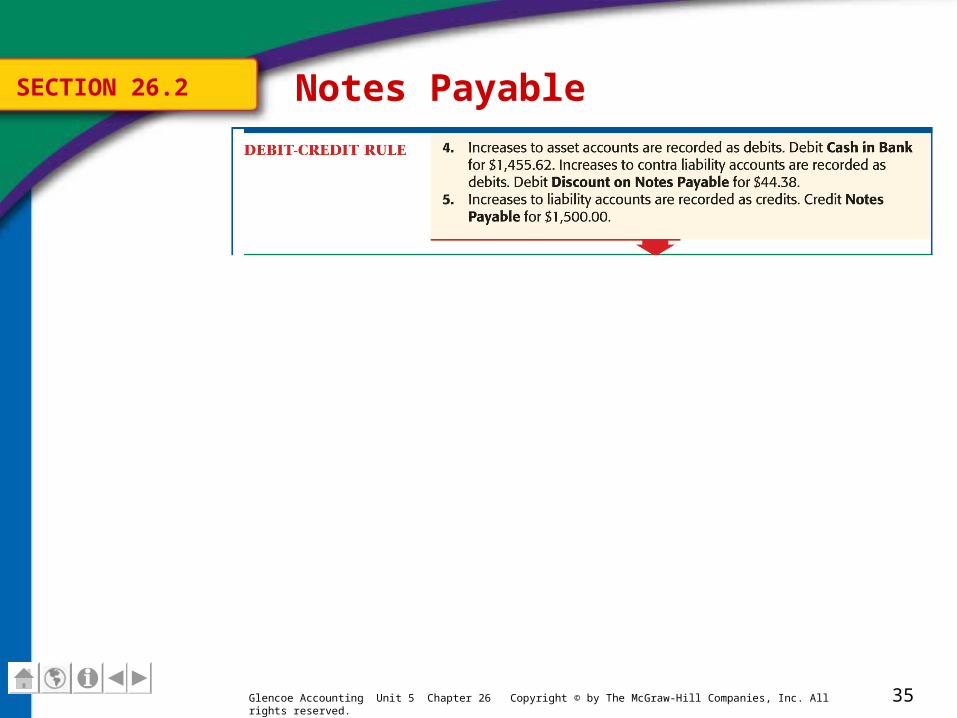

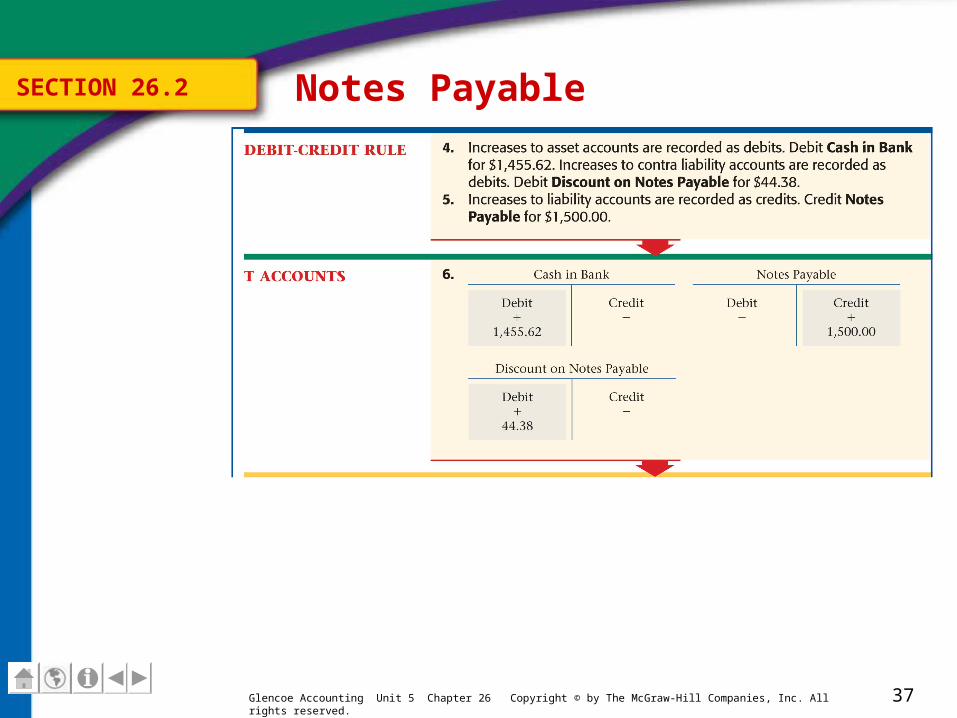

Recording the Issuance of a Non-Interest-Bearing Note PayableThe bank discount is recorded in a contra liability account called Discount on Notes Payable. The normal balance of Discount on Notes Payable is a debit. This transaction records the issuance of the non-interest-bearing note.

Notes PayableSECTION 26.2

Page 35

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 35

Notes PayableSECTION 26.2

Page 36

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 36

Notes PayableSECTION 26.2

Page 37

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 37

Notes PayableSECTION 26.2

Page 38

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 38

Recording the Payment of a Non-Interest-Bearing Note PayableWhen a non-interest-bearing note payable matures, the amount of the bank discount is recorded as an expense. Record a matured note using two separate journal entries or a compound entry:

the payment of the non-interest-bearing note payable, and

the interest expense

The Interest Expense account is classified as an other expense, which is nonoperating expense. It appears on the income statement below operating income.

Notes PayableSECTION 26.2

Page 39

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 39

Key Terms Review long-term liabilities

Debts that are not required to be paid within the next accounting period.

interest-bearing note payable

A note that requires the face value plus interest to be paid on the maturity date.

non-interest-bearing note payable

A note from which the interest is deducted in advance from the face value of the note; no interest rate is stated on the note.

Notes PayableSECTION 26.2

Page 40

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 40

Key Terms Review bank discount

The interest charge deducted in advance on a non-interest-bearing note payable.

proceeds

The cash actually received by the borrower on a non-interest-bearing note payable.

other expense

A nonoperating expense; an expense that does not result from the normal operations of the business.

Notes PayableSECTION 26.2

Page 41

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 41

Chapter 26, Section 3Notes Payable and Receivable

What Do You Think?Why should a business record a note receivable that it accepted?

Page 42

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 42

Main IdeaBusinesses record the receipt of a note receivable as well as the payment of the note.

You Will Learn how to record a note receivable. how to record the payment of a note receivable.

Notes ReceivableSECTION 26.3

Page 43

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 43

Key Term other revenue

Notes ReceivableSECTION 26.3

Page 44

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 44

Recording the Receipt of a Note ReceivableIf a customer needs additional time to pay an account receivable, he or she might sign a promissory note, called a note receivable.

The interest earned on a note receivable is recorded in the Interest Income account, an other revenue account.

Notes ReceivableSECTION 26.3

Page 45

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 45

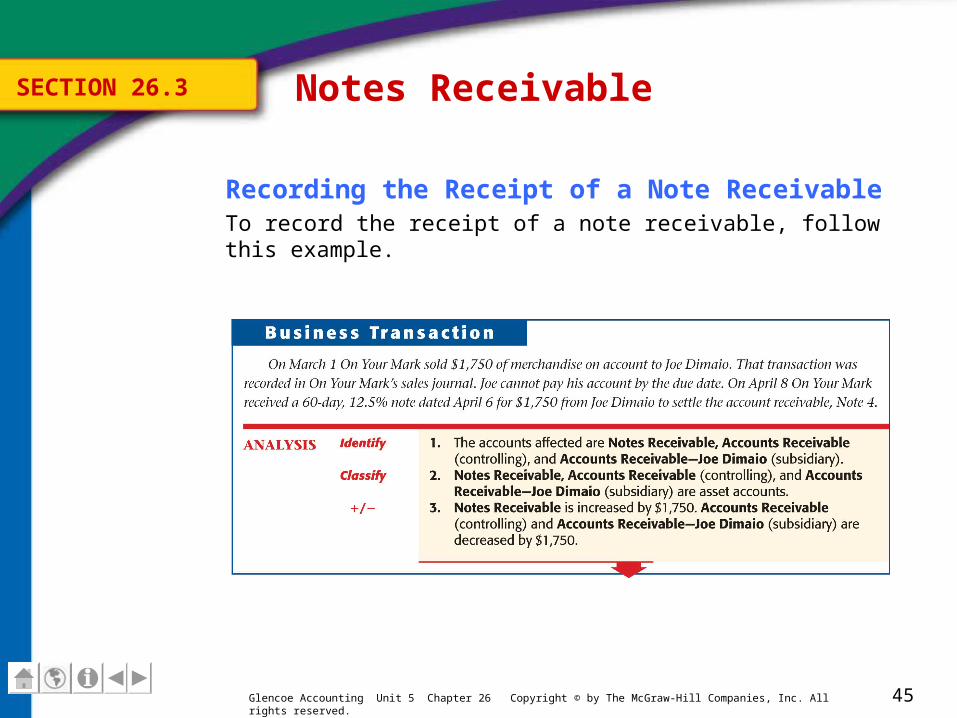

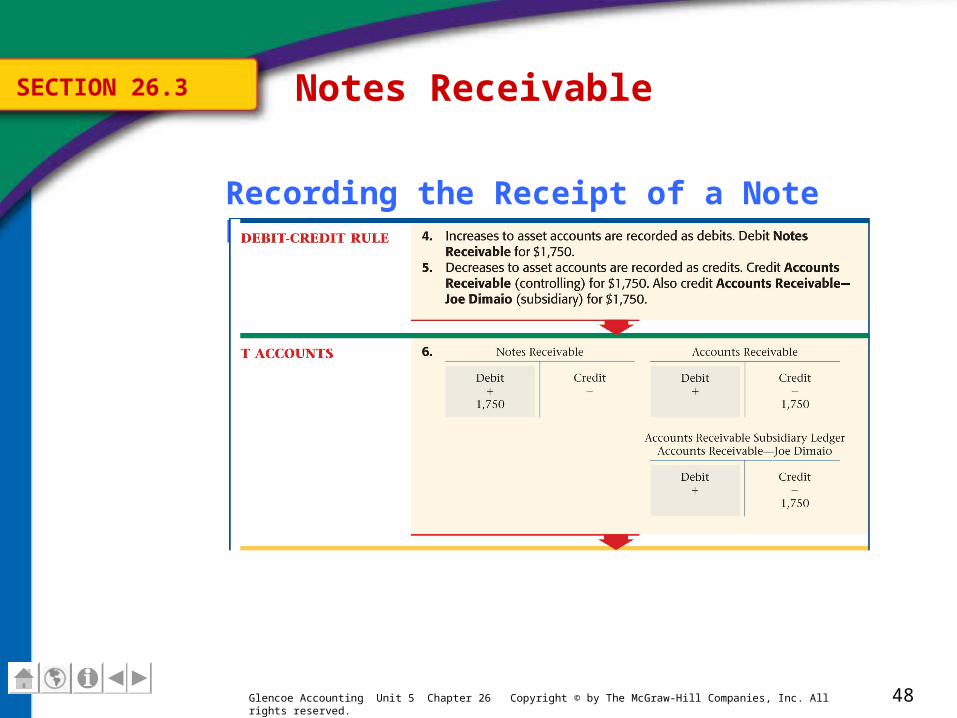

Recording the Receipt of a Note ReceivableTo record the receipt of a note receivable, follow this example.

Notes ReceivableSECTION 26.3

Page 46

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 46

Recording the Receipt of a Note Receivable

Notes ReceivableSECTION 26.3

Page 47

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 47

Recording the Receipt of a Note Receivable

Notes ReceivableSECTION 26.3

Page 48

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 48

Recording the Receipt of a Note Receivable

Notes ReceivableSECTION 26.3

Page 49

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 49

Recording the Payment of a Note ReceivableTo record a payment of a note receivable follow this example.

Notes ReceivableSECTION 26.3

Page 50

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 50

Key Term Review other revenue

Nonoperating revenue that a business receives from activities other than its normal operation.

Notes ReceivableSECTION 26.3

Page 51

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 51

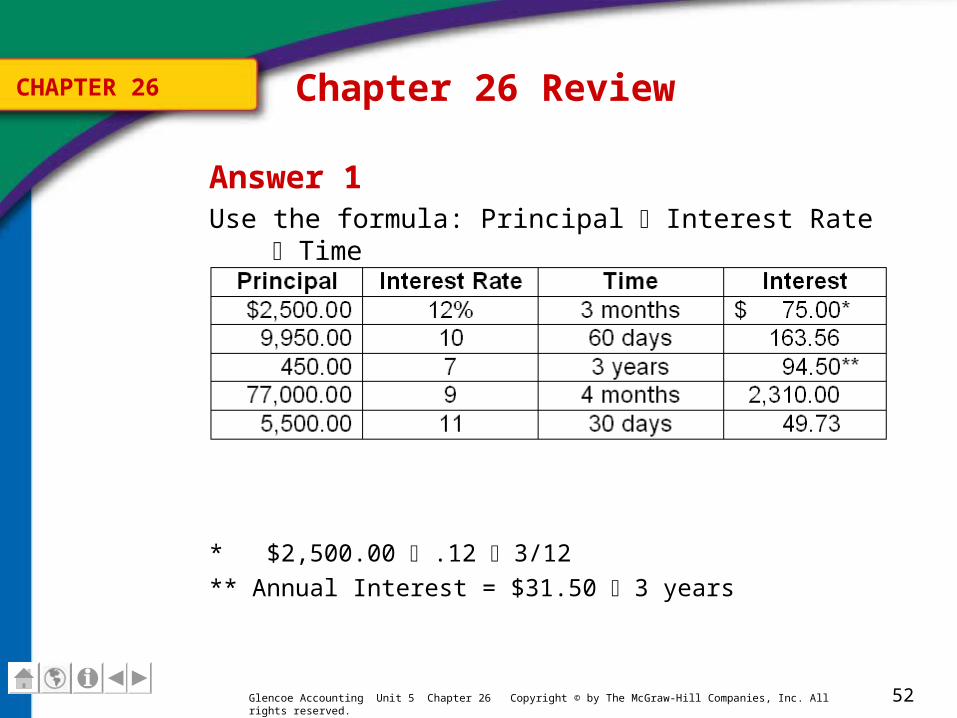

Question 1Calculate the interest for the following:

Chapter 26 ReviewCHAPTER 26

Page 52

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 52

Answer 1Use the formula: Principal Interest Rate Time

* $2,500.00 .12 3/12

** Annual Interest = $31.50 3 years

Chapter 26 ReviewCHAPTER 26

Page 53

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 53

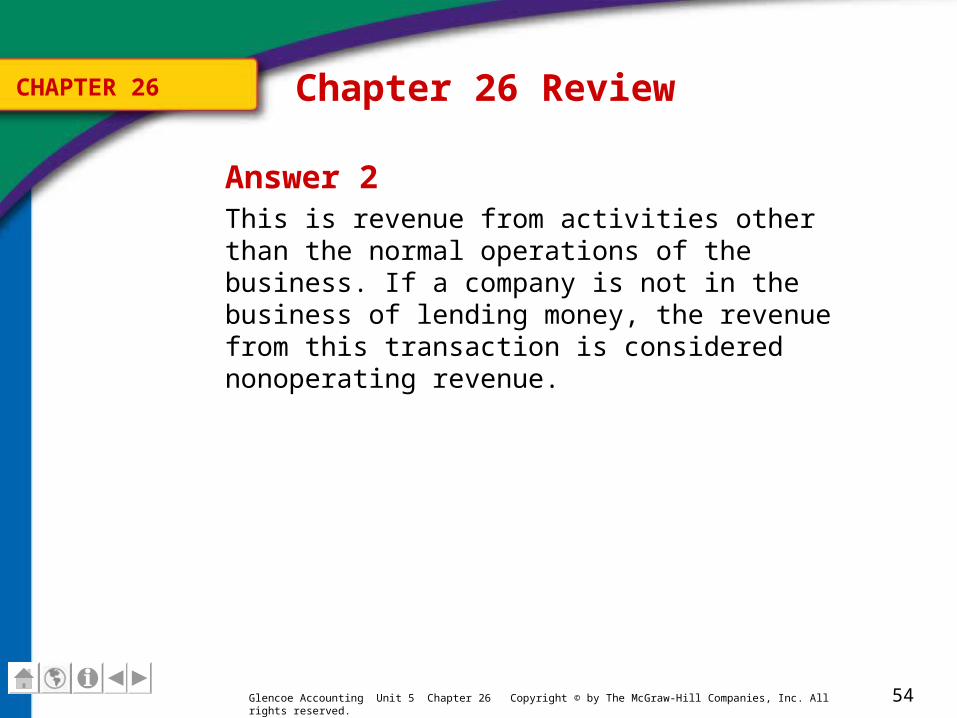

Question 2Why is interest received from customers considered “other revenue”?

Chapter 26 ReviewCHAPTER 26

Page 54

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 54

Answer 2This is revenue from activities other than the normal operations of the business. If a company is not in the business of lending money, the revenue from this transaction is considered nonoperating revenue.

Chapter 26 ReviewCHAPTER 26

Page 55

Glencoe Accounting Unit 5 Chapter 26 Copyright © by The McGraw-Hill Companies, Inc. All rights reserved. 55

Resources

Glencoe Accounting Online Learning Center

English Glossary

Spanish Glossary