39

1 Cyber Hurricane The Potential for Aggregated Internet Losses and the Insurance Industry Professional Liability Underwriting Society 16 th Annual Conference Philadelphia, PA

| Date post: | 03-Jan-2016 |

| Category: |

Documents |

| Upload: | aron-miller |

| View: | 213 times |

| Download: | 0 times |

11

Cyber Hurricane

The Potential for Aggregated Internet Losses and the Insurance Industry

Professional Liability Underwriting Society

16th Annual Conference

Philadelphia, PA

22

Panel

Paul Nicholas Rich ReedDirector for Critical Infrastructure Protection Vice President Homeland Security Council Chubb & Son, Inc.

Rob Hammesfahr Harrison Oellrich

Managing Partner Managing Director

Cozen O’Connor Guy Carpenter

3

4

The National StrategyThe National Strategy “Securing cyberspace is an

extraordinarily difficult strategic challenge that requires a coordinated and focused effort from our entire society—the federal government, state and local governments, the private sector, and the American people.”

“The cornerstone of America’s cyberspace security strategy is and will remain a public-private partnership.”

President George W. BushPresident George W. Bush

5

The Case for ActionThe Case for Action

6

Cyber Threats Cyber Threats

• Organized cyber attacks that may cause debilitating disruption to our infrastructures, economy, or national security is a primary concern.

• Attack tools and methodologies are widely available, and the technical skills of attackers capable of causing disruption is growing.

• A spectrum of malicious actors can and do attack critical information infrastructures.

7

Dangerous CurvesDangerous Curves

8

Cyberspace Security PolicyCyberspace Security Policy

Prevent cyber attacks against our Prevent cyber attacks against our critical infrastructures;critical infrastructures;

Reduce our national vulnerabilities Reduce our national vulnerabilities to cyber attack; andto cyber attack; and

Minimize the damage and recovery Minimize the damage and recovery time from cyber attacks that do time from cyber attacks that do occur.occur.

9

National PrioritiesNational Priorities

1.1. National Cyberspace Security National Cyberspace Security Response SystemResponse System

2.2. Threat and Vulnerability Threat and Vulnerability ReductionReduction

3.3. Awareness & TrainingAwareness & Training

4.4. Securing Government’s Securing Government’s CyberspaceCyberspace

5.5. International CooperationInternational Cooperation

PLUS - 16th Annual PLUS - 16th Annual International ConferenceInternational Conference

November 9-11, 2003 November 9-11, 2003

Rich Reed, Global Intellectual Rich Reed, Global Intellectual Property and eCommerce Property and eCommerce Product Manager Product Manager

Chubb Commercial Insurance Chubb Commercial Insurance

[email protected]@chubb.com

1111

The views, information and content The views, information and content expressed herein are those of the authors expressed herein are those of the authors and do not necessarily represent the views of and do not necessarily represent the views of any of the Insurers of The Chubb Group of any of the Insurers of The Chubb Group of Insurance Companies. Chubb did not Insurance Companies. Chubb did not participate in and takes no position on the participate in and takes no position on the nature, quality or accuracy of such content. nature, quality or accuracy of such content. The information provided should not be relied The information provided should not be relied on as legal advice or a definitive statement of on as legal advice or a definitive statement of the law in any jurisdiction. For such advice, the law in any jurisdiction. For such advice, an applicant, insured, listener or reader an applicant, insured, listener or reader should consult their own legal counsel. should consult their own legal counsel.

1212

Developing Insurance SolutionsDeveloping Insurance Solutions

Events are categorized Events are categorized Causation determined Causation determined Cost/Impact - frequency/severity/sources Cost/Impact - frequency/severity/sources

of aggregationsof aggregations Preferred risk classes are identified Preferred risk classes are identified Spread of risk is achieved Spread of risk is achieved Market is establishedMarket is established

1313

Where is the Cyber Where is the Cyber Insurance Marketplace? Insurance Marketplace?

MaturingMaturing

1414

Events - Some of the OldEvents - Some of the Old

Physical damage to Critical Resources:Physical damage to Critical Resources: – Natural and man made disasters Natural and man made disasters – Cyber-terrorismCyber-terrorism– Machinery breakdownMachinery breakdown– Vandalism – employee/third parties Vandalism – employee/third parties – Computer fraud/theft Computer fraud/theft

– Remote locations - storage/supplierRemote locations - storage/supplier

1515

Events - Some of the NewEvents - Some of the New

Proliferation and strengthening of Proliferation and strengthening of computer viruses and worms.computer viruses and worms. – Reduces functionality, and increasingly Reduces functionality, and increasingly

causing damage causing damage – Can impact single or multiple customers Can impact single or multiple customers – Insurers can’t subrogate against developers Insurers can’t subrogate against developers – Prosecution of culprits, has slowed, but not Prosecution of culprits, has slowed, but not

stopped the trendstopped the trend

1616

Events - Some of the NewEvents - Some of the New

Unauthorized computer access or useUnauthorized computer access or use– Insider or outsider Insider or outsider – Reducing functionality, causing damage Reducing functionality, causing damage – Theft data, money or securities Theft data, money or securities – Launching an attack aimed at multiple Launching an attack aimed at multiple

parties parties Denial of service attacks Denial of service attacks

1717

Dependence on the “Web”Dependence on the “Web”

The Internet is resilient….but:The Internet is resilient….but: – Productivity rests on the operation, security Productivity rests on the operation, security

and continuity of a “public network” and continuity of a “public network” – Individual risk profile varies:Individual risk profile varies:

based on business modelbased on business model proactive – security policies and procedures proactive – security policies and procedures reactive - loss mitigation through recovery reactive - loss mitigation through recovery

and planning and planning – Can the causation be identified?Can the causation be identified?

1818

Sources of AggregationSources of Aggregation

Service providersService providers– Critical infrastructure - energy, financial Critical infrastructure - energy, financial

and telecommunications on a global basis and telecommunications on a global basis

Third party data storage facilities Third party data storage facilities Vulnerable softwareVulnerable software

1919

Loss Mitigation - Service Loss Mitigation - Service ProvidersProviders

Known and managed exposure Known and managed exposure Networks are well engineered, scalable Networks are well engineered, scalable

and time tested and time tested Carriers frequently respond to natural Carriers frequently respond to natural

disasters disasters Extensive inter-provider support Extensive inter-provider support Proven practices and proceduresProven practices and procedures

2020

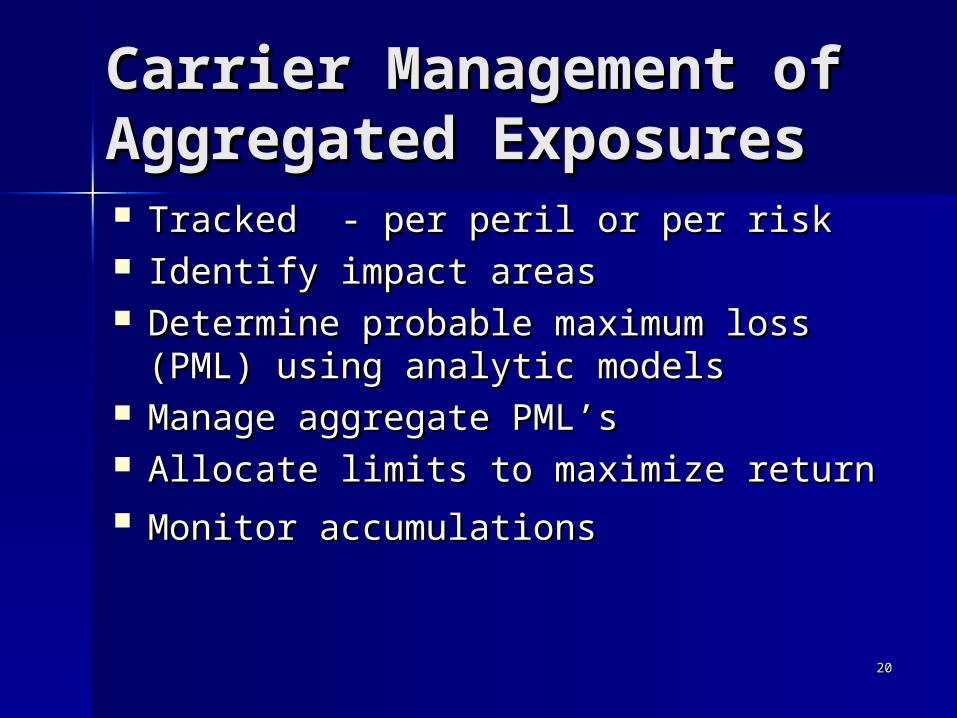

Carrier Management of Carrier Management of Aggregated ExposuresAggregated Exposures Tracked - per peril or per risk Tracked - per peril or per risk Identify impact areas Identify impact areas Determine probable maximum loss Determine probable maximum loss

(PML) using analytic models (PML) using analytic models Manage aggregate PML’s Manage aggregate PML’s Allocate limits to maximize return Allocate limits to maximize return Monitor accumulationsMonitor accumulations

2121

Loss Mitigation - Remote Loss Mitigation - Remote StorageStorage

Single entity/location exposure - Single entity/location exposure - impacting multiple customers impacting multiple customers

Inside/outside exposure assessment Inside/outside exposure assessment – physical, contractual, DRP and continuityphysical, contractual, DRP and continuity

Accumulated limits – direct and Accumulated limits – direct and contingent contingent

2222

ReinsuranceReinsurance

Availability Availability Capacity Capacity Cost - near term and long termCost - near term and long term Partnership - can the understanding of risk Partnership - can the understanding of risk

expand? expand? Scope of protection Scope of protection Terms Terms

Robert W. Hammesfahr, Esq.Robert W. Hammesfahr, Esq.Cozen O’ConnorCozen O’Connor222 South Riverside Plaza, Suite 1500222 South Riverside Plaza, Suite 1500Chicago, IL 60606Chicago, IL [email protected]@cozen.com

PLUS - 16th Annual PLUS - 16th Annual International International ConferenceConference

24

Burch/Cheswick map of the Internet showing the major ISPsData collected June 28, 1999http://www.cheswick.com/map/index.htmlcopyright © 1999 - Lucent Technologies

2525

Network, software and infrastructure failure Media and content liabilities Privacy Virus, malware, hacking, and cyber extortion

Most Common Types of Third Party Losses

2626

New Coverage v. Traditional Coverage Economic loss v. physical damage Intangible property/data IP v. protection of

physical property Statutory causes of action Copyright and trademark liability Privacy and identity theft

2727

Cyber Damage Litigation:Experience and Emerging Issues

Claims exist– Denial of service and virus cases– Theft of intellectual property and hacking– Cookie litigation– Privacy litigation

Claims are expensive to defend The law is new and uncertain

2828

Key Decisions

Liability– Doubleclick/Cybersource– Intel– Database damage cases

Coverage– AOL v. St. Paul

November 11, 2003

Cyber Hurricane

The Current State Of PlayThe Current State Of Play

Harrison OellrichHarrison Oellrich Managing DirectorManaging Director

Guy Carpenter & Co., Inc.Guy Carpenter & Co., Inc.

The Potential for Aggregated Internet Losses & the Insurance Industry

30

Quick Emergence of Cyber Exposures

Sophisticated exposures

Create insurer/reinsurer concerns

– Never contemplated

– Cannot be underwritten within context of traditional policies

Not sufficiently able to

– Quantify

– Underwrite

– Price

31

Result

Dramatically curtailed coverage, if any under traditional policies

Development of specific stand alone policies

32

Stand Alone Policies

Allow underwriters to:

– Assess

– Underwrite

– Price

each insureds unique internet exposure

Current Total Limits:

– $250M market wide

– However rarely if ever more than $100M available per insured

33

Challenge

Need data to model

– Mine

– Massage

– Methodology

Sophisticated models now used for physical perils

Cyber perils seemingly subvert ability to model

34

Cyber Hurricane (Aggregation)

Need method to slice and dice a la traditional property cat perils

Otherwise must aggregate every dollar written against every other dollar of exposure

Initial attempts to do so successful

Thinking validated by WW property cat leaders/marketplace

35

Need for Data/Modeling Capability

Loss data plentiful for “bricks and mortar” cat perils

Virtually non-existent for emerging cyber perils

– past attacks unreported

– Reputational risk

Credible data +modeling techniques =

a substantive/sustainable marketplace

36

Government Involvement/ Why us?

Multiple collaborative initiatives

Internet deemed a critical component of nation’s infrastructure

It must therefore be protected at all costs

Disciplines insurers/reinsurers can provide are same as government wishes to impose if it were able

If successful; network environment hardened

National security enhanced!!

37

Irrational Exuberance?

Forrester Research predicts Business to Business E-Commerce: $1.3Trillion by 2005

– Insurance Information Institute: this will result in $2.5B of premium by 2006

– Conning & Co.: $5B of premium likely during same period

Even if overstated all must agree that opportunities are real/significant

38

A Future Vision

Every business will have a presence on the internet

Potential for Cyber Risk Insurance to be the next major growth area of our industry

– Buildings of the 21st Century

Opportunities will arise/evolve swiftly

Creating exposures never contemplated

– Industry must be creative to fully capitalize on this opportunity

3939

Cyber Hurricane

The Potential for Aggregated Internet Losses and the Insurance Industry

Professional Liability Underwriting Society

16th Annual Conference

Philadelphia, PA