20

1 State of the Big Three: Presentation to the United Auto Workers Stephen J. Girsky December 3, 2008 [email protected]

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | julius-hodge |

| View: | 213 times |

| Download: | 0 times |

1

State of the Big Three:Presentation to the United

Auto Workers

Stephen J. GirskyDecember 3, 2008

L P

2

Overview

1. Girsky Background• Wall Street Analyst covering Global Auto Industry for 20 years

• Special Advisor to the CEO/CFO of GM in 2005/2006

• Centerbridge Partners - $7bn investment fund

– Evaluated a number of significant auto-related investments

– Lead Dana Corp.’s exit from bankruptcy in partnership with UAW/USW

2. UAW Assignment• Help evaluate possible GM/Chrysler tie up

3. Findings• GM/Chrysler merger difficult to accomplish

• GM, Chrysler situation precarious

4. Where We Go From Here

L P

3

GM/Chrysler Potential Merger Observations

• Logic of the merger based on significant cost saving opportunities including:

– Purchasing

– Product portfolio

– White collar staffing

• Questions around potential tie-up included:– Aggressive assumptions

– Execution risk

– GM has a lot on its plate

• Would Chrysler be better off with a foreign partner?

L P

4

Diligence on a potential GM/Chrysler tie up exposed a different more significant issue

GM was running out of money

L P

5

Auto Sales Were Relatively Steady For Many Years…

U.S. Light Vehicle SAAR

16.1

17.3

16.9

16.6

16.8

17.1

16.9

16.5

15.0

16.0

17.0

18.0

2000 2001 2002 2003 2004 2005 2006 2007Source: Autodata, Company data

L P

6

…But Have Experienced Rapid Deterioration In 2008

2008 Annualized U.S. Light Vehicle SAAR

13.7

12.5

10.6

12.6

13.7

15.4

15.1

14.514.3

15.4

10.0

12.0

14.0

16.0

18.0

January February March April May June July August September October

Source: Autodata, Company data

L P

7

External Events Contributing to the Crisis

• Gasoline prices soared leading to a significant demand shift away from high profit trucks/SUV’s towards lower margin cars

• Commodity prices soared, pressuring material costs

• Credit crisis on Wall Street spread to “Main Street”– Dealers can’t borrow to fund inventory

– Consumers can’t borrow to buy cars

• OEMs and Suppliers can’t borrow money to fund losses

Playing field has shifted dramatically toward companies with cash or access to it and companies with well-balanced product portfolios

L P

8

Not Just a US Problem; Western European Sales Are Starting To Weaken As Well

Source: Autodata, Company data

L P

9

GM: Cash Crisis

1.8 1.1

6.5

(5.5)(7.4)

(9.2)

(13.8)

(11.4)(12.3) (12.1) (12.1)(12.4)

(16.2)

(19.5)

(27.1)

(0.7)

11.5

27.3

16.2

23.9

21.022.9

26.427.2

23.325.0

17.6 17.3

23.7

26.9

20.2 20.4

($30.0)

($25.0)

($20.0)

($15.0)

($10.0)

($5.0)

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

Q4 01

Q202Q402

Q203Q403

Q204Q404

Q205Q405

Q206Q406

Q207Q407

Q108Q208

Q308

$ B

illio

ns

Net Cash Gross Cash (1) (2)

Notes:1. Excluding GMAC-related debt2. Including readily available VEBA assets

Source: Company data

Debt ($) 12.2 15.8 16.2 17.2 32.4 32.4 32.5 32.6 34.2 34.3 38.7 39.3 39.4 40.1 40.5 43.3

L P

10

GM Stock Price Has Fallen In Response

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

$45.0

1/3/05

4/2/05

6/30/05

9/27/05

12/25/05

3/24/06

6/21/06

9/18/06

12/16/06

3/15/07

6/12/07

9/9/07

12/7/07

3/5/08

6/2/08

8/30/08

11/27/08

Source: Capital IQ

L P

11

GM: Not Just a North American Problem

GM Third Quarter Adjusted Results$ Millions

3Q 2007 3Q 2008 Difference

GMNA ($298) ($2,295) ($1,997)

GME (136) (974) (838)

GMLAAM 374 514 140

GMAP 186 (6) (192)

Total Auto Earnings Before Tax (pre-eliminations) $126 ($2,761) ($2,887)

• The North American market has deteriorated significantly since 3Q2007

• However, European and Asian markets have also shown significant weakening

L P

12

GM: Significant Current Obligations

GM Obligations as of 9/30/08

$ Millions

Amount

Accounts payable (principally suppliers) $27,839

UAW VEBA contribution due 2010 8,900

Approximate debt maturities through 2010 (1) 1,921

Total Obligations $38,660

Note:

1. Excludes debt issued by subsidiaries and consolidated affiliates

L P

13

Ford Situation Less Severe, Although Recently Burning Cash At A Rapid Rate

10.9 11.1

5.1

7.4 7.9

3.9

7.25.9

3.9

(7.2)

0.1

1.6

3.75.2

7.9

14.2

17.7

21.8

25.1

34.6

25.9

28.7

25.324.9

26.8

23.6

37.4

33.9

23.6

26.6

28.7

18.9

($10.0)

($5.0)

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

Q4 01

Q202Q402

Q203Q403

Q204Q404

Q205Q405

Q206Q406

Q207Q407

Q108Q208

Q308

$ B

illio

ns

Net Cash Gross Cash (1) (2)

Notes:1. Excluding Ford Credit debt2. Including short-term VEBA assets

Source: Company data

Debt ($) 13.8 14.0 14.2 14.5 20.8 18.9 18.4 18.1 17.9 17.7 30.0 30.0 26.7 27.1 26.5 26.1

L P

14

Ford Stock Price Has Fallen In Response

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

1/3/05

4/2/05

6/30/05

9/27/05

12/25/05

3/24/06

6/21/06

9/18/06

12/16/06

3/15/07

6/12/07

9/9/07

12/7/07

3/5/08

6/2/08

8/30/08

11/27/08

Source: Capital IQ

L P

15

Ford: Not Just A North American Problem

• The North American market has deteriorated significantly since 3Q2007

• However, European and Asian markets have also shown significant weakening

Ford Third Quarter Adjusted Results$ Millions

3Q 2007 3Q 2008 Difference

Ford North America ($1,017) ($2,589) ($1,572)

Ford South America $386 480 94

Ford Europe $293 69 (224)

Ford Asia Pacific & Africa $30 4 (26)

Total Auto Earnings Before Tax (pre-eliminations) ($308) ($2,036) ($1,728)

L P

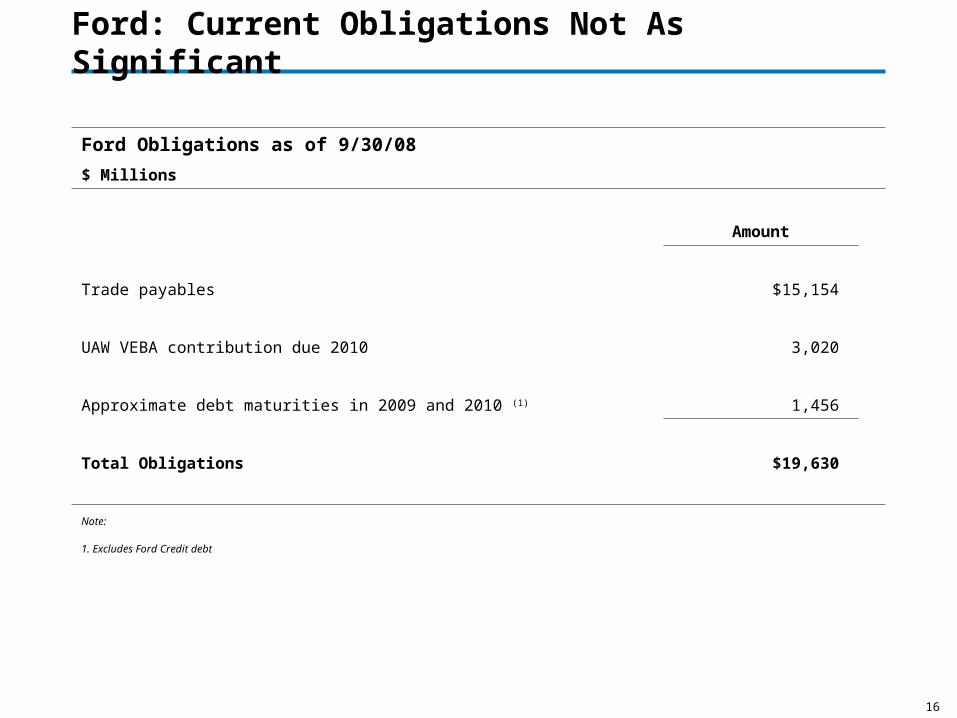

16

Ford: Current Obligations Not As Significant

Ford Obligations as of 9/30/08

$ Millions

Amount

Trade payables $15,154

UAW VEBA contribution due 2010 3,020

Approximate debt maturities in 2009 and 2010 (1) 1,456

Total Obligations $19,630

Note:

1. Excludes Ford Credit debt

L P

17

Chrysler Issues

•Cerberus LP purchased Chrysler from Daimler for approximately $7.2Bn in August 2007

•Most of Cerberus’ investment is in the Finance Company, which was legally separated from the auto company at the time of purchase

•Auto Company currently has $9bn in debt, backed up assets of the Company. VEBA obligations due in 2010 of roughly $3bn technically

rank below the $9bn.

L P

18

Chrysler Liability Structure

Chrysler Liability Structure

$ Millions

Amount

1st Lien Term Loan $7,000

2nd Lien Term Loan 2,000

UAW VEBA due 1/1/2010 3,100

Total $12,100

L P

19

Where Do We Go From Here?

•All constituents faced with painful choices

•Need a plan with enough credibility among stakeholders that will keep the company on the field in the near term and allow it to thrive longer term

–Every stakeholder needs to contribute

–Stakeholder concessions today are an investment in the future

•Alternative is a disaster–S&P estimates recovery on GM unsecured debt in a bankruptcy at $0.05

–All contracts can be rejected in a bankruptcy

•UAW needs to be part of the solution but can’t be the only part

•UAW can play a significant role in the process

![[XLS]inls.orginls.org/INLS-life-members-list-2016.xlsx · Web viewKhaniya M. nasnani76@yahoo.com FL Prakash prakashnepal7@yahoo.com Neupane Devraj devaneupane@yahoo.com Niraula Bimala](https://static.documents.pub/doc/80x56/5aed65b37f8b9ac36191c89f/xlsinls-viewkhaniya-m-nasnani76yahoocom-fl-prakash-prakashnepal7yahoocom.jpg)