1 Overview of the Overview of the Leveraging Concept in Leveraging Concept in Economic Development Economic Development Prepared for the Prepared for the California Integrated California Integrated Waste Management Board Waste Management Board Victor Hoskins Victor Hoskins Vice President Vice President UrbanAmerica, LP UrbanAmerica, LP August 12, 2002 August 12, 2002

Transcript

1

Overview of the Leveraging Overview of the Leveraging Concept in Economic Concept in Economic

DevelopmentDevelopmentPrepared for the California Integrated Prepared for the California Integrated

Waste Management BoardWaste Management Board

Victor HoskinsVictor Hoskins

Vice PresidentVice President

UrbanAmerica, LPUrbanAmerica, LP

August 12, 2002August 12, 2002

2

OverviewOverview DefinitionDefinition

GoalGoal

ProblemProblem

SolutionSolution

3

Definition:What is Leveraging?Definition:What is Leveraging?

Merrian-WebsterMerrian-Webster The use of credit to enhance one’s speculative capacity The use of credit to enhance one’s speculative capacity

Irving Bonios Co. Real Estate DictionaryIrving Bonios Co. Real Estate Dictionary The use of financing to allow a small amount of cash to The use of financing to allow a small amount of cash to

purchase a large property investmentpurchase a large property investment

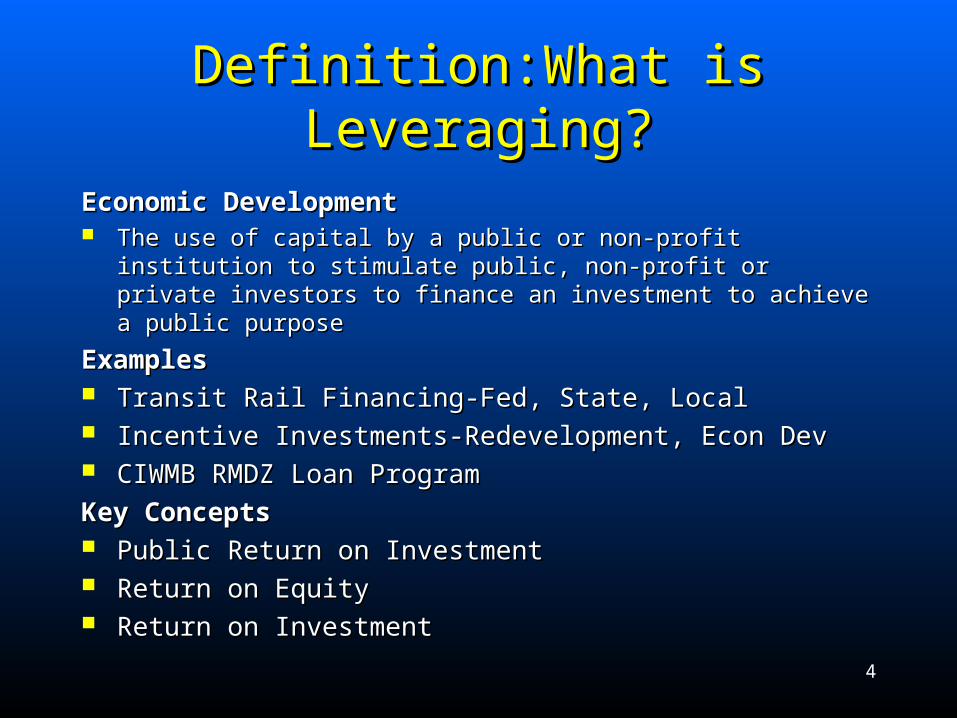

Economic DevelopmentEconomic Development The use of capital by a public or non-profit institution to The use of capital by a public or non-profit institution to

stimulate public, non-profit or private investors to finance stimulate public, non-profit or private investors to finance an investment to achieve a public purposean investment to achieve a public purpose

4

Definition:What is Leveraging?Definition:What is Leveraging?

Economic DevelopmentEconomic Development The use of capital by a public or non-profit institution to stimulate public, non-The use of capital by a public or non-profit institution to stimulate public, non-

profit or private investors to finance an investment to achieve a public purposeprofit or private investors to finance an investment to achieve a public purpose

ExamplesExamples Transit Rail Financing-Fed, State, LocalTransit Rail Financing-Fed, State, Local Incentive Investments-Redevelopment, Econ DevIncentive Investments-Redevelopment, Econ Dev CIWMB RMDZ Loan ProgramCIWMB RMDZ Loan Program

Key ConceptsKey Concepts Public Return on InvestmentPublic Return on Investment Return on EquityReturn on Equity Return on InvestmentReturn on Investment

5

Goal:What is the Challenge?Goal:What is the Challenge?

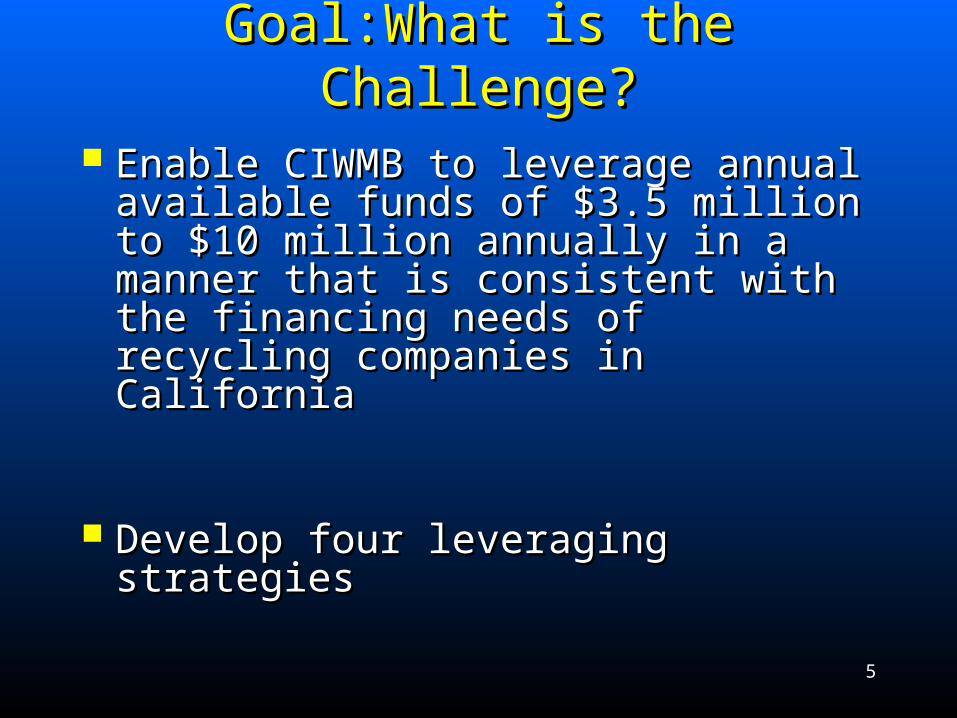

Enable CIWMB to leverage annual Enable CIWMB to leverage annual available funds of $3.5 million to $10 available funds of $3.5 million to $10 million annually in a manner that is million annually in a manner that is consistent with the financing needs of consistent with the financing needs of recycling companies in Californiarecycling companies in California

Develop four leveraging strategiesDevelop four leveraging strategies

6

Goal:What is the Challenge?Goal:What is the Challenge?

Creating a Sustainable Financing ProgramCreating a Sustainable Financing Program Leveraging existing and anticipated resourcesLeveraging existing and anticipated resources Blending RMDZ funds with investment Blending RMDZ funds with investment

resources from Private or Public resources from Private or Public organizations to reduce waste by meeting the organizations to reduce waste by meeting the financing requirements of recycling financing requirements of recycling businessesbusinesses

Discussion of Leveraging Options Discussion of Leveraging Options for the RMDZ Loan Programfor the RMDZ Loan Program

Prepared for the California Integrated Prepared for the California Integrated Waste Management BoardWaste Management Board

Betsy Zeidman, Milken InstituteBetsy Zeidman, Milken Institute

Paul Pryde, Capital Access GroupPaul Pryde, Capital Access Group

Bill Schmidt, Milken InstituteBill Schmidt, Milken Institute

August 12, 2002August 12, 2002

9

OverviewOverview GoalGoal

MethodologyMethodology

Market ResearchMarket Research

Leveraging StrategiesLeveraging Strategies

10

GoalGoal

Enable CIWMB to leverage annual Enable CIWMB to leverage annual available funds of $3.5 million to $10 available funds of $3.5 million to $10 million annually in a manner that is million annually in a manner that is consistent with the financing needs of consistent with the financing needs of recycling companies in Californiarecycling companies in California

11

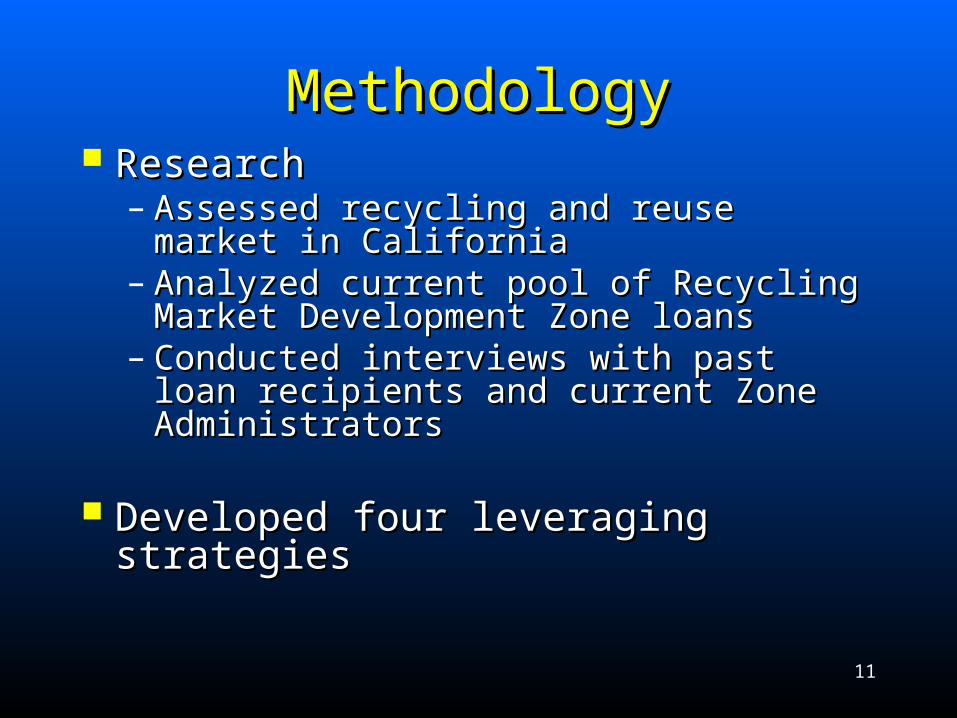

MethodologyMethodology ResearchResearch

– Assessed recycling and reuse market in Assessed recycling and reuse market in CaliforniaCalifornia

– Analyzed current pool of Recycling Market Analyzed current pool of Recycling Market Development Zone loansDevelopment Zone loans

– Conducted interviews with past loan recipients Conducted interviews with past loan recipients and current Zone Administratorsand current Zone Administrators

Developed four leveraging strategiesDeveloped four leveraging strategies

12

Key Findings from Industry Key Findings from Industry ResearchResearch

13

Key Findings from Market Research:Key Findings from Market Research:

Recycling and reuse is a $14 billion industry Recycling and reuse is a $14 billion industry in Californiain California

$55,910,300 have been made in loans through $55,910,300 have been made in loans through RMDZ programRMDZ program– Growth stage of companies in loan poolGrowth stage of companies in loan pool

– Use of loan proceedsUse of loan proceeds

– Average interest rate of loan poolAverage interest rate of loan pool

14

Key Findings from Industry Research:Key Findings from Industry Research:Barriers to Access and Use of Current ProgramBarriers to Access and Use of Current Program

Collateral requirementsCollateral requirements Timing of interest paymentsTiming of interest payments Replenishment of loan poolReplenishment of loan pool Financial incentives to increase level of Financial incentives to increase level of

participationparticipation Perceptions of confidentialityPerceptions of confidentiality

15

Key Findings from Industry Research:Key Findings from Industry Research:Top Current Financing SourcesTop Current Financing Sources

Private InvestmentPrivate Investment

Private LendingPrivate Lending

Government and CharitableGovernment and Charitable

16

Overview and Discussion of Overview and Discussion of Leveraging StrategiesLeveraging Strategies

17

Criteria Used to Evaluate Leveraging Criteria Used to Evaluate Leveraging StrategiesStrategies

Financing CapacityFinancing Capacity

Financial StabilityFinancial Stability

Market ResponsivenessMarket Responsiveness

Customer FriendlinessCustomer Friendliness

AffordabilityAffordability

18

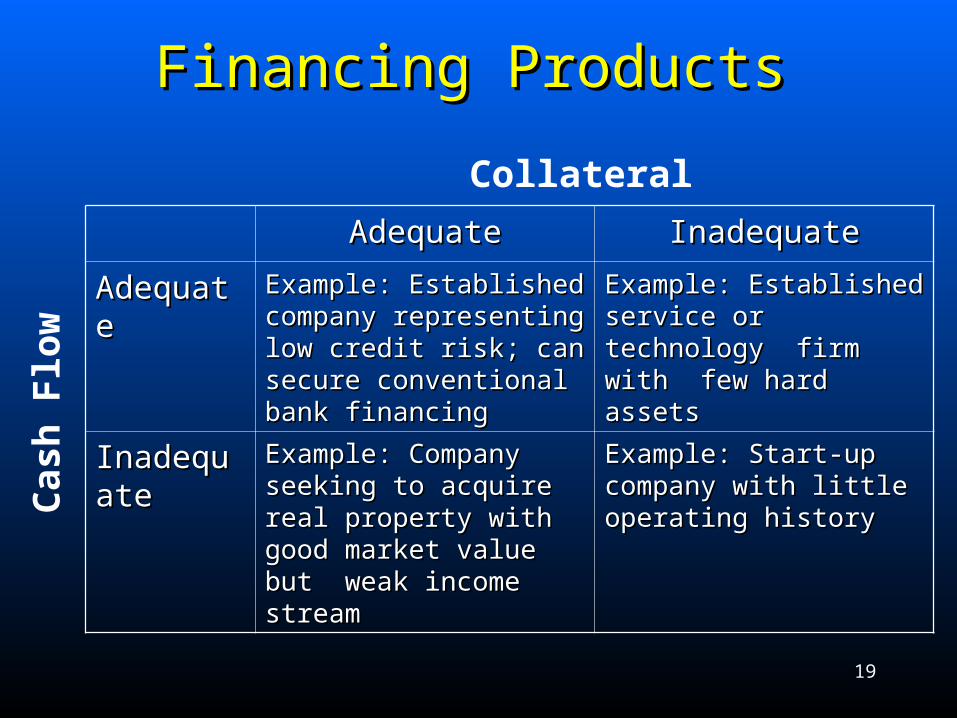

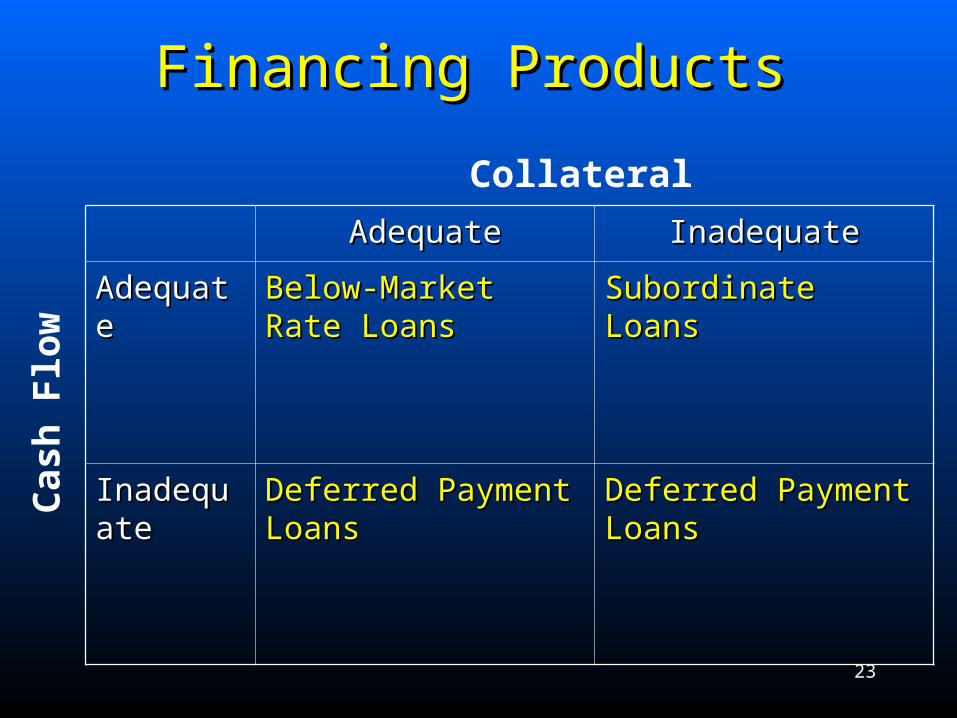

Capital NeedsCapital Needs Types of CapitalTypes of Capital

– EquityEquity– DebtDebt

» SubordinatedSubordinated» SeniorSenior

Dependent on Growth StageDependent on Growth Stage– Development-stage and small low-growth Development-stage and small low-growth

AdequateAdequate Example: Established Example: Established company representing low company representing low credit risk; can secure credit risk; can secure conventional bank financingconventional bank financing

Example: Established service Example: Established service or technology firm with few or technology firm with few hard assetshard assets

InadequateInadequate Example: Company seeking Example: Company seeking to acquire real property with to acquire real property with good market value but weak good market value but weak income streamincome stream

Example: Start-up company Example: Start-up company with little operating historywith little operating history

Example: Established service Example: Established service or technology firm with few or technology firm with few hard assetshard assets

InadequateInadequate Example: Company seeking Example: Company seeking to acquire real property with to acquire real property with good market value but weak good market value but weak income streamincome stream

Example: Start-up company Example: Start-up company with little operating historywith little operating history

InadequateInadequate Example: Company seeking Example: Company seeking to acquire real property with to acquire real property with good market value but weak good market value but weak income streamincome stream

Example: Start-up company Example: Start-up company with little operating historywith little operating history

InadequateInadequate Deferred Payment LoansDeferred Payment Loans Example: Start-up company Example: Start-up company with little operating historywith little operating history

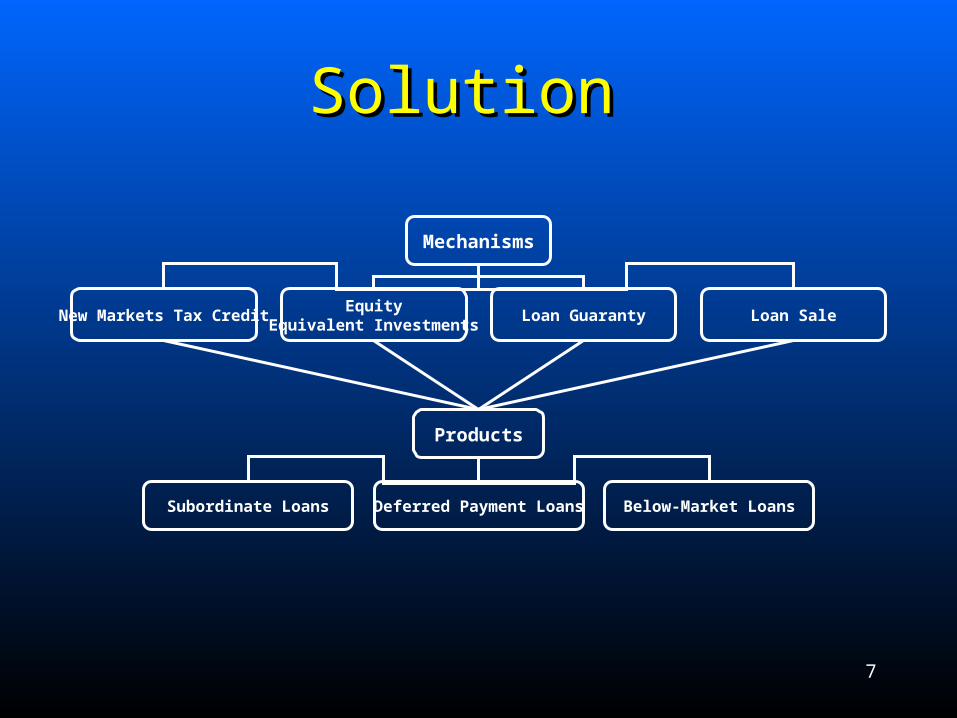

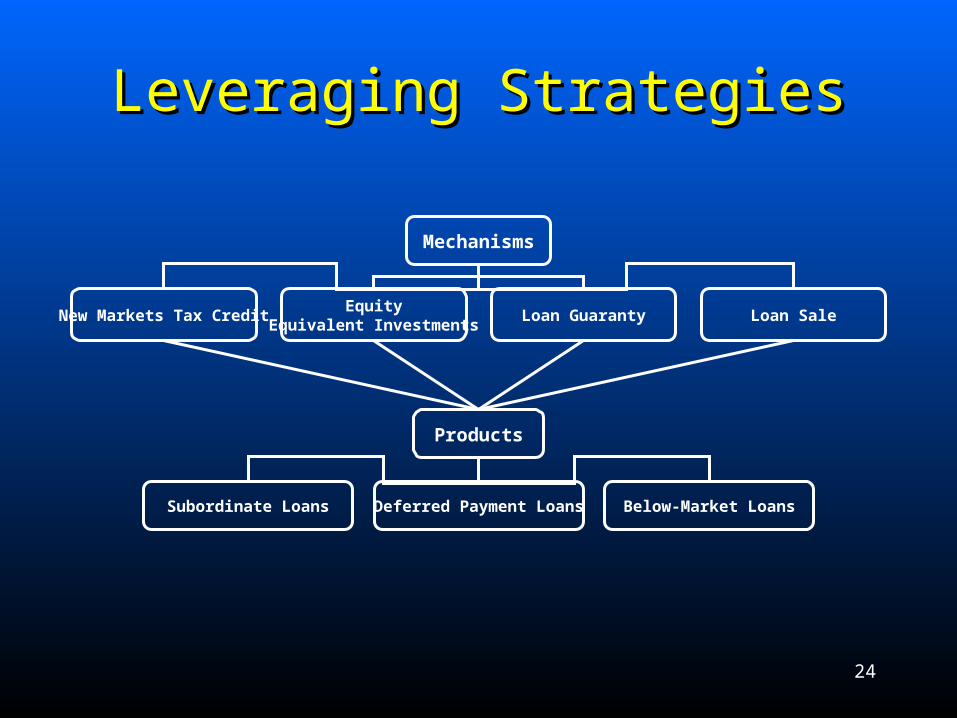

All strategies use same three productsAll strategies use same three products All strategies can be done in isolation or All strategies can be done in isolation or

combinedcombined All strategies leverage Board’s $3.5 million into All strategies leverage Board’s $3.5 million into

$10 million of loanable funds on a sustainable $10 million of loanable funds on a sustainable basisbasis

Current:Current:– Established 48%Established 48%

– Early-Stage 38%Early-Stage 38%

– Start-Up 14%Start-Up 14%

Target:Target:– Established 50%Established 50%

– Early-Stage 30%Early-Stage 30%

– Start-Up 20%Start-Up 20%

26

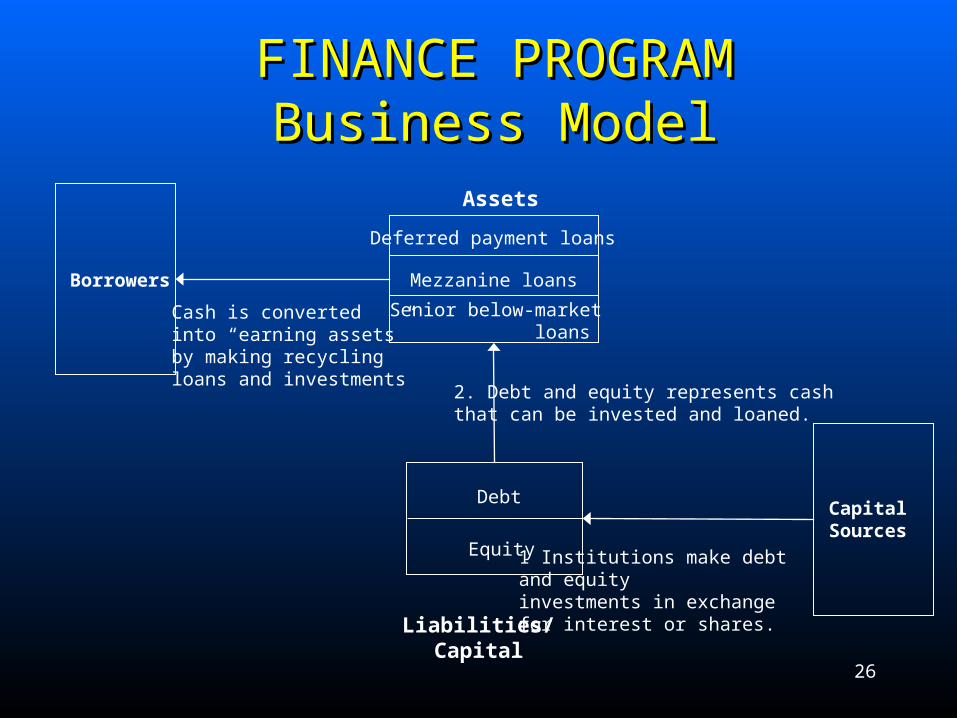

Mezzanine loans

CapitalSources

Debt

Equity

Liabilities/Capital

Assets

Deferred payment loans

Senior below-market loans

Borrowers

1 Institutions make debt and equity investments in exchangefor interest or shares.

2. Debt and equity represents cash that can be invested and loaned.

Cash is convertedinto “earning assets”by making recyclingloans and investments

FINANCE PROGRAMFINANCE PROGRAMBusiness ModelBusiness Model

27

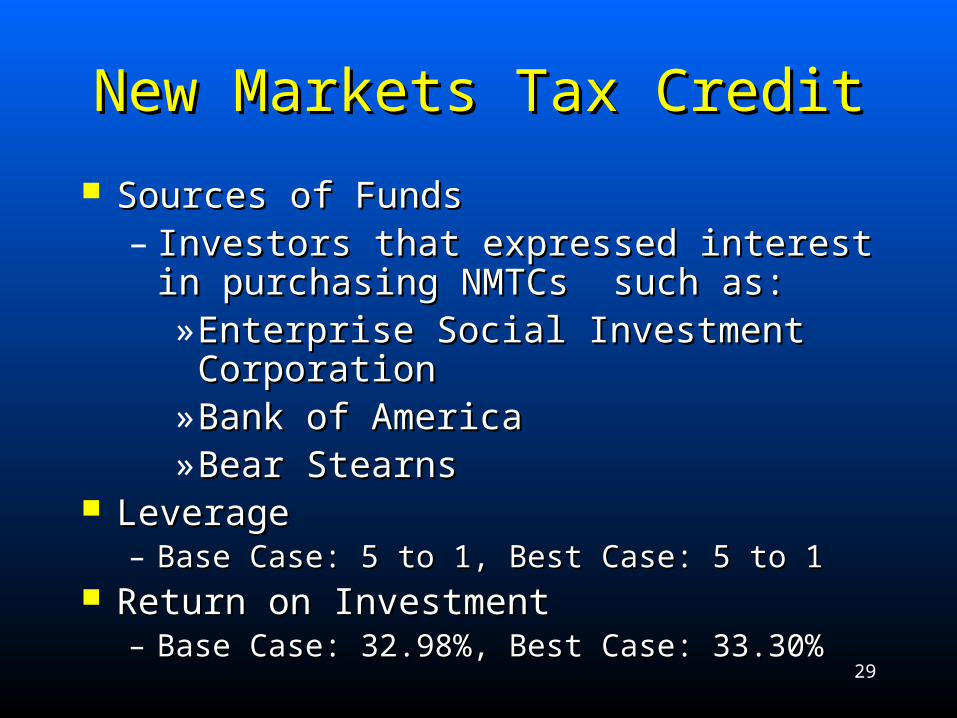

New Markets Tax CreditNew Markets Tax Credit

A new federal incentive program under A new federal incentive program under which taxpayers are allowed to reduce their which taxpayers are allowed to reduce their federal income tax payments by 39 percent federal income tax payments by 39 percent of the amount invested in a qualifying of the amount invested in a qualifying Community Development Entity (CDE)– a Community Development Entity (CDE)– a for-profit organization that makes business for-profit organization that makes business loans and investments in low-income areas.loans and investments in low-income areas.

28

New Markets Tax CreditNew Markets Tax Credit

Investors

Lender CDE BoardMakes $10 millionmarket-rate loan

Invests $30 million inexchange for $11.7Million (39%) NMTC

Makes $10 millionlong term loan (funded over 3 years)

29

New Markets Tax CreditNew Markets Tax Credit

Sources of FundsSources of Funds– Investors that expressed interest in purchasing Investors that expressed interest in purchasing

NMTCs such as:NMTCs such as:» Enterprise Social Investment CorporationEnterprise Social Investment Corporation» Bank of AmericaBank of America» Bear StearnsBear Stearns

LeverageLeverage– Base Case: 5 to 1, Best Case: 5 to 1Base Case: 5 to 1, Best Case: 5 to 1

Return on InvestmentReturn on Investment– Base Case: 32.98%, Best Case: 33.30%Base Case: 32.98%, Best Case: 33.30%

30

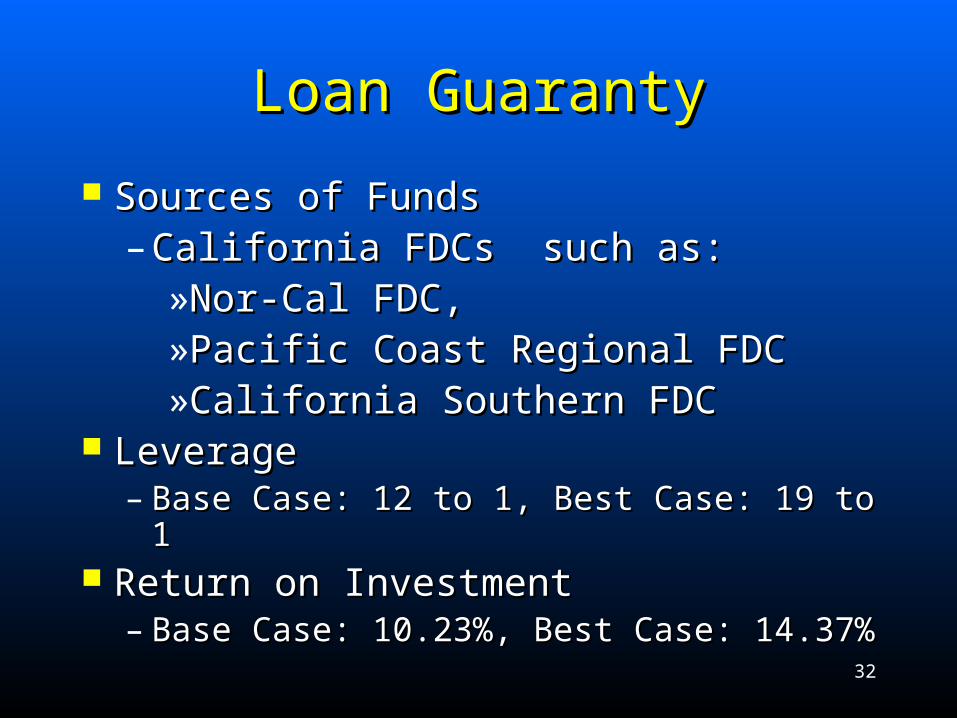

Loan GuarantyLoan Guaranty

A risk-sharing partnership between A risk-sharing partnership between CIWMB and one or more existing small CIWMB and one or more existing small business loan guarantors – preferably with a business loan guarantors – preferably with a California Financial Development California Financial Development Corporation (FDC) that provide guaranties Corporation (FDC) that provide guaranties of up to 80 percent on small business bank of up to 80 percent on small business bank loans of up to $350,000.loans of up to $350,000.

31

Loan GuarantyLoan Guaranty

Lenders

BoardSmall BusinessExpansion Fund

1. Contributes $3 million

Borrowers

2. Provides up to $12 million in guarantees

3. Provides up to $12 million in loans

32

Loan GuarantyLoan Guaranty

Sources of FundsSources of Funds– California FDCs such as:California FDCs such as:

LeverageLeverage– Base Case: 12 to 1, Best Case: 19 to 1Base Case: 12 to 1, Best Case: 19 to 1

Return on InvestmentReturn on Investment– Base Case: 10.23%, Best Case: 14.37%Base Case: 10.23%, Best Case: 14.37%

33

Loan SaleLoan Sale

Selling loans to secondary market investors, Selling loans to secondary market investors, such as the Community Reinvestment Fund, such as the Community Reinvestment Fund, and using the cash to make more loans. and using the cash to make more loans. Interest rates on the loans would be Interest rates on the loans would be structured so that loans would be sold at a structured so that loans would be sold at a premium.premium.

34

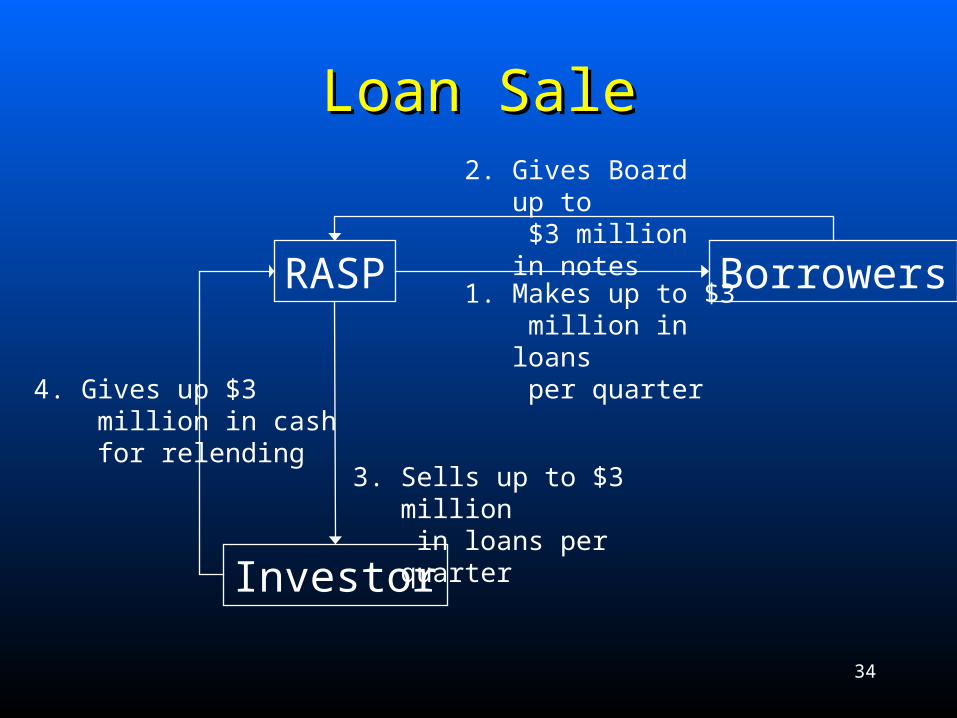

Loan SaleLoan Sale

RASP

Investor

Borrowers

2. Gives Board up to $3 million in notes

3. Sells up to $3 million in loans per quarter

1. Makes up to $3 million in loans per quarter

4. Gives up $3 million in cash for relending

35

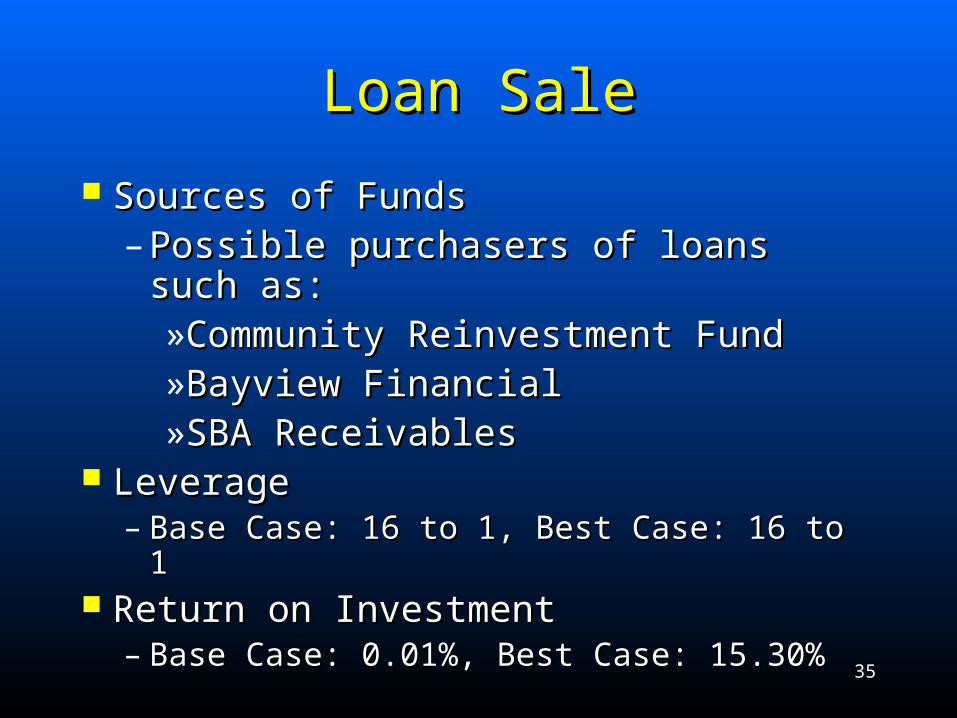

Loan SaleLoan Sale

Sources of FundsSources of Funds– Possible purchasers of loans such as:Possible purchasers of loans such as:

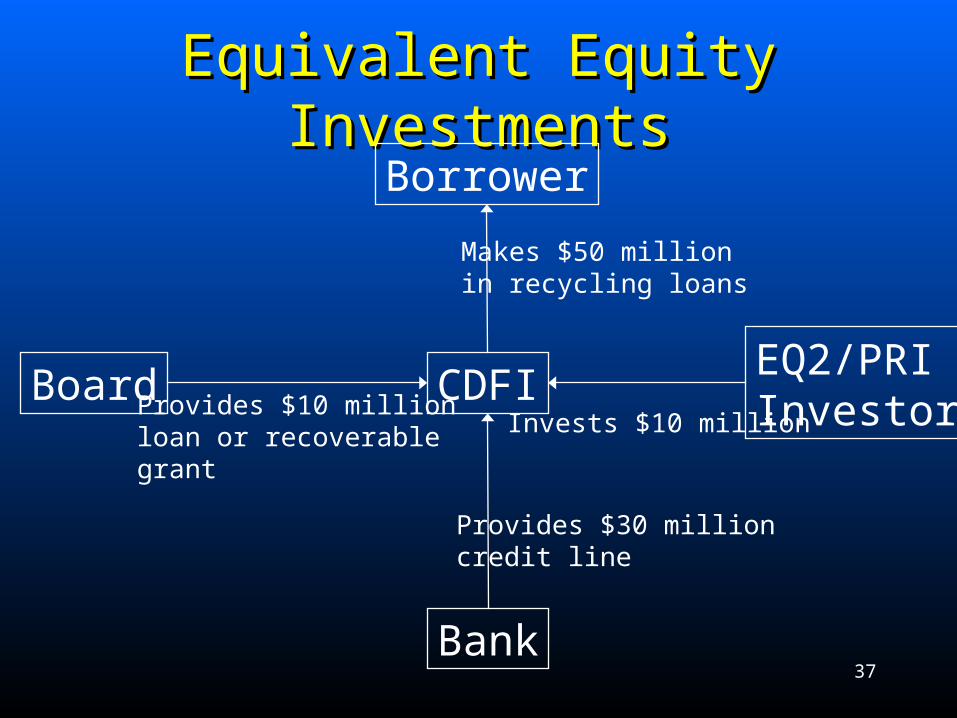

Forming a financing partnership with an Forming a financing partnership with an established non-profit Certified established non-profit Certified Development Financial Institution (CDFI) Development Financial Institution (CDFI) that would agree to use funds obtained that would agree to use funds obtained through PRIs, low-interest loans that through PRIs, low-interest loans that foundations provide, or EQ2s, long-term, foundations provide, or EQ2s, long-term, low interest loans made by commercial low interest loans made by commercial banks to community development banks to community development organizations. organizations.

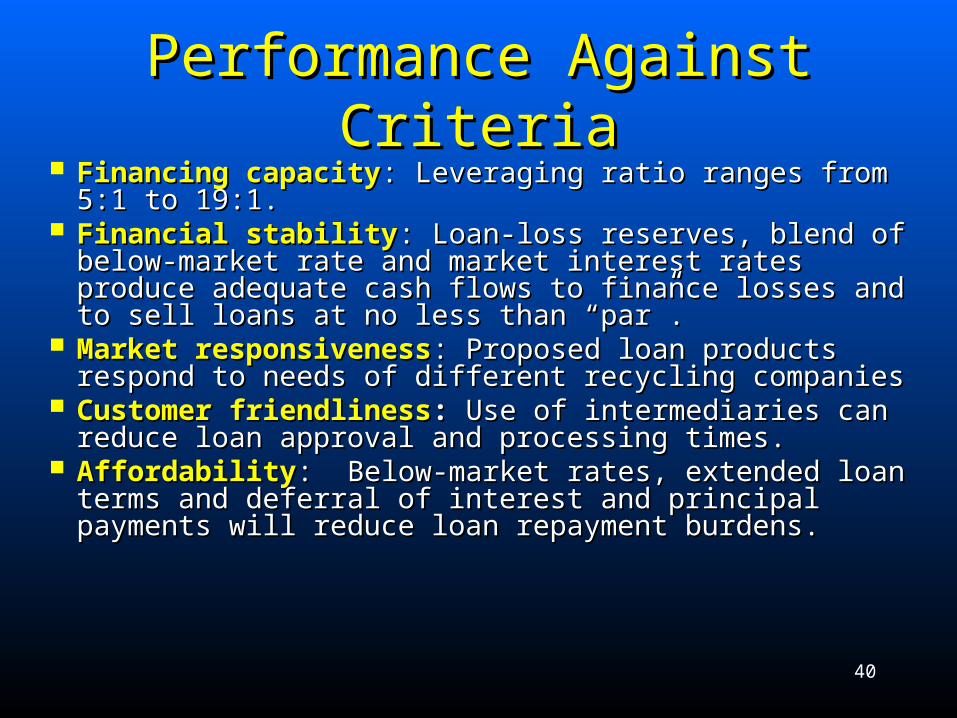

Performance Against CriteriaPerformance Against Criteria Financing capacityFinancing capacity: Leveraging ratio ranges from 5:1 to : Leveraging ratio ranges from 5:1 to

19:1. 19:1. Financial stabilityFinancial stability: Loan-loss reserves, blend of below-: Loan-loss reserves, blend of below-

market rate and market interest rates produce adequate market rate and market interest rates produce adequate cash flows to finance losses and to sell loans at no less cash flows to finance losses and to sell loans at no less than “par”. than “par”.

Market responsivenessMarket responsiveness: Proposed loan products respond : Proposed loan products respond to needs of different recycling companiesto needs of different recycling companies

Customer friendlinessCustomer friendliness:: Use of intermediaries can reduce Use of intermediaries can reduce loan approval and processing times. loan approval and processing times.

AffordabilityAffordability: Below-market rates, extended loan terms : Below-market rates, extended loan terms and deferral of interest and principal payments will reduce and deferral of interest and principal payments will reduce loan repayment burdens. loan repayment burdens.

41

Discussion of Leveraging Options Discussion of Leveraging Options for the RMDZ Loan Programfor the RMDZ Loan Program

Prepared for the California Integrated Prepared for the California Integrated Waste Management BoardWaste Management Board

Betsy Zeidman, Milken InstituteBetsy Zeidman, Milken Institute

Paul Pryde, Capital Access GroupPaul Pryde, Capital Access Group

Bill Schmidt, Milken InstituteBill Schmidt, Milken Institute