1 Chapter 11 – Investment Basics • Investment is something that generates a return through dividends, interest and/or market appreciation – Speculation – a bet price will go up or down • Financial Planning – everything begins with your goals – Checklist: set goals, focus on time frame, be realistic, risk appetite, taxes, reality of plan

Transcript

1

Chapter 11 – Investment Basics

• Investment is something that generates a return through dividends, interest and/or market appreciation– Speculation – a bet price will go up or down

• Financial Planning – everything begins with your goals– Checklist: set goals, focus on time frame, be

realistic, risk appetite, taxes, reality of plan

2

Goal Setting

• Write them down and then ask

– Consequence of failing?– Willing to make necessary sacrifices?– How much money needed?– When?

3

Starting the Program

• Longer you postpone, harder to reach goal– Time is your best ally

• Set aside savings first, can spend the rest• Take advantage of Uncle Sam and

employer– Tax–free or tax-deferred– Company match savings plans

4

Personal Profile

• Age and stage in career

• Need for liquidity and cash flow needs

• Size of portfolio

• Income tax bracket

• Required rate of return

• Your risk tolerance

5

What’s Important to You?

• Liquidity and safety

• Current versus future income

• Capital growth

• Diversification

• Marketability

• Ease of management

6

Types of Investments

• Lending investments – fixed returns known in advance; has maturity date

• Ownership investments – stocks and real estate (but illiquid)

• Stocks – ownership interest in a corporation– As profits and dividends increase, so should

price; no upside limit

7

Bonds

• Pay interest periodically– Usually semiannually

• Often fixed for life of the bond

• At maturity repay principal

• Many, many kinds and features

• Subject to different types of risk

• As interest rates rise, bond prices fall

8

Interest Rates

• Nominal yield is the quoted rate, such as a bond yielding 10%

• Starts with risk-free rate – return with no risk such as short-term Treasury bills– To get to the nominal rate, add premiums

for inflation, default, maturity and liquidity risks to risk-free rate

• Real rate – nominal rate less inflation

9

Common Stock

• Common stockholders own the company and elect directors

• Returns come from increase in market value and dividends

• Rate of return equalsEnd value – Begin Value + Dividends

Beginning Value

10

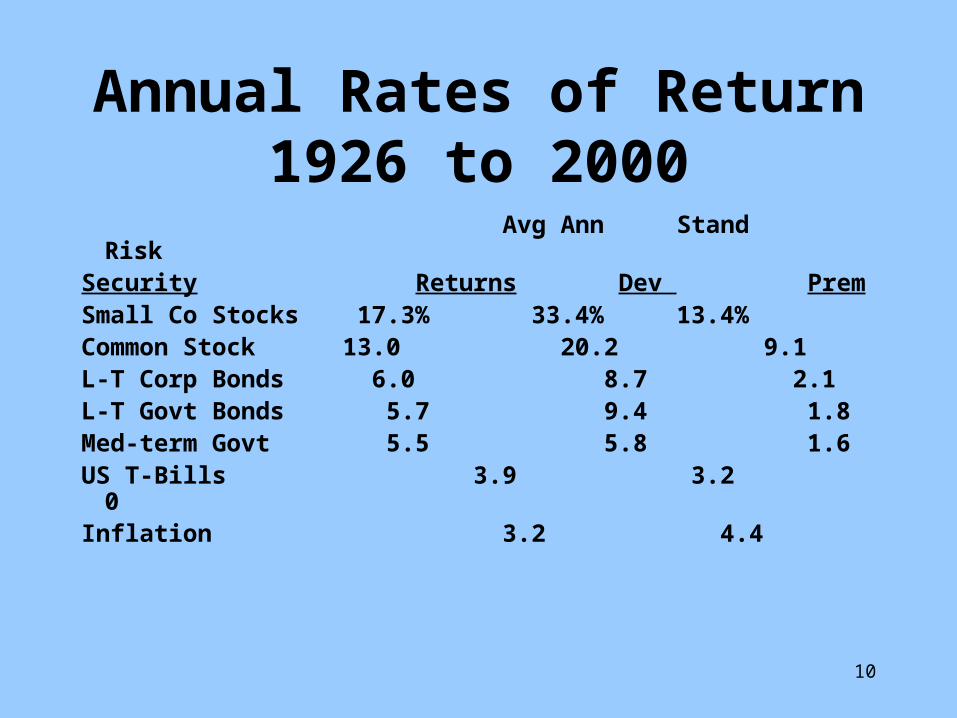

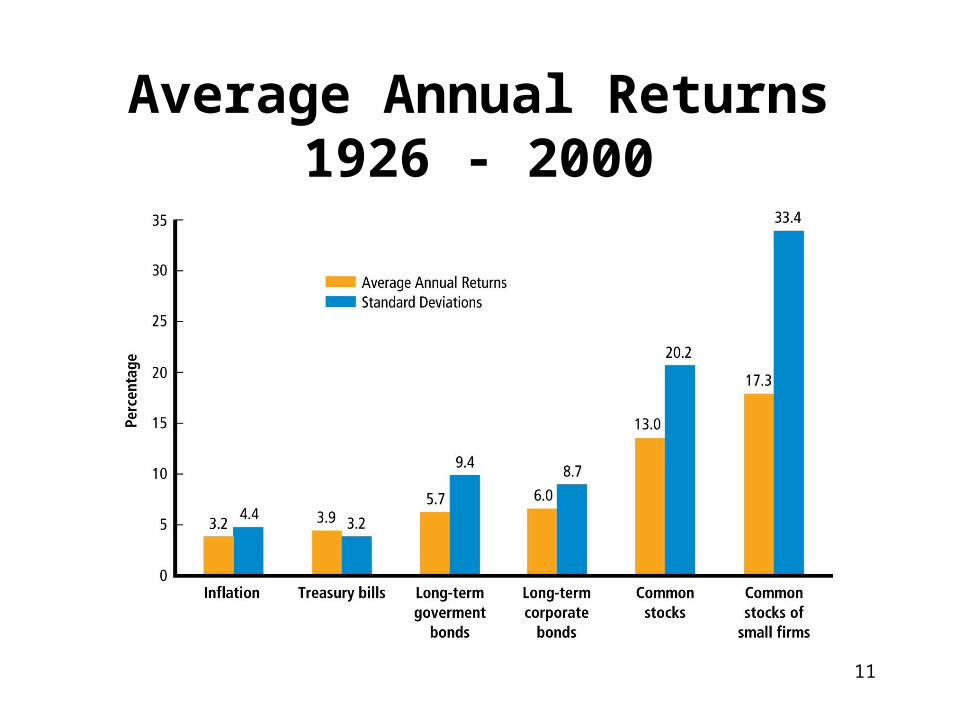

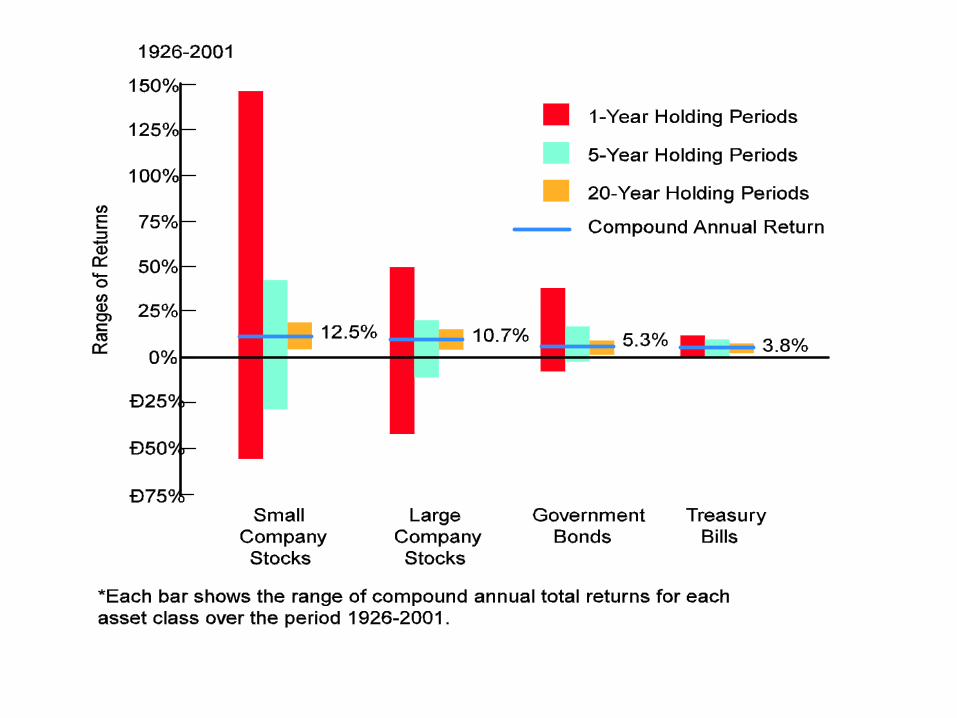

Annual Rates of Return1926 to 2000

Avg Ann Stand RiskSecurity Returns Dev PremSmall Co Stocks 17.3% 33.4% 13.4%Common Stock 13.0 20.2 9.1L-T Corp Bonds 6.0 8.7 2.1L-T Govt Bonds 5.7 9.4 1.8Med-term Govt 5.5 5.8 1.6US T-Bills 3.9 3.2 0Inflation 3.2 4.4

11

Average Annual Returns1926 - 2000

13

2004

• Dow – 30 Industrials +3.15%

• S&P 500 +8.99

• S&P Small Cap +21.59

• Treasury Bonds flat

• Dollar down

14

2005

• My guess – stocks up modestly (5 to 10%); bonds down