61

1 Colombia Capacity Auction Peter Cramton (with many ideas from Steven Stoft) 9 June 2006

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | karin-randall |

| View: | 217 times |

| Download: | 1 times |

1

Colombia Capacity Auction

Peter Cramton(with many ideas from Steven Stoft)

9 June 2006

2

Outline• Purpose of market• Why forward procurement?• Key features

– Product– Planning period– Commitment period– Cost of new entry (CONE)– Demand curve– Descending clock auction– Price formation– Performance incentives– Fail-safe mechanism– Secondary market

• Transition• Supplier concerns

3

Purpose of Market

4

Purpose of market

• Induce just enough investment to maintain adequate resources

• Induce efficient mix of resources

• Reduce market risk

• Avoid market power in capacity market

• Reduce market power in energy market

• Pay no more than necessary

5

Why forward procurement?

6

Why forward procurement?

• New projects compete in advance of entry– Coordinated entry

• Less uncertainty in achieving target• Avoid boom/bust• New capacity sets price directly• Less reliance on demand curve for price setting

• Long-term commitment for new capacity– Reduced investor risk– Better price signal for new investment

7

Key features

8

Key Features

• Product• Planning period• Commitment period• Cost of new entry (CONE)• Demand curve• Descending clock auction• Price formation• Performance incentives• Fail-safe mechanism• Secondary market

9

Product

10

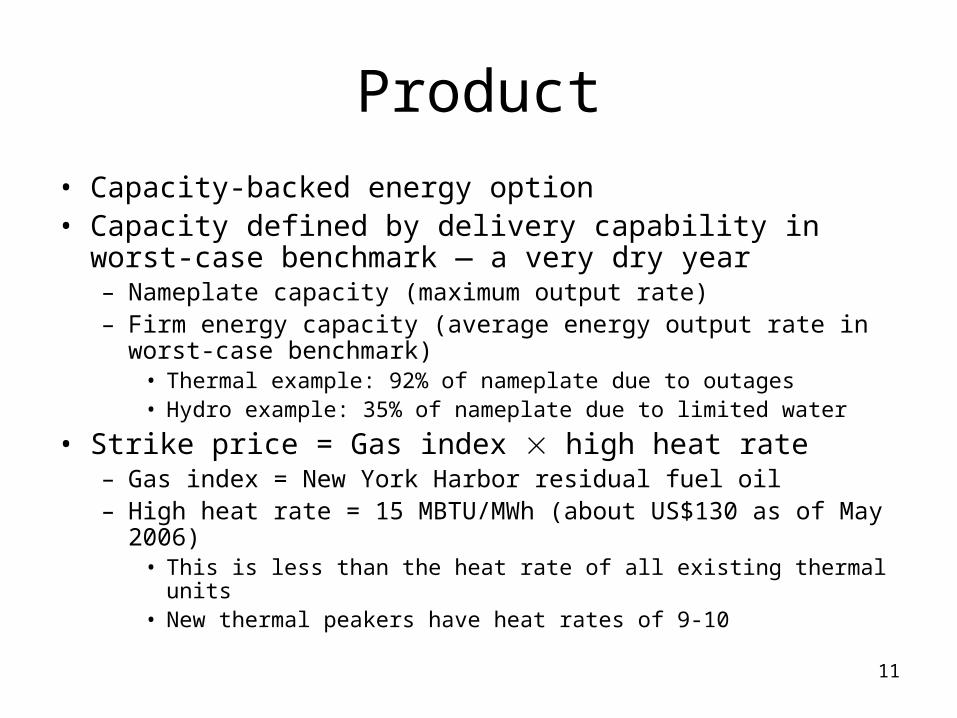

Product

• Firm energy ― availability of energy during scarcity events– Dry year (seasonal scarcity)– Outages (spot scarcity)

• Scarcity event defined by high energy price– Energy price is a transparent trigger– Energy price is a reliable trigger

11

Product

• Capacity-backed energy option• Capacity defined by delivery capability in worst-case

benchmark ― a very dry year– Nameplate capacity (maximum output rate)– Firm energy capacity (average energy output rate in worst-case

benchmark)• Thermal example: 92% of nameplate due to outages• Hydro example: 35% of nameplate due to limited water

• Strike price = Gas index high heat rate– Gas index = New York Harbor residual fuel oil– High heat rate = 15 MBTU/MWh (about US$130 as of May 2006)

• This is less than the heat rate of all existing thermal units• New thermal peakers have heat rates of 9-10

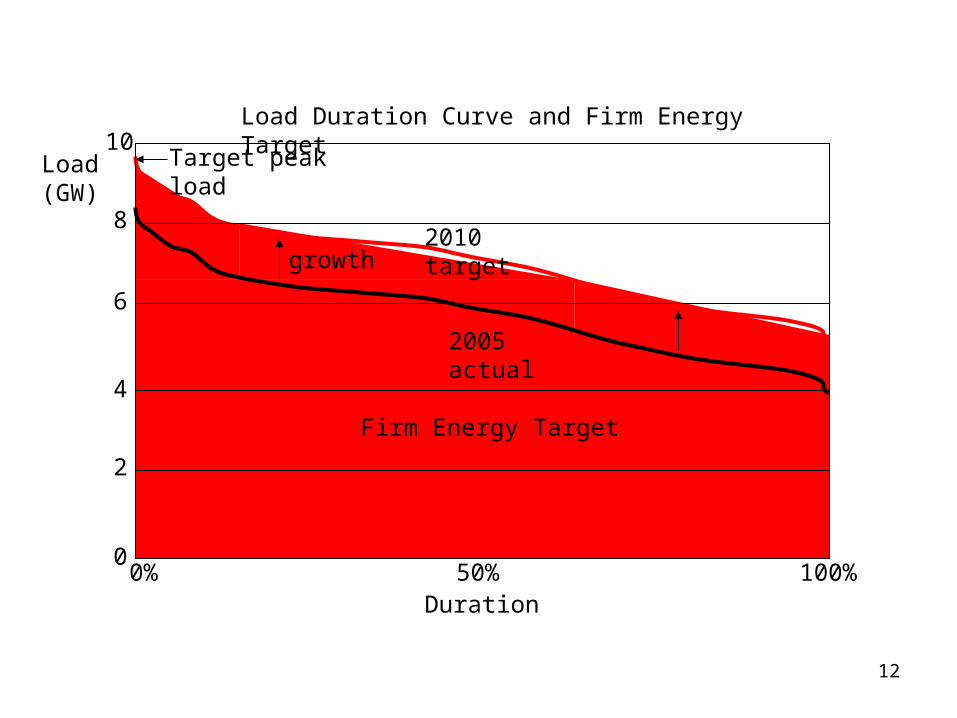

12

2010 target

2005 actual

0% 50% 100%

2

4

6

8

10

0

Duration

Load(GW)

Firm Energy Target

Load Duration Curve and Firm Energy Target

growth

Target peak load

13

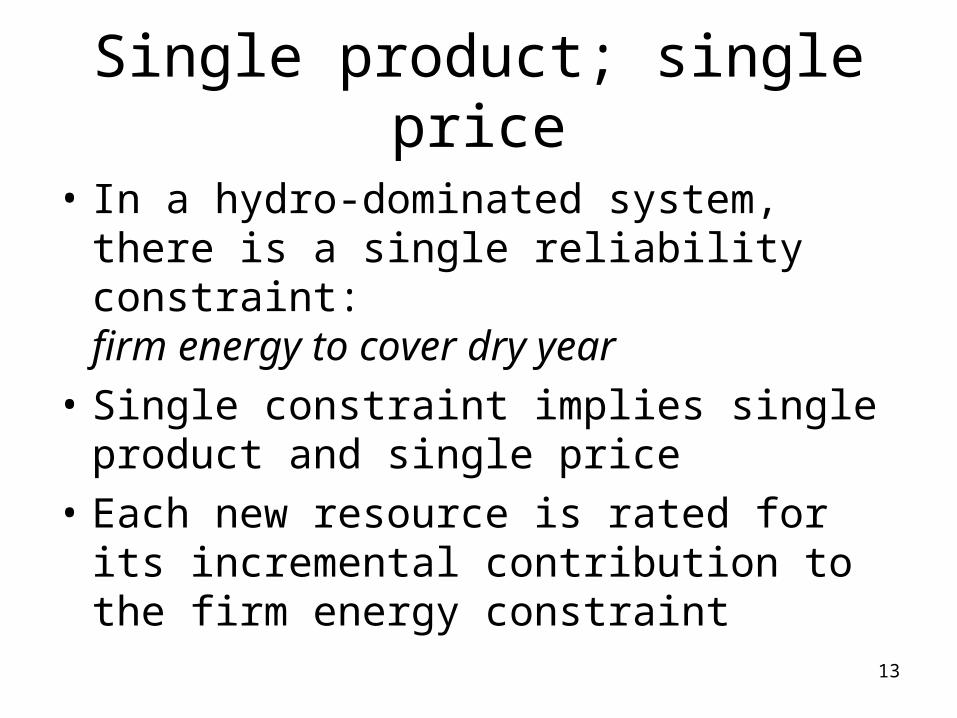

Single product; single price

• In a hydro-dominated system, there is a single reliability constraint:firm energy to cover dry year

• Single constraint implies single product and single price

• Each new resource is rated for its incremental contribution to the firm energy constraint

14

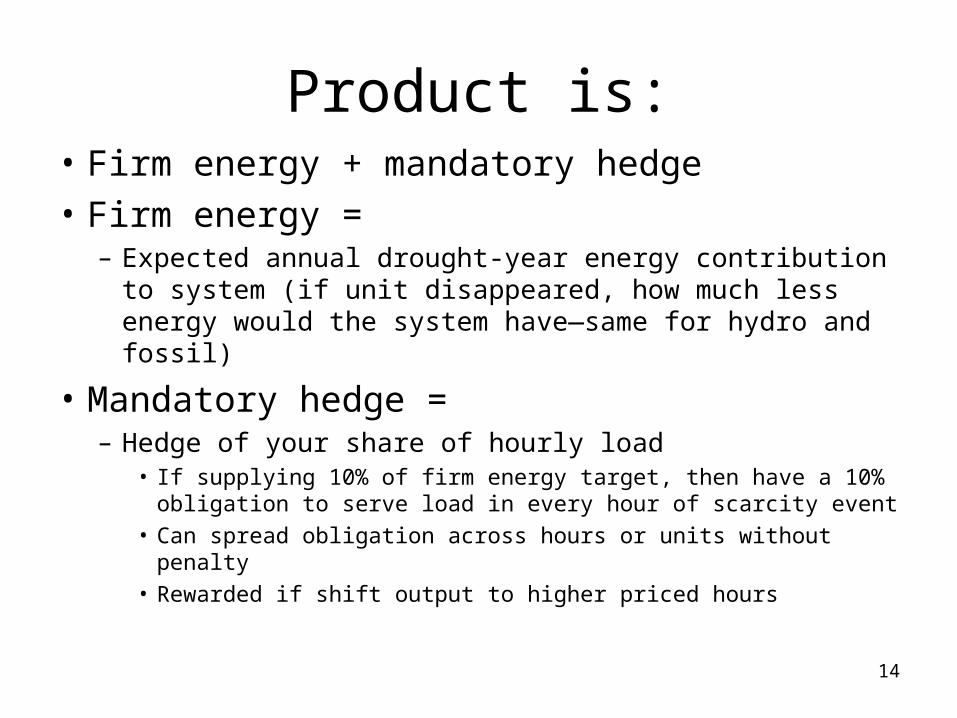

Product is:• Firm energy + mandatory hedge

• Firm energy =– Expected annual drought-year energy contribution to

system (if unit disappeared, how much less energy would the system have—same for hydro and fossil)

• Mandatory hedge = – Hedge of your share of hourly load

• If supplying 10% of firm energy target, then have a 10% obligation to serve load in every hour of scarcity event

• Can spread obligation across hours or units without penalty• Rewarded if shift output to higher priced hours

15

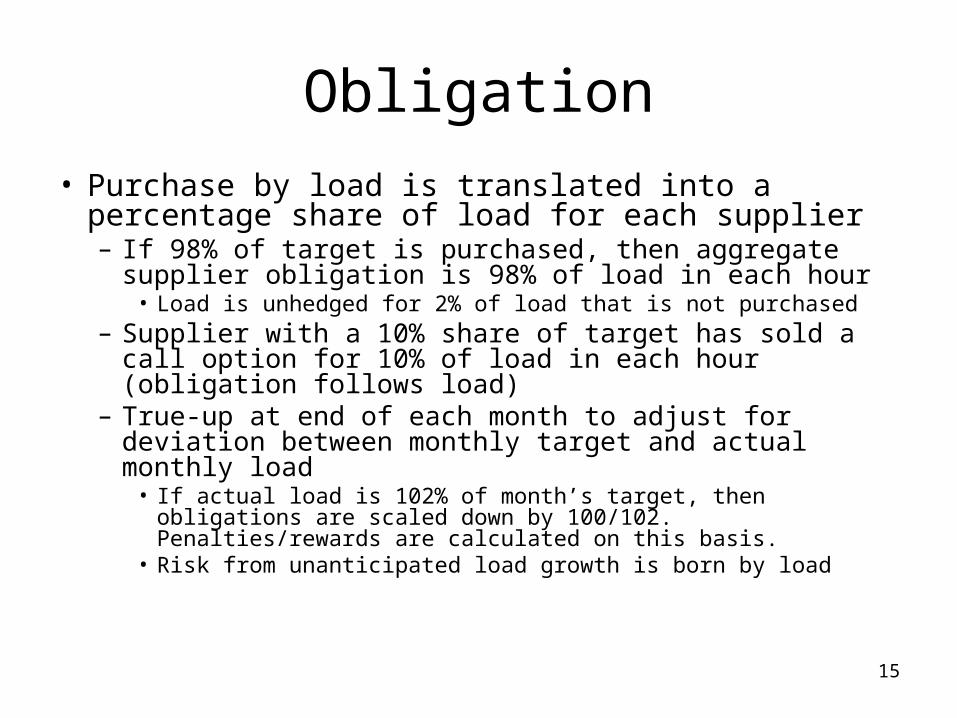

Obligation

• Purchase by load is translated into a percentage share of load for each supplier– If 98% of target is purchased, then aggregate supplier

obligation is 98% of load in each hour• Load is unhedged for 2% of load that is not purchased

– Supplier with a 10% share of target has sold a call option for 10% of load in each hour(obligation follows load)

– True-up at end of each month to adjust for deviation between monthly target and actual monthly load

• If actual load is 102% of month’s target, then obligations are scaled down by 100/102. Penalties/rewards are calculated on this basis.

• Risk from unanticipated load growth is born by load

16

Settlement

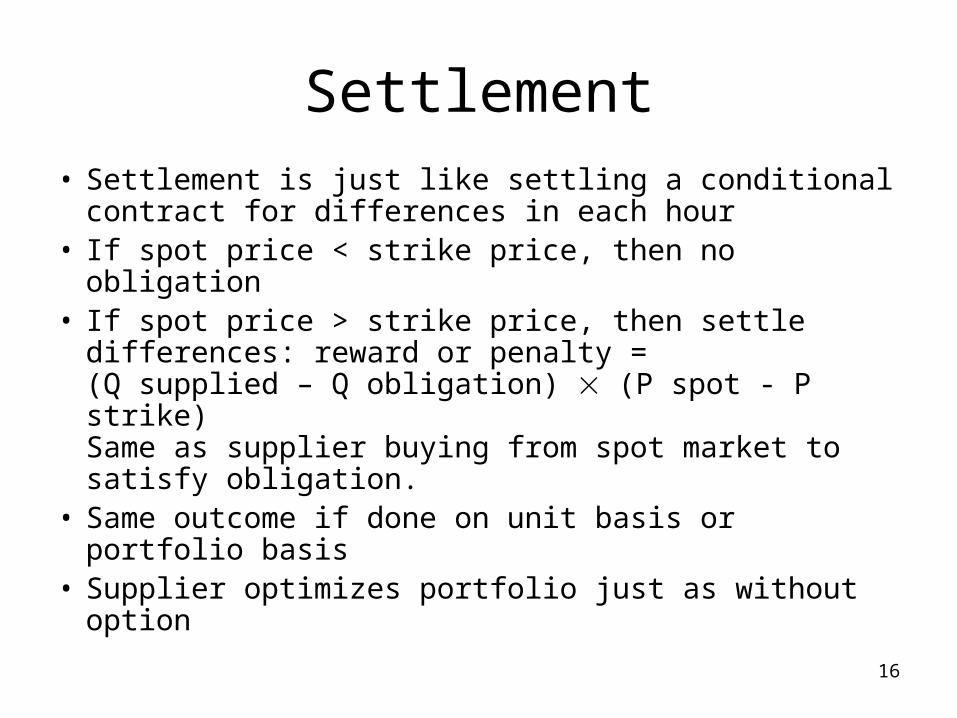

• Settlement is just like settling a conditional contract for differences in each hour

• If spot price < strike price, then no obligation• If spot price > strike price, then settle

differences: reward or penalty =(Q supplied – Q obligation) (P spot - P strike)Same as supplier buying from spot market to satisfy obligation.

• Same outcome if done on unit basis or portfolio basis

• Supplier optimizes portfolio just as without option

17

Planning period

18

Planning period

• Time between auction date and start of commitment

• 3 to 4 years ― long enough for new entry to occur

• Makes capacity market contestable and allows new entry to set the price– Existing capacity would set the wrong price

because of sunk costs and market power

19

Planning period

• First auction (2010): 3 year

• Second auction (2011): 3.5 year

• All later auctions (2012…): 4 year

20

Commitment period

21

Commitment period

• New capacity ― up to 10 years– Supplier selected at qualification– Long commitment lets new capacity lock-in capacity

price, reducing risk and encouraging investment– Price is in constant $ (adjusted for inflation)

• Existing capacity ― one year– Does not need long commitment, since costs are

already sunk– Short commitment reduces risk (more draws from

price distribution)

22

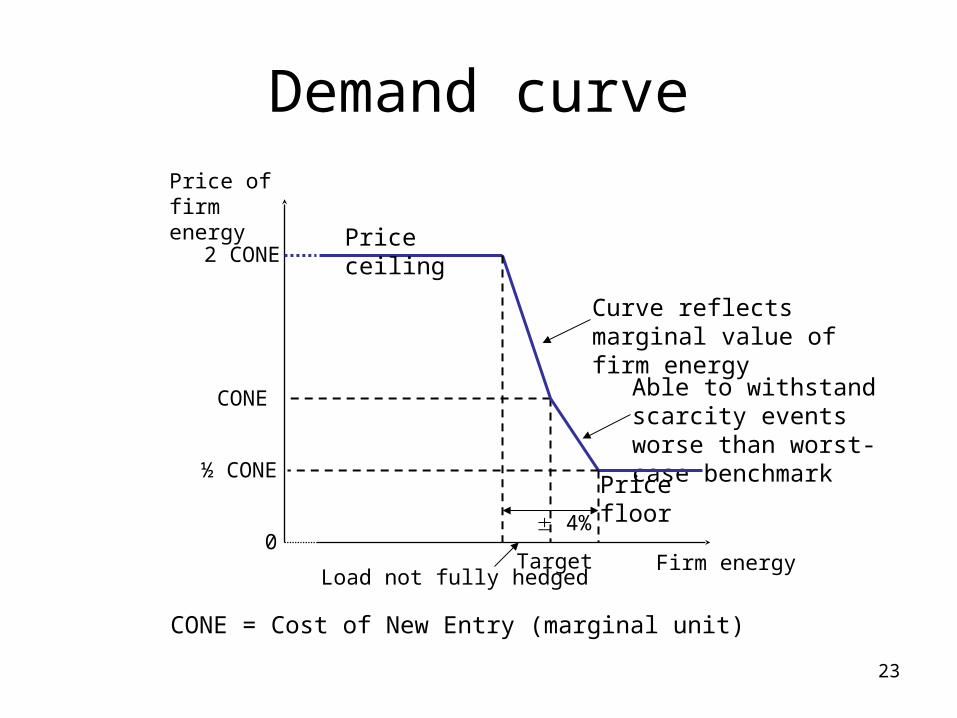

Demand curve

23

Demand curvePrice offirm energy

Firm energyTarget

CONE

2 CONE

CONE = Cost of New Entry (marginal unit)

0

Curve reflects marginal value of firm energy

Able to withstand scarcity events worse than worst-case benchmark

½ CONE

Price ceiling

Price floor

4%

Load not fully hedged

24

Descendingclock auction

25

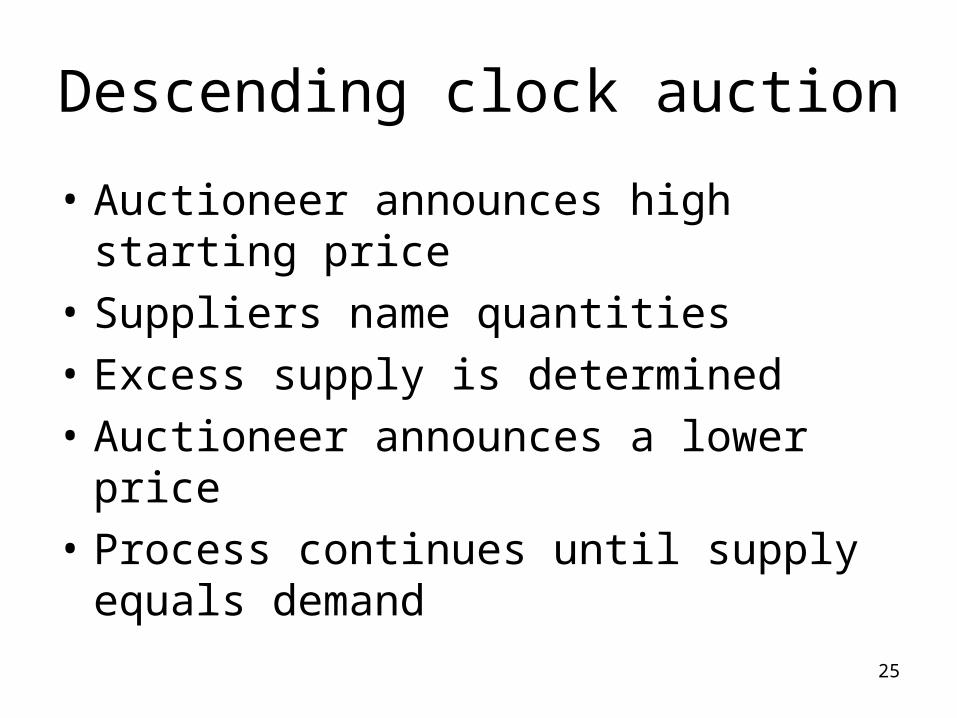

Descending clock auction

• Auctioneer announces high starting price

• Suppliers name quantities

• Excess supply is determined

• Auctioneer announces a lower price

• Process continues until supply equals demand

26

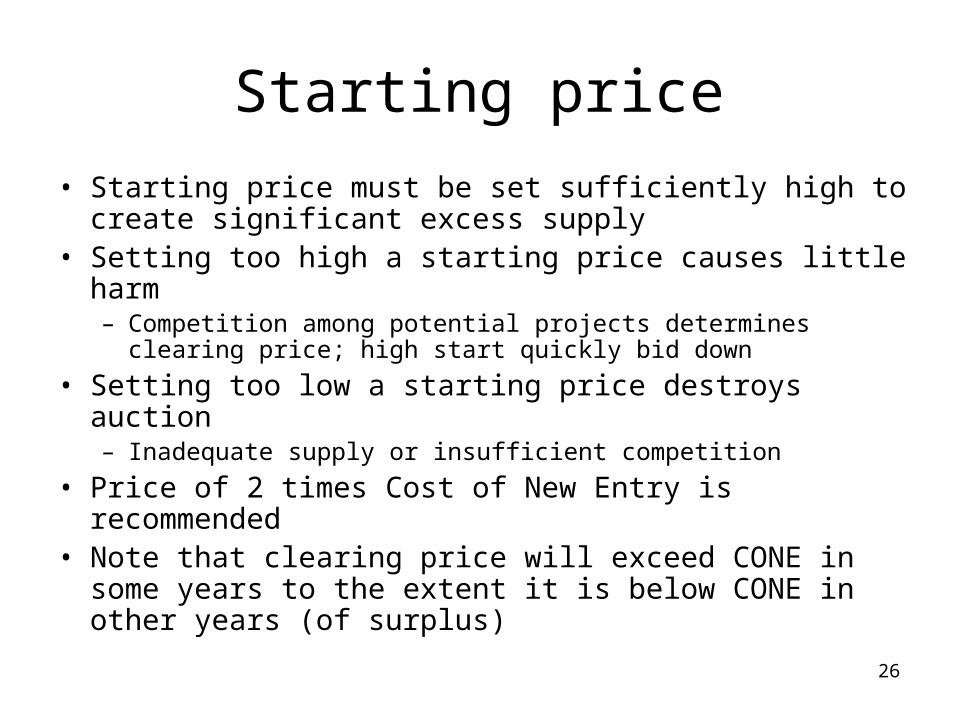

Starting price

• Starting price must be set sufficiently high to create significant excess supply

• Setting too high a starting price causes little harm– Competition among potential projects determines clearing price;

high start quickly bid down

• Setting too low a starting price destroys auction– Inadequate supply or insufficient competition

• Price of 2 times Cost of New Entry is recommended• Note that clearing price will exceed CONE in some years

to the extent it is below CONE in other years (of surplus)

27

CONE updates

• If auction in year t is successful,CONE in year t+1 = .7 CONE in year t

+ .3 clearing price in year t

• If auction in year t fails,

CONE in year t+1 = CONE in year t

28

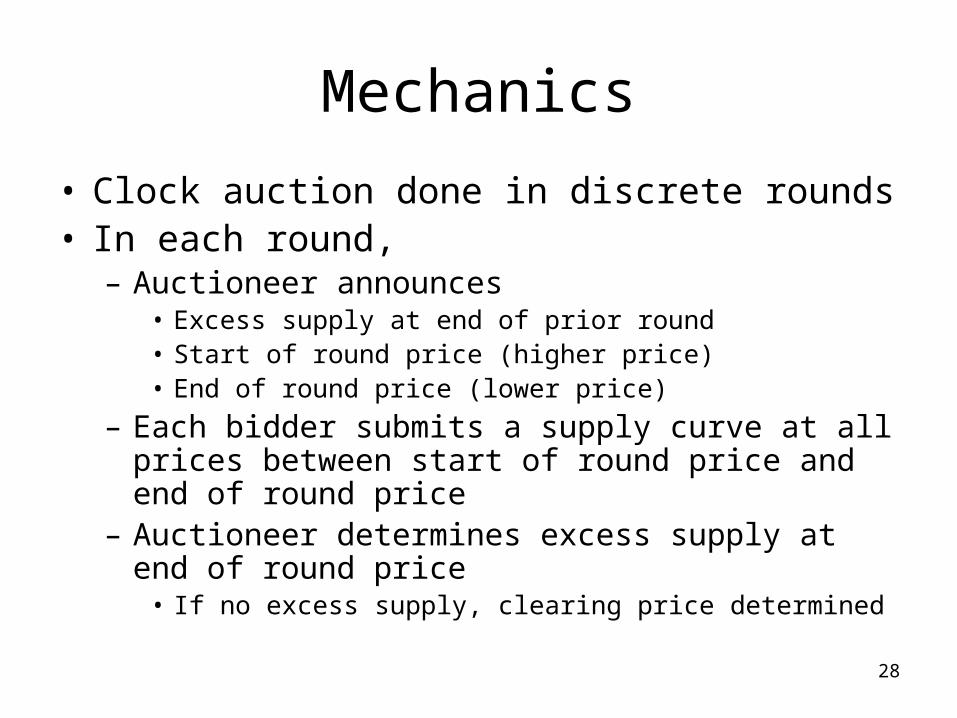

Mechanics

• Clock auction done in discrete rounds• In each round,

– Auctioneer announces• Excess supply at end of prior round• Start of round price (higher price)• End of round price (lower price)

– Each bidder submits a supply curve at all prices between start of round price and end of round price

– Auctioneer determines excess supply at end of round price

• If no excess supply, clearing price determined

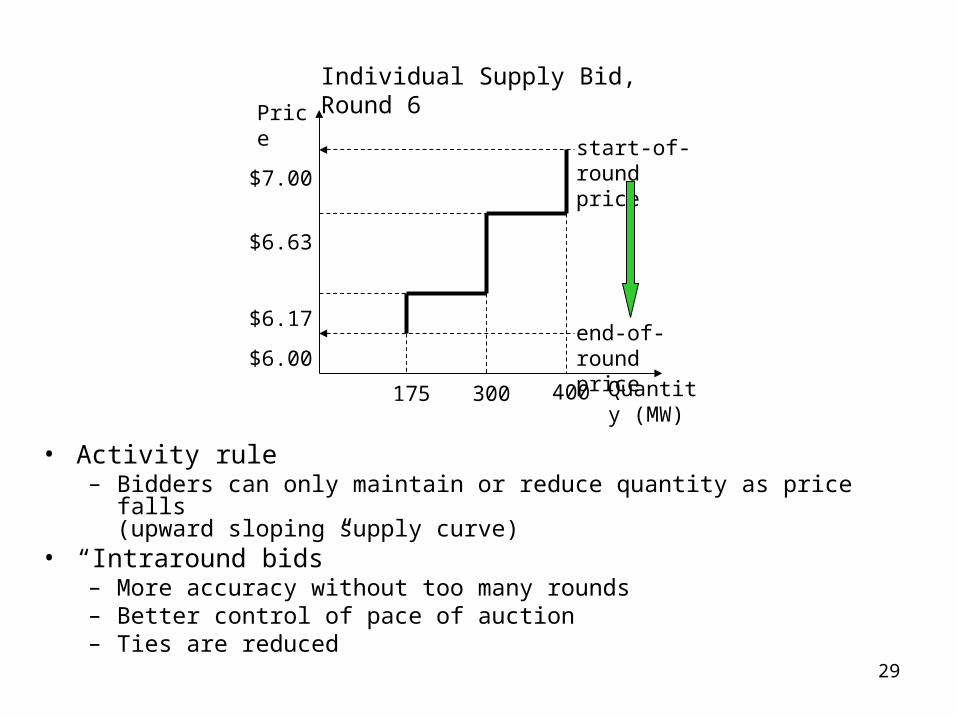

29

Price

$7.00

$6.63

$6.17

$6.00

Quantity (MW)

175 300 400

start-of-roundprice

end-of-roundprice

Individual Supply Bid, Round 6

• Activity rule– Bidders can only maintain or reduce quantity as price falls

(upward sloping supply curve)• “Intraround bids”

– More accuracy without too many rounds– Better control of pace of auction– Ties are reduced

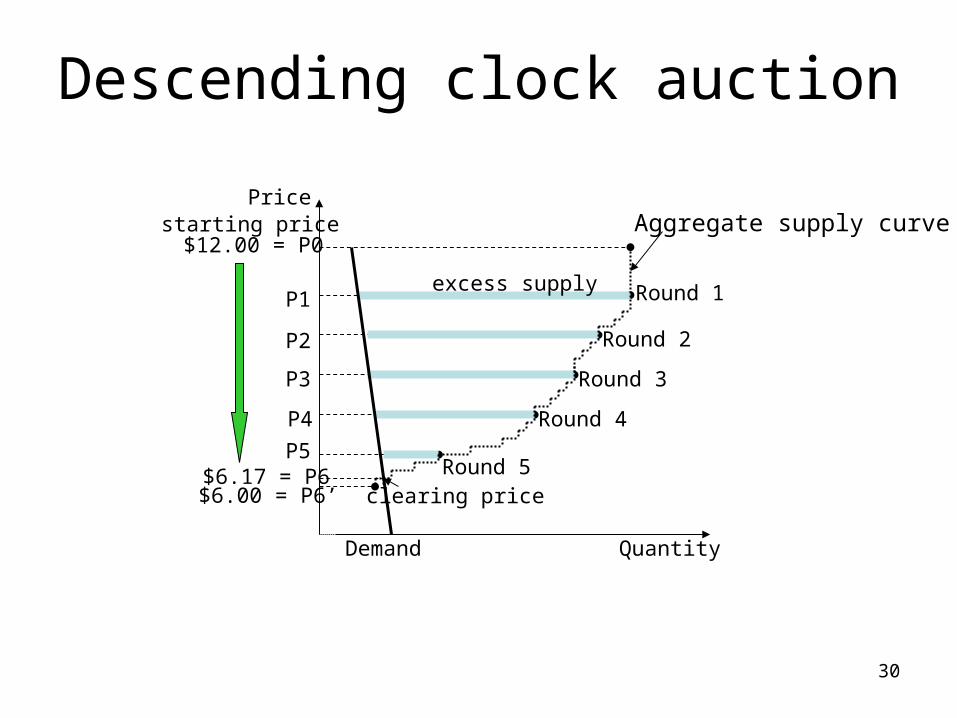

30

Price

$12.00 = P0

P1

P2

P3

QuantityDemand

Round 5

Round 4

starting price

clearing price

Aggregate supply curve

P4

P5 $6.17 = P6

Round 3

Round 2

Round 1 excess supply

$6.00 = P6’

Descending clock auction

31

Information policy

• Demand curve and starting price announced before auction

• After every round, auctioneer reports– Excess supply at end of round price– End of round price for next round

(determined from extent of excess supply)

32

New projects are all or nothing

• Lumpy investment respected; investor does not fear partial acceptance

• If multiple bidders drop at the clearing price, the group of bids are accepted that minimizes excess supply

33

Price formation

34

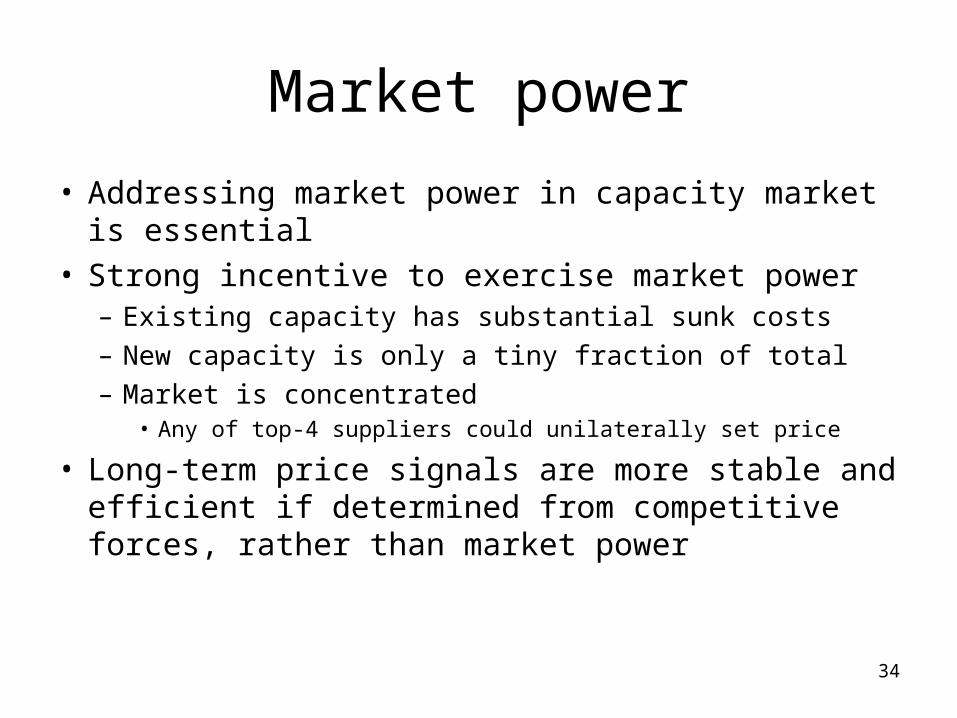

Market power

• Addressing market power in capacity market is essential

• Strong incentive to exercise market power– Existing capacity has substantial sunk costs– New capacity is only a tiny fraction of total– Market is concentrated

• Any of top-4 suppliers could unilaterally set price

• Long-term price signals are more stable and efficient if determined from competitive forces, rather than market power

35

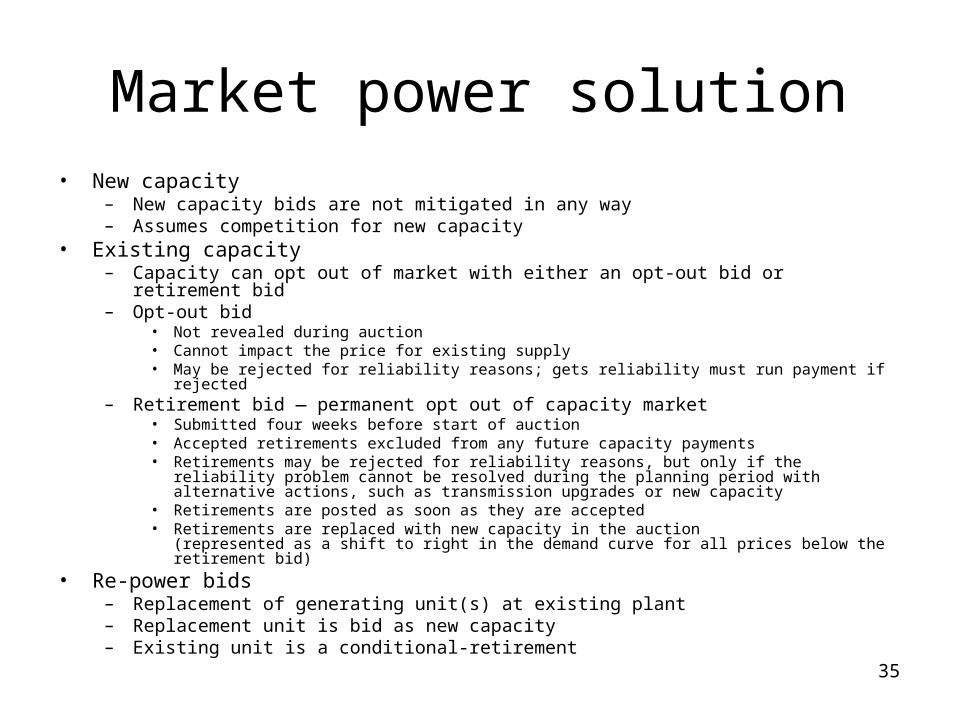

Market power solution• New capacity

– New capacity bids are not mitigated in any way– Assumes competition for new capacity

• Existing capacity– Capacity can opt out of market with either an opt-out bid or retirement bid– Opt-out bid

• Not revealed during auction• Cannot impact the price for existing supply• May be rejected for reliability reasons; gets reliability must run payment if rejected

– Retirement bid ― permanent opt out of capacity market• Submitted four weeks before start of auction• Accepted retirements excluded from any future capacity payments• Retirements may be rejected for reliability reasons, but only if the reliability problem cannot be

resolved during the planning period with alternative actions, such as transmission upgrades or new capacity

• Retirements are posted as soon as they are accepted• Retirements are replaced with new capacity in the auction

(represented as a shift to right in the demand curve for all prices below the retirement bid)

• Re-power bids– Replacement of generating unit(s) at existing plant– Replacement unit is bid as new capacity– Existing unit is a conditional-retirement

36

Market power solution

• New capacity almost always sets the price

• Demand curve sets the price in surplus years in which new entry is not needed

• Retirements occasionally set the price

• Other than retirements, existing capacity never impacts the price

37

Replacing accepted opt-outs

• Opt-outs are replaced by new capacity– March up the supply curve revealed in the

clock auction• But not more than a 30% increase in price• Any additional replacements occur in

reconfiguration

– All new capacity receives this higher price

• Existing capacity receives the original clearing price

38

Performanceincentives

39

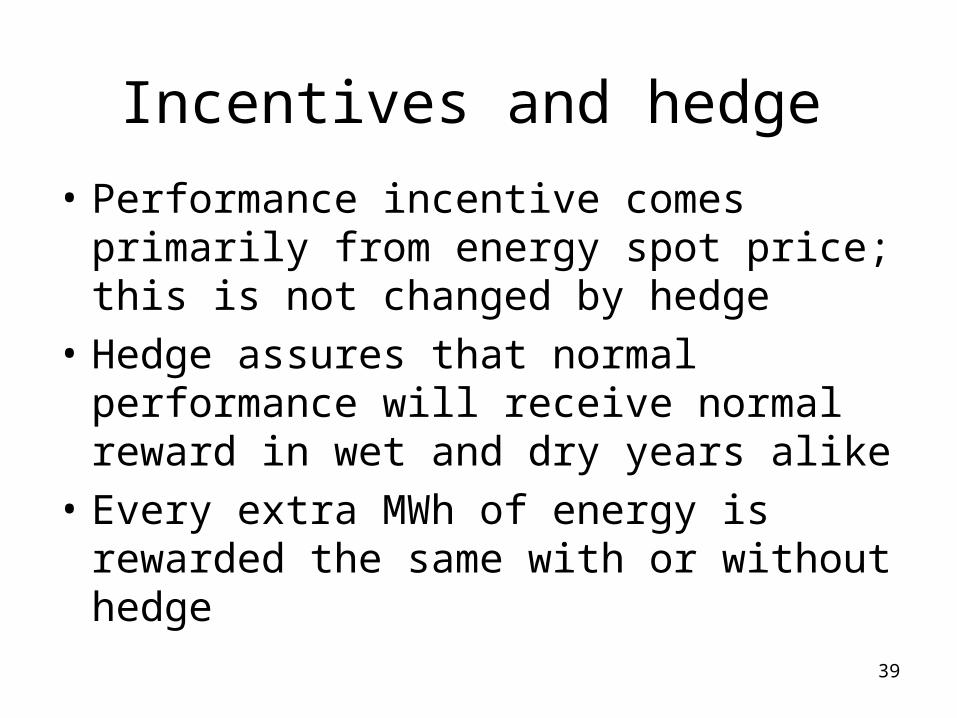

Incentives and hedge

• Performance incentive comes primarily from energy spot price; this is not changed by hedge

• Hedge assures that normal performance will receive normal reward in wet and dry years alike

• Every extra MWh of energy is rewarded the same with or without hedge

40

Energy price motivates performance

• Hedged resources still face the energy spot price at all times– Those that perform better receive more– Those that perform worse receive less

• An additional incentive to perform is impact on firm energy qualified for sale in auctions in future years

• Under performing units are downgraded• Over performing units are upgraded

41

Fail-safe mechanism

42

Protections if auction fails: Inadequate supply

• If, at the starting price, there is insufficient supply of firm energy– New capacity is paid starting price– Existing capacity is paid 1.1 CONE

• Note: Rule does not discourage new projects

43

Protections if auction fails:Insufficient competition

• Existing capacity, less retirements, is less than demand at the starting price, and

• At the starting price, the capacity bid exceeds demand but less than 4% excess, or a supplier’s new capacity is pivotal– Auction is conducted– New capacity is paid the clearing price– Existing capacity is paid the smaller of the clearing

price and 1.1 CONE

• Note: Rule does not discourage new projects

44

Secondary market

45

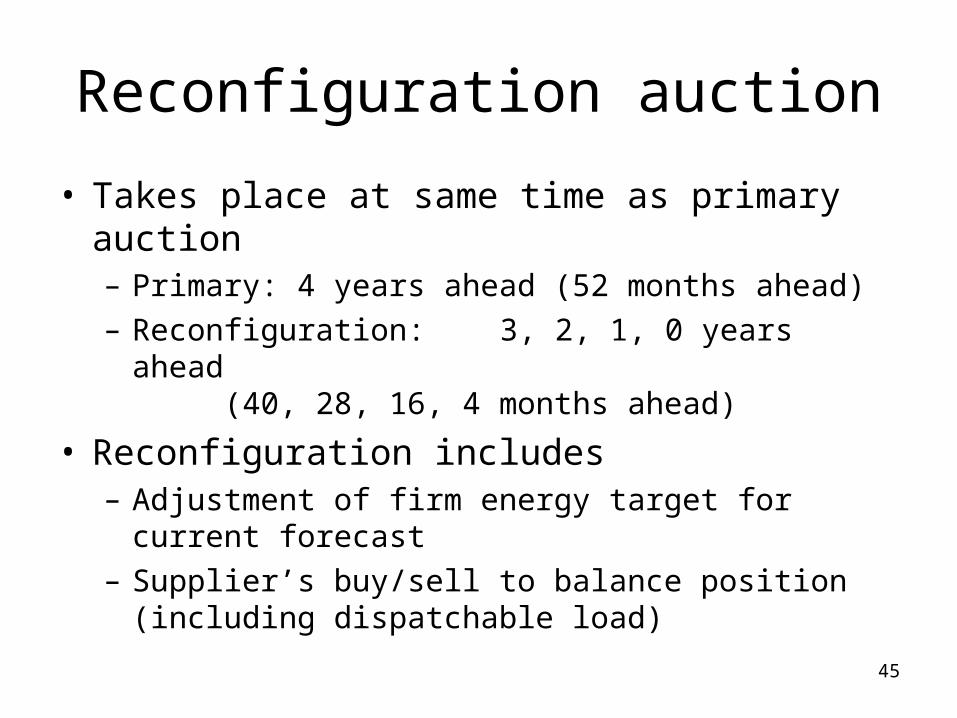

Reconfiguration auction

• Takes place at same time as primary auction– Primary: 4 years ahead (52 months ahead)– Reconfiguration: 3, 2, 1, 0 years ahead

(40, 28, 16, 4 months ahead)

• Reconfiguration includes– Adjustment of firm energy target for current forecast– Supplier’s buy/sell to balance position

(including dispatchable load)

46

Reconfiguration auction

• Standard sealed-bid clearing-price auction

• Same demand curve as in primary auction, netting out capacity already purchased

• No bid mitigation

47

Monthly spot exchange

• Monthly simultaneous clearing– Standard sealed-bid clearing-price auction– Suppliers buy/sell to balance positions– Demand curve same as in primary auction

48

Transition

49

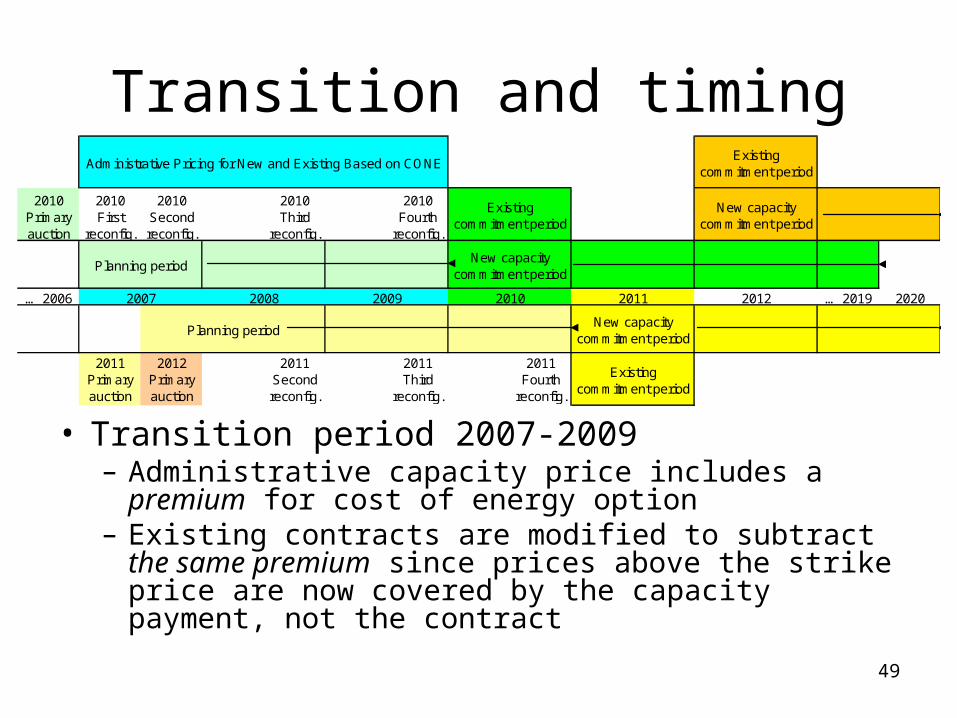

Transition and timing

• Transition period 2007-2009– Administrative capacity price includes a premium for

cost of energy option– Existing contracts are modified to subtract the same

premium since prices above the strike price are now covered by the capacity payment, not the contract

2010 Primary auction

2010 First

reconfig.

2010 Second reconfig.

2010 Third

reconfig.

2010 Fourth

reconfig.

… 2006 … 2019 2020

2011 Primary auction

2012 Primary auction

2011 Second reconfig.

2011 Third

reconfig.

2011 Fourth

reconfig.

Existing commitment period

New capacity commitment period

Existing commitment period

Planning period

New capacity commitment period

Planning periodNew capacity

commitment period

Administrative Pricing for New and Existing Based on CONE

2007 2008 2009 2010 2011 2012

Existing commitment period

50

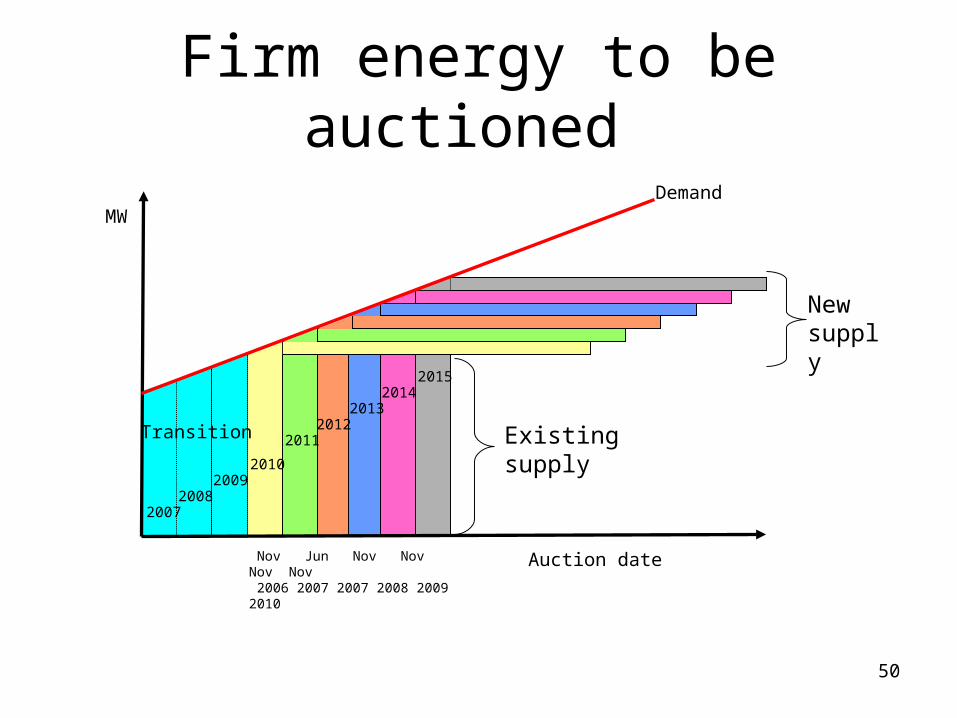

MWDemand

Transition

Auction date

Firm energy to be auctioned

20072008

20092010

20112012

20132014

2015

Existing supply

New supply

Nov Jun Nov Nov Nov Nov 2006 2007 2007 2008 2009 2010

51

Supplier concerns

52

Supplier concerns

• Please note that these concerns were as expressed to CREG on Monday, 5 June 2006, in response to the original CREG proposal. These concerns may not apply to proposal presented here, which is significantly different from the original proposal.

53

1. Approach not used elsewhere

• Similar approach was adopted in New England (32 GW peak load) in March 2006– Approach currently being implemented– Approach endorsed by FERC

• All elements of proposal are commonly used in markets around the world– Options are used everywhere– Clock auctions used for many years in US, UK,

France, Germany, Belgium, Hungary, Denmark, …

54

2. Call option increases risk

Price Coverage

Forward Energy Contract

US$130

US$250

US$0 US$0

US$250

Forward Energy Contract

Energy Option

55

3. Consumers will pay more

• Minimizing risk while addressing market power and performance incentives means that consumers will pay less

56

4. Price not a reliable measure of scarcity

• High prices come from two sources– Scarcity– Market power

• Option fully addresses market power in spot market; thus, high prices can only come from scarcity

• If spot prices are still unreliable, then market must have another flaw. Fix it!

57

5. Approach is complex

• Effective capacity markets are necessarily complex because the economic challenges are great, especially market power

• Proposal uses clear and simple market-based methods

58

Supplier alternative

59

Does not adequately address performance incentives

• Fails to induce right mix of resources

• Fails to induce efficient operation of resources

• Requires greater command-and-control regulation

60

Does not address market power

• Yields unstable an uneconomic capacity prices– Greater financial and political risk

• Higher contract costs due to potential for market power in energy spot market

• Higher energy spot prices and less efficient energy spot market

61

Questions