10

1 The German model of risk distribution in supplementary occupational pensions Csaba Burger, Gordon L Clark Exeter, 7th January 2010

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 214 times |

| Download: | 0 times |

1

The German model of risk distribution in

supplementary occupational pensions

Csaba Burger,

Gordon L Clark

Exeter, 7th January 2010

2

Research background

• The German pension reform of 2001 was a milestone on the road towards pension individualisation; it

• decreased the level of the public pensions;• enhanced the voluntary, funded, occupational (and private) pension system

(Riester-pensions); • and therefore shifted investment risks to employers and individuals.

• The aim of this research is to

• Understand the nature of risk involved in the new occupational pensions;• Discuss the importance of the employee’s risk-related decisions;• Investigate the employee-level determinants of risk-related decisions.

• Our paper• Gives an overview of German occupational pensions from the nineteenth

century onwards;• Explains the unique, low-risk environment of the German pension system;• Reinforces existing research on risk-aversion and behavioural finance.

3

Occupational Pensions in Germany – the legal environment

Right to occupational

pensions

Immediate risk sharing

Institutional risk sharing

At the employer

All risk at the employee

No strong legal requirements

Some employee rights

Employee has the right for an

occupational pension

Employers bear the risk of pension provision

Minor institutional protection (with some external

providers)

Complex institutional protection

Before 1974

1974 – 20011974:

Occupational Pensions Act

After 20012001: „Riester”

Pension Reform

Sources: BetrAVG, VAG, Wiedemann (1991)

4

Two choices define the risk situation: scope and sharing

Choice I:Risk Scope

• Direct insurance• Life insurance: taken by the

employer, beneficiary is the employee

• Provided by life insurers• Low administrative burden

• Pensionskasse• Traditional institutions with the

exclusive mission of pension provision

• Similar rules to direct insurance

• Pension funds• New institutions in 2001• Aim: to imitate the returns of the

Anglo-Saxon pension funds• Liberal investment policies

Choice II:Risk Sharing (from the Employee’s View)

• Defined benefit• Guaranteed positive rate of return• Permitted defined rate of return is

maximised for new contracts: decreased from 3.25% in 2002 to 2.25% in 2008

• (German) Defined contribution• Guaranteed non-negative rate of

return• Nominal value of contributions

plus subsidies (less the cost of insurance) must be guaranteed

Low risk in these occupational pensions

5

Investment and institutional regulations limit occupational products’ risk exposure

Regulation of investment risks Institutional regulation

• Regulated by the Insurance Act(s) and Solvency II (EU-directive)

• Quantitative (asset allocation) requirements

• Rules on permitted asset types, asset mixing, geographical regions, etc.

• More liberal rules for pension funds

• Reporting and controlling processes• Regular ALM reports• Mandatory stress-tests with 4

scenarios• Transparency requirements

• Tight supervision, intervention rights (BAFin)

• Liability order for pension provision:

1. External provider, if fails, then

2. Re-insurer: Protektor AG (for pension funds: PSVaG), if fails, then

3. Employer

• Not all Pensionskassen are re-insured – in exchange for even tighter supervision

6

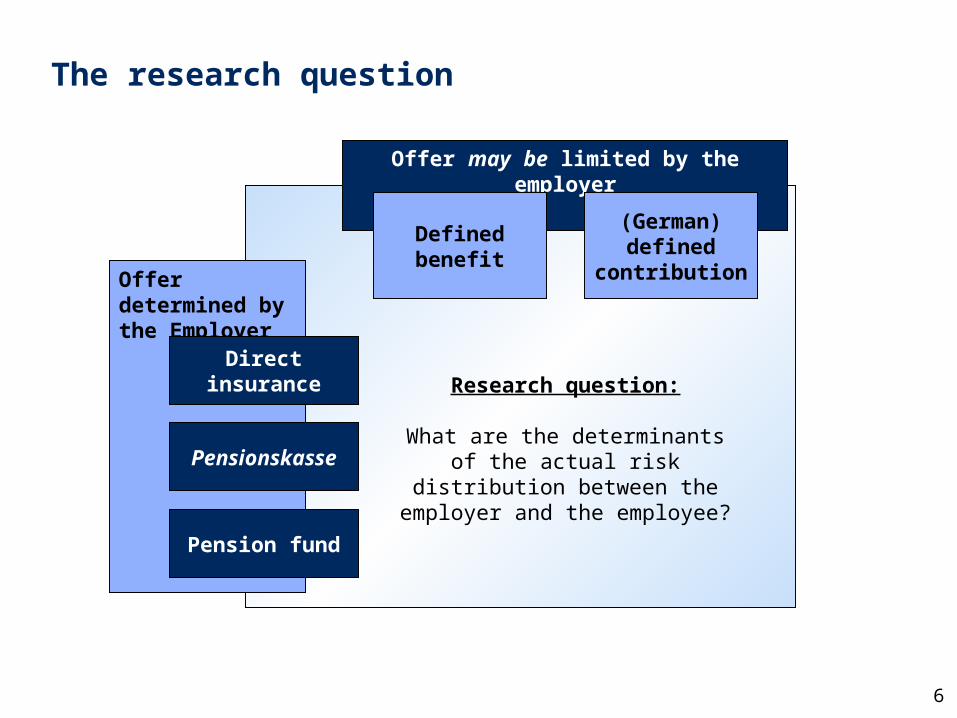

Offer determined by the Employer

Offer may be limited by the employer

The research question

Pensionskasse

Direct insurance

Pension fund

Defined benefit(German) defined

contribution

Research question:

What are the determinants of the actual risk distribution between the

employer and the employee?

7

Decisions are modelled by binary-logistic and multinomial regressions on a unique, proprietary database

Data

• Database of a German occupational pension provider

• 270 000 employees, linked to • 12 000 employers

• Details of the pension contracts• Enrolment dates from the start of

2002 till the end of 2008

1. Product choice

2. Defined benefit or defined contribution

Dependent variables

Explanatory variables

• Gender• Age in the year of enrolment• Yearly contribution amount• Source of financing (if there is

employee contribution)• Enrolment year (2002, 2003, …, 2008)

Employer offer

8

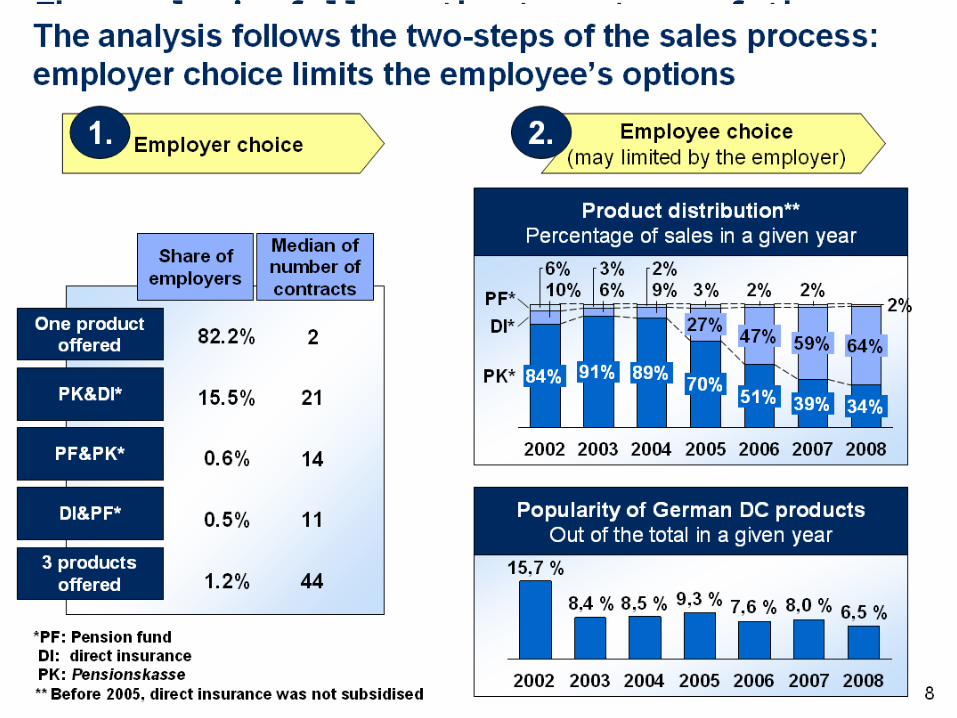

The analysis follows the two-steps of the sales process: employer choice limits the employee’s options

9

Findings reinforce existing theories and show the specialities of the German situation

Results

• Similar results both for product choice and for DB-DC variables

• Usual risk-related variables• Gender, age are have explanatory power: male and the young are more

risk-tolerant• The higher the savings amount, the more risk the employee is willing to

take• No employee financing implies the most risk-averse product

• Specific environmental characteristics• The later the enrolment happened (2002-2008), the less risk the individual

was willing to take• The financial crisis of 2008 hardly had any effect – results are a part of a

greater trend• Employer: the larger the company, the more options are available; the

more likely employees choose risky products

• Germany is distinctive for the low risk environment rather than the low risk-tolerance

10

• Beckstette A. und Zwiesler H.J. (2004): ‘Die Abgrenzung beitragsbezogener Pensionspläne aus Sicht des Asset-Liability-Managements’. Preprint Series. Fakultät für Mathematik und Wirtschaftswissenschaften Universität Ulm

• Börsch-Supan, A., Reil-Held, A. and Schunk, D. (2008) ‘Savings incentives, old-age provision and displacement effects: evidence from the recent German pension reform’. Journal of Pension Economics & Finance, 7 (3): 295-319

• Burger, Cs (forthcoming) ‘The role of social partners in transforming the German welfare state’. Draft version of the paper is available from the author at request.

• Clark G L, Knox-Hayes J, Strauss K (2009) ‘Financial sophistication, salience, and the scale of deliberation in UK retirement planning’. Environment and Planning A 41(10) 2496 – 2515

• Strauss, K (2009) ‘Cognition, context, and multimethod approaches to economic decision making’. Environment and Planning A 2009, volume 41, pages 302-317

• Wiedemann, G (1991) Die arbeitsrechtliche Entwicklung der betrieblichen Altersversorgung in Deutschland 1920-1974. Archiv für Sozialgeschichte 1991/31, pp 157-178.

Selected references