16

1 Health Care Reform Your Timeline for Compliance June 2010 © USI Insurance Services LLC 2010. All rights reserved.

| Date post: | 03-Jan-2016 |

| Category: |

Documents |

| Upload: | toby-reynolds |

| View: | 215 times |

| Download: | 1 times |

1

Health Care Reform Your Timeline for Compliance

June 2010

© USI Insurance Services LLC 2010. All rights reserved.

2

Disclosure Statement – Confidentiality

These materials are produced by Kibble & Prentice for the sole use of its clients, prospective clients, and their representatives. Certain information contained in these materials are considered proprietary information created by Kibble & Prentice and/or their licensed and appointed insurance carriers. Such information and any insurance designs furnished by Kibble & Prentice are considered “Confidential Material.” Such information shall not be used in any way, directly or indirectly, detrimental to Kibble & Prentice and clients and/or potential clients and any of their representatives will keep that information confidential.

Neither Kibble & Prentice nor any of its respective representatives or advisors has made or makes any representation or warranty, expressed or implied, as to the accuracy or completeness of the Confidential Material. Neither Kibble & Prentice nor their respective representatives or advisors shall have any liability resulting from the use of the Confidential Material or any errors or omission therein. These materials contain confidential information and provide general information for the use of our clients, potential clients, or that of our clients’ legal and tax advisors. Only a qualified attorney may prepare any document needed to implement any strategy explained in these materials, and the agent/broker or advisor is not in the business of practicing law, legally representing clients, or drafting legal documents.

3

Today’s Agenda

Immediate Considerations On the Horizon Action Planning

4

Key Components

Health Care Reform consists of two pieces of legislation:

Patient Protection and Affordable Care Act, enacted March 23, 2010 (Senate Bill)

Health Care and Education Affordability Reconciliation Act of 2010, enacted on March 30, 2010 (House Companion Legislation)

5

Immediate Considerations

March 23, 2010 Grandfathered status established

¬ Coverage in place on March 23, 2010 is considered grandfathered

¬ Changes made to coverage after this date (except enrollment changes) may cause the plan to lose this status

Small business tax credit available (see www.irs.gov)

On and after March 30, 2010 Children up to age 27 in the taxable year receive tax favored

treatment of health benefits

June 21, 2010 Early retiree reinsurance program becomes available

6

Immediate Considerations

For all plans effective the first plan year on or after September 23, 2010 No annual limitations on essential benefits, except

as allowed by HHS

No lifetime limitations on essential benefits

Cover adult children to age 26 (special exception applies for grandfathered plans)

No pre-existing condition exclusions on children under age 19

No rescission

7

Immediate Considerations

For non-grandfathered plans effective the first plan year on or after September 23, 2010

Cover preventive care at 100%

105(h) nondiscrimination rules apply to insured plans

If plan requires PCP designation, allow enrollees to designate any in-network doctors (including OB/GYN and pediatrician)

Emergency services covered as in-network and no required preauthorization

New appeals process for insured plans

8

Immediate ConsiderationsAs of January 1, 2011 No OTC drugs or medicines through a health FSA,

HRA or HSA without a prescription¬ Supplies, equipment and diagnostic devices appear

permissible (Rev. Rul. 2003-58)¬ Insulin still permissible

W-2 reporting of health benefits for taxable year ¬ (W-2 issued in 2012)

CLASS Act ¬ Employer may (but is not required to) allow employees to

make payroll contributions to the program

20% penalty on non-medical HSA distributions

9

On the Horizon

2012 New benefits summary provided to enrollees HHS reporting

2013 $2,500 cap on the health FSA Increased Medicare tax on high-income earners

¬ 2.35% on wages; 3.8% on unearned income

New health plan fees for Outcomes Research Fund Employer notice on the existence of the Exchange

10

On the Horizon

2014 State-based Exchanges operational and tax subsidies

available to lower income individuals Individual mandate and large employer penalties (50 or

more employees) are in effect $3,000 per FTE receiving government assistance; capped at

$2,000 multiplied by the number of FTEs in excess of 30

Free Choice Vouchers Automatic enrollment for large employers (200+) Wellness program rewards expanded (30%) IRS and participant coverage notification

11

On the Horizon

2014 Benefit Design Reforms – All Plans

¬ No pre-existing condition exclusions

¬ Plan cannot impose more than a 90-day waiting period

¬ No annual benefit limitations

¬ Eligibility for children up to age 26

Benefit Design Reforms – Non-grandfathered Plans¬ Limited out-of-pocket costs

¬ Deductible limitations on small groups

12

On the Horizon

2017 States may allow large employers (over 100

employees) to purchase coverage through the Exchange

2018 40% excise tax on high cost plans

13

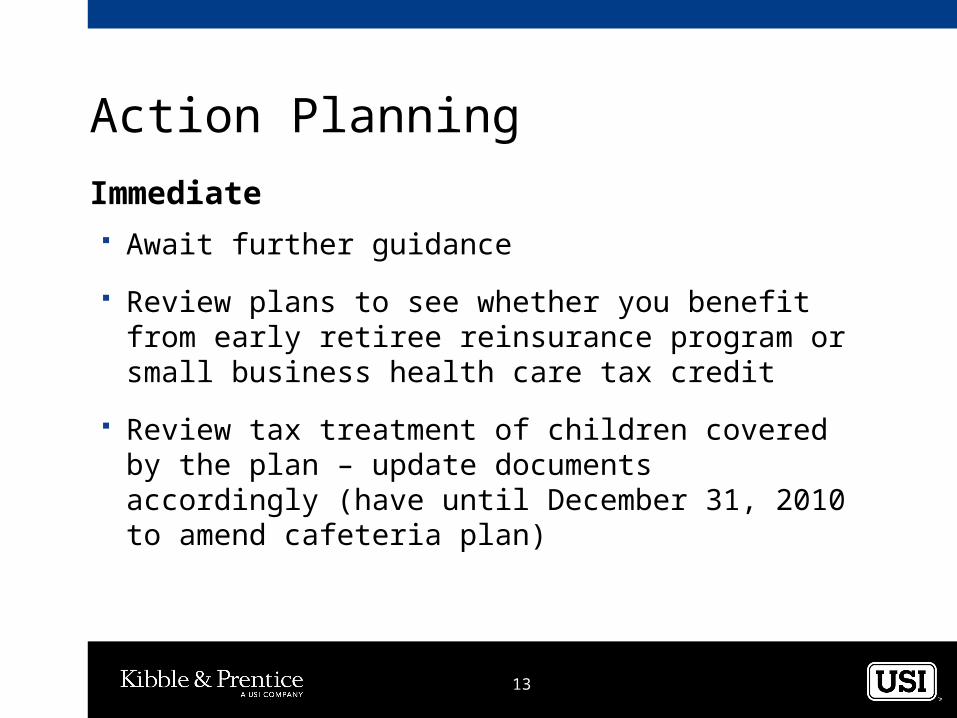

Action Planning

Immediate Await further guidance

Review plans to see whether you benefit from early retiree reinsurance program or small business health care tax credit

Review tax treatment of children covered by the plan – update documents accordingly (have until December 31, 2010 to amend cafeteria plan)

14

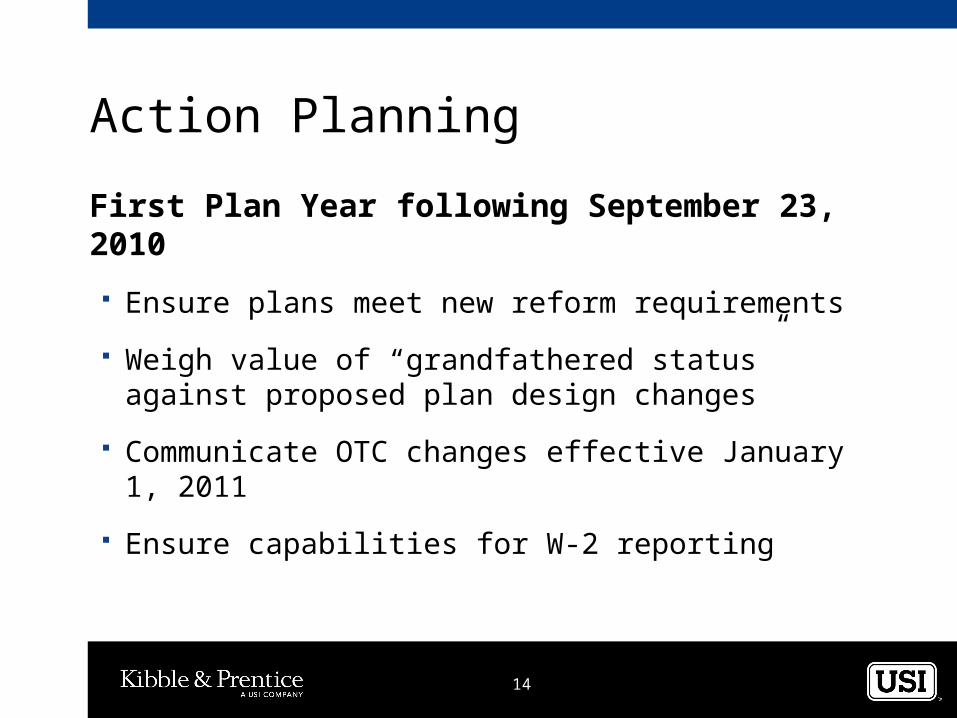

Action Planning

First Plan Year following September 23, 2010

Ensure plans meet new reform requirements

Weigh value of “grandfathered status” against proposed plan design changes

Communicate OTC changes effective January 1, 2011

Ensure capabilities for W-2 reporting

15

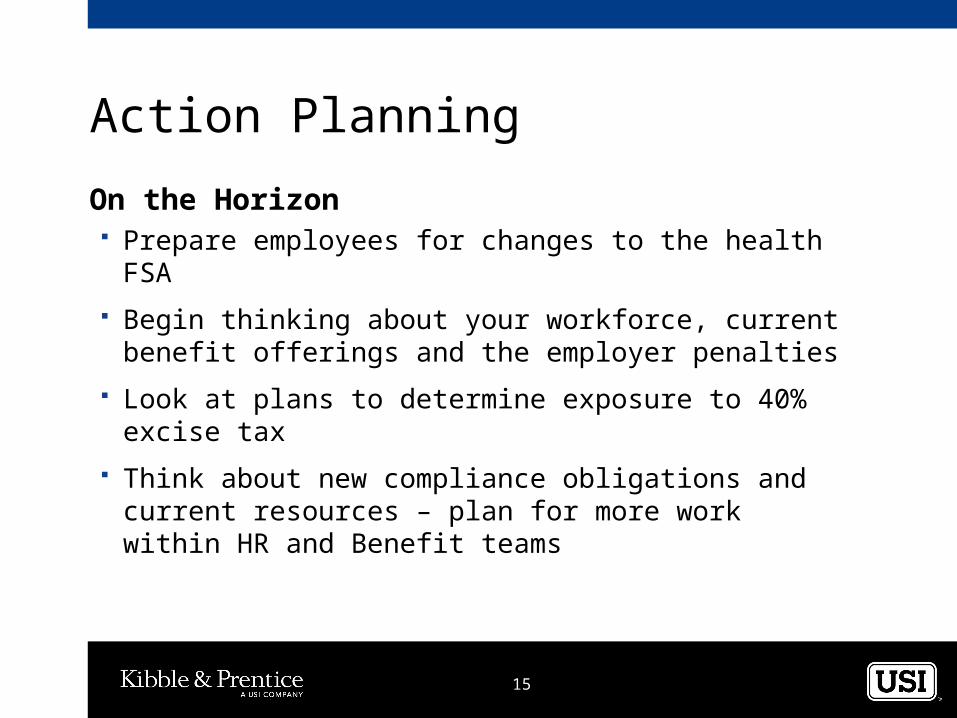

Action Planning

On the Horizon Prepare employees for changes to the health FSA

Begin thinking about your workforce, current benefit offerings and the employer penalties

Look at plans to determine exposure to 40% excise tax

Think about new compliance obligations and current resources – plan for more work within HR and Benefit teams

16

Thank you!

ALICIA SCALZO WILMOTH, JD

Kibble & Prentice, a USI Company

p. 206.441.6300

www.kpcom.com