27

1 Kenneth R. Meyers Executive Vice President – Finance, CFO and Treasurer Tenth Annual UBS Global Communications Conference November 17, 2005

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | skylar-jarvis |

| View: | 214 times |

| Download: | 0 times |

1

Kenneth R. MeyersExecutive Vice President – Finance,

CFO and Treasurer

Tenth Annual UBS Global Communications Conference

November 17, 2005

Safe HarborSafe Harbor Statement Under the Private Securities Litigation Reform Act of 1995: All information set forth in this news release, except historical and factual information, represents forward-looking statements. This includes all statements about the company’s plans, beliefs, estimates and expectations. These statements are based on current estimates and projections, which involve certain risks and uncertainties that could cause actual results to differ materially from those in the forward-looking statements. Important factors that may affect these forward-looking statements include, but are not limited to: the final results of the restatements and results of operations for the quarter ended Sept. 30, 2005; possible future restatements; possible material weaknesses in internal controls; the ability of the company to successfully manage and grow the operations of the Chicago MTA and newly launched markets; changes in the overall economy; changes in competition in the markets in which the company operates; changes due to industry consolidation; advances in telecommunications technology; changes in the telecommunications regulatory environment; changes in the value of investments, including variable prepaid forward contracts; an adverse change in the ratings afforded our debt securities by accredited ratings organizations; pending and future litigation; acquisitions/divestitures of properties and/or licenses; and changes in customer growth rates, average monthly revenue per unit, churn rates, roaming rates and the mix of products and services offered in the company’s markets. Investors are encouraged to consider these and other risks and uncertainties that are discussed in documents furnished to the Securities and Exchange Commission.

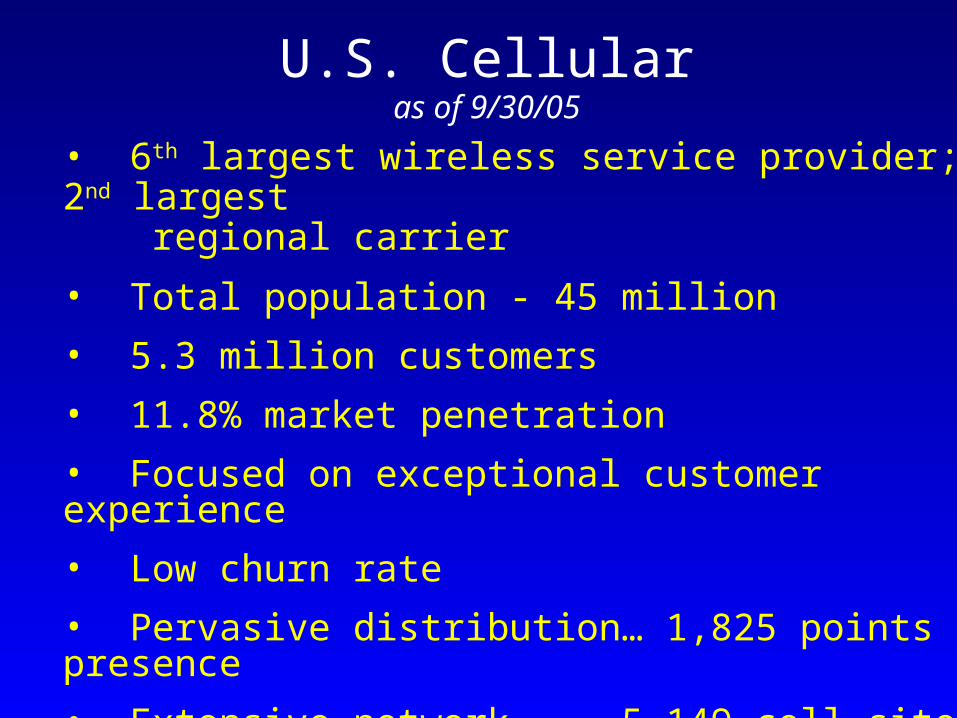

• 6th largest wireless service provider; 2nd largest regional carrier

• Total population - 45 million

• 5.3 million customers

• 11.8% market penetration

• Focused on exceptional customer experience

• Low churn rate

• Pervasive distribution… 1,825 points of presence

• Extensive network ... 5,149 cell sites

• Well positioned in our markets

U.S. Cellularas of 9/30/05

USM Growth Strategies• Regional carrier• Differentiate by driving for high level of

customer satisfaction• Excellent customer service• Quality CDMA 1X network• Broad distribution

• Strategically strengthen regional footprint

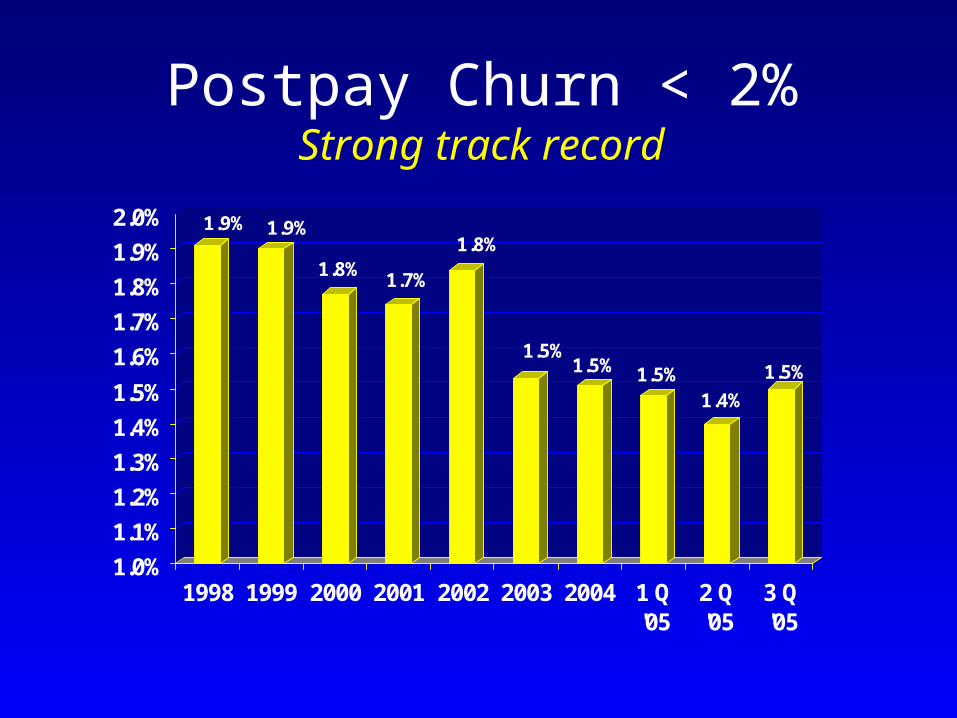

Postpay Churn < 2%Strong track record

1.9% 1.9%

1.8%1.7%

1.8%

1.5%1.5% 1.5%

1.4%

1.5%

1.0%

1.1%

1.2%

1.3%

1.4%

1.5%

1.6%

1.7%

1.8%

1.9%

2.0%

1998 1999 2000 2001 2002 2003 2004 1 Q'05

2 Q'05

3 Q'05

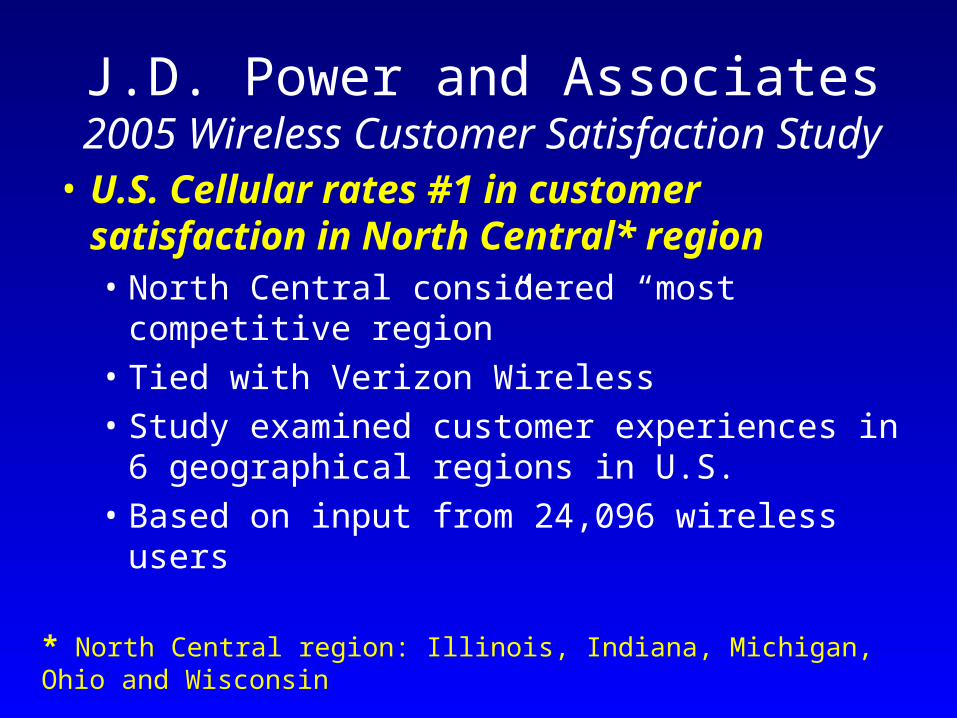

J.D. Power and Associates2005 Wireless Customer Satisfaction

Study• U.S. Cellular rates #1 in customer

satisfaction in North Central* region• North Central considered “most competitive

region”• Tied with Verizon Wireless• Study examined customer experiences in 6

geographical regions in U.S. • Based on input from 24,096 wireless users

* North Central region: Illinois, Indiana, Michigan, Ohio and Wisconsin

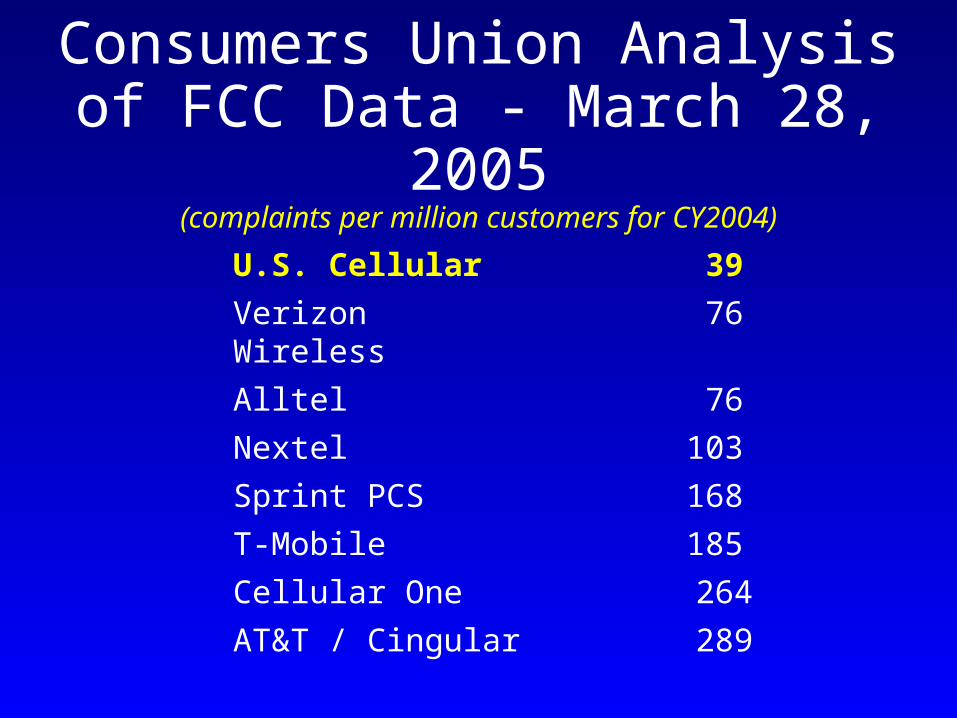

Consumers Union Analysis of FCC Data - March 28, 2005

(complaints per million customers for CY2004)

U.S. Cellular 39

Verizon Wireless 76

Alltel 76

Nextel 103

Sprint PCS 168

T-Mobile 185

Cellular One 264

AT&T / Cingular 289

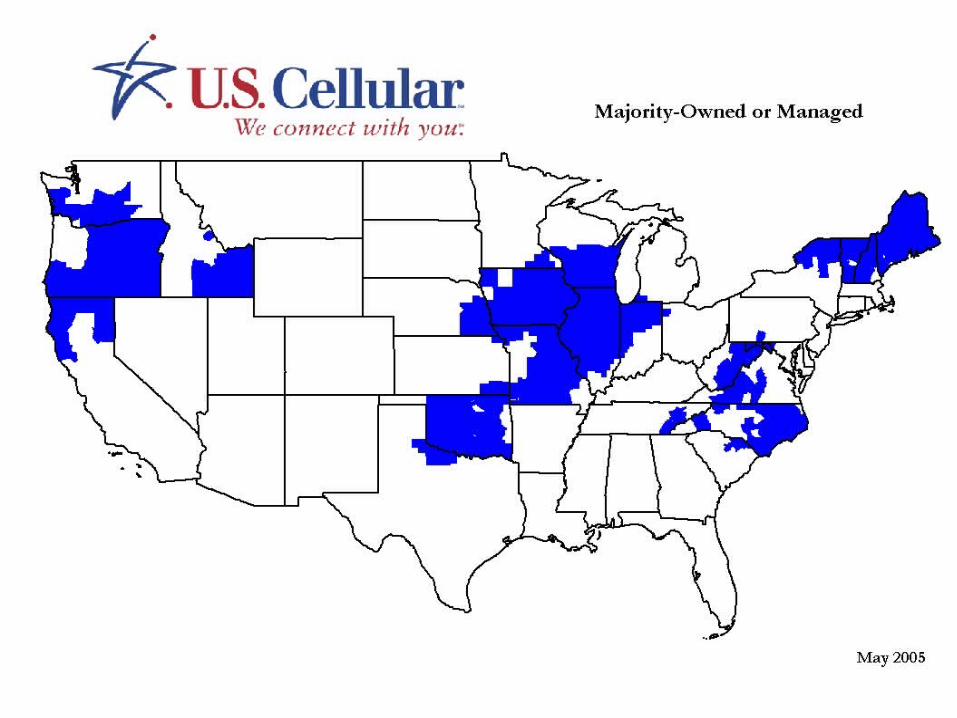

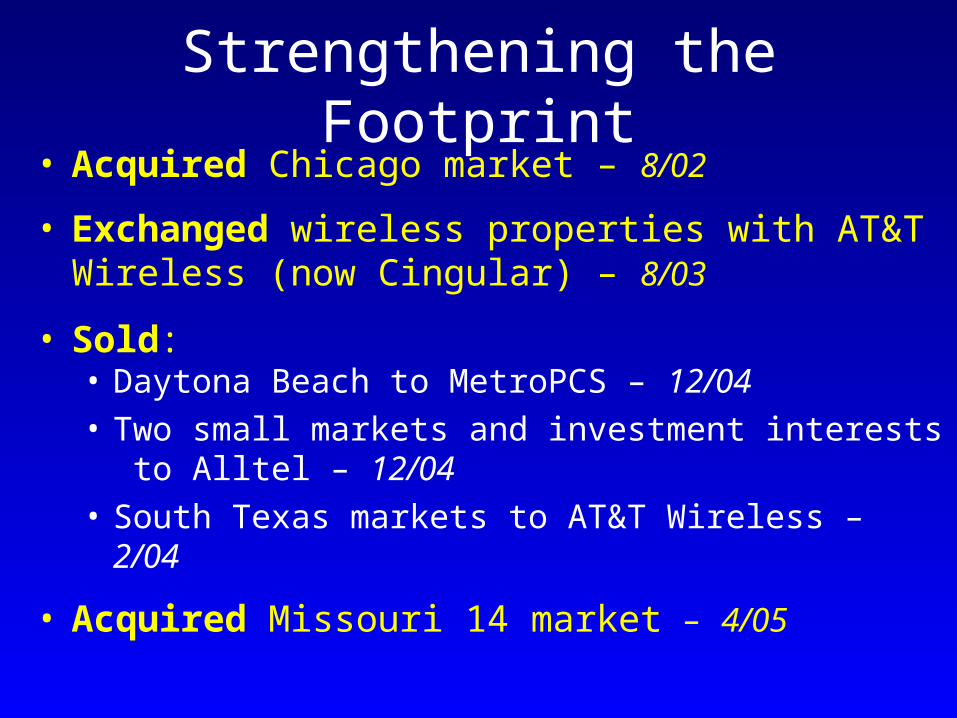

Strengthening the Footprint• Acquired Chicago market – 8/02

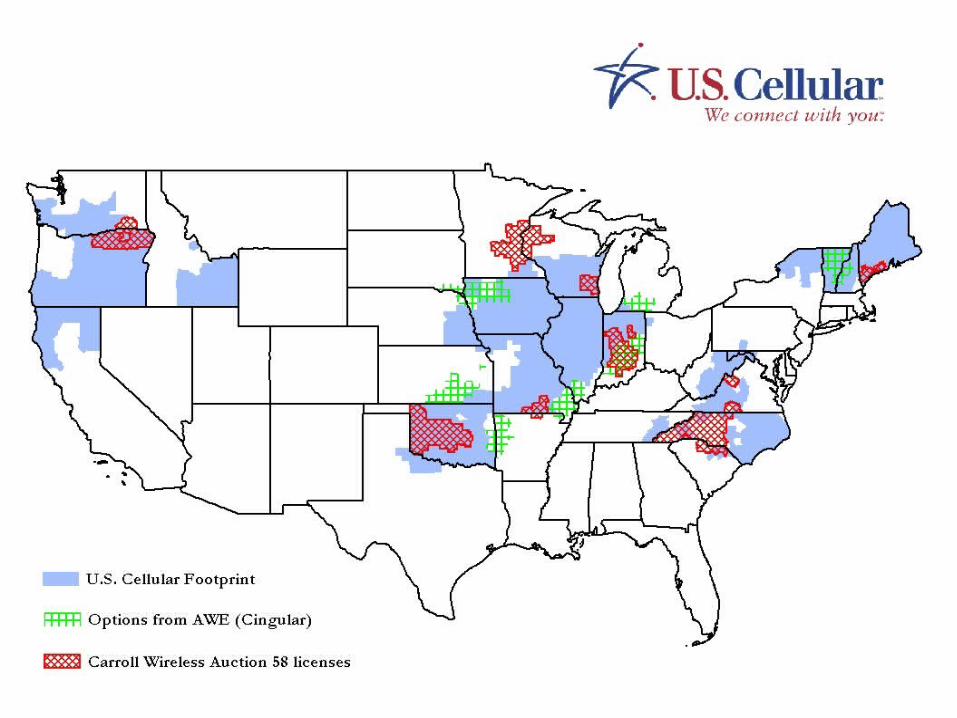

• Exchanged wireless properties with AT&T Wireless (now Cingular) – 8/03

• Sold:• Daytona Beach to MetroPCS – 12/04• Two small markets and investment interests

to Alltel – 12/04• South Texas markets to AT&T Wireless – 2/04

• Acquired Missouri 14 market – 4/05

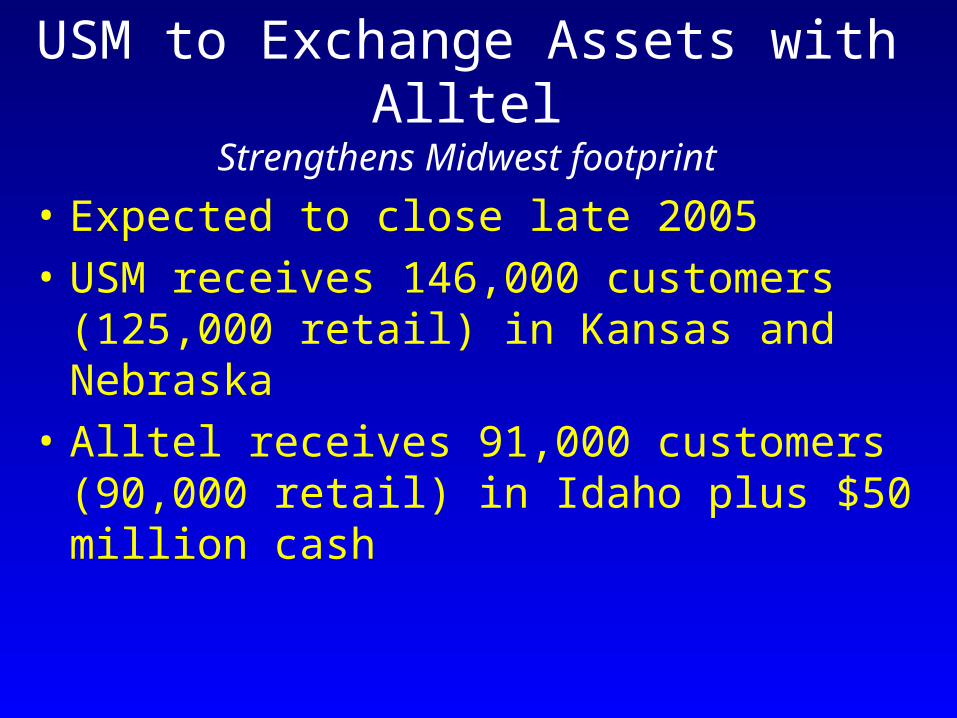

USM to Exchange Assets with AlltelStrengthens Midwest footprint

• Expected to close late 2005

• USM receives 146,000 customers (125,000 retail) in Kansas and Nebraska

• Alltel receives 91,000 customers (90,000 retail) in Idaho plus $50 million cash

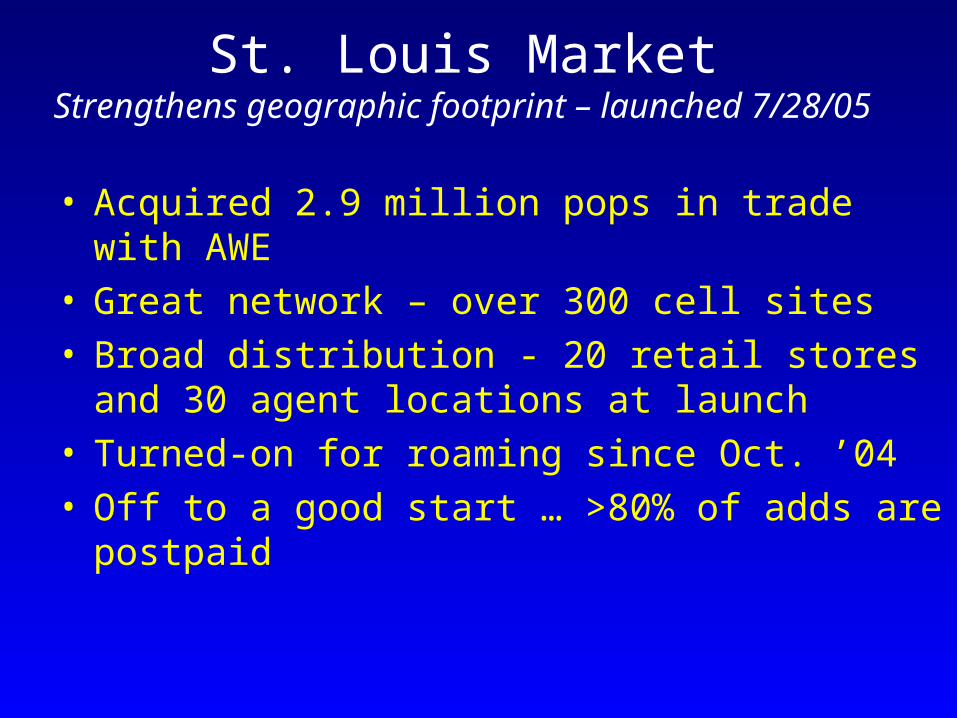

St. Louis MarketStrengthens geographic footprint – launched

7/28/05

• Acquired 2.9 million pops in trade with AWE• Great network – over 300 cell sites• Broad distribution - 20 retail stores and 30 agent

locations at launch• Turned-on for roaming since Oct. ’04• Off to a good start … >80% of adds are

postpaid

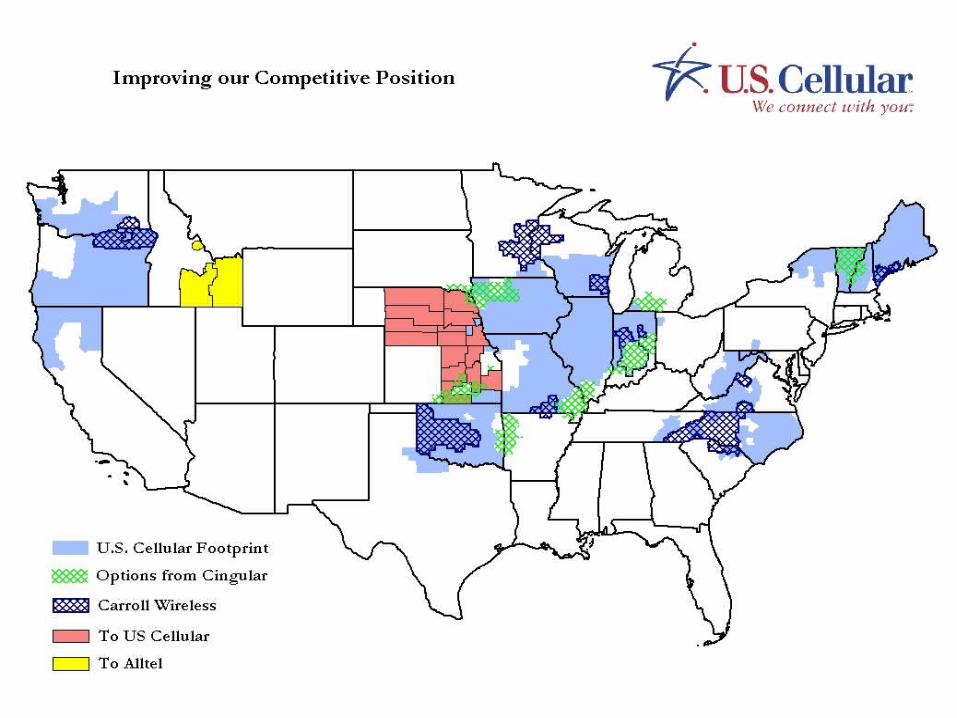

Auction 58

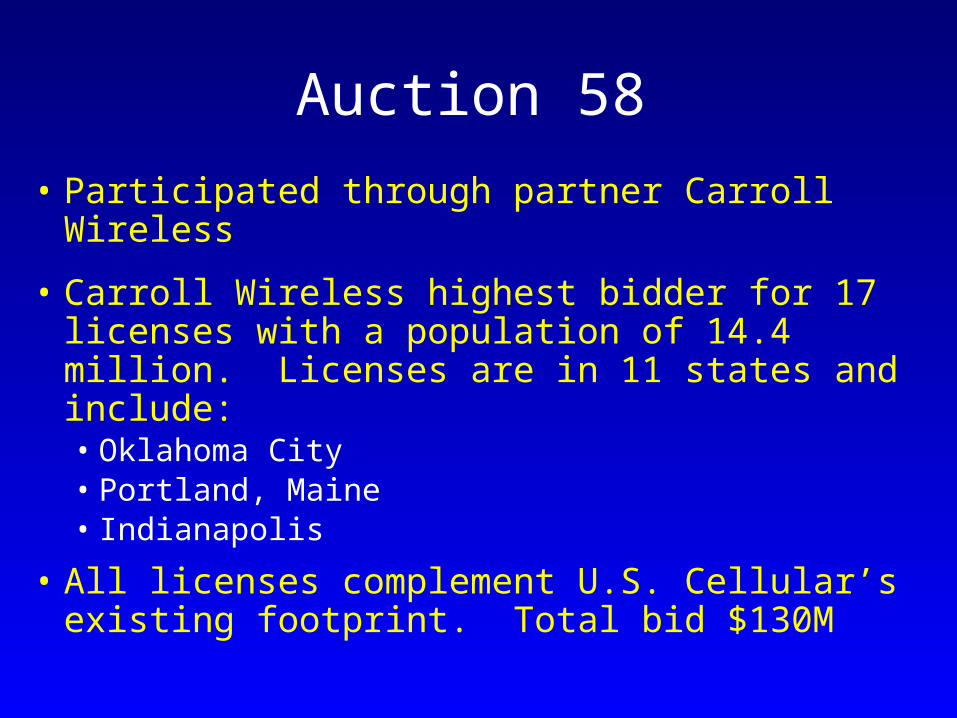

• Participated through partner Carroll Wireless

• Carroll Wireless highest bidder for 17 licenses with a population of 14.4 million. Licenses are in 11 states and include:• Oklahoma City• Portland, Maine• Indianapolis

• All licenses complement U.S. Cellular’s existing footprint. Total bid $130M

CDMA 1X Initiative

• Improved voice capacity and coverage; cost-effective use of wireless spectrum

• Enables offering of high-speed data products

• Completed the 3-year project in 2004

• Ahead of schedule, below planned cost

• Total cost to build CDMA ... ≈ $300 million

Data – easyedgeSM

• easyedgeSM Phone Download Applications (BREWTM)

• Applications: games, news, traffic, calendar

• Launched nWebSM Nov. 2004 – enables Internet access

• Launched AOL® Instant MessengerTM service March 2005

• easyedgeSM Picture Messaging (MMS)

• Take, send or receive photos

• easyedgeSM Wireless Modem Service

• Wireless Internet access for laptops; e-mail; calendar

• Available in select areas to business customers

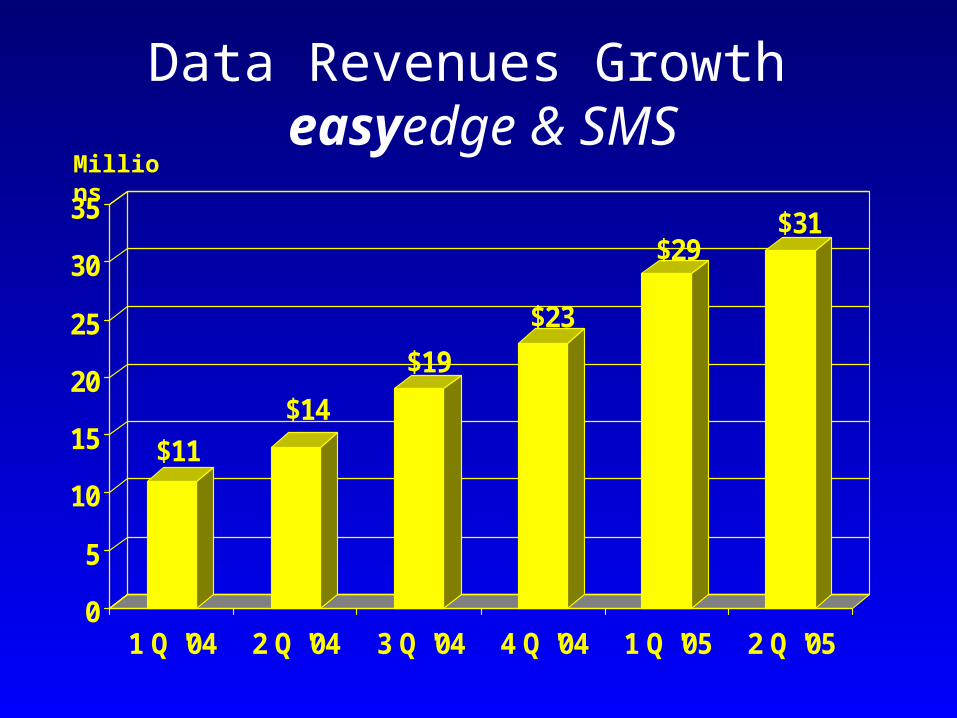

Data Revenues Growth easyedge & SMS

$11

$14

$19

$23

$29$31

0

5

10

15

20

25

30

35

1 Q '04 2 Q '04 3 Q '04 4 Q '04 1 Q '05 2 Q '05

Millions

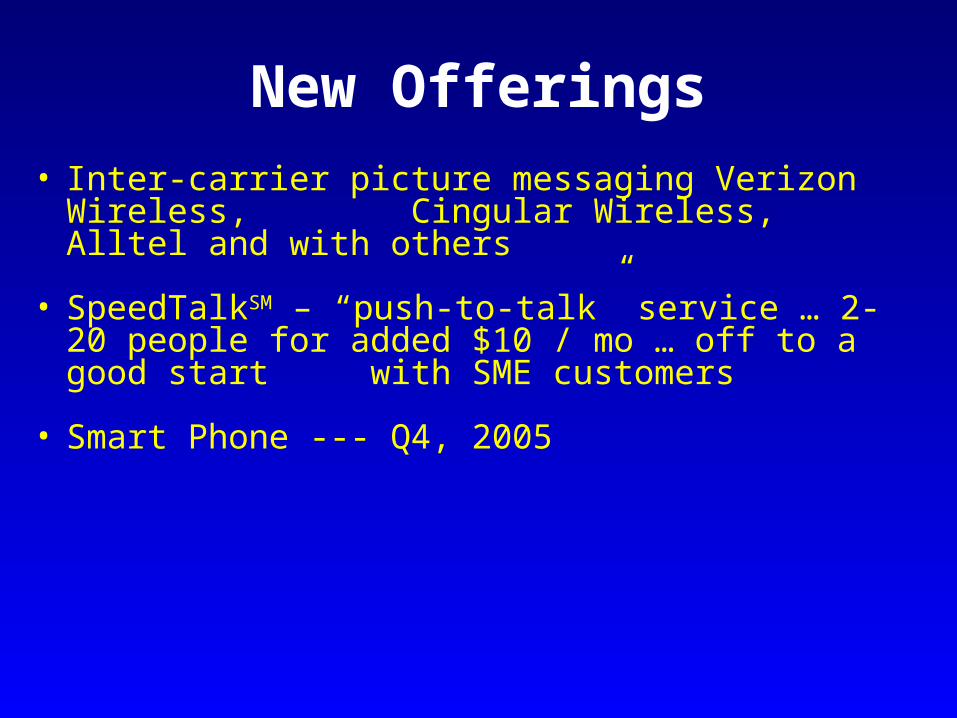

New Offerings• Inter-carrier picture messaging Verizon

Wireless, Cingular Wireless, Alltel and with others

• SpeedTalkSM – “push-to-talk” service … 2-20 people for added $10 / mo … off to a good start with SME customers

• Smart Phone --- Q4, 2005

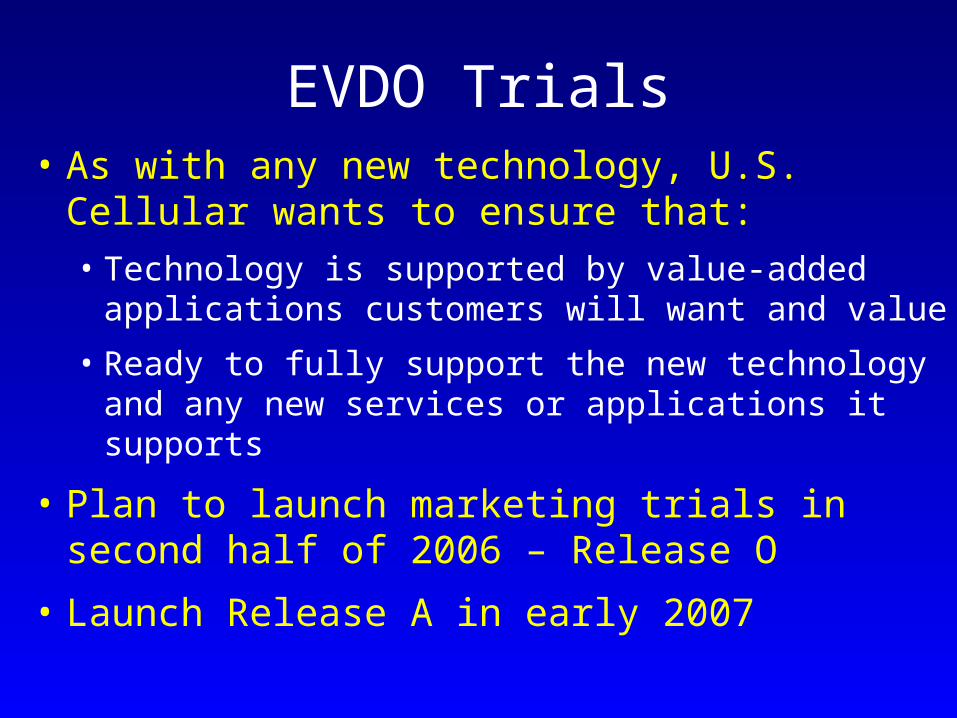

EVDO Trials• As with any new technology, U.S. Cellular

wants to ensure that:

• Technology is supported by value-added applications customers will want and value

• Ready to fully support the new technology and any new services or applications it supports

• Plan to launch marketing trials in second half of 2006 – Release O

• Launch Release A in early 2007

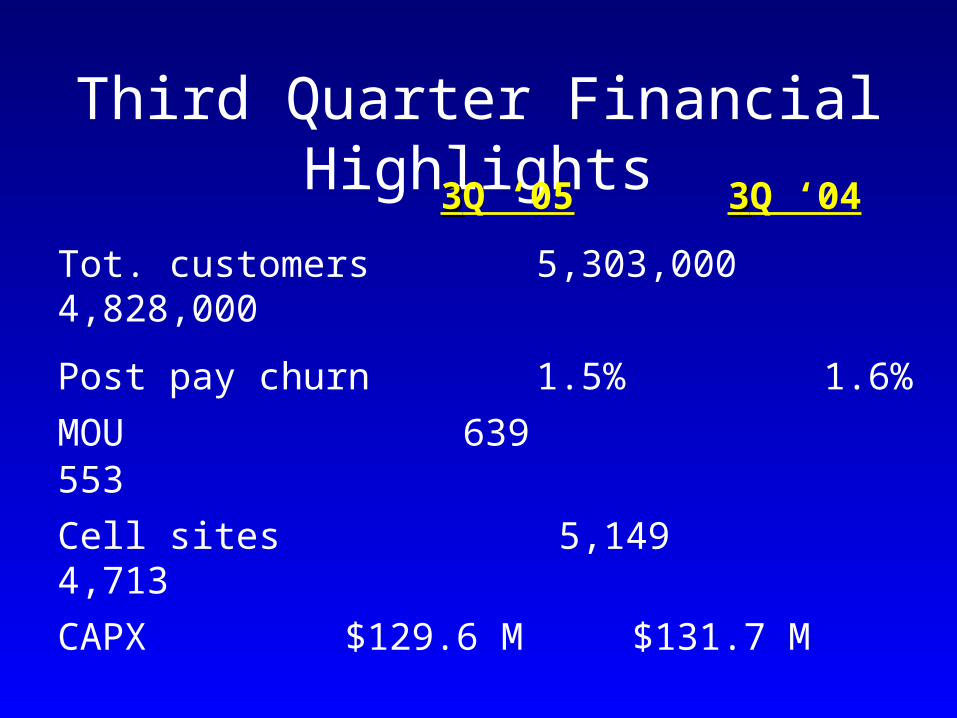

Third Quarter Financial Highlights

33Q ‘05 33Q ‘04

Tot. customers 5,303,000 4,828,000

Post pay churn 1.5% 1.6%

MOU 639 553

Cell sites 5,149 4,713

CAPX $129.6 M $131.7 M

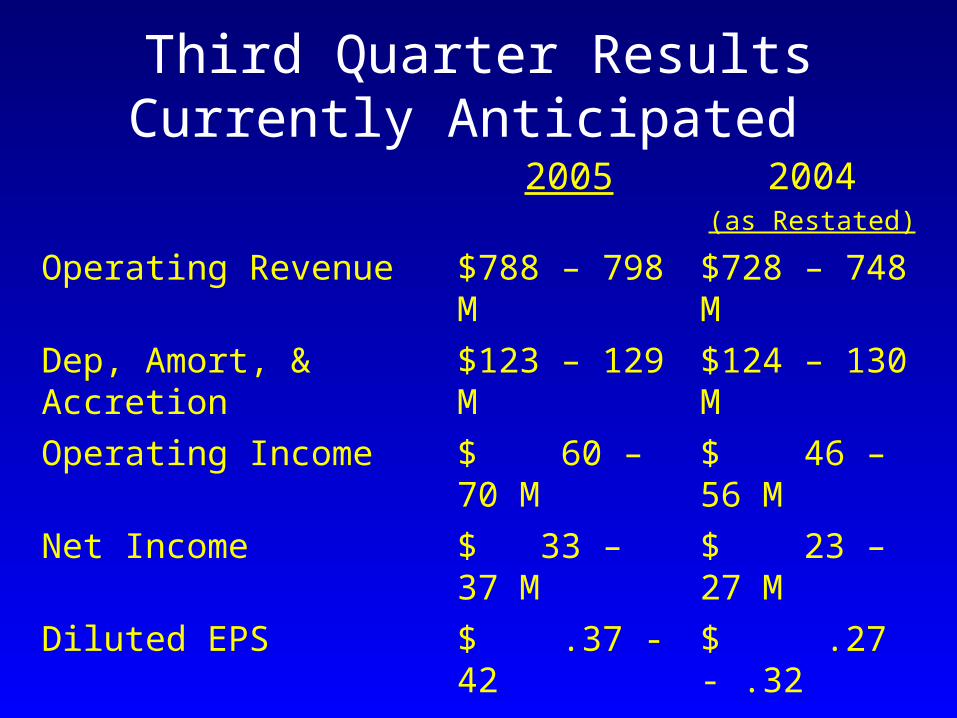

Third Quarter ResultsCurrently Anticipated

2005 2004(as Restated)

Operating Revenue $788 – 798 M $728 – 748 M

Dep, Amort, & Accretion $123 – 129 M $124 – 130 M

Operating Income $ 60 – 70 M $ 46 – 56 M

Net Income $ 33 – 37 M $ 23 – 27 M

Diluted EPS $ .37 - 42 $ .27 - .32

OCF $183 – 199 M $170 – 186 M

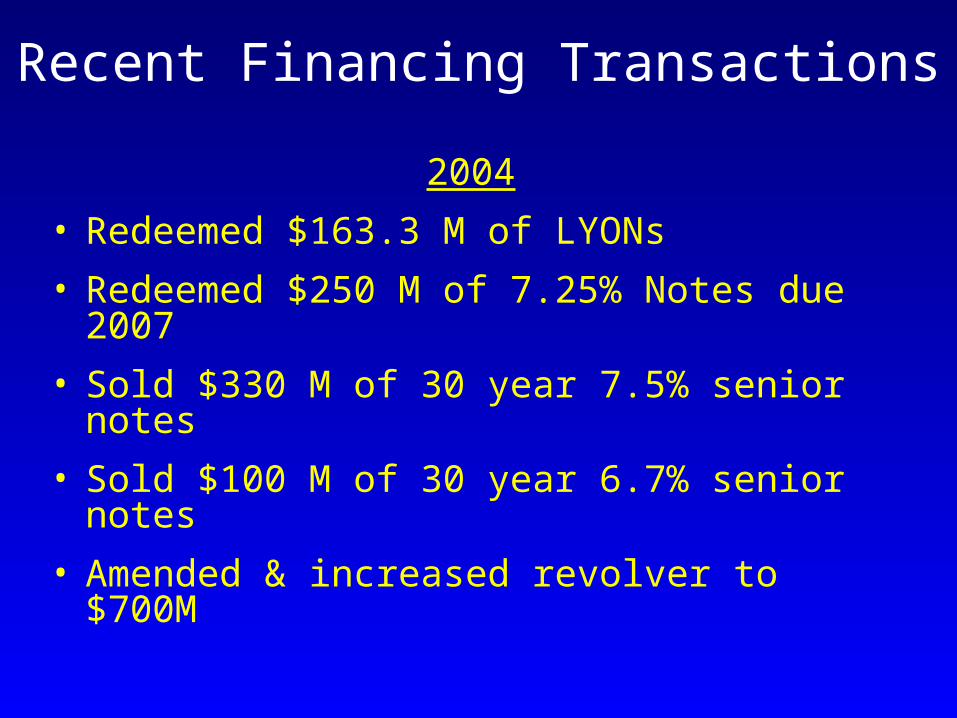

Recent Financing Transactions

2004

• Redeemed $163.3 M of LYONs

• Redeemed $250 M of 7.25% Notes due 2007

• Sold $330 M of 30 year 7.5% senior notes

• Sold $100 M of 30 year 6.7% senior notes

• Amended & increased revolver to $700M

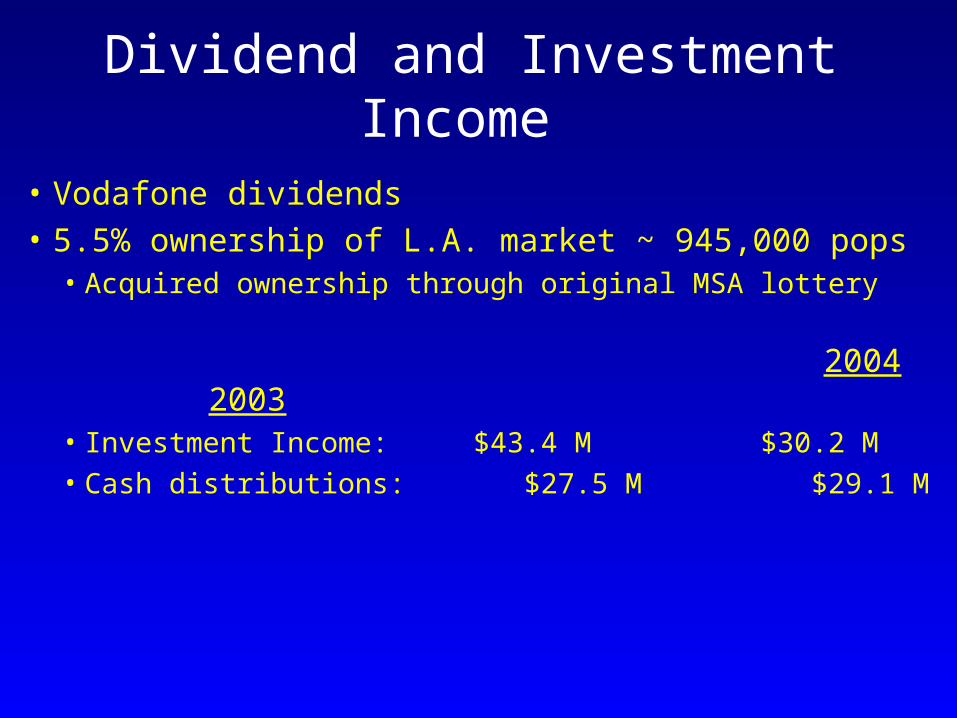

Dividend and Investment Income

• Vodafone dividends

• 5.5% ownership of L.A. market ~ 945,000 pops • Acquired ownership through original MSA lottery

2004 2003• Investment Income: $43.4 M $30.2 M • Cash distributions: $27.5 M $29.1 M

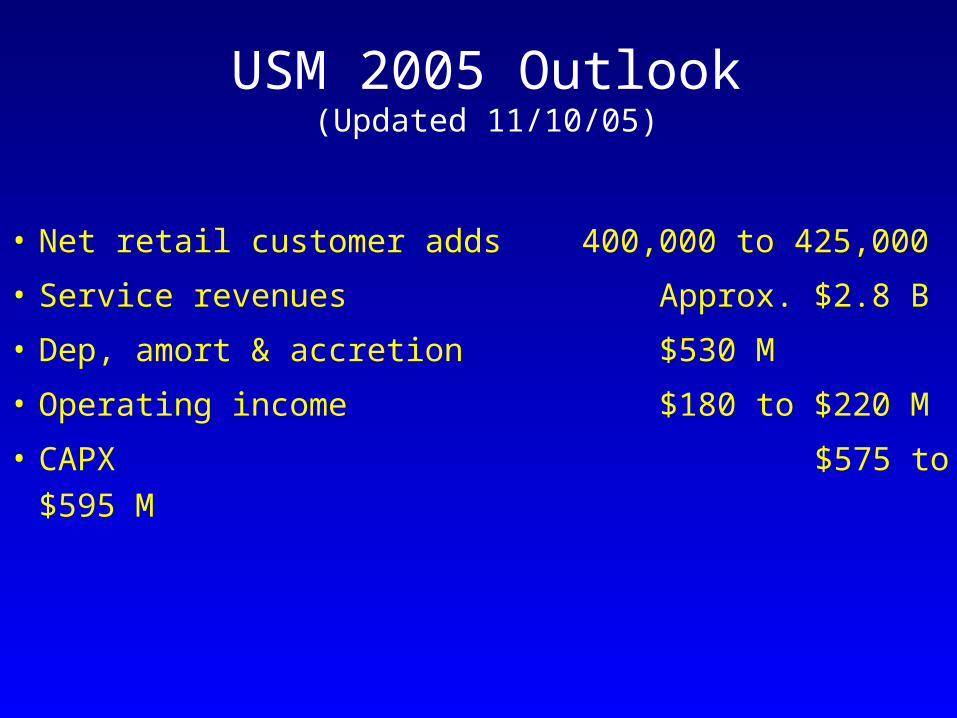

USM 2005 Outlook(Updated 11/10/05)

• Net retail customer adds 400,000 to 425,000

• Service revenues Approx. $2.8 B

• Dep, amort & accretion $530 M

• Operating income $180 to $220 M

• CAPX $575 to $595 M

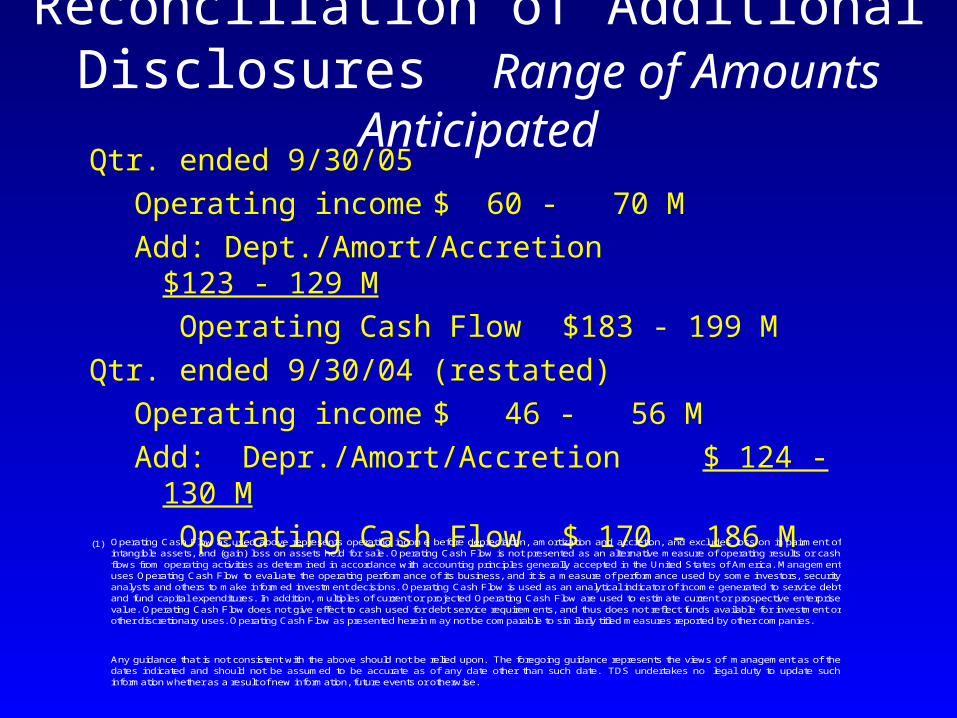

Reconciliation of Additional Disclosures Range of Amounts Anticipated

Qtr. ended 9/30/05

Operating income $ 60 - 70 M

Add: Dept./Amort/Accretion $123 - 129 M

Operating Cash Flow $183 - 199 M

Qtr. ended 9/30/04 (restated)

Operating income $ 46 - 56 M

Add: Depr./Amort/Accretion $ 124 - 130 M

Operating Cash Flow $ 170 - 186 M

(1)

Any guidance that is not consistent with the above should not be relied upon. The foregoing guidance represents the views of management as of thedates indicated and should not be assumed to be accurate as of any date other than such date. TDS undertakes no legal duty to update suchinformation whether as a result of new information, future events or otherwise.

Operating Cash Flow as used above represents operating income before depreciation, amortization and accretion, and excludes loss on impairment ofintangible assets, and (gain) loss on assets held for sale. Operating Cash Flow is not presented as an alternative measure of operating results or cashflows from operating activities as determined in accordance with accounting principles generally accepted in the United States of America. Managementuses Operating Cash Flow to evaluate the operating performance of its business, and it is a measure of performance used by some investors, securityanalysts and others to make informed investment decisions. Operating Cash Flow is used as an analytical indicator of income generated to service debtand fund capital expenditures. In addition, multiples of current or projected Operating Cash Flow are used to estimate current or prospective enterprisevalue. Operating Cash Flow does not give effect to cash used for debt service requirements, and thus does not reflect funds available for investment orother discretionary uses. Operating Cash Flow as presented herein may not be comparable to similarly titled measures reported by other companies.

USM: Excellent Prospects

• Proven strategy

• Financially strong

• Extensive network and distribution

• Terrific people; dynamic organization

• Positive momentum

Chicago White Sox2005 World Champions