14

1 School Finance in Iowa

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | nathaniel-edgecombe |

| View: | 214 times |

| Download: | 0 times |

1

School Finance in Iowa

2

Key Concepts of Iowa School Finance

Dillon’s Rule vs. Home Rule “Bright line” between General Fund

and Building Expenditures Pupil Based Formula Source of Revenues Property Poor (kid rich) Spending Authority vs. Cash

3

School Finance - Background

Dillon’s rule:– School districts only have those powers

expressly authorized by the Code of Iowa. Home rule:

– Cities and counties can do anything not expressly prohibited.

4

School Aid - Basics

The “Bright” Line in School Finance– Educational program expenditures are

funded and equalized by the state foundation formula.

– Facility expenditures are not under the finance formula and may not be used for educational program expenditures (and vice versa).

5

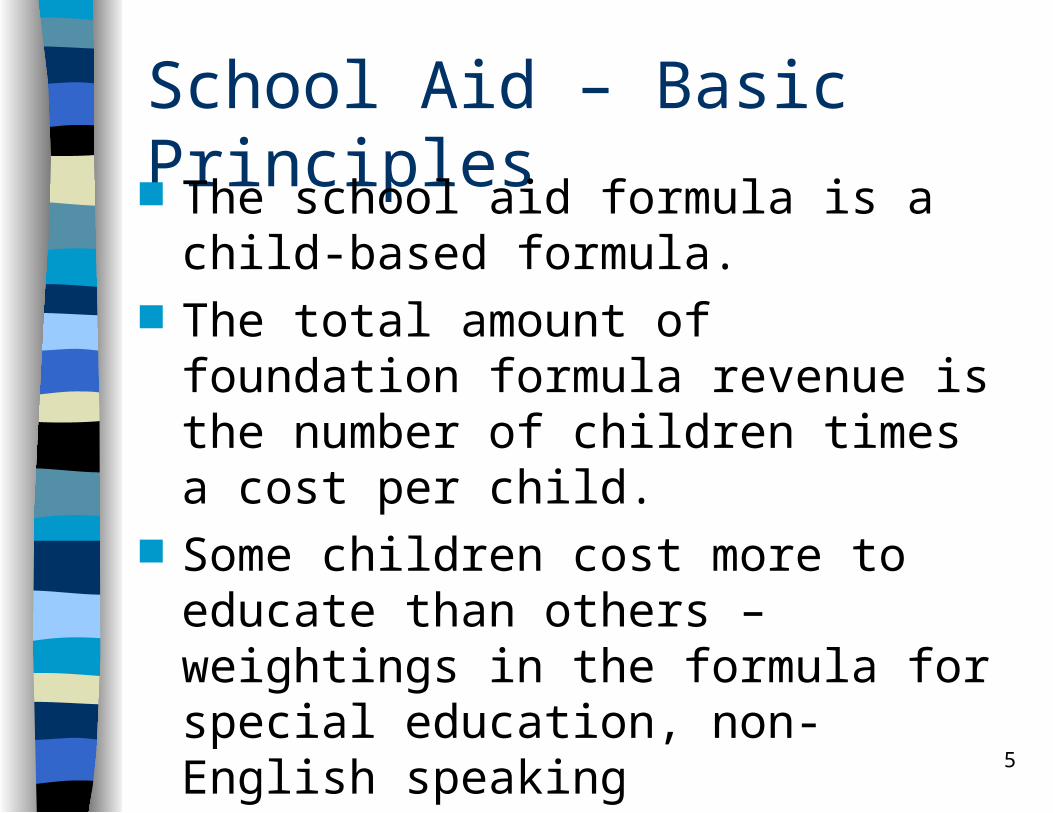

School Aid – Basic Principles The school aid formula is a child-based

formula. The total amount of foundation formula

revenue is the number of children times a cost per child.

Some children cost more to educate than others – weightings in the formula for special education, non-English speaking

6

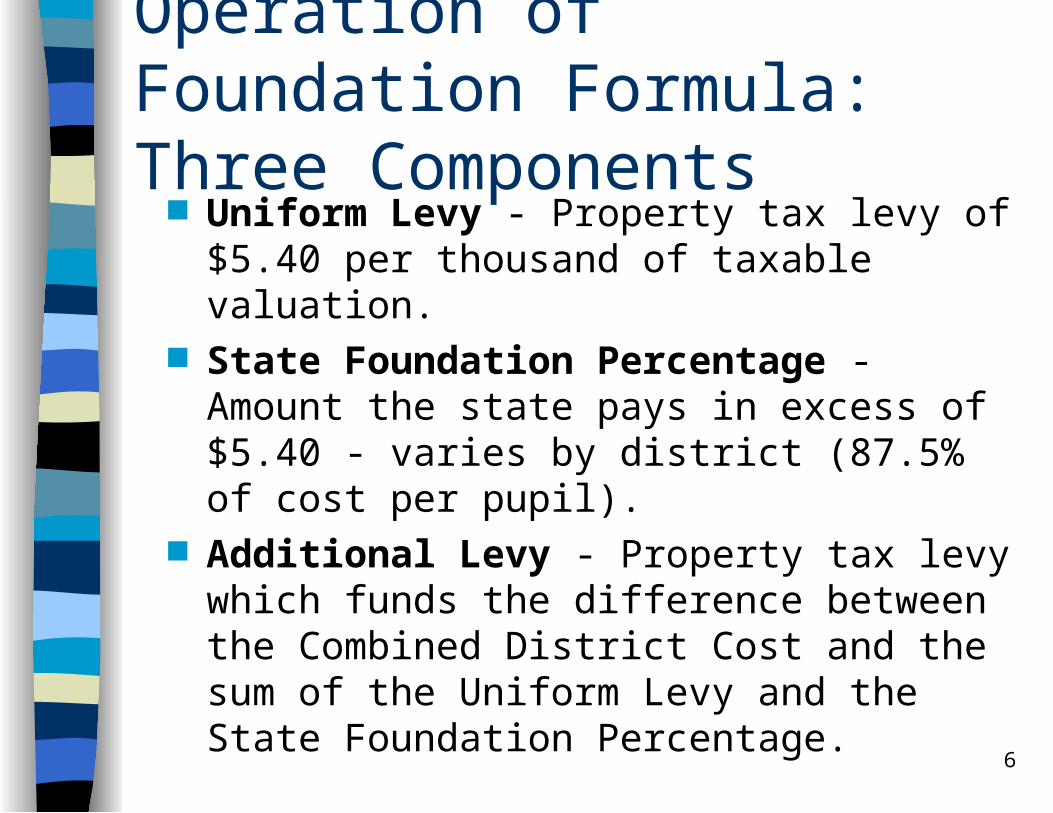

Operation of Foundation Formula: Three Components

Uniform Levy - Property tax levy of $5.40 per thousand of taxable valuation.

State Foundation Percentage - Amount the state pays in excess of $5.40 - varies by district (87.5% of cost per pupil).

Additional Levy - Property tax levy which funds the difference between the Combined District Cost and the sum of the Uniform Levy and the State Foundation Percentage.

7

Operation of Foundation Formula

8

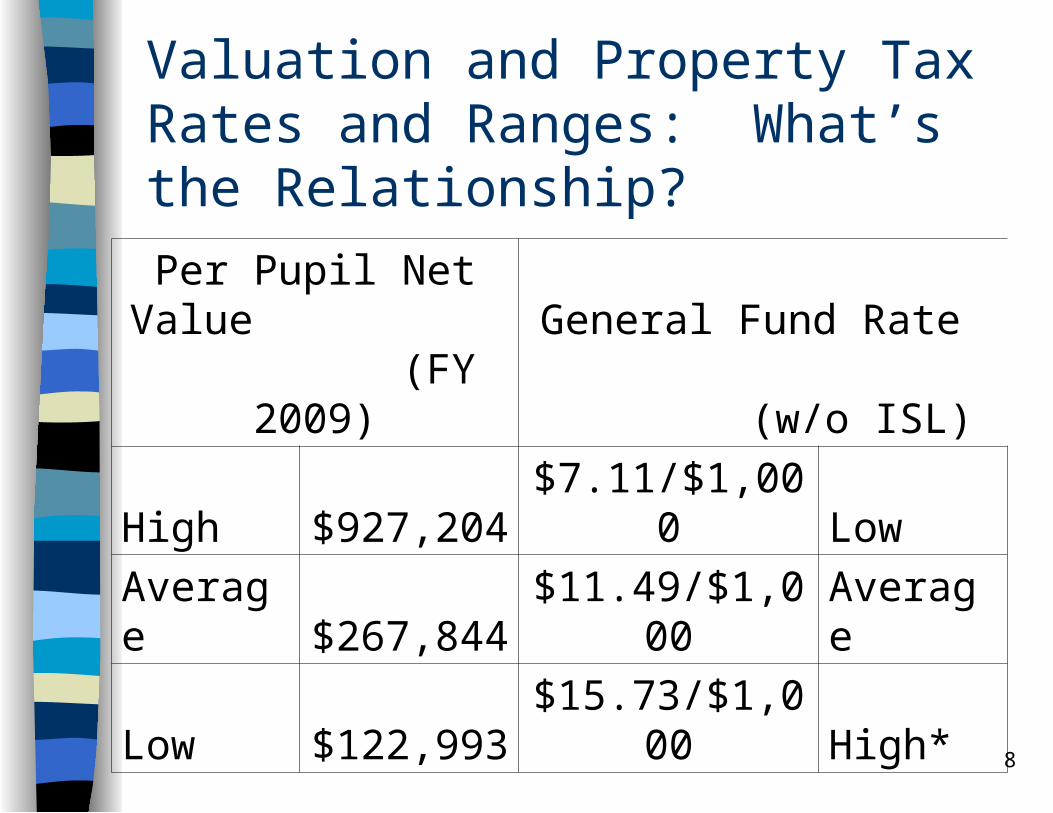

Valuation and Property Tax Rates and Ranges: What’s the Relationship?

Per Pupil Net Value (FY

2009)General Fund Rate

(w/o ISL)

High $927,204 $7.11/$1,000 Low

Average $267,844 $11.49/$1,000 Average

Low $122,993 $15.73/$1,000 High*

*Range in levy rate from high to low has narrowed with state property tax equity payments, which will eventually lower the top half to the average.

9

School Finance - Spending Authority Spending authority is the sum of:

– Combined District Cost (property tax and state aid)

– Miscellaneous income – anything not above– Unspent balance from previous years

Why important?– It’s a ceiling: Districts cannot exceed

spending authority– It’s not a measure of cash– Why allow districts to carry forward unused

spending authority?

10

To Increase Spending Authority:

Claim full At-Risk amount (5% enrollment) Approve ISL (for those who don’t have it) Efficiency incentives Sharing incentives Lobby legislature to increase the ceiling

(allowable growth) Decrease or shift expenditures:

– Early retirement

– State Penny/PPEL expenditures

– Sharing (reduce costs)

11

Comparing Spending Authority and Cash Concepts

Term Explanation Analogy Type

Spending Authority

Total amount a school district can legally spend during a year.

Income + credit cards

Recurring

Unspent Balance Remaining amount of spending authority at end of the year (Spending Authority minus Actual Expenditures).

Credit cards One time

Term Explanation Analogy Type

Cash On Hand Total cash on hand. Savings account

One time

State Aid Amount received by a district from state General Fund.

Paycheck Recurring

Property Taxes Amount received by a district from local property taxes.

Paycheck Recurring

Miscellaneous Income

Any income which is not property tax or state aid (must be actually received).

Birthday money from Grandma

One time/ recurring

12

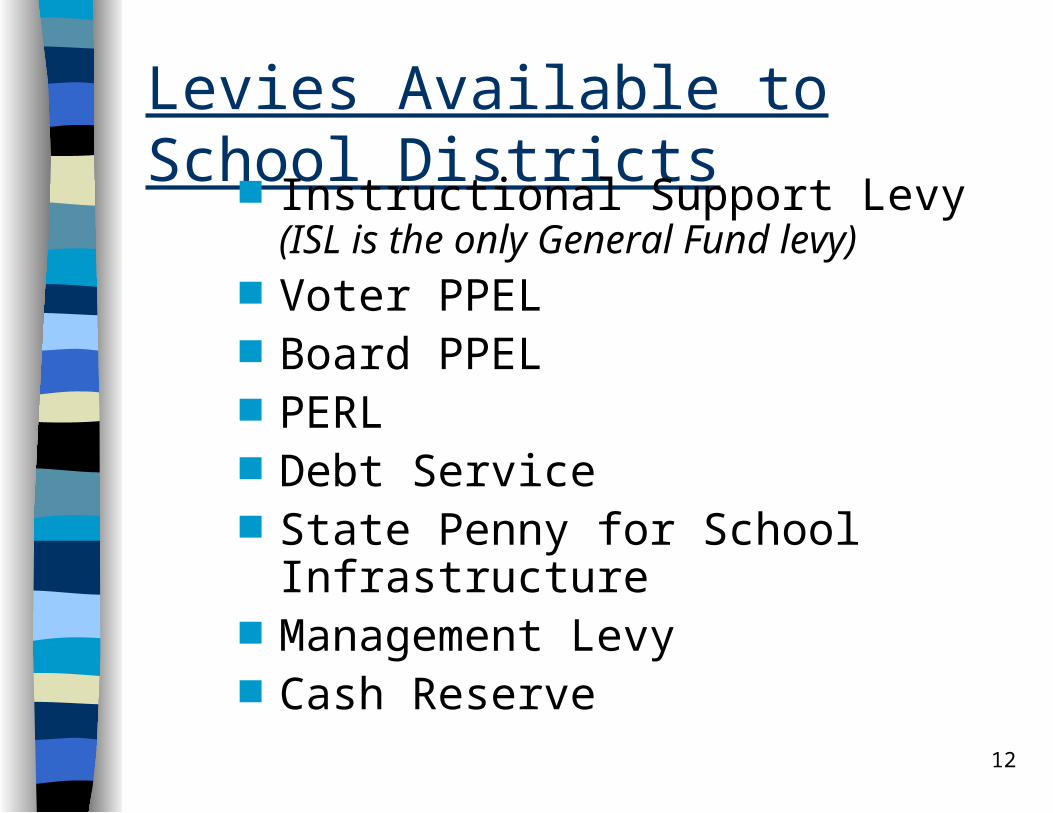

Levies Available to School Districts Instructional Support Levy (ISL is

the only General Fund levy) Voter PPEL Board PPEL PERL Debt Service State Penny for School

Infrastructure Management Levy Cash Reserve

13

Four Questions Why do we have enough money to

pave the parking lot but can’t pay teachers?

Why can’t we just levy whatever we need to support the school?

Why don’t schools become more efficient?

Why don’t property taxes ever decrease?

14

School Aid - Contacts Iowa Association of School Boards

(IASB)– Larry Sigel, School Finance Director 515-

288-1991 ext. 235 [email protected]– Website: www.ia-sb.org – Margaret Buckton, Assoc. Executive Dir.,

Public Policy ext. 228 [email protected]