16 Income Taxes Overview Financial accounting for income taxes is far more complicated then what you have experienced thus far. Previously, you probably saw income tax expense being simply recorded as “income before taxes” multiplied by a given rate. Unfortunately, accounting for income taxes isn’t quite that easy. Otherwise, an entire chapter—this chapter— would, obviously, not be needed. Having already taken a tax course before this chapter can be useful, but it is not absolutely essential. This chapter will emphasize how financial accounting is affected by different kinds of tax adjustments, rather than your knowledge of specific tax rules and regulations. Taxable income and financial income are almost always two different numbers. Hence, merely multiplying financial “income before taxes” by a constant rate every year would distort what is actually happening. Frequently, the differences between the two (financial and taxable income) are made up of numerous, even dozens, of different adjustments. There are two different kinds of adjustments. One kind is called temporary because the adjustment will reverse itself in a different year. Temporary adjustments relate to timing differences. The tax law requires a different timetable for the recognition of some revenue and expense items. Over the life of a business, the total revenue and expenses are the same for financial and taxable income when it comes to temporary adjustments. The other kind of adjustment is called permanent. Permanent differences result when an item of revenue or expense is never recorded for taxable income but is for financial income or vice versa. When a company has higher taxable income now (due to more revenue or fewer expenses on a tax basis) relative to financial income, and it is due to temporary differences, that means the company will have lower taxable income later (again, relative to financial income). Lower taxable income and, hence, taxes later is a future economic benefit, and that sounds like our definition of an asset. Hence, a company in this situation will report a deferred tax asset.

Transcript

16

Income Taxes

Overview

Financial accounting for income taxes is far more complicated then what you have experienced thus far. Previously, you probably saw income tax expense being simply recorded as “income before taxes” multiplied by a given rate. Unfortunately, accounting for income taxes isn’t quite that easy. Otherwise, an entire chapter—this chapter—would, obviously, not be needed. Having already taken a tax course before this chapter can be useful, but it is not absolutely essential. This chapter will emphasize how financial accounting is affected by different kinds of tax adjustments, rather than your knowledge of specific tax rules and regulations. Taxable income and financial income are almost always two different numbers. Hence, merely multiplying financial “income before taxes” by a constant rate every year would distort what is actually happening. Frequently, the differences between the two (financial and taxable income) are made up of numerous, even dozens, of different adjustments. There are two different kinds of adjustments. One kind is called temporary because the adjustment will reverse itself in a different year. Temporary adjustments relate to timing differences. The tax law requires a different timetable for the recognition of some revenue and expense items. Over the life of a business, the total revenue and expenses are the same for financial and taxable income when it comes to temporary adjustments. The other kind of adjustment is called permanent. Permanent differences result when an item of revenue or expense is never recorded for taxable income but is for financial income or vice versa. When a company has higher taxable income now (due to more revenue or fewer expenses on a tax basis) relative to financial income, and it is due to temporary differences, that means the company will have lower taxable income later (again, relative to financial income). Lower taxable income and, hence, taxes later is a future economic benefit, and that sounds like our definition of an asset. Hence, a company in this situation will report a deferred tax asset.

16-2 Chapter 16

If, on the other hand, a company has lower taxable income now, relative to financial income, it means the time to pay the piper will come later. Future obligations sound like liabilities, and indeed, that is the case here as well. Hence, a company in this situation will report a deferred tax liability. That’s not so difficult, right? Well, the prior discussion begins to scratch the surface, but there is even more to it than that. We also have to consider changing tax rates, the effect of net operating losses getting carried back and forward to offset taxable income, and several other issues. Plus, most companies don’t have just one adjusting item, so things can get messy when there are many adjustments going different ways and on differing schedules. It’s time to roll up your sleeves and get a little mess on you because this topic takes more than a bit of common sense and skimming over to master.

Learning Objectives

Refer to the Review of Learning Objectives at the end of the chapter. It is crucial that this section of the chapter is second nature to you before you attempt the homework, a quiz, or exam. This important piece of the chapter serves as your CliffsNotes or “cheat sheet” to the basic concepts and principles that must be mastered. If after reading this section of the chapter you still don’t feel comfortable with all of the Learning Objectives covered, you will need to spend additional time and effort reviewing those concepts that you are struggling with. The following “Tips, Hints, and Things to Remember” are organized according to the Learning Objectives (LOs) in the chapter and should be gone over after reading each of the LOs in the textbook.

Tips, Hints, and Things to Remember

LO1 – Describe the circumstances in which leasing makes more business sense than does an outright sale and purchase. How? There are three parts to a financial accounting entry dealing with income taxes. For academic purposes, you are usually given enough information to solve for two of the parts. The third is a plug to make the debits and credits equal. The two “fixed” parts are sometimes a debit to Income Tax Expense and a credit to Income Tax Payable. The third part is either a debit to Deferred Tax Asset or a credit to Deferred Tax Liability. The two fixed parts can also be the Income Tax Payable and either the Deferred Tax Asset or Deferred Tax Liability if that is the information provided. In that case, the Income Tax Expense is the plug.

Chapter 16 16-3

If financial income before taxes is given, then that number multipled by the tax rate (assuming the tax rate isn’t changing) will give you Income Tax Expense as always. If taxable income is given, or can be solved for, then that number multiplied by the tax rate will give you Income Tax Payable. If the item that gives rise to the difference between financial and taxable income is given, then that number multiplied by the tax rate will give you your Deferred Tax Asset (Liability). If the tax rate is different in future years, then Income Tax Expense will always be the plug and can’t be as easily solved for.

LO2 – Compute the amount of deferred tax liabilities and assets. Why? What is the point of a valuation allowance? First, note that valuation allowances only apply to deferred tax assets. If it is thought that a deferred tax asset will not be used, or will only partially be used, then it shouldn’t be listed, or should only be partially listed, on the balance sheet. This is similar to the allowance for bad debts. The amount of accounts receivable listed as an asset should be the amount that is expected to turn into cash, not the full amount due. When won’t a deferred tax asset be used? Perhaps the most common situation is when a company doesn’t have taxable income year after year. Without taxable income, the benefits of a deferred tax asset are no longer benefits. Many tax credits and losses that can carry forward to offset future taxable income expire. If it isn’t likely that the credits or losses will be used, because of expiration or because the company isn’t generating taxable income, then the deferred tax asset is reduced with a contra account, known as a valuation allowance.

LO3 – Explain the provisions of tax loss carrybacks and carryforwards, and be able to account for these provisions. How? When a loss is carried back and used, the calculation is as simple as multiplying the prior years’ rate(s) by the amount that was carried back and used. The entry is a debit to a receivable and a credit to an income tax benefit account, which serves to decrease (bring closer to zero) the current year loss that gave rise to the net operating loss. When a loss is carried forward, either because an election was made, there was no prior income to offset, or because there wasn’t adequate income in prior years to fully absorb the entire current year loss, there is no immediate refund. Rather, an asset is created (for the tax benefits of the future use of the net operating loss). Deferred Tax Asset receives a credit and, similar to a carryback, an income tax benefit account receives a credit.

16-4 Chapter 16

LO4 – Schedule future tax rates, and determine the effect on tax assets and liabilities. How? Future tax liabilities and tax assets should be based on future, not current, rates. If future, enacted rates change, then the current tax asset and/or liability need to be adjusted according to the new rates.

LO5 – Determine appropriate financial statement presentation and disclosure associated with deferred tax assets and liabilities. How? Classified balance sheets can have both current and noncurrent tax assets and/or liabilities. The classification of the deferred tax items are different than for others on the balance sheet. Other items are based on when they will be paid or when they will be collected. For tax assets and liabilities, however, it is based on what the asset or liability is that gives rise to the tax adjustment. Therefore, if depreciation, for instance, is going to be reversed (for book versus income tax purposes) in the coming year, it is not listed as current because it relates to “property, plant, and equipment,” which is a noncurrent asset. Tax assets and liabilities can only offset each other if they are both of the same classification (i.e., both current or both noncurrent) and both for the same jurisdiction (i.e., both federal or both a single state’s taxes).

LO6 – Comply with income tax disclosure requirements associated with the statement of cash flows. How? Taxes will always be an operating activity. Usually, the amount of income taxes paid in a period will be different than the amount of income taxes accrued. Therefore, there is frequently an adjustment to net income, using the indirect method, to arrive at the correct cash flow from operating activities as it pertains to income taxes paid. The most common adjustment relative to net income is the change in the Income Taxes Payable account. If there are changes in the Deferred Tax Asset, Deferred Tax Liability, or Income Taxes Receivable accounts, then similar adjustments will need to be made for them as well. The adustments relative to net income will move in the same directions as those for current assets (for receivables and deferred tax asset changes) and for current liabilities (for tax liability changes) as discussed back in Chapter 5.

Chapter 16 16-5

LO7 – Describe how, with respect to deferred income taxes, international accounting standards have converged toward the U.S. treatment. Why? There is little to worry about here. The methods are nearly identical internationally when it comes to the financial accounting for income taxes (even though the tax laws and rates are very different in each country). It is doubtful that you will need to know the historical differences since they no longer apply. The following sections, featuring various multiple choice questions, matching exercises, and problems, along with solutions and approaches to arriving at the solutions, is intended to develop your problem-solving and critical-thinking abilities. While learning through trial and error can be effective for improving your quiz and exam scores, and it can be a more interesting way to study than merely re-reading a chapter, that is only a secondary objective in presenting this information in this format. The main goal of the following sections is to get you thinking, “How can I best approach this problem to arrive at the correct solution—even if I don’t know enough at this point to easily arrive at the proper results?” There is not one simple approach that can be applied to all questions to arrive at the right answer. Think of the following approaches as possibilities, as tools that you can place in your problem-solving toolkit—a toolkit that should be consistently added to. Some of the tools have yet to even be created or thought of. Through practice, creative thinking, and an ever-expanding knowledge base, you will be the creator of the additional tools.

Multiple Choice

MC16-1 (LO1) The purpose of an interperiod income tax allocation is to a. show separately stated items net of tax. b. allow reporting entities whose tax liabilities vary significantly from year to

year to smooth payments to taxing agencies. c. amortize the deferred tax liability shown on the balance sheet. d. recognize an asset or liability for the tax consequences of temporary

differences that exist at the balance sheet date.

16-6 Chapter 16

MC16-2 (LO1) An example of a “deductible temporary difference” creating a deferred tax asset occurs when a. the installment sales method is used for income tax purposes, but the

accrual method of recognizing sales revenue is used for financial reporting purposes.

b. accelerated depreciation is used for income tax purposes, but straight-line depreciation is used for accounting purposes.

c. warranty expenses are recognized on the accrual basis for financial reporting purposes, but recognized as the warranty conditions are met for income tax purposes.

d. the completed-contract method of recognizing construction revenue is used for income tax purposes, but the percentage-of-completion method is used for financial reporting purposes.

MC16-3 (LO2) The Wayne Static Company had taxable income of $12,000 during 2011. Wayne Static used accelerated depreciation for income tax purposes ($3,400) and straight-line depreciation for financial accounting purposes ($2,000). Assuming Wayne Static had no other temporary or permanent differences, what would the company's pretax financial accounting income be for 2011? a. $6,600 b. $10,600 c. $13,400 d. $17,400 MC16-4 (LO2) Monteblanco Corporation paid $20,000 in January 2011 for premiums on a two-year life insurance policy which names the company as the beneficiary, an item that is never deductible for income tax purposes. Additionally, Monteblanco Corporation's financial statements for the year ended December 31, 2011, revealed the company paid $105,000 in nondeductible taxes during the year and also accrued estimated litigation losses of $200,000 which aren’t deductible until paid for income tax purposes. Assuming the lawsuit was resolved in February 2012 (at which time a $200,000 loss was recognized for income tax purposes) and that Monteblanco’s tax rate is 30 percent for both 2011 and 2012, what amount should Monteblanco report as asset for net deferred income taxes on its 2011 balance sheet? a. $0 b. $57,000 c. $60,000 d. $66,000 MC16-5 (LO3) Recognizing tax benefits in a loss year due to a loss carryforward that will likely be used requires a. only a footnote disclosure. b. creating a new carryforward for the next year. c. creating a deferred tax liability. d. creating a deferred tax asset.

Chapter 16 16-7

MC16-6 (LO3) In 2011, Boothe Corporation reported $90,000 of income before income taxes. The tax rate for 2011 was 30 percent. Boothe had an unused $60,000 net operating loss carryforward arising in 2010 when the tax rate was 35 percent. The income tax payable Boothe would report for 2011 would be a. $6,000. b. $9,000. c. $10,500. d. $27,000. MC16-7 (LO4) The following information is taken from Ibarra Corporation's 2011 financial records: Pretax accounting income $1,500,000 Excess tax depreciation (45,000) Taxable income $1,455,000 Assume the taxable temporary difference was created entirely in 2011 and will reverse in equal net taxable amounts in each of the next three years. If tax rates are 40 percent in 2011, 35 percent in 2012, 35 percent in 2013, and 30 percent in 2014, then the total deferred tax liability Ibarra should report on its December 31, 2011, balance sheet is a. $13,500. b. $15,000. c. $15,750. d. $18,000. MC16-8 (LO5) A deferred tax liability arising from the use of an accelerated method of depreciation for income tax purposes and the straight-line method for financial reporting purposes would be classified on the balance sheet as a(n) a. current liability. b. noncurrent liability. c. current liability for the portion of the temporary difference reversing within a

year and a noncurrent liability for the remainder. d. offset to the accumulated depreciation reported on the balance sheet.

MC16-9 (LO6) On the statement of cash flows using the indirect method, an increase in the deferred tax asset would be shown as a(n) a. addition to net income. b. deduction from net income. c. increase in investing activities. d. increase in financing activities. MC16-10 (LO7) International accounting standards currently are moving toward the a. no-deferral approach. b. partial recognition approach. c. comprehensive recognition approach. d. discounted comprehensive recognition approach.

16-8 Chapter 16

Matching

Matching 16-1 (LO1) Listed below are the terms and associated definitions from the chapter for LO1. Match the correct definition letter with each term number. ___ 1. financial

income ___ 2. taxable income ___ 3. deferred

income tax asset

___ 4. permanent differences

___ 5. temporary differences

___ 6. taxable temporary differences

___ 7. deductible temporary differences

___ 8. interperiod tax allocation

___ 9. deferred income tax liability

a. differences between financial and taxable income that result in future taxable amounts

b. expected future benefits from tax deductions that have been recognized as expenses in the income statement but not yet deducted for income tax purposes

c. expected future income taxes to be paid on income that has been recognized in the income statement but not yet taxed

d. an accounting method that recognizes the tax effect of temporary differences between financial and taxable income in the financial statements rather than reporting as tax expense the actual tax liability in each year

e. income reported on the financial statements as opposed to income that is reported to taxing authorities in accordance with tax regulations

f. differences between financial and taxable income that will result in deductible amounts in future years

g. income as defined by income tax regulations as the basis for determining the income tax liability for a given entity

h. differences between pretax financial income and taxable income arising from business events that are recognized for both financial and tax purposes, but in different time periods; a common example is depreciation expense on equipment

i. nondeductible expenses or nontaxable revenues that are recognized for financial reporting purposes but that are never part of taxable income

Chapter 16 16-9

Matching 16-2 (LO2, LO3, LO5) Listed below are the terms and associated definitions from the chapter for LO2, LO3, and LO5. Match the correct definition letter with each term number. ___ 1. asset and

liability method of interperiod tax allocation

___ 2. valuation allowance

___ 3. net operating loss (NOL) carryback

___ 4. net operating loss (NOL) carryforward

___ 5. effective tax rate

a. the amount of operating loss that can be carried back and offset against the income of earlier profitable years to obtain a refund of previously paid income taxes

b. rate computed by dividing reported income tax expense by earnings before income taxes

c. a method of income tax allocation that determines deferred tax assets or tax liabilities based on the expected future benefit or obligation associated with temporary difference reversals; if tax rates change, the asset or liability balances are adjusted to reflect the tax rates legislated to be in effect in the year when reversal is expected to occur

d. the amount of operating loss that can be carried forward and offset against income of future profitable years to reduce the tax liability for those years

e. a contra asset account that reduces an asset to its expected realizable value; this type of account can be used with accounts receivable and deferred tax assets

16-10 Chapter 16

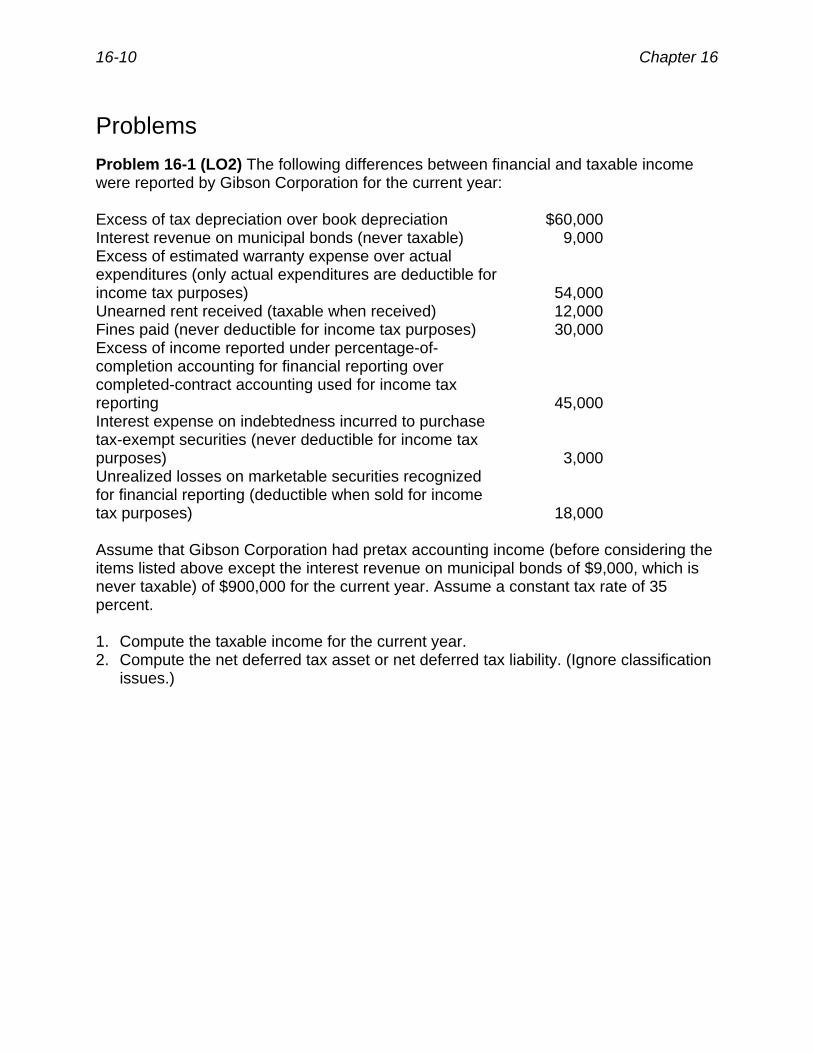

Problems

Problem 16-1 (LO2) The following differences between financial and taxable income were reported by Gibson Corporation for the current year: Excess of tax depreciation over book depreciation $60,000 Interest revenue on municipal bonds (never taxable) 9,000 Excess of estimated warranty expense over actual expenditures (only actual expenditures are deductible for income tax purposes)

54,000

Unearned rent received (taxable when received) 12,000 Fines paid (never deductible for income tax purposes) 30,000 Excess of income reported under percentage-of-completion accounting for financial reporting over completed-contract accounting used for income tax reporting

45,000 Interest expense on indebtedness incurred to purchase tax-exempt securities (never deductible for income tax purposes)

3,000

Unrealized losses on marketable securities recognized for financial reporting (deductible when sold for income tax purposes)

18,000

Assume that Gibson Corporation had pretax accounting income (before considering the items listed above except the interest revenue on municipal bonds of $9,000, which is never taxable) of $900,000 for the current year. Assume a constant tax rate of 35 percent. 1. Compute the taxable income for the current year. 2. Compute the net deferred tax asset or net deferred tax liability. (Ignore classification

issues.)

Chapter 16 16-11

Problem 16-2 (LO3) Acorn Squirrel, a corporation organized on January 1, 2003, reported the following incomes (losses) for the ten-year period, 2003–2012: Year Income (Loss) Income Tax Rate Income Tax Paid 2003 $ 16,000 50% ? 2004 (40,000) 50 ? 2005 16,000 48 ? 2006 24,000 48 ? 2007 (32,000) 45 ? 2008 16,000 42 ? 2009 32,000 42 ? 2010 64,000 34 ? 2011 80,000 34 ? 2012 (16,000) 30 ? Applying the carryback and carryforward provisions in the tax law, compute the net amount of taxes paid (amounts paid less refunds) for the ten-year period ending December 31, 2012. Problem 16-3 (LO4) Angus Associates computed a pretax financial income of $280,000 for the first year of its operations ended December 31, 2011. Included in financial income was $20,000 of nondeductible expense and $70,000 gross profit on installment sales that was deferred for income tax purposes until the installments were collected. The temporary differences are expected to reverse in the following pattern: 2012 $20,000 2013 30,000 2014 20,000 $70,000 The enacted tax rates for this year and the next three years are as follows: 2011 40% 2012 35% 2013 32% 2014 30% 1. Prepare a schedule showing the reversal of the temporary differences and the

computation of income taxes payable and deferred tax assets or liabilities as of December 31, 2011.

2. Prepare journal entries to record income taxes payable and deferred income taxes. 3. Prepare the income statement for Angus beginning with "Income from continuing

operations before income taxes" for the year ended December 31, 2011. 4. Discuss when a valuation should be placed against the deferred tax asset or

deferred tax liability that was created in part 2.

16-12 Chapter 16

Solutions, Approaches, and Explanations

MC16-1 Answer: d Approach and explanation: Don’t confuse interperiod income tax allocation with the intraperiod income tax allocation discussed in a previous chapter. Choice a goes along with intraperiod income tax allocation. “Intra” means within the same, and the placement of taxes both as a separate line item and for separately stated items (discontinued operations and extraordinary items) within the same income statement is intraperiod income tax allocation. Interperiod income tax allocation is what we are dealing with in Chapter 16. It is the recognition of assets or liabilities for income tax consequences that will affect future periods. Choice b is nonsense. Choice c is also something that doesn’t happen. If you understand the difference in the meaning between “intra” and “inter,” then, hopefully, this question wasn’t too difficult for you. MC16-2 Answer: c Approach and explanation: Check with your professor to see if you need to understand specific tax adjustments, some of which are listed in Exhibit 16-2. Some professors don’t require you to know any specific tax laws since many students may not have previously had a tax course. Others may require such knowledge. Virtually all professors will require you to understand adjustments related to this chapter when they are spelled out like they are in this question. In other words, when the timing of the revenue or expense recognition for both financial reporting and income tax reporting is given in the problem, you need to know whether that results in a temporary or permanent situation and whether it results in a taxable or a deductible difference. Deductible temporary differences result in tax deductions, relative to financial income, in later years. Hence, deferred tax assets are created out of them. Deductions, relative to financial income, include not only expenses that can be taken for income tax purposes later but also income items that are recognizable for financial accounting purposes later (and don’t have to be recognized for taxable income purposes later because they already were).

Chapter 16 16-13

For you visual learners, the following strategy in keeping these kinds of items straight may prove useful. Create a grid as follows:

Current Year (CY)

Future Year(s)

(FY) Effect on financial income (FI) relative to taxable income Effect on taxable income (TI) relative to financial income

After you get used to what is on the grid and how the grid works, you may want to shorten it to the following for quicker use on a quiz, exam, or just to help you think through a given scenario: CY FY FI TI

Using the grid for the first choice results in the following: CY FY FI + – TI – +

The first cell to fill in is either the CY FI or CY TI. If the accrual method is used for financial reporting, that means that full recognition of profit will occur in the current year. That results in the + in the CY FI cell. If the installment sales method is used for income tax purposes, recognition of profit is going to occur as cash is collected for taxable income. In other words, the taxable income is somewhat delayed compared to financial income. One of the nice things about the grid method is that you only need to come up with one cell’s correct solution. The other cells will flow off of it. Adjacent cells will always be the opposite sign and diagonal cells will be the same sign. The most important part of using the grid method is understanding what it means once you have it completed. A grid that looks like the one just completed for choice a means that taxable income will be more in the future (relative to financial income). More income tax in the future is, obviously, a liability situation. Therefore, choice a creates a deferred tax liability. An easy way to remember this, if it isn’t coming to you intuitively, is to always create your grid alphabetically (C before F and F before T), as shown. Then, look at your future column and if it shows a – on the top, you have a deferred tax liability (– signs associate more readily with liabilities). If it shows a + on the top, then you have a deferred tax asset (+ signs associate more readily with assets).

16-14 Chapter 16

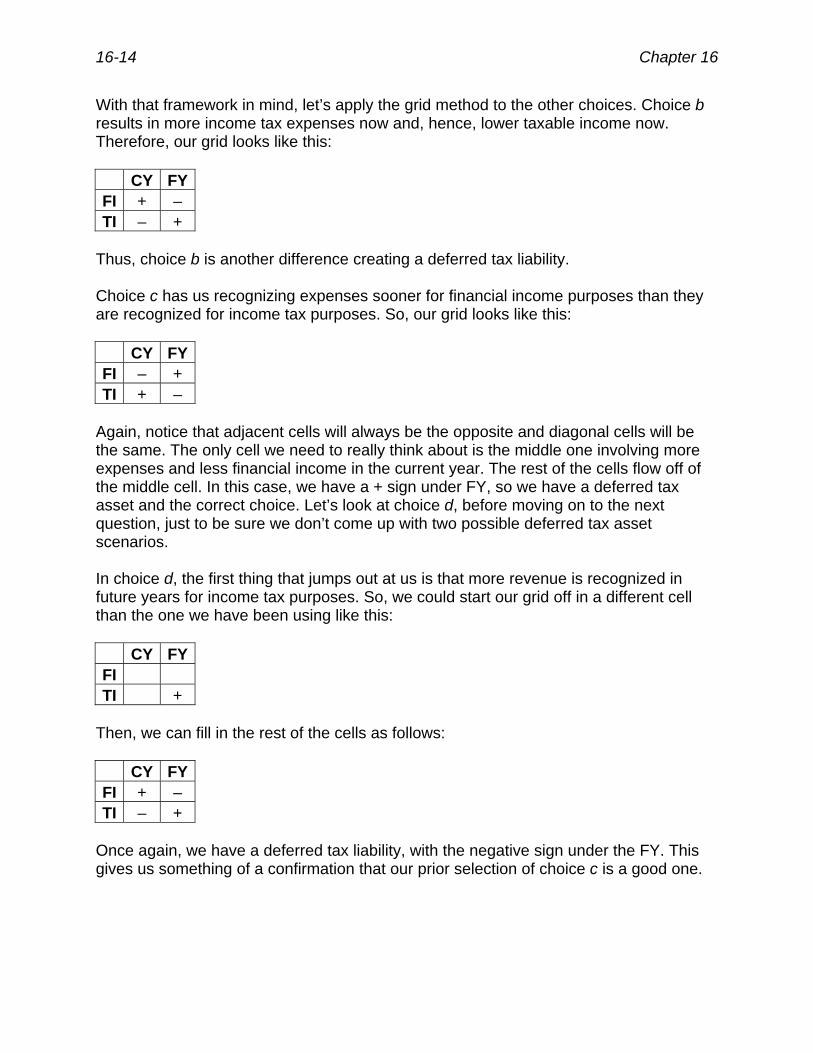

With that framework in mind, let’s apply the grid method to the other choices. Choice b results in more income tax expenses now and, hence, lower taxable income now. Therefore, our grid looks like this: CY FY FI + – TI – +

Thus, choice b is another difference creating a deferred tax liability. Choice c has us recognizing expenses sooner for financial income purposes than they are recognized for income tax purposes. So, our grid looks like this: CY FY FI – + TI + –

Again, notice that adjacent cells will always be the opposite and diagonal cells will be the same. The only cell we need to really think about is the middle one involving more expenses and less financial income in the current year. The rest of the cells flow off of the middle cell. In this case, we have a + sign under FY, so we have a deferred tax asset and the correct choice. Let’s look at choice d, before moving on to the next question, just to be sure we don’t come up with two possible deferred tax asset scenarios. In choice d, the first thing that jumps out at us is that more revenue is recognized in future years for income tax purposes. So, we could start our grid off in a different cell than the one we have been using like this: CY FY FI TI +

Then, we can fill in the rest of the cells as follows: CY FY FI + – TI – +

Once again, we have a deferred tax liability, with the negative sign under the FY. This gives us something of a confirmation that our prior selection of choice c is a good one.

Chapter 16 16-15

MC16-3 Answer: c Approach and explanation: The shortcut to this solution is to find out the difference between the income tax and financial accounting number ($3,400 – $2,000 = $1,400) and then add or subtract it to the given taxable income number to arrive at the financial accounting income solution. The problem in the shortcut is that you may add it when it should be subtracted or subtract it when it should be added. Therefore, you should probably not go the shortcut route. Instead, you should probably do a more thorough analysis to make sure that you come up with the correct solution. A question you should probably raise is, “What is taxable income without consideration of depreciation expense?” The answer is $15,400 ($12,000 + $3,400). $15,400 is also pretax financial accounting income before financial accounting depreciation expense since there are no other temporary or permanent differences between the two sets of books. Therefore, you can take the $15,400 and subtract financial accounting depreciation expense to arrive at pretax financial accounting income, which yields $13,400 ($15,400 – 2,000). Therefore, choice c must be correct. MC16-4 Answer: c Approach and explanation: For all the words in this question, the solution (and means to it) is rather quite simple. Remember, just because a problem has loads of information in it doesn’t mean that you have to use it all. Let’s look at the pieces of information that are given and see which ones can be discarded. The insurance premiums need not be used in any calculation because they are permanent differences. Permanent differences do affect calculations of taxable income versus financial income, but they have no bearing on deferred tax assets or liabilities. The same goes for nondeductible taxes paid. They are permanent adjustments and aren’t ever going to reverse for the calculations of taxable and financial accounting income. Therefore, they don’t give rise to deferred tax assets or liabilities. That leaves us with just the litigation accrual. Using the grid method, described in the explanation to MC16-2, yields the following: CY FY FI – + TI + –

Therefore, Monteblanco is going to have a deferred tax asset with respect to the temporary difference of the lawsuit. Choice a can be safely ruled out. The amount of the deferred tax asset depends on the future tax rate in the year that the deferred item will be realized on the income tax return. The tax rate will be 30 percent and the amount it is to be applied to is $200,000. Therefore, the deferred tax asset is $60,000 (0.30 percent × $200,000).

16-16 Chapter 16

MC16-5 Answer: d Approach and explanation: A loss carryforward means that a company will obtain tax deductions in the future and pay less in taxes. Future economic benefits are assets, so more than a mere disclosure occurs under this circumstance. A deferred tax asset is created with the following journal entry under this situation: Deferred Tax Asset xxx

Income Tax Benefit xxx The deferred tax asset shows up on the balance sheet if a valuation isn’t placed against it. Since this question stated that it would likely be used, no valuation is necessary. The income tax benefit shows up on the income statement, for financial accounting purposes, in the loss year. It will show up as a deduction on the income tax return in a future, non-loss year(s). MC16-6 Answer: b Approach and explanation: The prior year’s rate means nothing for the 2011 calculation. The calculation for income tax payable is ($90,000 – $60,000) × 0.30, or $9,000. If the question was asking for the income tax expense, instead of the income tax payable, the correct choice would become choice d. The journal entry for the year, assuming no other differences between financial accounting income and taxable income, would be: Income Tax Expense 27,000*

Income Tax Payable 9,000Deferred Tax Asset 18,000

*$90,000 × 0.30 = $27,000 MC16-7 Answer: b Approach and explanation: The reversal of the depreciation and amount of the deferred tax liability can be mapped out as follows: 2011 2012 2013 2014 Depreciation differences $45,000 $(15,000) $(15,000) $(15,000) Rate 35% 35% 30%

In practice, it is highly unlikely that you would ever know a tax rate more than a year in advance with any certainty. But for these kinds of theoretical problems, which you will possibly see on your course exam or the CPA Exam, make sure to use the future given rates for the calculations and not the current year rate. MC16-8 Answer: b Approach and explanation: The answer to this question is not intuitive. Choice c sounds like the most reasonable answer—an answer that makes sense given the balance sheet “rules” you learned in an earlier chapter. However, as mentioned in the How? on page 16-4, deferred tax assets and liabilities are classified based on the classification of the asset which gave rise to the temporary difference. Since property, plant, and equipment is always a noncurrent asset, a deferred tax asset or deferred tax liability associated with depreciation will always be noncurrent. MC16-9 Answer: b Approach and explanation: Deferred tax assets and deferred tax liabilities are adjusted for on the statement of cash flows in the same manner as current assets and current liabilities. Therefore, an increase in a deferred tax asset will result in the same adjustment, relative to net income, that an increase in accounts receivable would. For example, if accounts receivable is increasing it means that less cash is coming in and, hence, a negative adjustment to net income, by the amount of the increase, results. Choices c and d would never be correct for a change in a deferred tax asset or liability balance. MC16-10 Answer: c Approach and explanation: The current U.S. standards, under FAS 109, require the comprehensive recognition approach. This whole chapter has been dealing with how to account for deferred tax assets and deferred tax liabilities under the comprehensive recognition approach. The international standards have been moving closer to the U.S. standards since the mid-1990s. Choice a is the opposite extreme of the comprehensive recognition approach. It is where some countries were at just a decade or two ago. Under that approach, no deferred tax assets or deferred tax liabilities are shown on the balance sheet.

16-18 Chapter 16

Matching 16-1 1. e 2. g 3. b 4. i 5. h 6. a 7. f 8. d 9. c Complete these terminology matching exercises without looking back at the textbook or on to the glossary. After all, you probably won’t have those as a reference at test time. Learning through trial and error causes the item to be learned better and to stick in your memory longer than if you just look at the textbook, glossary, or a dictionary and “cook book” the answers. Sure you may get the answer correct on your first attempt, but missing something is sometimes best for retention. Don’t be afraid of failure while studying and practicing. Matching 16-2 1. c 2. e 3. a 4. d 5. b

Chapter 16 16-19

Problem 16-1 1. Pretax financial income $900,000

Add (Deduct) permanent differences: Interest revenue on municipal bonds (9,000) Fines paid 30,000 Interest expense on indebtedness incurred to

purchase tax-exempt securities 3,000 Total $924,000 Add (Deduct) temporary differences: Excess of tax depreciation over book depreciation $ (60,000) Excess of estimated warranty expense over actual

expenditures 54,000 Unearned rent received 12,000 Excess of income reported under percentage-of-

completion accounting for financial reporting over completed-contract accounting used for income tax reporting (45,000)

Unrealized losses on marketable securities recognized for financial reporting 18,000

Total $ (21,000) Taxable income $903,000

2. Net temporary differences equal $(21,000) (based on the difference between

$924,000 and $903,000 computed above). This means that there will be positive adjustments to taxable income, relative to financial accounting income, of $21,000 in future years. More taxes in future years indicate an obligation. The amount of the net deferred tax liability is $7,350 ($21,000 × 0.35).

Problem 16-2 Income taxes paid through December 31, 2008, net to zero because the $40,000 net operating loss in 2004 and the $32,000 net operating loss in 2007 are applied against the entire income earned for the years 2003, 2005, 2006, and 2008. Net taxes paid between January 1, 2009, and December 31, 2012, were:

Year Net Taxes

Paid 2009 $13,440 2010 16,320* 2011 27,200 2012 —

Total income taxes actually paid (2003–2012) $56,960 *After applying 2012 loss ($64,000 – $16,000) = $48,000 × 0.34 = $16,320

16-20 Chapter 16

Problem 16-3 1.

2011 2012 2013 2014 Pretax financial income $280,000

Under the provisions of FASB Statement No. 109, the classification of the deferred tax liability into current and noncurrent portions follows the classification of the underlying installment receivable.

2. Income Tax Expense—Current 92,000 Income Taxes Payable 92,000 Income Tax Expense—Deferred 22,600 Deferred Tax Liability—Current 7,000 Deferred Tax Liability—Noncurrent 15,600 Normally, as shown in the explanation to MC16-6, income tax expense is computed as pretax income multiplied by the current tax rate. In this case, that would yield a result of $112,000 ($280,000 × 0.40) instead of the $114,600 shown in the journal entries. What makes up the difference? There are two items that will cause the shortcut income tax expense calculation to not work.

Chapter 16 16-21

The first item is permanent differences. Instead of using $280,000, let’s see what happens when we use $300,000, the after-permanent-differences income number. $300,000 × 0.40 = $120,000. We didn’t get any closer. In fact, we overshot our mark by $5,400 ($120,000 – $114,600).

The second item is changing tax rates. The decreasing tax rates make up for the $5,400 difference as follows:

It is perfectly OK to use the shortcut income tax expense calculation in many situations. However, if permanent differences exist, they need to be adjusted for before the calculation. If the tax rates are changing (instead of, or in addition to, permanent differences), then it is probably easier to back into the income tax expense number by computing the income tax payable and deferred tax asset and/or deferred tax liability and then plugging the income tax expense number as the missing debit in the entry.

3.

Income from continuing operations before income taxes

$280,000

Less income taxes: Current provision $92,000 Deferred provision 22,600 114,600

Income from continuing operations $165,400 4. No valuation is ever needed for a deferred tax liability. Therefore, no valuation is

necessary in this case.

A valuation allowance against a deferred tax asset would be needed if a deferred tax asset was created and it was not more likely than not that all, or part of it, was going to be used. This situation of it not being used might arise if the company is not generating taxable income.

16-22 Chapter 16

Glossary

Note that Appendix C in the rear portion of the textbook contains a comprehensive glossary for all of the terms used in the textbook. That is the place to turn to if you need to look up a word but don’t know which chapter(s) it appeared in. The glossary below is identical with one major exception: It contains only those terms used in Chapter 16. This abbreviated glossary can prove quite useful when reviewing a chapter, when studying for a quiz for a particular chapter, or when studying for an exam which covers only a few chapters including this one. Use it in those instances instead of wading through the 19 pages of comprehensive glossary in the textbook trying to pick out just those words that were used in this chapter.

asset and liability method of interperiod tax allocation A method of income tax allocation that determines deferred tax assets or tax liabilities based on the expected future benefit or obligation associated with temporary difference reversals. If tax rates change, the asset or liability balances are adjusted to reflect the tax rates legislated to be in effect in the year when reversal is expected to occur.

deductible temporary differences Differences between financial and taxable income that will result in deductible amounts in future years; expected benefits (tax savings) are reported on the balance sheet as deferred tax assets.

deferred income tax asset Expected future benefits from tax deductions that have been recognized as expenses in the income statement but not yet deducted for income tax purposes.

deferred income tax liability Expected future income taxes to be paid on income that has been recognized in the income statement but not yet taxed. Deferred income tax liabilities often arise from the temporary tax shielding provided by accelerated depreciation.

effective tax rate Rate computed by dividing reported income tax expense by earnings before income taxes.

financial income Income reported on the financial statements as opposed to taxable income that is reported to taxing authorities in accordance with tax regulations.

interperiod tax allocation An accounting method that recognizes the tax effect of temporary differences between financial and taxable income in the financial statements rather than reporting as tax expense the actual tax liability in each year. The allocation may be made either by (1) the deferred method or (2) the asset and liability method. The latter method is currently required by GAAP.

net operating loss (NOL) carryback The amount of operating loss that can be carried back and offset against the income of earlier profitable years to obtain a refund of previously paid income taxes.

Chapter 16 16-23

net operating loss (NOL) carryforward The amount of operating loss that can be carried forward and offset against income of future profitable years to reduce the tax liability for those years.

permanent differences Nondeductible expenses or nontaxable revenues that are recognized for financial reporting purposes but that are never part of taxable income.

taxable income Income as defined by income tax regulations as the basis for determining the income tax liability for a given entity.

taxable temporary differences Differences between financial and taxable income that result in future taxable amounts; income taxes expected to be paid on future taxable amounts are reported in the balance sheet as a deferred tax liability.

temporary differences Differences between pretax financial income and taxable income arising from business events that are recognized for both financial and tax purposes, but in different time periods. For example, it is common for a temporary difference to result from depreciation expense on equipment.

uncertain tax position Might be taken by taxpayers but the tax benefits are not immeidately recognized for financial accounting purposes because those benefits are not yet more likely than not.

valuation allowance A contra asset account that reduces an asset to its expected realizable value. This type of account is used, for example, in valuing accounts receivable and deferred tax assets.