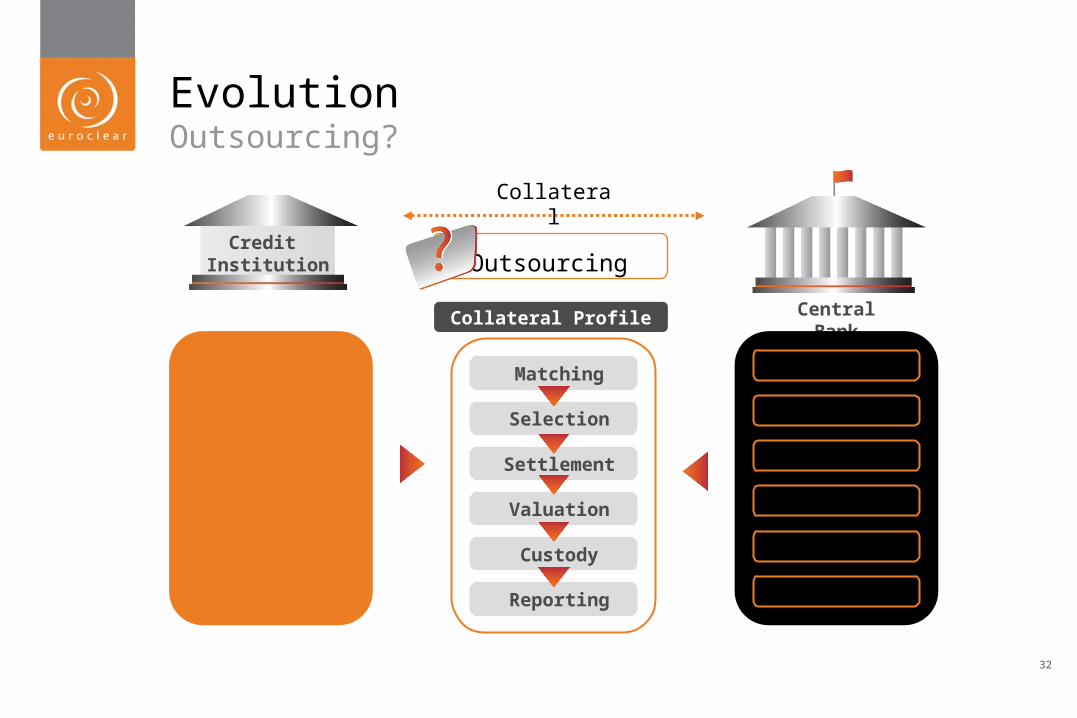

• Collateral Allocation Interface – Central Bank model

AMEDA – Beirut 29 April 2010Agenda

3

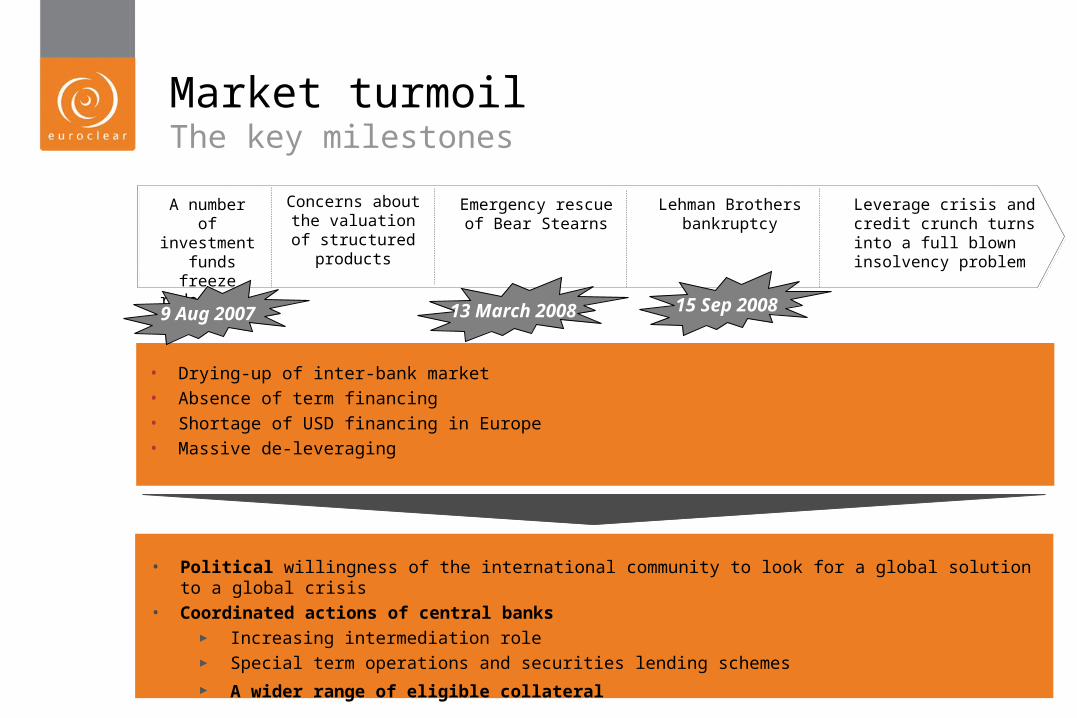

Lehman Brothersbankruptcy

A number of investment funds freeze redemptions

Leverage crisis and credit crunch turns into a full blown insolvency problem

Emergency rescueof Bear Stearns

• Drying-up of inter-bank market• Absence of term financing• Shortage of USD financing in Europe• Massive de-leveraging

Concerns about the valuation of

structured products

• Political willingness of the international community to look for a global solution to a global crisis• Coordinated actions of central banks

► Increasing intermediation role► Special term operations and securities lending schemes► A wider range of eligible collateral

9 Aug 2007 15 Sep 200813 March 2008

Market turmoilThe key milestones

4

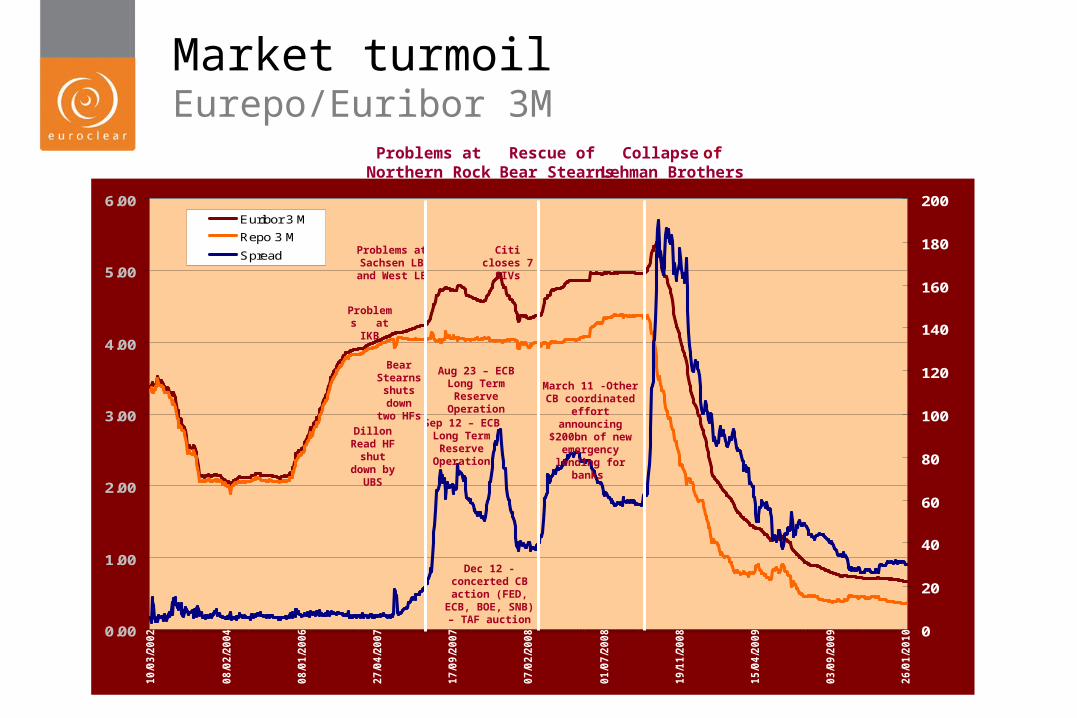

Market turmoilEurepo/Euribor 3M

Rescue of Bear Stearns

0.00

1.00

2.00

3.00

4.00

5.00

6.00

10/0

3/2

002

08/0

2/2

004

08/0

1/2

006

27/0

4/2

007

17/0

9/2

007

07/0

2/2

008

01/0

7/2

008

19/1

1/2

008

15/0

4/2

009

03/0

9/2

009

26/0

1/2

010 0

20

40

60

80

100

120

140

160

180

200Euribor 3 M

Repo 3 M

Spread

Collapse ofLehman Brothers

Problems atNorthern Rock

Problems at IKB

Problems at Sachsen LB and West LB

Dillon Read HF

shut down by UBS

Bear Stearns shuts down

two HFs

Citi closes 7 SIVs

Aug 23 – ECB Long Term

Reserve Operation

Sep 12 – ECB Long Term

Reserve Operation

Dec 12 - concerted CB

action (FED, ECB, BOE, SNB) – TAF

auction

March 11 -Other CB coordinated effort

announcing $200bn of new emergency lending for banks

5

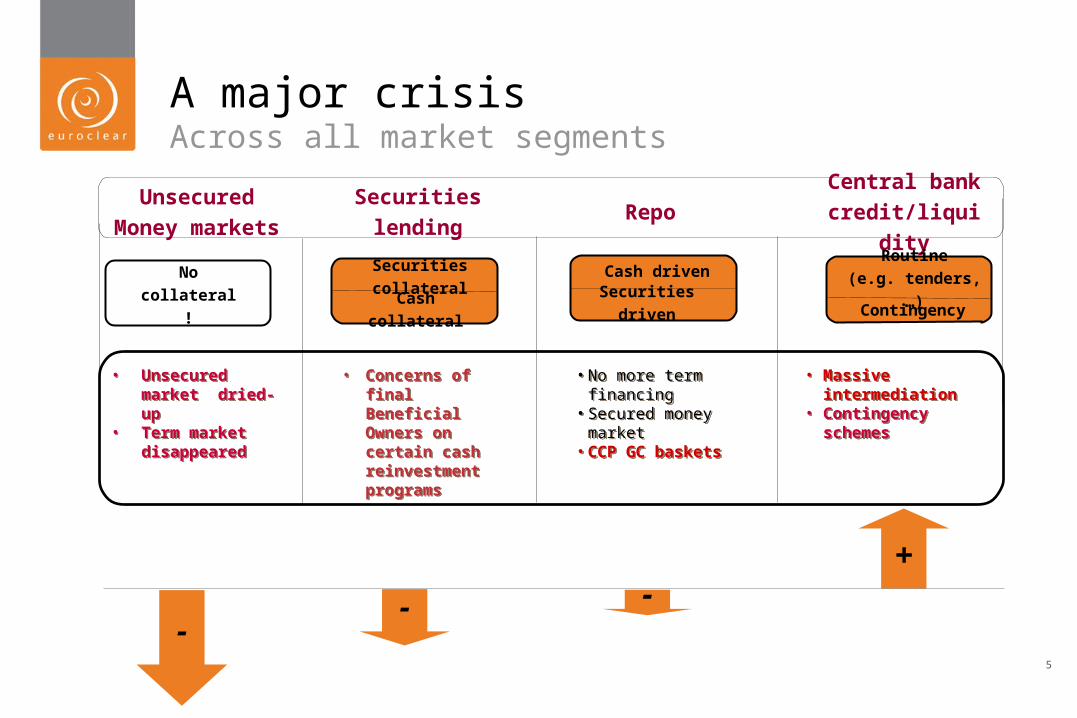

• Unsecured market dried-up

• Term market disappeared

• Unsecured market dried-up

• Term market disappeared

• No more term financing

• Secured money market

•CCP GC baskets

• No more term financing

• Secured money market

•CCP GC baskets

• Massive intermediation

• Contingency schemes

• Massive intermediation

• Contingency schemes

UnsecuredMoney

markets

No collateral !

Central bank credit/liquidi

tyRoutine

(e.g. tenders, …)Contingency

Repo

Cash drivenSecurities

driven

Securities lending

Securities collateral

Cash collateral

• Concerns of final Beneficial Owners on certain cash reinvestment programs

• Concerns of final Beneficial Owners on certain cash reinvestment programs

+

---

A major crisisAcross all market segments

6

• By order or priority, the money-markets investors will focus on

► Credit/counterparty risk

► Liquidity risk

► Return

What investors focus on ?Priorities

Need to find a secured financing solution

The repo markets

7

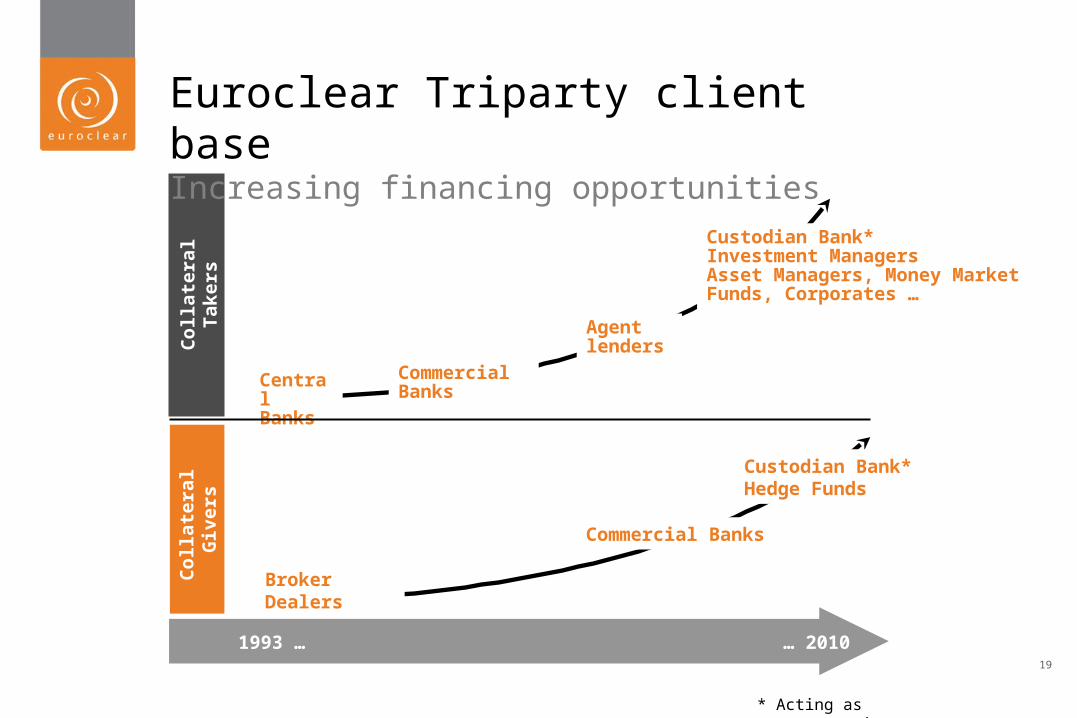

From Unsecured to Secured FinancingThe club is growing

• Unsecured is no longer an option• Move to the secured space, in particular to the repo space• However, managing collateral brings new challenges:

►Operational risks, substitution, settlement, corporate actions, valuation, etc.

►Requires resources and know-how

•Cash investors (e.g. MMF, Corporates, hedge funds, insurance companies) as new entrants in collateral management opt for the Triparty Solution

8

• Introduction

• Repos and the repo markets

• Triparty collateral management

• Collateral Allocation Interface – Central Bank model

AMEDA – Beirut 29 April 2010Agenda

9

• What is a repo?► Repo can be defined as an agreement in which one

party sells securities or other assets to a counterparty, and simultaneously commits to repurchase the same or similar assets from the counterparty, at an agreed future date, at a repurchase price equal to the original sale price plus an interest

• History of repo► Created by the Federal Reserve Bank of New York in

1916► Boosted by the Glass-Steagall act of 1933 when US

investment banks massively started to fund their inventory (development of the ‘general collateral repo’).

Repos and the repo marketsAn introduction

10

• What are the different repo products?► “Repos” – borrow of cash against securities► “Reverse repos” – investment of cash against

securities► “SecLending” - borrow against cash► “Total Return Swap”

Repos and the repo marketsAn introduction

11

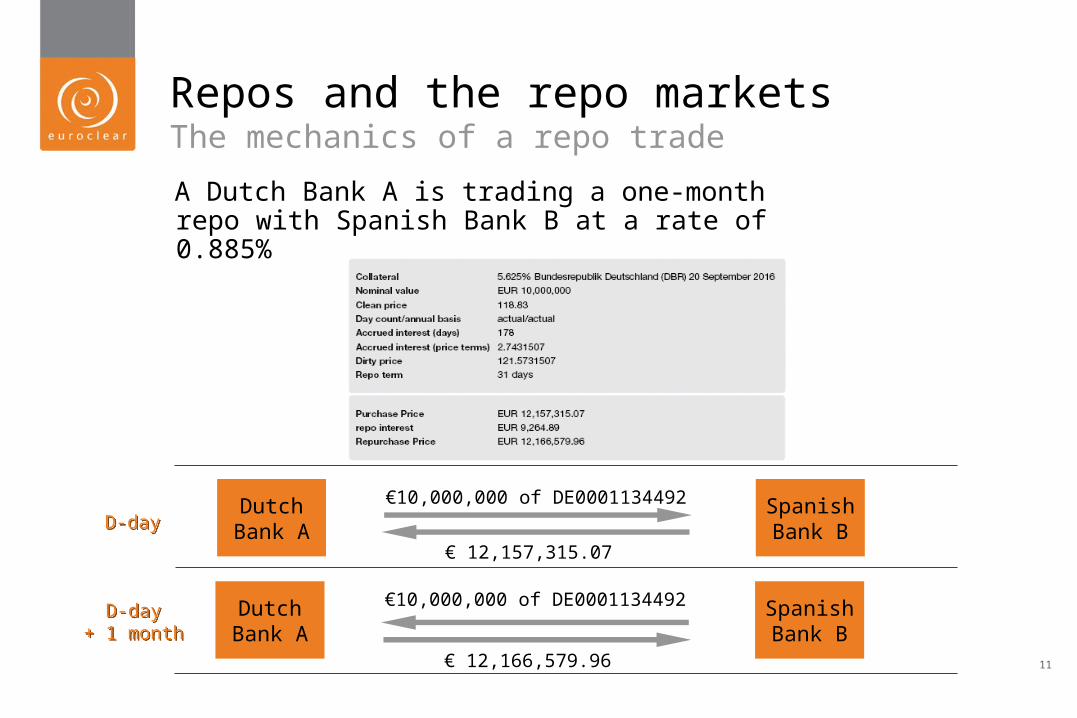

A Dutch Bank A is trading a one-month repo with Spanish Bank B at a rate of 0.885%

SpanishBank B

€10,000,000 of DE0001134492DutchBank A

€ 12,157,315.07

D-dayD-day

D-day+ 1 month

D-day+ 1 month

SpanishBank B

€10,000,000 of DE0001134492DutchBank A

€ 12,166,579.96

Repos and the repo marketsThe mechanics of a repo trade

12

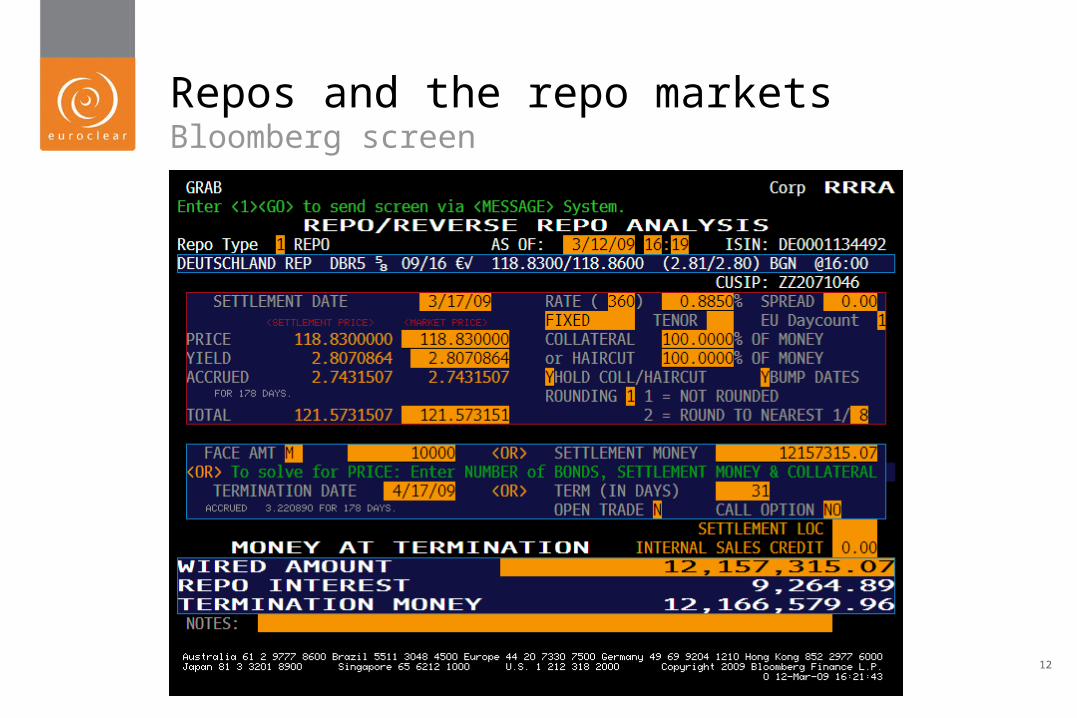

Repos and the repo marketsBloomberg screen

13

• Firm financing► Borrowing cash to fund long positions in securities

• Match book trading► Traders make two-way dealing prices on repo

• Securities lending► Borrowing of securities to cover short positions► Structured trading

Repos and the repo marketsThe functions of a repo desk

14

• Legal risk► Market standard legal agreements (e.g. GMRA)

• Risk of default of counterparty► Thorough selection of counterparties

• Market and liquidity risk on securities collateral► Clear definition of acceptable collateral► Imposed diversification through concentration limits► Over-collateralisation of transactions through margins

Repos and the repo marketsRisks and risk mitigation

15

ICMA Survey (in €bn)

4,868

4,633

2,298

6,5046,3826,4305,883

5,000

3,7883,377

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2001 2002 2003 2004 2005 2006 2007 June 08 2008 June 09

ICMA Survey

Repos and the repo marketsThe European repo market

16

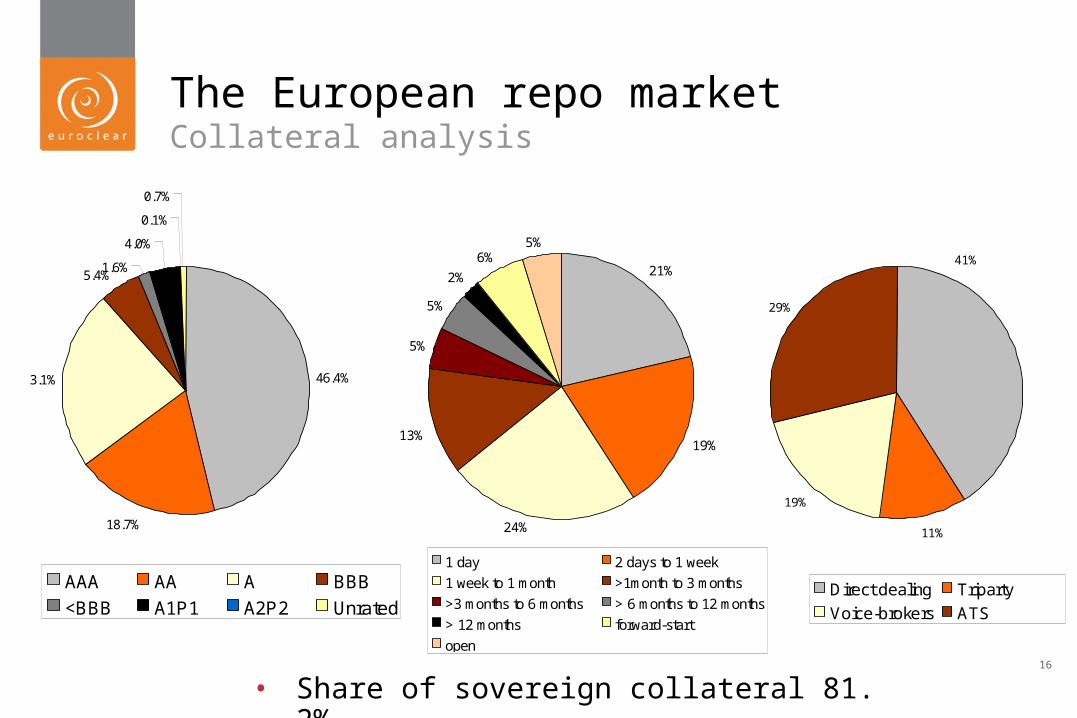

The European repo marketCollateral analysis

46.4%

18.7%

23.1%

1.6%

4.0%

0.1%

0.7%

5.4%

AAA AA A BBB

<BBB A1P1 A2P2 Unrated

21%

19%

5%

5%

2%

6%5%

24%

13%

1 day 2 days to 1 week

1 week to 1 month >1month to 3 months

>3 months to 6 months > 6 months to 12 months

> 12 months forward-start

open

11%

19%

29%

41%

Direct dealing Triparty

Voice-brokers ATS

• Share of sovereign collateral 81. 2%

17

• Introduction

• Repos and the repo markets

• Triparty collateral management

• Collateral Allocation Interface – Central Bank model

AMEDA – Beirut 29 April 2010Agenda

18

Triparty Collateral ManagementHistory

• Bevil, Bressler and Schulman, a US securities firm► Bankruptcy in 1985► Hold-in-custody (HIC) repos► ‘Double-dipping’

– BB&S was using the same piece of collateral for more than one repo

► Loss of over $1bn

• The US Securities and Exchange Commission (SEC) asked US banks Chase Manhattan Bank and Bank of New York to become custodians for repos (“Triparty agents”)

• Triparty was launched in Europe in the early 90’s

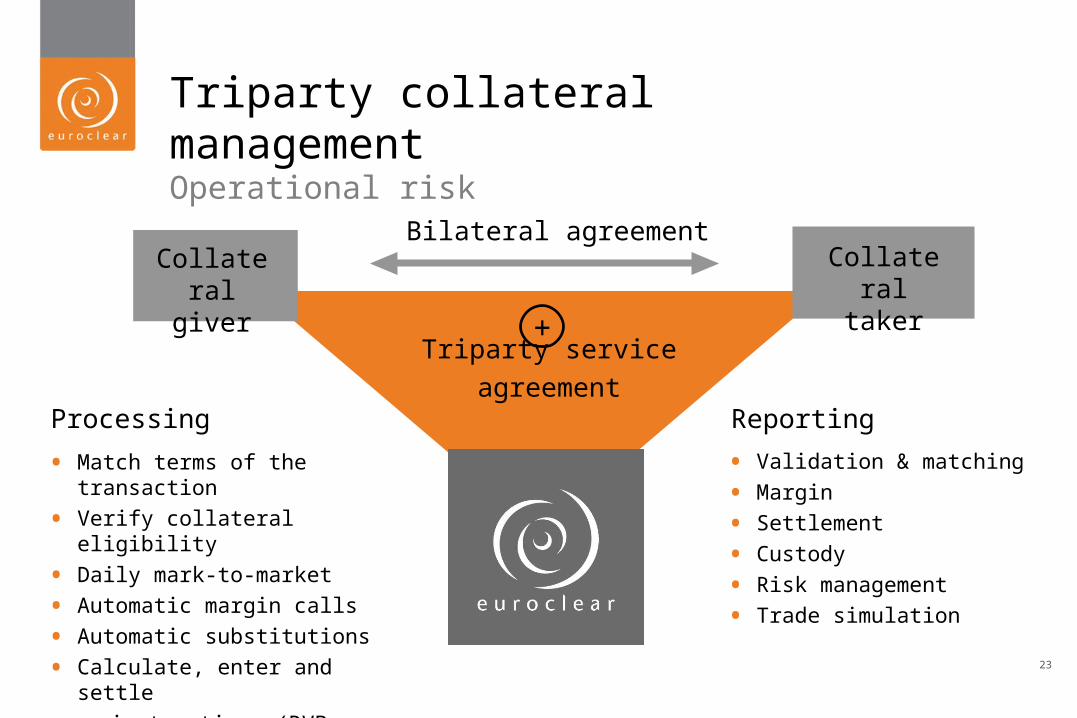

• Legal risk► Market standard legal agreements (e.g. GMRA)

• Risk of default of counterparty► Thorough selection of counterparties

• Market and liquidity risk on securities collateral► Clear definition of acceptable collateral► Imposed diversification through concentration limits► Over-collateralisation of transactions through margins