37

1 CHAPTER 9 The Cost of Capital Omar Al Nasser, Ph.D.

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | brendan-cummings |

| View: | 220 times |

| Download: | 1 times |

1

CHAPTER 9

The Cost of Capital

Omar Al Nasser, Ph.D.FIN 6352

2

Topics in Chapter Cost of Capital Components

Debt Preferred Common Equity

The Weighted Average Cost Of Capital (WACC).

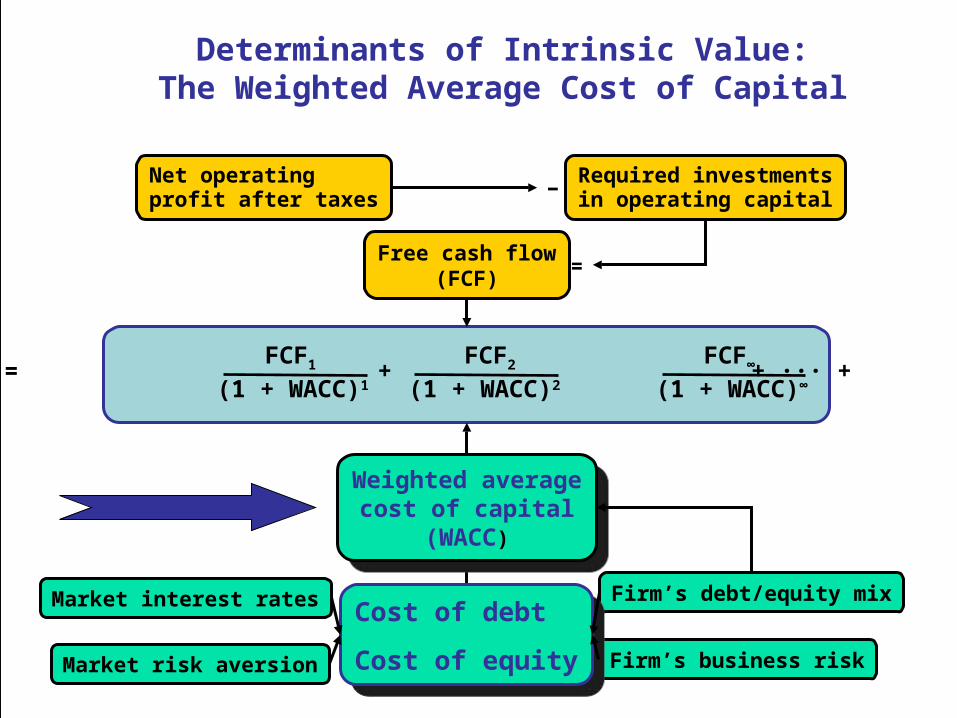

Value = + + ··· +FCF1 FCF2 FCF∞

(1 + WACC)1 (1 + WACC)∞

(1 + WACC)2

Free cash flow(FCF)

Market interest rates

Firm’s business riskMarket risk aversion

Firm’s debt/equity mix

Cost of debt

Cost of equity

Cost of debt

Cost of equity

Weighted averagecost of capital

(WACC)

Weighted averagecost of capital

(WACC)

Net operatingprofit after taxes

Required investmentsin operating capital−

=

Determinants of Intrinsic Value:The Weighted Average Cost of Capital

4

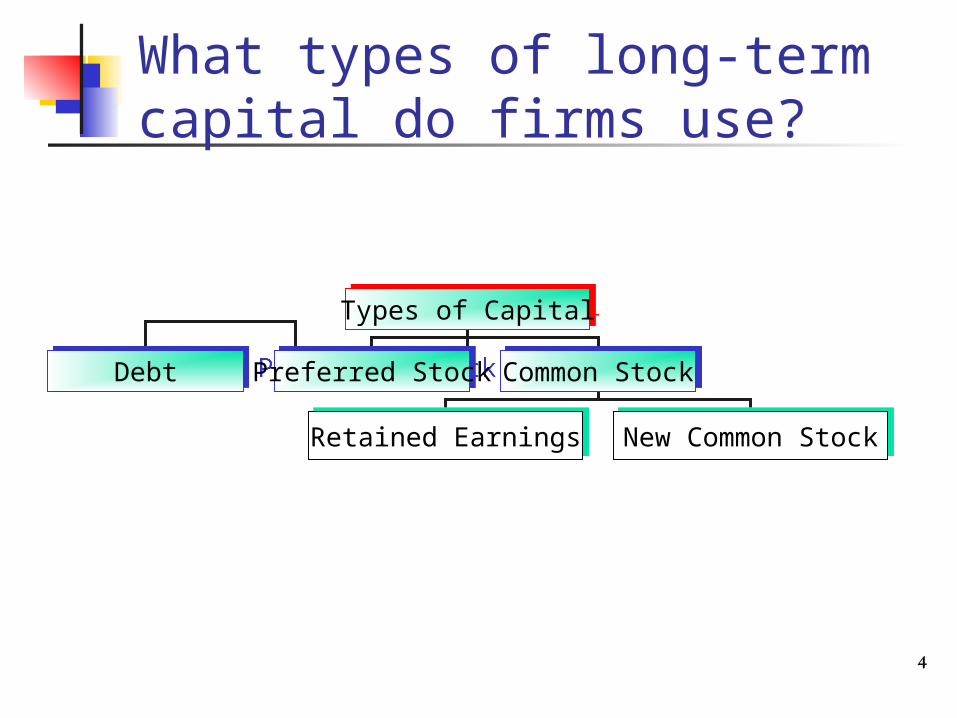

What types of long-term capital do firms use?

Types of CapitalTypes of Capital

DebtDebt Preferred StockPreferred Stock Common StockCommon Stock

Retained EarningsRetained Earnings New Common StockNew Common Stock

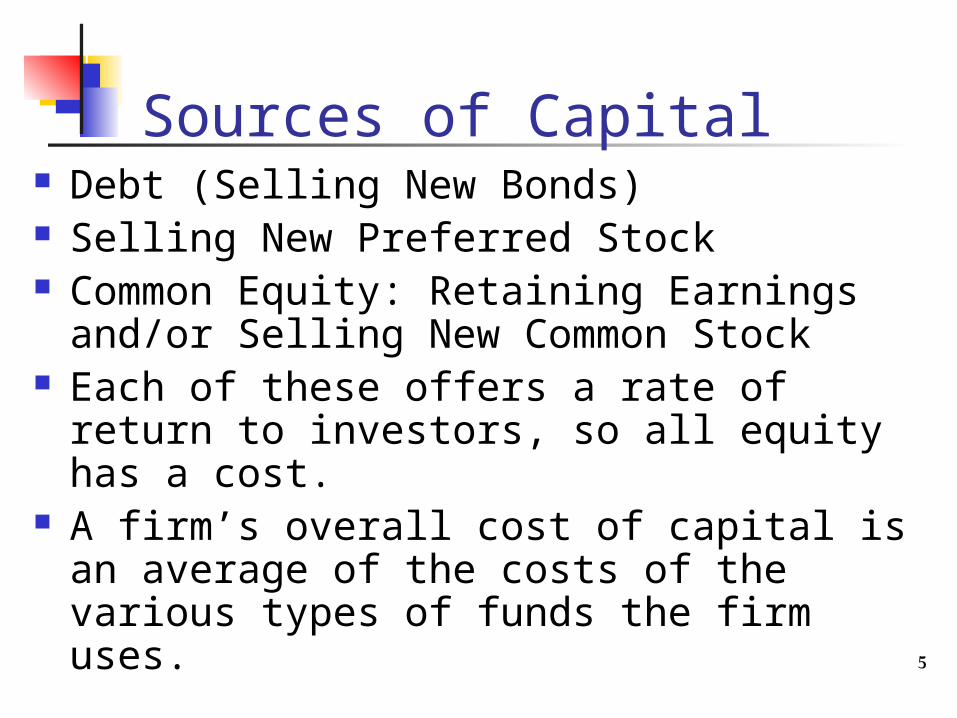

5

Sources of Capital Debt (Selling New Bonds) Selling New Preferred Stock Common Equity: Retaining Earnings and/or

Selling New Common Stock Each of these offers a rate of return to

investors, so all equity has a cost. A firm’s overall cost of capital is an average

of the costs of the various types of funds the firm uses.

6

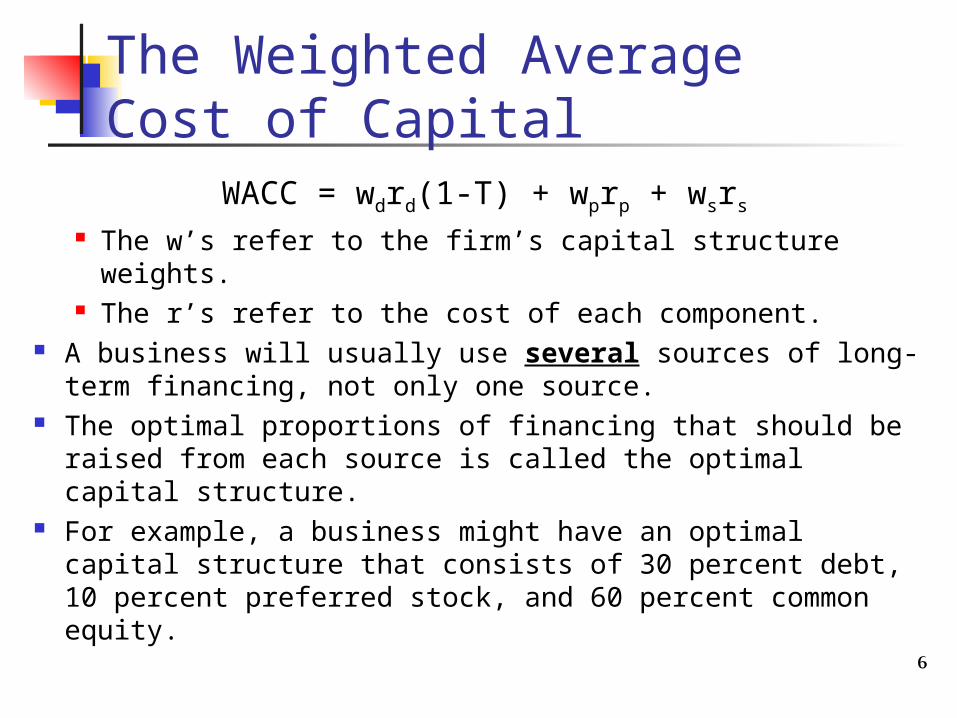

The Weighted Average Cost of Capital

WACC = wdrd(1-T) + wprp + wsrs The w’s refer to the firm’s capital structure weights. The r’s refer to the cost of each component.

A business will usually use several sources of long-term financing, not only one source.

The optimal proportions of financing that should be raised from each source is called the optimal capital structure.

For example, a business might have an optimal capital structure that consists of 30 percent debt, 10 percent preferred stock, and 60 percent common equity.

7

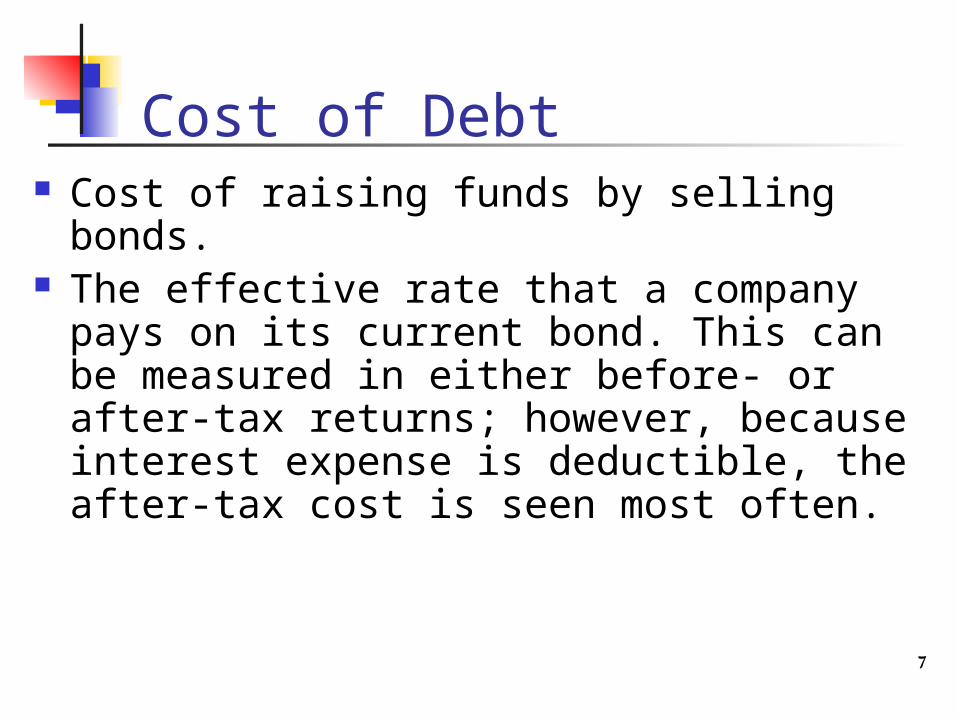

Cost of Debt Cost of raising funds by selling bonds. The effective rate that a company pays on

its current bond. This can be measured in either before- or after-tax returns; however, because interest expense is deductible, the after-tax cost is seen most often.

8

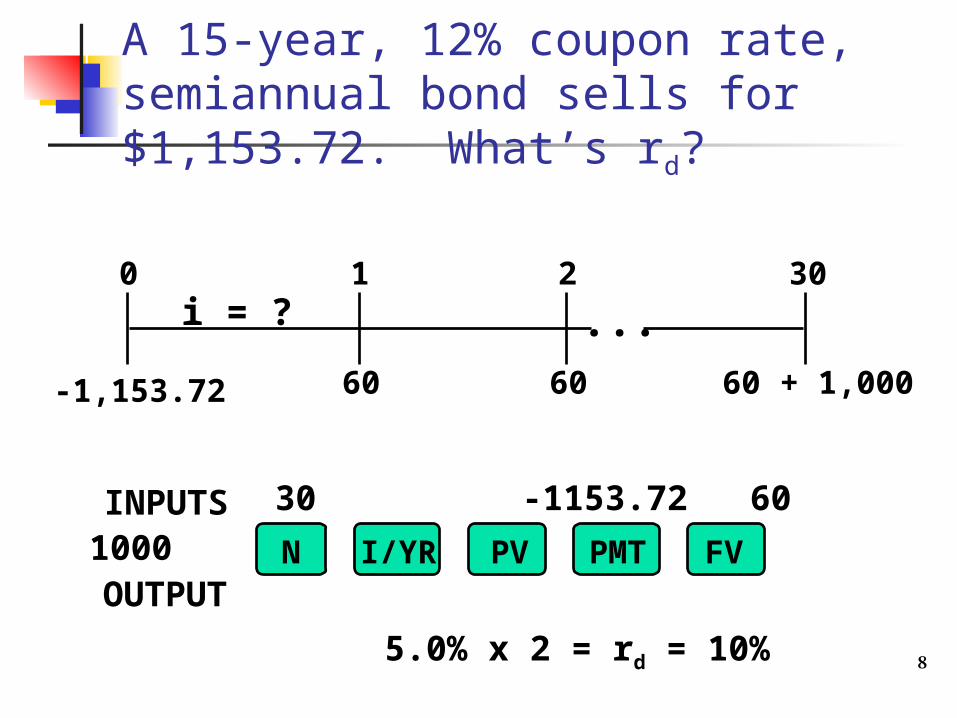

A 15-year, 12% coupon rate, semiannual bond sells for $1,153.72. What’s rd?

60 60 + 1,00060

0 1 2 30i = ?

-1,153.72

...

30 -1153.72 60 1000

5.0% x 2 = rd = 10% N I/YR PV FVPMT

INPUTS

OUTPUT

9

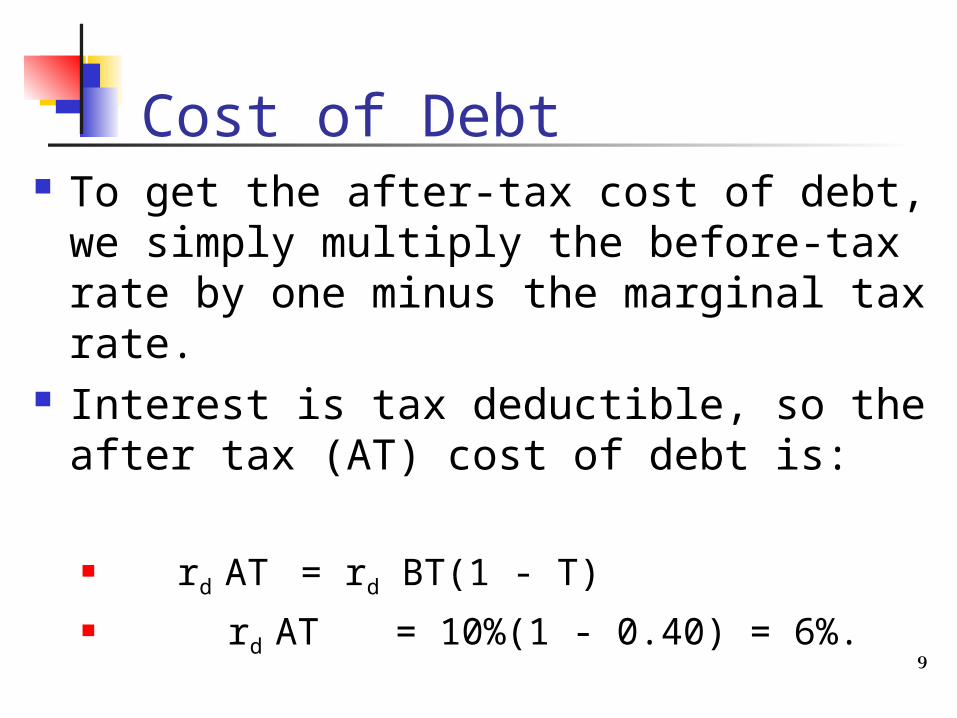

Cost of Debt To get the after-tax cost of debt, we

simply multiply the before-tax rate by one minus the marginal tax rate.

Interest is tax deductible, so the after tax (AT) cost of debt is:

rd AT = rd BT(1 - T) rd AT= 10%(1 - 0.40) = 6%.

10

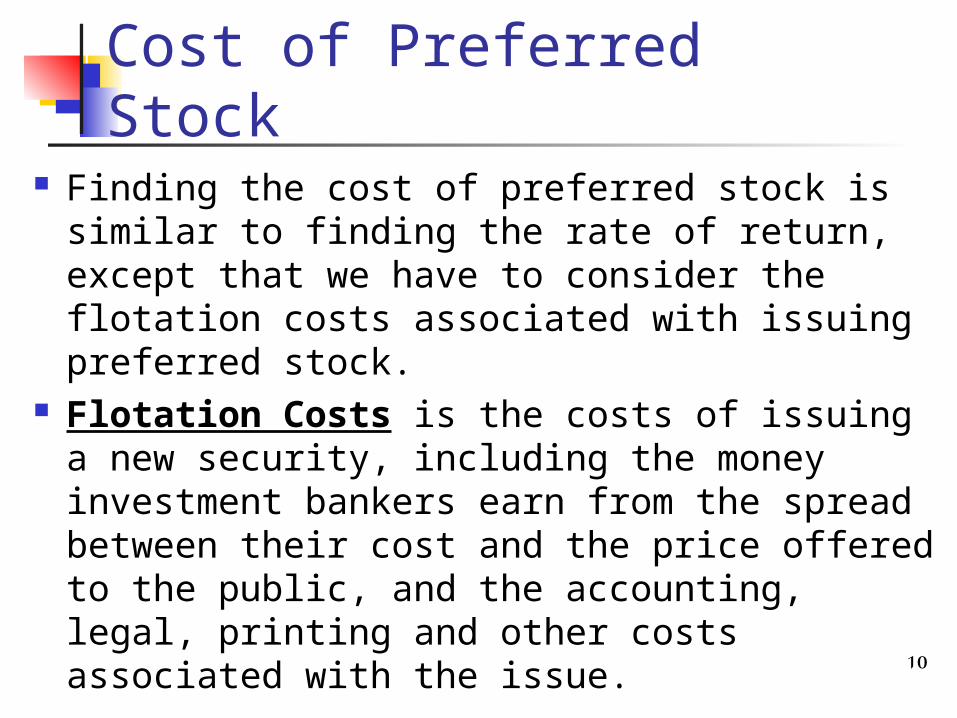

Cost of Preferred Stock Finding the cost of preferred stock is

similar to finding the rate of return, except that we have to consider the flotation costs associated with issuing preferred stock.

Flotation Costs is the costs of issuing a new security, including the money investment bankers earn from the spread between their cost and the price offered to the public, and the accounting, legal, printing and other costs associated with the issue.

11

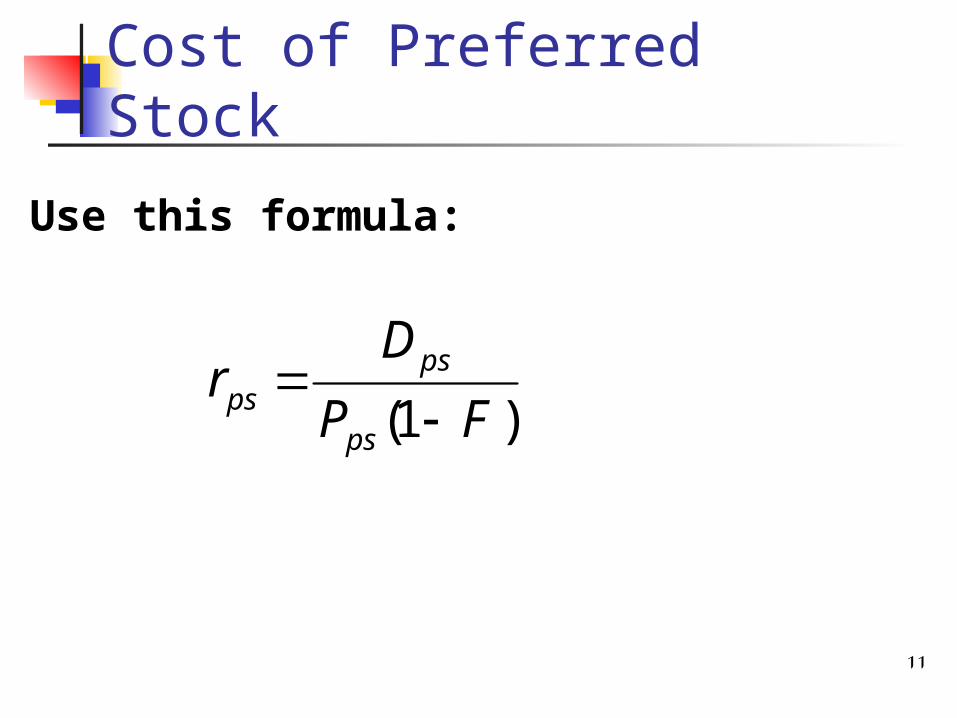

Cost of Preferred Stock

Use this formula:

)1( FP

Dr

ps

psps

12

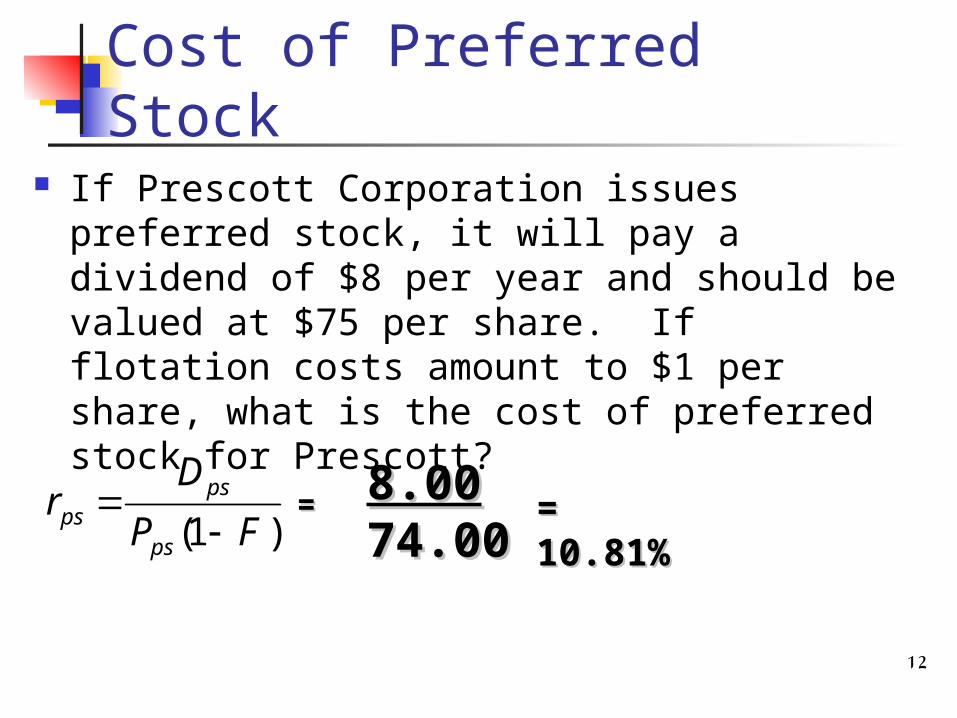

Cost of Preferred Stock If Prescott Corporation issues preferred

stock, it will pay a dividend of $8 per year and should be valued at $75 per share. If flotation costs amount to $1 per share, what is the cost of preferred stock for Prescott?

)1( FP

Dr

ps

psps

8.008.0074.0074.00

== = 10.81%= 10.81%

13

Cost of Common Stock

14

What are the two ways that companies can raise common equity?

Directly, by issuing new shares of common stock.

Indirectly, by reinvesting earnings that are not paid out as dividends (i.e., retaining earnings).

15

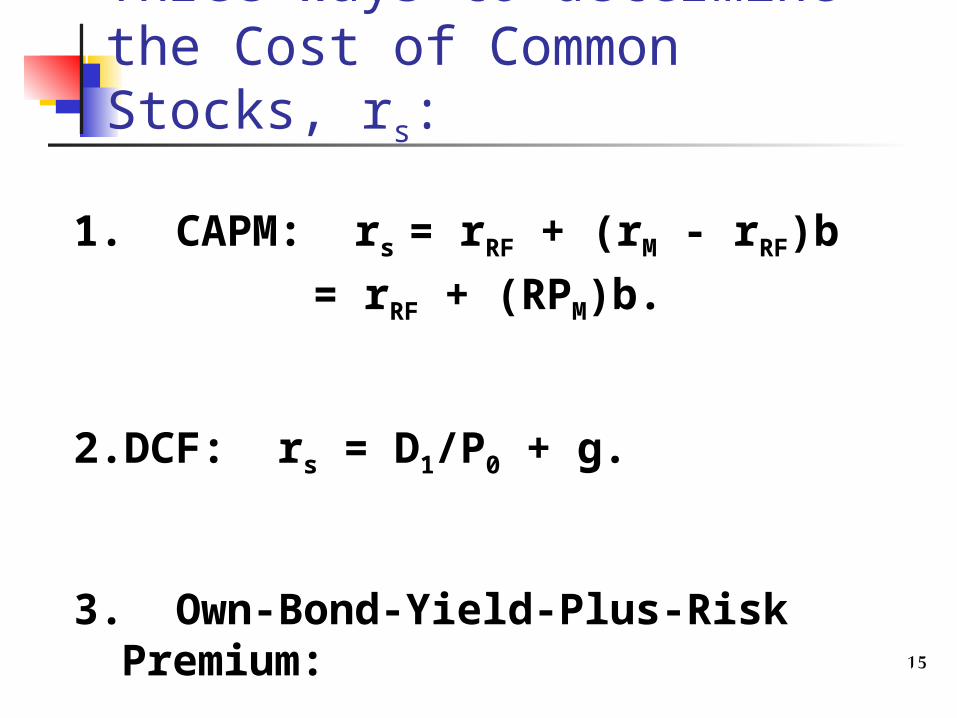

Three ways to determine the Cost of Common Stocks, rs:

1. CAPM: rs = rRF + (rM - rRF)b

= rRF + (RPM)b.

2. DCF: rs = D1/P0 + g.

3. Own-Bond-Yield-Plus-Risk Premium:

rs = Bond Yield + Bond risk premium.

16

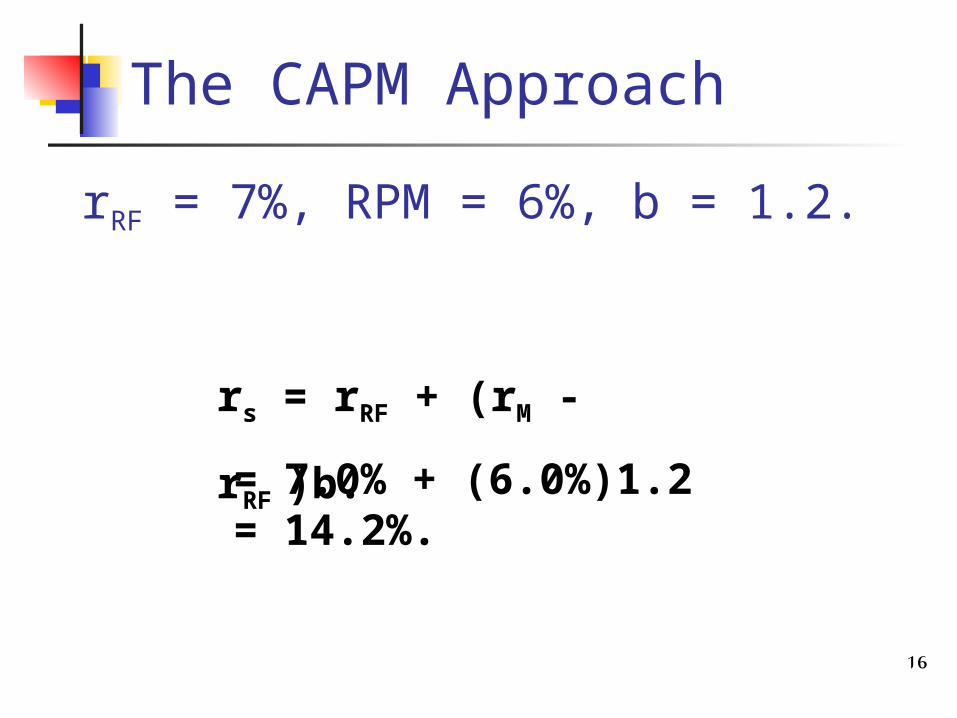

rRF = 7%, RPM = 6%, b = 1.2.

rs = rRF + (rM - rRF )b.

= 7.0% + (6.0%)1.2 = 14.2%.

The CAPM Approach

17

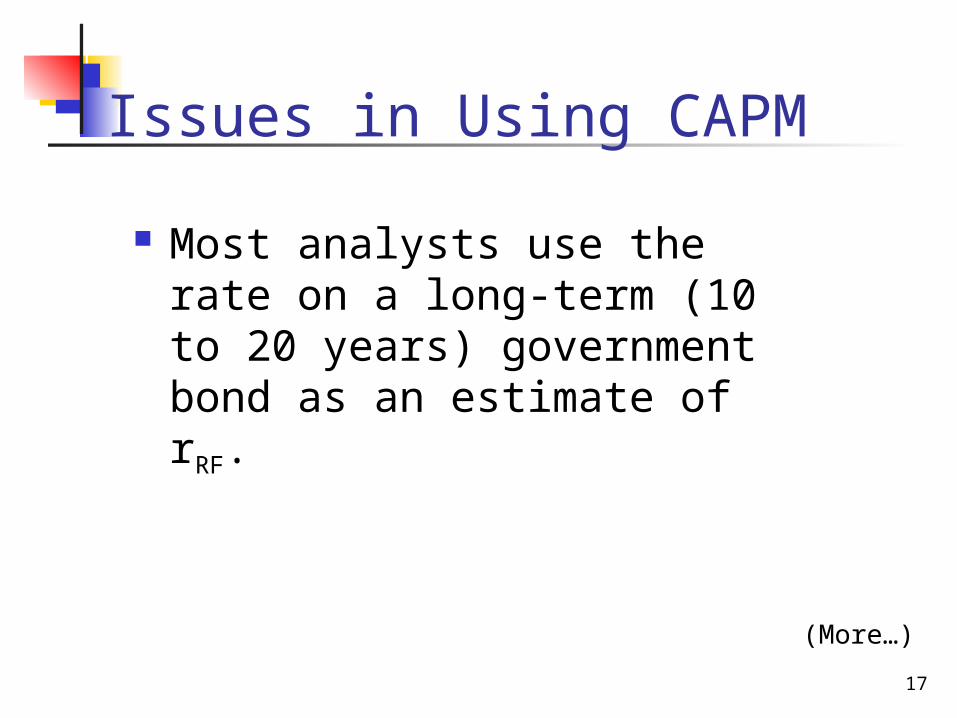

Issues in Using CAPM

Most analysts use the rate on a long-term (10 to 20 years) government bond as an estimate of rRF.

(More…)

18

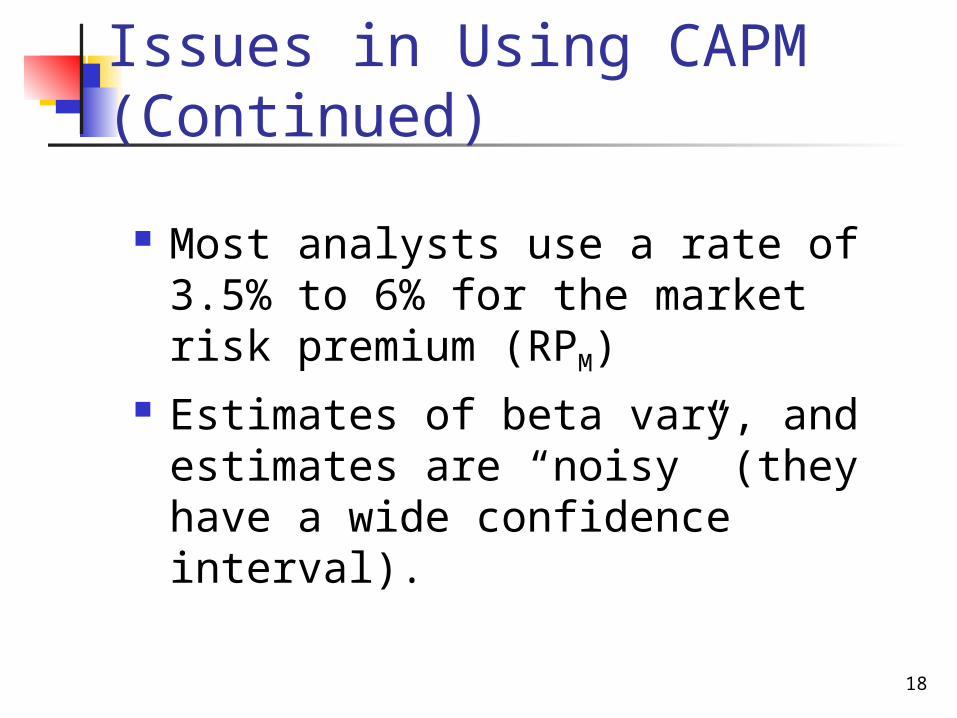

Issues in Using CAPM (Continued)

Most analysts use a rate of 3.5% to 6% for the market risk premium (RPM)

Estimates of beta vary, and estimates are “noisy” (they have a wide confidence interval).

19

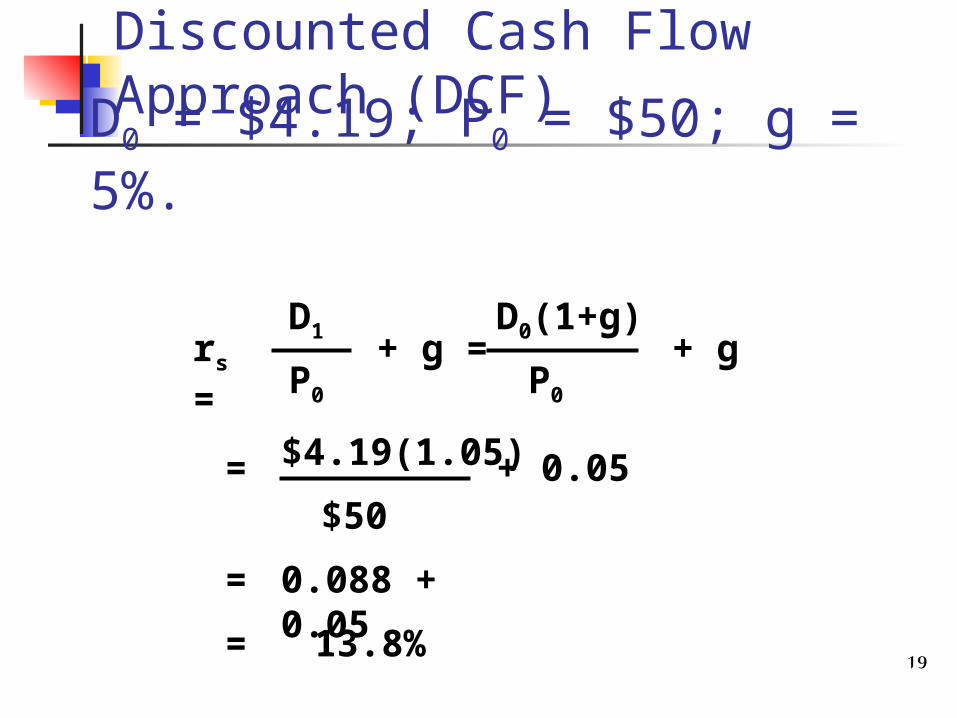

D0 = $4.19; P0 = $50; g = 5%.

rs = D1

P0

+ g =D0(1+g)

P0

+ g

= $4.19(1.05)

$50+ 0.05

= 0.088 + 0.05

= 13.8%

Discounted Cash Flow Approach (DCF)

20

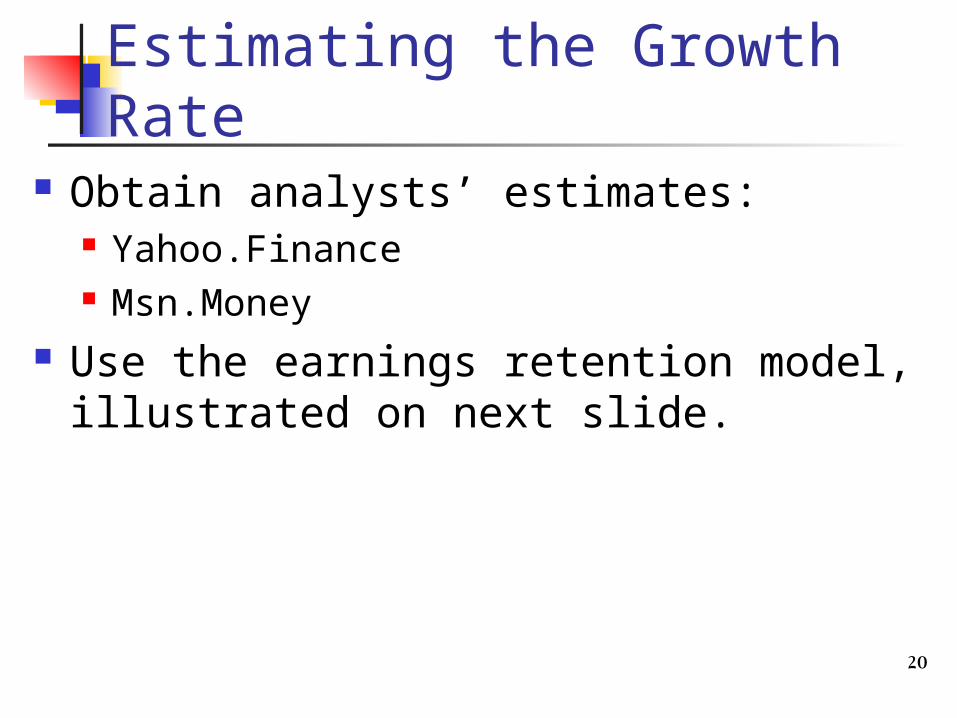

Estimating the Growth Rate

Obtain analysts’ estimates: Yahoo.Finance Msn.Money

Use the earnings retention model, illustrated on next slide.

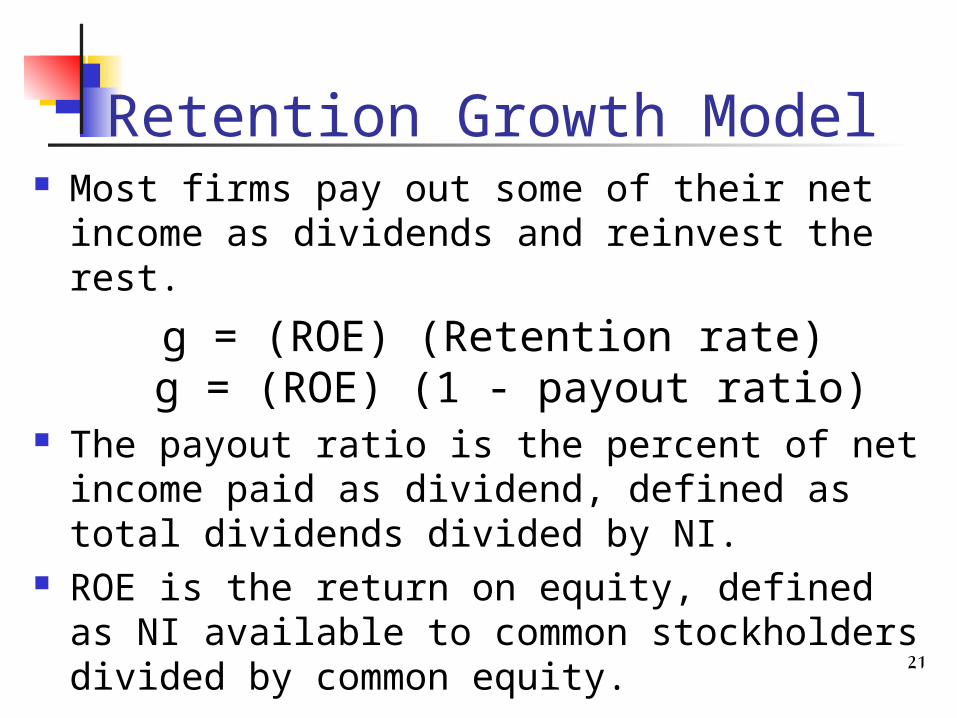

21

Retention Growth Model Most firms pay out some of their net income

as dividends and reinvest the rest.

g = (ROE) (Retention rate) g = (ROE) (1 - payout ratio)

The payout ratio is the percent of net income paid as dividend, defined as total dividends divided by NI.

ROE is the return on equity, defined as NI available to common stockholders divided by common equity.

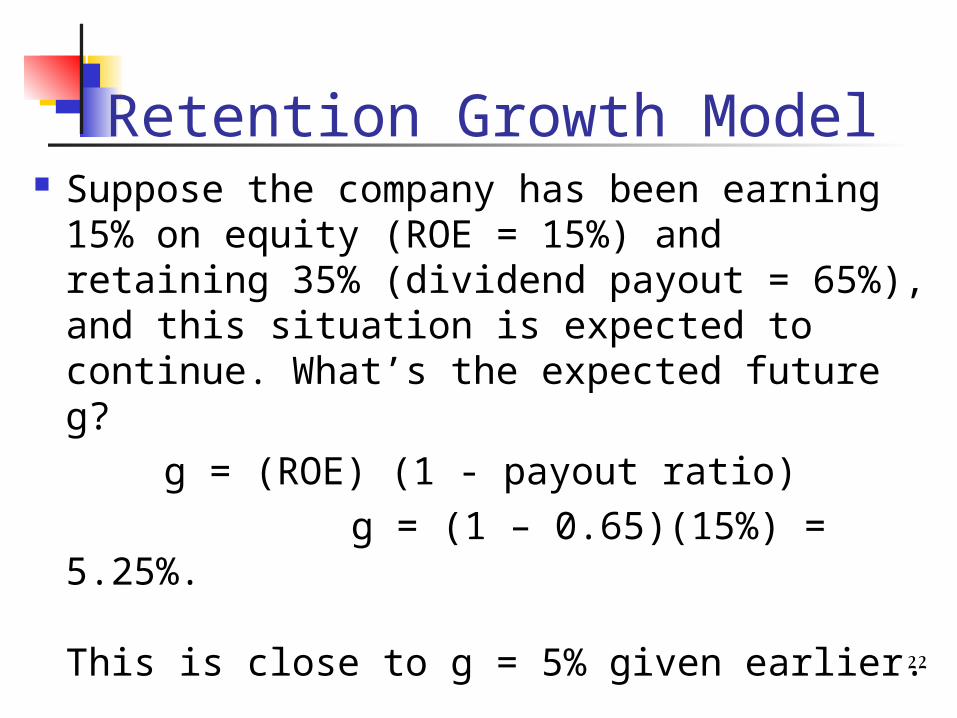

22

Retention Growth Model Suppose the company has been

earning 15% on equity (ROE = 15%) and retaining 35% (dividend payout = 65%), and this situation is expected to continue. What’s the expected future g?

g = (ROE) (1 - payout ratio) g = (1 – 0.65)(15%) = 5.25%.

This is close to g = 5% given earlier.

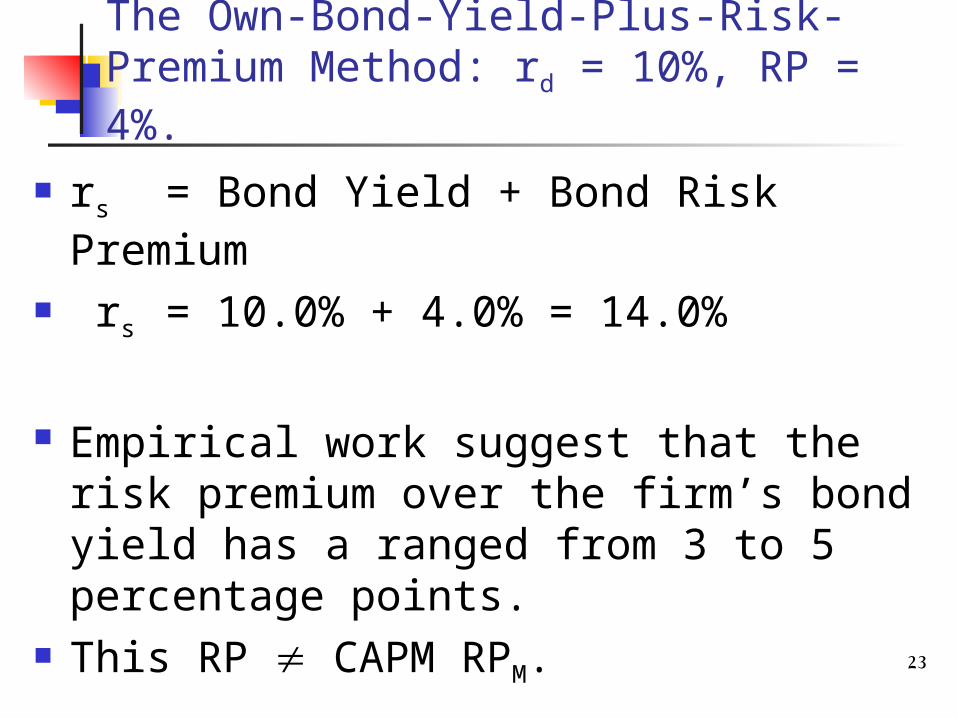

23

The Own-Bond-Yield-Plus-Risk-Premium Method: rd = 10%, RP = 4%.

rs = Bond Yield + Bond Risk Premium rs = 10.0% + 4.0% = 14.0%

Empirical work suggest that the risk premium over the firm’s bond yield has a ranged from 3 to 5 percentage points.

This RP CAPM RPM.

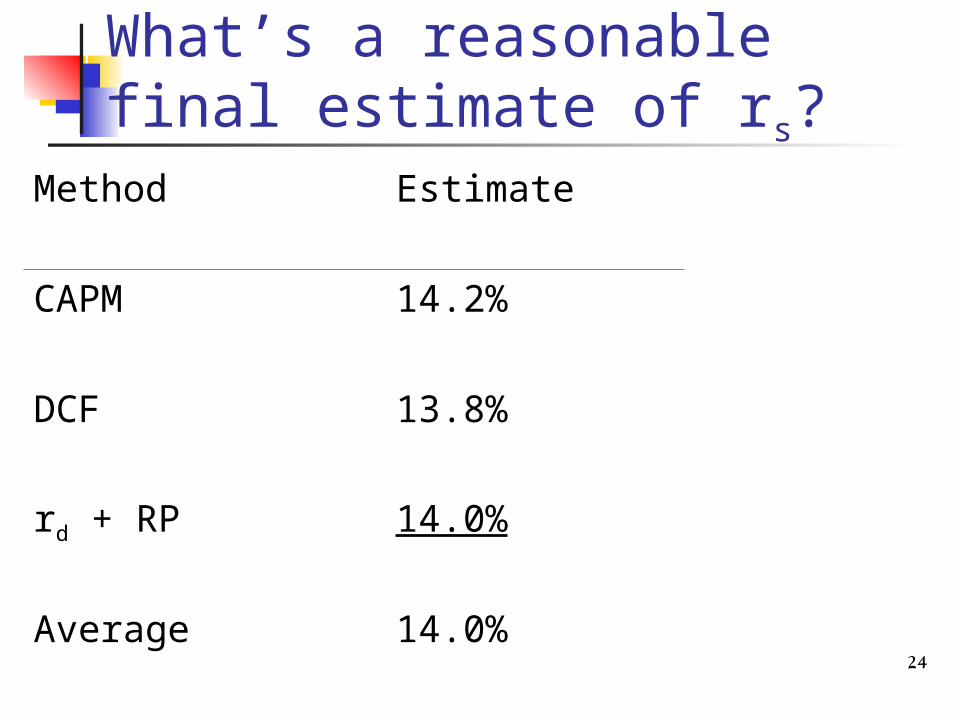

24

What’s a reasonable final estimate of rs?

Method Estimate

CAPM 14.2%

DCF 13.8%

rd + RP 14.0%

Average 14.0%

25

Determining the Weights for the WACC

The weights are the percentages of the firm that will be financed by each component.

If possible, always use the target weights for the percentages of the firm that will be financed with the various types of capital.

26

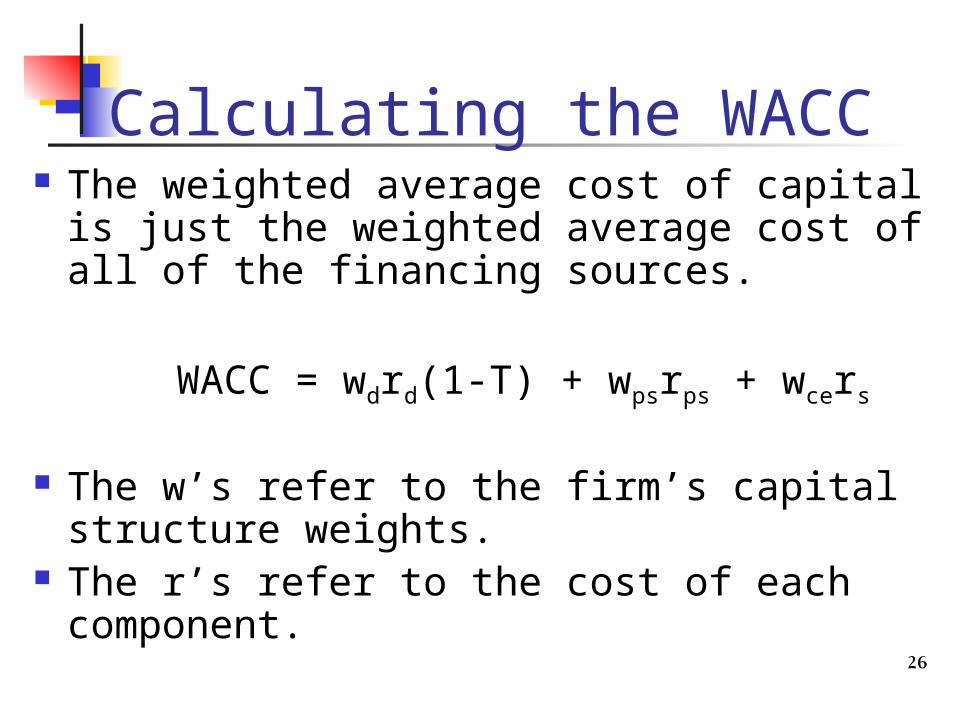

Calculating the WACC The weighted average cost of capital is

just the weighted average cost of all of the financing sources.

WACC = wdrd(1-T) + wpsrps + wcers

The w’s refer to the firm’s capital structure weights.

The r’s refer to the cost of each component.

27

Estimating Weights for the Capital Structure

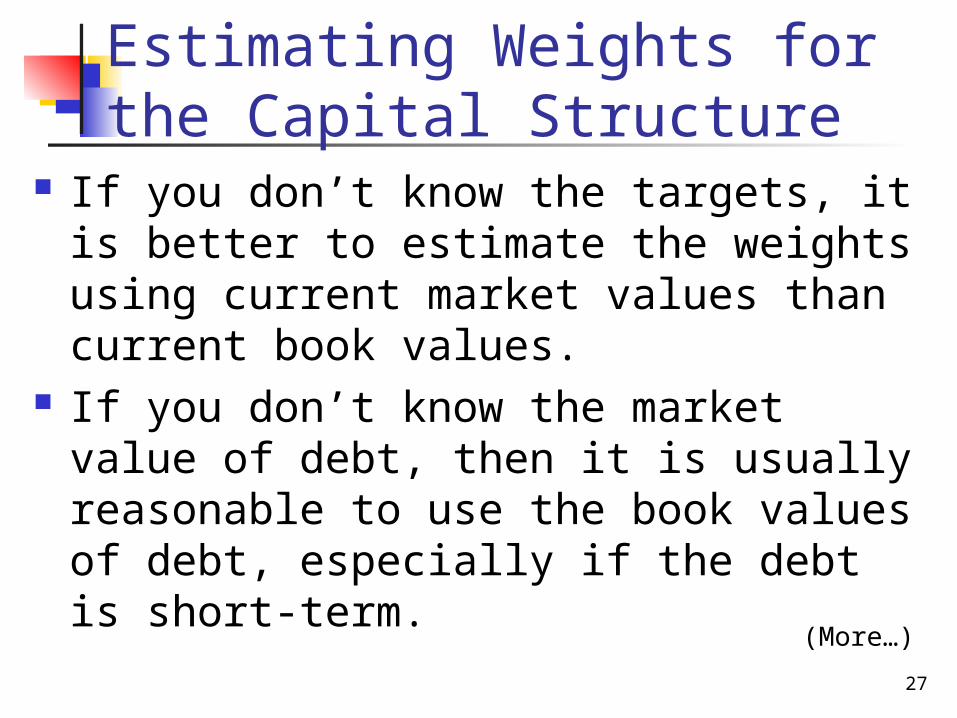

If you don’t know the targets, it is better to estimate the weights using current market values than current book values.

If you don’t know the market value of debt, then it is usually reasonable to use the book values of debt, especially if the debt is short-term.

(More…)

28

Determining the Weights for the WACC

Each firm has an optimal capital structure defined as the mix of debt, preferred, and common equity that causes its stock price to be maximized.

Therefore, a value-maximizing firm will establish an optimal capital structure and then raise new capital in a manner that will keep the actual capital structure on optimal over time.

The weights are the percentages of the firm that will be financed by each component.

29

Estimating Weights (Continued)

Suppose the stock price is $50, there are 3 million shares of stock, the firm has $25 million of preferred stock, and $75 million of debt. Vce = $50 (3 million) = $150 million. Vps = $25 million. Vd = $75 million. Total value = $150 + $25 + $75 = $250

million. (More...)

30

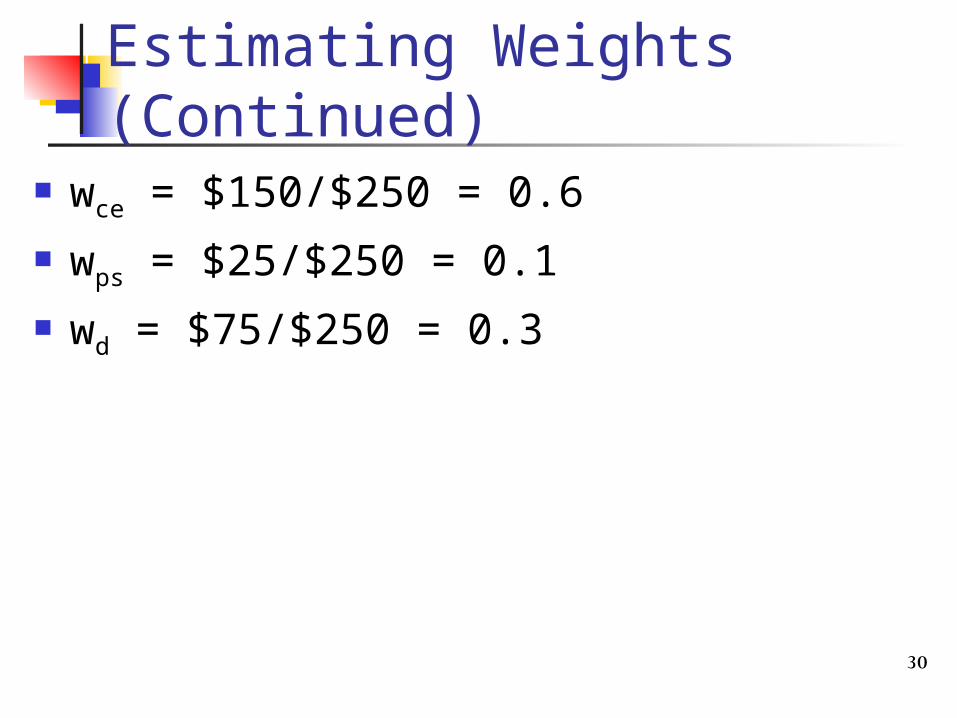

Estimating Weights (Continued)

wce = $150/$250 = 0.6 wps = $25/$250 = 0.1 wd = $75/$250 = 0.3

31

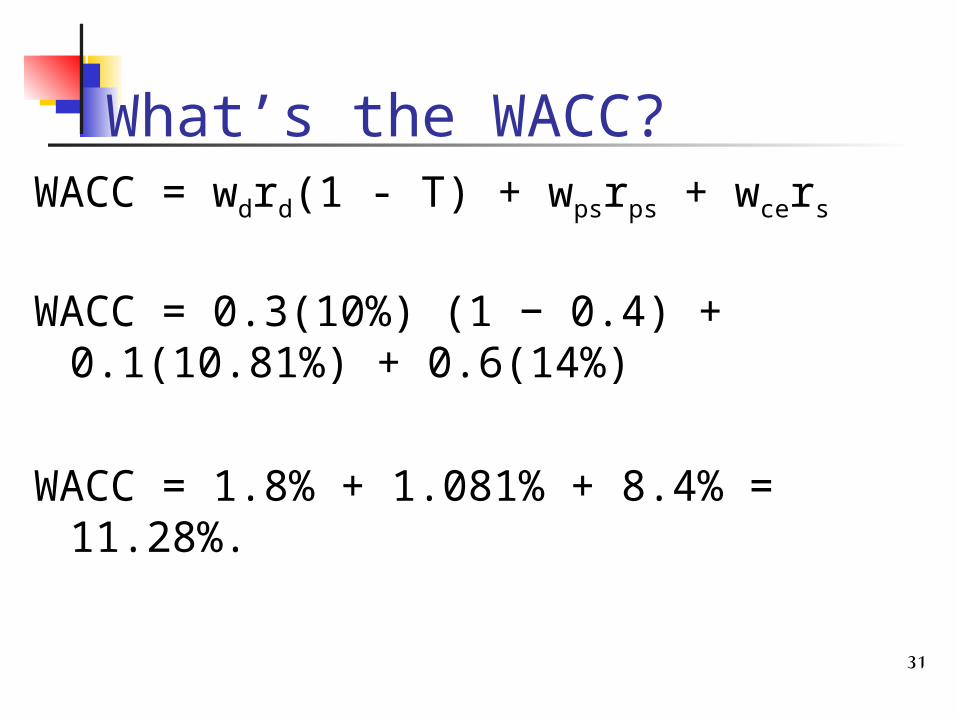

What’s the WACC?WACC = wdrd(1 - T) + wpsrps + wcers

WACC = 0.3(10%) (1 − 0.4) + 0.1(10.81%) + 0.6(14%)

WACC = 1.8% + 1.081% + 8.4% = 11.28%.

32

Example:

Consider a business whose optimal capital structure was 30 % debt, 10 % preferred stock, and 60% common equity.

Assume investors require an 8% after-tax return on bonds, a 12% return on preferred stock, and a 16% return on common stock.

The business’ WACC = (.30 x .08) + (.10 x .12) + (.60 x .16) = 13.2%.

33

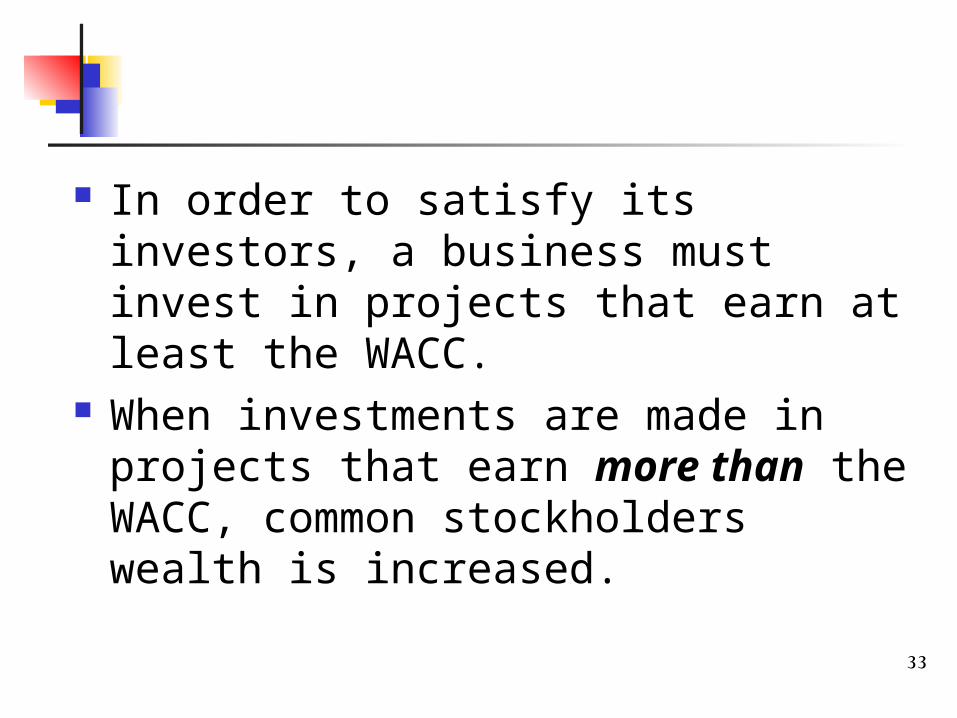

In order to satisfy its investors, a business must invest in projects that earn at least the WACC.

When investments are made in projects that earn more than the WACC, common stockholders wealth is increased.

34

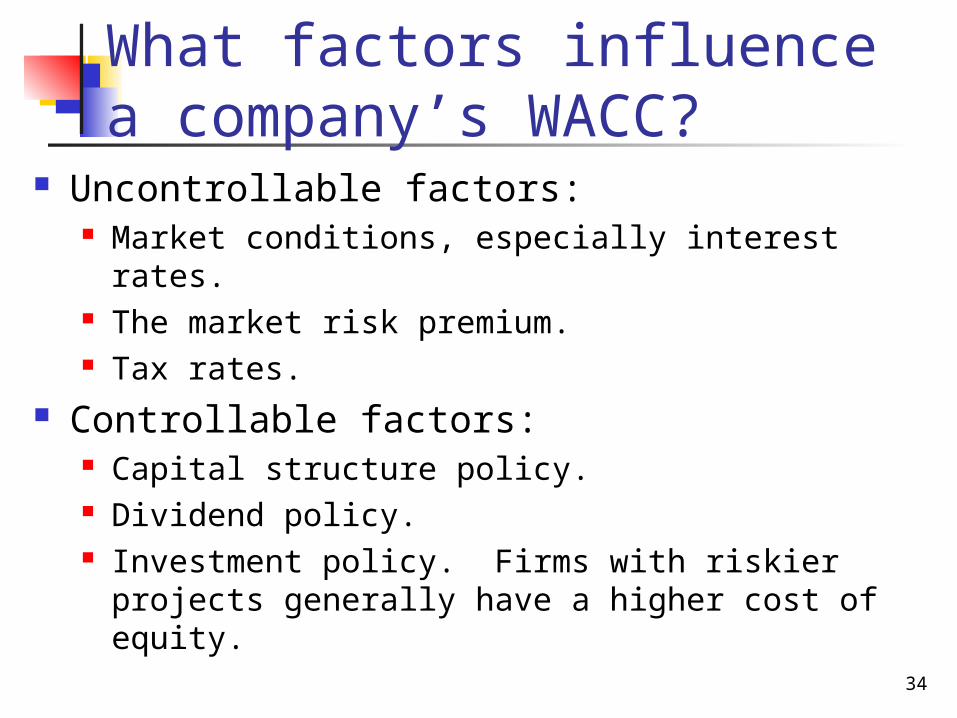

What factors influence a company’s WACC?

Uncontrollable factors: Market conditions, especially interest rates. The market risk premium. Tax rates.

Controllable factors: Capital structure policy. Dividend policy. Investment policy. Firms with riskier projects

generally have a higher cost of equity.

35

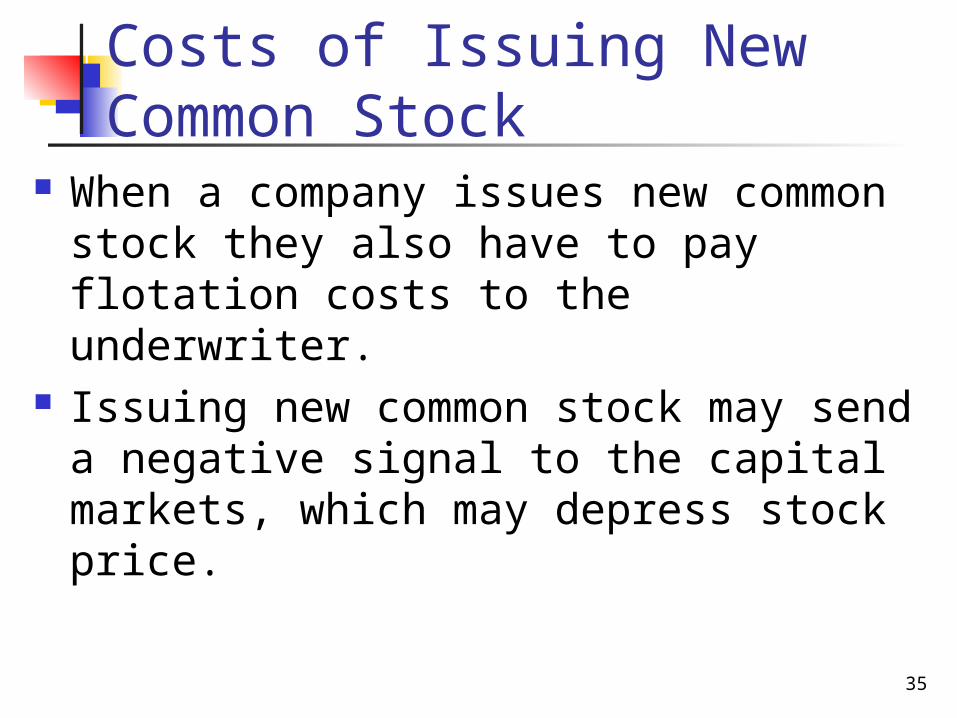

Costs of Issuing New Common Stock

When a company issues new common stock they also have to pay flotation costs to the underwriter.

Issuing new common stock may send a negative signal to the capital markets, which may depress stock price.

36

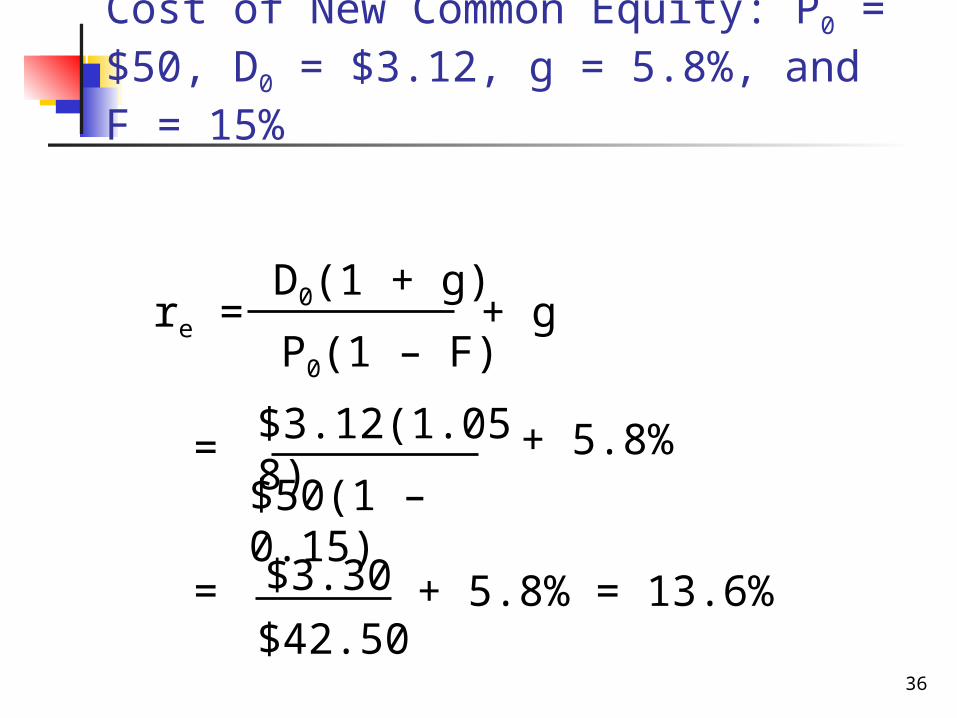

Cost of New Common Equity: P0 = $50, D0 = $3.12, g = 5.8%, and F = 15%

re =D0(1 + g)

P0(1 – F)+ g

= $3.12(1.058)$50(1 – 0.15)

+ 5.8%

= $3.30

$42.50+ 5.8% = 13.6%

37

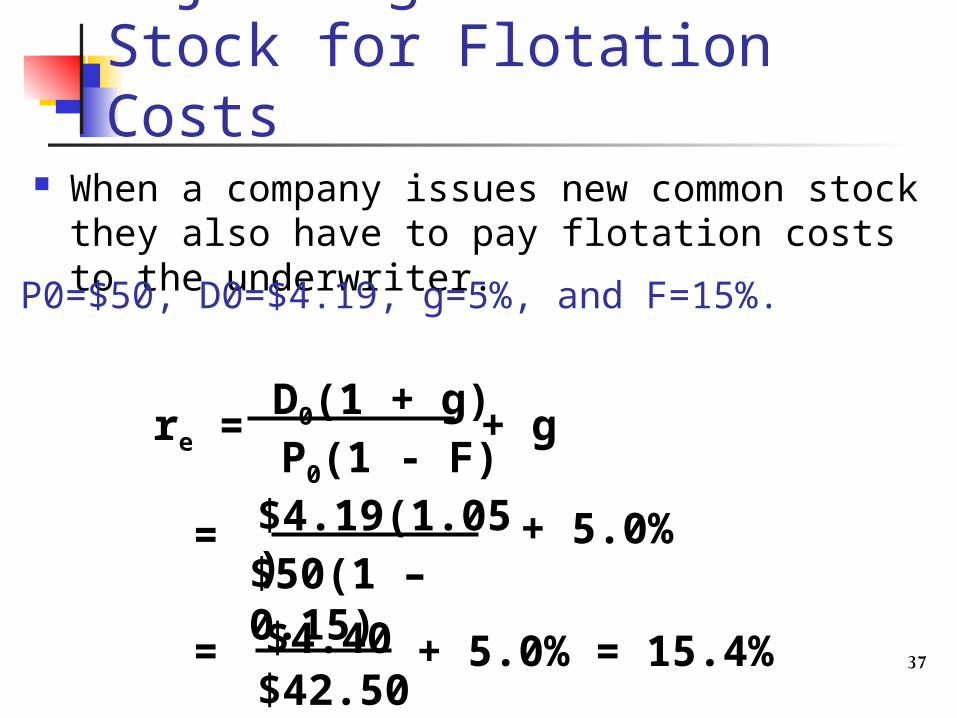

Adjusting the Cost of Stock for Flotation Costs

When a company issues new common stock they also have to pay flotation costs to the underwriter.

re =D0(1 + g)P0(1 - F)

+ g

= $4.19(1.05)$50(1 – 0.15)

+ 5.0%

= $4.40$42.50

+ 5.0% = 15.4%

P0=$50, D0=$4.19, g=5%, and F=15%.