36

10 commandments of Captive auto financing in India February 2016

10 commandments of

Captive auto financing in India

February 2016

Page 2

The Indian auto and auto finance industry is steadily moving toward recovery

Auto financing market in India – Point of view

Improving socio- economic

environment

► Current Account Deficit declined from a peak of 6.7% of GDP (in 3Q, 2012–13) to an estimated 1% in 2014–15, 26% growth in FDI in 2015

► 10% growth in disposable incomes, 2/3rd of Indian population in working age

GDP growth projections FY16 7.5%

1

Turnaround in auto industry

The Indian automotive industry is moving on its path of recovery, and is expected to gain further impetus in the medium term, mainly driven by:

► Economic growth ► Reduced fuel prices ► Government’s focus on road development

Expected 5 year CAGR: ~12%

2

PV Finance largest and expected to

grow

► PV finance forms the largest segment of auto financing Industry at ~INR 761 Bn (~60% share).

► PV finance penetration set to grow again buoyed by underlying asset sales, new customer segments and entry of new players in the market.

Expected 5 year CAGR: ~17%

3

PV finance market is evolving

► Entry of fleet operators has created a new customer segment; rural market continues to grow; financiers have to innovate faster to tackle competition

► Ubiquitous nature of internet usage has made customers more knowledgeable, demanding of hassle free service and bundled products and services

Ability to innovate has become critical

4

Used car financing is also growing

► The used car market is currently 1.2X of the new car market, with organised share of used car financing at 14% only

► The average age of used cars is 4 years and reducing product lifecycle will ensure further penetration

Expected CAGR 14%%

5

*Source: SIAM, RBI Data, EY Analysis

Page 3

Captives are emerging as a key driver of growth and innovation in the Industry

Auto financing market in India – Point of view

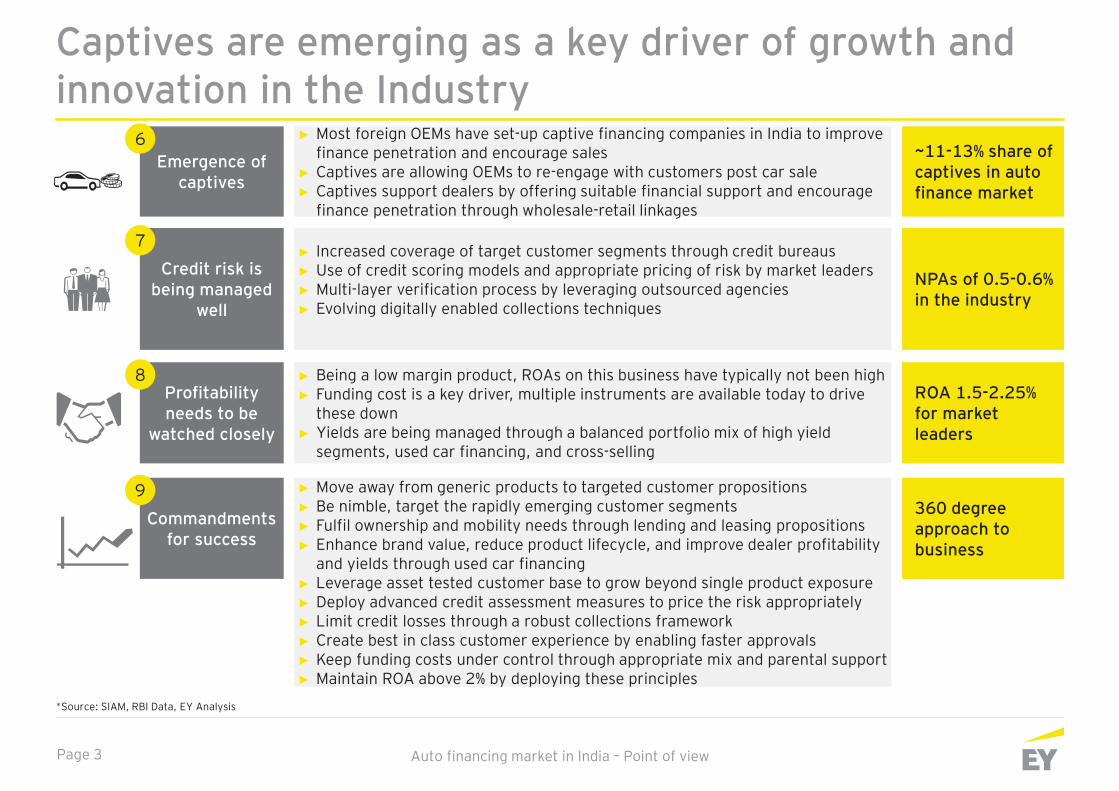

Emergence of captives

► Most foreign OEMs have set-up captive financing companies in India to improve finance penetration and encourage sales

► Captives are allowing OEMs to re-engage with customers post car sale ► Captives support dealers by offering suitable financial support and encourage

finance penetration through wholesale-retail linkages

~11-13% share of captives in auto finance market

6

Credit risk is being managed

well

► Increased coverage of target customer segments through credit bureaus ► Use of credit scoring models and appropriate pricing of risk by market leaders ► Multi-layer verification process by leveraging outsourced agencies ► Evolving digitally enabled collections techniques

NPAs of 0.5-0.6% in the industry

7

Profitability needs to be

watched closely

► Being a low margin product, ROAs on this business have typically not been high ► Funding cost is a key driver, multiple instruments are available today to drive

these down ► Yields are being managed through a balanced portfolio mix of high yield

segments, used car financing, and cross-selling

ROA 1.5-2.25% for market leaders

8

Commandments for success

► Move away from generic products to targeted customer propositions ► Be nimble, target the rapidly emerging customer segments ► Fulfil ownership and mobility needs through lending and leasing propositions ► Enhance brand value, reduce product lifecycle, and improve dealer profitability

and yields through used car financing ► Leverage asset tested customer base to grow beyond single product exposure ► Deploy advanced credit assessment measures to price the risk appropriately ► Limit credit losses through a robust collections framework ► Create best in class customer experience by enabling faster approvals ► Keep funding costs under control through appropriate mix and parental support ► Maintain ROA above 2% by deploying these principles

360 degree approach to business

9

*Source: SIAM, RBI Data, EY Analysis

Table of contents

1. The automotive environment

2. The auto finance market

3. 10 commandments

4. About EY

The automotive environment

Page 6

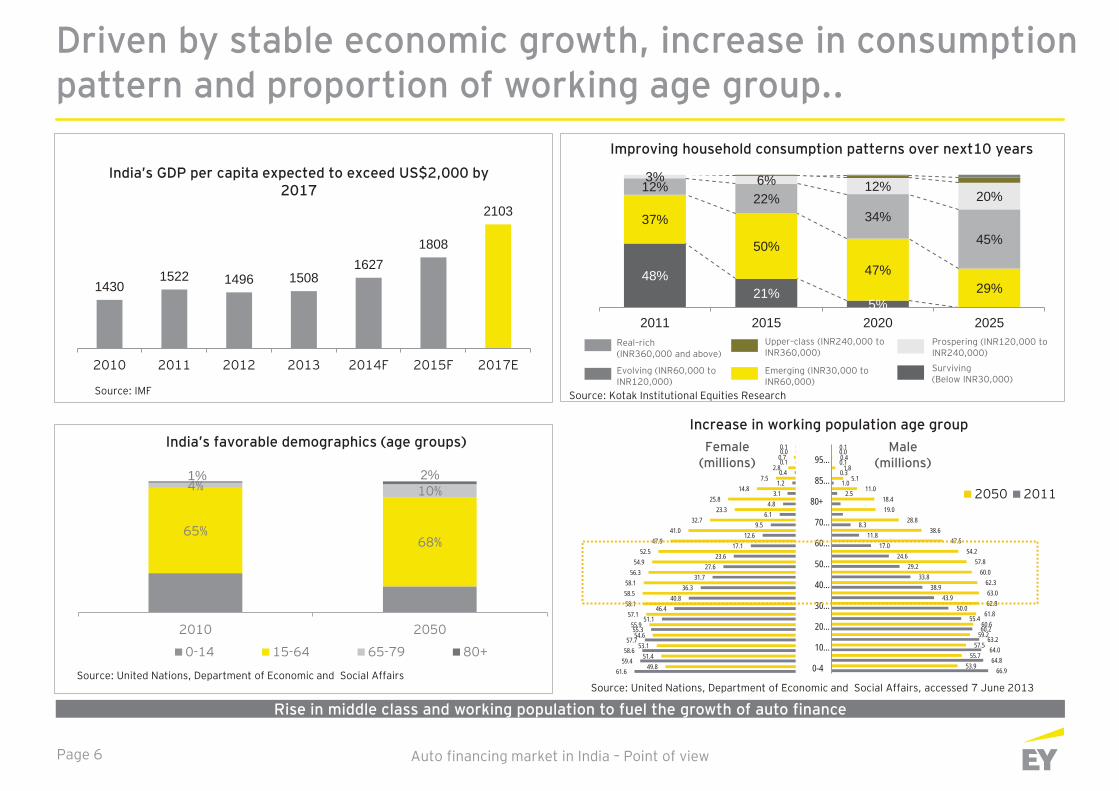

Driven by stable economic growth, increase in consumption pattern and proportion of working age group..

Source: IMF

India’s GDP per capita expected to exceed US$2,000 by 2017

1430 1522 1496 1508

1627 1808

2103

2010 2011 2012 2013 2014F 2015F 2017E

Real–rich (INR360,000 and above)

Prospering (INR120,000 to INR240,000)

Upper–class (INR240,000 to INR360,000)

Emerging (INR30,000 to INR60,000)

Surviving (Below INR30,000)

Source: Kotak Institutional Equities Research

Evolving (INR60,000 to INR120,000)

Improving household consumption patterns over next10 years

48% 21%

5%

37%

50%

47% 29%

12% 22%

34%

45%

3% 6% 12% 20%

2011 2015 2020 2025

66.9 64.8

64.0 63.2

60.2 55.4

50.0 43.9

38.9 33.8

29.2 24.6

17.0 11.8

8.3

2.5 1.0

0.3 0.1 0.0

53.9 55.7

57.5 59.2

60.6 61.8 62.8 63.0

62.3 60.0

57.8 54.2

47.5 38.6

28.8 19.0 18.4

11.0 5.1

1.8 0.4 0.1

0-4

10…

20…

30…

40…

50…

60…

70…

80+

85…

95…

2050 2011

61.6 59.4 58.6 57.7

55.3 51.1

46.4 40.8

36.3 31.7

27.6 23.6

17.1 12.6

9.5 6.1

4.8 3.1

1.2 0.4 0.1 0.0

49.8 51.4

53.1 54.6

55.9 57.1

58.1 58.5 58.1

56.3 54.9

52.5 47.9

41.0 32.7

23.3 25.8

14.8 7.5

2.8 0.7 0.1 Female

(millions) Male

(millions)

Increase in working population age group

Source: United Nations, Department of Economic and Social Affairs, accessed 7 June 2013 Rise in middle class and working population to fuel the growth of auto finance Source: United Nations, Department of Economic and Social Affairs, accessed 7 June 2013

65% 68%

4% 10% 1% 2%

2010 2050

0-14 15-64 65-79 80+

Source: United Nations, Department of Economic and Social Affairs

India’s favorable demographics (age groups)

Auto financing market in India – Point of view

Page 7

...and emergence of new fast growing and high OEM focus segments such as mini, compact and UV..

Auto financing market in India – Point of view

Micro, 1% Mini, 20%

Compact, 41% Super Compact, 2%

Mid Size, 7%

Executive, 1%

Premium, 0.2% Luxury, 1%

UV, 21%

Vans, 6%

FY15: PV Industry segment mix

Micro, 1% Mini, 15%

Compact, 32%

Super Compact, 4% Mid Size, 9%

Executive, 1%

Premium, 0.2%

Luxury, 2%

UV, 29%

Vans, 8%

FY20E: PV Industry segment mix

Micro Mini Compact Super Compact Mid size Executive Premium Luxury UV Van

Price Range (INR) Below 250K 250 – 450K 450 – 800K 600 – 800K 750K –

1.2Mn 1.3 –

1.85Mn 1.85 – 3Mn Above 3Mn UV 1,2,3 -600K – 1.5Mn Up to 1Mn

Body Style Hatchback Hatchback Sedan/ Estate/ Hatch/ Notchback Sedan/Estate/Hatch/Notchback

Sedan/Estate/Notch

Utility (SUV/ MPV) Box

CAGR (FY16E-FY20E) 17% 6% 7% 29% 17% 17% 49% 13.5% 19% 17%

Level of competition

UV 1,2,4 – UV3

V1 V2

Top OEMs Tata Maruti, Hyundai, Chevrolet

Maruti, Hyundai, Tata

Toyota, Maruti, Mahindra

Honda, Maruti, Hyundai

Toyota, Hyundai, Fiat

Skoda, Toyota, Hyundai

Audi, Mercedes, BMW

Mahindra, Maruti, Ford. Hyundai, VW

Maruti, Tata, Mahindra

High Moderate Low Source: SIAM,, EY Analysis Segment mix is by number of units

Page 8

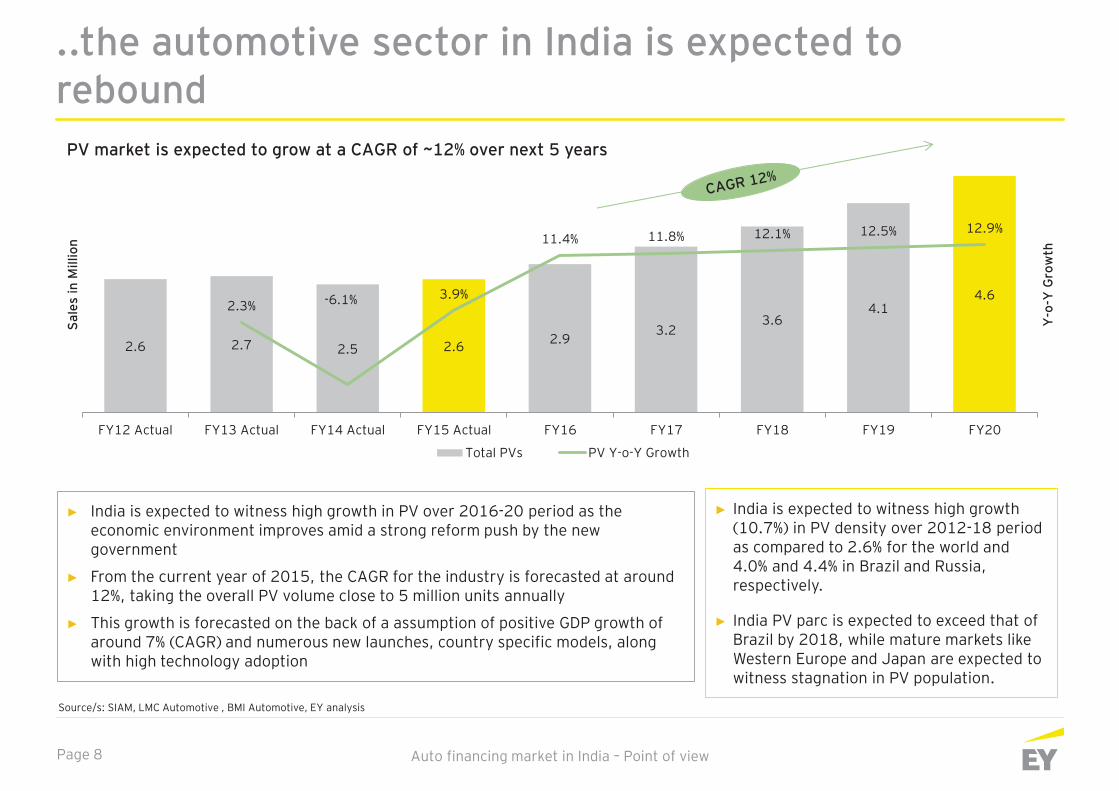

..the automotive sector in India is expected to rebound

Auto financing market in India – Point of view

2.6 2.7 2.5 2.6 2.9 3.2

3.6 4.1

4.6 2.3% -6.1% 3.9%

11.4% 11.8% 12.1% 12.5% 12.9%

FY12 Actual FY13 Actual FY14 Actual FY15 Actual FY16 FY17 FY18 FY19 FY20

Y-o

-Y G

row

th

Sale

s in

Mill

ion

Total PVs PV Y-o-Y Growth

► India is expected to witness high growth in PV over 2016-20 period as the economic environment improves amid a strong reform push by the new government

► From the current year of 2015, the CAGR for the industry is forecasted at around 12%, taking the overall PV volume close to 5 million units annually

► This growth is forecasted on the back of a assumption of positive GDP growth of around 7% (CAGR) and numerous new launches, country specific models, along with high technology adoption

PV market is expected to grow at a CAGR of ~12% over next 5 years

► India is expected to witness high growth (10.7%) in PV density over 2012-18 period as compared to 2.6% for the world and 4.0% and 4.4% in Brazil and Russia, respectively.

► India PV parc is expected to exceed that of Brazil by 2018, while mature markets like Western Europe and Japan are expected to witness stagnation in PV population.

Source/s: SIAM, LMC Automotive , BMI Automotive, EY analysis

The auto finance market

Page 10

The Indian auto financing market has gone through several peaks and troughs over the last 17 years…

Auto financing market in India – Point of view

1998 ~2006 2007~2009 2010 ~ 2015

Business circumstance

► Strong auto sales growth (~20%) and liquidity in economy attracts banks

► Liquidity crunch, rising defaults force leading financiers to exit the market

► ~75 bps increase in auto loan interest rates dampens sales growth (~9%)

► Intense competition leads to reduced interest rates, product innovation

Financier needs

► Aggressive to capture auto financing market share

► Reluctance to lend to retail segment ► Focus on building strong OEM relationships

► Focus on increasing penetration and volumes

OEM needs ► No specific financing needs ► Seek to Increase focus on semi-

urban/rural areas ► Focus on relationship with financiers

► Consolidate/strengthen market position ► Improve dealer control and profitability

OEM

Fin

anci

ng s

trat

egie

s

Financier tie-ups All OEMs

All OEMs; some OEMs tie up with local market NBFCs to increase rural focus. (For

example, Maruti ties up with MMFSL) Maruti, Hyundai, Honda, GM, Fiat

White-label finance

Maruti tied up with Citicorp Financial to form Citicorp Maruti Finance Ltd. (CMFL) No white label financiers in market after CMFL experiment failed

Indian captives Mahindra & Mahindra and Tata Motors Mahindra & Mahindra and Tata Motors Mahindra & Mahindra and Tata Motors

Foreign captives

Limited presence; GMAC, Ford’s JV with Kotak Existing players exit; no new entrants VW (VW, Audi, Skoda, Porsche), BMW

Daimler, Toyota, Renault-Nissan, Ford

Source: EY analysis, market insights

Page 11

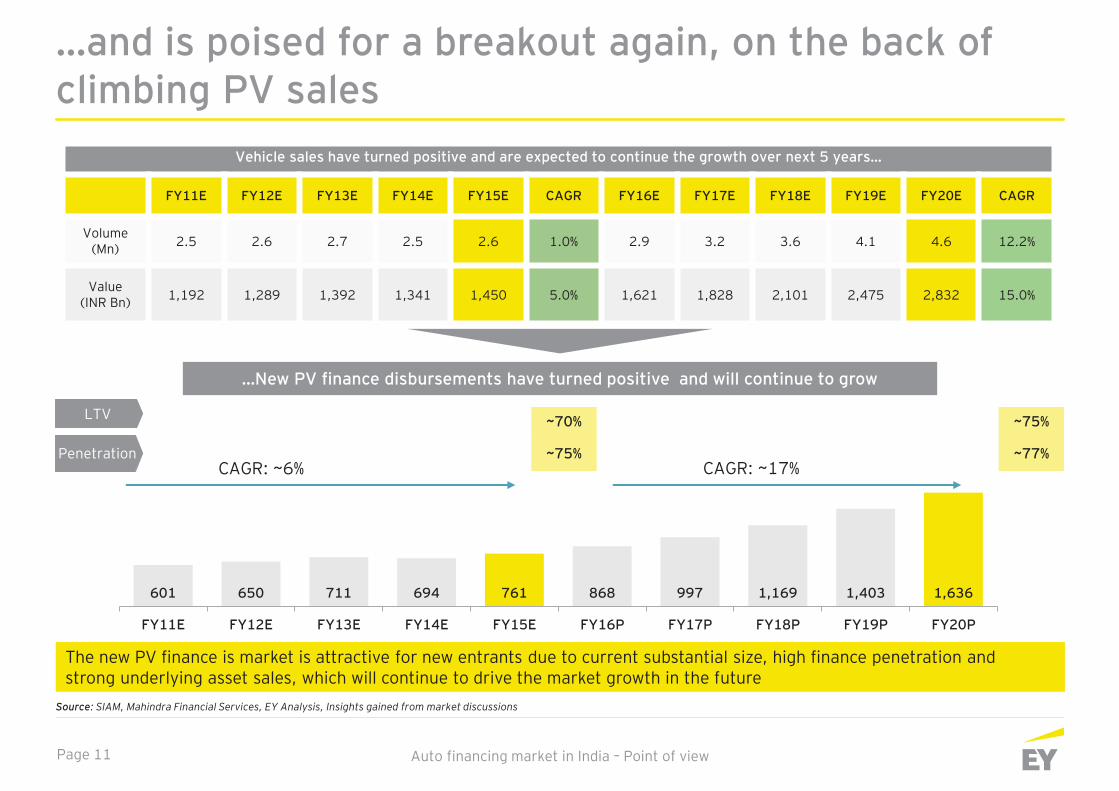

…and is poised for a breakout again, on the back of climbing PV sales

Auto financing market in India – Point of view

Source: SIAM, Mahindra Financial Services, EY Analysis, Insights gained from market discussions

The new PV finance is market is attractive for new entrants due to current substantial size, high finance penetration and strong underlying asset sales, which will continue to drive the market growth in the future

601 650 711 694 761 868 997 1,169 1,403 1,636

FY11E FY12E FY13E FY14E FY15E FY16P FY17P FY18P FY19P FY20P

CAGR: ~6% CAGR: ~17%

Vehicle sales have turned positive and are expected to continue the growth over next 5 years…

FY11E FY12E FY13E FY14E FY15E CAGR FY16E FY17E FY18E FY19E FY20E CAGR

Volume (Mn) 2.5 2.6 2.7 2.5 2.6 1.0% 2.9 3.2 3.6 4.1 4.6 12.2%

Value (INR Bn) 1,192 1,289 1,392 1,341 1,450 5.0% 1,621 1,828 2,101 2,475 2,832 15.0%

…New PV finance disbursements have turned positive and will continue to grow

~77% ~75% Penetration

~75% ~70% LTV

Page 12 Auto financing market in India – Point of view

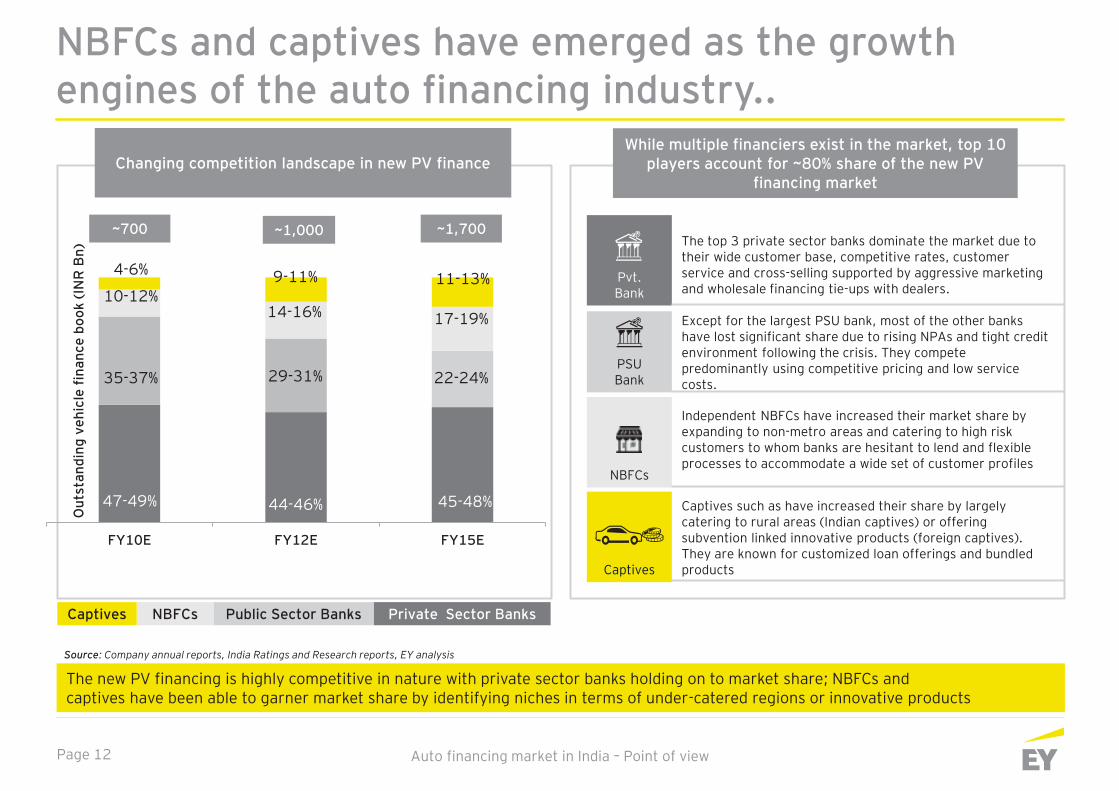

NBFCs and captives have emerged as the growth engines of the auto financing industry..

Out

stan

ding

veh

icle

fina

nce

book

(IN

R B

n) The top 3 private sector banks dominate the market due to

their wide customer base, competitive rates, customer service and cross-selling supported by aggressive marketing and wholesale financing tie-ups with dealers.

Pvt. Bank

Independent NBFCs have increased their market share by expanding to non-metro areas and catering to high risk customers to whom banks are hesitant to lend and flexible processes to accommodate a wide set of customer profiles

NBFCs

Captives such as have increased their share by largely catering to rural areas (Indian captives) or offering subvention linked innovative products (foreign captives). They are known for customized loan offerings and bundled products Captives

Source: Company annual reports, India Ratings and Research reports, EY analysis

The new PV financing is highly competitive in nature with private sector banks holding on to market share; NBFCs and captives have been able to garner market share by identifying niches in terms of under-catered regions or innovative products

Except for the largest PSU bank, most of the other banks have lost significant share due to rising NPAs and tight credit environment following the crisis. They compete predominantly using competitive pricing and low service costs.

PSU Bank

Changing competition landscape in new PV financeWhile multiple financiers exist in the market, top 10

players account for ~80% share of the new PV financing market

FY10E FY12E FY15E

NBFCs Captives

47-49% 44-46% 45-48%

35-37% 29-31% 22-24%

10-12% 14-16% 17-19%

11-13% 9-11% 4-6%

~700 ~1,000 ~1,700

Public Sector Banks Private Sector Banks

Page 13 Auto financing market in India – Point of view

..and have been particularly successful in “bank ignored” niche segments such as premium and low income…

► Private and PSU banks ► Low risk: low yield ► Dealer and direct channels

important

1 ► NBFCs and Indian captives ► High risk: high yield model ► DSA and dealer important

2

► Foreign captives ► High-end customer segment ► Dealer is most important

3

Ris

k

Yiel

d

Low Income High Income

Self employed: without income proof

SB

Self employed: with income proof

Salaried: private and government

S: Large South Indian NBFC M: Large rural/semi-urban NBFC C: Large diversified NBFC MM: Rural focused auto finance

TM: Large Indian captive V: European captive finance company D: Luxury car finance company B: Luxury car finance company

HB

IB

1

3

V D

B

Middle income

2

Segment Profile

C S

M

TM

M2 KP

Banks NBFCs Captives

SB: Large public sector bank IB&HB: Large private sector banks

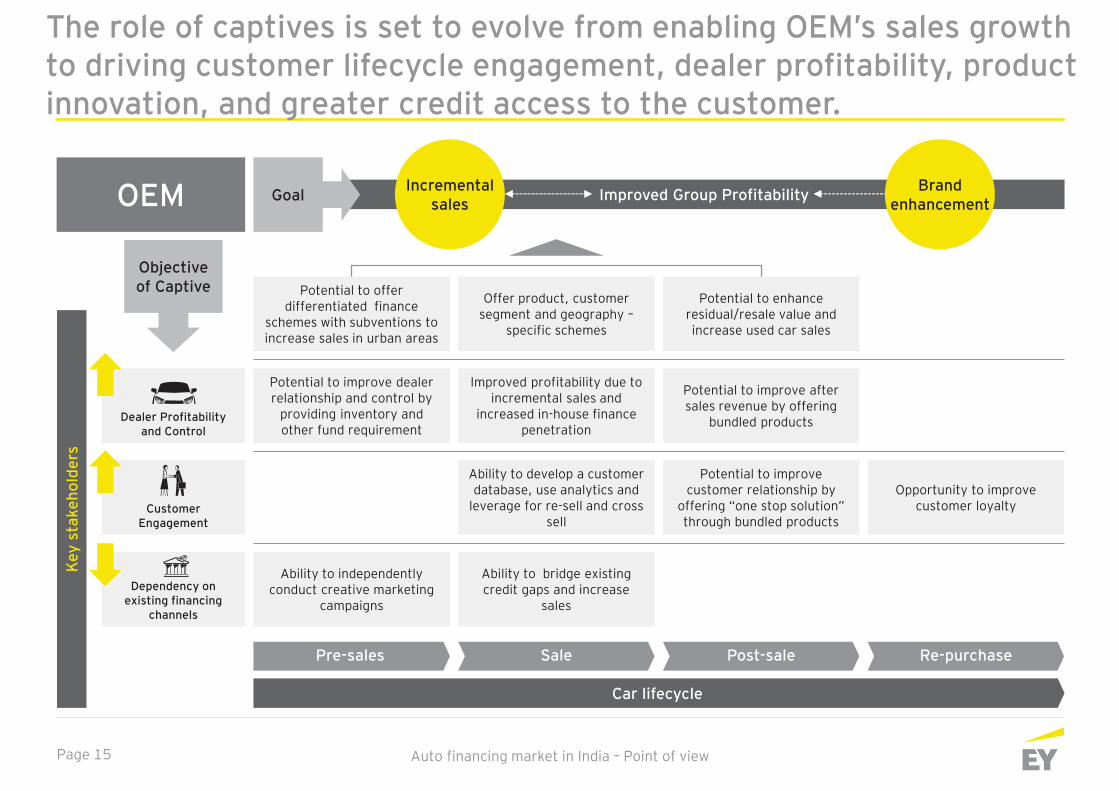

Emergence of captives

Page 15

Key

stak

ehol

ders

Auto financing market in India – Point of view

The role of captives is set to evolve from enabling OEM’s sales growth to driving customer lifecycle engagement, dealer profitability, product innovation, and greater credit access to the customer.

Potential to offer differentiated finance

schemes with subventions to increase sales in urban areas

Potential to improve dealer relationship and control by

providing inventory and other fund requirement

Ability to bridge existing credit gaps and increase

sales

Offer product, customer segment and geography –

specific schemes

Improved profitability due to incremental sales and

increased in-house finance penetration

Ability to develop a customer database, use analytics and

leverage for re-sell and cross sell

Ability to independently conduct creative marketing

campaigns

Potential to enhance residual/resale value and increase used car sales

Potential to improve after sales revenue by offering

bundled products

Potential to improve customer relationship by

offering “one stop solution” through bundled products

Opportunity to improve customer loyalty

Pre-sales Sale Post-sale Re-purchase

Improved Group Profitability

Car lifecycle

Goal Incremental sales

Brand enhancement

Objective of Captive

OEM

Dealer Profitability and Control

Customer Engagement

Dependency on existing financing

channels

Page 16

Foreign OEMs with captive financing set ups

Auto financing market in India – Point of view

...hence, most foreign OEMs have adopted the captive route to improve finance penetration

Hig

h M

ediu

m

Fina

ncin

g pr

oduc

t di

ffer

enti

atio

n

50% 100% Finance penetration

6%

9% Indian OEM

2

Low

Japanese OEM

3%

American OEM

45% Indian OEM

16%

Korean OEM

1.8%

American OEM

3

7%

Size of bubble represents market share (FY’15) Source: Company annual reports, India Ratings and Research reports, EY analysis

OEM categorization

1

Indian OEMs with captive financing set ups 2

Financing through tie-ups: Banks and NBFCs 3

► Increased usage of differentiated products

► Enhanced dealer relationship management

► Reduced finance penetration due to focus on rural segments

► Offer a combination of standardized and customized products

► Standardized finance product offerings and cash discounts

► Very high penetration by market leader

5%

Japanese OEMs

1.7%

0.6%

0.3%

0.4%

European 0.4%

European OEMs

European 1.8%

1

1.8%

Indian OEM

Page 17 Auto financing market in India – Point of view

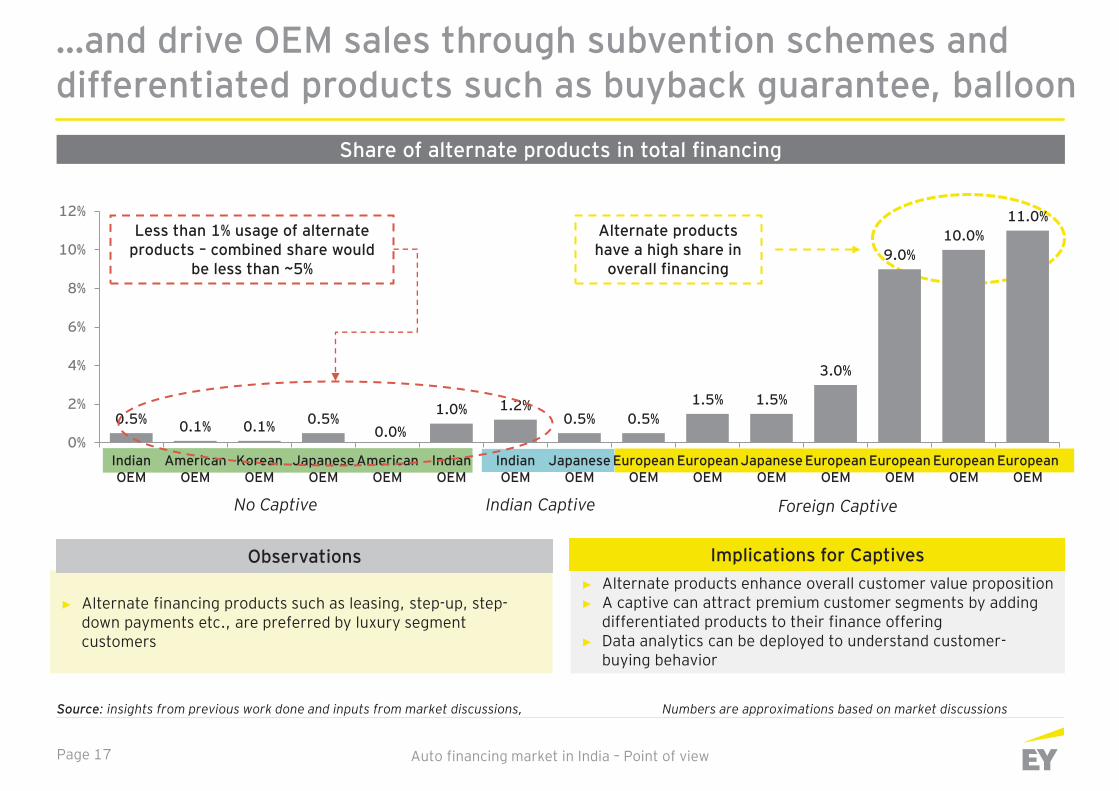

…and drive OEM sales through subvention schemes and differentiated products such as buyback guarantee, balloon

0.5% 0.1% 0.1% 0.5% 0.0%

1.0% 1.2% 0.5% 0.5%

1.5% 1.5%

3.0%

9.0% 10.0%

11.0%

0%

2%

4%

6%

8%

10%

12%

IndianOEM

AmericanOEM

KoreanOEM

JapaneseOEM

AmericanOEM

IndianOEM

IndianOEM

JapaneseOEM

EuropeanOEM

EuropeanOEM

JapaneseOEM

EuropeanOEM

EuropeanOEM

EuropeanOEM

EuropeanOEM

Auto sales and finance growth

Share of alternate products in total financing

Less than 1% usage of alternate products – combined share would

be less than ~5%

Alternate products have a high share in

overall financing

► Alternate products enhance overall customer value proposition ► A captive can attract premium customer segments by adding

differentiated products to their finance offering ► Data analytics can be deployed to understand customer-

buying behavior

Implications for Captives

► Alternate financing products such as leasing, step-up, step-down payments etc., are preferred by luxury segment customers

Observations

No Captive Indian Captive Foreign Captive

Source: insights from previous work done and inputs from market discussions, Numbers are approximations based on market discussions

Page 18 Auto financing market in India – Point of view

Dealer financing, besides addressing the financial needs of the dealer, leverages the wholesale-retail linkage to drive retail penetration..

Sustain business Working capital

Grow existing business Inventory funding

Expand (additional showrooms)

Term Loans

Retail sales with Wholesale-Retail Linkage

Inventory funding rate

Retail target achievement

Captive + OEM

Dealer

Retail rebate

Captive support Dealer requirement

3

Address all financial needs of dealers Flexible Inventory Funding Terms

Credit free periods

► Offer 30-day, credit-free period for inventory funding for select dealers

Relaxed payment scheme

► Flexibility and relaxed norms for re-payment such as staggered payments

► Relaxation of penal interest charges on a case-to-case basis

Support in difficult times

► Support the dealers in downturns to help develop a robust relationship

2 1

Page 19

Contact center connects with the customer

for collections.

Contact center notifies the customer on payment due/

updates address and contact details

Cross-sell re-finance/top-up/ to select customers

Auto financing market in India – Point of view

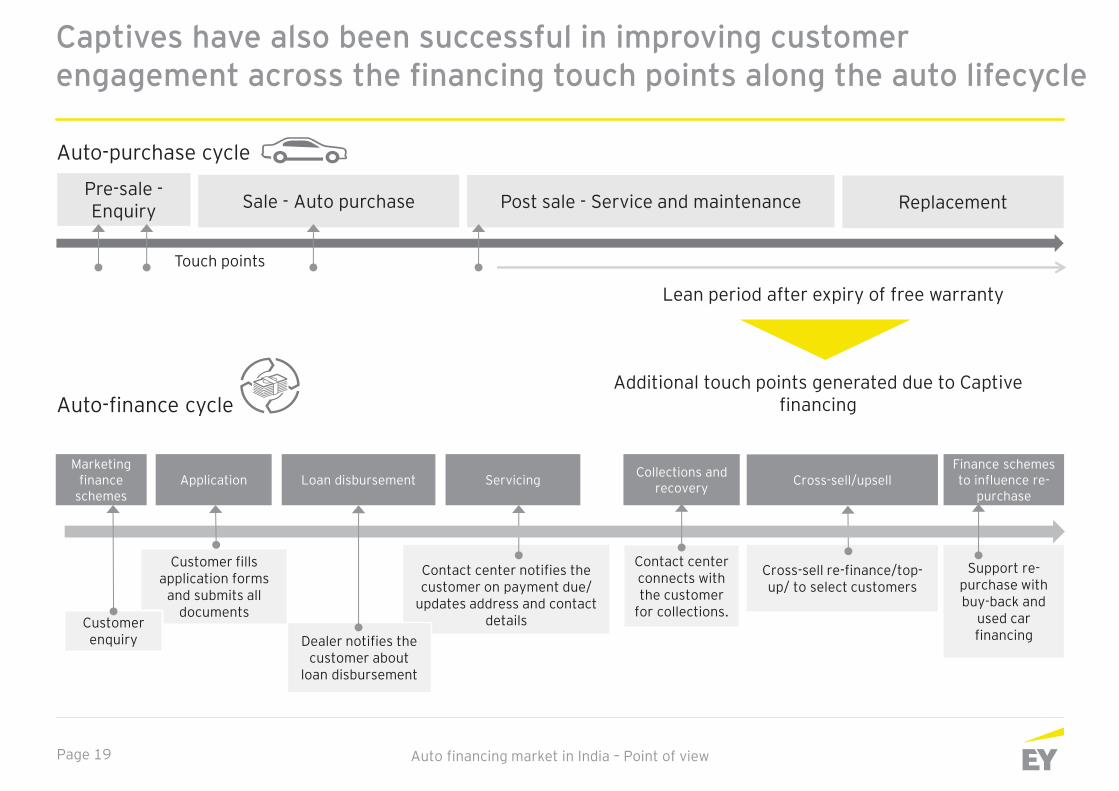

Captives have also been successful in improving customer engagement across the financing touch points along the auto lifecycle

Customer fills application forms

and submits all documents

Customer enquiry

Marketing finance

schemes Loan disbursement Application Collections and

recovery

Finance schemes to influence re-

purchase Cross-sell/upsell

Support re- purchase with buy-back and

used car financing

Auto-purchase cycle

Sale - Auto purchase Replacement Post sale - Service and maintenance Pre-sale - Enquiry

Auto-finance cycle

Servicing

Touch points

Lean period after expiry of free warranty

Additional touch points generated due to Captive financing

Dealer notifies the customer about

loan disbursement

The 10 commandments

Page 21 Auto financing market in India – Point of view

1. Move away from generic products to targetted “Customer value propositions”

Compact

Mid and Compact,

SUV

Premium,

SUV

Car segments Key customer segments A captive’s value proposition

First time buyers

Fleet Taxi segment (Drivers)

Rural segment

• Flexible and affordable finance schemes • Subventions and High LTV schemes

• Re-payment flexibility • High LTVs and longer tenure schemes backed by

risk-based pricing

• Subventions and products such as bundling and EMI structuring

• Ease of loan documentation

• High LTVs and longer tenure schemes backed by risk-based pricing

• Schemes designed according to income pattern

Mass urban

• Subvention and bundled products; buy back guarantee

• Ease and reduced TAT of loan documentation High income group

1

2

3

4

5

Page 22 Auto financing market in India – Point of view

2. Be nimble, target the rapidly emerging customer segments

Customer segments Segment characteristics Captive’s segment strategy Captive value proposition

Fleet/taxi

Low/middle income; difficult to get bank credit

Providing affordable finance

Re-payment flexibility and bundled maintenance contracts

Fleet Taxi segment (Drivers)

Avg. share of PV sales

is ~10%

► Low/middle income, prefer low immediate cash outflow

► Usually do not qualify for loans from private banks

► Target customers for local NBFCs with high interest rates

► Focus on providing affordable finance

► Tie ups with big fleet/ taxi players, for background checks and risk mitigation

► High LTVs and longer tenure schemes with risk-based pricing

► Schemes designed according to income pattern, such as daily repayment mechanism

► Bundled discount on extended warranty and annual maintenance

Rural

Low irregular/seasonal income; difficult to get bank credit

Making finance available

High LTVs and long tenure credit schemes with high interest rates

Rural segment

Avg. share of PV sales is ~20%

► Low income ► Irregular/seasonal income ► Limited reach of banks/usually

do not qualify for loans from private banks

► Target customers for NBFCs with high interest rates

► Focus on availability of finance

► High risk: high reward model ► Schemes designed according to the

income pattern for rural customers, with flexibilities on re-payment

Page 23 Auto financing market in India – Point of view

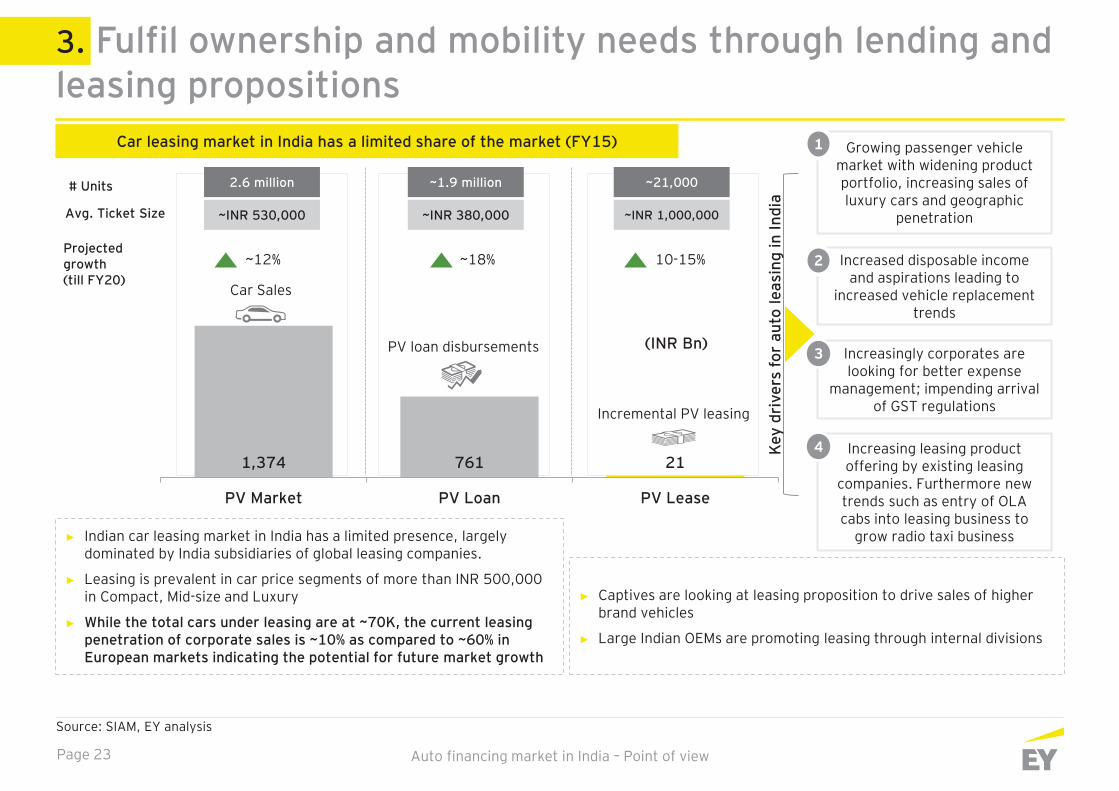

3. Fulfil ownership and mobility needs through lending and leasing propositions

1,374 761 21

PV Market PV Loan PV Lease

Car leasing market in India has a limited share of the market (FY15)

Car Sales

PV loan disbursements

Incremental PV leasing

(INR Bn)

# Units 2.6 million ~1.9 million ~21,000

Avg. Ticket Size ~INR 530,000 ~INR 380,000 ~INR 1,000,000

10-15% ~18% ~12% Projected growth (till FY20)

Growing passenger vehicle market with widening product portfolio, increasing sales of luxury cars and geographic

penetration

Increased disposable income and aspirations leading to

increased vehicle replacement trends

Increasingly corporates are looking for better expense

management; impending arrival of GST regulations

Increasing leasing product offering by existing leasing

companies. Furthermore new trends such as entry of OLA cabs into leasing business to

grow radio taxi business

2

► Indian car leasing market in India has a limited presence, largely dominated by India subsidiaries of global leasing companies.

► Leasing is prevalent in car price segments of more than INR 500,000 in Compact, Mid-size and Luxury

► While the total cars under leasing are at ~70K, the current leasing penetration of corporate sales is ~10% as compared to ~60% in European markets indicating the potential for future market growth

► Captives are looking at leasing proposition to drive sales of higher brand vehicles

► Large Indian OEMs are promoting leasing through internal divisions

Source: SIAM, EY analysis

1

3

4 Key

driv

ers

for

auto

leas

ing

in In

dia

Page 24 Auto financing market in India – Point of view

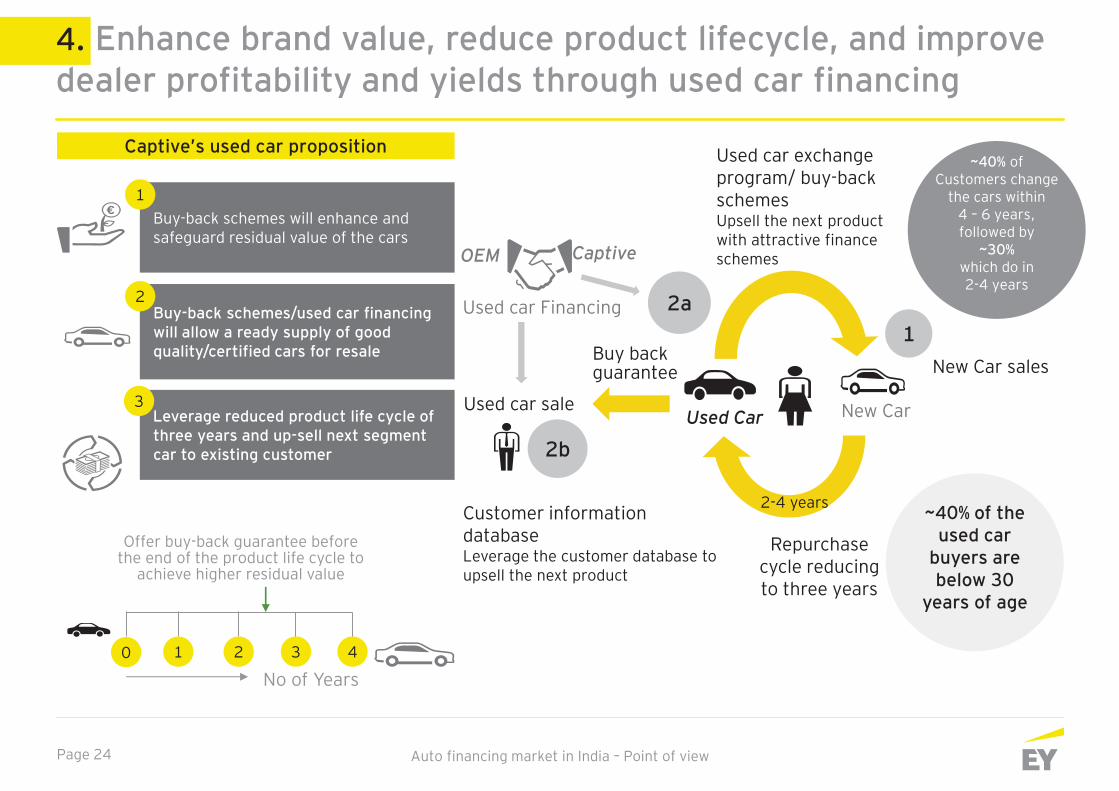

4. Enhance brand value, reduce product lifecycle, and improve dealer profitability and yields through used car financing

Buy-back schemes will enhance and safeguard residual value of the cars

1

Buy-back schemes/used car financing will allow a ready supply of good quality/certified cars for resale

2

Leverage reduced product life cycle of three years and up-sell next segment car to existing customer

3

Offer buy-back guarantee before the end of the product life cycle to

achieve higher residual value

No of Years 0 1 2 3 4

New Car sales

New Car Used Car Used car sale

OEM Captive

Buy back guarantee

1 2a

2b

Used car exchange program/ buy-back schemes Upsell the next product with attractive finance schemes

Repurchase cycle reducing to three years

Customer information database Leverage the customer database to upsell the next product

2-4 years ~40% of the used car

buyers are below 30

years of age

~40% of Customers change

the cars within 4 – 6 years, followed by

~30% which do in 2-4 years

Captive’s used car proposition

Used car Financing

Page 25 Auto financing market in India – Point of view

5. Leverage asset tested customer base to grow beyond single product exposure

Yield/risk

Strategic segments

Volume segments

Captives can improve yields by offering product variants such as used car, high tenor, high LTV, balloon etc products. Once stable, they can even leverage asset tested customer base to offer semi-unsecured and unsecured products based upon repayment track, at higher yields.

Phased approach of retail products

New vanilla car financing/ subventions

Car Leasing

Extended top-up/ refinance

Bundled products

Exchange/ buyback

Bullet/ balloon/ step up

High Tenor High LTV

Flexible EMI/ step up

Used car financing

Setup phase

Expansion phase

Breakout phase

Page 26

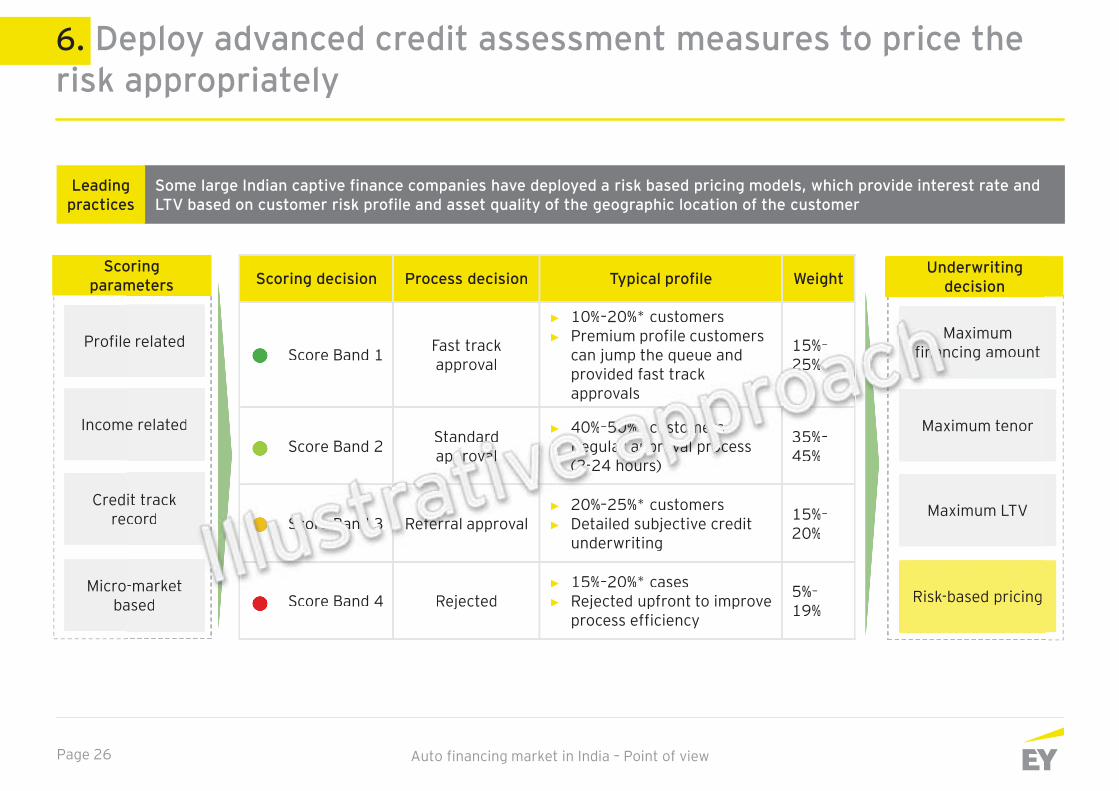

6. Deploy advanced credit assessment measures to price the risk appropriately

Scoring decision Process decision Typical profile Weight

Score Band 1 Fast track approval

► 10%–20%* customers ► Premium profile customers

can jump the queue and provided fast track approvals

15%–25%

Score Band 2 Standard approval

► 40%–50%* customers ► Regular approval process

(2-24 hours)

35%–45%

Score Band 3 Referral approval ► 20%–25%* customers ► Detailed subjective credit

underwriting

15%–20%

Score Band 4 Rejected ► 15%–20%* cases ► Rejected upfront to improve

process efficiency

5%–19%

Maximum financing amount

Maximum LTV

Maximum tenor

Risk-based pricing

Underwriting decision

Some large Indian captive finance companies have deployed a risk based pricing models, which provide interest rate and LTV based on customer risk profile and asset quality of the geographic location of the customer

Leading practices

Auto financing market in India – Point of view

Profile related

Credit track record

Income related

Micro-market based

Scoring parameters Scoring decision Process decision Typical profile Weight

Score Band 1 Fast track approval

► 10%–20%* customers► Premium profile customers

can jump the queue and provided fast trackapprovals

15%–25222225222222222222 %%%%%%%%%%%%%%%%%%%

Score Band 2 Standaaardrrrrrrrrrrrr apppppppprpprprprprprprprprprprprprprprprprrp ovovovovovovovovovovovvovovovaaalalalaaaaaaaalaalalalaaa

► 40%–5050505050505050505055505050505050505050%*%*%*%*%*%*%%%%%%*%%%%%%%%% cccusussusususuususussussusssuustoooooooooooooooomemmemememememememememememememmmeeersrrsrsrsrsrsrsrsrsrrrssrssssrs►►►►►►►►►►►►►►►►►►►►►►►►► ReReReReReReRReReReReeeeReReReReRReR gulaaaaaaaaaaaaaaaaarrrrrrrrrrrrrrrrrr apapappapappapapapapapapapapapaapapapprprprprprprpppprprprprprpprprpp ovovovovovovovovovovvvvovvvvvo alalalalalallalalalalalaaaaa prorororororororoooroooroororror cess

(2(2(2(2(2(2(22(2(2(2(2(2(2(22(2(2(2(2(2-24 hhhhhhhhours)

35%–45%

ScScScScScScScScSccScScScScSSScScScororrrrorrororrrorrorororeeeeeeeeeeeeeeeeeee BaBaBaBaBaBaBaBaBaBaBaBaBaBaBaBaBaaandndndndndndndnddndndndndndndnnnd 33333333333333333333 Reffffffffeffffffff rral approval► 20%–25%* customers► Detailed subjective credit

underwriting

15%–20%

Score Band 4 Rejected► 15%–20%* cases► Rejected upfront to improve

process efficiency

5%–19%

Maximumfinanananananananannaanananaaann ncing amount

Maximum LTV

Maximum tenor

Risk-based pricing

Underwriting decision

e related

it track cord

e related

-market ased

oringmeters

Page 27 Auto financing market in India – Point of view

7. Limit credit losses through a robust collections framework

Objective Prevent delinquencies Collect better to minimize flow Recover as much as possible

Ownership In-house + Outsourced In-house + Outsourced Largely outsourced

Collaboration Sales involvement for non-starter, early defaulters Legal involvement Extensive use of legal

Activity Tele-calling and SMS/IVR reminders Field collections Restructuring Repossessions and recovery

Analytics Decision trees Collections score-cards Repossession agencies

IT tools • Centralized Collections IT system to track bucket wise case movement • Exhaustive MIS (Bucket/Asset/Collector wise flow and normalization performance) and Analytics • Hand-held devices for field collectors with receipt generation capability

Leading practices

A rural finance company requires Sales Executive to handle early bucket collections to encourage right sourcing and manage customer relationships

Leading private sector banks monitor pre-NPA accounts stringently and use legal effectively

NBFCs dealing in cash collections utilize mobile apps for tracking of collections force; online sale of repossessed vehicles for faster disposal

Current Due Bucket 1 (DPD 0-30)

Bucket 2 (DPD 31-60)

Bucket 4 (DPD 91-

120)

Bucket 5 onwards (DPD 120+)

Early buckets Mid buckets Hard buckets

Bucket 3 (DPD 61-90)

Page 28

Bank-led

Auto financing market in India – Point of view

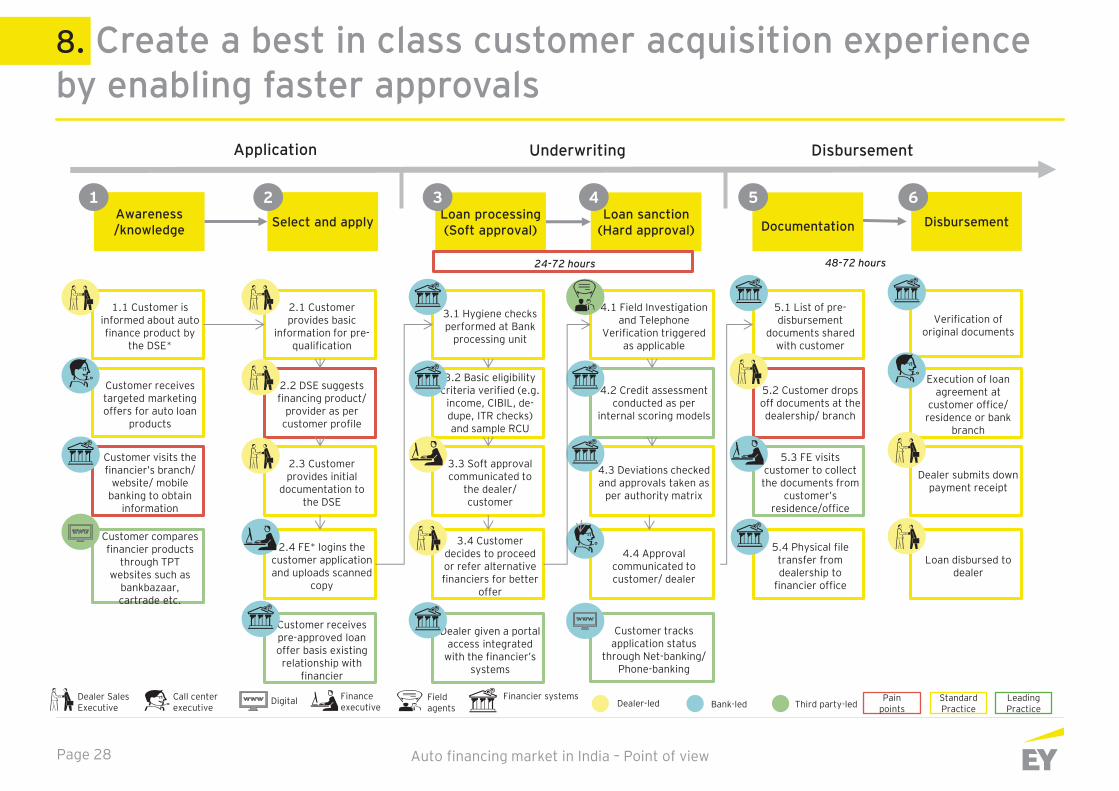

8. Create a best in class customer acquisition experience by enabling faster approvals

1.1 Customer is informed about auto finance product by

the DSE*

3.2 Basic eligibility criteria verified (e.g.

income, CIBIL, de-dupe, ITR checks) and sample RCU

Application Underwriting

Awareness /knowledge

Loan sanction (Hard approval)

Loan processing (Soft approval)

Documentation Disbursement Select and apply

Customer receives targeted marketing offers for auto loan

products

Customer visits the financier’s branch/

website/ mobile banking to obtain

information

Customer compares financier products

through TPT websites such as

bankbazaar, cartrade etc.

2.1 Customer provides basic

information for pre-qualification

2.2 DSE suggests financing product/

provider as per customer profile

Customer receives pre-approved loan offer basis existing

relationship with financier

3.1 Hygiene checks performed at Bank

processing unit

3.3 Soft approval communicated to

the dealer/ customer

2.3 Customer provides initial

documentation to the DSE

2.4 FE* logins the customer application and uploads scanned

copy

3.4 Customer decides to proceed or refer alternative financiers for better

offer

4.2 Credit assessment conducted as per

internal scoring models

4.1 Field Investigation and Telephone

Verification triggered as applicable

4.3 Deviations checked and approvals taken as

per authority matrix

4.4 Approval communicated to customer/ dealer

Customer tracks application status

through Net-banking/ Phone-banking

Disbursement

5.2 Customer drops off documents at the dealership/ branch

5.1 List of pre-disbursement

documents shared with customer

5.3 FE visits customer to collect the documents from

customer’s residence/office

5.4 Physical file transfer from dealership to

financier office

Verification of original documents

1 2 3 4 5 6

Dealer submits down payment receipt

Execution of loan agreement at

customer office/ residence or bank

branch

Loan disbursed to dealer

Dealer given a portal access integrated

with the financier’s systems

24-72 hours 48-72 hours

Pain points

Standard Practice

Leading Practice

Dealer Sales Executive

Call center executive

Digital Finance executive

Financier systems Dealer-led Third party-led

Field agents

Page 29 Auto financing market in India – Point of view

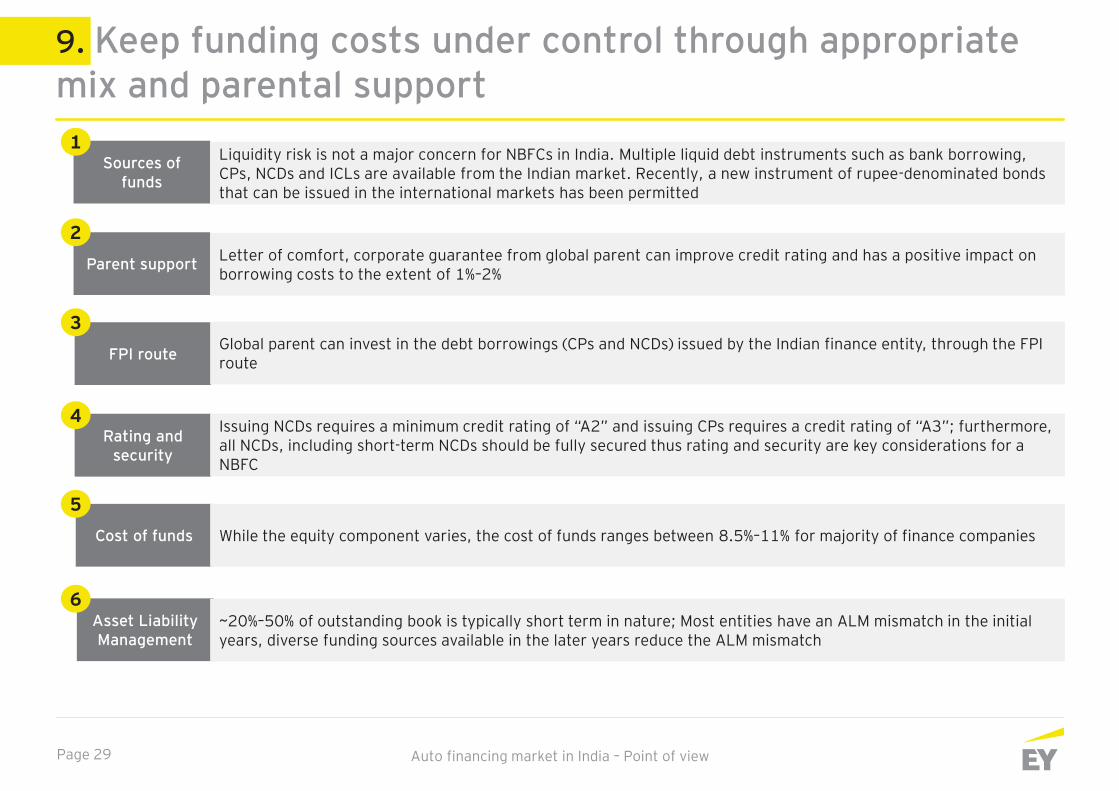

9. Keep funding costs under control through appropriate mix and parental support

Asset Liability Management

Cost of funds

Rating and security

FPI route

Parent support

Sources of funds

Liquidity risk is not a major concern for NBFCs in India. Multiple liquid debt instruments such as bank borrowing, CPs, NCDs and ICLs are available from the Indian market. Recently, a new instrument of rupee-denominated bonds that can be issued in the international markets has been permitted

Letter of comfort, corporate guarantee from global parent can improve credit rating and has a positive impact on borrowing costs to the extent of 1%–2%

Issuing NCDs requires a minimum credit rating of “A2” and issuing CPs requires a credit rating of “A3”; furthermore, all NCDs, including short-term NCDs should be fully secured thus rating and security are key considerations for a NBFC

Global parent can invest in the debt borrowings (CPs and NCDs) issued by the Indian finance entity, through the FPI route

While the equity component varies, the cost of funds ranges between 8.5%–11% for majority of finance companies

~20%–50% of outstanding book is typically short term in nature; Most entities have an ALM mismatch in the initial years, diverse funding sources available in the later years reduce the ALM mismatch

1

2

3

4

5

6

Page 30 Auto financing market in India – Point of view

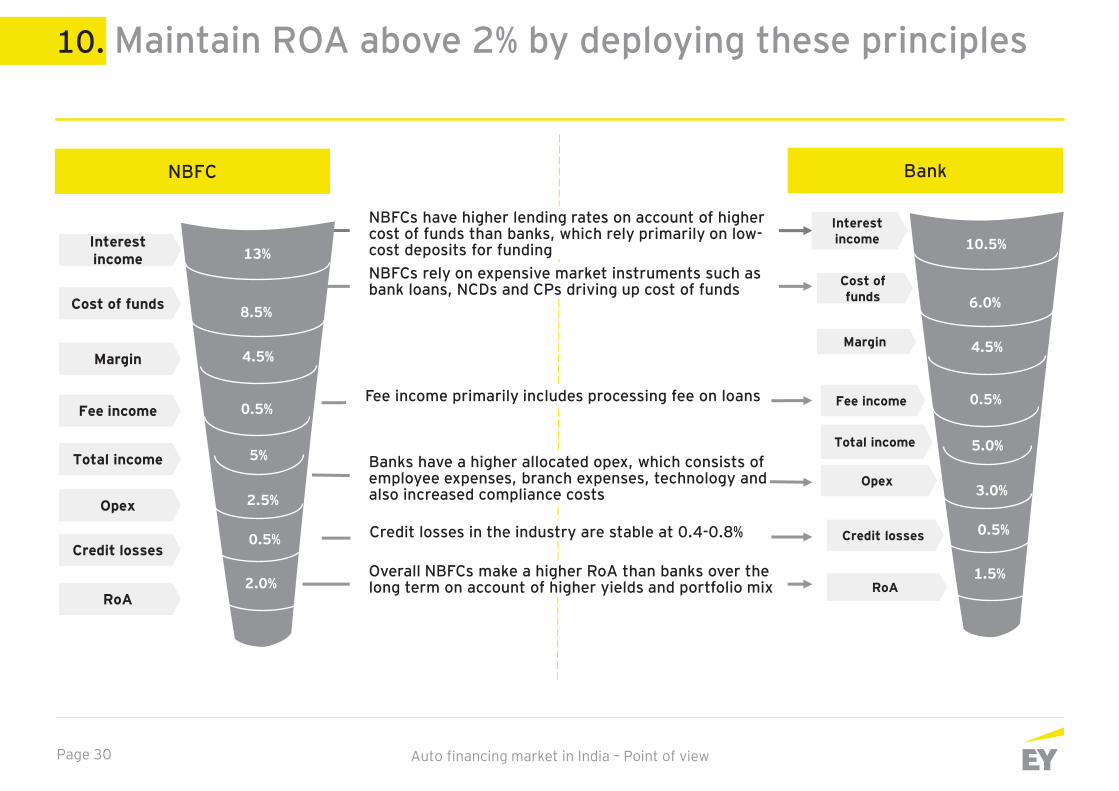

10. Maintain ROA above 2% by deploying these principles

NBFC Bank

NBFCs have higher lending rates on account of higher cost of funds than banks, which rely primarily on low-cost deposits for funding NBFCs rely on expensive market instruments such as bank loans, NCDs and CPs driving up cost of funds

Fee income primarily includes processing fee on loans

Banks have a higher allocated opex, which consists of employee expenses, branch expenses, technology and also increased compliance costs

Credit losses in the industry are stable at 0.4-0.8%

Overall NBFCs make a higher RoA than banks over the long term on account of higher yields and portfolio mix

Interest income

Fee income

Opex

Credit losses

RoA

13%

4.5%

2.5%

0.5%

2.0%

8.5% Cost of funds

Margin

0.5%

Total income 5%

Interest income

Fee income

Opex

Credit losses

RoA

10.5%

4.5%

3.0%

0.5%

1.5%

6.0% Cost of funds

Margin

0.5%

Total income 5.0%

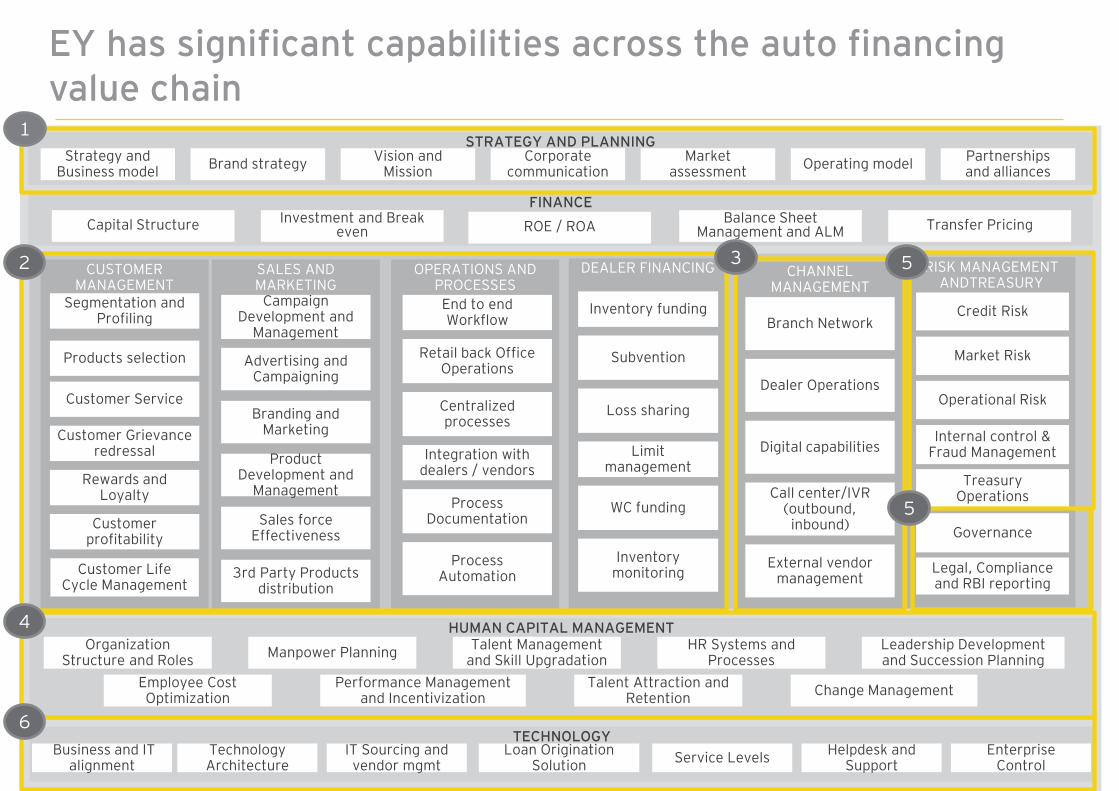

About EY

Page 32 NBL assistance

FINANCE

STRATEGY AND PLANNING

Balance Sheet Management and ALM Transfer Pricing Capital Structure Investment and Break

even

Operating model Brand strategy Corporate communication

Vision and Mission

Market assessment

Partnerships and alliances

Strategy and Business model

CHANNEL MANAGEMENT

Dealer Operations

Call center/IVR (outbound, inbound)

External vendor management

Branch Network

Digital capabilities

SALES AND MARKETING

Product Development and

Management

Campaign Development and

Management

3rd Party Products distribution

Advertising and Campaigning

Sales force Effectiveness

Branding and Marketing

OPERATIONS AND PROCESSES End to end Workflow

Retail back Office Operations

Centralized processes

Integration with dealers / vendors

Process Documentation

Process Automation

RISK MANAGEMENT ANDTREASURY

Operational Risk

Internal control & Fraud Management

Legal, Compliance and RBI reporting

Credit Risk

Treasury Operations

Governance

Market Risk

CUSTOMER MANAGEMENT

Customer Life Cycle Management

Segmentation and Profiling

Rewards and Loyalty

Customer Grievance redressal

Products selection

Customer Service

Customer profitability

DEALER FINANCING

Inventory funding

Subvention

Loss sharing

Limit management

WC funding

Inventory monitoring

TECHNOLOGY Business and IT

alignment Technology Architecture

IT Sourcing and vendor mgmt Service Levels Helpdesk and

Support Enterprise

Control Loan Origination

Solution

HUMAN CAPITAL MANAGEMENT Organization

Structure and Roles Manpower Planning Talent Management and Skill Upgradation

HR Systems and Processes

Leadership Development and Succession Planning

Employee Cost Optimization

Performance Management and Incentivization

Talent Attraction and Retention Change Management

1

2

4

6

5

5

3

ROE / ROA

EY has significant capabilities across the auto financing value chain

Page 33

EY Global Automotive Practitioner Network

U.S. 1556

Mexico 333

Brazil 290

UK 180

Germany 827

France 178

Italy 161

India 648

China 873 Korea

117

Indonesia 91

Philippines 76

Thailand 159

Japan 444

EY’s Automotive team comprises of ~7300 practitioners across the world

EMEIA 2840

AsiaPac 1550

Japan 444

Americas 2497

Auto financing market in India – Point of view

Page 34 Auto financing market in India – Point of view

..and a ‘industry’ experienced local auto finance execution team

India Financial Services Advisory leader

Rohan Sachdev Partner ► Leader, Financial Services – Performance

Improvement practice in India ► 15 years of experience in assisting large

international and domestic BFSI entities in strategic and operational transformation

Global Automotive Finance Leader

Jens Diehlmann Partner ► 18 years of automotive finance experience ► Co-author of the Book “Automotive

Management” which comprises the full automotive value-chain under the focus of financial aspects

Partner – financial services and auto finance expert

Fali Hodiwalla Partner ► 15 years of experience with advising

banking and financial services clients ► Extensive leadership experience in defining

entry strategy and setting up captive auto finance entities in India

India Leader – Automotive Sector

Rakesh Batra Partner ► Account partner for large auto OEMs

globally and in India ► Leadership experience in assisting large

automotive and eco-system players in strategic and operational improvement

NBFC leader and auto finance expert

Himanshu Bansal Director ► Over 14 years of Banking & Consulting

experience in Strategy, customer solutions and retail lending

► Extensive leadership experience consulting auto finance companies and captives in market entry

Auto Finance Team

Bhavin Sejpal Manager ► BFSI experience of over 5 years with focus

on retail and wholesale finance segment ► Recently assisted a large OEM in feasibility

study for a captive finance company set-up

Auto Finance Team

Trupti Bagwe Manager ► BFSI experience of over 5 years with focus

on non-banking finance space ► Extensive experience in auto finance

market entry, strategy and operational improvements

Auto Finance Team

Vivek Sapre Manager ► BFSI experience of over 5 years with

industry experience in auto finance ► Assisted large vehicle finance companies in

operational transformation and new company set-up

Page 35 Auto financing market in India – Point of view

EY Offices

Ahmedabad 2nd floor, Shivalik Ishaan Near. C.N Vidhyalaya, Ambawadi, Ahmedabad - 380 015 Tel: + 91 79 6608 3800 Fax: + 91 79 6608 3900 Bengaluru 12th & 13th floor , “U B City” Canberra Block, No.24, Vittal Mallya Road Bengaluru - 560 001 Tel: + 91 80 4027 5000 + 91 80 6727 5000 Fax: + 91 80 2210 6000 + 91 80 2224 0695 Prestige Emerald, No. 4, 1st Floor, Madras Bank Road, Lavelle Road Junction, Bangalore - 560001 Chandigarh 1st Floor, SCO: 166-167 Sector 9-C, Madhya Marg Chandigarh - 160 009 Tel: + 91 172 671 7800 Fax: + 91 172 671 7888

Chennai Tidel Park, 6th & 7th Floor A Block (Module 601,701-702) No.4, Rajiv Gandhi Salai, Taramani Chennai - 600 113 Tel: + 91 44 6654 8100 Fax: + 91 44 2254 0120 Hyderabad Oval Office 18, iLabs Centre, Hitech City, Madhapur, Hyderabad - 500 081 Tel: + 91 40 6736 2000 Fax: + 91 40 6736 2200 Kochi 9th Floor “ABAD Nucleus” NH-49, Maradu PO, Kochi – 682 304 Tel: + 91 484 304 4000 Fax: + 91 484 270 5393 Kolkata 22, Camac Street 3rd Floor, Block C” Kolkata – 700 016 Tel: + 91 33 6615 3400 Fax: + 91 33 2281 7750

Mumbai 14th Floor, The Ruby 29 Senapati Bapat Marg Dadar (west) Mumbai - 400 028 Tel :+ 91 22 6192 0000 Fax : + 91 22 6192 1000 5th Floor Block B-2, Nirlon Knowledge Park Off. Western Express Highway Goregaon (E) Mumbai - 400 063 Tel: + 91 22 6192 0002 Fax: + 91 22 6192 3000 NCR Golf View Corporate Tower - B Near DLF Golf Course, Sector 42 Gurgaon – 122 002 Tel: + 91 124 464 4000 Fax: + 91 124 464 4050 3rd & 6th Floor, Worldmark-1 IGI Airport Hospitality District Aerocity New Delhi-110037, India Tel: +91 11 6671 8000 Fax +91 11 6671 9999

4th & 5th Floor, Plot No 2B, Tower 2, Sector 126, Noida - 201 304 Gautam Budh Nagar, U.P. India Tel: + 91 120 671 7000 Fax: + 91 120 671 7171 Pune C-401, 4th floor Panchshil Tech Park Yerwada (Near Don Bosco School) Pune – 411 006 Tel: + 91 20 6603 6000 Fax: + 91 20 6601 5900

For further insights, please contact: Fali Hodiwalla Partner Performance Improvement - Financial Services Email: [email protected] Phone: +91 98201 39302 Himanshu Bansal Director Financial Services – NBFC sector Email: [email protected] Phone: +91 97698 43789

Ernst & Young LLP EY | Assurance | Tax | Transactions | Advisory

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in. Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata – 700016 © 2016 Ernst & Young LLP. Published in India. All Rights Reserved. EYIN1602-014 ED None This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor. PP