1Copyright © 2013 McGraw-Hill Ryerson Limited

Learning Objectives

LO4 Explain the three categories of cash flow reported in the cash flow statement and identify the types of transactions that apply to each category.

LO5 Read and interpret the cash flow statement.

LO6 Explain how manager decisions can affect cash flow information and how accrual accounting policy choices affect the cash flow statement.

2

Cash Flows - Financing Activities

• Quite straightforward:▫Changes in long term liabilities and

capital stock accounts▫Do not net out positive and negative

changes▫Includes only transactions affecting cash

• Financing activities help to meet cash needs not met by cash from operations

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

3

Cash Flows - Investing Activities

• Quite straightforward:▫Changes in long term asset accounts▫Do not net out positive and negative

changes▫Includes only transactions affecting cash

• Involves assets typically used for more than one period

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

4

Cash From Operations

• Important source of liquidity• Usually positive, but can be negative

• Choice of presentation▫Direct Method▫Indirect Method

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

5

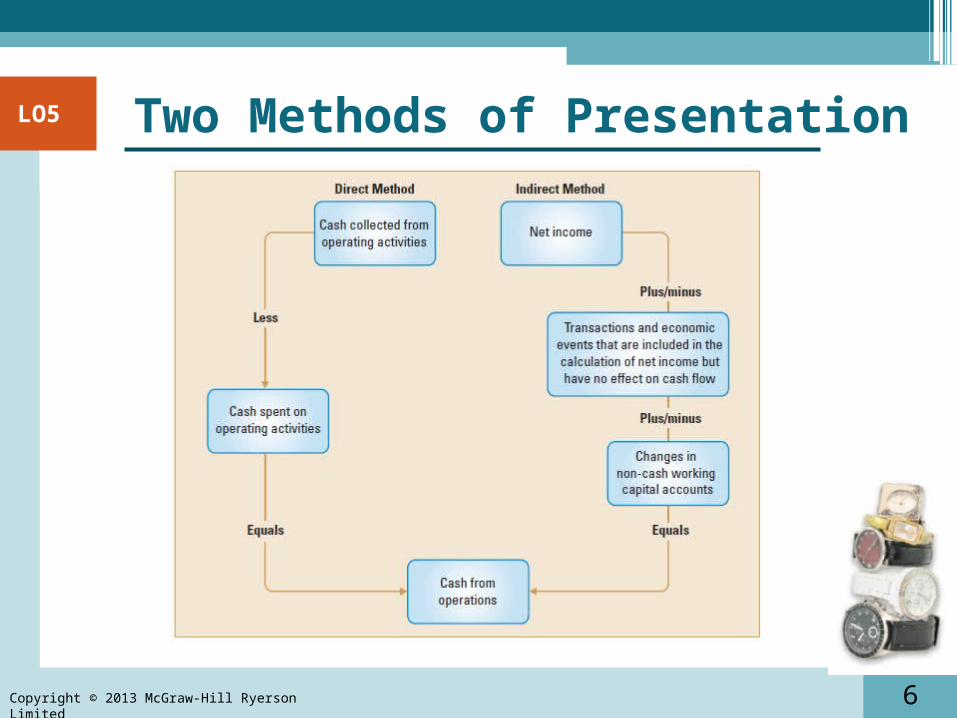

Cash From Operations

• Direct Method▫Reports cash collections and

disbursements in detail

• Indirect Method▫Starts with net income▫Adjusts net income for non cash items

included ▫Adjusts for operating cash flows that are

not included in net income

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

6

Two Methods of Presentation

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

7

Indirect Method

• Adjustments required: 1. Changes in non-cash current operating

accounts2. Transactions included in the

calculation of net income not involving cash

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

8

Indirect Method: Non-Cash Items

• Non-cash items subtracted when calculating net income must be added back when reconciling to CFO

• Include depreciation, gains, losses, deferred income taxes, writedowns of assets and writeoffs

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

9

Indirect Method: Accruals

• Adjust net income for accrual based revenues and expenses to reflect cash flows• Convert by adjusting for changes in

non-cash working capital accounts• Examples of non-cash working capital

accounts include: accounts receivable, inventory, prepaids, accounts payable, wages payable, accrued liabilities, etc.

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

10

Interpreting Cash Flows

• Used to predict future events• Operating cash flow sustains the

business• Financing activities supports growth• Investing activities are required to

maintain position in the market

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

11

Qualitative Considerations

• Provides information relating to solvency• Consider life cycle and entity

characteristics

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

12

Quantitative Considerations

• Operating cash flow to current liability ratio ▫= CFO/Avg. Current Liabilities

• Free Cash Flow ▫= CFO – Capital Expenditure

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5

13

IFRS Requirements

• A cash flow statement is a requirement • Classification of interest paid and

received• Classification of dividends paid and

received

Copyright © 2013 McGraw-Hill Ryerson Limited

LO5