27

1 Budgets and budgetary control Lecture 2 Semester B Dr. Haider Shah Dr. George H. Papadopoulos

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | randall-skinner |

| View: | 214 times |

| Download: | 1 times |

1

Budgets and budgetary control

Lecture 2

Semester B

Dr. Haider ShahDr. George H. Papadopoulos

2

Learning outcomes

Understand preparation of production budget

Understand preparation of cash budget

Understand use of flexed budget

3

Sales Budget

Sales forecast prepared ( normally various drafts before a final achieved)

Production capacity forecast prepared

Based on these the Sales Budget prepared in detail

4

Production & related budgets

Is this the ‘principle budget factor’?

Need to check

5

Production & related budgets

Production director may need to face problems of excesses or shortfalls in capacity

Final budget will reflect quantities and costs for each product and product group.

Must cross relate with Sales budget and various inventory budgets

6

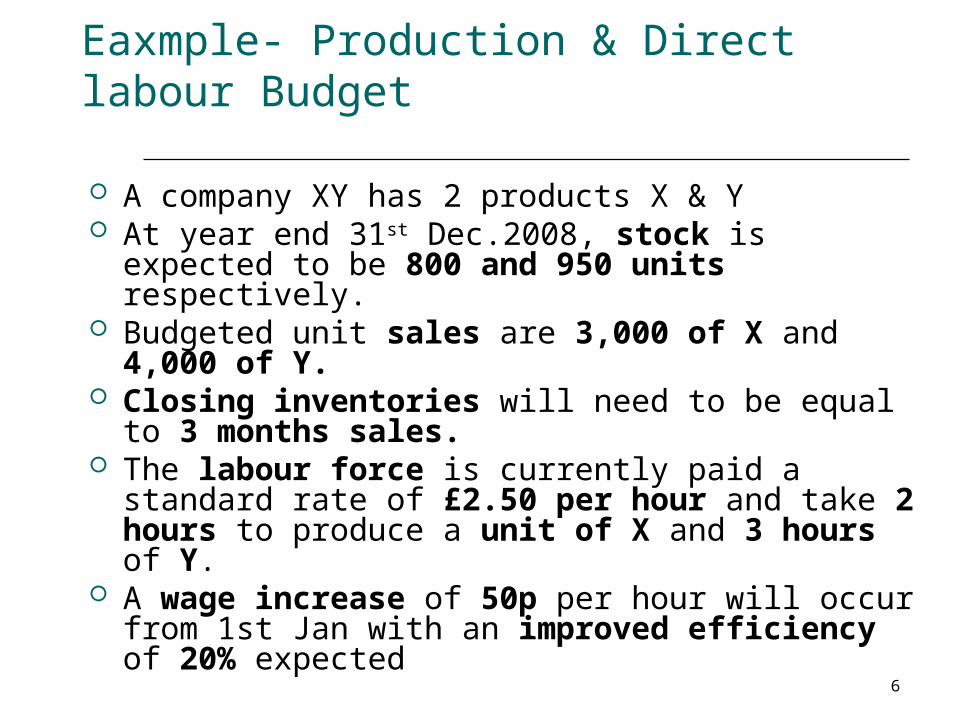

Eaxmple- Production & Direct labour Budget

A company XY has 2 products X & Y At year end 31st Dec.2008, stock is expected to

be 800 and 950 units respectively. Budgeted unit sales are 3,000 of X and 4,000

of Y. Closing inventories will need to be equal to 3

months sales. The labour force is currently paid a standard

rate of £2.50 per hour and take 2 hours to produce a unit of X and 3 hours of Y.

A wage increase of 50p per hour will occur from 1st Jan with an improved efficiency of 20% expected

7

Production Budget- Product X

Units Units

Sales 3,000

Closing stock (3/12 x 3,000) 750

Opening stock 800

Decrease)/ increase in Stock (50)

Production requirement 2,950

8

Direct Labour Budget - Product X

Hours reqd. = 2,950 x 2 x 0.80 = 4,720 hours

Cost:4,720 x (£2.50 + £0.50) = £14,160

9

Production Budget- Product Y

Units Units

Sales 4,000

Closing stock (3/12 x 4,000) 1000

Opening stock 950

Decrease/ increase in Stock 50

Production requirement 4050

10

Direct Labour Budget - Product Y

Hours reqd. = 4050 x 3 x 0.80 = 9,720 hours

Cost:9,720 x (£2.50 + £0.50) = £29,160

11

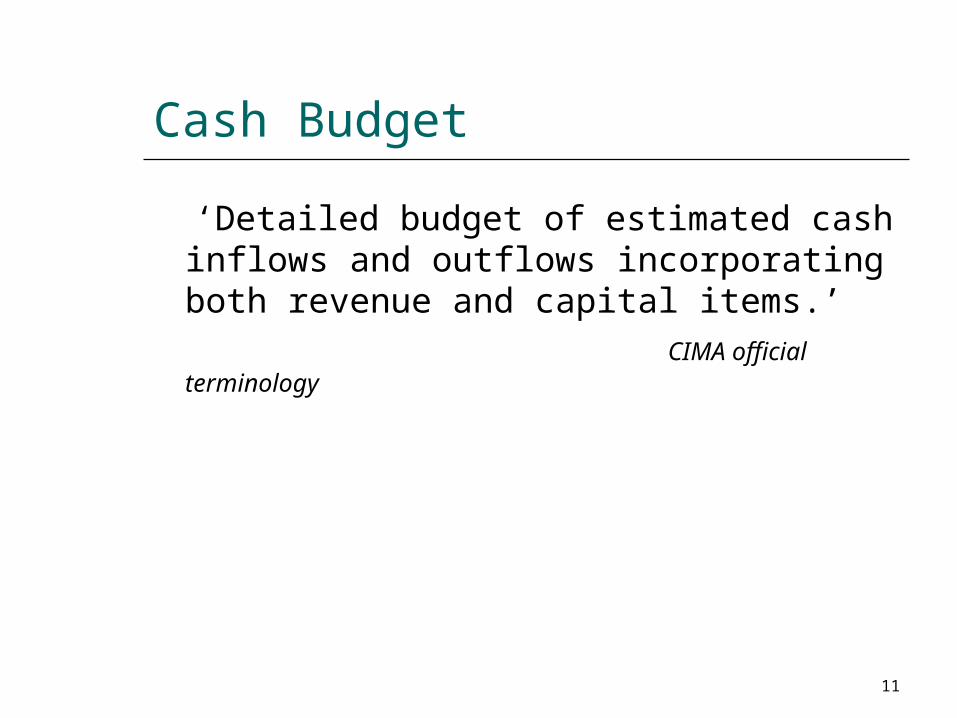

Cash Budget

‘Detailed budget of estimated cash inflows and outflows incorporating both revenue and capital items.’

CIMA official terminology

12

Solving cash flow problems Short-term surplus 1. Make short term investments2. Use it to finance growth(e.g.debtors)3. ...

Short-term deficit1. Reduce receivables2. Review payables (timing / delay)3. ...

13

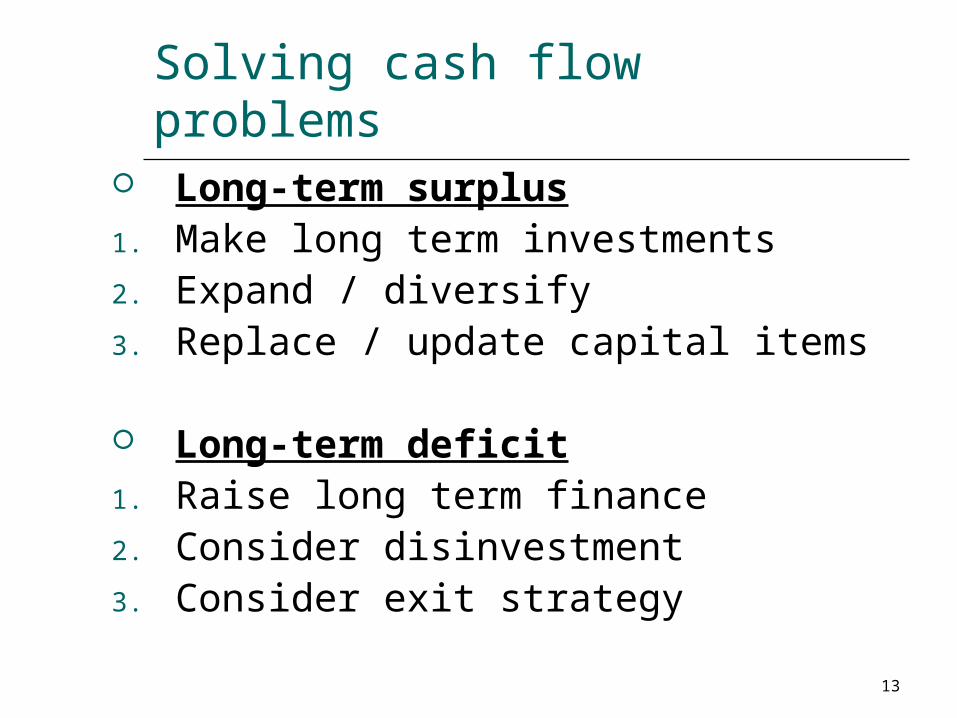

Solving cash flow problems Long-term surplus 1. Make long term investments2. Expand / diversify3. Replace / update capital items

Long-term deficit1. Raise long term finance2. Consider disinvestment3. Consider exit strategy

14

Cash Budget – monthly basis

How much you already have in pocket at start of this month?

How much would you need to pay? How much would you receive? (from

work, parents, friends) How much would be the balance in

the end? This will be starting balance for next

month

15

Cash budgets – a proforma Month 1 Month 2 £ £

Opening balance (a) x x

Cash Receipts:Sales x x

Other x x

(b) x x

Cash PaymentsPurchases x x

Other x x

(c) x x

Net cashflow (b-c) X X X X

Closing balance (a+b-c) X X

16

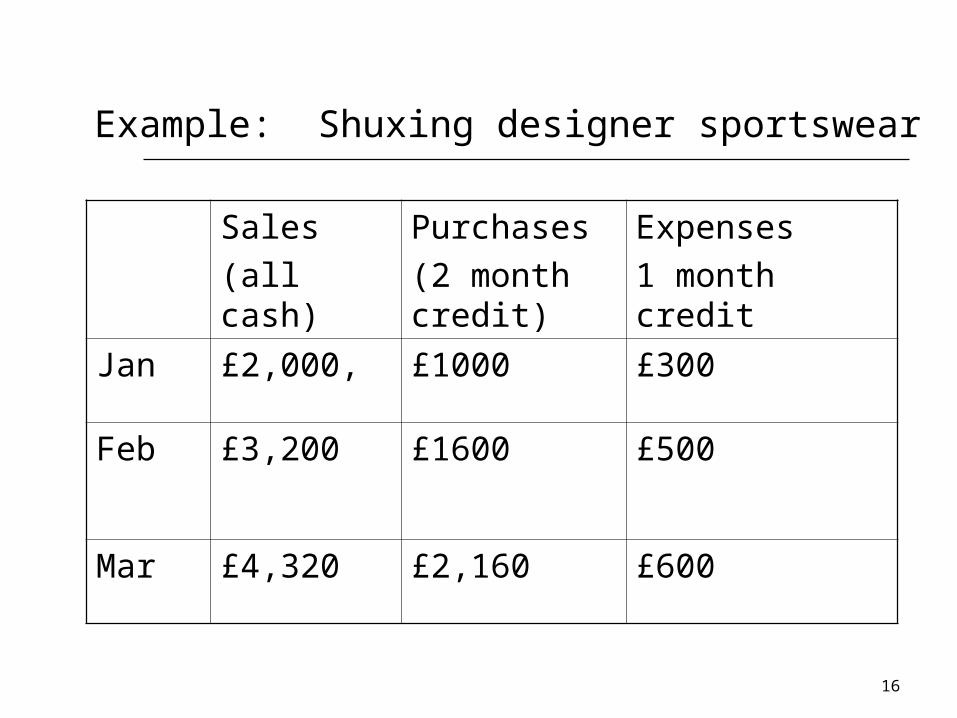

Example: Shuxing designer sportswear

Sales(all cash)

Purchases(2 month credit)

Expenses1 month credit

Jan £2,000, £1000 £300

Feb £3,200 £1600 £500

Mar £4,320 £2,160 £600

17

• Rent and rates £4,000, payable quarterly starting on 1st March.• She receives an interest free loan from her parents in February for £1,000• She buys a computer (£2,000) in January• Equipment(£5,000) is to be paid for in on 1st January • Opening cash balance is £1,000

REQUIRED Using the pro forma, prepare a cash budget for Shuxing for the first three months of trading. Interpret her cash position, explaining her options.

Shuxing designer sportswear

Control and Controls

Finish

Control is the ability to stay on the path which leads to the desired end.

Controls are the devices with which you are able to exercise control. e.g brake, clutch, gear, mirrors etc

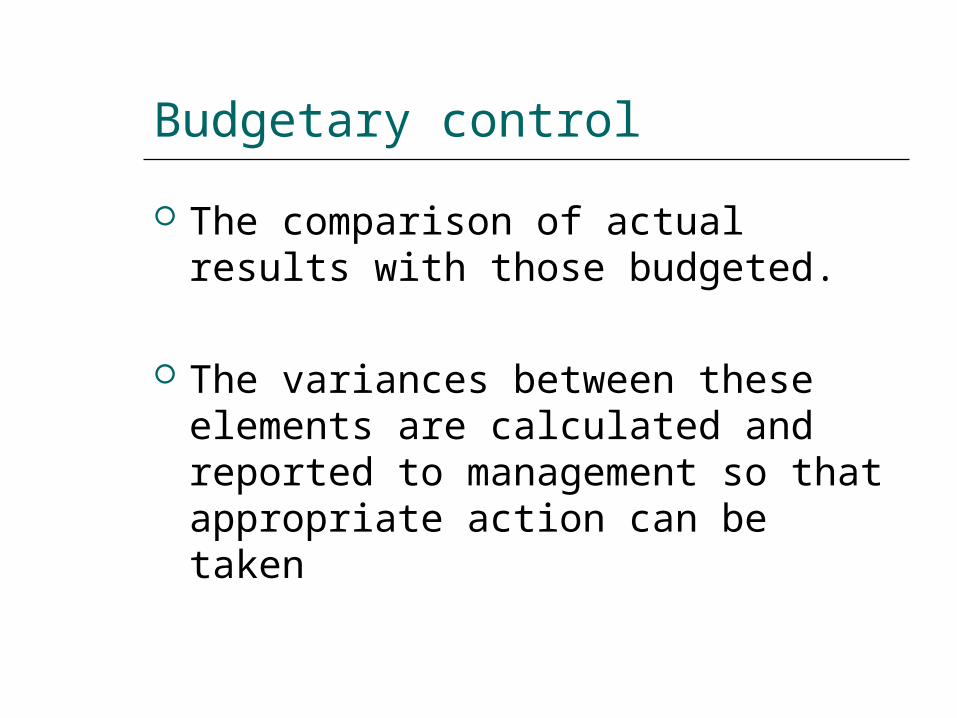

The comparison of actual results with those budgeted.

The variances between these elements are calculated and reported to management so that appropriate action can be taken

Budgetary control

Budgets can be viewed either as:

Fixed :

◦ do not change with the level of activity ( A major limitation for control purposes)

or

Flexed ◦ are the opposite they are constructed such

that they can be altered to reflect the actual activity achieved. So excludes any volume variance from the total variance.

Budgetary control

A Flexed budget excludes any volume variance from the total variance.

Impact of Volume

£10

£8

£11

UH sports café sold 156 mars bars in a week for £62.40.

It had a budget of 150 bars at £67.50.

This gives a variance of £5.10. What caused this variance?

Example:

Qty Price TotalActual = 156 0.40 62.40

Budget = 150 0.45 67.50

Variance 5.10 UCauses

Volume = 6 0.45 2.70 FPrice = 156 0.05 7.80 UTotal variance 5.10 U

A Flexible budget would eliminate the volume variance

Answer UH sports cafe

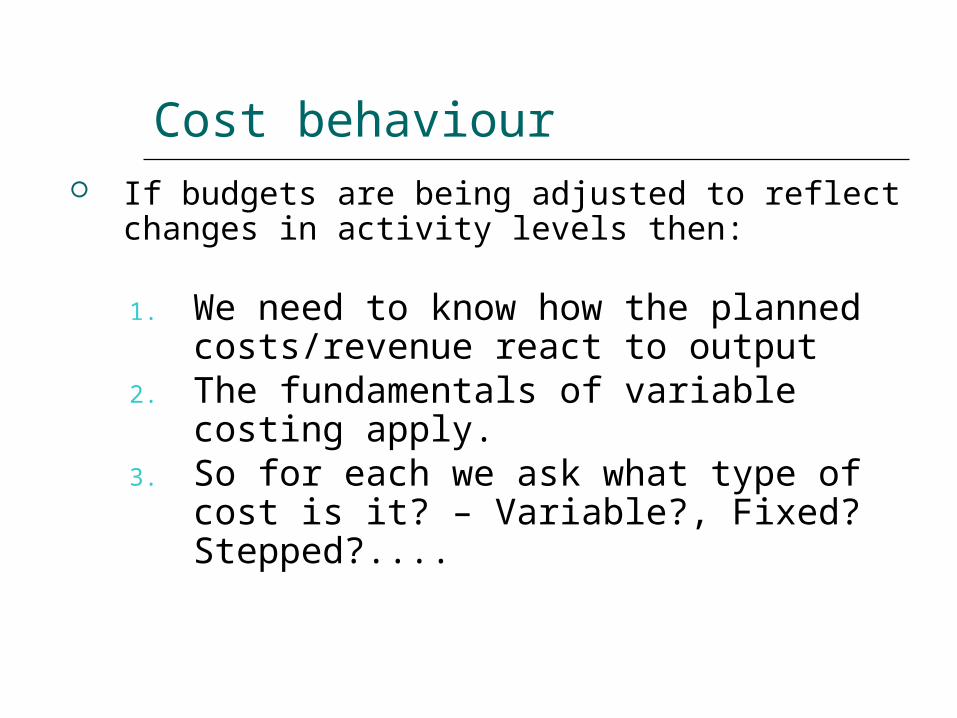

If budgets are being adjusted to reflect changes in activity levels then:

Cost behaviour

1. We need to know how the planned costs/revenue react to output

2. The fundamentals of variable costing apply.

3. So for each we ask what type of cost is it? – Variable?, Fixed? Stepped?....

At the planning stage If output is uncertain then a number of flexible

budgets may be constructed and then the outcomes can be assessed prior to the acceptance of one as the fixed. (‘What if?’ analysis)

At the control stage Businesses are dynamic, so its improbable that

actual activity will match that what was planned Management need to know what elements have

caused a variance in order to exert control and react

Importance of flexible budgets

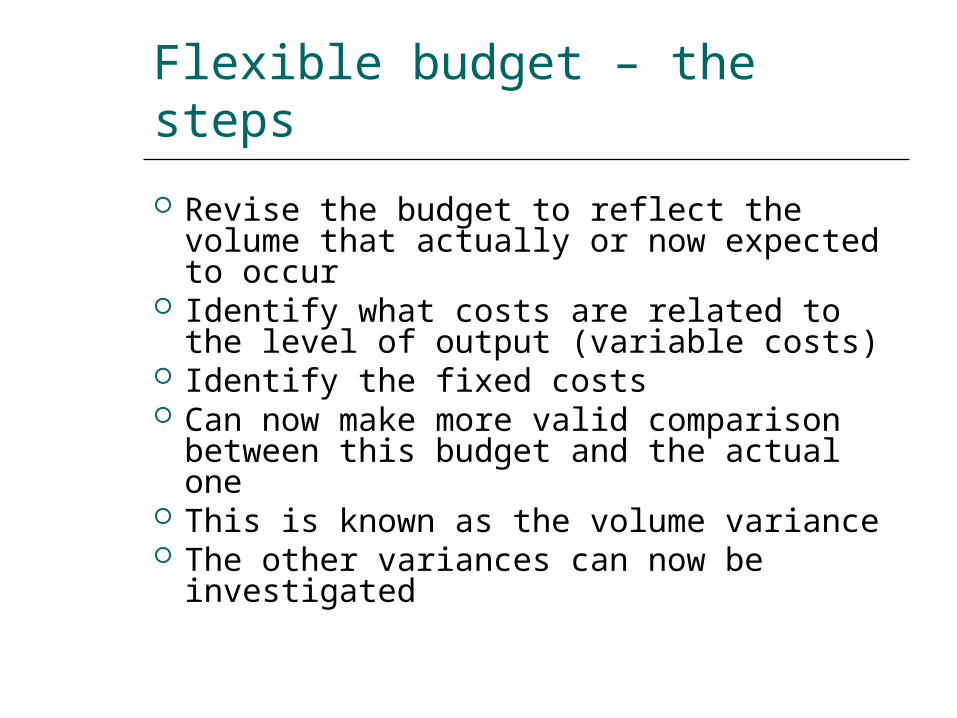

Revise the budget to reflect the volume that actually or now expected to occur

Identify what costs are related to the level of output (variable costs)

Identify the fixed costs Can now make more valid comparison

between this budget and the actual one This is known as the volume variance The other variances can now be

investigated

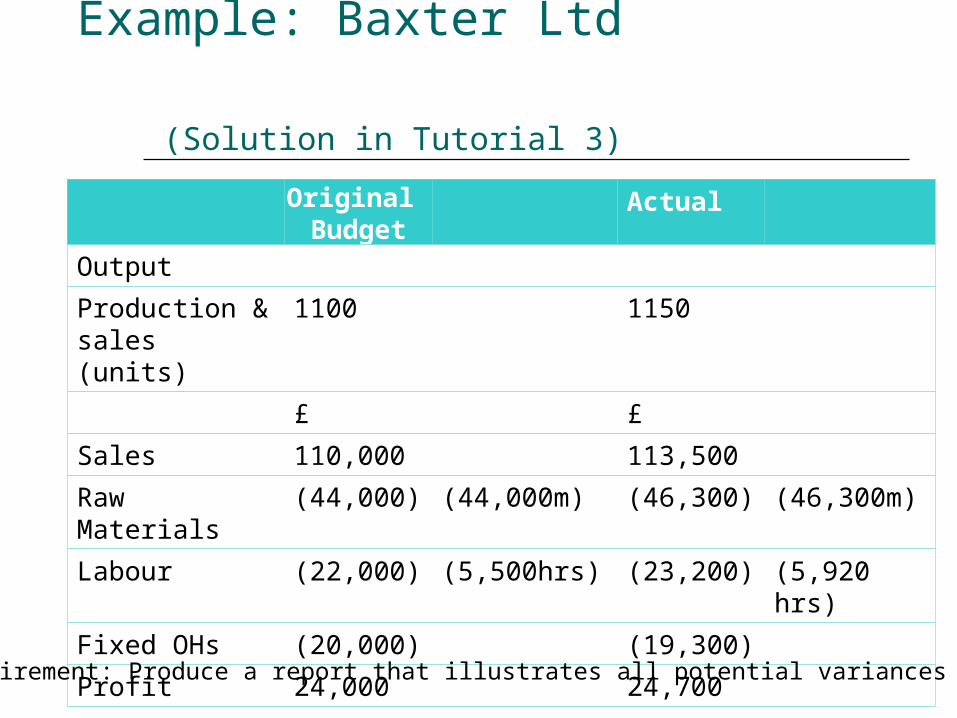

Flexible budget – the steps

Original Budget

Actual

Output

Production & sales (units)

1100 1150

£ £

Sales 110,000 113,500

Raw Materials (44,000) (44,000m) (46,300) (46,300m)

Labour (22,000) (5,500hrs) (23,200) (5,920 hrs)

Fixed OHs (20,000) (19,300)

Profit 24,000 24,700

Example: Baxter Ltd (Solution in Tutorial 3)

Requirement: Produce a report that illustrates all potential variances