25

1 International Portfolio Management

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | derek-reed |

| View: | 214 times |

| Download: | 0 times |

11

International Portfolio Management

22

We will talk about...

1. Why investors diversify their portfolios internationally.

2. How much the investors can gain from international diversification.

3. The effect of fluctuating exchange rates on international portfolio investments.

4. Portfolio Theory (unhedged and hedged versions).

33

International Investment

Direct Purchase of Foreign Shares

– This route is usually reserved for large institutional investors because of high transaction costs.

American Depositary Receipts (ADRs)– After a U.S. bank has taken custody of foreign shares

in its foreign office, ADRs can be issued as claims against the foreign shares.

– The issuing bank services the ADRs by collecting all dividends, rights offerings, etc., and distributing the proceeds in US$ to the ADR owners.

44

Mutual Funds

– Mutual funds that invest in foreign stocks can be grouped into several categories from a U.S. perspective:Global - Investing in U.S. and non-U.S. shares.International - Investing in non-U.S. shares only.Regional - Investing in a geographic area.Country - Investing in a single country.Specialty - International investments in an industry

group such as telecommunications, or special themes such as newly privatized firms.

International Investment

55

Exchange Traded Funds (ETFs)

– ETFs represent shares in an index fund that is intended to track the performance of a single country index.

International Investment

66

0

50

100

150

200

250

300

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

US

$ B

illi

on

sMutual Fund Investment in International Equities

77

Correlation structure and risk

• Average $ return on emerging market index in 1990-1998:

3.5% + high volatility.

• Average $ return on S&P500 index in 1990-1998:

13% + low volatility.

Why would investors buy emerging markets stocks?

88

Correlation structure and risk

“Don’t put all your eggs in one basket”

Individually, emerging stock markets are more risky than developed ones, but because the ups and downs of rich-country markets are not strongly matched with the ups and downs of emerging countries markets , holding emerging-market share as part of a diversified portfolio allows investors to reduce the volatility of their overall portfolio.

If an investor has put money into foreign markets which are highly correlated with his home market then all of the investor’s eggs are still in the same basket.

99

Portfolio Riskin domestic and international stocks

• A fundamental result in portfolio theory is that the idiosyncratic risks of individual securities can be reduced by investing in a broadly diversified portfolio of many securities.

• Various empirical studies indicate that: For the same portfolio size, randomly selected international

stocks offered more diversification than randomly selected U.S. stocks.

Diversification across countries reduced risk more than diversification across industries within a single country.

The world portfolio offered a risk/return trade-off at least as favorable, and often considerably more favorable, than any individual country.

1010

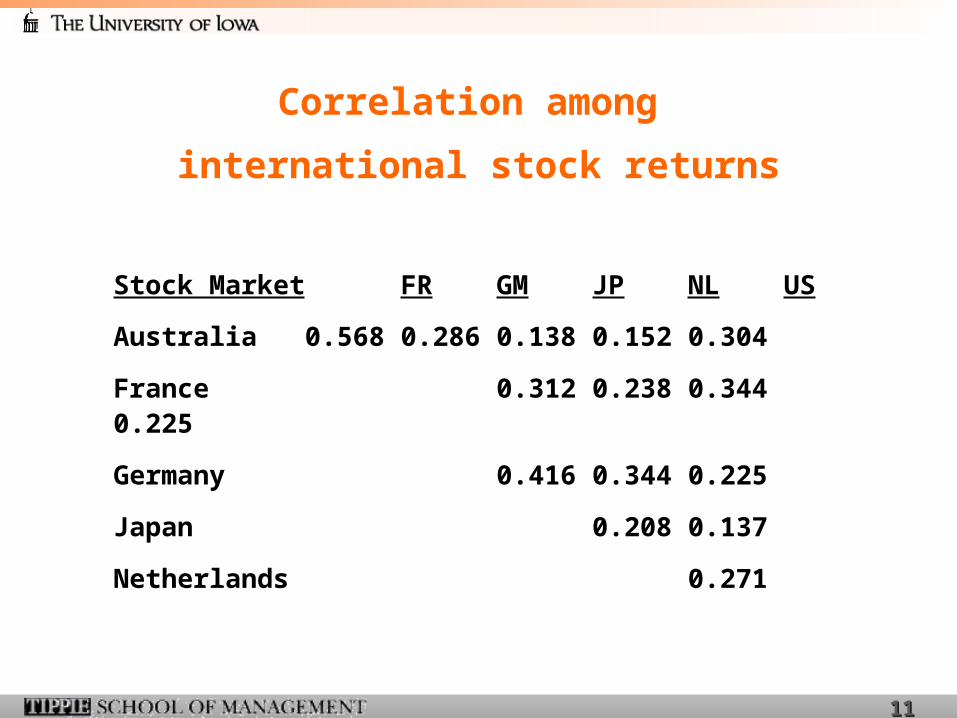

Correlation structure and risk

Security returns are much less correlated across countries than within country.

Investors want as high return as possible for the amount of risk they are willing to bear…

…or to get the return they want by taking as little risk as possible.

1111

Correlation among

international stock returns

Stock Market FR GM JP NL US

Australia 0.568 0.286 0.138 0.152 0.304

France 0.312 0.238 0.344 0.225

Germany 0.416 0.344 0.225

Japan 0.208 0.137

Netherlands 0.271

1212

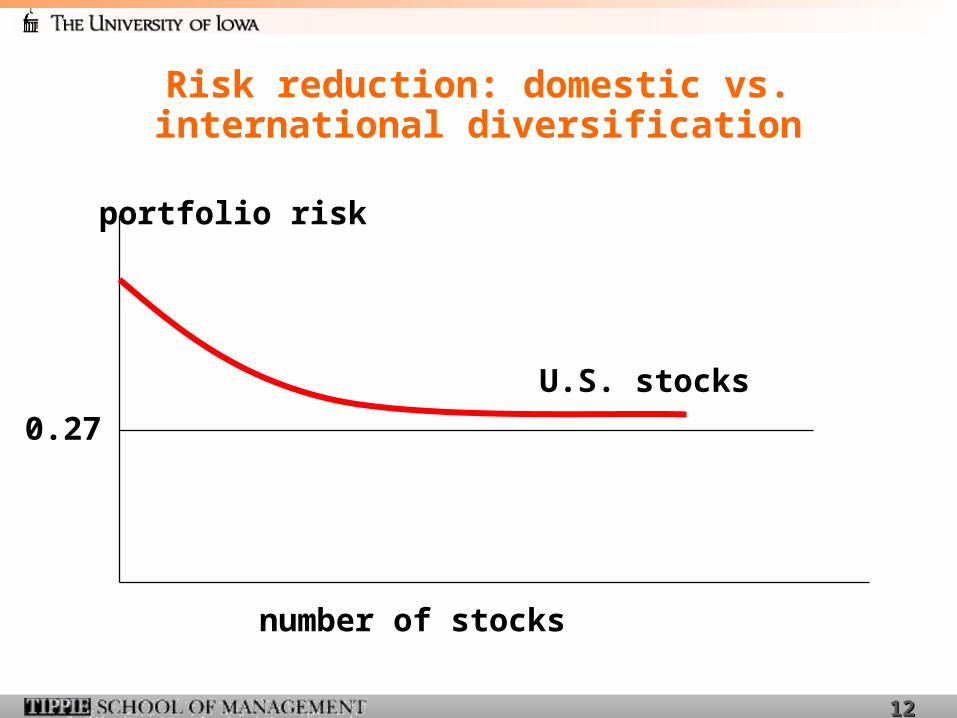

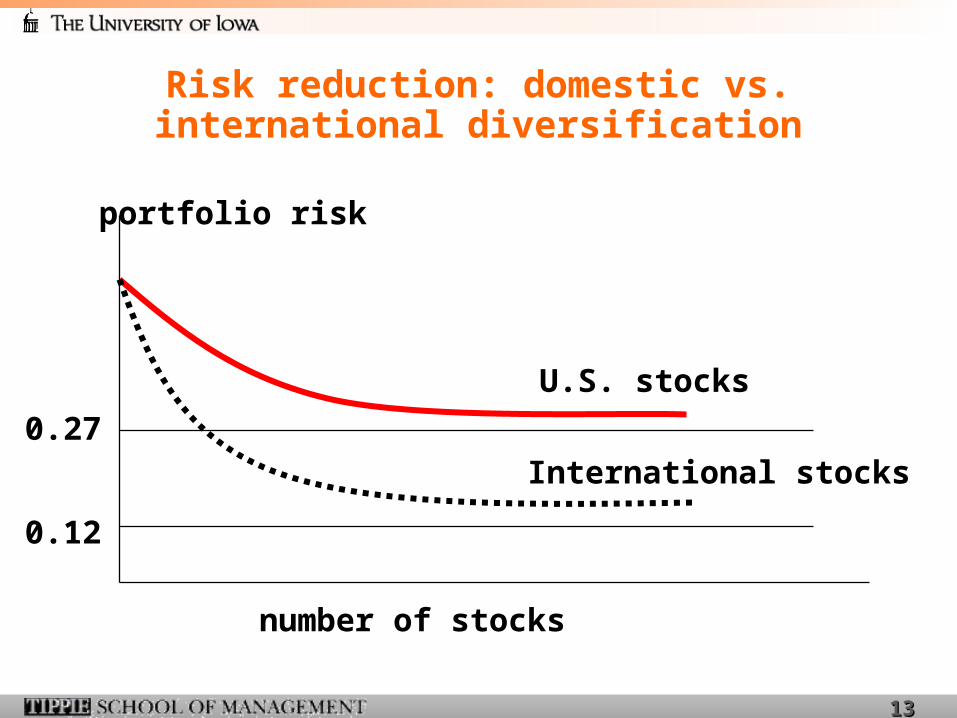

Risk reduction: domestic vs. international diversification

number of stocks

portfolio risk

U.S. stocks

0.27

1313

number of stocks

portfolio risk

U.S. stocks

International stocks

0.12

0.27

Risk reduction: domestic vs. international diversification

1414

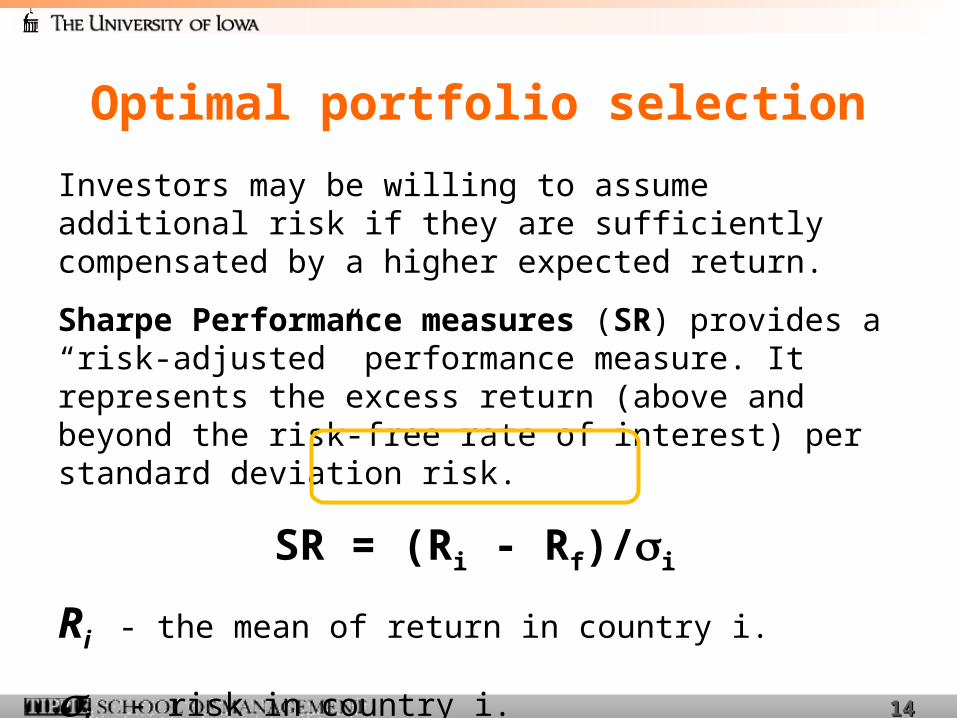

Investors may be willing to assume additional risk if they are sufficiently compensated by a higher expected return.

Sharpe Performance measures (SR) provides a “risk-adjusted” performance measure. It represents the excess return (above and beyond the risk-free rate of interest) per standard deviation risk.

SR = (Ri - Rf)/i

Ri - the mean of return in country i.

i - risk in country i.

Optimal portfolio selection

1515

When finding optimal portfolio allocation we need to consider 3 factors:

Return

Risk (stock price volatility + exchange rate volatility)

Correlation with other countries’ stock prices.

Optimal portfolio for U.S. investors can be different from optimal portfolio for Japanese investor.

Optimal portfolio selection

1616

The gains from holding international portfolio is measured by the increase in Sharpe performance measure.

SR = SR(OIP) - SR(DP)

OIP = optimal international portfolio

DP = domestic portfolio

SR represents the extra return per standard deviation risk accruing from international investment.

The SRs of the international portfolios demonstrates potential benefits of international diversification.

Evaluating the gains

1717

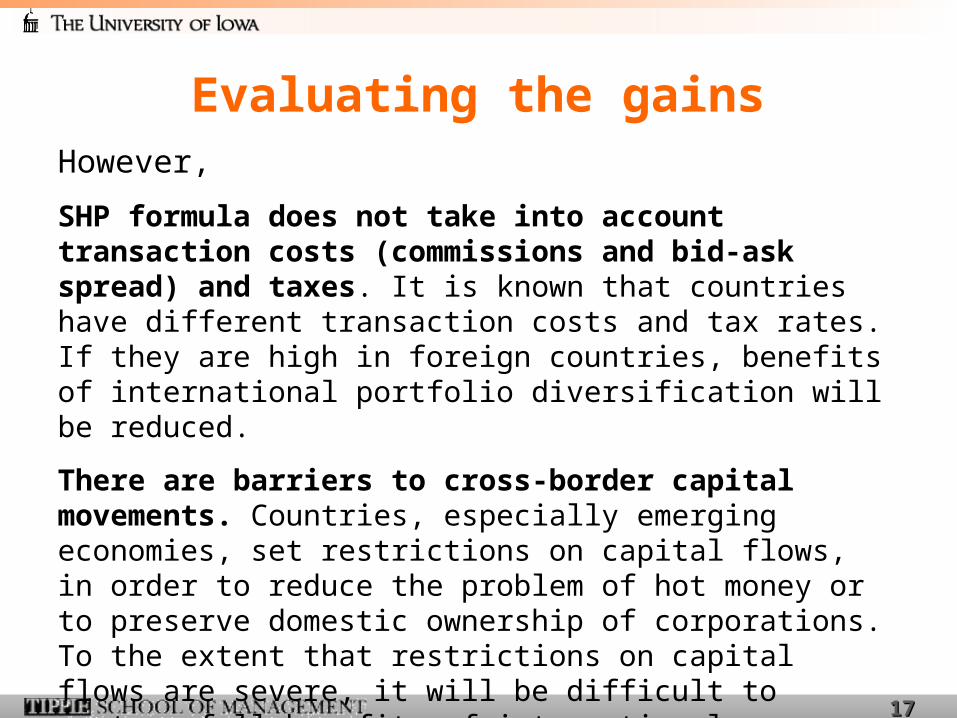

However,

SHP formula does not take into account transaction costs (commissions and bid-ask spread) and taxes. It is known that countries have different transaction costs and tax rates. If they are high in foreign countries, benefits of international portfolio diversification will be reduced.

There are barriers to cross-border capital movements. Countries, especially emerging economies, set restrictions on capital flows, in order to reduce the problem of hot money or to preserve domestic ownership of corporations. To the extent that restrictions on capital flows are severe, it will be difficult to capture full benefits of international diversification.

Evaluating the gains

1818

• Rate of return on Dax 100 is 20%.

• Rate of return on Dow Jones is 15%.

• Would you buy Dax 100 or Dow Jones?

• What if Euro depreciates against dollar?

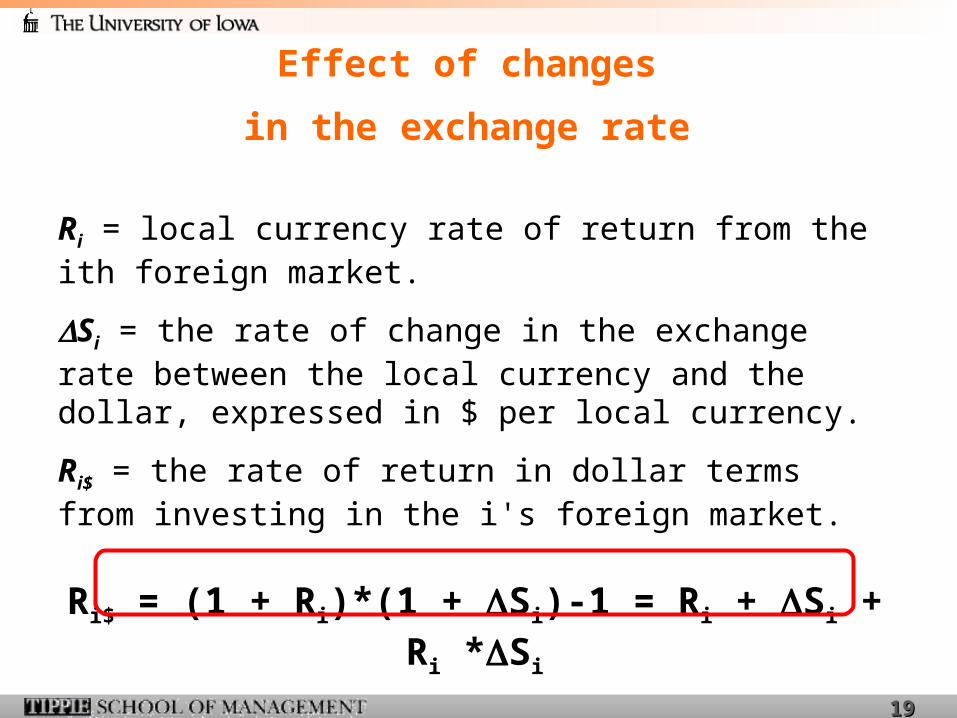

• The realized dollar returns for a U.S. resident investing in a foreign market will depend not only on the return in the foreign market but also on the change in the exchange rate between the dollar and the foreign currency.

Effect of changes

in the exchange rate

1919

Ri = local currency rate of return from the ith foreign market.

Si = the rate of change in the exchange rate between the local currency and the dollar, expressed in $ per local currency.

Ri$ = the rate of return in dollar terms from investing in the i's foreign market.

Ri$ = (1 + Ri)*(1 + Si)-1 = Ri + Si + Ri *Si

Effect of changes

in the exchange rate

2020

Pension funds in Argentina, Bolivia, Columbia, Mexico, and Chile. By investing internationally they show better performance but money leaves the country.

Those pensions will be paid in home currency. But exchange rate fluctuations can cause big swings in the domestic-currency value of foreign assets.

Effect of changes

in the exchange rate

2121

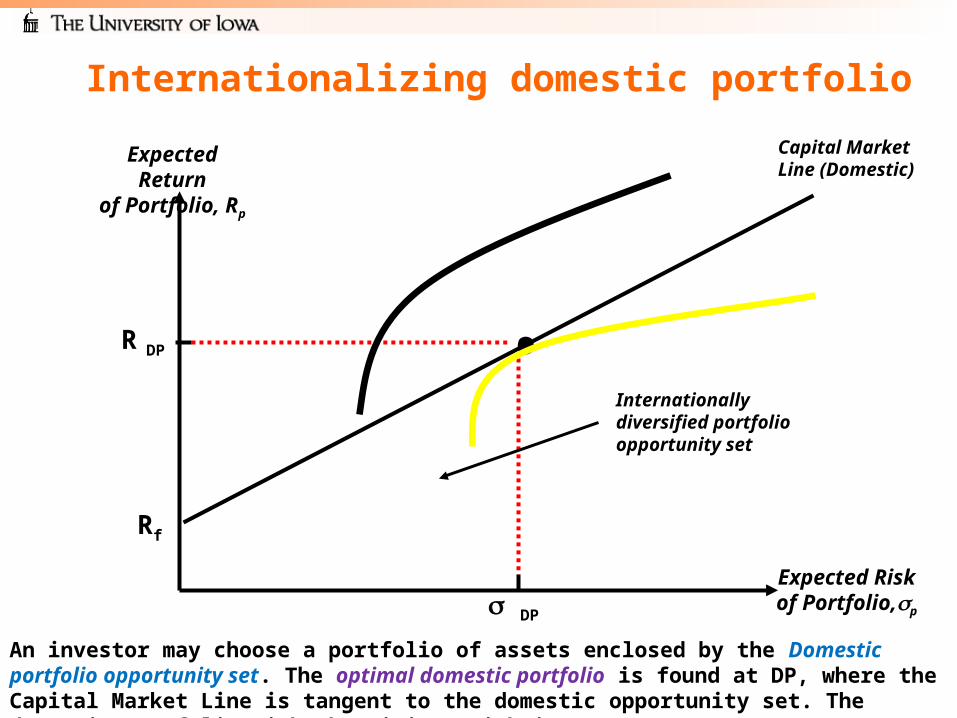

Expected Returnof Portfolio, Rp

Expected Riskof Portfolio,p

An investor may choose a portfolio of assets enclosed by the Domestic portfolio opportunity set. The optimal domestic portfolio is found at DP, where the Security Market Line is tangent to the domestic

portfolio opportunity set. The domestic portfolio with the minimum risk is MRDP.

Rf

Capital MarketLine (Domestic)

•

DP

R DP

•Minimum risk (MRDP )domestic portfolio

MRDP

DP

Optimal domesticportfolio (DP)

Internationalizing domestic portfolio

2222

Expected Returnof Portfolio, Rp

Expected Riskof Portfolio,p

An investor may choose a portfolio of assets enclosed by the Domestic portfolio opportunity set. The optimal domestic portfolio is found at DP, where the Capital Market Line is tangent to the domestic opportunity set. The domestic portfolio with the minimum risk is MRDP.

Rf

Capital MarketLine (Domestic)

•

DP

R DP

Internationally diversified portfolio opportunity set

Internationalizing domestic portfolio

2323

Expected Returnof Portfolio, Rp

Expected Riskof Portfolio,p

An investor may choose a portfolio of assets enclosed by the Domestic portfolio opportunity set. The optimal domestic portfolio is found at DP, where the Security Market Line is tangent to the domestic portfolio opportunity set. The domestic portfolio with the minimum risk is MRDP.

Rf

CML (Domestic)

•

DP

R DP

R IP •

IP

IP

Optimal international portfolio

CML (International)

Internationalizing domestic portfolio

2424

Correlation among

international stock returns

• Correlation between shares declines as markets become globalized.

• Globalization is good for any economy (more trade).

• Globalization may be bad for investors.

• As the world’s financial markets grow more integrated their movements may also become more correlated.

• Investors with money (U.S.) may not be willing to invest abroad which might slow economic growth down in developing countries.

2525

1. International portfolio investment has been growing rapidly in recent years due to (a) the deregulation of financial markets, and (b) the introduction of mutual funds.

2. Investors diversify to reduce risk. The extent by which the risk is reduced depends on the covariance among individual securities comprising the portfolio. Since the security returns tend to covary much less across countries than within a country, investors can reduce portfolio risk more by diversifying internationally than purely domestically.

3. Foreign exchange rate uncertainty contributes to the risk of foreign investment through its own volatility as well as with through its covariance with local market returns.

Key points

![A Population-based Incremental Learning Method for ...pszrq/files/SYNASC14.pdf · diversify the portfolio and thus reduce the risk. However, according to [9], investors prefer a small](https://static.documents.pub/doc/80x56/602d1552eb5e0c4c381d9c0d/a-population-based-incremental-learning-method-for-pszrqfiles-diversify.jpg)