95

1 Project Profitability Assessment

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | edmund-clarke |

| View: | 213 times |

| Download: | 2 times |

1

Project Profitability Assessment

2

Contents Capital budgeting (of

“environmental” projects) Project cash flows and simple

payback The Time Value of Money (TVM) and

Net Present Value (NPV) Two small group exercises Capital budgeting with inflation and

tax Sensitivity analysis Key profitability indicators

3

Capital Budgeting(of “Environmental”

Projects)[15 min]

4

Capital budgeting

The process by which an organization: Decides which investment projects are

needed & possible, with a special focus on projects that require significant up-front investment (i.e., capital)

Decides how to allocate available capital between different projects

Decides if additional capital is needed

5

Capital budgeting practices

Capital budgeting practices vary widely from company to company – Larger companies tend to have more

formal practices than smaller companies– Larger companies tend to make more and

larger capital investments than smaller companies

– Some industry sectors require more capital investment than others

Capital budgeting practices may also vary from country to country

6

Typical project types & goals (1)

Maintenance– Maintain existing equipment and operations

Improvement– Modify existing equipment, processes, and

management and information systems to improve efficiency, reduce costs, increase capacity, improve product quality, etc.

Replacement– Replace outdated, worn-out, or damaged

equipment or outdated/inefficient management and information systems

7

Typical project types & goals (2)

Expansion– e.g., obtain and install new process

lines, initiate new product lines Safety

– make worker safety improvements Environmental

– e.g., reduce use of toxic materials, increase recycling, reduce waste generation, install waste treatment

Others...

8

The poor reputation of “environmental” investment

projects

The poor reputation of “environmental” investment

projects

Many people in industry view “environmental” projects as increasingly necessary to stay in business, but as automatic financial losers because:

– they associate “environmental projects” with pollution control systems such as wastewater treatment plants, which can be quite costly (end-of-pipe)

– they are unaware of the potential financial benefits of preventive environmental management practices

9

We know better!We know better!

We have learned that some environmental projects, i.e., Cleaner Production (CP) projects, can go hand in hand with:– Production efficiency improvements– Product quality improvements– Production expansion

So, do not place your project idea into a single narrow category — think broadly about all the possible benefits

10

Decision-making factors

Project selection

Technical

Organizational

FinancialRegulatory

Today’s focus

11

Project Cash Flowsand

Simple Payback

[15 min]

The Cash Flow Concept

The Cash Flow Concept is a common management planning tool.

It distinguishes between:

(a) costs -> cash outflows (b) revenues/savings -> cash inflows

12

13

Cash Flow Analysis

• Relies on every day life principles

• Measures the difference between

– What we received, and

– What we paid out

• Only cash receipts and cash payments are included in the analysis

• Applicable also to forecast cash available

Types of Cash Flows

One-time

Annual

Other

Inflow

Equipment salvage

value

Operating revenues & savings

Working capital

Outflow

Initial investment

cost

Operating costs &

taxes

Working capital

14

15

Cash Outflow Analysis (1)

• Planning/

Engineering

• Permitting

• Site Preparation

• Purchased

Equipment

• Working Capital

• Utility Systems &

Connections

• Start-up/Training

• Contingency

• (Salvage Value)

INITIAL INVESTMENT

Working Capital

Working Capital is: “the total value of goods and money necessary to maintain project operations”

It includes items such as:– Raw materials inventory– Product inventory– Accounts payable/receivable– Cash-on-hand

16

Salvage Value

Salvage Value is the resale value of equipment or other materials at the end of the project

17

18

•Direct costs

•Input costs

•Other costs

•Loan repayments

•Interest on loan application

Cash Outflow Analysis (2)

19

•Sales

•Savings

•Salvage value

•Cash shortfall / surplus

Cash Inflow Analysis

20

Cash Flow Forecast/Projection (1)

•We are looking at the likely future cash position.

•We examine the possible effects of changes in the cash flow components .

21

Cash Flow Forecast/Projection (2)

Make assumptions about likely outcomes regarding:– Inflation– Market size – Demand for goods and services– Interest Rates

22

I nvestment Year 0 1 2 3

I NI TI AL I NVESTMENTTotal I nvestment Costs

OPERATI NG COSTSTotal Operating Costs

OPERATI NG AND MAI NTENANCETotal Operating and Maintenance Costs

WASTE MANAGEMENTTotal Waste Management Costs

COMPLI ANCE AND REG. (LessTangibles)

Total Compliance Costs

REVENUES AND SAVI NGSREVENUESOperating CostsLess DepreciationTaxable I ncomeTax payableNet I ncome af ter Depreciation and Tax

Cashflow Projection Worksheet

23

Operating Inputs

• Materials

• Energy

• Labour

• Floor Space

• Taxes

• Depreciation

• Cost of capital

Waste Management includes waste handling, recycling, treatment, disposal, and regulatory compliance

• Materials

• Energy

• Labour

• Floor space

• Fees

• Taxes & Depreciation

• Cost of Capital

Less Tangibles• Productivity• Future regulation• Potential liability• Insurance• Company image

Revenues• Product sales• By-product sales • Pollution credits

Annual Operating Costs & Savings

(see also Cleaner Production Investment Decision: Costs and Savings checklist)

Timing of Cash Flows

Workingcapital

Annual Operating CostsAnnual Tax Payments

Annual Financing Payments

Salvage Value

End of project:

Time zero:

Initial InvestmentWorking Capital

TIMEYear 1 Year 2 Year 3

Annual Revenues/Savings

24

Cash Flow Analysis structure

There are two basic ways to structure a project financial analysis:

1) Stand-alone analysis Considers only the cash flows of the proposed project

2) Incremental analysisCompares the cash flows of the proposed project to the “business as usual” cash flows

25

Incremental analysis for CP

For many CP projects, you will need to do an incremental analysis — compare the CP cash flows to the “business as usual” cash flows

You only need to estimate the cash flows that change when you improve the “business as usual” operations

26

Profitability indicatorsA profitability indicator, or “financial indicator”, is: “a single number that is calculated for characterisation of project profitability in a concise, understandable form.”Common examples are:

• Simple Payback

• Return on Investment (ROI)

• Net Present Value (NPV)

• Internal Rate of Return (IRR)

27

Simple payback

This indicator incorporates:– the initial investment cost – the first year cash flow from the

project

Simple Payback (in years)

Initial Investment

Year 1 Cash Flow=

28

How to interpretsimple payback

The simple payback calculated for a project is usually compared to a company rule of thumb called a “hurdle” rate:

e.g., if the payback period is less than 3 years, then the project is viewed as profitable

29

30

Small Group Exercise:Profitability Assessment

at the PLS Company— Part I

“Cash Flows & Simple Payback”

[30 min]

31

The PLS company’sQC camera project

PLS decided to purchase and install a camera system to monitor quality control (QC) of the print jobs as they actually occur

Allows the operators to detect print errors earlier and halt the operations before too much solid scrap is generated

Has reduced generation of full-run solid scrap by about 40%

Costs and savingsincluded in the QC camera

analysis Initial investment costs

– purchase of the camera system, delivery, installation, start-up

Annual operating costs (and savings)– Operating input — materials (plastic film,

ink), energy, labour– Incineration — fuel, fuel additive, labour,

ash to landfill– Wastewater treatment — chemicals,

electricity, labour, sludge to landfill

32

QC camera projectCash flows

Annual Tax Payments = 0 (PLS has tax holiday)Financing Payments = 0 (PLS paid cash)

Initial Investment = $105,000Working Capital = 0 (not important for this project)

TIMEYear 1 Year 2 Year 3

Annual savings = ???

Time zero:

33

The PLS company’sQC camera project

Initial Investment

Cost

Annual Operating

Costs

BusinessAs

Usual Annual Savings =

???The QC Camera Project

0

US $ 105,000

???

???

34

35

Exercise instructionsPart I

Introduction (5 min.), detailed in your handout

Question 1 (15 min.) Question 2 (5 min.) Discuss your answers with

the other small groups and the instructor (5 min.)

36

The Time Value of Moneyand

Net Present Value (NPV)

[30 min]

37

Question:

If we were giving away money, would you rather

have:(A) $10,000 today, or(B) $10,000 3 years

from now

Explain your answer...

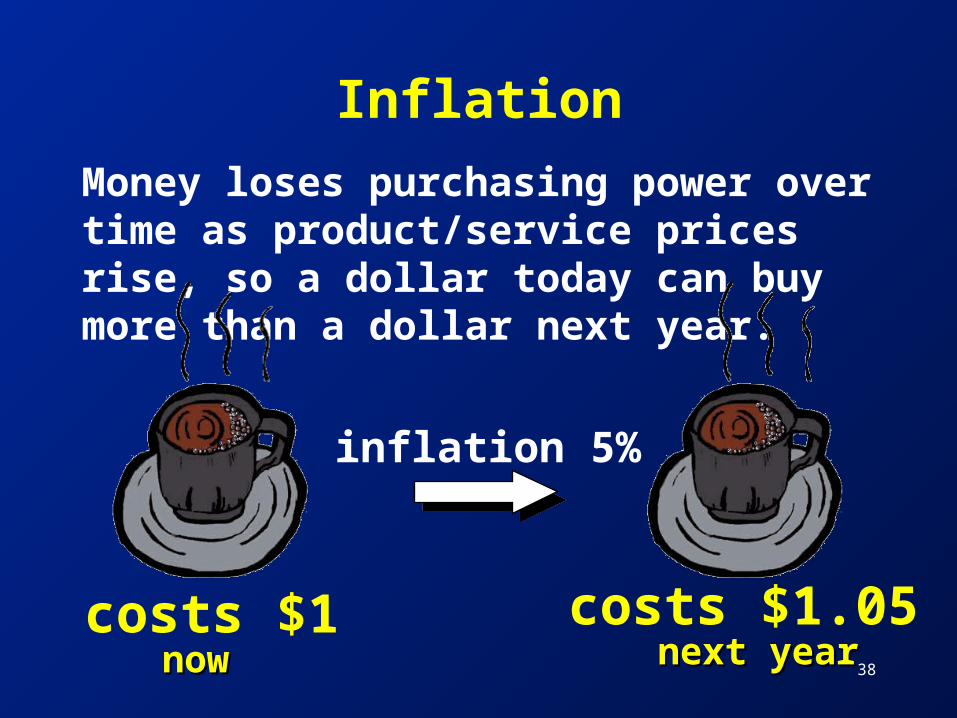

Inflation

Money loses purchasing power over time as product/service prices rise, so a dollar today can buy more than a dollar next year.

costs $1 costs $1.05

inflation 5%

nownow next yearnext year38

Investment opportunity

A dollar that you invest today will bring you more than a dollar next year — having the dollar now provides you with an investment opportunity

Interest, or “return on investment”

Investing $1 now

InvestmentGives you

$1.10 a year from now

39

40

Time Value of Money (TVM)

Money now is worth more than money in the future because of:a) inflationb) investment opportunity

The exact “time value” of your money depends on the magnitude of the:a) rate of inflation andb) rate of return on investment

41

TVM and project profitability

When you invest in a capital project, you have:(1) An initial investment happening NOW(2) A series of future cash inflows, over time,

that pay back the initial investment

So, it is important to take the Time Value of Money (TVM) into account when you are estimating project profitability

The PLS company’sQC camera project

Initial Investment

Cost

Annual Operating

Costs

BusinessAs

Usual Annual Savings =

US$38,463The QC Camera Project

0

$ 105,000

$ 2,933,204

$ 2,894,741

(in US$)42

43

Question:

Is the annual savings of$38,463 per year for 3 years

a sufficient returnon the initial investment of

$ 105,000?

44

You might think about adding up the annual savings over the 3 years:

Savings per year $38,463x 3 years

Total savings $115,389

But: this ignores the Time Value of Money (the fact that $38,463 in year 1 is not the same as $38,463 in year 2 or year 3)

Answer?

Comparing cash flowsfrom different years

Before you can compare cash flows from different years, you need to convert them all to their equivalent values in a single year

It is easiest to convert all project cash flows to their “present value” now, at the very beginning of the project

45

Converting the PLS cash flowsto their “present value”

End of project

Time zero:

Initial Investment = $105,000

TIMEYear 1 Year 2 Year 3

$38,463 $38,463 $38,463

= ??= ??= ??

Annual Savings

46

Converting cash flowsto their present value

You can convert future year cash flows to their present value using a “discount rate” that incorporates:– Desired return on investment– Inflation

The discount rate calculation is simple — mathematically, it is the reverse of an interest rate calculation

47

48

Invested at an interest rate of 20%, how much will $10,000 now be worth after 3 years?

Afteryear

1 $10,000 x 1.20 = $12,000

2 $10,000 x 1.20 x 1.20 = $14,400

3 $10,000 x 1.20 x 1.20 x 1.20 = $17,280

Note: these calculations are on a compound basis

Interest rate calculation

49

The discounting calculation is essentially the opposite of the interest rate calculation.

If you want to have $17,280 in 3 years, how much would you have to invest now?

$17,280 = $10,000

1.20 x 1.20 x 1.20 needed now

In other words, $17,280 in year 3 has a present value of $10,000

Discounting calculation

50

Which discount rate? (1)

The discount rate a company chooses should be equal to the required rate of return for the project investment

The required rate of return will usually incorporate three distinct elements:– A basic return - pure compensation for

deferring consumption– Any ‘risk premium’ for that project’s risk– Any expected fall in the value of money over

time through inflation

51

Which discount rate? (2)

At a minimum, the chosen discount rate should cover the costs of raising the investment financing from investors or lenders (i.e. the company’s “cost of capital”)

Often, rather than trying to identify the exact source of capital (and its associated cost) for each individual project, a firm will develop a single “Weighted Average Cost of Capital” (WACC) that characterises the sources and cost of capital to the company as a whole.

Discounting (1)

Present Value = Future Valuen

(1 + d)n

The value of the cash flow in year n

The value of the cash flow at

“Time Zero,” i.e., at project start-up

d = the discount rate

n = the number of years after

project start-up

52

Discounting (2)

Present Value = Future Valuen x (PV Factor)

The value of the cash flow in year n

The value of the cash flow at

“Time Zero,” i.e., at project start-up

Present Value (PV) Factors have been calculated for various

values of d (discount rate) and n (number of years) and have been

tabulated for easy use.

(Also called discount factors)53

54

PresentValue factors Value of $1 in the future, NOW

Discount rate (d): 10% 20% 30% 40%

Years into future (n)

1 .9091 .8333 .7692 .7142

2 .8264 .6944 .5917 .5102

3 .7513 .5787 .4552 .3644

4 .6830 .4823 .3501 .2603

5 .6209 .4019 .2693 .1859

10 .3855 .1615 .0725 .0346

20 .1486 .0261 .0053 .0012

30 .0573 .0042 .0004 .0000

55

Net Present Value (NPV)

Net Present Value (NPV) = the sum of the present values of all of a project’s cash flows, both negative (cash outflows) and positive (cash inflows)

NPV characterises the present value of the project to the company

If NPV > 0, the project is profitable

If NPV < 0, the project is not

EstimatingNet Present Value

Expected Future Cash

Flows

- $105,000

+ $38,463

+ $38,463

+ $38,463

PVFactor

Present Value of Cash Flows (at time zero)

- $???

$???

$???

$???

$???

Year

0

1

2

3

* =

???

???

???

???

Sum = the project’s Net Present Value = 56

57

Time for lunch! [60 min]

Time for lunch! [60 min]

58

Small Group Exercise:Profitability Assessment

at the PLS Company— Part II

“Net Present Value”

[45 min]

59

Also — you will need the handout:

“Performing Net Present Value (NPV) Calculations”

Also — you will need the handout:

“Performing Net Present Value (NPV) Calculations”

Located in your handout

Converting the PLS cash flowsto their “present value”

End of project

Time zero:

Initial Investment = $105,000

TIMEYear 1 Year 2 Year 3

$38,463 $38,463 $38,463

= ??= ??= ??

60

61

Exercise instructionsPart II

Introduction (5 min.), detailed in your handout

Question 3 (15 min.) Question 4 (5 min.) Discuss your answers with

the other small groups and the instructor (15 min.)

Lessons learned (5 min.)

62

Capital Budgeting: inflation & tax

[30 min]

63

Discounting and inflation (1)

even without inflation, money has a time value due to supply/demand for money

inflation increases both:- future cash flows

- interest rates (and discount rates)

these offset each other

64

Discounting and inflation (2)

With 10% inflation (say), future cash flows will by 10% each year

Investors & lenders will also require a higher rate to compensate for their loss in purchasing power

If 15% was acceptable with no inflation, with 10% inflation they will now require

115% x 110% = 126.5%

65

Discounting and inflation (3)

PLS Company, now assuming 10% inflation and 26.5% discount rate:

Year Cash flow PV factor PV ($) @ 26.5% ($)

1 42,309 0.791 33,466 2 46,540 0.625 29,088 3 51,194 0.494 25,289

87,843less: initial investment 105,000

Net Present Value -17,157

i.e. same NPV* as with zero inflation, 15% discount rate

* ignoring minor rounding difference

66

What is the current rate of inflation in the economy?

What return on their capital will the lender really earn on their money, after allowing for the erosion of their capital over time through inflation?

Tax payments

Taxes can be an important project cash flow

Depending on a facility’s location, a firm may have to pay national and/or local income taxes on the revenues or savings generated by a project

Other types of taxes may also be relevant - sales taxes, pollution taxes, etc.

67

Tax deductions or credits

Tax deductions or credits can also be important

One example is the income tax deduction often given for equipment depreciation, which is the loss in value of a physical asset (e.g., a piece of equipment) as the asset ages

Some “environmental” investments can receive special tax credits

68

69

Tax and project appraisal

assume 30% rate of taxes of firms’ profits

tax is based on accounting profits, not on cashflows

accounting profits are after deducting depreciation

tax is payable 1 year after the profits have been realised

70

Depreciation

A project needs $12,000 for a new machine which will last 3 years

assume the machine has no residual value after 3 years

depreciation per year: initial cost = $12,000 = $4,000 per

yearasset life 3 years

71

Profit earned by project

Profit earned by project in each year:

cash inflow per year $6,000less: depreciation $4,000

contribution to profit $2,000

tax @ 30% $600

72

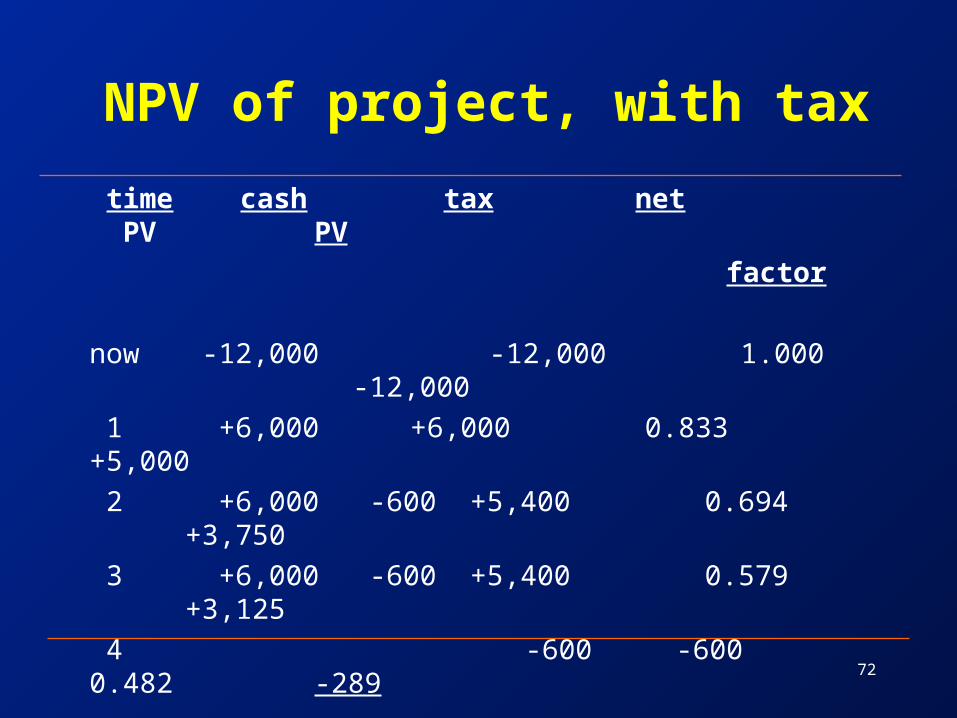

NPV of project, with tax

time cash tax net PV PV factor

now -12,000 -12,000 1.000 -12,000 1 +6,000 +6,000 0.833 +5,000 2 +6,000 -600 +5,400 0.694+3,750 3 +6,000 -600 +5,400 0.579+3,125 4 -600 -600 0.482 -289

Net Present Value - $414

73

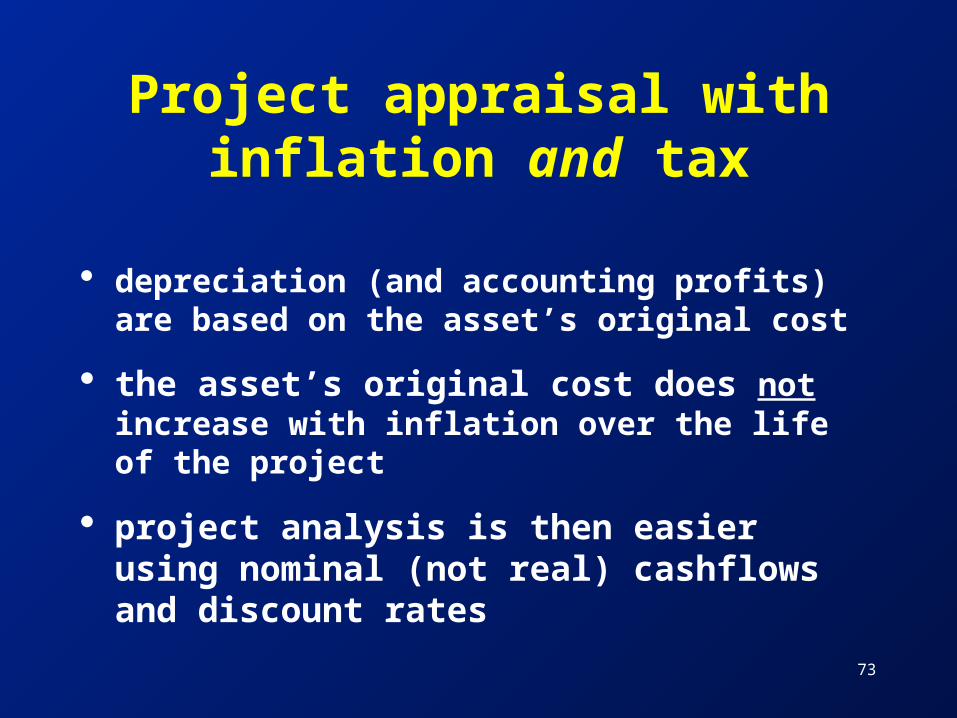

Project appraisal with inflation and tax

depreciation (and accounting profits) are based on the asset’s original cost

the asset’s original cost does not increase with inflation over the life of the project

project analysis is then easier using nominal (not real) cashflows and discount rates

74

Some good reasons to use a longer analysis

time horizon

Some good reasons to use a longer analysis

time horizon

Some out-year costs may be missed if the time horizon is too short, e.g., a required wastewater treatment plant upgrade in the future

Some annual operating costs may change significantly over time, e.g., disposal fees at landfills

Short time horizons neglect the impact of the time value of money, especially in times of significant inflation, deflation, changing cost of capital, etc.

75

Profitability assessment tips

Be sure to:– Include all relevant and significant

costs/savings in the profitability analysis

– Think long-term (or at least medium-term!)

– Incorporate the time value of money– Use multiple profitability indicators– Perform sensitivity analyses for data

estimates that are uncertain

76

Time for a break! [15 min]

Time for a break! [15 min]

77

Sensitivity Analysis

[15 min]

78

Sensitivity AnalysisIntroduction

An important management tool questioning potential project benefit risks.

Assumptions surrounding a project are computed to produce a base NPV and IRR.

From the base case, changes in the original assumptions are made to gauge their effect on the NPV and IRR.

Input variables varied adversely by 10%

79

Sensitivity Analysis Example

Input Variables Varied by 10%

OriginalData

10% increasein Cost of

Capital

10% increasein I nvestment

cost

10% decreasein cashflows

Year 0 - 2735000 - 11323650 - 12456015 - 2735000Year 1 - 14978753 12951647 - 14978753 - 14828965Year 2 17122990 2592375 17122990 16951760Year 3 8022274 5151626 8022274 7942051Year 4 376354 117364 376354 372590.5Year 5 8203865 374538 8203865 8121826Year 6 76133 5142598 76133 75371.67DiscountRate

35% 48,5% 35% 35%

Project Life 5 years 5 years 5 years 5 yearsNPV 7810 - $2,741,092 - $8,940,009 $745,846I RR 39% 54% 9% 39%

80

Sensitivity Analysis

Summary

Sensitivity Analysis permits project proposals to be evaluated simply.

The model can evaluate sensitive variables without having to input any additional data.

81

Sensitivity AnalysisConclusion

•By amending the original data, a variable whose change generates a negative NPV and /or an IRR lower than the firm’s cost of capital, is deemed to be sensitive.

•An investigation would need to be undertaken for a contingent plan. If results of the investigation are unfavourable, the project is unacceptable on economic grounds.

However, development projects with social aspects may be treated differently.

82

KeyProfitability Indicators

[15 min]

Profitability indicators

We have seen so far:• Simple Payback

• Net Present Value (NPV)

But there are others, common examples are:

• Return on Investment (ROI)

• Internal Rate of Return (IRR)

83

Simple Payback andReturn on Investment

(ROI)

These indicators incorporate:– the initial investment cost – the first year cash flow

Simple Payback (in years)

Initial Investment

Year 1 Cash Flow=

ROI (in %)Year 1 Cash Flow

Initial Investment=

84

How to interpretSimple Payback and ROI

The simple payback or ROI calculated for a project are usually compared to a company rule of thumb called a “hurdle” rate:– e.g., if the project payback period is

less than 3 years, then the project is viewed as profitable

– e.g., if the ROI is 33%, then the project is viewed as profitable

85

Net Present Value (NPV)

NPV is a more reliable profitability indicator than Simple Payback or ROI as it considers both the time value of money and all future year cash flows

NPV = the sum of the discounted cash flows over the lifetime of the project, using the company’s cost of capital as the discount rate

86

Internal Rate of Return (IRR)

IRR is similar to NPV in that it considers both the time value of money and all future year cash flows

IRR = the discount rate for which NPV = 0, over the project lifetime (calculated in an iterative fashion)

It tells you exactly what “discount rate” makes the project just barely profitable

87

88

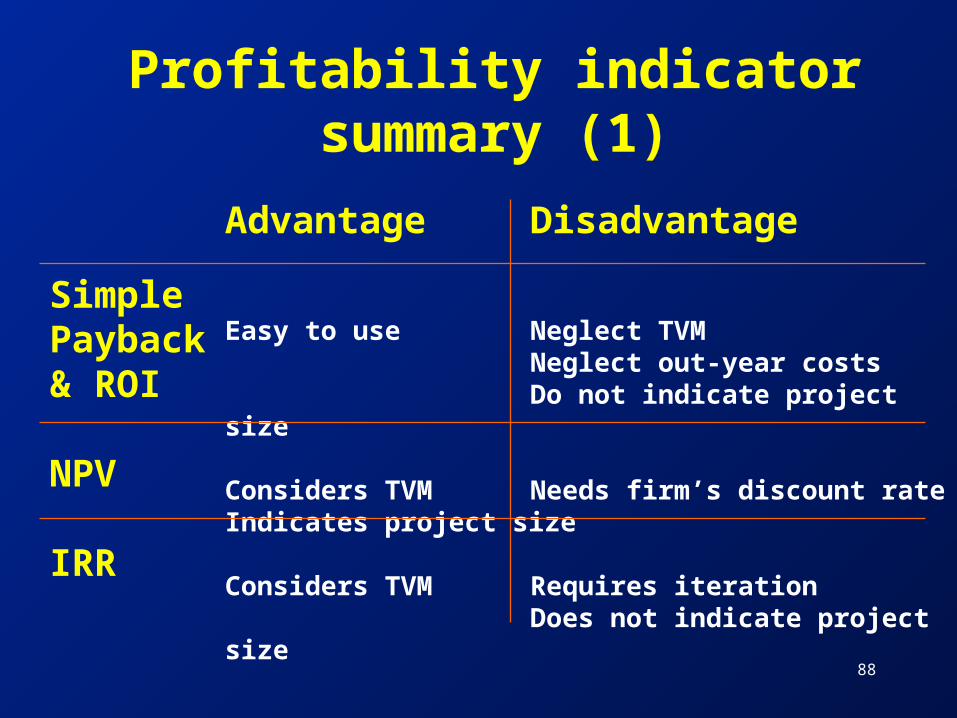

Profitability indicator summary (1)

Profitability indicator summary (1)

Advantage Disadvantage

Easy to use Neglect TVMNeglect out-year costsDo not indicate project size

Considers TVM Needs firm’s discount rateIndicates project size

Considers TVM Requires iterationDoes not indicate project size

SimplePayback& ROI

NPV

IRR

Profitability indicator summary (2)

NPV is generally the most valuable, problem-free indicator

Other indicators that consider the time value of money (e.g., IRR) are also useful

Payback and ROI are easy to understand and use, but of limited accuracy

However, Simple Payback is particularly useful with uncertain or risky investment climates

89

90

Interpret profitability indicators with

caution...

Interpret profitability indicators with

caution... We have seen that Simple Payback

has some limitations as a project profitability indicator

Be aware of the advantages and limitations of the indicators you use

The best approach is to use several indicators to give a balanced view of project profitability

91

Other Profitability Assessment Issues

[15 min]

92

Other issues

There are other issues that impact a project’s profitability, which we do not have time to address today– Source and cost of project financing– Can you think of others?

Project financing

Different sources of project financing may have differing impacts on project profitability

Be sure to take financing payments such as lease payments or payments on loan principal and interest into account appropriately when estimating profitability

93

94

Project Profitability Assessment

Summary and Q&A[15 min]

95

Project profitability assessment

Capital budgeting (of “environmental” projects)

Project cash flows and simple payback

The Time Value of Money and Net Present Value (NPV)

Two small group exercises Capital budgeting : inflation and tax Sensitivity analysis Key profitability indicators