1 DEALING WITH ASSETS DEALING WITH ASSETS Fixed assets appear in the Balance Sheet Fixed assets appear in the Balance Sheet Cost to the organization is the total cost of Cost to the organization is the total cost of acquisition acquisition Purchase price Purchase price Cost of installation Cost of installation Cost of transportation to organization Cost of transportation to organization Assets decrease in value as time progresses, Assets decrease in value as time progresses, i.e. Assets depreciate with time i.e. Assets depreciate with time Possible exceptions - land, property, collectable Possible exceptions - land, property, collectable items items Classifications of depreciation: Classifications of depreciation: Physical Physical Functional Functional

Transcript

1

DEALING WITH ASSETSDEALING WITH ASSETS

Fixed assets appear in the Balance SheetFixed assets appear in the Balance Sheet Cost to the organization is the total cost of acquisitionCost to the organization is the total cost of acquisition

Purchase pricePurchase price Cost of installationCost of installation Cost of transportation to organizationCost of transportation to organization

Assets decrease in value as time progresses, Assets decrease in value as time progresses, i.e. Assets depreciate with timei.e. Assets depreciate with time Possible exceptions - land, property, collectable itemsPossible exceptions - land, property, collectable items

Classifications of depreciation:Classifications of depreciation: PhysicalPhysical FunctionalFunctional

2

PHYSICAL DEPRECIATIONPHYSICAL DEPRECIATION

Depreciation resulting from physical impairment of the assetDepreciation resulting from physical impairment of the asset Example: corrosion of tubes in a heat exchangerExample: corrosion of tubes in a heat exchanger

This type of depreciation results in the lowering of the This type of depreciation results in the lowering of the ability of a physical asset to perform its intended purposeability of a physical asset to perform its intended purpose

Primary causes:Primary causes: Deterioration due to action of the elements including the Deterioration due to action of the elements including the

corrosion of pipes, rotting of timber, chemical corrosion of pipes, rotting of timber, chemical decomposition, bacterial action. Deterioration is decomposition, bacterial action. Deterioration is substantially independent of use.substantially independent of use.

Wear and tear from use that subjects the asset to Wear and tear from use that subjects the asset to abrasion, shock, vibration, impact, etc. These forces abrasion, shock, vibration, impact, etc. These forces primarily result from use and result in a loss of value primarily result from use and result in a loss of value over time.over time.

3

FUNCTIONAL DEPRECIATIONFUNCTIONAL DEPRECIATION

Depreciation resulting from changes in the demand for the Depreciation resulting from changes in the demand for the services it is designed to provideservices it is designed to provide

Demand change can result from it being a more profitable Demand change can result from it being a more profitable tool for the manufacture of a part, the more efficient tool for the manufacture of a part, the more efficient achievement of a task or provision of a specific service. Can achievement of a task or provision of a specific service. Can also result when the asset is used in excess of its designed also result when the asset is used in excess of its designed capacitycapacity

Primary causes:Primary causes: Obsolescence of another assetObsolescence of another asset Inadequacy or inability to meet demand placed upon the Inadequacy or inability to meet demand placed upon the

asset due to revised product demandasset due to revised product demand

Examples of functional obsolescence include steam trains, Examples of functional obsolescence include steam trains, sailing ship (other than for pleasure), horse drawn carriagessailing ship (other than for pleasure), horse drawn carriages

4

SUMMARYSUMMARY

Depreciation:Depreciation:

““... the measure of the wearing out, consumption or other ... the measure of the wearing out, consumption or other reduction in the useful economic life of a fixed asset reduction in the useful economic life of a fixed asset whether arising from use, passage of time or obsolescence whether arising from use, passage of time or obsolescence through technology or market changes”through technology or market changes”

Fact based:Fact based: Original total cost of acquisition of the assetOriginal total cost of acquisition of the asset Ownership strategy – expected lifeOwnership strategy – expected life

5

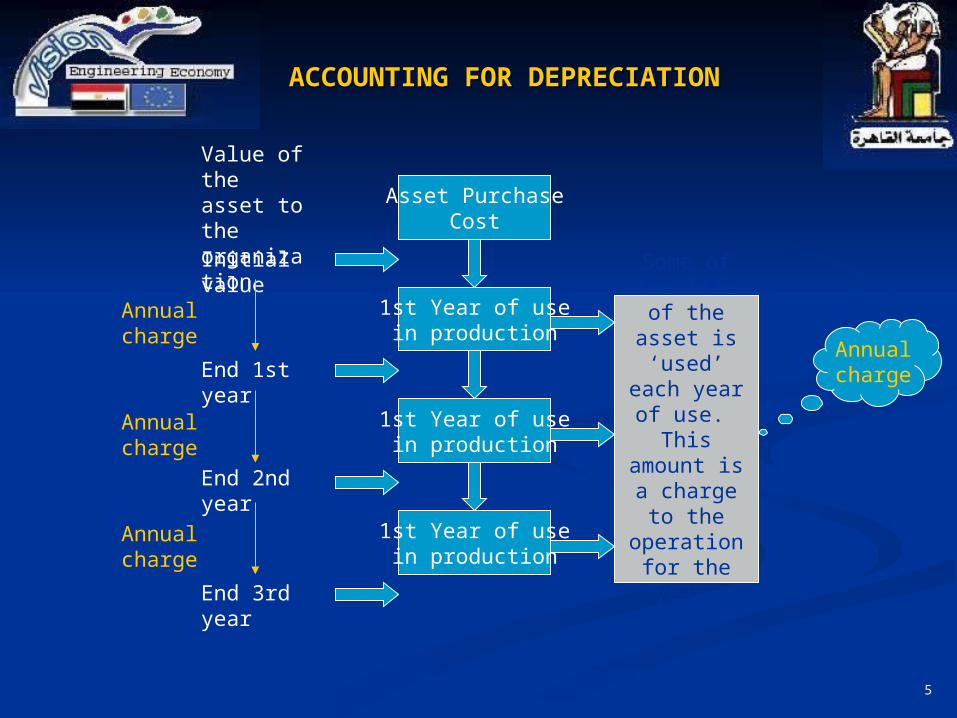

ACCOUNTING FOR ACCOUNTING FOR DEPRECIATIONDEPRECIATION

Asset PurchaseCost

1st Year of usein production

1st Year of usein production

1st Year of usein production

Some of the life of the

asset is ‘used’ each year of

use. This amount is a

charge to the operation for

the year

Value of the asset to the organization

Initial value

End 1st year

End 2nd year

End 3rd year

Annualcharge

Annual charge

Annual charge

Annual charge

6

DEPRECIATIONDEPRECIATION

Depreciation is the annual amount by which an asset is Depreciation is the annual amount by which an asset is reduced in ‘book value’ within the organisationreduced in ‘book value’ within the organisation

This annual depreciation is also the annual amount This annual depreciation is also the annual amount charged to the profit and loss statement in recognition of charged to the profit and loss statement in recognition of the use of the asset for the purposes of producing the use of the asset for the purposes of producing somethingsomething

Note the notion of a balance hereNote the notion of a balance here

we need this to ensure the balance sheet balances!we need this to ensure the balance sheet balances!

‘‘Book Value’ is the acquisition cost of an asset less its Book Value’ is the acquisition cost of an asset less its accumulated depreciation charges.accumulated depreciation charges.

How do we decide the annual charge?How do we decide the annual charge?

Modern methodsModern methods Accelerated Cost Recovery System (ACRS)Accelerated Cost Recovery System (ACRS) Modified Accelerated Cost Recovery System (MACRS)Modified Accelerated Cost Recovery System (MACRS)

8

STRAIGHT LINE DEPRECIATIONSTRAIGHT LINE DEPRECIATION

Characterized by a constant annual depreciation amountCharacterized by a constant annual depreciation amount

Where:Where: A = annual chargeA = annual charge C = total acquisition costC = total acquisition cost n = useful life of the asset in yearsn = useful life of the asset in years

Simple method, requires definition of ‘n’Simple method, requires definition of ‘n’

€

A =C − R( )n

9

STRAIGHT LINE - EXAMPLESTRAIGHT LINE - EXAMPLE

A high specification compressor is purchased for 100,000 A high specification compressor is purchased for 100,000 m.u.m.u.

It is expected to have a usable life of 5 years after which it It is expected to have a usable life of 5 years after which it will have a residual value of 10,000 m.u.will have a residual value of 10,000 m.u.

The compressor is used to make balloons. Each balloon The compressor is used to make balloons. Each balloon costs 1.00 m.u. and sells for 2 m.u. costs 1.00 m.u. and sells for 2 m.u.

25,000 balloons are sold each year25,000 balloons are sold each year

1.1. Calculate the annual depreciation chargeCalculate the annual depreciation charge

2.2. Show how the asset book value changes over timeShow how the asset book value changes over time

3.3. Show how the depreciation charge affects reported profitShow how the depreciation charge affects reported profit

10

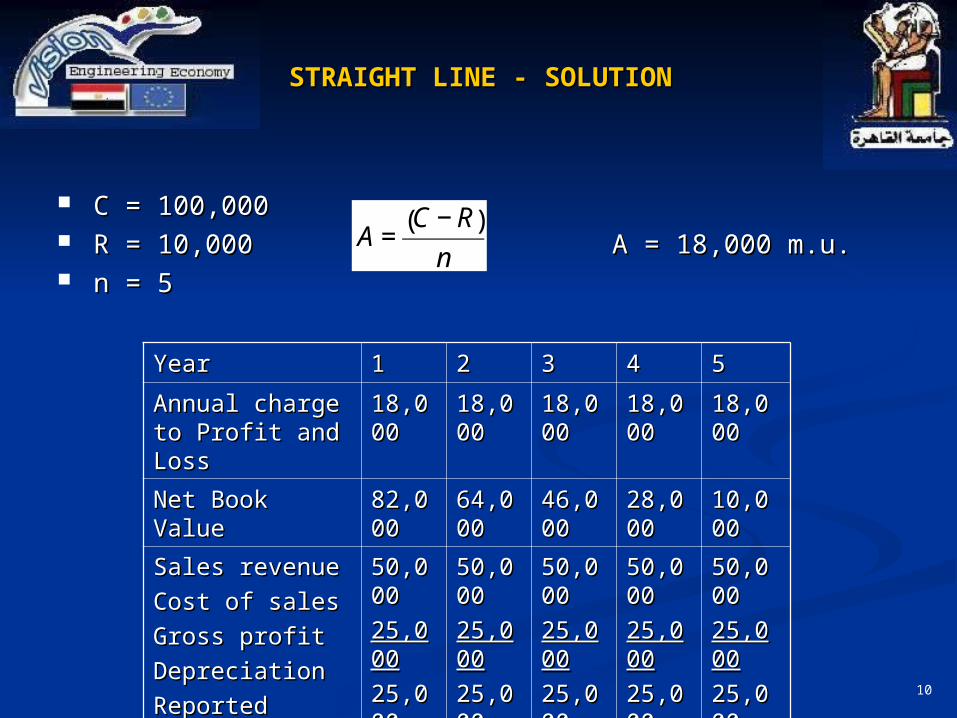

STRAIGHT LINE - SOLUTIONSTRAIGHT LINE - SOLUTION

C = 100,000C = 100,000 R = 10,000R = 10,000 A = 18,000 m.u.A = 18,000 m.u. n = 5n = 5

€

A =C − R( )n

YearYear 11 22 33 44 55

Annual charge Annual charge to Profit and to Profit and LossLoss

18,018,00000

18,018,00000

18,018,00000

18,018,00000

18,0018,0000

Net Book ValueNet Book Value 82,082,00000

64,064,00000

46,046,00000

28,028,00000

10,0010,0000

Sales revenueSales revenue

Cost of salesCost of sales

Gross profitGross profit

DepreciationDepreciation

Reported profitReported profit

50,050,00000

25,025,00000

25,025,00000

18,018,00000

7,007,0000

50,050,00000

25,025,00000

25,025,00000

18,018,00000

7,007,0000

50,050,00000

25,025,00000

25,025,00000

18,018,00000

7,007,0000

50,050,00000

25,025,00000

25,025,00000

18,018,00000

7,007,0000

50,0050,0000

25,0025,0000

25,0025,0000

18,0018,0000

7,0007,000

11

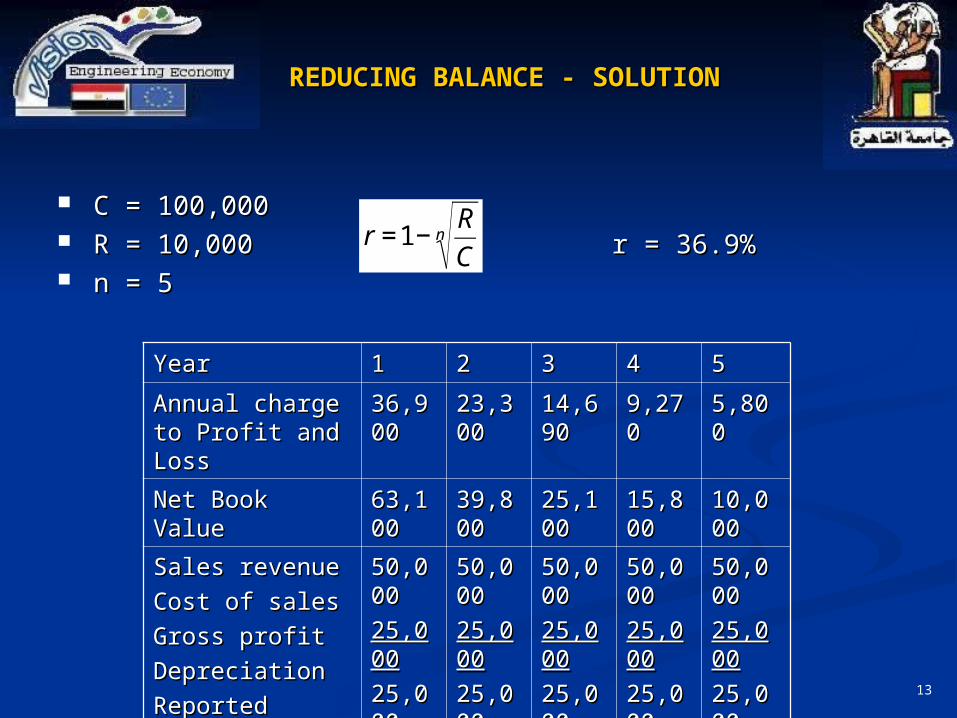

REDUCING BALANCE METHODREDUCING BALANCE METHOD

Characterized by a constant annual percentage reduction Characterized by a constant annual percentage reduction in asset valuein asset value

Where:Where: r = depreciation rater = depreciation rate C = total acquisition costC = total acquisition cost R = residual value of the assetR = residual value of the asset n = useful life of the asset in yearsn = useful life of the asset in years

€

r =1−R

Cn

12

REDUCING BALANCE - EXAMPLEREDUCING BALANCE - EXAMPLE

A high specification compressor is purchased for 100,000 A high specification compressor is purchased for 100,000 m.u.m.u.

It is expected to have a usable life of 5 years after which it It is expected to have a usable life of 5 years after which it will have a residual value of 10,000 m.u.will have a residual value of 10,000 m.u.

The compressor is used to make balloons. Each balloon The compressor is used to make balloons. Each balloon costs 1.00 m.u. and sells for 2 m.u. costs 1.00 m.u. and sells for 2 m.u.

25,000 balloons are sold each year25,000 balloons are sold each year

1.1. Calculate the annual depreciation chargeCalculate the annual depreciation charge

2.2. Show how the asset book value changes over timeShow how the asset book value changes over time

3.3. Show how the depreciation charge affects reported profitShow how the depreciation charge affects reported profit

3.3. Apply declining-balance depreciation (which switches to Apply declining-balance depreciation (which switches to straight line depreciation (see table)straight line depreciation (see table)

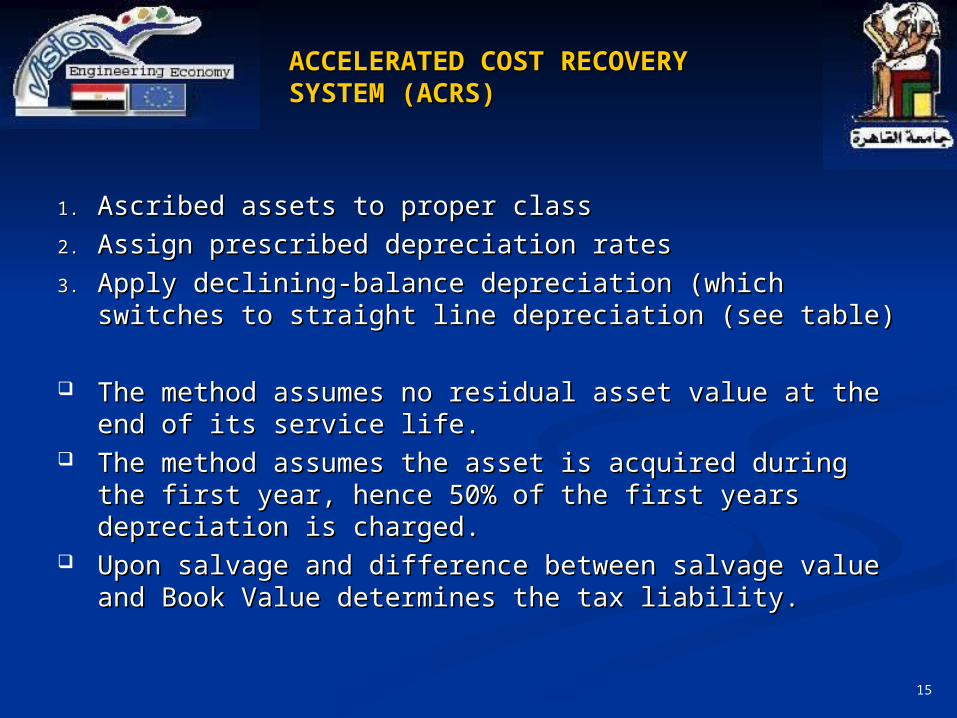

The method assumes no residual asset value at the end of The method assumes no residual asset value at the end of its service life.its service life.

The method assumes the asset is acquired during the first The method assumes the asset is acquired during the first year, hence 50% of the first years depreciation is charged.year, hence 50% of the first years depreciation is charged.

Upon salvage and difference between salvage value and Upon salvage and difference between salvage value and Book Value determines the tax liability.Book Value determines the tax liability.

16

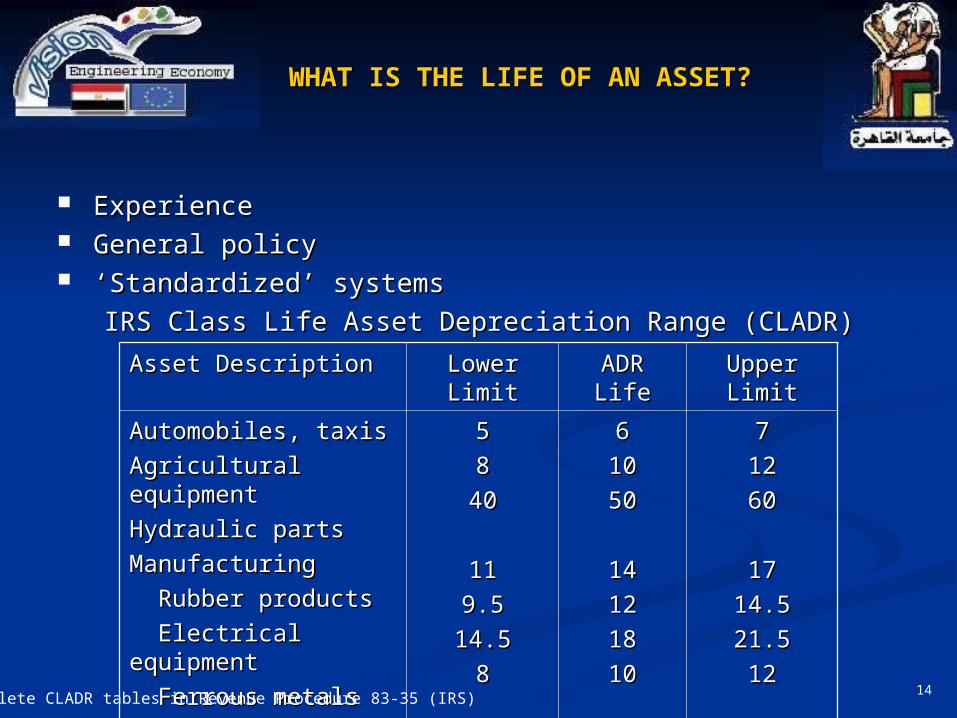

ACCELERATED COST RECOVERY ACCELERATED COST RECOVERY SYSTEM (ACRS)SYSTEM (ACRS)

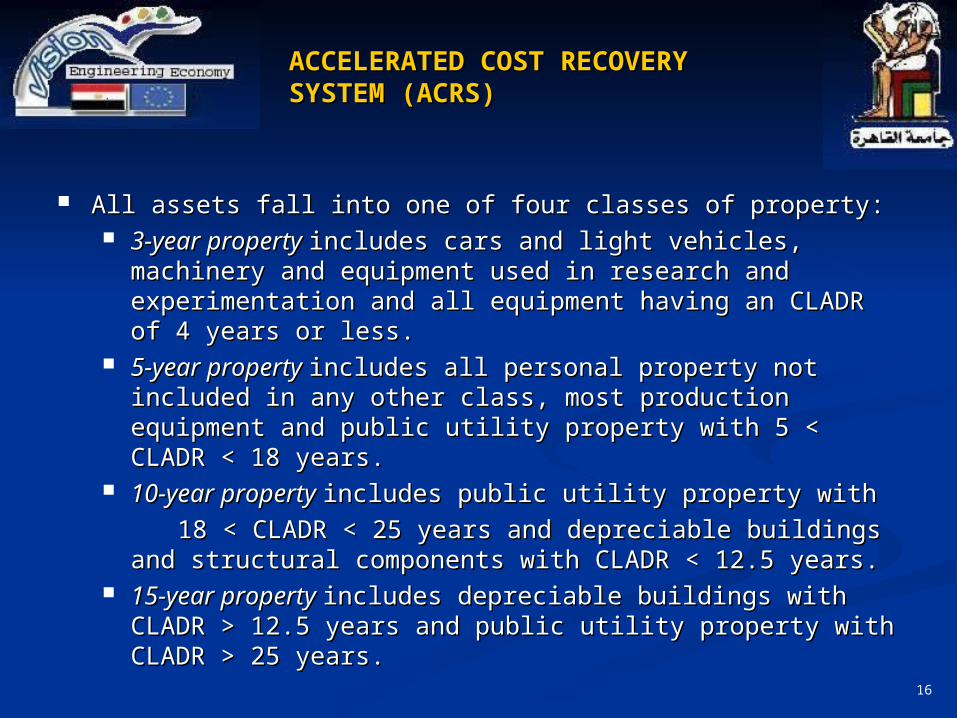

All assets fall into one of four classes of property:All assets fall into one of four classes of property: 3-year property 3-year property includes cars and light vehicles, includes cars and light vehicles,

machinery and equipment used in research and machinery and equipment used in research and experimentation and all equipment having an CLADR of experimentation and all equipment having an CLADR of 4 years or less.4 years or less.

5-year property 5-year property includes all personal property not includes all personal property not included in any other class, most production equipment included in any other class, most production equipment and public utility property with 5 < CLADR < 18 years.and public utility property with 5 < CLADR < 18 years.

10-year property 10-year property includes public utility property with includes public utility property with

18 < CLADR < 25 years and depreciable buildings and 18 < CLADR < 25 years and depreciable buildings and structural components with CLADR < 12.5 years.structural components with CLADR < 12.5 years.

15-year property 15-year property includes depreciable buildings with includes depreciable buildings with CLADR > 12.5 years and public utility property with CLADR > 12.5 years and public utility property with CLADR > 25 years.CLADR > 25 years.

17

ACCELERATED COST RECOVERY ACCELERATED COST RECOVERY SYSTEM (ACRS)SYSTEM (ACRS)

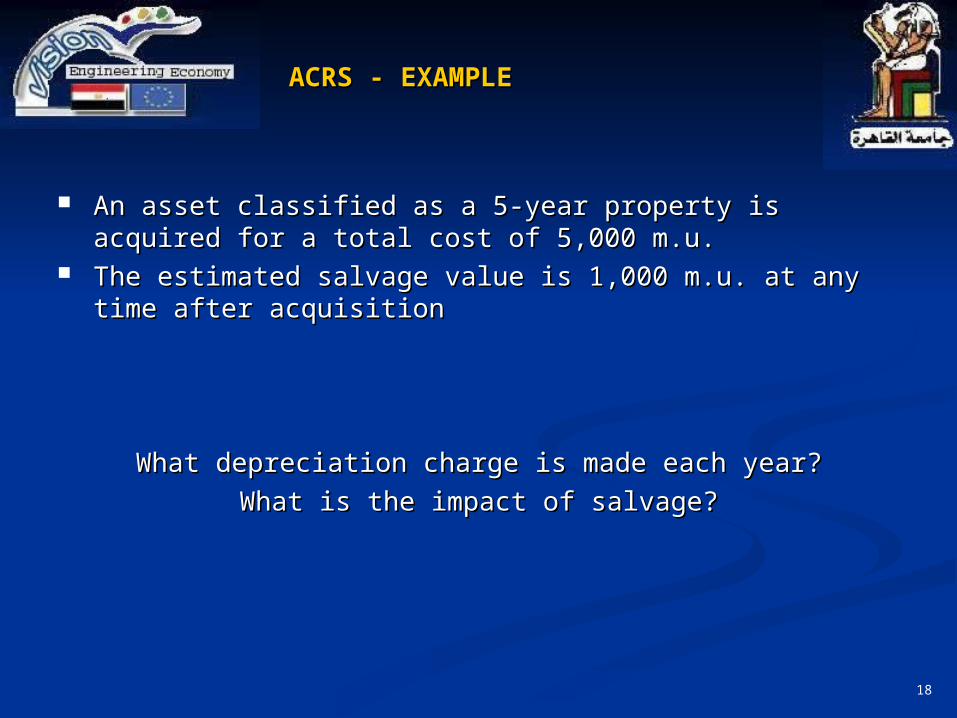

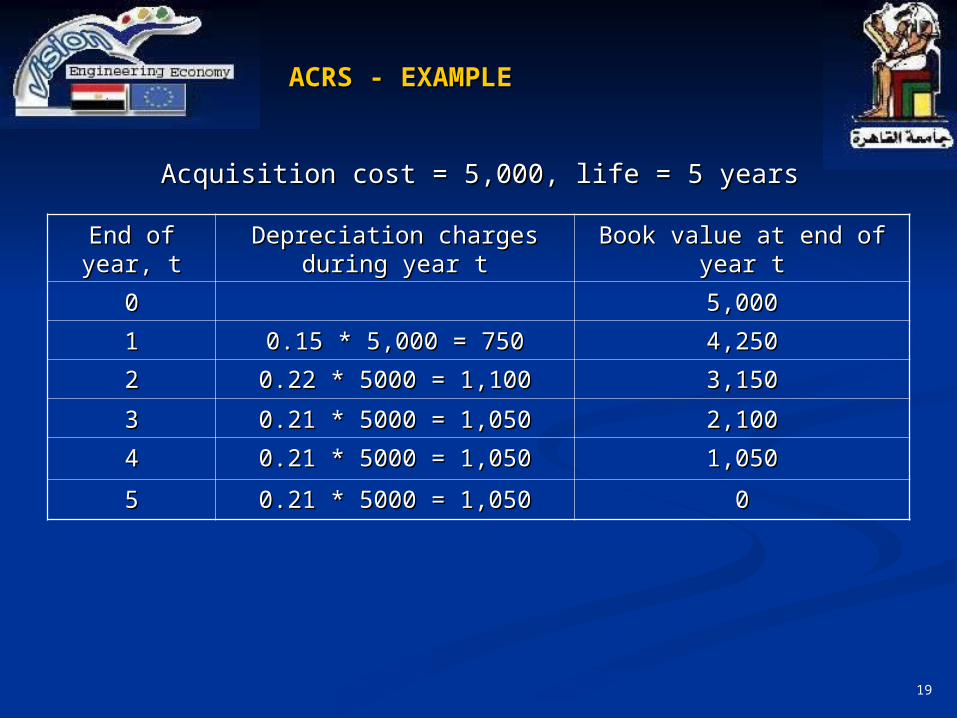

An asset classified as a 5-year property is acquired for a An asset classified as a 5-year property is acquired for a total cost of 5,000 m.u.total cost of 5,000 m.u.

The estimated salvage value is 1,000 m.u. at any time after The estimated salvage value is 1,000 m.u. at any time after acquisitionacquisition

What depreciation charge is made each year?What depreciation charge is made each year?

What is the impact of salvage?What is the impact of salvage?

19

ACRS - EXAMPLEACRS - EXAMPLE

End of year, End of year, tt

Depreciation charges Depreciation charges during year tduring year t

Book value at end of year Book value at end of year tt

Acquisition cost = 5,000, life = 5 years, Salvage value = 1,000Acquisition cost = 5,000, life = 5 years, Salvage value = 1,000

If asset sold before fully depreciated no depreciation can be If asset sold before fully depreciated no depreciation can be charged in the year of salvage.charged in the year of salvage.

Consider salvage in year 3Consider salvage in year 3

21

ACRS - EXAMPLEACRS - EXAMPLE

End of year, End of year, tt

Depreciation charges Depreciation charges during year tduring year t

Book value at end of year Book value at end of year tt

33 Asset sold during this yearAsset sold during this year

44

55

Acquisition cost = 5,000, life = 5 years, Salvage value = 1,000Acquisition cost = 5,000, life = 5 years, Salvage value = 1,000

Consider salvage in year 3Consider salvage in year 3Book value at time of disposal = 3,150. Salvage value = 1,000. Book value at time of disposal = 3,150. Salvage value = 1,000. Write-off to Profit and Loss Account = 3,150 - 1,000 = 2,150 Write-off to Profit and Loss Account = 3,150 - 1,000 = 2,150 m.u.m.u.

22

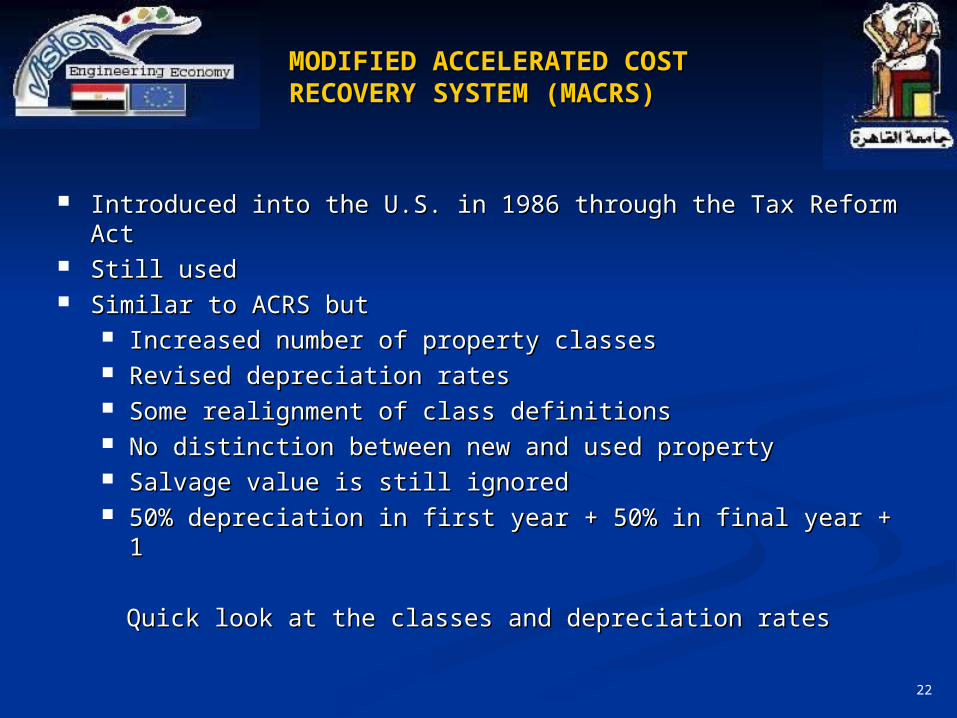

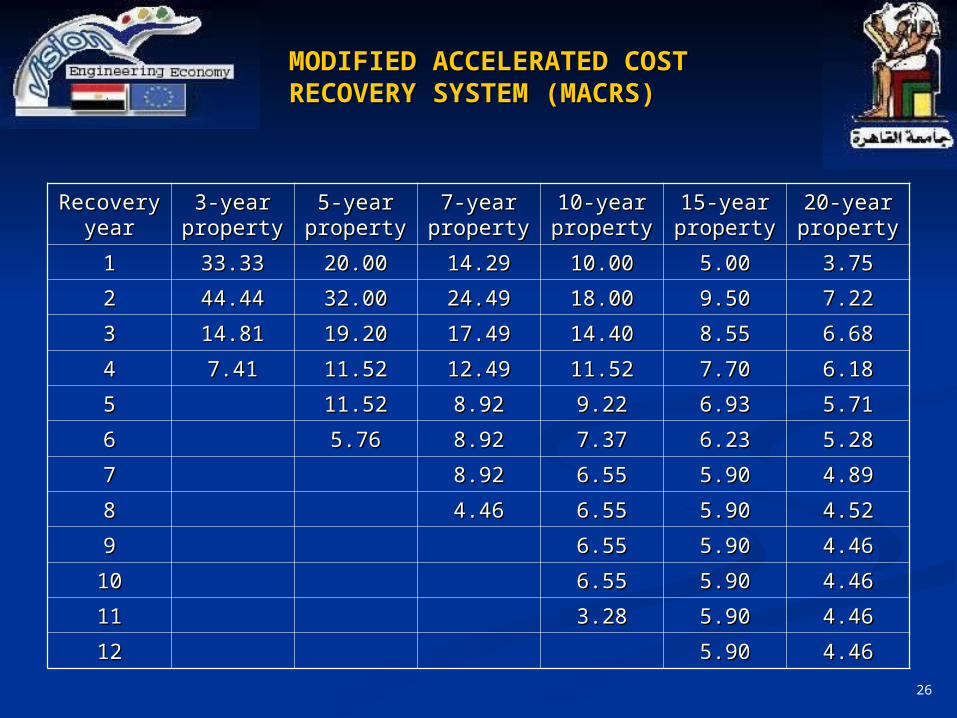

MODIFIED ACCELERATED COST MODIFIED ACCELERATED COST RECOVERY SYSTEM (MACRS)RECOVERY SYSTEM (MACRS)

Introduced into the U.S. in 1986 through the Tax Reform Introduced into the U.S. in 1986 through the Tax Reform ActAct

Still usedStill used Similar to ACRS butSimilar to ACRS but

Increased number of property classesIncreased number of property classes Revised depreciation ratesRevised depreciation rates Some realignment of class definitionsSome realignment of class definitions No distinction between new and used propertyNo distinction between new and used property Salvage value is still ignoredSalvage value is still ignored 50% depreciation in first year + 50% in final year + 150% depreciation in first year + 50% in final year + 1

Quick look at the classes and depreciation ratesQuick look at the classes and depreciation rates

23

MODIFIED ACCELERATED COST MODIFIED ACCELERATED COST RECOVERY SYSTEM (MACRS)RECOVERY SYSTEM (MACRS)

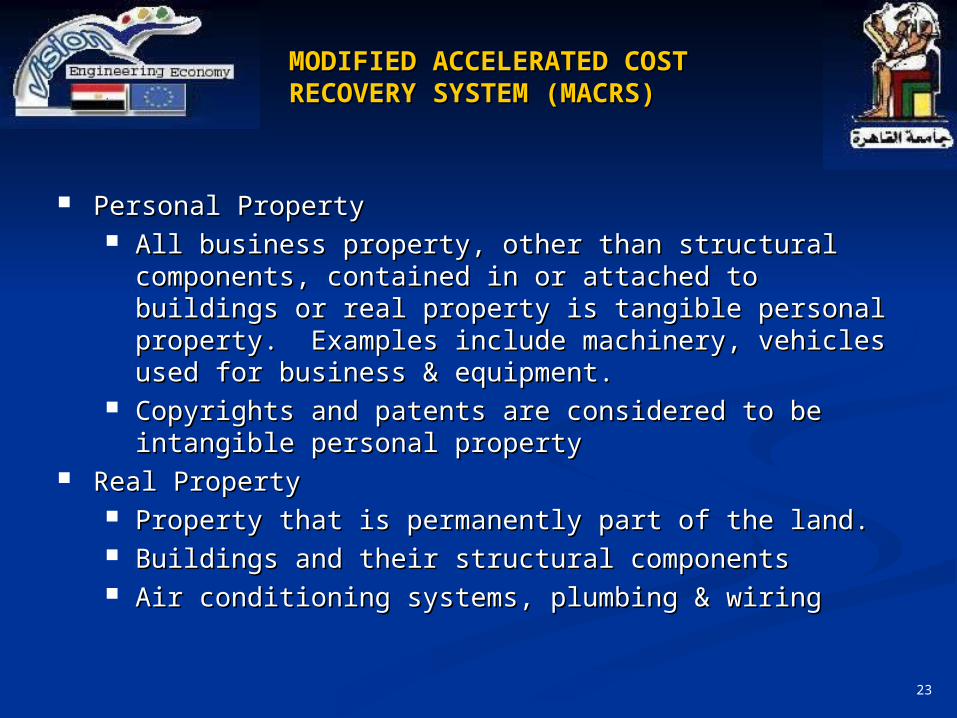

Personal PropertyPersonal Property All business property, other than structural All business property, other than structural

components, contained in or attached to buildings or components, contained in or attached to buildings or real property is tangible personal property. Examples real property is tangible personal property. Examples include machinery, vehicles used for business & include machinery, vehicles used for business & equipment.equipment.

Copyrights and patents are considered to be intangible Copyrights and patents are considered to be intangible personal propertypersonal property

Real PropertyReal Property Property that is permanently part of the land.Property that is permanently part of the land. Buildings and their structural componentsBuildings and their structural components Air conditioning systems, plumbing & wiringAir conditioning systems, plumbing & wiring

24

MODIFIED ACCELERATED COST MODIFIED ACCELERATED COST RECOVERY SYSTEM (MACRS)RECOVERY SYSTEM (MACRS)

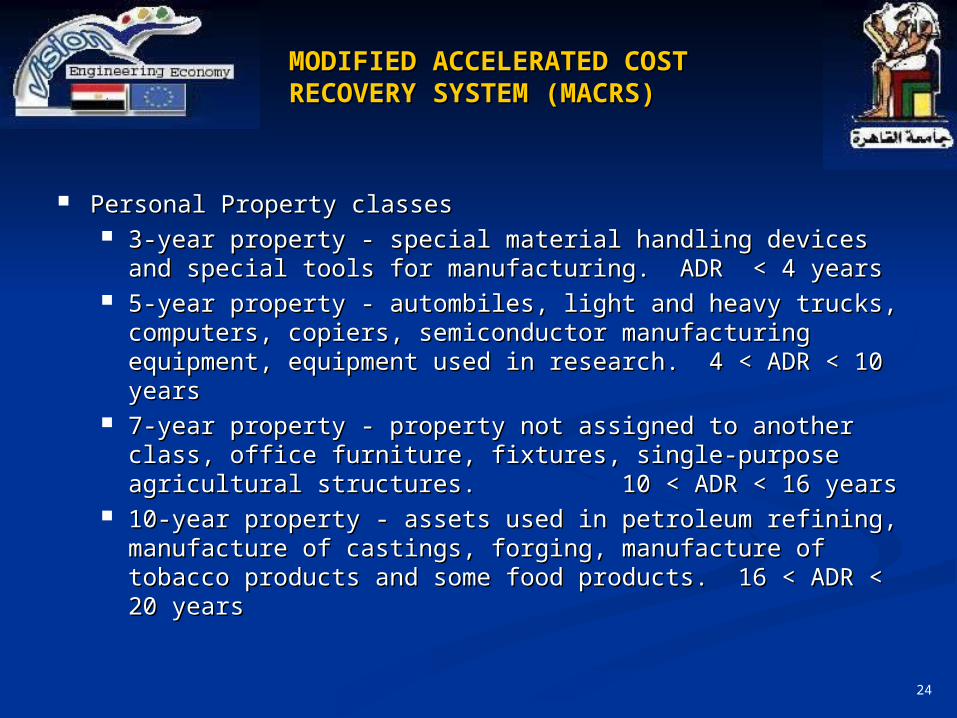

Personal Property classesPersonal Property classes 3-year property - special material handling devices and 3-year property - special material handling devices and

special tools for manufacturing. ADR < 4 yearsspecial tools for manufacturing. ADR < 4 years 5-year property - autombiles, light and heavy trucks, 5-year property - autombiles, light and heavy trucks,

computers, copiers, semiconductor manufacturing computers, copiers, semiconductor manufacturing equipment, equipment used in research. 4 < ADR < 10 equipment, equipment used in research. 4 < ADR < 10 yearsyears

7-year property - property not assigned to another class, 7-year property - property not assigned to another class, office furniture, fixtures, single-purpose agricultural office furniture, fixtures, single-purpose agricultural structures. 10 < ADR < 16 yearsstructures. 10 < ADR < 16 years

10-year property - assets used in petroleum refining, 10-year property - assets used in petroleum refining, manufacture of castings, forging, manufacture of tobacco manufacture of castings, forging, manufacture of tobacco products and some food products. 16 < ADR < 20 yearsproducts and some food products. 16 < ADR < 20 years

25

MODIFIED ACCELERATED COST MODIFIED ACCELERATED COST RECOVERY SYSTEM (MACRS)RECOVERY SYSTEM (MACRS)

Personal Property classesPersonal Property classes 15-year property - telephone distribution equipment, 15-year property - telephone distribution equipment,

municipal water and sewerage treatment plants. 20 < ADR municipal water and sewerage treatment plants. 20 < ADR < 25 years< 25 years

20-year property - vessels, barges and tugs and municipal 20-year property - vessels, barges and tugs and municipal sewers. 25 years < ADRsewers. 25 years < ADR

Real Property classesReal Property classes Residential property - includes apartment buildings and Residential property - includes apartment buildings and

rental houses. rental houses. [Straight line depreciation 27.5 years with [Straight line depreciation 27.5 years with half-year conventionhalf-year convention11]]

Nonresidential property - office buildings, warehouses, Nonresidential property - office buildings, warehouses, manufacturing facilities, refineries, mills, parking facilities, manufacturing facilities, refineries, mills, parking facilities, fences and roads. fences and roads. [Straight line depreciation 31.5 years [Straight line depreciation 31.5 years with half-year conventionwith half-year convention11]]

1 1 Half-year’s depreciation in year of purchase & year of Half-year’s depreciation in year of purchase & year of disposal disposal

26

MODIFIED ACCELERATED COST MODIFIED ACCELERATED COST RECOVERY SYSTEM (MACRS)RECOVERY SYSTEM (MACRS)