20

January 2007 Commerzbank The Leading German Commercial Bank Dr. Eric Strutz Chief Financial Officer

January 2007

CommerzbankThe Leading German Commercial Bank

Dr. Eric StrutzChief Financial Officer

1

2006: a strong year for Commerzbank Group

Various efficiency programs initiated to fund growth projects

Mittelstand and Corporates & Markets preserved strong momentum

Eurohypo successfully integrated

Strong Group performance continued along with increased earnings quality

Commerzbank is on track to achieve its mid-term targets

Commerzbank reinforced its position as the leading German commercial bank��

��

��

��

��

2

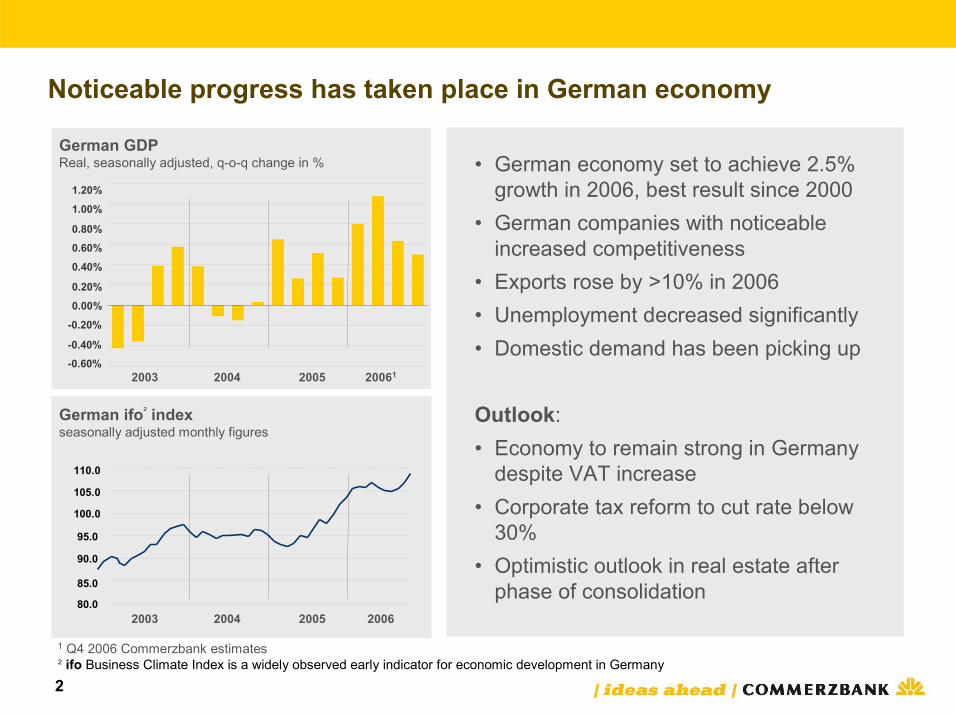

Noticeable progress has taken place in German economy

• German economy set to achieve 2.5% growth in 2006, best result since 2000

• German companies with noticeable increased competitiveness

• Exports rose by >10% in 2006• Unemployment decreased significantly• Domestic demand has been picking up

Outlook: • Economy to remain strong in Germany

despite VAT increase • Corporate tax reform to cut rate below

30%• Optimistic outlook in real estate after

phase of consolidation

German GDPReal, seasonally adjusted, q-o-q change in %

German ifo² indexseasonally adjusted monthly figures

-0.60%-0.40%

-0.20%0.00%0.20%

0.40%0.60%0.80%

1.00%1.20%

2003 2004 2005 20061

1 Q4 2006 Commerzbank estimates² ifo Business Climate Index is a widely observed early indicator for economic development in Germany

80.0

85.0

90.0

95.0

100.0

105.0

110.0

2003 2004 2005 2006

3

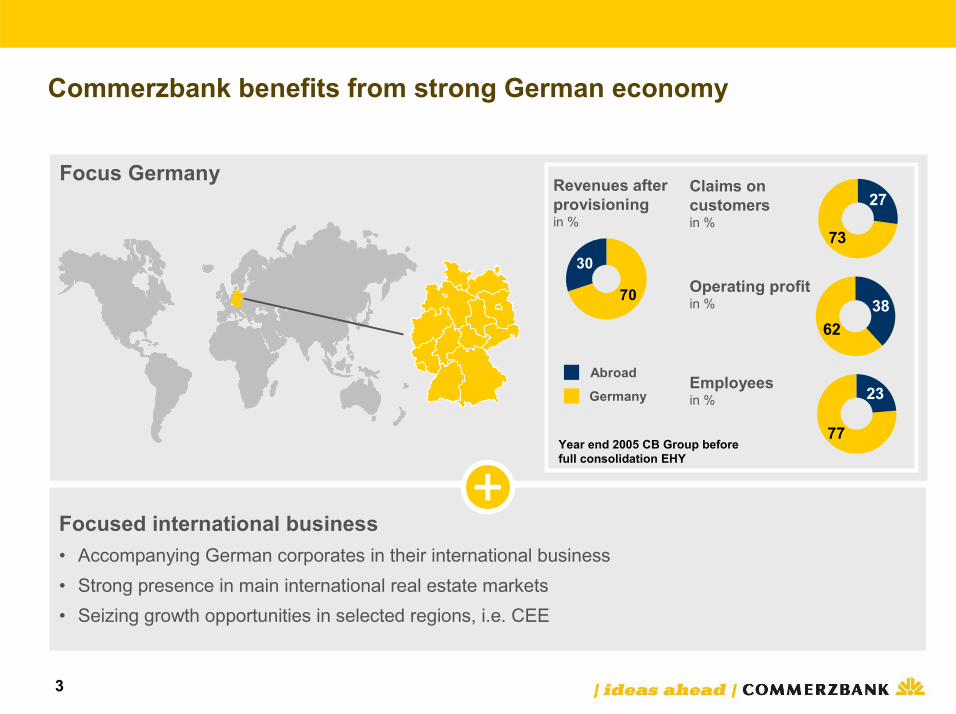

Focus Germany

Commerzbank benefits from strong German economy

Focused international business• Accompanying German corporates in their international business• Strong presence in main international real estate markets• Seizing growth opportunities in selected regions, i.e. CEE

73

62

77

Claims on customersin %

Operating profitin %

Germany

Abroad Employeesin %

Year end 2005 CB Group before full consolidation EHY

27

38

23

70

30

Revenues after provisioningin %

4

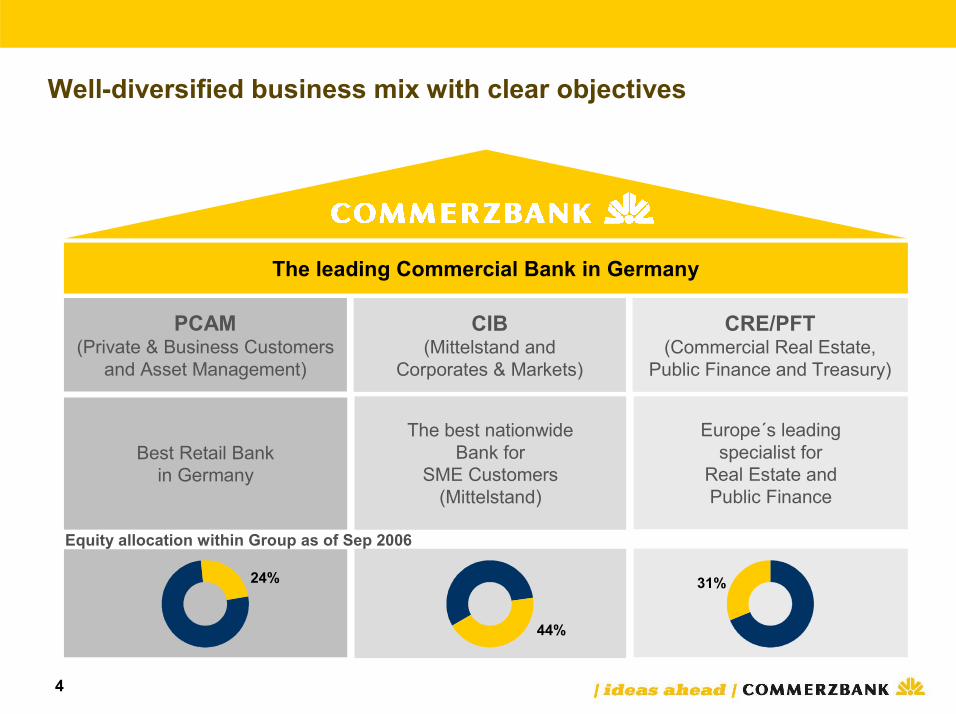

PCAM (Private & Business Customers

and Asset Management)

CIB(Mittelstand and

Corporates & Markets)

CRE/PFT (Commercial Real Estate,

Public Finance and Treasury)

The leading Commercial Bank in Germany

Best Retail Bank in Germany

The best nationwide Bank for

SME Customers (Mittelstand)

Europe´s leading specialist for

Real Estate and Public Finance

Well-diversified business mix with clear objectives

24%

44%

31%

Equity allocation within Group as of Sep 2006

5

Core segments

CRE/PFT

CIB

PCAM

• No 3 German retail bank (5m customers): high market share among affluents• No 1 in online brokerage• No 2 home finance provider• Among top 3 in private banking

Well-positioned in defined segments

• No. 2 Mittelstand (SME) bank (~ 40% of German „SME“ with CB account)• Top 10 player in CEE (BRE one of the leading banks in Poland)• Strong niche player in investment banking, i.e. leading issuer of structured

products in Germany

• No 1 in Commercial Real Estate in Germany • No 1 in Public Finance• No 1 in jumbo covered bonds

Status quo market position

6

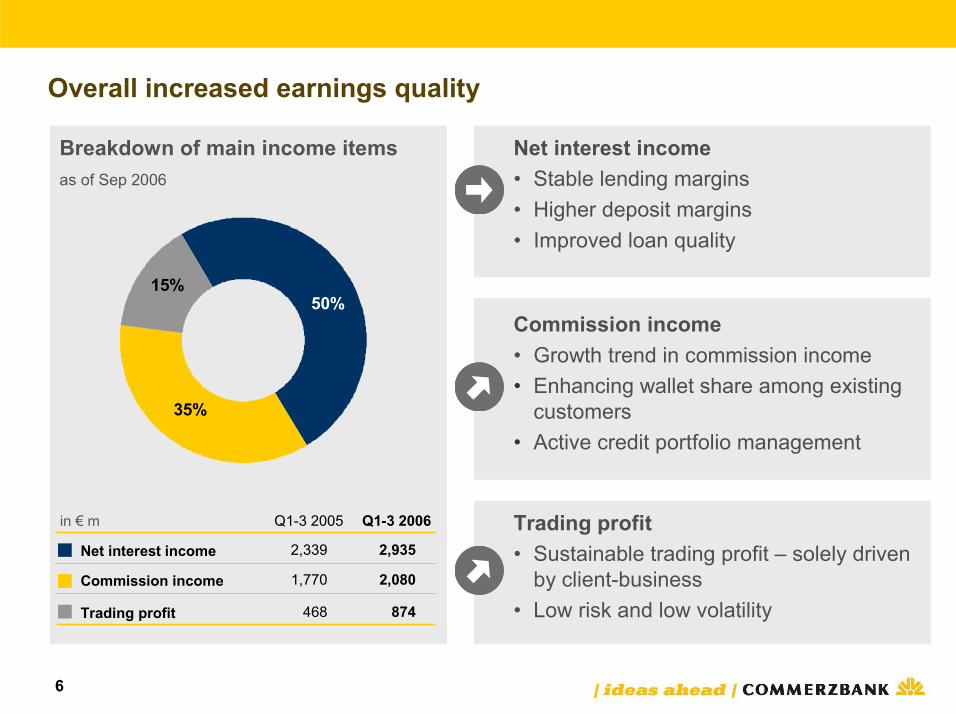

Net interest income• Stable lending margins• Higher deposit margins• Improved loan quality

Commission income• Growth trend in commission income• Enhancing wallet share among existing

customers• Active credit portfolio management

Trading profit• Sustainable trading profit – solely driven

by client-business• Low risk and low volatility

Breakdown of main income itemsas of Sep 2006

Overall increased earnings quality

15%50%

35%

Net interest income 2,935

Commission income 2,080

Trading profit 874

2,339

1,770

468

Q1-3 2006Q1-3 2005in € m

7

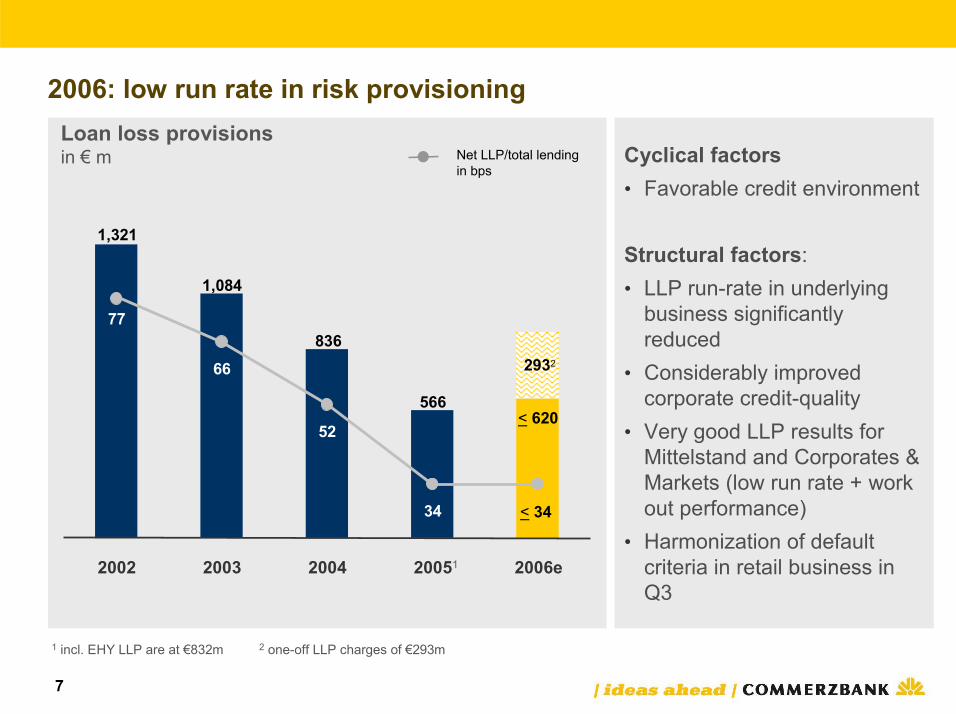

Cyclical factors• Favorable credit environment

Structural factors: • LLP run-rate in underlying

business significantly reduced

• Considerably improved corporate credit-quality

• Very good LLP results for Mittelstand and Corporates & Markets (low run rate + work out performance)

• Harmonization of default criteria in retail business in Q3

2006: low run rate in risk provisioningLoan loss provisionsin € m

1 incl. EHY LLP are at €832m

Net LLP/total lendingin bps

< 620566

836

1,084

1,321

2932

2002 2003 2004 20051 2006e

< 34

77

66

52

34

2 one-off LLP charges of €293m

8

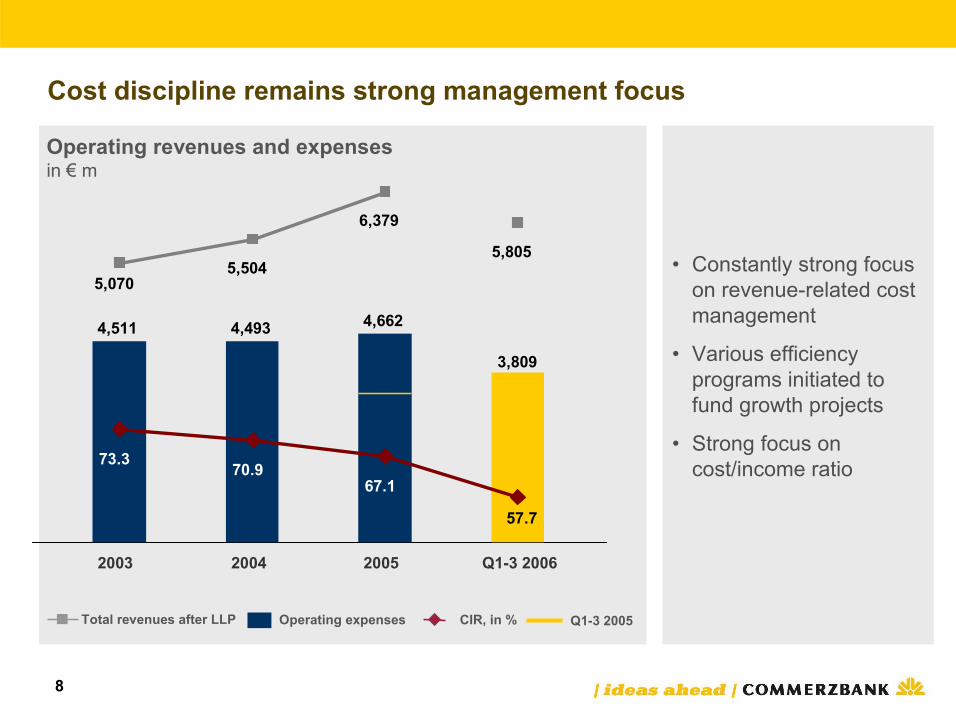

Operating revenues and expensesin € m

Cost discipline remains strong management focus

Total revenues after LLP CIR, in %Operating expenses

• Constantly strong focus on revenue-related cost management

• Various efficiency programs initiated to fund growth projects

• Strong focus on cost/income ratio

4,511 4,493 4,662

3,809

5,5045,805

6,379

5,070

2003 2004 2005 Q1-3 2006

70.9

57.7

67.173.3

Q1-3 2005

9

Operating profit in € m

1,996

559

1,011

1,717

Net return on equity (RoE)

2003 2004 2005

Operating profit and profitability increased significantly

Q1-3 2006

14.5%*

-22.3%

4.0%

12.4%

2003 2004 2005 Q1-3 2006

Q1-3 2005 * annualized

10

Commerzbank management committed to achieving more

Achievements

Financial achievements

• Strong underlying business will lead to best-ever result in 2006

Strategic achievements

• Germany’s leading commercial bank

• Europe’s leading specialist bank for real estate and public finance

Group targets

Financial targets by 2010• Sustainable profitability of 15% net RoE • CIR < 60%• Double-digit EPS growth (in %) p.a.• Steady increase in dividend

Strategic targets• Building on leading position in Germany• Leverage core competencies

��

��

11

Levers to achieve Group targets sustainable

• Optimizing capital structure via active capital management• Extracting more value per RWA

Capital

• Consistent profitability enhancement in all divisions• Strict cost management

Costs

• Risk-adjusted pricing in the light of Basel II• Prudent growth of loan book • Gradual decrease of problem loan portfolio

Risk

• Extracting more value from existing businesses (value manager)• Investing in organic growth of core divisions• Expanding in regions and products with competitive strengths • Strengthening position via selective acquisitions

Revenues1.

2.

3.

4.

12

Following a balanced approach of growth and further profitability

Self funded growth

Costs• Cost efficiency gains of

€250m to €300m p.a. from 2008 onwards

Main focus• Branch network• Credit administration (=>

reaching cost leadership)• IT and transaction banking • Facility management

Growth• Significant investment

programs in 2007 and 2008• Focused external growth

Main focus • Enhancing organic growth in

all divisions• Strengthening core division

via selective acquisitions

13

German Asset Management

• Growth of AuM• Strengthening distribution,

product quality and innovation

Overview of main efficiency and growth initiatives within GroupC

osts

PBC – Branch businessRetail / Private Banking• Further improvement in

cost efficiency of branches (Branch of the future)

• Optimizing credit administration via new credit centers

Foreign branches • Cost efficiency and

profitability enhancement in Western Europe

Mittelstand• Optimizing credit

processes => reaching cost leadership

Corporates & Markets• De-risking Investment

Banking• Reducing complexity

Gro

wth

PBC • Private Banking:

Continuing organic growth strategy

• Business Customers: New customer advisory model

• Direct Banking: Further focusing on customer growth

• Upper Retail/Affluents: Gaining new customers via new marketing approach and stronger media presence

Mittelstand• Increase wallet share

with existing customers

• Revenue growth by product initiative

• Acquiring new customers

• Strategic initiatives at BRE Bank

IT / TxB• Reducing expenses and

optimizing processes in IT and Transaction Banking

Facility Management

• Further reduction of idle office space

Eurohypo• Back office cost

reduction• Exploring further

synergy potential

External growth 2004: Takeover of

SchmidtBank2005: Acquisition of

Eurohypo2006: Acquisition of

MünchenerKapitalanlageges.

2006: Participation in Promsvyazbank

Corporates & Markets• Focus on areas with

competitive edge, i.e. derivatives and structured products CRE

• Strong focus on origination strategy• Increase of real estate capital market product range

14

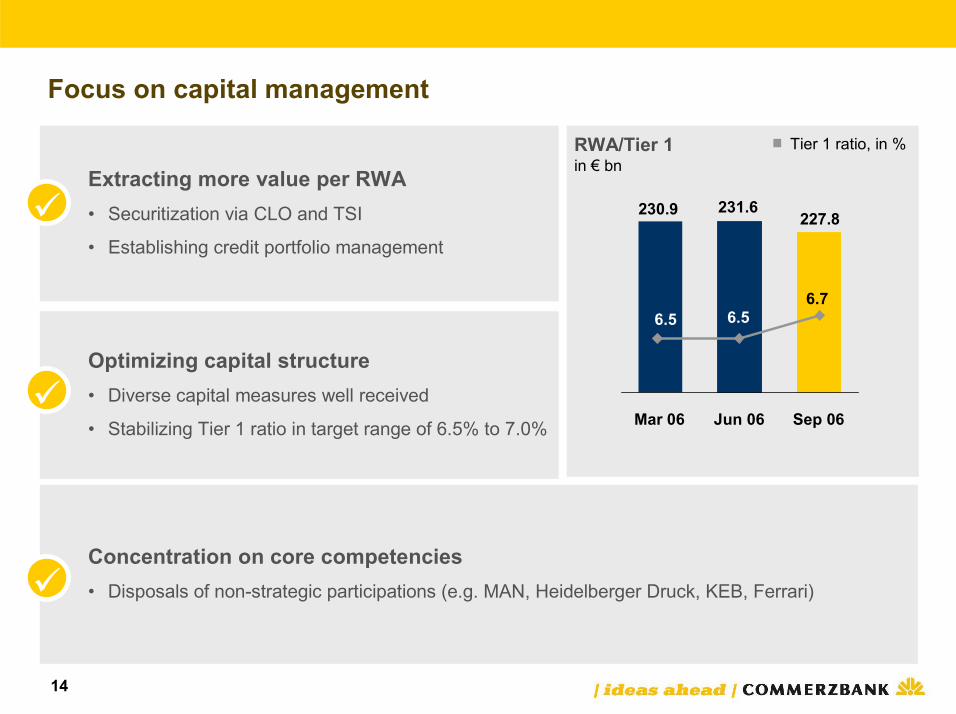

Focus on capital management

Concentration on core competencies• Disposals of non-strategic participations (e.g. MAN, Heidelberger Druck, KEB, Ferrari)

Extracting more value per RWA• Securitization via CLO and TSI

• Establishing credit portfolio management

��

Optimizing capital structure• Diverse capital measures well received

• Stabilizing Tier 1 ratio in target range of 6.5% to 7.0%��

��

RWA/Tier 1in € bn

Mar 06 Jun 06 Sep 06

Tier 1 ratio, in %

6.5 6.5

231.6227.8230.9

6.7

15

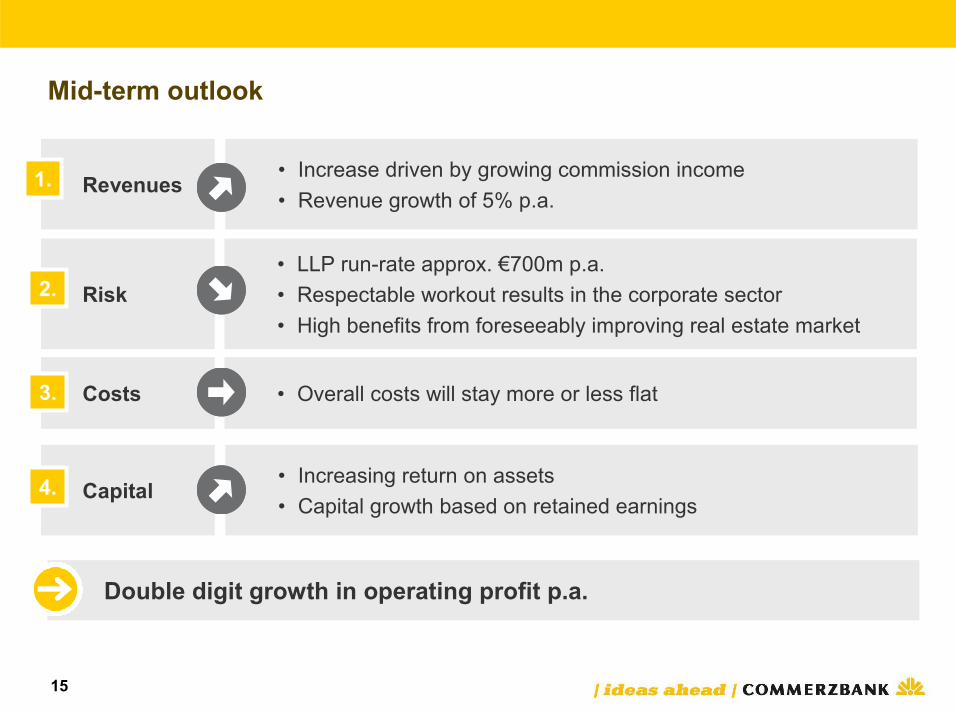

Mid-term outlook

• Increase driven by growing commission income• Revenue growth of 5% p.a.

Revenues

• Increasing return on assets• Capital growth based on retained earnings

Capital

• Overall costs will stay more or less flatCosts

• LLP run-rate approx. €700m p.a.• Respectable workout results in the corporate sector • High benefits from foreseeably improving real estate market

Risk

Double digit growth in operating profit p.a.

1.

2.

3.

4.

16

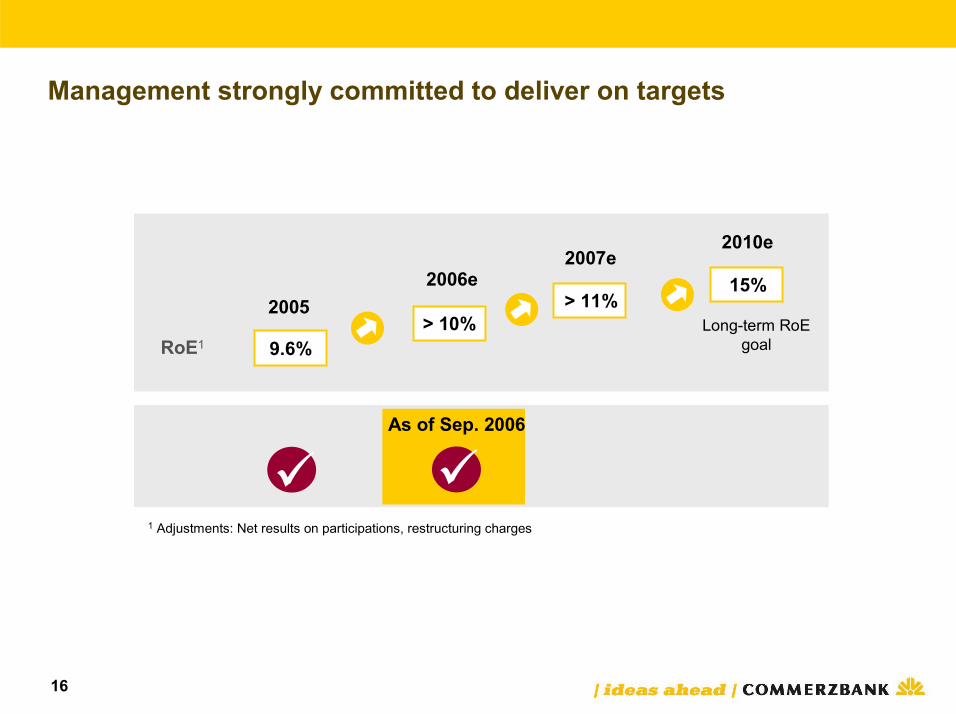

Management strongly committed to deliver on targets

2005

9.6%

2006e

> 10%

1 Adjustments: Net results on participations, restructuring charges

2010e

15%

Long-term RoEgoal

As of 1H 2006

RoE1

2007e

> 11%

���

As of Sep. 2006

�

Jürgen Ackermann (Head of IR)P: +49 69 136 22338M: [email protected]

Sandra Büschken (Deputy Head of IR)P: +49 69 136 23617M: [email protected]

Andrea Flügel (Assistant)P: +49 69 136 22255M: [email protected]

Ute Heiserer-JäckelP: +49 69 136 41874M: [email protected]

Simone NuxollP: +49 69 136 45660M: [email protected]

Stefan PhilippiP: +49 69 136 45231M: [email protected]

www.commerzbank.com/ir

For more information, please contact:

18

Disclaimer

/ investor relations /

This presentation has been prepared and issued by Commerzbank AG. This publication is intended for professional and institutional investors./Any information in this presentation is based on data obtained from sources considered to be reliable, but no representations or guarantees are made by Commerzbank Group with regard to the accuracy of the data. The opinions and estimates contained herein constitute our best judgement at this date and time, and are subject to change without notice. This presentation is for information purposes; it is not intended to be and should not be construed as an offer or solicitation to acquire, or dispose of any of the securities or issues mentioned in this presentation./Commerzbank AG and/or its subsidiaries and/or affiliates (herein described as Commerzbank Group) may use the information in this presentation prior to its publication to its customers. Commerzbank Group or its employees may also own or build positions or trade in any such securities, issues, and derivatives thereon and may also sell them whenever considered appropriate. Commerzbank Group may also provide banking or other advisory services to interested parties./Commerzbank Group accepts no responsibility or liability whatsoever for any expense, loss or damages arising out of, or in any way connected with, the use of all or any part of this presentation./Copies of this document are available upon request or can be downloaded from www.commerzbank.com/aktionaere/index.html

19

Notes

![Translating Science into Technology 070108.ppt [Read-Only] · 2009. 4. 4. · • Favorable IP regime post 2005 • Strong diaspora with high technical and managerial skills Enablers](https://static.documents.pub/doc/80x56/5ff7d693640056738b061776/translating-science-into-technology-read-only-2009-4-4-a-favorable-ip-regime.jpg)