the Star Logo, and South-Western are trademarks used herein under license.

Task Force Image Gallery clip art included in this electronic presentation is used with the

permission of NVTech Inc.

Task Force Image Gallery clip art included in this electronic presentation is used with the

permission of NVTech Inc.

F1311Accounting Accounting and and OrganizationsOrganizations

Financial Accounting

Ingram and Albright

6th edition

Information for DecisionsInformation for Decisions

1-2

ObjectivesObjectivesObjectivesObjectives

Once you have completed this chapter, you should be able to—

Once you have completed this chapter, you should be able to—

1-3

1. Identify how accounting information helps decision makers.

ObjectivesObjectivesObjectivesObjectives

ContinuedContinuedContinuedContinued

2. Compare major types of organizations and explain their purpose.

3. Describe how businesses create value.4. Explain how accounting helps investors and

other decision makers understand businesses.

1-4

5. Identify business ownership structures and their advantages and disadvantages.

ObjectivesObjectivesObjectivesObjectives

6. Identify uses of accounting information for making decisions about corporations.

7. Explain the purpose and importance of accounting regulations.

8. Explain why ethics are important for businesses and accounting.

1-5

11ObjectiveObjectiveObjectiveObjective

Identify how accounting information helps decision makers.

1-6

Accounting information helps decision makers determine where they

have been, where they are, and where they are going.

Accounting information helps decision makers determine where they

have been, where they are, and where they are going.

1-7

Maria and Stan decide to start a business selling purchased bakery

cookies to local grocery stores. They determine they can sell $12,000 of merchandise (cookies) each month.

Maria and Stan decide to start a business selling purchased bakery

cookies to local grocery stores. They determine they can sell $12,000 of merchandise (cookies) each month.

1-8

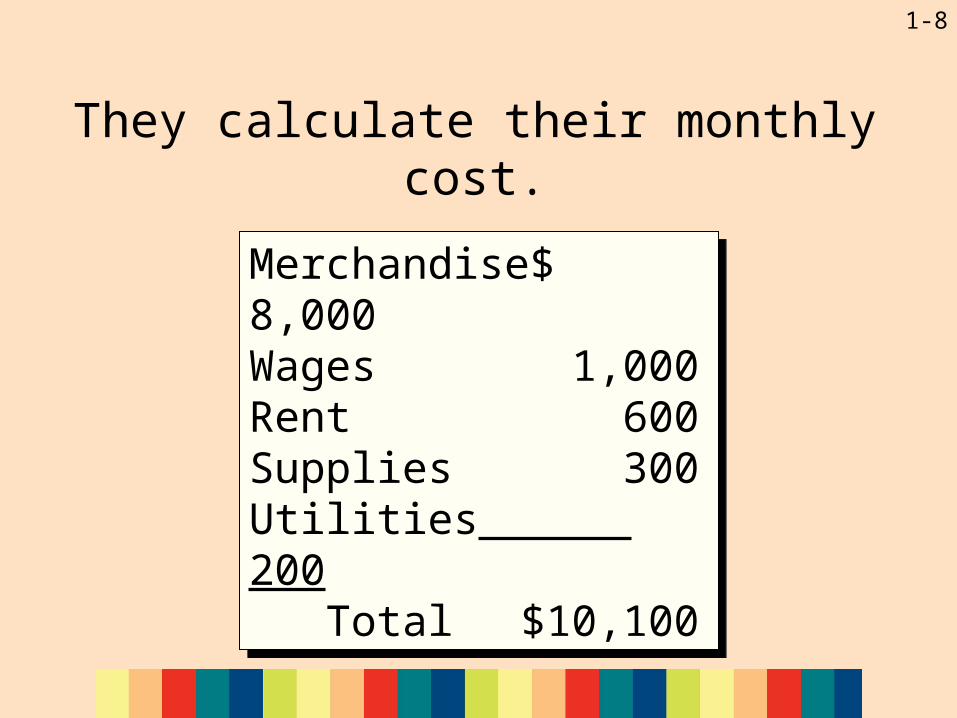

They calculate their monthly cost.

Merchandise $ 8,000Wages 1,000Rent 600Supplies 300Utilities 200 Total $10,100

Merchandise $ 8,000Wages 1,000Rent 600Supplies 300Utilities 200 Total $10,100

1-9

Profit $1,900Profit $1,900

They determine how much they expect to make from the business each month.

Merchandise sold $ 8,000Wages 1,000Rent 600Supplies 300Utilities 200 Total $10,100

Merchandise sold $ 8,000Wages 1,000Rent 600Supplies 300Utilities 200 Total $10,100

Costs

Sales of merchandise

$12,000

Sales of merchandise

$12,000

Sales

1-10

Risk is uncertainty about an outcome, such as the amount of profit a business will earn.

Risk is uncertainty about an outcome, such as the amount of profit a business will earn.

1-11

The purpose of accounting is to help people make decisions

about economic activities.

The purpose of accounting is to help people make decisions

about economic activities.

1-12

Accounting can help with these decisions by providing

information about the results that owners and other decision makers should expect to occur.

Accounting can help with these decisions by providing

information about the results that owners and other decision makers should expect to occur.

1-13

Stakeholders include—1. those who have an economic

interest in an organization and

2. those who are affected by its activities.

1-14

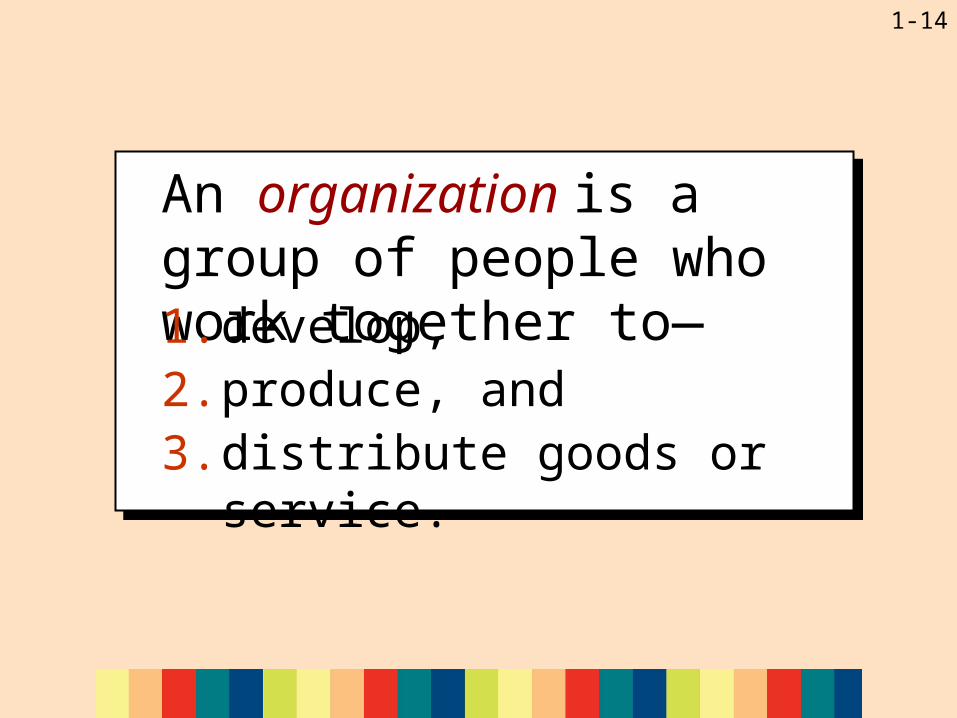

An organization is a group of people who work together to—1. develop,2. produce, and3. distribute goods or service.

1-15

22Compare major types of organizations and explain their purpose.

ObjectiveObjectiveObjectiveObjective

1-16

Exhibit 3Exhibit 3Exhibit 3Exhibit 3 Types of Organizations

1-17

Exhibit 4Exhibit 4Exhibit 4Exhibit 4 Transformation of Resources into Goods and Services

1-18

The transformation, if it meets a need of society,

creates value because people are better off after the

transformation than before.

The transformation, if it meets a need of society,

creates value because people are better off after the

transformation than before.

1-19

Exercise 1-4Exercise 1-4Exercise 1-4Exercise 1-4

Click the button to skip this exercise.

a. What type of organization provides goods or services without the intent of making a profit? Examples include the IRS and the United Way.

1. Merchandising (or retail) companies2. Manufacturing companies3. Service companies4. Governmental and nonprofit

Press “Enter” or click left mouse button for answer.

If you experience trouble making the button work, type 23 and press “Enter.”

1-20

Exercise 1-4Exercise 1-4Exercise 1-4Exercise 1-4

1. Merchandising (or retail) companies2. Manufacturing companies3. Service companies4. Governmental and nonprofit

b. What type of organization produces goods that are sold to consumers or to merchandising companies? Examples include Ford Motor Company and PepsiCo.

Press “Enter” or click left mouse button for answer.

1-21

Exercise 1-4Exercise 1-4Exercise 1-4Exercise 1-4

1. Merchandising (or retail) companies2. Manufacturing companies3. Service companies4. Governmental and nonprofit

c. What type of organization sells goods to consumers that are produced by other companies? Examples include Wal-Mart and Sears.

Press “Enter” or click left mouse button for answer.

1-22

Exercise 1-4Exercise 1-4Exercise 1-4Exercise 1-4

1. Merchandising (or retail) companies2. Manufacturing companies3. Service companies4. Governmental and nonprofit

d. What type of organization sells services rather than goods? Examples include H&R Block and Delta Air Lines.

Press “Enter” or click left mouse button for answer.

1-23

33Describe how businesses create value.

ObjectiveObjectiveObjectiveObjective

1-24

Creating Value Creating Value Creating Value Creating Value

A market is any location or process that permits resources

to be bought and sold.

A market is any location or process that permits resources

to be bought and sold.

1-25

Creating Value Creating Value Creating Value Creating Value

Accounting measures the increase in value created by a transformation as the

difference between the total price of goods and service sold and the total

costs of resources consumed in developing, producing, and selling the

goods and services.

Accounting measures the increase in value created by a transformation as the

difference between the total price of goods and service sold and the total

costs of resources consumed in developing, producing, and selling the

goods and services.

1-26

Creating Value Creating Value Creating Value Creating Value

Sales Price of Box of Cookies

Total Cost of Resources

Consumed to Produce and Make a Box of Cookies

Available

Value Added

$3.50 $3.00 $0.50– =

1-27

Profit is the difference between the price a seller receives for goods or

services and the total cost of all resources consumed in developing,

producing, and selling these goods or services during a particular period.

Profit is the difference between the price a seller receives for goods or

services and the total cost of all resources consumed in developing,

producing, and selling these goods or services during a particular period.

1-28

Favorite Cookie CompanyProfit Earnedfor January

Resources created from selling cookies $11,400Resources consumed:

Cost of merchandise sold $7,600Wages 1,000Rent 600Supplies 300Utilities 200 Total cost of resources consumed 9,700

Profit earned $ 1,700

Exhibit 6Exhibit 6Exhibit 6Exhibit 6

1-29

Exercise 1-5Exercise 1-5Exercise 1-5Exercise 1-5

Click the button to skip this exercise.

Eduardo has started a small business making sundials. The following transactions occurred for the business during a recent period. How much profit did the company earn for the period?

Press “Enter” or click left mouse button for answer.

Sales to customers $1,050Rent for the period 425Supplies used during the period 250Wages for the period 175

If you experience trouble making the button work, type 31 and press “Enter.”

1-30

Exercise 1-5Exercise 1-5Exercise 1-5Exercise 1-5

Resources created from selling sundials $1,050Resources consumed:

Rent $425Supplies 250Wages 175 Total cost of resources consumed 850

Profit earned $ 200

1-31

44Explain how accounting helps investors and other decision makers understand businesses.

ObjectiveObjectiveObjectiveObjective

1-32

Owners invest in a business to receive a return on their investments from

profits earned by that business.

Owners invest in a business to receive a return on their investments from

profits earned by that business.

ROI = Profit

Amount Invested

Investment by OwnersInvestment by OwnersInvestment by OwnersInvestment by Owners

1-33

ROI = Profit

Amount Invested

Return on investment (ROI) is the amount of

profit earned by a business that could be

paid to owners.

Return on investment (ROI) is the amount of

profit earned by a business that could be

paid to owners.

Investment by OwnersInvestment by OwnersInvestment by OwnersInvestment by Owners

1-34

If Maria and Stan invested $10,000 to start Favorite Cookie Company and

earned a $1,700 profit, what would be the return on investment?

If Maria and Stan invested $10,000 to start Favorite Cookie Company and

earned a $1,700 profit, what would be the return on investment?

ROI = Profit

Amount Invested

$1,700 $10,000

17% =

Investment by OwnersInvestment by OwnersInvestment by OwnersInvestment by Owners

Identify each of the following as describing corporations (C), proprietorships (PR), and/or partnerships (PN).

Some items have more than one answer.

Press “Enter” or click the left mouse button for answer.

a. Distinct legal entity separate from its owners.b. More than one owner.c. Ownership by stockholders.d. Controlled by a board of directors.e. Legal identity changes when a company is sold.

CC, PN

CC

PR, PN

If you experience trouble making the button work, type 60 and press “Enter.”