Aggregate Dynamics and Staggered Contracts Author(s): John B. Taylor Source: Journal of Political Economy, Vol. 88, No. 1 (Feb., 1980), pp. 1-23 Published by: The University of Chicago Press Stable URL: http://www.jstor.org/stable/1830957 . Accessed: 05/06/2014 03:02 Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. . The University of Chicago Pressis collaborating with JSTOR to digitize, preserve and extend access toJournal of Political Economy. http://www.jstor.org

Aggregate Dynamics and Staggered ContractsAuthor(s): John B. TaylorSource: Journal of Political Economy, Vol. 88, No. 1 (Feb., 1980), pp. 1-23Published by: The University of Chicago PressStable URL: http://www.jstor.org/stable/1830957 .

Accessed: 05/06/2014 03:02

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .

Staggeredwage contracts s shortas 1 yearare shownto be capableofgenerating hetypeofunemploymentpersistencewhich has beenobserved during postwar business cycles in the United States. Acontract multipliercauses business cycles to persist beyond thelength of the longest contract,and a diffusionof shocks acrosscontracts auses the persistenceto increase for several periods be-forediminishing.A persistence f inflation s also generatedbythecontracts. This persistence is represented as a reduced-form

distributed-lagwage equation in which the lag coefficientshave apure-expectations omponentand an inertiacomponentdue to theoverhang of outstandingcontracts.Using rational expectationstoseparate these components suggests that aggregate demand mayhave a greater impact on inflation han the simple reduced-formestimateswould indicate.

A distinctive feature of recent theoretical models of macroeconomic

fluctuations is the emphasis on partial rigidities, either in the form ofinformation lags or temporary inflexibility f prices and wages. Theserigidities have been remarkably successful in explaining observedcorrelations between such aggregates as inflationand unemployment,despite the constraints of rational expectations and a fixed naturalrate of unemployment. Indeed, statistical Phillips curves are an es-sential property of these models.'

I am grateful o GuillermoCalvo and Edmund Phelps for extensivediscussionsandto Larry Christianoforvaluable research assistance.This research is supported by agrant from the National Science Foundation.

l Models which have stressed informational igidities nclude Lucas (1973, 1975),Sargent nd Wallace (1975), and Barro (1976, 1978). Modelswhich have stressedwageor price rigiditiesnclude Fischer 1977) and Phelps and Taylor (1977). A recentpaperbyHall (1977) incorporates uch rigidities ut leaves open whethertheyare informa-[Journal fPoliticalEconomy, 980, vol. 88, no. 11? 1980 byThe University f Chicago. 0022-3808/80/8801-0010$02.00

1

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

As is well known, however, these models have been unable toexplain the observed serialcorrelation n unemploymentwithout he

imposition of additional sources of persistence-either exogenousserial correlation of shocks or capital formation ags. Neither infor-mational rigidities ortemporarywage and price contracts, herefore,have seemed capable of independentlygenerating the kind of serialpersistenceobserved in most modern economies.

This paper considers a rational expectations model in which wagecontracts are the only source of rigidity,yet which is capable ofendogenously generating serial correlation n unemploymentwhich

significantly utlasts the duration of the longest contract. Hence,contractswhich last only about 1 year can generate the degree ofcyclical persistence which has been observed in the United Statesduring the postwar period. Two key assumptions underlie themodel:2 1) wage contracts re staggered, hat s,notallwage decisionsin the economy are made at thesame time; and (2) when makingwagedecisions, firms and unions) look at the wage rates which are set atother firms nd which will be in effectduring theirown contractperiod. Because of the staggering, ome firmswillhave establishedtheir wage rates prior to the current negotiations,but others willestablish heirwage rates n futureperiods. Hence, whenconsideringrelative wages, firms nd unions must look both forward and back-ward in time to see what other workerswill be paid during theirown contract period. In effect, ach contract s writtenrelativetoothercontracts, nd thiscauses shocks tobe passed on fromone con-tractto another-a sort of "contractmultiplier." n statistical ermsthe overlapping contracts cause unemployment to follow a mixed

autoregressive-moving-averageprocess, rather than the relativelylow-order moving-averageprocess found in previous contract mod-els. The mixed process implies that the impactof shocks on unem-ploymentwillfirst ise for several periods beforedecreasing towardzero-a lag shape which s characteristic ftheunemployment ate inthe United States.

The concern of this paper, however, s not solelywithendogenouspersistenceof unemployment.As willbe shown below, contractfor-

tionor contractbased. The lack of persistence n models with ontract-based igiditieshas notbeen emphasized as muchas in models based on informationags. An examina-tion of the atter hree papers will ndicate,however, hat persistence funemploymentis veryshort without xogenous serial correlation.Sargent (1977) and Fischer (1979)are two recentpapers which examine thispersistenceproblem.

2 The 2-period versionof this contractmodel was suggested as a device to explainthe existenceof lagged inflation ates n a rationalexpectationsPhillips urvebyTaylor(1979). The implicationsof a multiperiodversion of the contractequation for thedesign of guideposts to reduce inflationwhile maintainingfull employment re dis-

cussed in Phelps (1978). Furtherreferencesto similar typesof models are given inPhelps (1978).

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

mation n thismodel generatesan inertiaofwageswhichparallelsthepersistence f unemployment.The econometricspecification f this

inertia s a wage equation which includes a distributed ag of pastwage rates-much like an expectations-augmented hillipscurve. Incontrast o other Phillipscurves,however,the distributed ag of pastwagesincorporatesnotonlytheexpectations ffuturewage decisionsbutalso theoverhang of previous wage decisions. Giventhe assump-tions of themodel, this ag shape has a predictableform: tdeclinessteadily verthe engthofthe lag and at a decreasingrate.Moreover,the lag shape depends on economic policy.A more accommodative

monetarypolicy, for example, tends to increase the sum of the lagweights nd thereby ncrease the serial persistenceof wages.This dependence of parameters on policy, a propertywhich has

been emphasized by Lucas (1976) in a related context,has botheconometric nd policy mplications. tsuggests hat twillbe difficultto estimatethe structuralparameters of themodel without knowl-edge of the aggregate-demandpolicyrule. It also suggeststhatthePhillips-curve olicytrade-offwilldepend on expectations fpolicy nfutureperiods, a pointwhichhas been discussed by Fellner 1976). Inparticular, ecause wage determinationsboth forward nd backwardlooking,aggregate demand may have a greater effecton inflationthan currentmodels of thePhillipscurvewould suggest. One advan-tage of themodel specifiedhere is that tpermits ne to calculate thesize of thisexpectationseffect.

Section introduces hestructuralmodel, and Section I derivestherational expectationsreduced-form contractequations. Because ofcertain ymmetriesn the contract quations and the policy rule,we

are able to make use offactorizationheoremswhichfrequentlyrisein time-seriesanalysis to derive explicit relationships among thereduced-formparameters,the structuralparameters, nd the policyrule. The spectral density functionof the contractwages is derivedand shownto be a convenientway to describe theirstochasticprop-erties when contracts re fairly ong. Section III describes the per-sistenceeffects generated by the model with 2-, 3-, or 4-quartercontracts nd compares these withthe actual persistence of unem-

ployment n the United States. In Section IV theeffect f aggregatedemand on wages, as implied by a particularpolicyrule, is comparedwith he conventional hort-run hillips-curve pproach for a certainset of parameter values. This comparison provides a way of separat-ing the impact of wage expectationsfrom pure wage inertia.

I. The Contract DeterminationEquation

As mentioned above, overlapping contracts are a key assumptionbehind the persistence effectsgenerated by thismodel. And while

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

pricecontracts re potentially s important s wage contracts,we willfocus on wage contracts n thispaper. We consider an economy in

whichall wage contracts re N periods long and a constantfraction1/Nof all firmsdetermine theirwage contracts n any given timeperiod.3A contract s assumed to specify implicitly r explicitly)fixednominal wage rate which will apply for the duration of thecontract;employment s then determinedby fluctuations n the de-mand for abor,giventhisnominalwage duringthe contractperiod.Let xt be the logarithmof thewage rate specified n contractsbegin-ning nperiod t.Then x,,whichapplies to 1/N f thefirms,willremain

ineffect ntilperiodt+ N-

1,whenit willbe changed toxt+. (Whilefor some purposes itmightbe useful to attach anotherindex toxt norder to represent particulargroup of firms,uch a notationwouldbe cumbersomeand does not directly elate to the resultspresentedhere. It should be noted, however, that whilextand Xt+Nefer to thesame group offirms, t nd xt+s or < N refer o different roups offirms.)

If contracts re set in thisway,theywillclearlyoverlap each other.At the timethata givenwage contract s in the processof being set,therewillbe an overhang of contracts et in the last N - 1 periodswhichwillstillbe in effect uringpart of thecurrent ontractperiod.Moreover,during the nextN - 1 periods, contractswill be writtenwhichwillalso be ineffect uringpartof thecurrent ontractperiod.Wage ratessetin thecurrentperiod should reflect hewage ratessetin these previous and future contracts.They serve as a base fordetermining he relativewage of the currentcontract.A simple andplausible wage-settingprocedure which weights other wage rates

proportionally o thenumber ofperiodsthey verlapwith hecurrentcontractperiod,and which s sensitive o excess demand in the labormarket, s then given by the log-linear form

N-1 N-1 N-1

xt=Ebsxts + Zbsit+s + N et+, + Et, (1)s=i s=l s=0

whereet s a measure of excess demand in the labor market et = 0representsfull employment),h is a positiveparameter, and Et is a

random shock, which will be assumed to be seriallyuncorrelated.(The "hat" over a variable representsthe mathematicalconditionalexpectationoperator, given information hroughtime t - 1.) Theweights n thefuture nd lagged contractwages are given bybs= (N

3 This uniformdistribution ssumption is made for simplicity.A nonuniform dis-tribution as long as it is not degenerate with all contractsset in 1 period) wouldintroduce easonal effectswhich,while mportant rom practicalpointofview,wouldnotalterthe generalqualitativefeaturesofthemodel. In thisregard it s interestingo

notethattheEconomist as recently uggested thatthedistribution f contractnegotia-tion n theUnitedKingdombe made less uniform, resumably o reduce overlapping.

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

- 1)-i (1 - s/N), = 1, 2, N - 1.Theydecline inearlynto hepastand future, nd they sum to one. Contracts lose to the current

contract re givenmostweight,while contracts n the more distantpastor future re given essweight.The symmetricinear decline is aresult of our assumption that these past and future wages areweightedproportionally o the number of periods theyoverlap withxt.Forexample, ifcontracts re N periodslong,thenkt?, ndxt~, for< N, willoverlap withx, forN - s periods each. The totalnumberofoverlappingperiodsfor all contractss,therefore, EN- (N - s) = (N- 1)N. The contracts?,8and xt,8should therefore ach be weighted

byN -s divided by (N - 1)N, which defines the b-weights.Theproportionalweighting chemedoes not allow foreitherdiscountingeffectswhichwould lead to a sharper decline on futureweightsorforgetting ffectswhich would lead to a sharper decline on pastweights.

In additionto pastand futurewages,equation (1) indicatesthat thecurrent ontractwage will be sensitive o expected labor marketcon-ditionsduring the contractperiod; thatis, xtwill respond to et, t+1,. e., I Equation (1) implies thatall of theseperiodsare weightedequallyand with weight1/N. Of course, 1/N ould be incorporatedin the parameter h, but we leave it explicit so that excess-demandeffects an be heldconstantwhen we considerchanges in thecontractlengthN.) It should be noted thatonlyexpected and notactual excessdemand in period t entersequation (1); it would be a relatively asymatterto include currentetin equation (1) and therebypermitthewage contract o reactsimultaneously o actual marketconditions nthe currentperiod.

Our assumption thatthecontractwage ratex, is fixedforthe entirelength of the contract mpliesheavyfront-end oading. That is, theentirewage adjustmentoccurs in the first eriod. Available informa-tion on explicitlong-termunion contracts ndicates that front-endloading is not generally this extreme. However, casual observationsuggests hatmost mplicit ontracts,which appear to be about 1yearin duration,are front-end oaded in this way.

In order toobtain a solutionforx,from quation (1), it s necessary

tomodel thedeterminants f the excess demand for abor etand therelationship etweencontractwages and prices. A very imple modelwhichachieves this end is given by

Yt+p, = m,+ v,, (2)N-1

Pt= + X-i(3)

i=()

et= g2yq (4)

Mt= g3pt, (5)

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

wherept = log of aggregateprice evel,yt= log of real output less logof full-employmentutput,mt= log of nominal money balances less

the og offull-employment oney balances, and vt = randomvelocityshock. Equation (2) is a simple quantity-theory epresentationofaggregate demand. It is written n deviation form; hence, yt = 0representsfull-employmentutput. The assumptionthat the elastic-ity f real balances withrespect to output is one introducesno loss ofgenerality, s will become clear below. The log of velocity t is as-sumed to be a serially uncorrelatedshock; thiswill highlightotherpersistenceeffects f the model.

Equation (3) statesthat the aggregateprice evel is determinedby asimple proportional markup over the average wage; hence, weabstractfrom the importantproblem of real wage and productivitychanges. The termN1 IN-01xtiis the logarithmof the geometricaverage of the contractwages in effectat timet. Equation (4) is asimple productionrelationshipwhich states thatexcess demand forlabor is a simple proportion of thedeviation of output fromtrend orfull-employment utput.

Equation (5) is thepolicy rule; g3 = 0 corresponds to a fixedmoneysupplywhileg3 > 0 allows for some accommodating ncrease in themoney supplyin response to price increases.By substituting4) into(1) and (5) into 2), we arrive at a simple two-equationrepresentationof the model:

N-1 N-I N-i

Xt= Zbsxts +Z t+. + N jt+S + Et, (6)8=1 8~~=1 ,=tO

t= -,apt + Vt, (7)

where y = hg2 and f3 (1 -g3). The parameter y is the majorstructuralparameter of the model. It represents the sensitivityfwages to aggregate-demand policy.The policyparameterf3measureshow accommodativeaggregate-demand policy is to changes in theprice level from ts long-run equilibriumlevel. We now turn to thederivation of the rationalexpectations solutionof the model.

II. The Reduced-Form ContractEquationDerivation

In order to eliminate the expectationvariables in equation (6), wemake use of the aggregate-demand policy rule (eq. [7]) and thedefinition f the aggregate price level in equation (3). That is, wesubstitute he conditional expectationof output

Yt+s =-/Pt+S =- t+S-i (8)

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

x ,bsXt-s + ,bsit+s- AY I , t+si-+ Et, (9)S=1 s=i s=0 i=O

where n = N- 1. Equation (9) involvesonlythe log of the contractwagextand itsexpectations. t statesthatthecurrent ontractwill beinfluencedbyrelativewage effectsrepresentedbythe firstwosumsineq. [9]) and also by the mpactofthe wage settlements n aggregatedemand, as impliedby thepolicyrule (this nfluence srepresentedbythe double sum in eq. [9]).

Taking expectations on both sides of equation (9), conditional oninformationvailable in period t - 1, and notingthe identity,4

n n n n

N2 N=Ibsxs + N+N E (10)

S=0 i=0S=I

where theb-weights re as in Section I, we have

( + - rN ) 1bskt's+ (I - )Ibst+s. (11)

Dividing throughby LI - (n,8/y/N)]nd rearrangingtermsreducesequation (11) to

n n

Ib.st-s - Ckt + Zbsit+s = 0, (12)S=1 S=1

where c = (N + /8y)/(N nr3y). Note that c is the only parameter ofequation (12) whichdepends on either the policy or the structuralparameters of the model. We assume that 0 83y o that

IcI

: 1.Using the lag-operator notation (Lsxt = xts), and defining thepolynomial

n

B(L)= >bsLs, (13)s=-n

where bo = -c and b-S = bs,s = 1, 2, . . .n, , equation (12) can berewritten

B(L)t = 0. (14)

Obtaininga unique rationalexpectationssolution to equation (14)involves some technical considerations. The polynomialB(L) hasnegative as well as positive powers of L; however, because of itssymmetrybs= b&s), tcan be factored nto a product of a polynomialinL and the same polynomial n L-l; that s,

B (L) = XAL)A (L-1), (15)

4

This identitys easilyestablishedusing induction.Note thatN times eq. (10) is anaverage of a sum, thatis, a Cesaro sum in the contractwage.

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

witha,, = 1. The canonical representation n equation (15) followsdirectly romfactorization heorems forsymmetric olynomials seeAnderson 1971, p. 224, e.g.), whichfrequently rise in the theory fstochasticprocesses. (It may be helpful to note that the problemofobtainingthefactorizationn eq. [15] is identicalwiththeproblemof obtaining the moving-averagerepresentation f a stochasticpro-cess given its autocovariance functionor correlogram.The poly-nomial [13] would be theautocovariance-generatingunction nd thecoefficient fA L] would be the coefficientsf the moving-averagerepresentation.)

From the factorization 15) we can obtaina unique rational expec-tations olution to (14) by imposingthe usual stabilityonditionandthereby hoosingthepolynomialA L) whichcorrespondsto therootsof B (L) that lie outside the unit circle.5 Again, the analogy from

stochasticprocesses s helpfulhere: our assumptionof stabilityorre-sponds to theassumptionof invertibilityf a moving-average rocess,which senough togivea unique representation.)Having chosen A L)in this fashion,we can then divide equation (14) by XA L-') to obtain

A(L)x= O. (17)

A comparisonof (17) with 9) indicatesthat the rational expectationsreduced-form tochastic ifference quation for the contractwage is

A(L)xt= Et, (18)

or, writing he lagged contracts n the right-hand ide of the equa-tion,

xt = a xt-1+ a2xt-2 + . + axt, + Et, (19)

where , = -ai, i = 1, . . ,n.

Note thatthere s an explicit etof constraintswhichthe structuralparametersy and f3,working hroughtheparameterb0,= -c, put onthis reduced-formequation. These constraintscan be derived byequating the coefficients f the polynomialson the left- nd right-hand side of (15) to obtain:

5 Let Xi, = 1, . , n be theroots ofB L) which ie outside or on the unitcircle;thenare theroots ofB(L) which ie within r on theunitcircle.The coefficientsfA(L)

are therefore qual to the coefficients f thecorrespondingpowersofL inflIn=L - Xi).

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

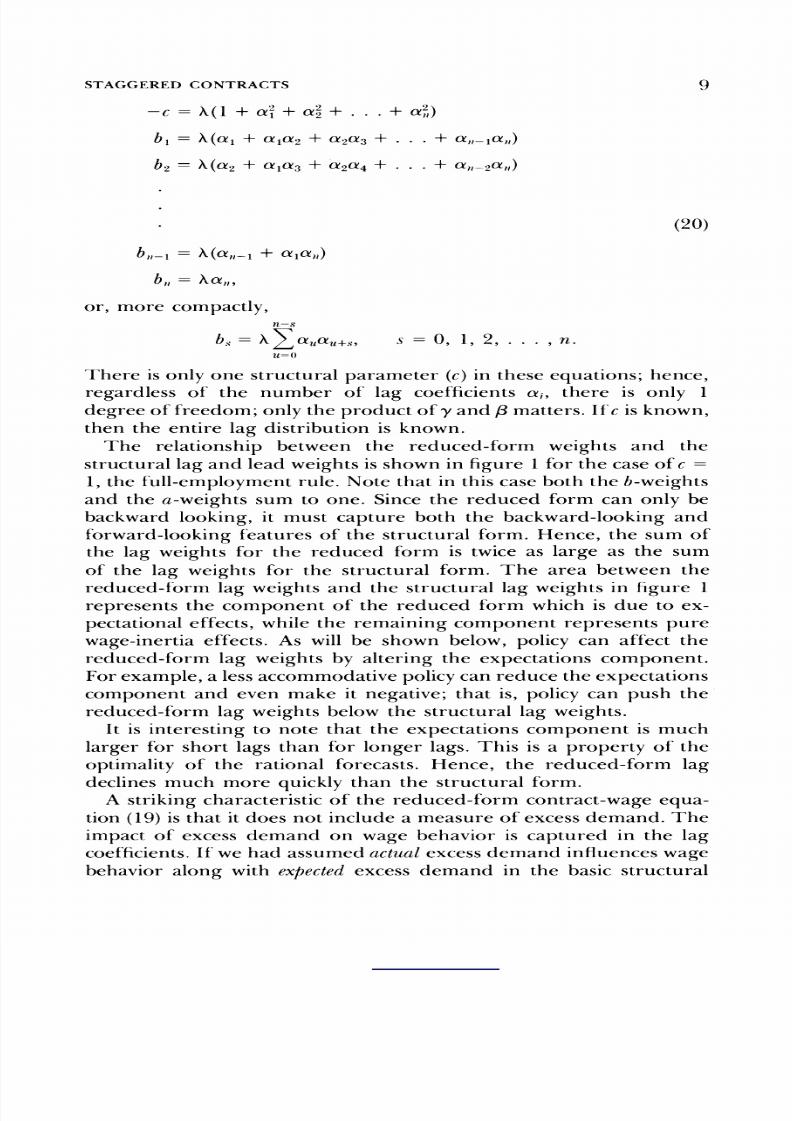

There is only one structural arameter c) in these equations; hence,regardless of the number of lag coefficients j, there is only 1degree of freedom; only the product of y and ,/matters. f c is known,then the entire lag distribution s known.

The relationship between the reduced-form weights and thestructural ag and lead weights s shown nfigure1 forthe case ofc =1, the full-employmentule. Note that n thiscase boththeb-weightsand the a-weightssum to one. Since the reduced form can only bebackward looking, it must capture both the backward-looking ndforward-looking eatures of the structuralform.Hence, the sum ofthe lag weights for the reduced formis twice as large as the sumof the lag weights for the structuralform. The area between the

reduced-form ag weightsand the structural ag weights n figure1represents he component of the reduced form whichis due to ex-pectationaleffects,while the remaining component represents purewage-inertia ffects.As will be shown below, policycan affectthereduced-form ag weights by alteringthe expectations component.For example, a less accommodativepolicy an reduce theexpectationscomponent and even make it negative; thatis, policycan push thereduced-form ag weightsbelow the structural ag weights.

It is interesting o note that the expectations component is muchlarger for short ags than for longer lags. This is a propertyof theoptimality f the rational forecasts.Hence, the reduced-formlagdeclines much more quicklythan the structural orm.

A striking haracteristic f the reduced-form ontract-wage qua-tion 19) is that tdoes not include a measure of excess demand. Theimpact of excess demand on wage behavior is captured in the lagcoefficients.fwe had assumed actual excess demand influenceswage

behavior alongwith

expectedxcess demand in the basic structural

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

FIG. 1.-Relationship between structural ontract wage equation and reduced form

equation (1), thenexcess-demandeffectswould be visible n equation(20). But even then, only unexpected excess demand would matter.Although the aggregate-demand ide of thismodel is very imple,thisfeatureof thewage equation is suggestive f the difficulties hich areinherent n econometric ttempts o estimate he impact of aggregate

demand on wage behavior. If the unemploymentrate were insertedon the right-hand ide of a regressionequation similar to (19), theestimatedcoefficient f the unemployment ate would have a proba-bility imitof zero.

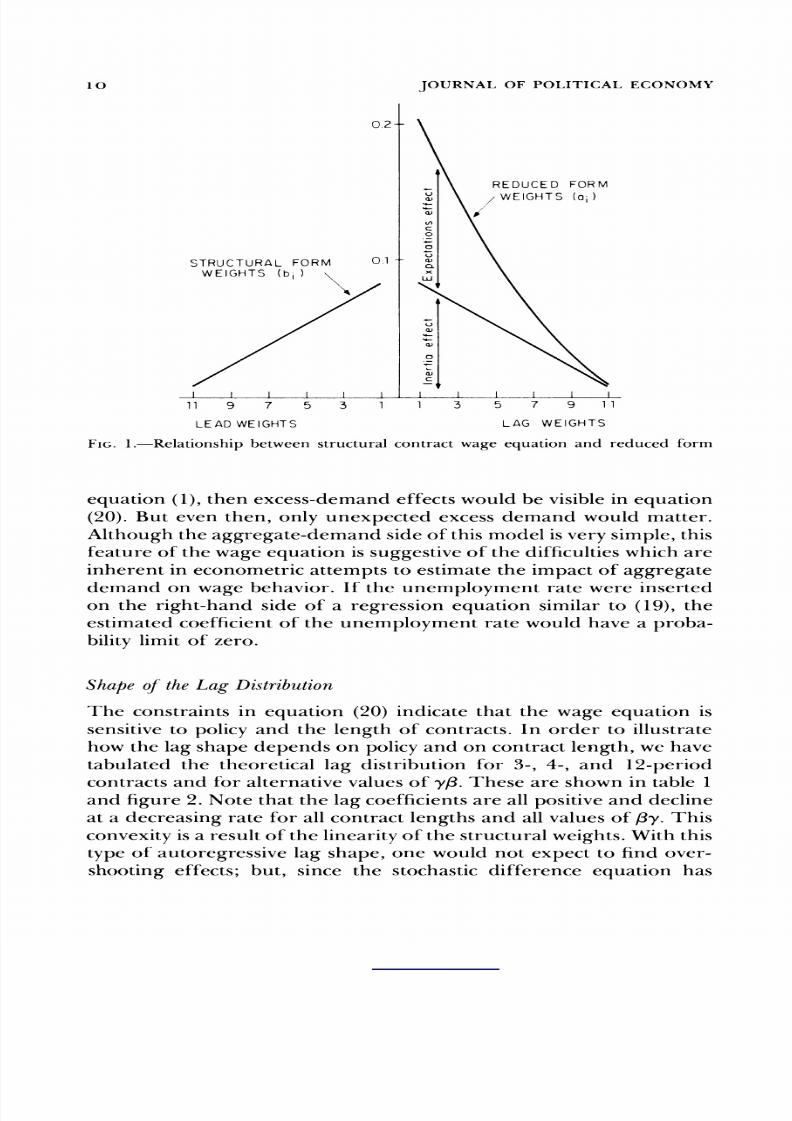

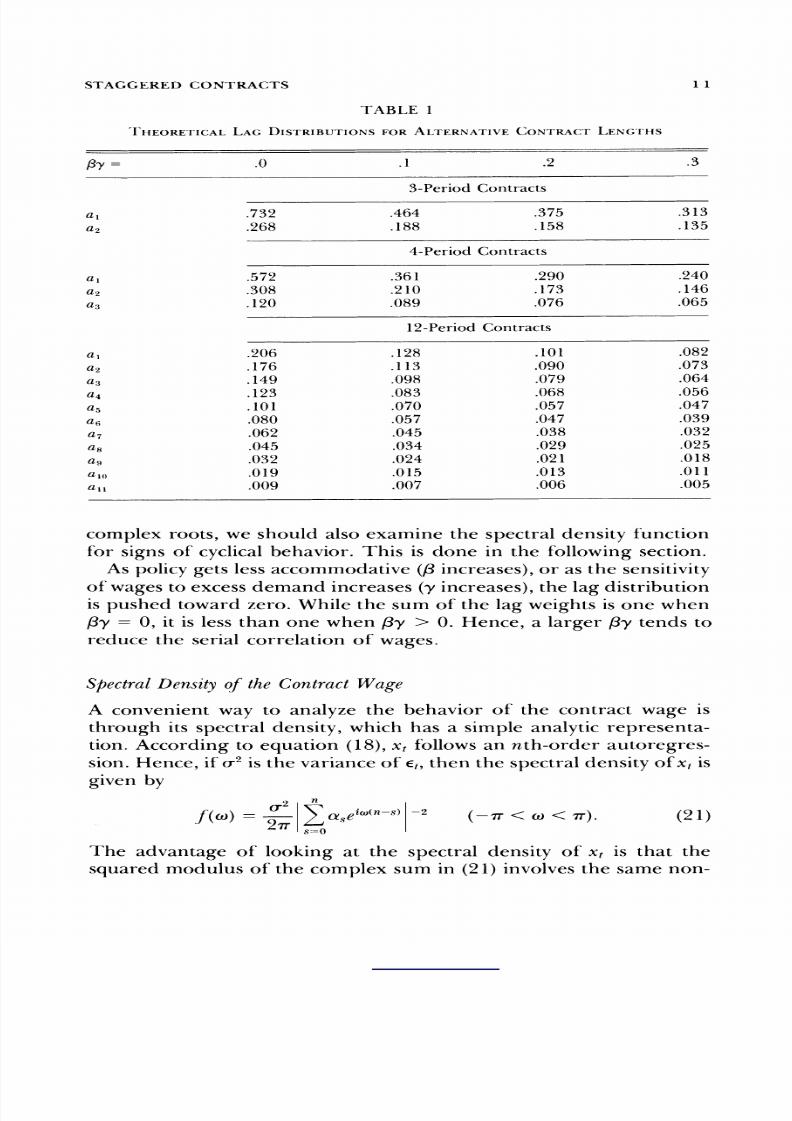

Shape oftheLag Distribution

The constraintsn equation (20) indicate that the wage equation is

sensitive o policyand the lengthof contracts. n order to illustratehowthelag shape depends on policy nd on contract ength,we havetabulated the theoretical ag distributionfor 3-, 4-, and 12-periodcontracts nd foralternativevalues of y,3.These are shown in table 1and figure2. Note that thelag coefficients re all positive nd declineat a decreasingrate for all contract engths nd all values of l8y.Thisconvexitys a resultof the inearity f thestructuralweights.Withthistypeof autoregressive ag shape, one would not expect to findover-

shooting effects; but,since the stochastic differenceequation has

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

complex roots,we should also examine the spectraldensityfunctionforsignsof cyclicalbehavior.This is done in the following ection.

As policygets ess accommodative f3ncreases),or as the sensitivity

ofwagesto excess demand increases y increases),the ag distributionis pushed towardzero. While the sum of thelag weights s one when

/(y = 0, it is less than one when f8y 0. Hence, a largerf3y endstoreduce the serial correlationof wages.

Spectral ensity f theContractWage

A convenientway to analyze the behavior of the contractwage is

through ts spectraldensity,whichhas a simple analyticrepresenta-tion. Accordingto equation (18), xtfollows n nth-order utoregres-sion. Hence, ifo-2is the varianceof Et, then thespectraldensity fx( isgivenby

J(as()=1as eiwO(n-s) -2

(-IT < Ct0 < or) . (21

The advantage of looking at the spectral densityof xt is that thesquared modulus of the complex sum in (21) involvesthe same non-

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

linear functions f the a coefficients hatwere found on the right-hand side of 20). Hence, wecan utilizetheformulas n (20) to obtain:

27r t A An E (1 coscnl2 bo (1 2 sin2/(N )1 (22)

27r A An An 2N sin (1/2W)

The second equality in (20) follows froma trigonometricdentitywhich rises nthe analysisof Fourier series see Lanczos 1966, p. 56).The expression sin2 '/2coN)(2IrNsin2 V/2co)-s known as Fejer's kerneland frequentlyccurs in studiesof the serialcorrelationpropertiesofaverages.

We know from he firstquation of (20) thatX< 0; hence,J(co)willhave maxima and minimaat the same values of coas Fejer's kernel.

6 See Anderson (1971, pp. 508-9) for a descriptionof the qualitativefeatures ofFejer's kernel. We make use of these features n analyzing eq. (22).

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

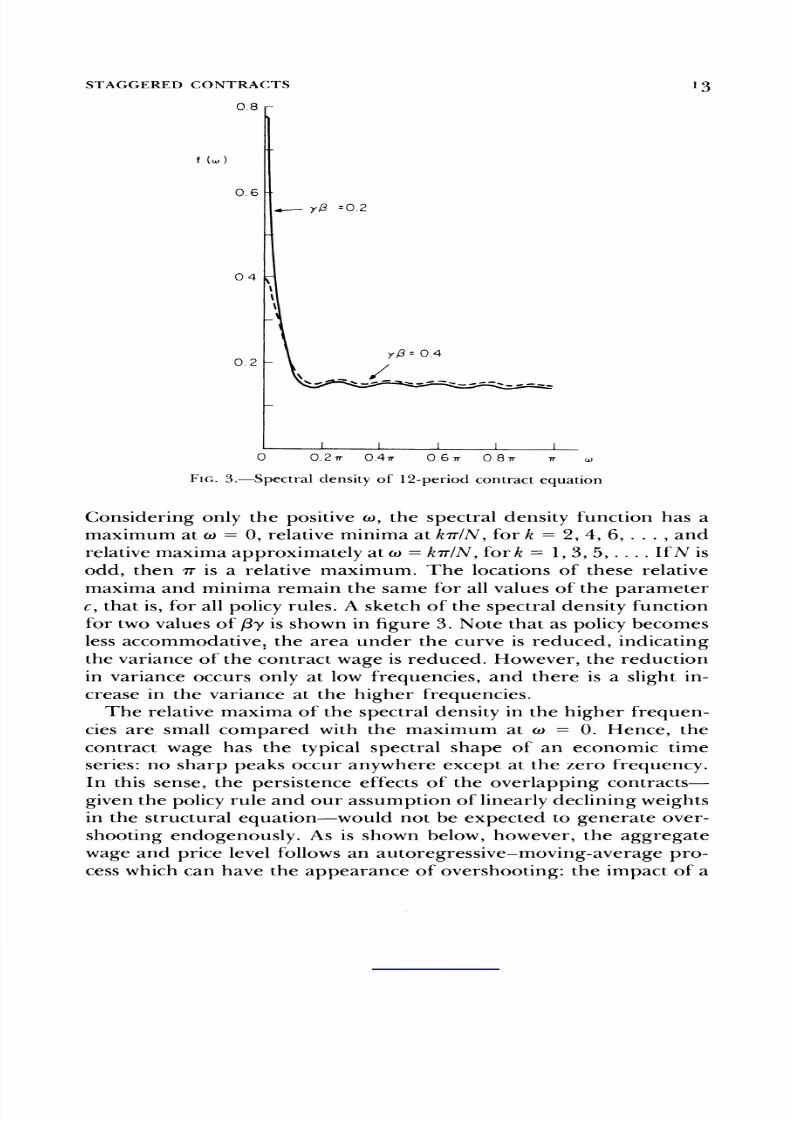

Considering only the positiveco,the spectral densityfunctionhas amaximumatw= 0. relativeminimaatkiriN, ork = 2, 4, 6, . . ., andrelativemaxima approximately tco= k7rN,fork= 1, 3, 5, IfN isodd, then 7v is a relativemaximum. The locations of these relative

maximaand minima remain thesame forall values of theparameterc, that s,forall policyrules.A sketchof thespectraldensityfunctionfortwo values of fBys showninfigure3. Note thatas policybecomesless accommodative,the area under the curve is reduced, indicatingthevarianceof the contractwage is reduced. However,thereductionin variance occurs only at low frequencies,and there is a slight n-crease in the variance at the higherfrequencies.

The relativemaxima of the spectral density n the higher frequen-

cies are small compared with the maximum at co = 0. Hence, thecontractwage has the typical spectral shape of an economic timeseries: no sharp peaks occur anywhereexcept at the zero frequency.In this sense, the persistence effects f the overlapping contracts-giventhepolicyruleand our assumptionoflinearlydecliningweightsin the structural quation-would not be expected to generate over-shooting endogenously.As is shownbelow, however,the aggregatewage and price level follows n autoregressive-moving-average ro-cesswhich

can have the appearance of overshooting:the impactof a

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

shock on the wage level can increase from its initial value for anumber of periods before diminishing oward zero.

III. Aggregate Dynamics and the Persistence ofUnemployment

Equations describingthe macroeconomic dynamicsof the model canbe derived by aggregatingthe contractwages todeterminetheaggre-gate wage and price level. Let

I n

D(L) = _ ILs (23)

be the unweightedmoving-average perator. Then, fromthe defini-tion of the aggregate price level in equation (3) of Section I,

pt = D (L)x,. (24)

Substitution f (24) into the contractwage equation (19) yieldstheaggregate price equation

A L)p, = D (L)Et. (25)Hence, the price evel follows n autoregressive-moving-average ro-cess,ARMA (n,n). The autoregressivepart of theprocessis the sameas that of the contract equation (19). In a deterministicperfectforesight ersion of this model, the aggregate equation would there-fore be described by the same differenceequation as the contractwages. Given equation (25), the behavior of aggregate output caneasilybe determinedfrom he aggregate-demand quation (7), that s,

Yt = -,pt + Vt- (26)

Aggregate output, therefore,has the same basic stochastic tructureas theprice evel.Of course,the realizationsofoutputwill ook muchdifferent hanthose of the pricelevel.The larger/ is, the largertheoutput fluctuations elative to price fluctuationswillbe. And, exceptfor the influence of velocity hocks, output and priceswill tend tomove in opposite directions. This result follows directlyfromour

simple quantitytheoryof aggregate demand combined witha fixedrule for money-supply ehavior.In the extremecase of thefixedandknown money supply (/3= 1), real output must fall by the sameproportion that the price level rises.

PersistenceEffects

The potential for this model to exhibit high serial correlation in

unemployment s evidentin

equations (25) and (26). Recall thatthe

unemployment ate is assumed to be proportionaltoyt.The autore-

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

gressive erms nequation (25) prevent he serialcorrelation etweenytand y,+,fromhitting ero as soon as s is greater than the contract

length. nstead,thecorrelationbetweenyt ndy,?;diminishesgradu-allyand approaches zero only asymptoticallys s -x oc. If the sum oftheautoregressive oefficientsn (25) is large,thenthe serial correla-tion willremain high forvery ong lags.

These general featurescan be illustratedn the case of two-periodcontractsN = 2). In thiscase, equation (25) becomes

Pt= alpt,+ Et + 21 I ?O al 1. (27)

From 20), a,- a, = c - .- 1 The ARMA (1,1) model in (27)can be inverted n order to represent , as a function f the Et only.That is,

Pt= 2[Et + qJFEit + f2Et-2 + . (28)

where

hi = at1(I + a,), i = 1, 2, (29)Fromequation (26), outputthenhas themoving-average epresenta-tion

Yt = Vt- -[Et + qJjEt- + 02Et-2 + . . ]- (30)2

According to equation (29), the ip weightsincrease for one lagbeforedecreasing geometrically o zero. If a, were close to 1, as it

would be ifyf3were small,thenthe qpweightswould decline to zerovery lowly ndytwould showhighcorrelation.On the otherhand, ify/3were large, the serial correlationwould be weaker but wouldnevertheless onverge to zero only asymptotically.

It is instructiveo compare thetype of serialpersistencegeneratedby this model withthe observed serial persistenceof unemploymentin the United States. The ip weights n the moving-averagerepre-sentation 30) are useful for thispurpose. Table 2 compares the qp

weightsmplied bythe modelwith he actual qPweightsfor theunem-ployment ate forthe case where velocity hocks are negligible vt =0). The estimated P weightswere obtained by first stimatinganARMA (2,1) process forthequarterlyunemployment ate formales20 and over (to avoid labor force compositionshifts), nd then bywriting hisprocess in pure moving-averageform.7The resulting Pweightsforthe sample period 1954: 1 through 1976:4 are given in

'The ARMA model was u, = 1.39u,-, - .49u,_2+ r, + .27rt, where u, is the

quarterlyunemployment ate and r, is the seriallyuncorrelatederror term.Nelson(1972) found thissame model adequate forthe 1947:1-1966:4 period.

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

Noi E:.-Ihe observed pi are obtained by estituating rlARMA (2,1) mttodel or the uttteneploymtentrate for ttales20 and over andtlnvertingtto obtainthe pure utoving-average ormt;he theoreticalweights re describedill thetext. 3 = .5, y = .2; contract ength:N = 2, 3, or 4 quarters.

the fourthcolumn of table 2. The estimatediPweightsshow a ten-dencytorise forthe first ewquartersand then decline fairlyteadily.

The theoreticalweights re reportedin the first hreecolumns oftable 2 forcontractengths f 2, 3, and 4 quarters,respectively. hesehave been calculatedusing the parametric ssumptionthat,8= .5 andy = .2 (or,more generally, haty/3 .1). The resultsfor the 3- and4-quarter contracts ppear quite similarto the observed serial corre-

lationin unemployment.The lag weightsrise for the first ew quar-tersbeforebeginning odiminishratherrapidly.However, the case of2-quarter ontracts ppears togivesubstantiallyess serialcorrelation.To some extent, these results are dependent on our parameterchoice; forexample, a largervalue for8-ywould reduce persistencebut would notchange the general humped shape of the lag distribu-tion. n any case, theresults howthecapability f this ypeof contractmodel to explain the observed persistence n unemployment-evenwhen there s no other source of persistence nd contract engths re

reasonably short.

A StatisticalhillipsCurve8

An essentialrequirement f a theoreticalmacromodel s that texhib-its a statistical hillips curve. Although the model of thispaper in-

' This section owes much to discussions I have had with Edmund Phelps on thissubject.

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

cludes a monetarypolicy rule which forces a positive correlationbetweentheprice eveland theunemployment ate,there does exist a

negativecorrelationbetween the change in the price level and theunemployment ate. To see this,consider the covariance betweeny,andp+i - p, forthe case of N = 2. If thiscovariance is positive, henthereis a statistical hillipscurve. From equation (28),

Pj+j -' E'+j + I(i -i-i)eti, (31)

and the covariancebetweeny,and PtI - pI is

E[yj(p+l-PI)] = 13[(iJ- 1 + v (qh, 01iii- 14

= - /3[a,+ ja~i(a, - 1)(1 + al)21 4i=9) 2 (32)

=- f3[al-(1 + a,)] 4

4,which s positive.Hence, duringboom periods,whenoutputis abovethe full-employmentevel, inflationwill be higher on the average.Note that the size of this covariance depends directly n aggregate-demand policy. Recall the assumptionthatpriceshocks and velocityshocksare uncorrelated. f there is a positivecorrelationbetweenv,and E,, then the above covariance would be larger.) The theoreticalregression oefficientfpt+l - Ptonyt s givenby 13/2.ence, themore

The policyproblem n thismodel is one ofstabilizing he fluctuationsofoutputabout itsfull-employmentevel and fluctuations fthepricelevel about itssteady state evel. The dimensions of the problemare

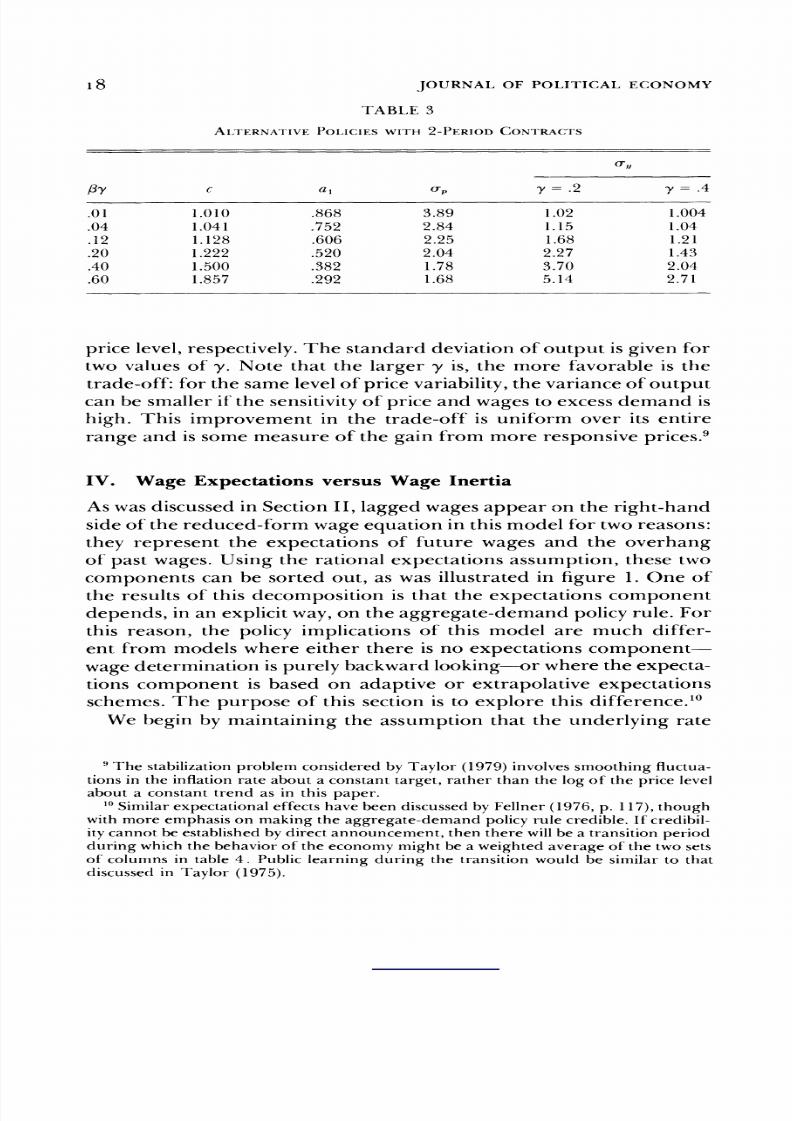

evident in equations (25) and (26). According to (26), when theaggregate-demandreactionparameter s zero, thevarianceofoutputisat its minimumvalue, which s equal tothevariance ofv,.However,when 8= 0 thevarianceoftheprice level s infinite,orthen the sumoftheautoregressiveweights nequation (25) isone. As thevalue of/3is increased,thevariance of theprice evelwillfalland thevarianceofoutput will rise. The resultingtrade-offbetween the variability foutputand prices s illustratedn table3 forthe case ofN = 2; theo-Yand o-. columns refer to the standard deviation of output and the

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

price evel, respectively. he standard deviationof output s given fortwo values of y. Note thatthe larger y is, the more favorableis thetrade-off: orthe same levelof price variability,he varianceof outputcan be smaller fthe sensitivityf price and wages to excess demand ishigh. This improvement n the trade-off s uniform over its entire

range and is some measure of the gain frommoreresponsiveprices.9

IV. Wage Expectations versus Wage Inertia

Aswasdiscussed nSectionII, lagged wages appear on theright-handsideof thereduced-formwage equation inthismodel fortworeasons:they representthe expectationsof futurewages and the overhangof past wages. Using the rationalexpectations ssumption,these two

componentscan be sorted

out,as was illustrated n

figure1. One of

the resultsof thisdecomposition s that theexpectationscomponentdepends, inan explicitway,on the aggregate-demandpolicyrule.Forthis reason, the policy implicationsof this model are much differ-ent from models where either there s no expectationscomponent-wagedeterminationspurelybackward ooking-or where theexpecta-tionscomponent is based on adaptive or extrapolative expectationsschemes.The purpose of this section s to explore this difference.'0

We begin by maintainingthe assumptionthat the underlyingrate

9 The stabilization roblemconsidered by Taylor (1979) involves moothingfluctua-tions n the inflation ateabout a constanttarget, atherthan the log of the price levelabout a constanttrend as in thispaper.

10Similarexpectational ffects ave been discussedby Fellner 1976, p. 117), thoughwithmore emphasis on making theaggregate-demand policy rule credible. Ifcredibil-ity annot be establishedby direct nnouncement,then there willbe a transition eriodduring which the behavior of theeconomy mightbe a weighted verage of the twosetsof columns in table 4. Public learning during the transitionwould be similarto thatdiscussed in Taylor (1975).

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

of inflation s zero, so that the steady-state verage price level isconstant.One of the objectivesofdemand policy s to stabilizefluctu-

ationsof prices (or wages) about thisconstant evel. (The case of arising-price ath can be considered using similartechniques.) It willbe convenient o considerthe problemwithin he contextof a singlerealization f a priceshockwhichraises, say,theaggregateprice levelabove itsequilibriumvalue. The objectiveof policy,therefore, s tobring the price level back to equilibrium.The appropriate rate ofreturn oequilibriumwilldepend on therelativeweights fprices andoutput in the social welfarefunction: quick return fpriceshave a

highweight,or a slow return foutput has a highweight.Assume thatN = 2 and that n aggregate-demandpolicyruleof theformdiscussed in thispaper is in forcewhen thispriceshockoccurs.This rule might have been the resultof decisionsmade withinthepoliticalprocess and whichplanned for such shocks, o thatwhen theshockoccursthere is no pressure to change therule. For illustrationpurposes,assume thattherule is,8= .5, thaty = .2, and thatE1 = 10percent Es = 0, s > 1). Ifp0 = 0 and E0 = 0 (i.e., thepricelevel was inequilibriumbefore the shock), thenpf = 5 and p, followsthe path

Pt= alpt-lEl2 E+ 2' t= 2, 3, . ,(33)

where a1 = .63. The pathforoutputis thengivenbyy -2.5, and

y,= -.5p,, t = 2, 3, .... (34)

For these numericalvalues, the two paths are given in table 4. The

convergencefthe price evel toequilibrium srelatively uickdespitethe accommodatingstrategy. f ifwere greater than .5, the return

wouldbe faster, ut the oss ofoutputwould be larger;converselyf/3were less than .5.

To compare theseresultswith model whichdoes not incorporateforward-looking age determination r which s based on extrapola-tiveexpectations, onsider equation (1) in the case ofN = 2,

Hence, either currentwage negotiations gnore futuredevelopmentsor they simplyextrapolate current developments by forecasting t+lwith t-Iandyt+?withyt-i. he aggregate price level is then given by

Pt=

Pt-i+

2 (Yt-I+

yt-2)+

Et

E2

1

(38)

The policy implicationsof equation (38) are clearly much differentfromequation (34). The path of the price level using (38) is given intable4 forthe same path of output considered above (startingwithPo= 0,Yo = 0, and E() = 0). It is evident that the reduction in the pricelevel is much smaller than in the case of rational forward-lookingexpectations; ccordingtoequation (38), a much larger ossof output

would be required to bring the price level back to the target path atthe same rate implied by equation (34). Price stability ppears to bevery ostlywhen expectations re not rationalor contracts o not ookforward.The differencebetween the twomodels provides a simplemeasure of the "expectation bonus" which comes from rational an-ticipatorywage determination.The difference ndicates that rationalexpectationsmattergreatly-despite the existence of contracts-formacroeconomic stabilization. t also indicates the need to determineempiricallywhetherwage-contractdecisions rationally nticipate inthisway.

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

The analysisof thispaper has centeredon a stationary conomywithstaggeredoverlapping wage contracts nd rational expectations.Theaggregate dynamics of thiseconomy-when subjectto continual de-mand and price shocks-were examined under alternativemonetarypolicy rules. In order to emphasize endogenous persistenceeffects,these shockswere assumed to be seriallyuncorrelated.

The results of the analysis can be summarized as follows. Persis-tenceofunemploymentimilar o that bserved ntheUnited States an

be generated by the model when contracts re 3 or 4 quarters longand there are no other sources of persistence.The time shape of thedynamic impact of shocks on unemployment-rising for severalquarters before tapering off-is characteristic oth of the estimatedprocess for unemployment nd the theoreticalprocess mplied by themodel. Moreover, the model generates a persistence of wages andpriceswhichgives rise to a statistical hillips urve and which presentsa policytrade-offbetween price stability nd output stability.Thepersistenceof wages has both an expectational component and aninertiacomponent, and these can be decomposed using the rationalexpectations pproach. Policy affects he behaviorofwages and em-ployment by altering the expectations component of persistence.Hence, the econometric wage equations depend on the policy rule,and the estimated impact of aggregate demand on wages will bebiased, unless expectations of policy n futureperiods are accountedfor.

By viewing he logarithms fthe price evel, the contractwage, and

the money supply as deviationsfrom a linear trend,all the resultspresented here carry over to an inflationary conomy. The policyproblem then would be to stabilize prices as well as output about anexponentiallygrowingtarget path. Given an aggregate-demand pol-icy rule, price shocks above thispath are followedby lower ratesofinflation nd higher unemployment,until the price level returns tothetargetpath; converselywithnegative price shocks. The statisticalPhillips urve derivedin SectionIII would be evident n the data left

by these paths fthe econometricianwere careful to take deviationsofthe nflation atefrom he underlying nflation ate before computingthe regressions.This Phillips curve would convey little nformationabout the sensitivityf wages or prices to excess demand, however.This sensitivity ould be implicitnthe reduced-formwage equations(again in deviation from trend form)derived in Section II, but itcould notbe extractedwithoutknowledgeof the policyrule. Finally,aggregate-demand policy makes a substantialdifferencefor the be-haviorof output, wages, and prices. The choice of a target rule foraggregate-demand policy is thereforeno less importantthan the

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

choice of a targetunemploymentrate or a target nflationrate. Itshould thereforebe considered as carefullyn the politicalprocess as

the other two targetstypically re.

Appendix

The Reduced-Form ContractEquation When Shocks AreCorrelated

In order to emphasize the persistencegenerated bythe staggeredcontracts,we have assumed that both velocityshocks and wage shocks are seriallyuncorrelated. n some applications,however,one mightwantto allow forthe

possibilityhat these shocks are correlated.The purpose of thisAppendix isto show how the solutiontechnique introduced in Section II can be used tohandle the case of serially orrelatedshocks.

Let thewage shockEAnd thevelocityhock v, nequations (6) and (7) ofthetext be represented as

et= A1 8iul-i (A 1)i=O

and

v,= IOimqt-i, (A2)i=()

where (u,,-q,)s a seriallyuncorrelatedrandom vector withzero mean andwhere6( = 0( = 1. Using this erialcorrelation tructure o forecast utput asin equation (8) and substitutingntoequation (6) gives

l Ifl n Uly

x

xt a, bsxw-+ Z, b,,+, - 1 a t+s-s+ - pt- + Eu?_i, (A3).8=1 S=l 8S=() i=() i=1i=

wherePi=

jnf+'i6. Taking expectations on both sides of (A3) and using theidentity 10) yields

Using the lag polynomialnotationas in Section II, thiscan be written

B L)t I-(1 - "') [-kR(L)i, + zX(L)i41, (A5)

whereR(L) = S1itlpiLj and A(L) = Yi;-=,iL. The polynomialB (L) is the same

as that nequation (14). Hence, itcan be factored sB (L) = XAL)A (L-1); andbydividingboth sides of (A5) byXAL-1), we have

A(L)k, = X- -n-3Y) L-)H(L)i, + G(L)itl, (A6)

whereH(L) is a polynomialobtainedbyomitting ll terms nvolvingnonposi-tivepowers ofL in the polynomial A(L-1)1-'R(L), and G(L) is a polynomialobtained by omittingall terms involvingnonpositivepowers of L in thepolynomial A L'1)]-'A(L). The nonpositivepowersofL cancel becauseL-,= ijt+s = 0 for 0 and L-uit = ,+, = 0 for : 0, sincetheexpectations reconditional on information hrough period I - 1 and mq,nd ut are each

This content downloaded from 146.155.94.33 on Thu, 5 Jun 2014 03:02:32 AMAll use subject to JSTOR Terms and Conditions

seriallyuncorrelated.Comparing (A6) with A3) indicates that the reduced-formcontract quation is givenby

A (L)x, =- lI - ) (L)-q, + G(L)ut] + u,. (A7)

Equation (A7) determines hecurrent ontract nterms f past contracts, astshocks, nd the current ontract hock. From thisrelationship he behavior oftheaggregate price level and aggregate output can be derived following hetechniques described in Section II.

References

Anderson, Theodore W. The StatisticalAnalysi'sof limes Series. New York:Wiley, 1971.

Barro,RobertJ. Rational Expectations nd the Role ofMonetaryPolicy."J.Motietary Econ. 2 (January 1976): 1-32.

"A Capital Market n an EquilibriumBusinessCycleModel." Mimeo-graphed. Univ. Rochester, Dept. Econ., 1978.

Fellner, William J. Towards a Reconstructionof Macroeconomics: Problems ofTheory nd Policy.Washington:American Enterprise nst., 1976.

![Taylor Series[1]](https://static.documents.pub/doc/80x56/577d388c1a28ab3a6b980b9b/taylor-series1.jpg)