35

1 Corporate governance Week 9

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 219 times |

| Download: | 0 times |

1

Corporate governance

Week 9

2

Outline Separation of ownership & managerial control Ownership concentration Boards of directors Executive compensation Multi-divisional structure International corporate governance Governance mechanisms and ethical behaviour

3

Corporate Governance

The relationship among stakeholders that is used to determine and control the strategic direction and performance of the organisation

Concerned with identifying ways to ensure that strategic decisions are made effectively

Used in corporations to establish order between the firm’s owners and its top-level managers

4

Shareholders The right to share in residual income means that

shareholders must accept the risk that no residual profits will remain if the firm’s expenses exceed its income.

Reduce risk efficiently by holding diversified portfolios In small firms, managers and owners are often one in the

same, so there is no separation of ownership and control.

As firms grow larger, individual owners generally do not have access to sufficient capital to fund the growth of the business and seek other investors with which to share residual profits (and risk).

5

Separation of Ownership & Managerial Control

Shareholders Purchase stock, becoming Residual Claimants Reduce risk efficiently by holding diversified portfolios

Professional managers contract to provide decision-making

Leads to efficient specialisation of tasks, such as: Risk bearing by shareholders Strategy development and decision-making by

managers

6

An agency relationship exists when:An agency relationship exists when:

Shareholders (Principals)

Firm Owners

Agency Relationship

Risk Bearing Specialist(Principal)

Managerial Decision-Making Specialist

(Agent)

Managers (Agents)

DecisionMakers

which creates

Hire

Agency TheoryAgency TheoryAgency TheoryAgency Theory

7

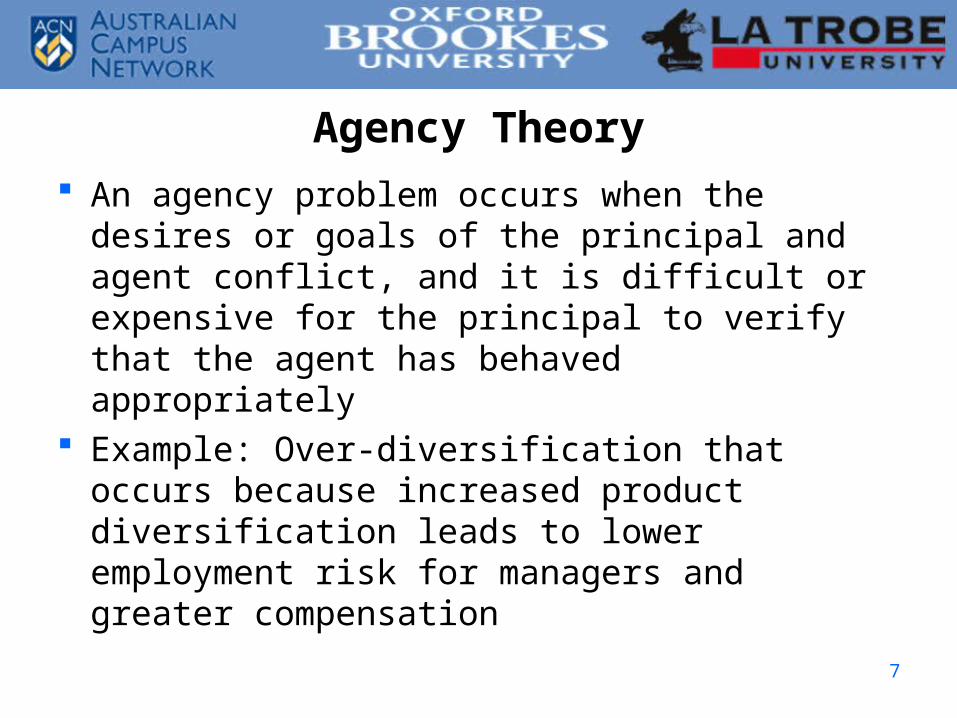

Agency Theory

An agency problem occurs when the desires or goals of the principal and agent conflict, and it is difficult or expensive for the principal to verify that the agent has behaved appropriately

Example: Over-diversification that occurs because increased product diversification leads to lower employment risk for managers and greater compensation

8

Risk

Risk

Level of Diversification

Manager & Shareholder Risk & DiversificationManager & Shareholder Risk & Diversification

DominantBusiness

UnrelatedBusinesses

RelatedConstrained

RelatedLinked

Shareholder (Business) Risk Profile

Managerial(Employment)

Risk Profile

9

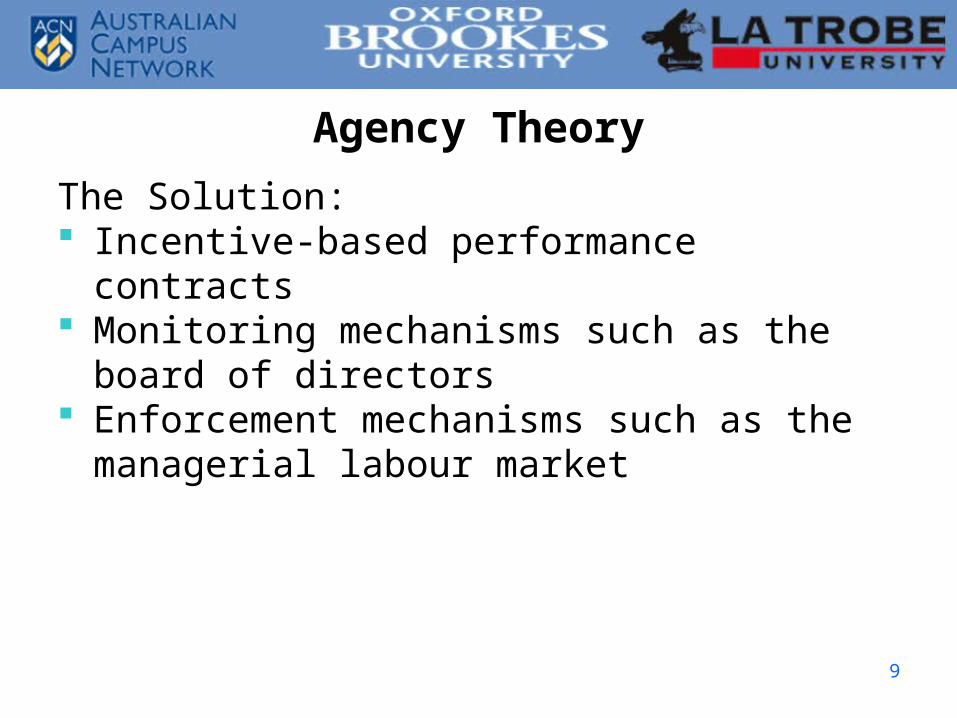

Agency Theory

The Solution: Incentive-based performance contracts Monitoring mechanisms such as the board of

directors Enforcement mechanisms such as the

managerial labour market

10

Agency Theory Principals may engage in monitoring behaviour

to assess the activities and decisions of managers

However, dispersed shareholding makes it difficult and inefficient to monitor management’s behaviour

Boards of directors have a fiduciary duty to their shareholders to monitor management

However, boards of directors are often accused of being lax in performing this function

11

Agency Costs The sum of incentive, monitoring, and

enforcement costs as well as any residual losses incurred by principals because it is not possible for principals to guarantee 100% compliance through monitoring arrangements.

12

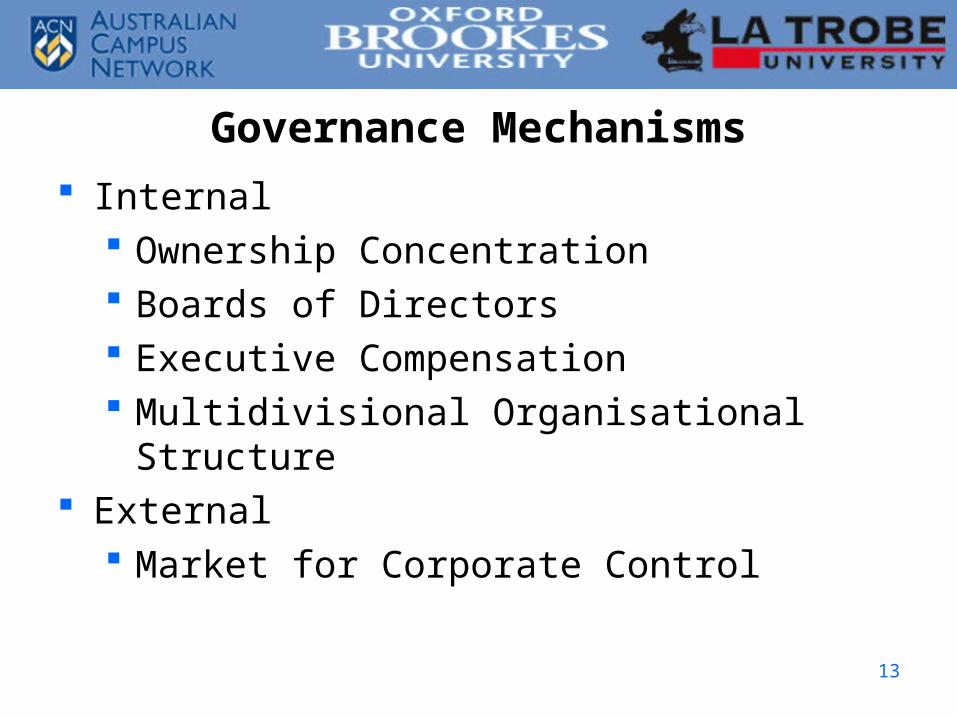

Corporate Governance Mechanisms

Prevent problems emanating from the separation of ownership and control by positively influencing managerial behaviour

Direct top level managers actions towards preferred shareholder aims is dependent on correct mechanisms

13

Governance Mechanisms

Internal Ownership Concentration Boards of Directors Executive Compensation Multidivisional Organisational Structure

External Market for Corporate Control

14

Internal Governance Mechanisms

Ownership concentration Relative amounts of stock owned by individual

shareholders & institutional investors Defined by the number of large block

shareholders and the total % they own Large block typically have at least 5% Large block shareholders have a strong

incentive to monitor management closely

15

Internal Governance Mechanisms

Ownership concentration Their large stakes make it worthwhile for them to

spend time, effort and expense to monitor closely

They can obtain board seats. This enhances their ability to monitor effectively (although financial institutions are legally forbidden to hold board seats directly)

Diffuse Ownership Produces weak monitoring of managerial

decisions

16

Internal Governance Mechanisms

Diffuse Ownership (cont.) Makes it difficult for owners to coordinate their

actions effectively May result in levels of diversification that are

beyond the optimum level desired by shareholders (especially when this condition is combined with weak monitoring)

17

Internal Governance Mechanisms

Board of Directors Responsible for representing the firms owners

by monitoring strategic decisions of top level managers

Consists of insiders, related outsiders and outsiders

Review and ratify important decisions Set compensation for the CEO and decide when

to replace the CEO Usually lack contact with day-to-day operations

18

Internal Governance Mechanisms

Board of Directors Must deal with Managerial Opportunism Seeking of self-interest with guile where

opportunism is represented by an attitude or inclination and a set of behaviors (self-interest seeking with guile).

19

Internal Governance Mechanisms

Executive Compensation Salary, bonuses, long-term incentive

compensation To align interests of managers with those of

shareholders Executive decisions are complex and non-

routine It is difficult to establish how managerial

decisions are directly responsible for outcomes

20

Internal Governance Mechanisms

Executive compensation Incentive systems do not guarantee that

managers make the ‘right’ decisions, but do increase the likelihood that managers will perform the activities and achieve the results for which they are rewarded

Stock ownership (long-term incentive compensation) makes managers more susceptible to market changes that are partially beyond their control

21

Internal Governance Mechanisms

Multi-divisional structure Designed to control managerial opportunism

Corporate office and board monitor business-unit managers’ strategic decisions

Increased managerial interest in maximising wealth

Broadly diversified product lines make it difficult for top-level managers to evaluate the strategic decisions of divisional managers

22

Internal Governance Mechanisms

Multi-divisional structure (cont.) It may not effectively govern actions taken by the

corporate office. Firms using the M-form structure are more likely

to continue diversification. The M-form facilitates further diversification. Continued diversification may create conditions

requiring division mangers to emphasize short-term results.

23

External Governance Mechanism

Market for corporate control The market for corporate control acts as an

important source of discipline over managerial incompetence and waste

Operates when firms face the risk of takeover where they are operated inefficiently

Changes in regulations have made hostile takeovers difficult

24

Board of Directors

Powers Directing the affairs of the organisation Punishing (disciplining) and rewarding

(compensating) managers Protecting the rights and interests of

shareholders (owners) As a result, if the board of directors is

appropriately structured and operates in an effective manner, it can protect owners from managerial opportunism.

25

Board of Directors

Problems Insiders continue to dominate boards (by

controlling the flow of information to outside directors)

Outside directors are nominated for board membership by insiders (primarily by the CEO) and thus are indebted to insiders

26

Board of Directors

Boards working collaboratively with management Make higher quality strategic decisions Make decisions faster Become more involved in decisions regarding

succession (rather than blindly supporting the incumbent’s choice)

27

Board of Directors

Recommendations for More Effective Board

Governance: Increase diversity of board members’

backgrounds (Australian boards obviously lack diversity)

Strengthen internal management and accounting control systems

Establish formal processes for evaluation of the board’s performance

28

Corporate Governance in Australia Importance of institutional shareholders A small market for corporate control compared

to the USA Boards are relatively small: 6-12 people,

very few females, many multiple board memberships, 75% non-executive directors

Australian landscape features an active financial press, an active shareholders’ association and an increasingly important role for government in corporate governance

29

Corporate Governance in Australia

Major banks dominate large companies The top three shareholders of Amcor, BHP and

Brambles are the same: Westpac Chase Manhattan (a US bank) National Nominees (NAB)

30

Corporate Governance in Australia There must be protection for all shareholders

(including those with a minority holding) Management must be held accountable to

shareholders regularly There must be transparency and full disclosure

by each Australian Stock Exchange-listed company

There must be an active, and independent, board that oversees a corporation’s management.

31

Laws and Institutions in Australia Legislation:

Corporations Law Trade Practices Act 1974 Prices Surveillance Act 1983

The Australian Competition and Consumer Commission (ACCC);

Australian Securities and Investments Commission (ASIC);

Australian Stock Exchange (ASX) Shareholder activists Financial media

32

Corporate Governance in Germany

Public firms often have a dominant shareholder frequently a bank

Medium-to-large firms have a two-tiered board: Vorstand monitors and controls managerial decisions Aufsichtsrat selects the Vorstand Employees, union members and shareholders appoint

members to the Aufsichtsrat

There is usually less emphasis on shareholder value than for Australian. firms, although this may be changing

33

Corporate Governance in Japan Obligation, ‘family’ and consensus are important factors Banks (especially ‘main bank’) are highly influential with

firm’s managers Keiretsus are strongly interrelated groups of firms tied

together by cross-shareholdings Powerful government intervention Close relationships between firms and government

sectors Passive and stable shareholders who exert little control Virtual absence of external market for corporate control

34

Ethical Corporate Behaviour It is important to serve the interests of multiple

stakeholder groups Important stakeholder groups

Shareholders are served by the board of directors Product market stakeholders (customers, suppliers

and host communities) and organisational stakeholders (managerial and non-

managerial employees) There is a controversial belief that ethically responsible

firms should introduce governance mechanisms that serve all stakeholders’ interests

35

Australian Shareholders Association

An active lobby group against corporate governance misbehaviour

Has policies about: Executive performance Conflict of interest Disclosure Poor firm performance