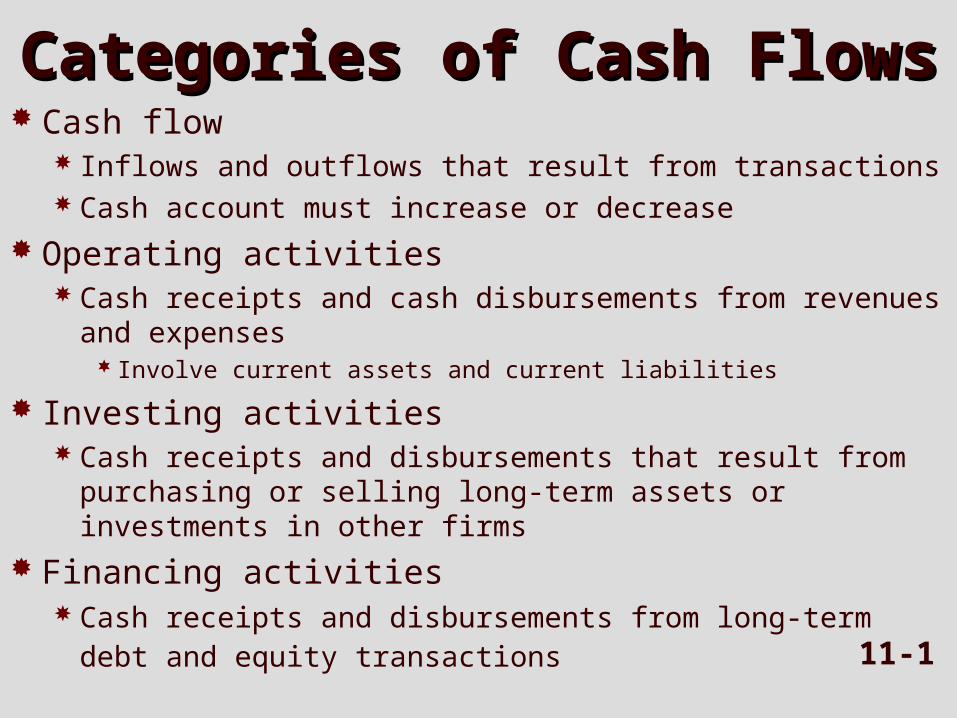

11-1 Categories of Cash Flows Categories of Cash Flows Cash flow Inflows and outflows that result from transactions Cash account must increase or decrease Operating activities Cash receipts and cash disbursements from revenues and expenses Involve current assets and current liabilities Investing activities Cash receipts and disbursements that result from purchasing or selling long-term assets or investments in other firms Financing activities Cash receipts and disbursements from long-term debt and equity transactions

Transcript

11-1

Categories of Cash FlowsCategories of Cash Flows Cash flow

Inflows and outflows that result from transactions Cash account must increase or decrease

Operating activities Cash receipts and cash disbursements from

revenues and expenses Involve current assets and current liabilities

Investing activities Cash receipts and disbursements that result from

purchasing or selling long-term assets or investments in other firms

Financing activities Cash receipts and disbursements from long-term

debt and equity transactions

11-2

Categories of Cash FlowsCategories of Cash FlowsFinancing activities

DebtIssuing debtRepaying debt

Interest expense results from financing activities because it arises from debt financing. Why is it reported in the operating section?

EquityReceiving contributions from ownersPaying dividends to owners

11-3

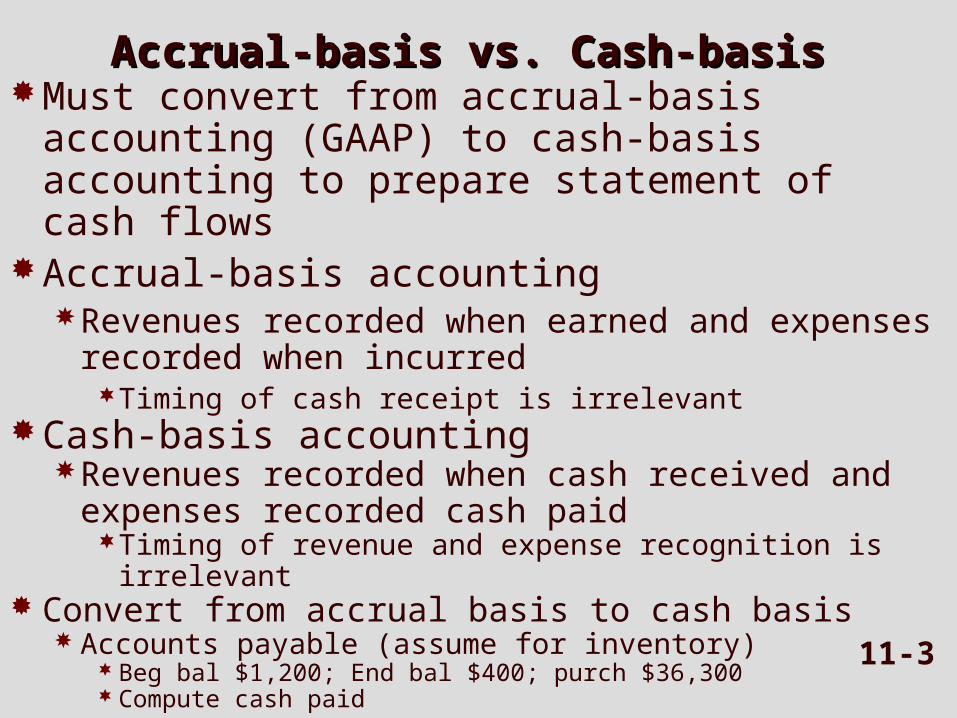

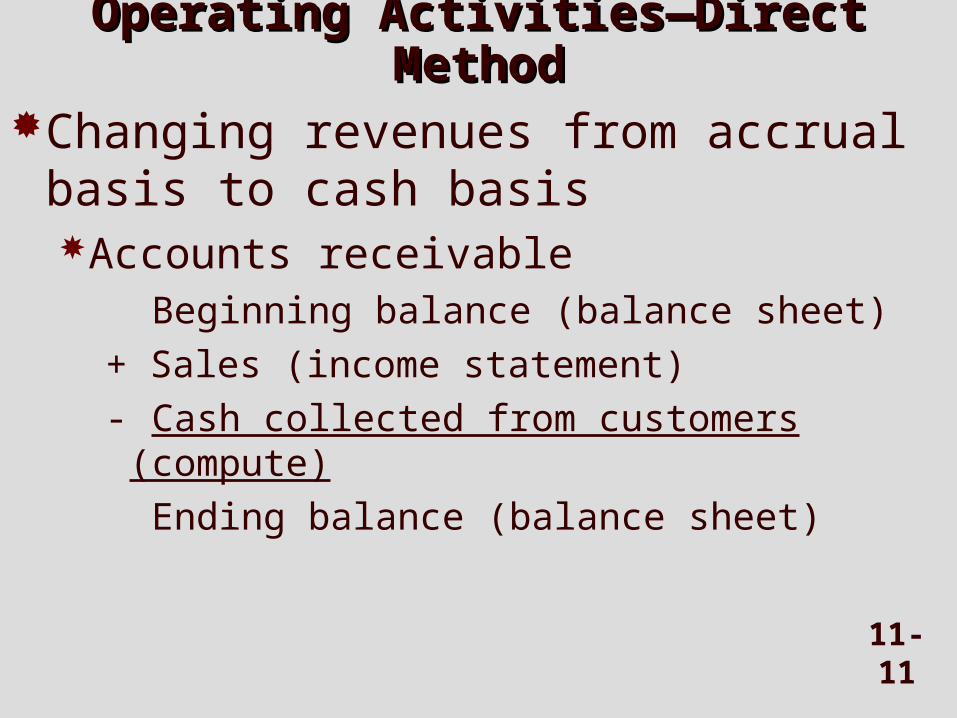

Accrual-basis vs. Cash-basisAccrual-basis vs. Cash-basis Must convert from accrual-basis accounting

(GAAP) to cash-basis accounting to prepare statement of cash flows

Accrual-basis accountingRevenues recorded when earned and expenses

recorded when incurredTiming of cash receipt is irrelevant

Cash-basis accountingRevenues recorded when cash received and

expenses recorded cash paidTiming of revenue and expense recognition is

irrelevant Convert from accrual basis to cash basis

Accounts payable (assume for inventory) Beg bal $1,200; End bal $400; purch $36,300 Compute cash paid

11-4

Operating activitiesDirect method

Cash inflows and outflows explicitly identified

Analyzes every item on income statementIndirect method

Reconciles net income and cash flowStarts with net incomeMakes adjustments for income statement

items that do not affect cashAdjust for changes in current assets and

current liabilitiesEnds with net cash flow

11-5

Investing and financing activitiesSame presentation for both direct and

indirect methodsCash flows for each activity directly

identifiedUsed by 90% of companies.Financial statements needed

Current year income statementBeginning and ending balance sheet

11-6

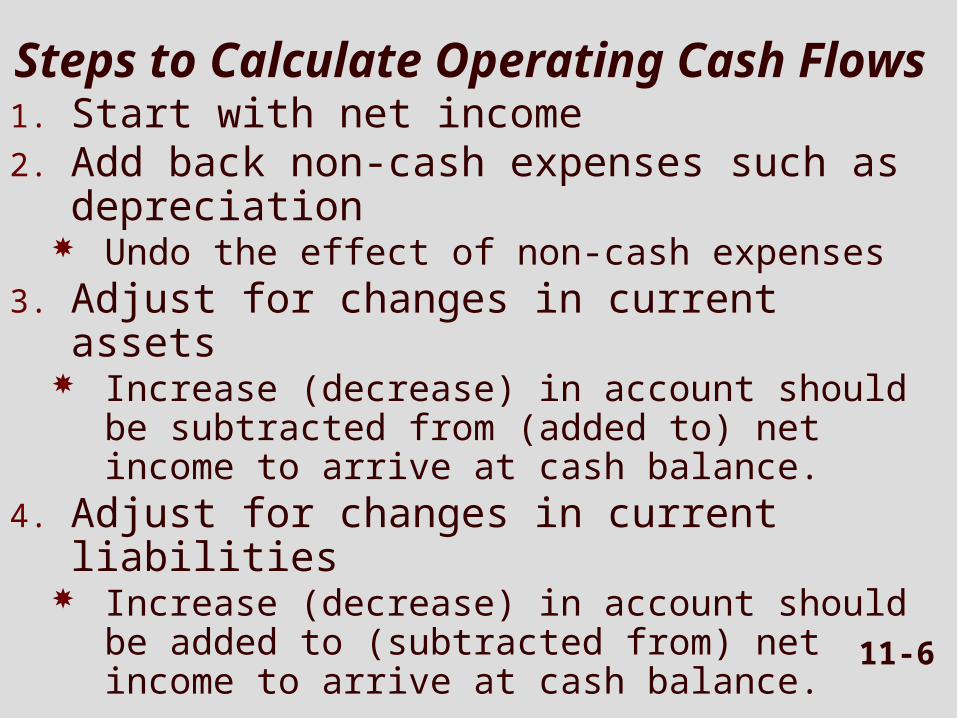

Steps to Calculate Operating Cash Flows

1. Start with net income2. Add back non-cash expenses such as

depreciation Undo the effect of non-cash expenses

3. Adjust for changes in current assets Increase (decrease) in account should

be subtracted from (added to) net income to arrive at cash balance.

4. Adjust for changes in current liabilities

Increase (decrease) in account should be added to (subtracted from) net income to arrive at cash balance.

11-7

Cash Flow Indirect Method

Sales Revenues 500,000$ Cost of Goods Sold 284,000 Gross Margin 216,000 Depreciation Expense 50,000$ Interest Expense 5,000 Salary Expense 105,000 160,000 Net Income 56,000$

11-8

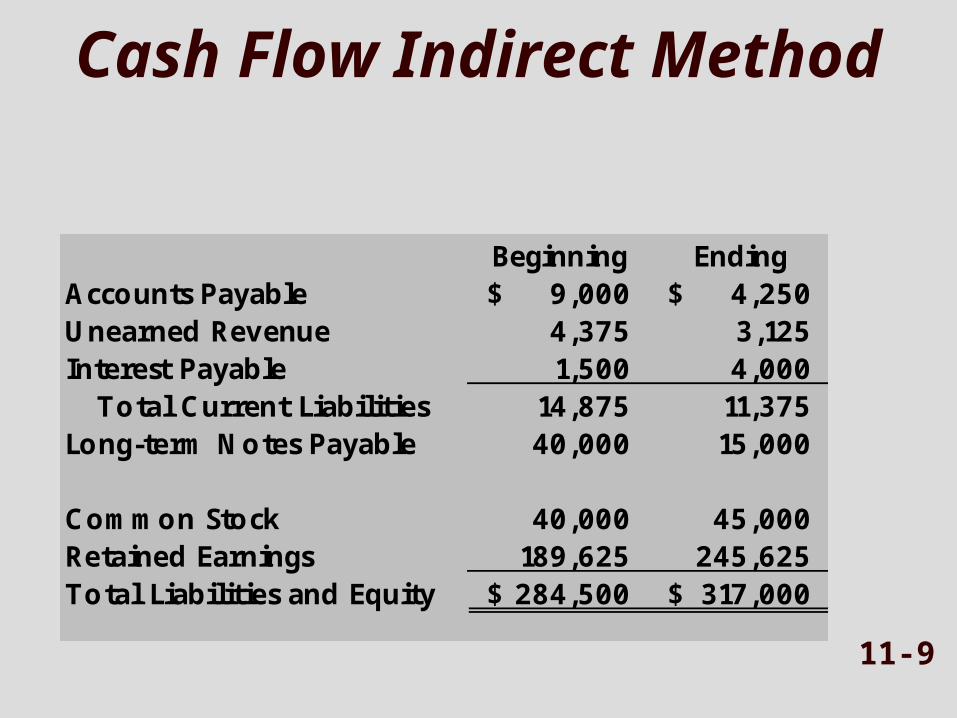

Cash Flow Indirect Method

Beginning EndingCash 37,500$ 75,000$ Accounts Receivable, net 17,000 13,000 Inventory 27,000 20,000 Prepaid Insurance - 12,000 Prepaid Rent 28,000 4,000 Total Current Assets 109,500 124,000 Equip, net of $75K & $125K Accum Depr 175,000 193,000 Total Assets 284,500$ 317,000$

Common Stock 40,000 45,000 Retained Earnings 189,625 245,625 Total Liabilities and Equity 284,500$ 317,000$

11-10

Cash Flow Indirect Method

+/-Net incomeDepreciation expenseDecrease in accounts receivableDecrease in inventoryIncrease in prepaid insuranceDecrease in prepaid rentDecrease in accounts payableDecrease in unearned revenueIncrease in interest payable Net cash from operating activities

+ Interest expense (income statement)- Cash paid for interest (compute)

Ending balance (balance sheet)

11-14

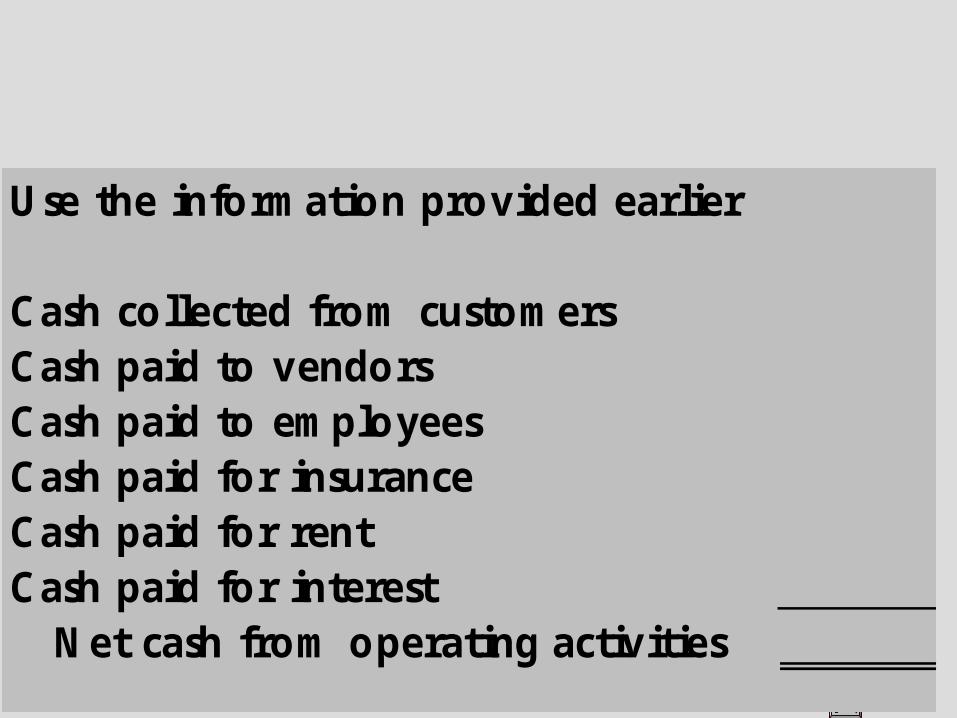

Use the information provided earlier

Cash collected from customersCash paid to vendorsCash paid to employeesCash paid for insuranceCash paid for rentCash paid for interest Net cash from operating activities

11-15

Investing and Financing Investing and Financing ActivitiesActivities

Investing cash flowsEquipment purchases/disposals require the

Need to analyze changes in long-term liability accounts

Equity financingAdditional capital contributions

Common and preferred stock accountsDividends

Retained earnings and current net income

11-16

Use the information provided earlier

Investing ActivitiesPurchase of equipment Net cash used by investing activities

Financing ActivitiesRepayment of note payableProceeds from issue of new stock Net cash used by financing activities

11-17

Preparing the Statement of Cash Preparing the Statement of Cash FlowsFlows

Prepare operating, investing, and financing sections

Supplementary disclosuresNoncash financing and investing

activitiesCash paid for interest expense and

income taxesBroken out in supplementary disclosures

because usually part of subtotals

11-18

Preparing the Statement of Cash Preparing the Statement of Cash FlowsFlows

Use the information provided earlier

Net cash provided by operations

Net cash used by investing activities

Net cash used by financing activities

Cash at beginning of yearCash at end of year

11-19

Free Cash FlowNet cash from operating activities- Cash dividends- Capital expenditures _

Free cash flow

11-20

Cash Flow Adequacy Ratio

Measures the firm’s ability to generate enough cash from operating activities to pay for its capital expenditures Net cash from operating activities _ Cash required for investing activities

Cash required for investing activities Cash paid for capital expenditures and acquisitions

minus cash proceeds from disposal of capital assets

11-21

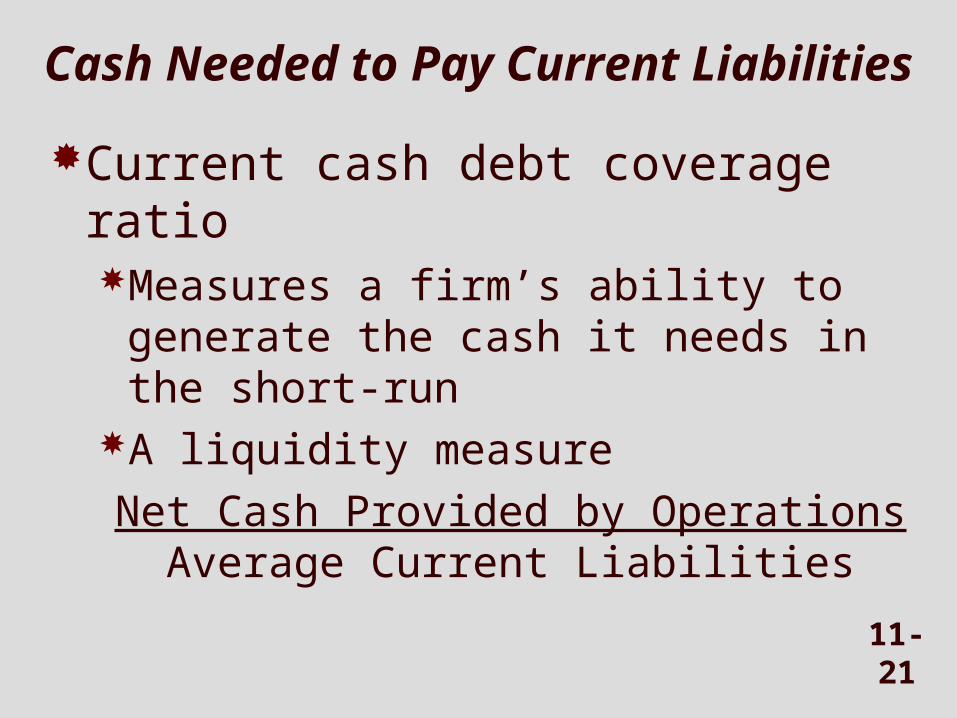

Cash Needed to Pay Current Liabilities

Current cash debt coverage ratioMeasures a firm’s ability to generate

the cash it needs in the short-runA liquidity measure

Net Cash Provided by OperationsAverage Current Liabilities

11-22

Business Risk, Control, and Business Risk, Control, and EthicsEthics

Investors’ risks associated with statement of cash flowsInvestors look for positive cash flows

![FY18 June Bernstein.pptx [Read-Only]s1.q4cdn.com/769663331/files/doc_presentations/2018/05/... · 2018-05-31 · Flow consists mainly of significant cash outflows and inflows that](https://static.documents.pub/doc/80x56/5e8b755e0a9a73246d6e3708/fy18-june-read-onlys1q4cdncom769663331filesdocpresentations201805.jpg)