25

1 Get a Handle on Your Money

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | lindsey-shepherd |

| View: | 214 times |

| Download: | 1 times |

1

Get a Handle on

Your Money

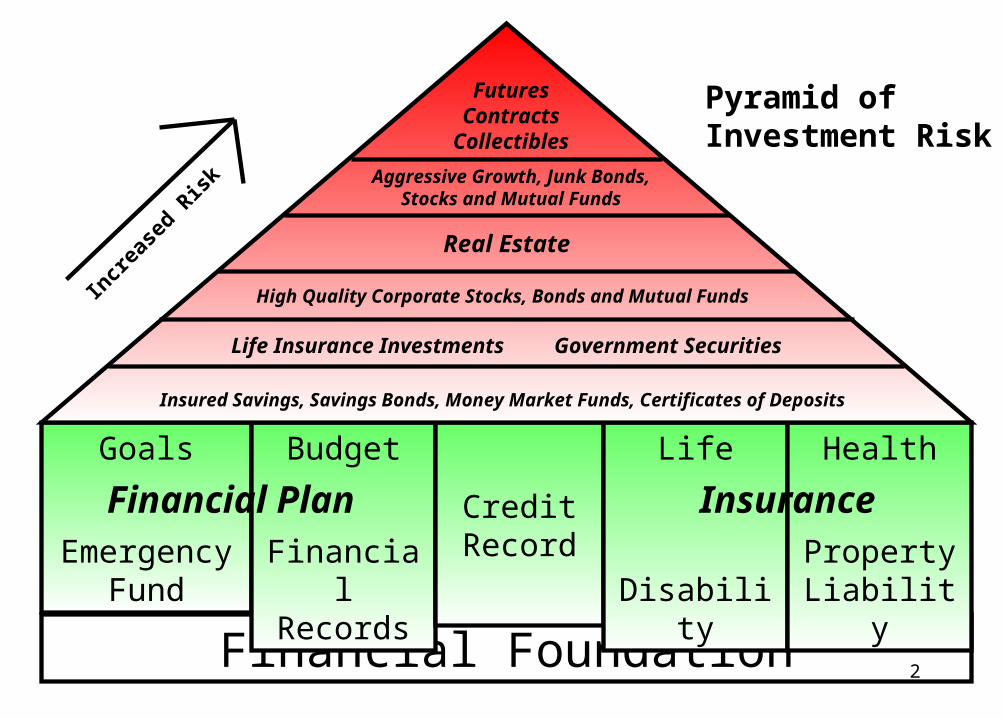

2Financial Foundation

Goals

Emergency Fund

Budget

Financial Records

Credit Record

Life

Disability

Health

Property Liability

Financial Plan Insurance

Insured Savings, Savings Bonds, Money Market Funds, Certificates of Deposits

Life Insurance Investments Government Securities

High Quality Corporate Stocks, Bonds and Mutual Funds

Real Estate

Aggressive Growth, Junk Bonds, Stocks and Mutual

Funds

Futures Contracts Collectible

s

Pyramid of Investment Risk

Incr

ease

d Ris

k

3

Cash Management

$ Earn maximum interest on funds

$ Maintain adequate funds to manage expenses, emergencies and financial goals

$ Keep cash and credit purchases in line with budget limits

$ Maintain purchasing power by exceeding inflation and taxes

4

Tools of Cash Management

$ Checking accounts

$ Savings accounts

$ Money Market accounts

$ Certificates of deposit and government savings bonds

5

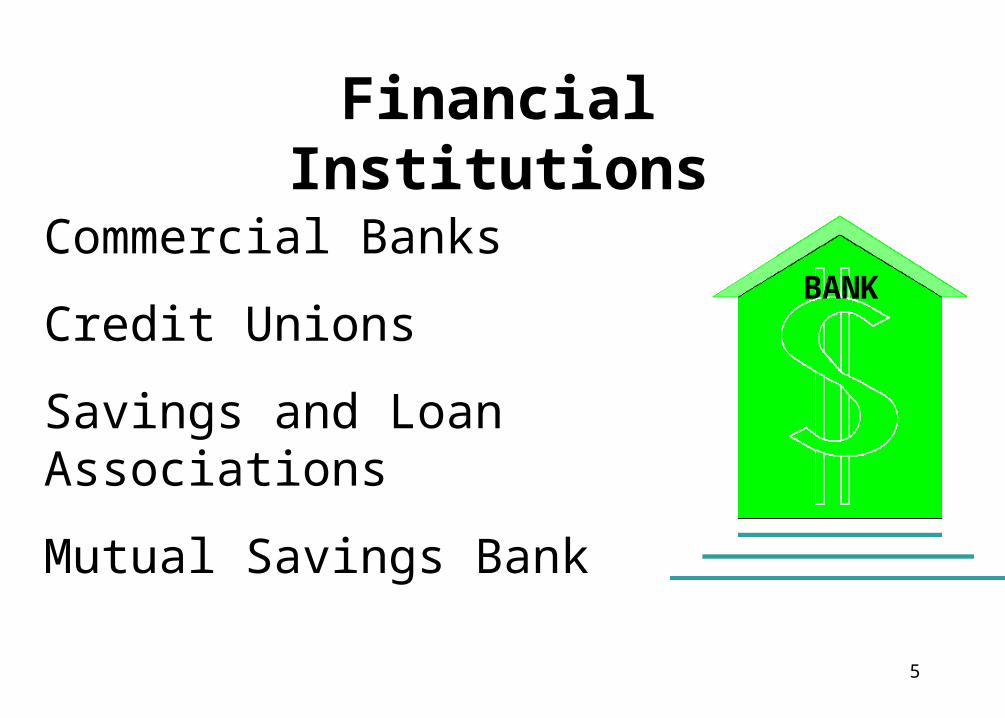

Financial Institutions

Commercial Banks

Credit Unions

Savings and Loan Associations

Mutual Savings Bank

BANK

6

Checking and Savings Accounts Costs and

PenaltiesAutomated teller machine transaction fee

Telephone, computer or teller information

Maintenance fee on minimum-balance account

Maintenance fee on average-balance account

7

Costs and Penalties

“Bounced” check

Delayed use of funds

Inactive account

Excessive withdrawals

Early withdrawal

Check clearing waiting period

Stop-payment order

8

Overdraft Protection

Automatic Funds Transfer

Automatic Overdraft Loan Agreement

9

Making Your Money Grow

10

Savings versus Investing --

What’s the difference?

11

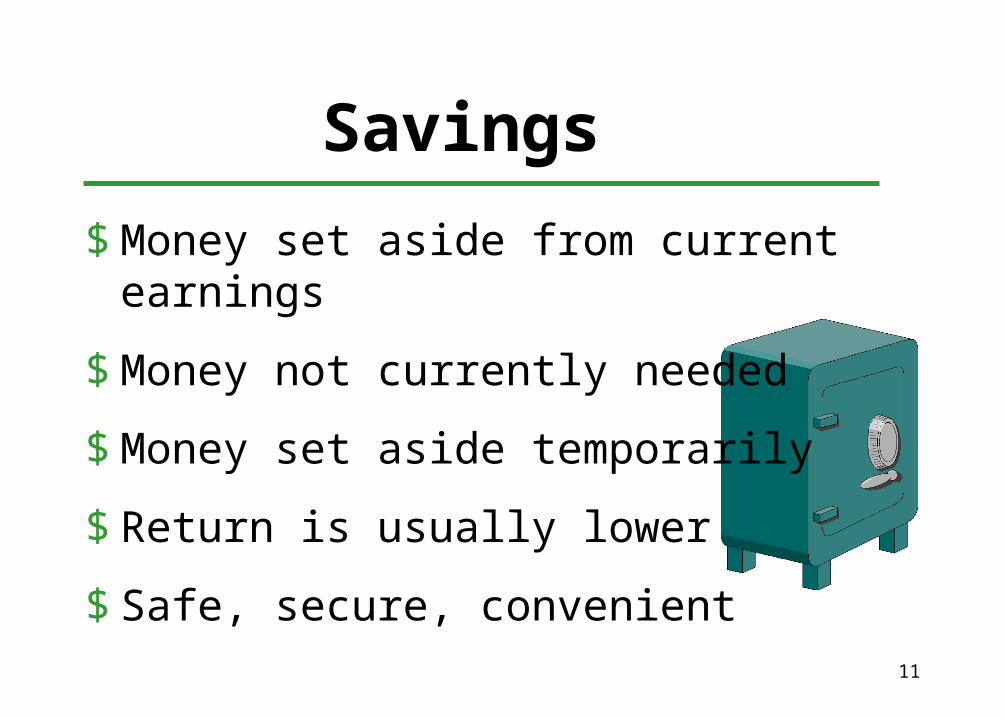

Savings

$ Money set aside from current earnings

$ Money not currently needed

$ Money set aside temporarily

$ Return is usually lower

$ Safe, secure, convenient

12

Investing

Putting what you’ve saved to work to produce a higher return

Money that is set aside to meet longer term goals

Higher risk than savings

13

Reasons Families Save

Emergencies, seasonal expenses, major purchases

Educate self or children

Minimize taxes

Retirement income

Capital accumulationToys

Children’s Education

New Home

Candy

14

Every Little

Bit

Counts

15

Pay Yourself First (A little can add up)

Save this each week At % interest In 10 years, you will have

$ 7.00 5% $ 4,720$14.00 5%

$ 9,440 $21.00 5%$14,160 $28.00 5%

$18,880 $35.00 5%$23,600

16

Savings Options

Savings Accounts

Certificates of Deposit

Money Market Accounts

Government Savings Bonds

Treasury Certificates

17

Low-Risk, Long-Term Savings

$ Certificates of Deposit Fixed or variable

rate

$ U.S. Savings Bonds Series EE Series HH Series I

18

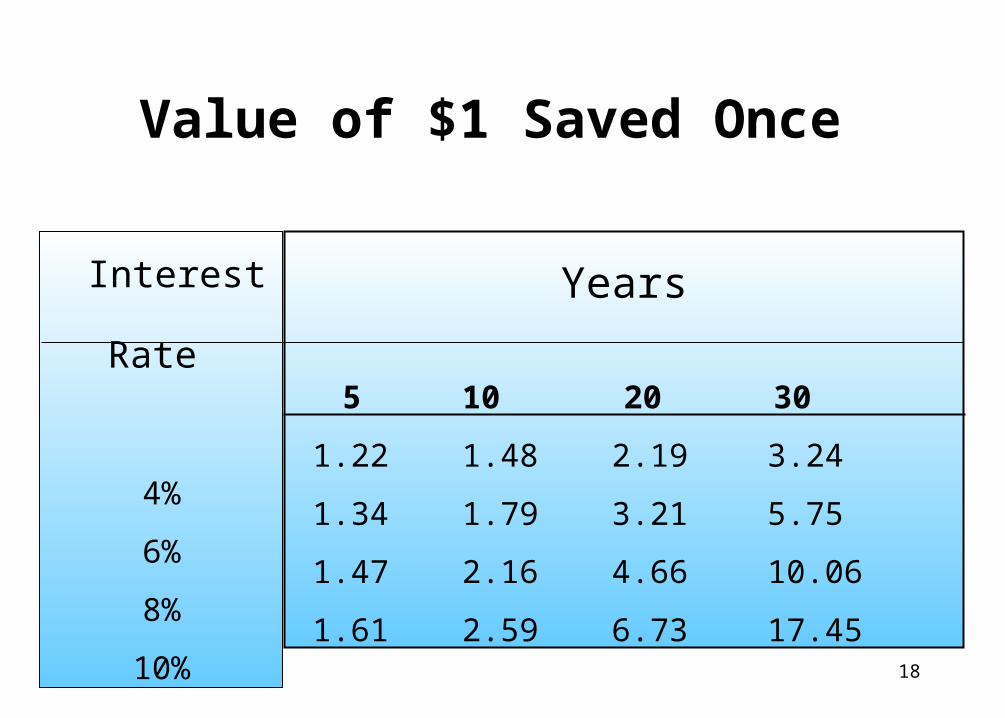

Value of $1 Saved Once

Years

5 10 20 30

1.22 1.48 2.19 3.24

1.34 1.79 3.21 5.75

1.47 2.16 4.66 10.06

1.61 2.59 6.73 17.45

Interest Rate

4%

6%

8%

10%

19

Interest Rate

4%

6%

8%

10%

Years

5 10 20 30

5.42 12.01 29.78 56.08

5.64 13.18 36.79 79.06

5.87 14.49 45.76 113.28

6.11 15.94 57.27 164.49

Value of $1 Saved Yearly

20

Save $1,000 a

year @ 4% for

20 years =

$29,778

You earned $9,778!!!

21

$25 a month or $300 a year @ 4% interest for 20 years = $8,933

You earned

$2,933!!!

22

Finding $1,000 To Save$ 60 clothing/dry cleaning 60 phone bills 120 groceries 180 entertainment 160 collect coins ($3.20

each week) 360 meals away from

home 60 coffee/sodas

$1,000 SAVINGS

23

Painless Ways To Save

$ Pay yourself first

$ Reinvest interest and dividends

$ Set realistic goals

$ Be yield conscious

$ Keep it simple

$ Keep cash reserves to minimum

$ Use payroll deduction plans

24

Painless Ways To Save

$ Continue to make loan payments into savings after debt has been paid

$ Try a crash savings diet by purchasing only bare necessities

$ Kick a habit and save the money

$ Adjust your tax withholdings and save the difference

$ Save windfall money from lottery, inheritance and gifts

$ Save money from pay raise, bonus or working overtime

$ Start a part-time job and save the money

25

Get a Handle on

Your Money