26

1 Money and Banking Introduction

1

Money and Banking

Introduction

Week 1 Learning Goals

By the end of the week, you should …Be familiar with the different types of financial instruments and marketsBe aware of the different types businesses that make up the financial systemBe able to distinguish between direct and indirect financeUnderstand the reason for regulation in the financial systemBe able to distinguish between monetary and fiscal policy

2

3

Financial Instruments

Legal contracts specifying the payment of cash flows

4

Some Distinctions

• Primary vs. secondary markets

• Exchanges vs. over-the-counter markets

• Money markets vs. capital markets

5

Exchanges: Single Location

Larger older companies trade on New York Stock Exchange.

6

OTC (over the counter) markets: organized networks of dealers

Newer and small companies trade on NASDAQNationalAssociation ofSecurities DealersAutomatedQuotation System

7

1. Fixed Income Securities (Bonds)

• Corporate

• Municipal

• Treasury

Which ones have the highest and lowest yields?

2. Equities (Stocks)

• Represents ownership with limited liability

8

9

Dow Jones Industrial Average

NASDAQ

10

11

Debt (bonds)

Fixed cash flows (interest).

Principal to be repaid.

Default leads to bankruptcy.

Equity (stock)

Cash flows tied to profits (dividends).

No principal to be repaid.

Investors are residual claimants.

12

3. Money market instruments

• Less than a year in maturity.

• Low risk.

• High denomination.

Examples: Treasury bills, commercial paper, bankers acceptances, repurchase agreements.

4. Derivatives

a) Futures/forwards

b) Options

c) Swaps

By combining these building blocks, an endless number of complex derivatives can be created.

13

14

Eurodollar Futures trading at Chicago Mercantile Exchange

15

In sum …Four Major Financial Instruments

• Bonds (debt, fixed income securities)

• Stock (equities)

• Money market instruments

• Derivatives

16

Why do we need a financial system?

Coordination problem facing savers and businesses requiring capital.

Transactions costs.

17

Financial Intermediaries(Indirect Finance)

•Depository institutions

•Contractual savings institutions (insurance companies, pension funds)

•Investment intermediaries (finance companies, mutual funds)

Indirect finance characterized by asset transformation

• Liquidity transformation

• Maturity transformation

18

19

Broker-Dealers(Direct Finance)

• Sell and buy securities on behalf of clients (brokers)

• Sell and buy for firm’s own account (dealers)

• Issuing securities for corporations (investment banking)

“Wall Street”

• Broker-dealers (e.g., Goldman Sachs)

• Private equity firms (e.g., Blackstone)

• Hedge funds (e.g., Bridgewater)

20

Private Equity : Corporate Raider Rebranded

21

22

Function of Financial Markets

...

Problems in Financial Markets

1. Asymmetric information

Adverse selection

Moral hazard

2. Instability of indirect finance

23

Government’s role in financial markets

• Force disclosure – to deal with problem of asymmetric information

• Lender of last resort – to deal with instability of indirect finance

• Monetary policy—to keep system on an even keel

24

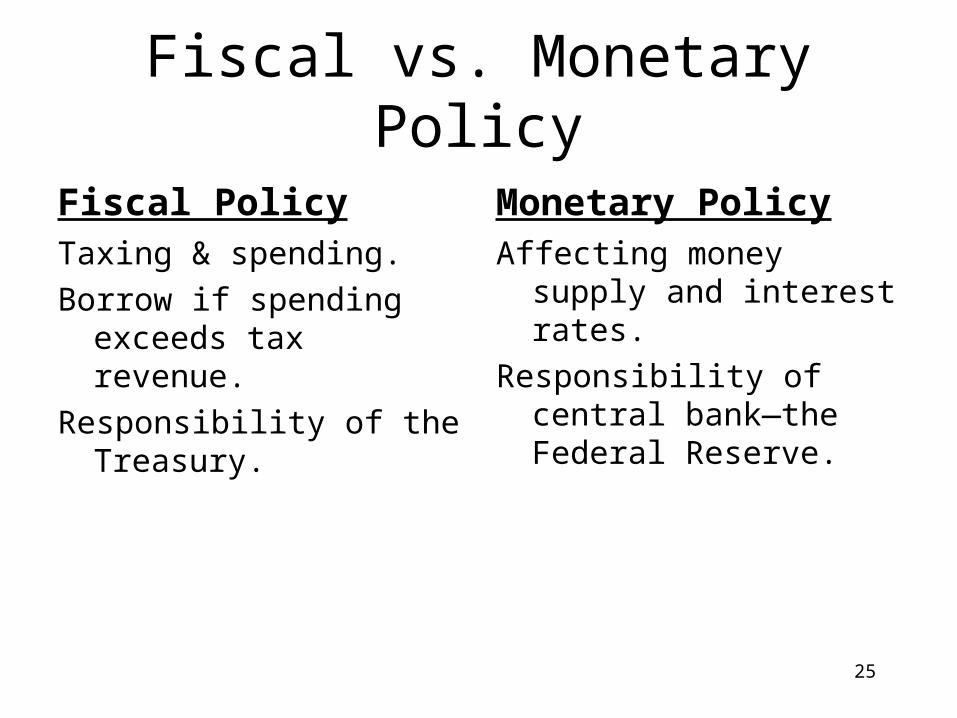

Fiscal vs. Monetary Policy

Fiscal PolicyTaxing & spending.

Borrow if spending exceeds tax revenue.

Responsibility of the Treasury.

Monetary PolicyAffecting money supply and

interest rates.

Responsibility of central bank—the Federal Reserve.

25

26

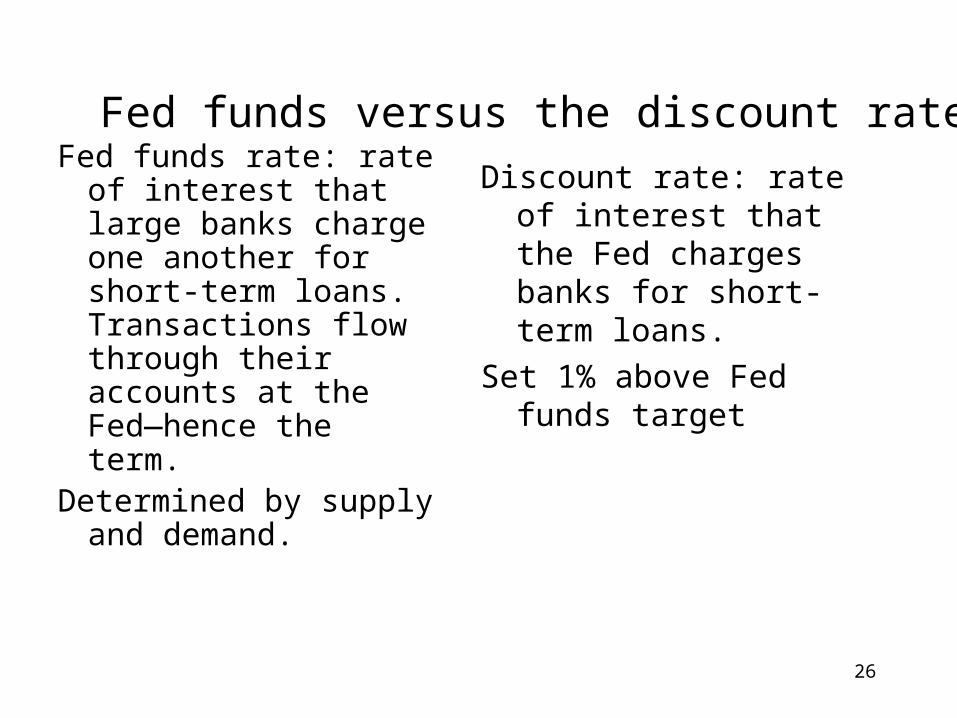

Fed funds rate: rate of interest that large banks charge one another for short-term loans. Transactions flow through their accounts at the Fed—hence the term.

Determined by supply and demand.

Discount rate: rate of interest that the Fed charges banks for short-term loans.

Set 1% above Fed funds target

Fed funds versus the discount rate