46

1 Introduction Management control is a must in any organization that practices decentralizatio n We begin with three terms : 1. Control 2. Managemen t 3. Systems

| Date post: | 21-Dec-2015 |

| Category: |

Documents |

| View: | 214 times |

| Download: | 0 times |

1

Introduction

Management control is a must in any

organization that practices

decentralization

Management control is a must in any

organization that practices

decentralization

We begin with three terms :1. Control

2. Management

3. Systems

2

Basic Concepts

An organization must be controlled, that is, devices that ensure it goes where its leaders want it to go

must be operative

An organization must be controlled, that is, devices that ensure it goes where its leaders want it to go

must be operative

Control

3

Basic Concepts

1. Detector/Sensor

A device that A device that measures what measures what

is actually is actually happening in happening in the process the process

being controlledbeing controlled

1. Detector/Sensor

A device that A device that measures what measures what

is actually is actually happening in happening in the process the process

being controlledbeing controlled

Elements of a Control System

Elements of a Control System

4

Basic Concepts

2. Assessor

A device that A device that determines the determines the significance of significance of

what is actually what is actually happening by happening by

comparing it with comparing it with some standard of some standard of

what should what should happenhappen

2. Assessor

A device that A device that determines the determines the significance of significance of

what is actually what is actually happening by happening by

comparing it with comparing it with some standard of some standard of

what should what should happenhappen

Significance is assessed by

comparing the information on what is actually happening with some standard

or expectation of what should be

happening

Significance is assessed by

comparing the information on what is actually happening with some standard

or expectation of what should be

happening

5

Basic Concepts

3. Effector

A device that A device that alters behavior alters behavior if the assessor if the assessor indicates the indicates the need to do soneed to do so

3. Effector

A device that A device that alters behavior alters behavior if the assessor if the assessor indicates the indicates the need to do soneed to do so

The device is often called “feedback”

The device is often called “feedback”

6

Basic Concepts

4. Communication network

Devices that Devices that transmits transmits

information information between the between the

detector and the detector and the assessor and assessor and

between assessor between assessor and the effectorand the effector

4. Communication network

Devices that Devices that transmits transmits

information information between the between the

detector and the detector and the assessor and assessor and

between assessor between assessor and the effectorand the effector

Communication network

Communication network

7

Basic Concepts

1.Detector, 1.Detector, observed observed

information information about what about what

is happeningis happening

1.Detector, 1.Detector, observed observed

information information about what about what

is happeningis happening

3. Effector, 3. Effector, behavior behavior altering altering

communication communication if neededif needed

3. Effector, 3. Effector, behavior behavior altering altering

communication communication if neededif needed

2.Assessor, 2.Assessor, comparison comparison with standarwith standar

2.Assessor, 2.Assessor, comparison comparison with standarwith standar

Entity being

controlled

Entity being

controlled

Control device

Control device

Elements of the Control Process

8

Basic Concepts

The management control process is the process by

which managers at all levels ensure that the people they supervise

implement their intended strategies

The management control process is the process by

which managers at all levels ensure that the people they supervise

implement their intended strategies

Management

9

Basic Concepts

A system is a prescribed and

usually repetitious way of carrying out

an activity or a set of activities

A system is a prescribed and

usually repetitious way of carrying out

an activity or a set of activities

Systems

10Boundaries of Management Control

Management control fits

between strategy formulation and task control in

several respects

11Boundaries of Management Control

Task ControlTask ControlTask ControlTask Control

Management ControlManagement ControlManagement ControlManagement Control

Strategy FormulationStrategy Formulation Goals, Strategies and Policies

Implementation of Strategies

Efficient and Effective Performance of

Individual Tasks

Activity Nature of End Product

General Relationships among Planning and Control Functions

12Boundaries of Management Control

Management control is the process by which managers influence other members of the organization to implement the organization’s strategies

13Boundaries of Management Control

1. Planning, what the organization should do

2. Coordinating, the activities of several parts of the organization

3. Communicating, information

4. Evaluating, information5. Deciding, what, if any,

action should be taken6. Influencing, people to

change their behavior

1. Planning, what the organization should do

2. Coordinating, the activities of several parts of the organization

3. Communicating, information

4. Evaluating, information5. Deciding, what, if any,

action should be taken6. Influencing, people to

change their behavior

Management control involves

a variety of activities,

including :

Management control involves

a variety of activities,

including :

14Boundaries of Management Control

Goal Congruence Goal congruence means that, insofar as is feasible, the goals of an organization’s individual members should be consistent with the goals of the organization itself.

Tool for Implementing StrategyManagement control focuses primarily on strategy execution.Management control are only one of the tools managers use in implementing desired strategies.Strategies are also implemented through the organization’s structure, its management of human resources and its particular culture.

Goal Congruence Goal congruence means that, insofar as is feasible, the goals of an organization’s individual members should be consistent with the goals of the organization itself.

Tool for Implementing StrategyManagement control focuses primarily on strategy execution.Management control are only one of the tools managers use in implementing desired strategies.Strategies are also implemented through the organization’s structure, its management of human resources and its particular culture.

15

Basic Concepts

OrganizationOrganizationStructureStructure

OrganizationOrganizationStructureStructure

HR HR ManagementManagement

HR HR ManagementManagement

PerformancePerformancePerformancePerformance

CultureCulture

ManagementControls

ManagementControls

Framework for Strategy Implementation

StrategyStrategy

Implementation Mechanism

16Boundaries of Management Control

Strategy formulation is the process of

deciding on the goals of the organization and the strategies for attaining these

goals

Strategy Formulation ?

17Boundaries of Management Control

Strategy Formulation

is the process of is the process of deciding on new deciding on new

strategiesstrategies

Management Control

is the process of is the process of implementing those implementing those

strategiesstrategies

Strategy Formulation

is the process of is the process of deciding on new deciding on new

strategiesstrategies

Management Control

is the process of is the process of implementing those implementing those

strategiesstrategies

Distinctions between strategy formulation and

Management Control

Distinctions between strategy formulation and

Management Control

18Boundaries of Management Control

Task control is the process of assuring that

specified tasks are carried out

effectively and efficiently

Task Control ?

19Boundaries of Management Control

Task Control• Transaction oriented Transaction oriented • ScientificScientific• The focus is on specific tasksThe focus is on specific tasks

Management Control• Involves the behavior of Involves the behavior of

managersmanagers• Can never be reduced to Can never be reduced to

sciencescience• The focus is on organizational The focus is on organizational

unitsunits• Concerned with the broadly Concerned with the broadly

activities of managersactivities of managers

Task Control• Transaction oriented Transaction oriented • ScientificScientific• The focus is on specific tasksThe focus is on specific tasks

Management Control• Involves the behavior of Involves the behavior of

managersmanagers• Can never be reduced to Can never be reduced to

sciencescience• The focus is on organizational The focus is on organizational

unitsunits• Concerned with the broadly Concerned with the broadly

activities of managersactivities of managers

Distinctions between Task Control and Management

Control

Distinctions between Task Control and Management

Control

20Boundaries of Management Control

Examples of Decisions in Planning and Control Functions

Strategy Formulation Management Control Task Control

Acquire an unrelated business

Introduce new product or brand within product line

Coordinate order entry

Enter a new business Expand a plant Schedule production

Add direct mail selling Determine advertising budget

Book TV commercials

Change debt/equity ratio

Issue new debt Manage cash flows

Devise inventory speculation policy

Decide inventory levels Reorder an item

21Boundaries of Management Control

• Instant access• Multi targeted communication

• Costless communication

• Ability to display images

• Shifting power and control to the

individual

• Instant access• Multi targeted communication

• Costless communication

• Ability to display images

• Shifting power and control to the

individual

Impact of the Internet on Management Control

22

The Concept of Strategy

Fix internal competenciesFix internal competenciesFix internal competenciesFix internal competencies

Opportunities and threatsOpportunities and threatsIdentify opportunitiesIdentify opportunities

Opportunities and threatsOpportunities and threatsIdentify opportunitiesIdentify opportunities

Environmental analysisCompetitorSupplierRegulatorySocial/Political

Environmental analysisCompetitorSupplierRegulatorySocial/Political

Strategy Formulation

Internal analysisTechnology know howManufacturing know howMarketing know howDistribution know howLogistics know how

Internal analysisTechnology know howManufacturing know howMarketing know howDistribution know howLogistics know how

Strengths and weaknessesIdentify core competencies

Strengths and weaknessesIdentify core competencies

Firm’s strategiesFirm’s strategies

23

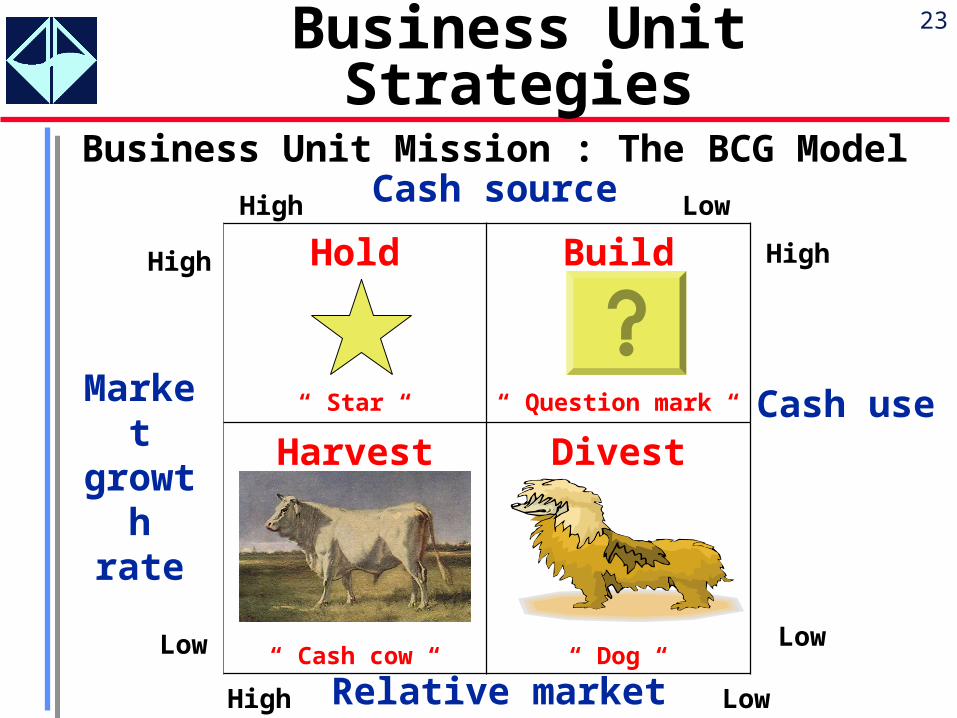

Business Unit Strategies

Hold

“ Star “

Build

“ Question mark “

Harvest

“ Cash cow “

Divest

“ Dog “

High

High

Low

High Low

Low

Low

High

Cash useMarket

growth rate

Business Unit Mission : The BCG ModelCash source

Relative market share

24

Business Unit Strategies

SubstitutesSubstitutesSubstitutesSubstitutes

SuppliersSuppliersSuppliersSuppliers

New EntrantsNew EntrantsNew EntrantsNew Entrants

Business Unit Competitive Advantage

CustomersCustomersCustomersCustomersIndustry Industry CompetitorsCompetitors

Industry Industry CompetitorsCompetitors

Industry Structure Analysis : Porter’s Five Forces Model

25

Types of Organizations

A firm’s strategy has a major influence on A firm’s strategy has a major influence on its structure. Their structures can be its structure. Their structures can be grouped into three general categories :grouped into three general categories :

1.1.A functional structureA functional structure• In which each manager is responsible for In which each manager is responsible for

a specified function such as production a specified function such as production or marketing.or marketing.

2. 2. A business unit structureA business unit structure• In which business unit managers are In which business unit managers are

responsible for most the activities of responsible for most the activities of their particular unit, and the business their particular unit, and the business unit functions as a semi independent unit functions as a semi independent part of the companypart of the company

3. 3. A matrix structureA matrix structure• In which functional units have dual In which functional units have dual

responsibilitiesresponsibilities

A firm’s strategy has a major influence on A firm’s strategy has a major influence on its structure. Their structures can be its structure. Their structures can be grouped into three general categories :grouped into three general categories :

1.1.A functional structureA functional structure• In which each manager is responsible for In which each manager is responsible for

a specified function such as production a specified function such as production or marketing.or marketing.

2. 2. A business unit structureA business unit structure• In which business unit managers are In which business unit managers are

responsible for most the activities of responsible for most the activities of their particular unit, and the business their particular unit, and the business unit functions as a semi independent unit functions as a semi independent part of the companypart of the company

3. 3. A matrix structureA matrix structure• In which functional units have dual In which functional units have dual

responsibilitiesresponsibilities

26

Types of OrganizationsA. Functional Organizations

CEO

Manufacturing

Manager

Marketing

Manager

Manager

Plant 1

Manager

Region A

Manager

Plant 2

Manager

Plant 3

Manager

Region B

Manager

Region C

StaffStaff

Staff

27

The Types of Organizations

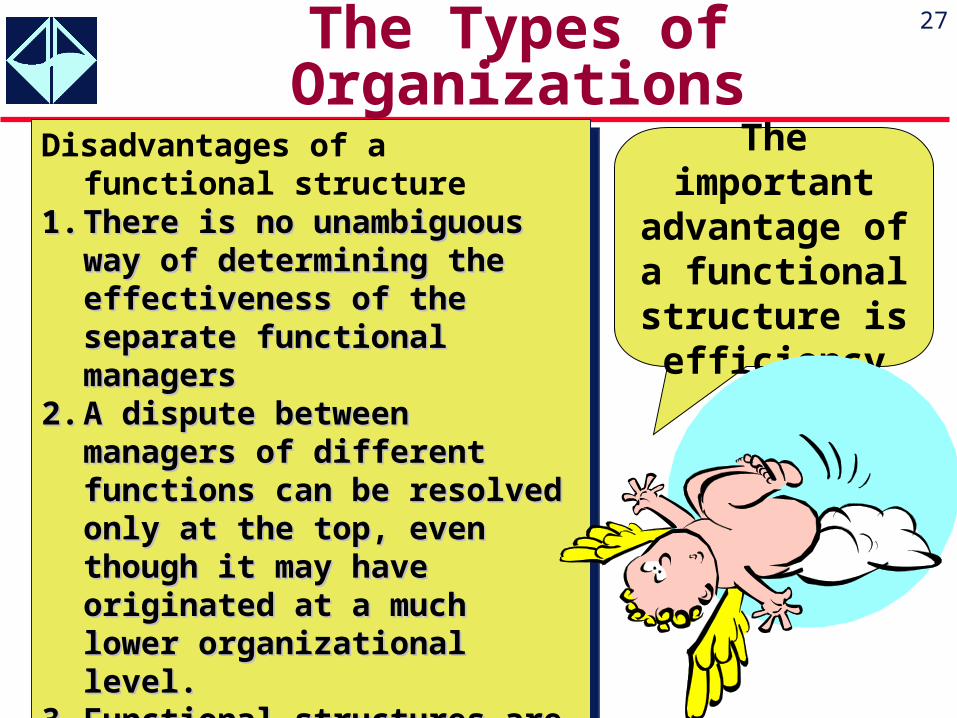

Disadvantages of a functional structure

1.1. There is no unambiguous There is no unambiguous way of determining the way of determining the effectiveness of the effectiveness of the separate functional separate functional managersmanagers

2.2. A dispute between A dispute between managers of different managers of different functions can be resolved functions can be resolved only at the top, even only at the top, even though it may have though it may have originated at a much lower originated at a much lower organizational level. organizational level.

3.3. Functional structures are Functional structures are inadequate for a firm with inadequate for a firm with diversified products and diversified products and marketsmarkets

Disadvantages of a functional structure

1.1. There is no unambiguous There is no unambiguous way of determining the way of determining the effectiveness of the effectiveness of the separate functional separate functional managersmanagers

2.2. A dispute between A dispute between managers of different managers of different functions can be resolved functions can be resolved only at the top, even only at the top, even though it may have though it may have originated at a much lower originated at a much lower organizational level. organizational level.

3.3. Functional structures are Functional structures are inadequate for a firm with inadequate for a firm with diversified products and diversified products and marketsmarkets

The important

advantage of a functional structure is efficiency

28

Types of OrganizationsB. Business Unit Organizations

CEO

Manager

Business Unit X

Manager

Business Unit Y

Plant Manager Plant ManagerMarketingManager

MarketingManager

StaffStaff

Staff

ManagerBusiness Unit Z

Plant Manager

Staff

MarketingManager

A business unit, also called a division, is responsible for all the functions involved in

producing and marketing a specified product line.

29

The Types of Organizations

Advantages of a business unit organizations :

1.1. Provides a training Provides a training ground in general ground in general management. The management. The business unit manager business unit manager should demonstrate the should demonstrate the same entrepreneurial same entrepreneurial spirit that characterizes spirit that characterizes the CEO of an the CEO of an independent company.independent company.

2.2. Its manager may make Its manager may make sounder production and sounder production and marketing decisions than marketing decisions than headquarters might, and headquarters might, and unit as a whole can react unit as a whole can react to new threats or to new threats or opportunities more opportunities more quicklyquickly

Advantages of a business unit organizations :

1.1. Provides a training Provides a training ground in general ground in general management. The management. The business unit manager business unit manager should demonstrate the should demonstrate the same entrepreneurial same entrepreneurial spirit that characterizes spirit that characterizes the CEO of an the CEO of an independent company.independent company.

2.2. Its manager may make Its manager may make sounder production and sounder production and marketing decisions than marketing decisions than headquarters might, and headquarters might, and unit as a whole can react unit as a whole can react to new threats or to new threats or opportunities more opportunities more quicklyquickly

Disadvantage of a business unit

organizations are :1. Each business unit

staff may duplicate some work that in a functional organization is done at headquarters.

2. The disputes between functional specialists in a functional organization may be replaced by disputes between business units in a business unit organization.

30

Types of OrganizationsC. Matrix Organizations

Function A Manager

Function BManager

Function CManager

Project ZManager

Staff

CEO

Project YManager

Project XManager

31

The Types of Organizations

Implications for System

DesignOnce Once

management management has decided that has decided that

a given a given structure is structure is

best, all things best, all things considered, then considered, then

the system the system designer must designer must

take that take that structure as structure as

givengiven

Implications for System

DesignOnce Once

management management has decided that has decided that

a given a given structure is structure is

best, all things best, all things considered, then considered, then

the system the system designer must designer must

take that take that structure as structure as

givengiven

32

Responsibility Centers

Nature of Responsibility Centers

• A responsibility center exists to A responsibility center exists to accomplish one or more purposes, accomplish one or more purposes, these purposes are its objectives.these purposes are its objectives.

• The objectives of responsibility The objectives of responsibility centers are to help implement the centers are to help implement the strategies.strategies.

• The goods and services produced by The goods and services produced by a responsibility centers may be a responsibility centers may be furnished either to another furnished either to another responsibility centers or to the responsibility centers or to the outside marketplace outside marketplace

Nature of Responsibility Centers

• A responsibility center exists to A responsibility center exists to accomplish one or more purposes, accomplish one or more purposes, these purposes are its objectives.these purposes are its objectives.

• The objectives of responsibility The objectives of responsibility centers are to help implement the centers are to help implement the strategies.strategies.

• The goods and services produced by The goods and services produced by a responsibility centers may be a responsibility centers may be furnished either to another furnished either to another responsibility centers or to the responsibility centers or to the outside marketplace outside marketplace

33

Responsibility Centers

WorkWork

The Core Operation of Responsibility Center

OutputInput

Resources used, measured by

cost Capital

Goods or services

The products produced by a responsibility center may be furnished either to another responsibility center (as input) or to the

outside marketplace (as output)

34

Responsibility Centers

Types of Responsibility Centers

Engineered Expense Centers

WorkWork

Optimal relationshipcan be establish

Inputs

Outputs

(Dollar) (Physical)

Manufacturingfunction

Examples

35

Responsibility Centers

Types of Responsibility Centers

Discretionary Expense Centers

WorkWork

Optimal relationshipcannot be establish

Inputs

Outputs

(Dollar) (Physical)

R&Dfunction

Examples…….. ……

......

......

36

Responsibility Centers

Types of Responsibility Centers

Revenue Centers

WorkWork

Input do not relatedto outputs

Inputs

Outputs

(Dollar only for costs directly incurred

(Dollar revenue)

Marketingfunction

Examples…….. ……

......

......

37

Responsibility Centers

Types of Responsibility Centers

Profit Centers

WorkWork

Input are relatedto outputs

Inputs

Outputs

(Dollar costs) (Dollar profits)

Businessunit

Examples…….. ……

......

......

38

Responsibility Centers

Types of Responsibility Centers

Investment Centers

Capital EmployedCapital

Employed

Profits are relatedto capital employed

Inputs

Outputs

(Dollar costs) (Dollar profits)

Businessunit

Examples…….. ……

......

......

39

Transfer Pricing Methods

Transfer Price is to refer to the amount used in

accounting for any transfer of goods and

services between responsibility centers.

Transfer Price is to refer to the amount used in

accounting for any transfer of goods and

services between responsibility centers.

40

Transfer Pricing Methods

Fundamental PrinciplesThe fundamental principle is that the transfer The fundamental principle is that the transfer

price should be similar to the price that would price should be similar to the price that would be charged if the product were sold to outside be charged if the product were sold to outside customers or purchased from outside vendorscustomers or purchased from outside vendors

When profit centers of a company buy products When profit centers of a company buy products from, and sell to, one another, two decisions from, and sell to, one another, two decisions must be made periodically for each product :must be made periodically for each product :

1.1. Should the company produce the product Should the company produce the product inside the company or purchase it from an inside the company or purchase it from an outside vendor ?. outside vendor ?. This is the sourcing This is the sourcing decision.decision.

2.2. If produced inside, at what price should the If produced inside, at what price should the product be transferred between profit centers product be transferred between profit centers ?. ?. This is the transfer price decision. This is the transfer price decision.

Fundamental PrinciplesThe fundamental principle is that the transfer The fundamental principle is that the transfer

price should be similar to the price that would price should be similar to the price that would be charged if the product were sold to outside be charged if the product were sold to outside customers or purchased from outside vendorscustomers or purchased from outside vendors

When profit centers of a company buy products When profit centers of a company buy products from, and sell to, one another, two decisions from, and sell to, one another, two decisions must be made periodically for each product :must be made periodically for each product :

1.1. Should the company produce the product Should the company produce the product inside the company or purchase it from an inside the company or purchase it from an outside vendor ?. outside vendor ?. This is the sourcing This is the sourcing decision.decision.

2.2. If produced inside, at what price should the If produced inside, at what price should the product be transferred between profit centers product be transferred between profit centers ?. ?. This is the transfer price decision. This is the transfer price decision.

41

Transfer Pricing Methods

Upstream Fixed Costs and Profits a. Agreement Among Business UnitsSome companies establish a Some companies establish a formal mechanism whereby formal mechanism whereby representatives from the representatives from the buying and selling units meet buying and selling units meet periodically to decide on periodically to decide on outside selling prices and the outside selling prices and the sharing of profits for products sharing of profits for products with significant upstream fixed with significant upstream fixed costs and profit costs and profit

Upstream Fixed Costs and Profits a. Agreement Among Business UnitsSome companies establish a Some companies establish a formal mechanism whereby formal mechanism whereby representatives from the representatives from the buying and selling units meet buying and selling units meet periodically to decide on periodically to decide on outside selling prices and the outside selling prices and the sharing of profits for products sharing of profits for products with significant upstream fixed with significant upstream fixed costs and profit costs and profit

42

Transfer Pricing Methods

Upstream Fixed Costs and Profits

b. Two Step PricingEstablish a transfer price that Establish a transfer price that

includes two charges :includes two charges :• For each unit sold, a charge For each unit sold, a charge

is made that is equal to the is made that is equal to the standard variable cost of standard variable cost of production.production.

• A periodic charge is made A periodic charge is made that is equal to the fixed that is equal to the fixed costs associated with the costs associated with the facilities reserved for the facilities reserved for the buying unit. buying unit.

Upstream Fixed Costs and Profits

b. Two Step PricingEstablish a transfer price that Establish a transfer price that

includes two charges :includes two charges :• For each unit sold, a charge For each unit sold, a charge

is made that is equal to the is made that is equal to the standard variable cost of standard variable cost of production.production.

• A periodic charge is made A periodic charge is made that is equal to the fixed that is equal to the fixed costs associated with the costs associated with the facilities reserved for the facilities reserved for the buying unit. buying unit.

43

Transfer Pricing Methods

Business Unit X (manufacturer) Product A

Expected monthly sales to business unit Y Expected monthly sales to business unit Y 5,000 units5,000 units

Variable cost per unit Variable cost per unit $ 5 $ 5

Monthly fixed costs assigned to product Monthly fixed costs assigned to product 20,000 20,000

Investment in working capital and facilities Investment in working capital and facilities 1,200,0001,200,000

Competitive return on investment per year Competitive return on investment per year 10 % 10 %

One way to transfer product A to business unit Y One way to transfer product A to business unit Y is at price per unit, calculated as follows :is at price per unit, calculated as follows :

Transfer price for Transfer price for product Aproduct A

Variable cost per unit $ 5Variable cost per unit $ 5Plus fixed cost per unit $ 4Plus fixed cost per unit $ 4Pus profit per unit Pus profit per unit $ 2$ 2Transfer price per unit $ 11Transfer price per unit $ 11

Business Unit X (manufacturer) Product A

Expected monthly sales to business unit Y Expected monthly sales to business unit Y 5,000 units5,000 units

Variable cost per unit Variable cost per unit $ 5 $ 5

Monthly fixed costs assigned to product Monthly fixed costs assigned to product 20,000 20,000

Investment in working capital and facilities Investment in working capital and facilities 1,200,0001,200,000

Competitive return on investment per year Competitive return on investment per year 10 % 10 %

One way to transfer product A to business unit Y One way to transfer product A to business unit Y is at price per unit, calculated as follows :is at price per unit, calculated as follows :

Transfer price for Transfer price for product Aproduct A

Variable cost per unit $ 5Variable cost per unit $ 5Plus fixed cost per unit $ 4Plus fixed cost per unit $ 4Pus profit per unit Pus profit per unit $ 2$ 2Transfer price per unit $ 11Transfer price per unit $ 11

44

Transfer Pricing MethodsCorrection by two step pricing :Transfer price for product “A” $ 5 + $ Transfer price for product “A” $ 5 + $

20,000/month fixed cost + $ 10,000 per month 20,000/month fixed cost + $ 10,000 per month for profit :for profit :

$ 1,200,000 x 0.10$ 1,200,000 x 0.10 = 10,000 = 10,000 1212Unit “Y” will pay the variable cost of Unit “Y” will pay the variable cost of (5,000 unit x $ 5/unit) : $ 25,000 (5,000 unit x $ 5/unit) : $ 25,000 Plus fixed cost and profit : Plus fixed cost and profit : $ 30,000$ 30,000Total $ 55,000Total $ 55,000Unit “X” will pay $ 11/unit (5.000 unit x $ 11 = $ Unit “X” will pay $ 11/unit (5.000 unit x $ 11 = $

55,000)55,000)If transfers in another month were 4,000 units, If transfers in another month were 4,000 units,

Unit “Y” would pay $ 50,000 [(4,000 unit x $ %) Unit “Y” would pay $ 50,000 [(4,000 unit x $ %) + $ 30,000], under two step pricing, compared + $ 30,000], under two step pricing, compared with $ 44,000 ($ 11 x 4,000 unit).with $ 44,000 ($ 11 x 4,000 unit).

The difference is penalty for not using a portion The difference is penalty for not using a portion of unit X’s capacity that it has reserved. of unit X’s capacity that it has reserved.

Correction by two step pricing :Transfer price for product “A” $ 5 + $ Transfer price for product “A” $ 5 + $

20,000/month fixed cost + $ 10,000 per month 20,000/month fixed cost + $ 10,000 per month for profit :for profit :

$ 1,200,000 x 0.10$ 1,200,000 x 0.10 = 10,000 = 10,000 1212Unit “Y” will pay the variable cost of Unit “Y” will pay the variable cost of (5,000 unit x $ 5/unit) : $ 25,000 (5,000 unit x $ 5/unit) : $ 25,000 Plus fixed cost and profit : Plus fixed cost and profit : $ 30,000$ 30,000Total $ 55,000Total $ 55,000Unit “X” will pay $ 11/unit (5.000 unit x $ 11 = $ Unit “X” will pay $ 11/unit (5.000 unit x $ 11 = $

55,000)55,000)If transfers in another month were 4,000 units, If transfers in another month were 4,000 units,

Unit “Y” would pay $ 50,000 [(4,000 unit x $ %) Unit “Y” would pay $ 50,000 [(4,000 unit x $ %) + $ 30,000], under two step pricing, compared + $ 30,000], under two step pricing, compared with $ 44,000 ($ 11 x 4,000 unit).with $ 44,000 ($ 11 x 4,000 unit).

The difference is penalty for not using a portion The difference is penalty for not using a portion of unit X’s capacity that it has reserved. of unit X’s capacity that it has reserved.

45

Transfer Pricing Methods

Upstream Fixed Costs and Profits

c. Profit SharingThe system operates as follows :The system operates as follows :• The product is transferred to the The product is transferred to the

marketing unit at standard marketing unit at standard variable costvariable cost

• After the product is sold, the After the product is sold, the business units share the business units share the contribution earned, which is the contribution earned, which is the selling price minus the variable selling price minus the variable manufacturing and marketing manufacturing and marketing costs.costs.

Upstream Fixed Costs and Profits

c. Profit SharingThe system operates as follows :The system operates as follows :• The product is transferred to the The product is transferred to the

marketing unit at standard marketing unit at standard variable costvariable cost

• After the product is sold, the After the product is sold, the business units share the business units share the contribution earned, which is the contribution earned, which is the selling price minus the variable selling price minus the variable manufacturing and marketing manufacturing and marketing costs.costs.

46

Transfer Pricing Methods

Upstream Fixed Costs and Profits d. Two Sets of PricesThe manufacturing unit’s The manufacturing unit’s revenue is credited at the revenue is credited at the outside sales price and outside sales price and the buying unit is the buying unit is charged the total charged the total standard costs. The standard costs. The difference is charged to a difference is charged to a headquarters account headquarters account and eliminated when the and eliminated when the business unit statements business unit statements are consolidated.are consolidated.

Upstream Fixed Costs and Profits d. Two Sets of PricesThe manufacturing unit’s The manufacturing unit’s revenue is credited at the revenue is credited at the outside sales price and outside sales price and the buying unit is the buying unit is charged the total charged the total standard costs. The standard costs. The difference is charged to a difference is charged to a headquarters account headquarters account and eliminated when the and eliminated when the business unit statements business unit statements are consolidated.are consolidated.