17

1 A preview of Mining in DRC- a new Christian Aid report Taxation for Development

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 215 times |

| Download: | 0 times |

1

A preview of Mining in DRC- a new Christian Aid report

Taxation for Development

2

Taxation as a development issue

• Taxation in the most obvious form of domestic resource mobilisation• Traditionally a neglected area- the domain of tax specialists- technical issue• ‘tax in its practical application is controlled by professional bodies, be they accounting or law. It

may suit the professions to keep tax safely within its technical box; a convenient lie to keep prying eyes from closely examining the hidden power plays at work’- Boden 2010

• Financial crisis brought focus onto financial flows, illicit flow, and taxation• G20 London 2009- Gordon Brown, crack down on tax havens- important • OECD tasked with exploring the issue further- ongoing• Picked up again at Seoul, 2010: as part of its multi year action plan on

development. Included- ‘Support the development of more effective taxation systems’

• Commission Communiqué June 2010, legislative proposals of October 2011 • Bettancourt(L’Oreal heiress) in France, Warren Buffet in states, Uncut in UK

etc all have had impact of bringing tax more mainstream, and shaped the discussion into one of tax fairness

3

All very positive• Potential to move states away from aid to something more

sustainable. • Aid flows are volatile, vulnerable to political factors• Taxation shifts accountability from donors to population- social

contract between state and citizen – ‘he who pays the piper, calls the tune’

• Incentive for government to promote economic activity• Higher governance indicators where taxation systems are

strong (Moss et al)• Potential for addressing inequality through redistribution of

wealth• Increases revenue take-Christian Aid estimate that two forms

of dodging alone deprive countries of $160 bn/yr, • OECD- more lost to tax dodging than received in aid

4

• ‘When a country makes reforms in taxation, transparency, and fighting corruption, it ignites a virtuous cycle. Taxpayers see what they’re getting for their money and they can no longer rely on the old excuses for not paying their share. Higher revenues means that the government can provide better services and pay decent wages to public employees. And so these reforms, in turn, create a more attractive climate for foreign investors and they strengthen the case we can make to our own citizens for continuing to support development programs. So if we partner with developing countries to break the vicious cycle and instead catalyze the virtuous cycle, we can not only help them provide more for their own people, but actually get on the path to self-sufficiency’ – Hillary Clinton, @ OECD, May 26th, 2011

5

Obstacles to tax collection• But yet, LIC in Africa collect about 11-15% of GDP in income tax, compared to about 35%

in OECD countries• Why?• Informal sector is large (est. 26% in Ghana, 40% Brazil)• Perception that tax burden carried by poor- rich can avoid• Legacy of colonialism- political realities change faster than long held prejudices• Tax compliancy seen as onerous-often seen as complex to tax payers. Esp. in countries

with low literacy levels, educational disadvantages, or different languages within country• Low capacity of revenue authorities and oversight bodies in country• Corruption between tax payers (citizens and foreign companies) and revenue authorities• Global financial regulation system does not do enough to curb to tax avoidance• The lack of transparency in the global financial regulation system, including the disclosure

and reporting requirements of MNCs, as well as the extensive use of tax havens makes it easy for some unscrupulous MNCs to pay little or no tax in developing countries.

• Use of tax havens- African Union estimate %150 billion from African-80% to havens

6

Greater transparency required

• Inter jurisdictionally: greater exchange of information on an automatic basis

• Intra-company: greater transparency in the reporting of multinational companies, including the profits made and taxes paid, in each of the jurisdictions in which they operate

7

Mining in DRC• 2 high profile cases involving international companies took place in 2010.• Involved disputes over millions of dollars of DRC mineral resources • Interesting things was that they took place not in DRC, not in London, or

Toronto, where these companies or listed- but in tax havens!1. FG Hemisphere’s vulture fund case against Groupement de Terrill de Lubumbashi(GTL) took place in Jersey2. Canadian firm First Quantum and ENRC took place in British Virgin Islands

• Not unusual!• Lundin in Sweden, Freeport McMoran(US) through Bermuda• ENRC various companies in the BVI• The company extracting from Terrill de Lubumbashi slagheap in registered

in Jersey• Glencore’s investment in Kamoto Copper Company appears to be routed

through various jurisdictions incl. Bermuda, Guernsey, Switzerland, BVI, and IoM

8

Mining companies presence in DRC and havens

- Attraction of tax haven- strong financial sectors, greater certainty for investments- but also financial secrecy, and possibility of profit shifting within a group of companies, so that costs are allocated to high tax jurisdictionsImpact of company structures such as this is that it is hard to assess how much profit group in making from particular project- looking at available data on how much profit is being paid in industrial mining sector- remarkably low, suggesting profits are being shifted offshore on a large scale. Well established method for doing this if companies wish to engage in this.

9

Congo• DRC- diamonds, coltan, tin, oil, natural • 34% of world’s cobalt, 10% of worlds copper reserves• WB- tax revenues as share of GDP are among the lowest in

the world• Weak governance, democracy in its infancy• Most of the mining investment comes if form of joint ventures-

overseas investors and one of DRC’s state mining companies (Gecamines or Sodimico) with minority holding.

• By such structures, and by keeping profits low, or shifting them offshore, companies can avoid paying profit tax, but also avoid paying the (typically) 20%-25% profit dividends, it is entitled to as minority shareholder.

• The lack of transparency makes it impossible to conclusively determine whether profit shifting is taking place.

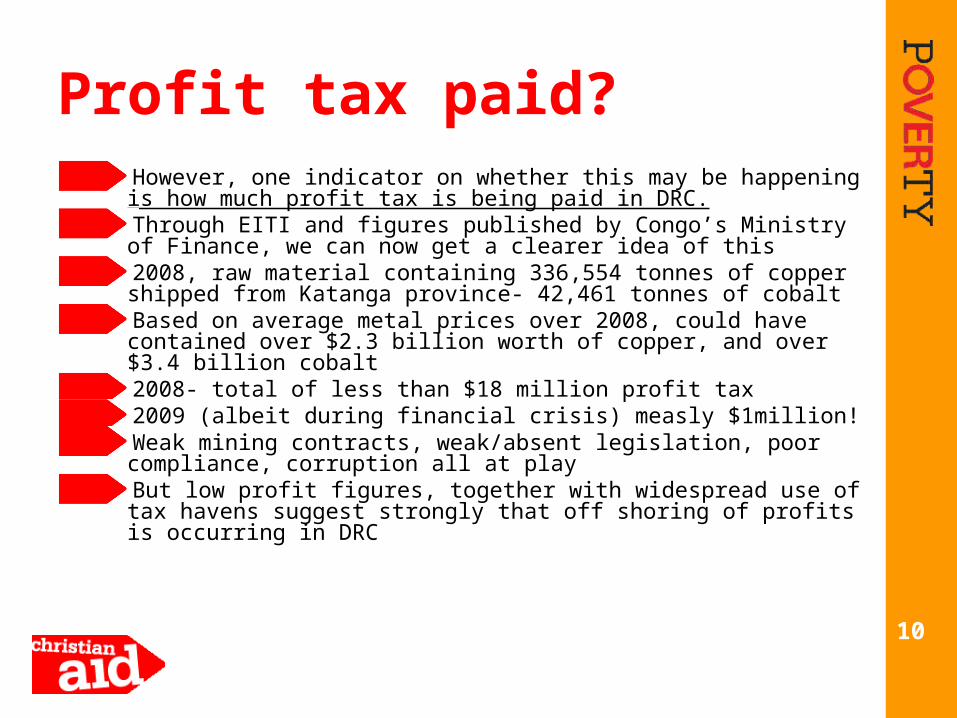

10

Profit tax paid?However, one indicator on whether this may be happening is how much profit tax is being paid in DRC.Through EITI and figures published by Congo’s Ministry of Finance, we can now get a clearer idea of this2008, raw material containing 336,554 tonnes of copper shipped from Katanga province- 42,461 tonnes of cobaltBased on average metal prices over 2008, could have contained over $2.3 billion worth of copper, and over $3.4 billion cobalt2008- total of less than $18 million profit tax2009 (albeit during financial crisis) measly $1million!Weak mining contracts, weak/absent legislation, poor compliance, corruption all at playBut low profit figures, together with widespread use of tax havens suggest strongly that off shoring of profits is occurring in DRC

11

One mechanism:mispricing of international trade

The OECD arms length price principle should govern intra-group sales

But companies can over price or under price exports to shift money in and out of a country

By looking at EU customs data we can see how imports from DRC are priced e.g. cobalt imports from EU over last 10 years

12

2000-2010 DRC is the largest supplying country of cobalt to EU countries.

Cobalt Export to EU 2000- 2010Weight (ton)

0

20

40

60

80

100

120

140

160

Congo-D

Malaysi

S.Africa

Australi

Congo

Tanzani

Canada USA

Russia

Brazil

Zambia

Morocco

Norway

Netherla UK

Japan

Germany

Uganda

Belgium

China

France

Finland

Thou

sand

s

13

Average Unit Value by Exporting CountryCobalt Mattes Export to EU 2000-2010

Cobalt Export to EU 2000- 2010Average unit value

€0

€5

€10

€15

€20

€25

€30

€35

€40

€45

Congo-D

Malaysi

S.Africa

Australi

Congo

Tanzani

Canada USA

Russia

Brazil

Zambia

Morocco

Norway

Netherla UK

Japan

Germany

Uganda

Belgium

China

France

Finland

EUR

1,00

0 p

er t

on

14

DRC's Export Price of Cobalt Mattes to Finland

15

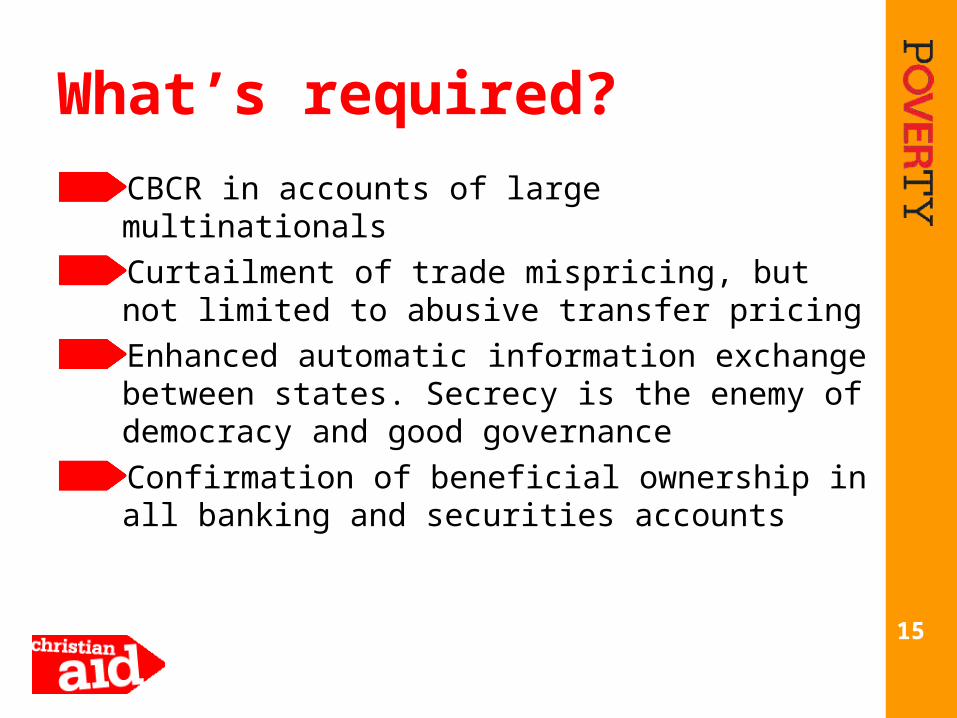

What’s required?

CBCR in accounts of large multinationals

Curtailment of trade mispricing, but not limited to abusive transfer pricing

Enhanced automatic information exchange between states. Secrecy is the enemy of democracy and good governance

Confirmation of beneficial ownership in all banking and securities accounts

16

WB 2008- mining sector in DRC could contribute 20-25% of GDP, and one third of total tax receiptsGreater political will- damaging effects of tax havens are well documented, but little to say about their positive effects. When has financial secrecy contributed to enhanced democracy? Aid remains the easier option compared to tackling capital flow from Africa- but it has potential to be a lot more important