30

1 Philanthropy and Government Funding

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 216 times |

| Download: | 0 times |

1

Philanthropy and Government Funding

2

Outline

• Private giving• Government support

3

Individuals Give the Bulk of Donations

Ref.: Oster 1985

4

Religion Gets the Biggest Part of Donations

5

Percent of Income Givenby State*

State Charity as a % of AGI Average level of charity State Charity as a % of AGI Average level of charityUtah 6.2% $5,347 California 2.7% $2,307Alabama 4.3% $3,656 Delaware 2.7% $2,338Mississippi 4.3% $3,699 Indiana 2.7% $2,301Tennessee 4.3% $3,713 Michigan 2.7% $2,299Arkansas 3.9% $3,314 New York 2.7% $2,283South Carolina 3.8% $3,248 West Virginia 2.7% $2,273Louisiana 3.6% $3,086 Illinois 2.6% $2,219Oklahoma 3.6% $3,062 Iowa 2.6% $2,184D.C. 3.5% $3,052 Montana 2.6% $2,177Georgia 3.5% $3,016 Nevada 2.6% $2,202Texas 3.5% $3,024 Pennsylvania 2.6% $2,189Idaho 3.4% $2,949 Washington 2.6% $2,226North Carolina 3.4% $2,938 Colorado 2.5% $2,111South Dakota 3.4% $2,864 Minnesota 2.5% $2,172Florida 3.2% $2,723 Ohio 2.5% $2,114Maryland 3.1% $2,678 Oregon 2.5% $2,127Kansas 3.0% $2,532 Hawaii 2.4% $2,096Wyoming 3.0% $2,599 New Jersey 2.4% $2,110Kentucky 2.9% $2,487 Wisconsin 2.1% $1,798Nebraska 2.9% $2,481 Connecticut 2.0% $1,740Alaska 2.8% $2,408 Maine 2.0% $1,677Arizona 2.8% $2,380 Rhode Island 2.0% $1,709Missouri 2.8% $2,361 Vermont 1.9% $1,611New Mexico 2.8% $2,413 Massachusetts 1.8% $1,591North Dakota 2.8% $2,421 New Hampshire 1.8% $1,536Virginia 2.8% $2,451 U.S. average 2.8% $2,423

*Taxpayers earning $75,000-$100,000 Ref.: Chronicle of Philanthropy, 8-8-02

6

What Is Associated with Charitable Giving?

Ref.: PB&F 2002

Gender: Effect depends on income

Variable Most common direction of effect on giving

Taxes Positive

Income Positive

Wealth Positive

Race Insignificant

Education Positive

Age Positive

Family size Negative

Marital status Positive or insignificant

7

The Role of Religion

Charity measure Religious people

Secular people

t-statistic

GIVES 0.91 0.66 293*

VOLUNTEERS 0.67 0.44 137*

VALUE OF GIFTS $2,210 $642 88*

GIVES TO NON-RELIGIOUS CAUSES

0.71 0.61 141*

VOLUNTEERS TO NON-RELIGIOUS CAUSES

0.60 0.39 121*

Ref.: 2000 SCCBS

8

Informal Giving

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Money Time Blood Help tohomeless

Place inline

Mistakenchange

Empatheticattitudes

Religious

All

Secular

Data: 2002 GSS

9

Nature vs. Nurture

• A “God and Giving Gene”?– .25-.50 of “innate religiosity”

appears to be genetic– Why not innate charity as well?

• Learning hypothesis– Giving is a learned behavior, and

religious communities teach it

10

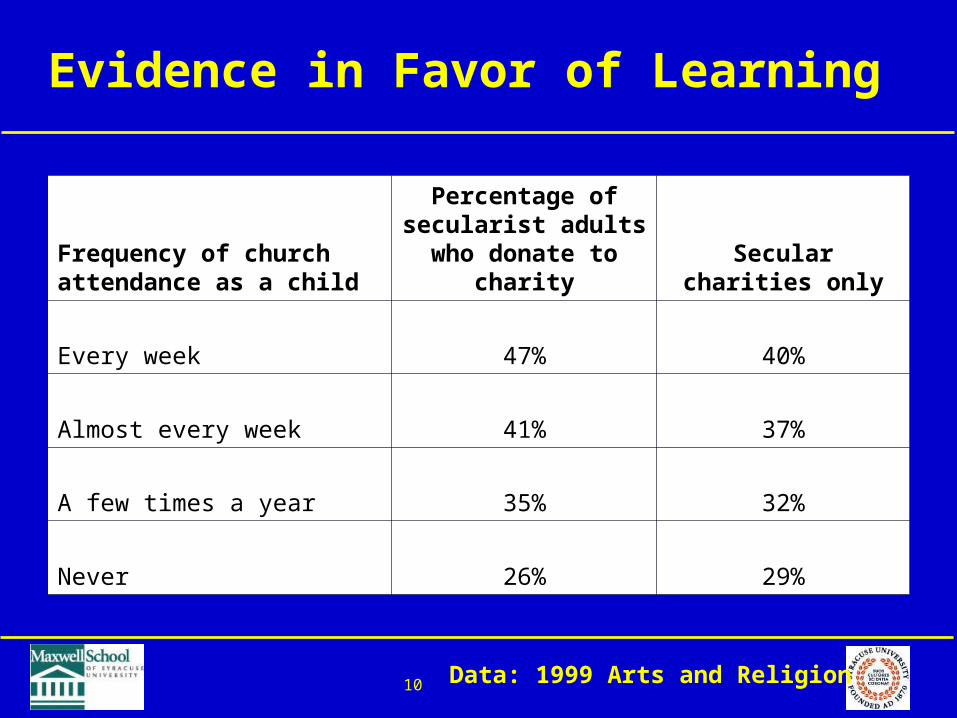

Evidence in Favor of Learning

Frequency of church attendance as a child

Percentage of secularist adults who donate to

charitySecular charities

only

Every week 47% 40%

Almost every week 41% 37%

A few times a year 35% 32%

Never 26% 29%

Data: 1999 Arts and Religion

11

What Is “Religious”?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

People who devote “a

great deal of effort” to

their spiritual lives

People who devote

“no effort” to their

spiritual lives

Gives to all causes

Gives to nonreligious

causes

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

People who belong to ahouse of worship

People who do notbelong to a house of

worship

Data: 1999 Arts and Religion

12

Evidence in Favor of Learning

Frequency of church attendance as a child

Percentage of secularist adults who donate to

charitySecular charities

only

Every week 47% 40%

Almost every week 41% 37%

A few times a year 35% 32%

Never 26% 29%

Data: 1999 Arts and Religion

13

The Importance of Family

51%

56%

61%

46%

48%

50%

52%

54%

56%

58%

60%

62%

1 2 3 to 6

Family size

Per

cen

tag

e vo

lun

teer

ing

14

Families teach giving behavior

56%

38%

0%

10%

20%

30%

40%

50%

60%

Parents volunteered Parents did not volunteer

Per

cen

tag

e o

f ad

ult

s w

ho

vo

lun

teer

15

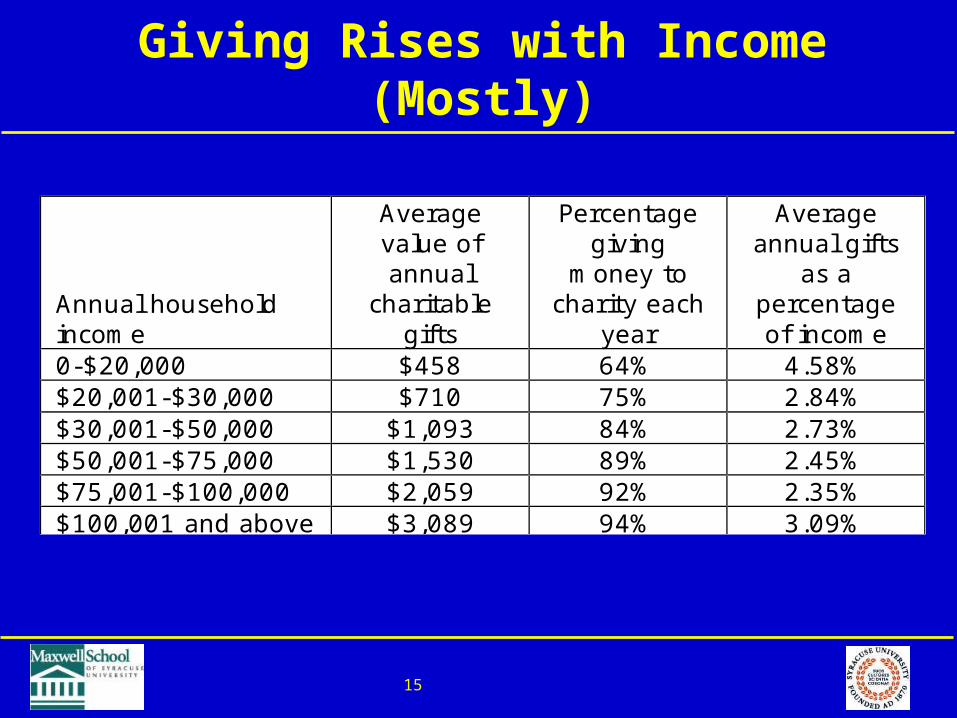

Giving Rises with Income (Mostly)

Annual household income

Average value of annual

charitable gifts

Percentage giving

money to charity each

year

Average annual gifts

as a percentage of income

0-$20,000 $458 64% 4.58% $20,001-$30,000 $710 75% 2.84% $30,001-$50,000 $1,093 84% 2.73% $50,001-$75,000 $1,530 89% 2.45% $75,001-$100,000 $2,059 92% 2.35% $100,001 and above $3,089 94% 3.09%

16

Age and “New Philanthropy”

• New philanthropists appear different from their predecessors– Younger wealthy give less than older wealthy, on

average– New wealth comes from new sources– New philanthropy tends to be more “hands-on” and

entrepreneurial– Relatively little geographical bounding

Ref.: Brown 2000

U.S. Silicon Valley, CA (1998) Belongs to a work-related organization 16% 52% Belongs to a religious organization 70% 26% Gives to religious organizations 48% 37% Gives to education organizations 20% 36% Gives to human-service organizations 25% 18%

17

Planned Giving Instruments

• Pooled income funds– Pay lifetime annuities– Split between charity and beneficiaries

• Charitable lead trust– Dividends pay to charity till time t– After t, principal pays to beneficiary

• Charitable remainder trust– Dividends pay to beneficiary till time t– After t, principal pays to charity

Ref.: Hodgkinson (Salamon) 2002

18

Development Innovations

• Venture philanthropy– Foundation giving in search of large,

immediate payoff outcomes across a wide variety of potential activities

• E-philanthropy– Donations given over the internet

• Credit card donations taken from websites• Donation portals: collect donor information and

donations for a commission• Charity malls: For-profits that advertise on NPO

sites and donate a percentage of sales to the charity

Ref. Brooks 2002

19

Institutional Philanthropy

• Foundations– 50,000 and growing– $450b in assets

• Corporations– 75% of corporate giving not from corporate

foundations– Cash and in-kind giving

• Federations (pass-through organizations)– General: United Ways– Specific: American Cancer Society, March of Dimes

• Gift funds– Donor-advised and controlled accounts– Run by for-profit investment firms

Ref.: Lenkowsky (Salamon) 2002

20

Foundation Types

• Independent: 95%– Operating (6%)– Non-operating (94%)– Usually connected with family

fortunes

• Community: 1%– Pool community assets

• Corporate: 4%

Ref.: Lenkowsky (Salamon) 2002

21

Outline

• Private giving• Government support

22

Direct Government Subsidies Are Large …

Billions of 1997 dollars Percent of total revenues

All nonprofits 207.8 31.3

Arts and culture 1.5 9.7

Health 137.7 42.2

Education 23.1 19.4

Social welfare 40.1 52.1

$138

$23

$7

$40

$2$0

$20

$40

$60

$80

$100

$120

$140

$160H

ealth

Edu

catio

n

Re

ligio

n

So

cia

lw

elfa

re

Art

s a

ndcu

lture

Bill

ion

s of

199

7 d

olla

rs

$138

$23

$7

$40

$2$0

$20

$40

$60

$80

$100

$120

$140

$160H

ealth

Edu

catio

n

Re

ligio

n

So

cia

lw

elfa

re

Art

s a

ndcu

lture

Bill

ion

s of

199

7 d

olla

rs

23

…and Growing

$0

$50

$100

$150

$200

$250

1977 1982 1987 1992 199724%

25%

26%

27%

28%

29%

30%

31%

32%

Sector revenues from government (1997 prices)

Percent of sector funding from government

$0

$50

$100

$150

$200

$250

1977 1982 1987 1992 199724%

25%

26%

27%

28%

29%

30%

31%

32%

Sector revenues from government (1997 prices)

Percent of sector funding from government

24

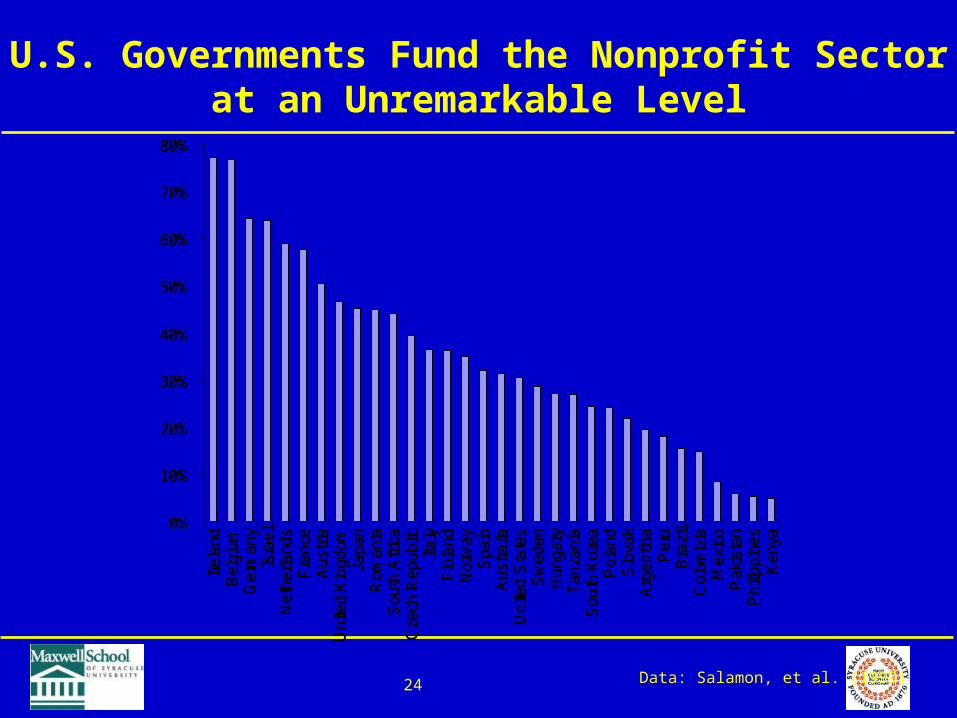

U.S. Governments Fund the Nonprofit Sector at an Unremarkable Level

0%

10%

20%

30%

40%

50%

60%

70%

80%

Ire

land

Be

lgiu

mG

erm

any

Isra

el

Ne

the

rland

sF

ran

ceA

ust

riaU

nite

d K

ingd

omJa

pan

Rom

ania

Sou

th A

fric

aC

zech

Re

pub

licIt

aly

Fin

land

No

rwa

yS

pain

Au

stra

liaU

nite

d S

tate

sS

we

den

Hun

gary

Tan

zan

iaS

outh

Ko

rea

Po

land

Slo

vak

Arg

en

tina

Pe

ruB

razi

lC

olo

mb

iaM

exi

coP

aki

stan

Ph

ilipp

ine

sK

enya

0%

10%

20%

30%

40%

50%

60%

70%

80%

Ire

land

Be

lgiu

mG

erm

any

Isra

el

Ne

the

rland

sF

ran

ceA

ust

riaU

nite

d K

ingd

omJa

pan

Rom

ania

Sou

th A

fric

aC

zech

Re

pub

licIt

aly

Fin

land

No

rwa

yS

pain

Au

stra

liaU

nite

d S

tate

sS

we

den

Hun

gary

Tan

zan

iaS

outh

Ko

rea

Po

land

Slo

vak

Arg

en

tina

Pe

ruB

razi

lC

olo

mb

iaM

exi

coP

aki

stan

Ph

ilipp

ine

sK

enya

Data: Salamon, et al. (1999)

25

Indirect Subsidies and Taxes

• Taxes foregone on deductible contributions

• UBIT• Property taxes• Tax credits

26

Income Tax Revenues Foregone

• t=individual’s marginal tax rate• m=gross income• D=tax-deductible donations• t(m-D)=taxes paid• tD=indirect government subsidy• 2002 estimate: $37.2b

27

Corporate Tax Exemption and the UBIT

• As a general rule, organizations have incentives to invest in activities where their earnings are tax exempt but other organizations must pay tax

• Nonprofits to a significant degree can shift costs from exempt to non-exempt activities

• → UBIT payments to government are very low

28

The Property Tax Exemption

• Could be thought of as a subsidy by the state, or as a reflection of the “sovereignty” of nonprofits

• Total US value of exemption around $6 billion (mostly in hospitals and education)

• Increased use of PILOTS: strategic move for nonprofits

29

Nonprofit Revenues Are Interrelated

Earnedincome

Governmentsupport

Privatecontributions

30

Crowding In orCrowding Out?

• Crowding out– Lowered perceived need– Donors resemble tax payments– Less incentive to fundraise

• Crowding in– Subsidy is a signal of quality or

guarantee of due diligence– Government grants only given as a

match to private gifts