20

Korean Container Shipping Market Forecasts Web: www.alphaliner.com E-mail: [email protected] 1 November 2018 Busan Port International Passenger Terminal

Korean Container Shipping Market Forecasts

Web: www.alphaliner.com E-mail: [email protected]

1 November 2018Busan Port International Passenger Terminal

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Déjà vu - has anything changed in the last 40 years?

Page 1

Recurring themes :

• Overcapacity

• Shipping companies struggle to stay afloat

• Governments continue to support struggling lines

• Changing regulatory regimes

– 2020 Sulphur Cap

– Ballast Water Management

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

True innovations remain elusive in container shipping

Page 2

Replace ‘Big Data’ with any of the latest innovation buzzwords in container shipping:-

• Digitization

• Blockchain

• Artificial Intelligence (AI)

• Predictive analytics

• Machine learning

Technology and innovations have so far failed to transform the shipping industry

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Industry consolidation – Last 10 years

Page 3

From 2008 To 2018

What has changed? ‘Global’ carriers down from 22 to 12 Scale of operations have increased by

2.0 X (Maersk) 2.2 X (MSC) 2.7 X (CMA CGM) 3.2 X (Hapag-Lloyd) 5.7 X (COSCO)

0.000.501.001.502.00

APM-Maersk

MSC

CMA CGM

Evergreen

Hapag-Lloyd

COSCO

APL

CSCL

NYK

MOL

Hanjin Shg

OOCL

K Line

Hamburg Süd

Yang Ming

CSAV

Zim

Hyundai M.M.

PIL

UASC

Wan Hai

MISC

Capacity Operated in TEU Millions (End 2008)

0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00

APM-Maersk

MSC

COSCO

CMA CGM

Hapag-Lloyd

ONE

Evergreen

Yang Ming

PIL

HMM

Zim

Wan Hai

Capacity Operated in TEU Millions (Nov 2018)

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Korean consolidation – no progress made

Page 4

From 2008 To 2018

What has changed? Fragmented market unchanged (11 carriers remain – SM Line replaced Hanjin Shg/Pan Ocean

replaced STX Pan Ocean). Only one carrier exited - Dongnama (C& Line) in 2008. Total capacity operated by Korean carriers increased by 7.6% between 2008 and 2018 But global capacity increased by 78.8% in the same period Korean carriers share have fallen behind global average by factor of 10 X

0.000.100.200.300.40

Hanjin Shg

Hyundai M.M.

KMTC

STX Pan Ocean

Sinokor

Heung-A Shg

Namsung Shg

CK Line

Pan Continental Shg

Dongjin Shg

Doowoo

Capacity Operated in TEU Millions (End 2008)

0.00 0.10 0.20 0.30 0.40

HMM

KMTC

Pan Ocean

Sinokor

Heung-A Shg

Namsung Shg

CK Line

Pan Continental Shg

Dongjin Shg

Doowoo

SM Line

Capacity Operated in TEU Millions (Nov 2018)

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

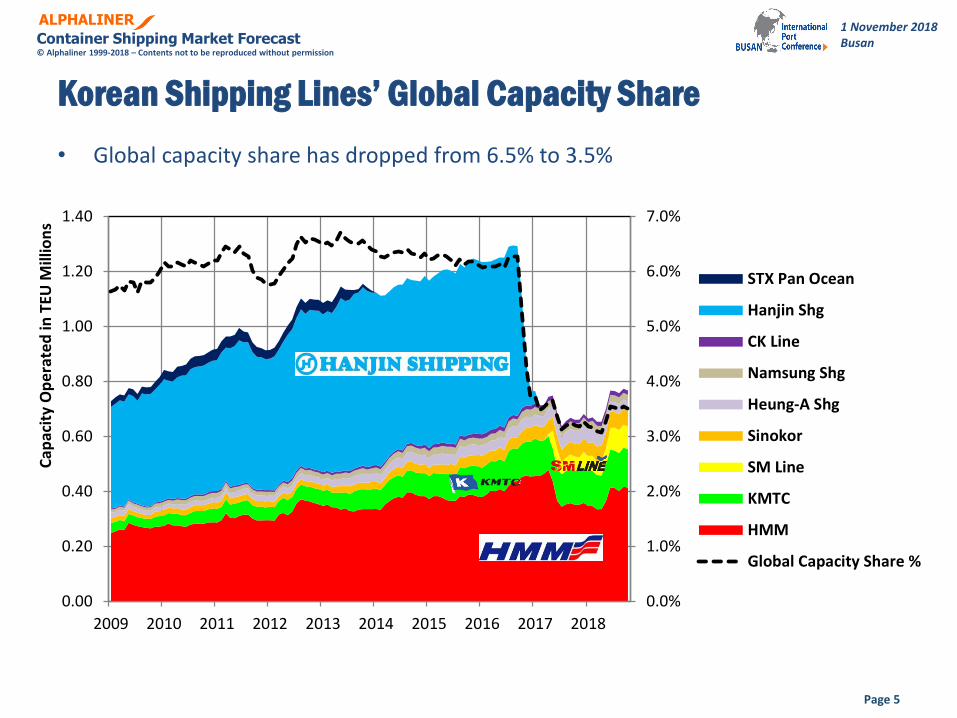

Korean Shipping Lines’ Global Capacity Share

Page 5

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Cap

acit

y O

pe

rate

d in

TEU

Mill

ion

s

STX Pan Ocean

Hanjin Shg

CK Line

Namsung Shg

Heung-A Shg

Sinokor

SM Line

KMTC

HMM

Global Capacity Share %

• Global capacity share has dropped from 6.5% to 3.5%

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

No simple fixes to complex problems

• Korea’s 100 Policy Tasks (Five-year Plan of the Moon Jae-In Administration)

– Task 80 : To make the nation a maritime power through the joint development of the shipping and shipbuilding industries

Korean’s five-year plan for the shipping industry is based on three major initiatives:

1. securing stable cargo bookings based on competitive services and freight,

2. constructing energy-efficient ships that operate at low costs, and

3. promoting stable management through continuous innovation.

But none of these initiatives address the fundamental problems that carriers face:

• Market fragmentation and excessive competition amongst Korean carriers

• Low operating margins

• Weak balance sheet and uncompetitive cost structure – especially HMM

• Over-supply of global containership fleet

When will Korean government support for shipping industry end?Page 6

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Page 7

HMM growth roadmap

• HMM capacity operated is expected to reach 940,000 teu in 2021 from 415,000 teu

• 2020 environmental regulations described as “golden opportunity for HMM’sresurgence” – but rapid expansion carries significant risks

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

Cap

acit

y O

pe

rate

d in

TEU

Mill

ion

s

HMM operated capacity evolution : 2009-2021

HMM Projections (2019-2021)

12 x 23,000 teu newbuildings to be delivered in 2Q 2020

9 x 10,000-13,000 teu to be redelivered from 2M in 2Q 2020

8 x 15,000 teu newbuildings

to be delivered in 3Q 2021

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Page 8

Korean carriers have consistently under-performed

• HMM operating margins the lowest amongst all main carriers since 2016

• Current HMM structure is set up to fail

• Future roadmap for HMM still unclear

– 2M/HMM – an unequal partnership

– New alliance partnership after 2020 still to be confirmed

– 2018 cost saving initiatives have not achieved desired results

• A complete restructuring of HMM is required – recapitalisation and removal of toxic assets together with onerous contracts

0.2%

5.5%

0.3%

-1.0%

4.7%

1.6%

-4.2%

-10.4%

3.5%

8.5%

6.8%

6.0%

5.9%

6.9%

0.4%

-8.6%

6.2%

10.0%

9.5%

4.1%

7.6%

10.5%

4.2%

-0.6%

5.4%

5.2%

4.5%

1.3%

3.3%

-1.9%

0.5%

-9.7%

2.1%

1.6%

1.2%

-2.3%

-0.3%

-2.3%

-6.5%

-15.6%

1.2%

1.2%

0.8%

0.5%

-0.5%

-4.6%

-5.8%

-10.7%

-16.4%

-20.0% -15.0% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0%

Hapag-Lloyd

CMA CGM

Wan Hai

Maersk

Zim

Evergreen

ONE

Yang Ming

HMM

Operating Profit Margin % by Quarter

1Q172Q173Q174Q171Q182Q18

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Page 9

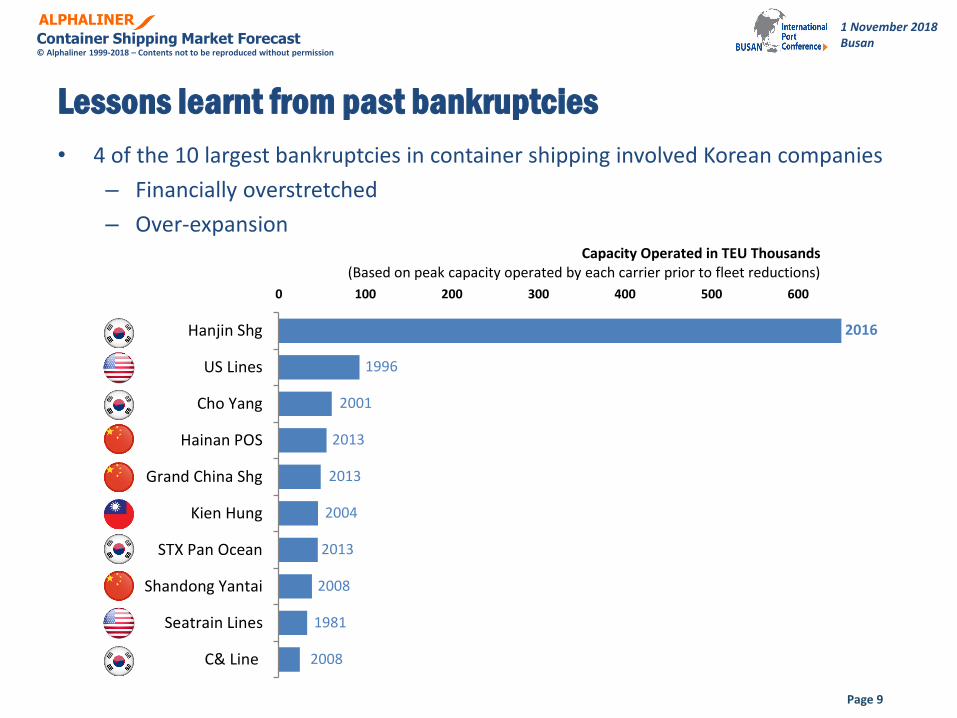

Lessons learnt from past bankruptcies

• 4 of the 10 largest bankruptcies in container shipping involved Korean companies

– Financially overstretched

– Over-expansion

0 100 200 300 400 500 600 700

Hanjin Shg

US Lines

Cho Yang

Hainan POS

Grand China Shg

Kien Hung

STX Pan Ocean

Shandong Yantai

Seatrain Lines

C& Line

Capacity Operated in TEU Thousands (Based on peak capacity operated by each carrier prior to fleet reductions)

2016

1996

2001

2013

2013

2004

2013

2008

1981

2008

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Page 10

Korea Shipping Partnership failed to address key challenges

0 100 200 300 400 500Capacity Operated in TEU Thousands

Intra-Asia(Far East)Other trades

TEU (Oct 2018)

HMM 414,073

KMTC 139,320

SM Line 81,799

Sinokor 58,116

Heung-A 33,923

Namsung 24,078

CK Line 15,776

Pan Ocean 9,820

Pan Continental 7,362

Dongjin 5,815

Doowoo 2,124

Taiyoung Shipping 672

Hansung Incl. in Sinokor

Dongyoung Incl. in Namsung

• 14 carriers (or 12 carriers if affiliated carriers are excluded)

• Only 3 limited rounds of service rationalisations , all in the intra-Asia routes

– Nov 2017 (Busan-Hakata/Moji service)

– Jan 2018 (Korea-Thailand & Korea-Indonesia)

– Mar 2018 (Korea-North Vietnam)

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Page 11

Korean Intra-Asia carriers remains highly fragmented

• 7 of the Top 25 carriers in Intra-Asia (Far East) trades are Korean but none have the scale to dominate the market

Country No. of carriers (Top 25)

S. Korea 7

China 5

Taiwan 5

Denmark 1

France 1

Japan 1

Switzerland 1

Thailand 1

Singapore 1

Indonesia 1

Russia 1

0 100 200 300

COSCO/OOCL/Golden Sea/PuhaiMaersk/MCC(Sealand Asia)

CMA CGM/CNC/APLEvergreen

Wan HaiSITCONE

KMTCMSC

Yang MingSinokorTS Line

HMMHeung-A

SinotransRCLPIL

SamuderaNamsung

FESCOCK Line

Taicang Container LineInterasia Lines

Shanghai Jin JiangSM Line

Capacity in TEU Thousands

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

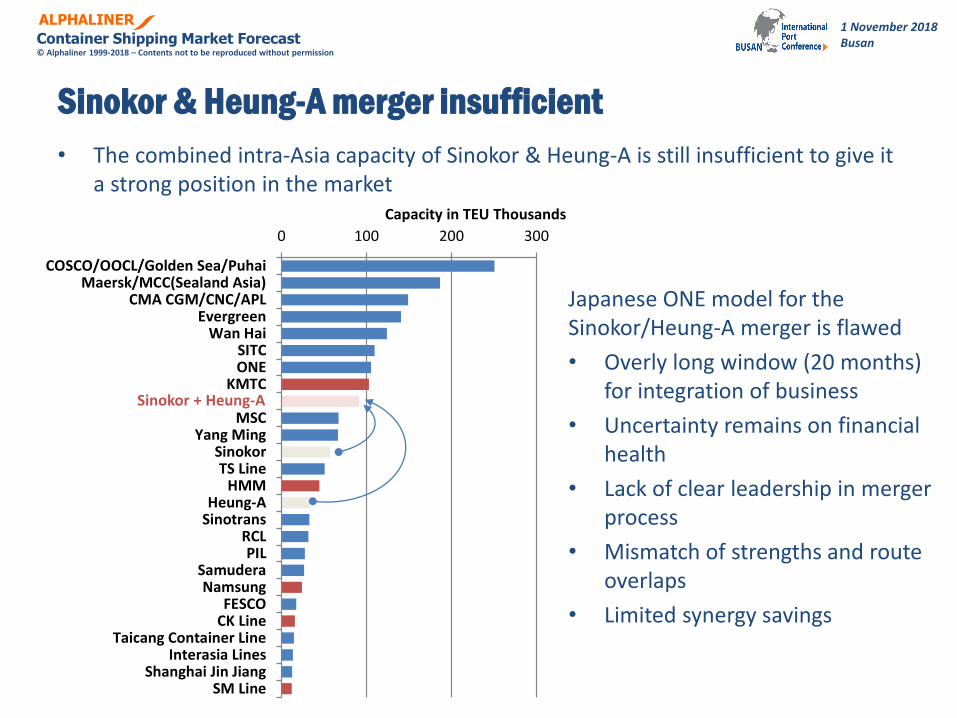

Sinokor & Heung-A merger insufficient

• The combined intra-Asia capacity of Sinokor & Heung-A is still insufficient to give it a strong position in the market

0 100 200 300

COSCO/OOCL/Golden Sea/PuhaiMaersk/MCC(Sealand Asia)

CMA CGM/CNC/APLEvergreen

Wan HaiSITCONE

KMTC

MSCYang Ming

SinokorTS Line

HMMHeung-A

SinotransRCLPIL

SamuderaNamsung

FESCOCK Line

Taicang Container LineInterasia Lines

Shanghai Jin JiangSM Line

Capacity in TEU Thousands

Sinokor + Heung-A

Japanese ONE model for the Sinokor/Heung-A merger is flawed

• Overly long window (20 months) for integration of business

• Uncertainty remains on financial health

• Lack of clear leadership in merger process

• Mismatch of strengths and route overlaps

• Limited synergy savings

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Page 13

22 November 2016

Market concentration correlates

with industry profitability …

October 2017

“Increasing liner concentration give

carriers much more control over market

and an end to era of low freight rates …”25 July 2017

“The demise of Hanjin has changed the

commercial landscape and the pricing

discipline of the carriers”

But consolidation in itself will not deliver dividends

• Predictions that consolidation will bring about market stability have proved to be premature

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

Page 14

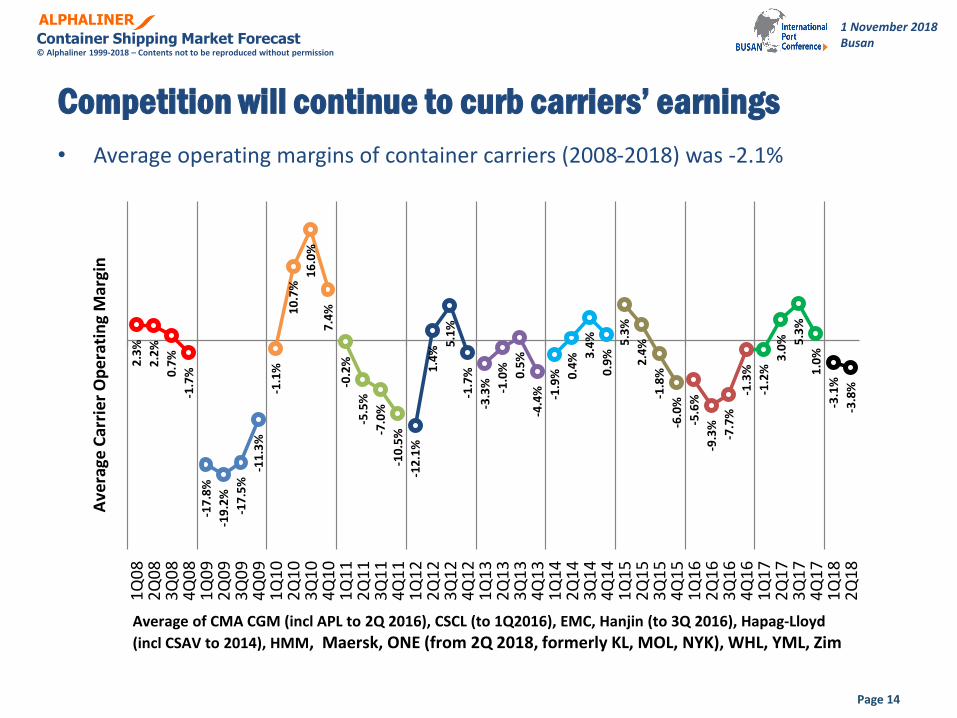

Competition will continue to curb carriers’ earnings2

.3%

2.2

%

0.7

%

-1.7

%

-17

.8%

-19

.2%

-17

.5%

-11

.3%

-1.1

%

10

.7%

16

.0%

7.4

%

-0.2

%

-5.5

%

-7.0

%

-10

.5%

-12

.1%

1.4

% 5.1

%

-1.7

%

-3.3

%

-1.0

%

0.5

%

-4.4

%

-1.9

%

0.4

% 3.4

%

0.9

% 5

.3%

2.4

%

-1.8

%

-6.0

%

-5.6

%

-9.3

%

-7.7

%

-1.3

%

-1.2

% 3

.0%

5.3

%

1.0

%

-3.1

%

-3.8

%

1Q0

82Q

08

3Q0

84Q

08

1Q0

92Q

09

3Q0

94Q

09

1Q1

02Q

10

3Q1

04Q

10

1Q1

12Q

11

3Q1

14Q

11

1Q1

22Q

12

3Q1

24Q

12

1Q1

32Q

13

3Q1

34Q

13

1Q1

42Q

14

3Q1

44Q

14

1Q1

52Q

15

3Q1

54Q

15

1Q1

62Q

16

3Q1

64Q

16

1Q1

72Q

17

3Q1

74Q

17

1Q1

82Q

18

Ave

rage

Car

rier

Op

erat

ing

Mar

gin

Average of CMA CGM (incl APL to 2Q 2016), CSCL (to 1Q2016), EMC, Hanjin (to 3Q 2016), Hapag-Lloyd

(incl CSAV to 2014), HMM, Maersk, ONE (from 2Q 2018, formerly KL, MOL, NYK), WHL, YML, Zim

• Average operating margins of container carriers (2008-2018) was -2.1%

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

2019 will remain challenging with supply overhang to persist

• Supply-Demand imbalance not expected to be cleared, with idle capacity of >750,000 teu expected to be carried over to 2019

Page 15

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

0

25

50

75

100

125

150

175

200

225

250

Idle

Fle

et a

s %

of

tota

l fle

et

Alp

hal

iner

Ch

arte

r In

dex

(Ja

n 2

00

0=1

00

)

Idle fleet as % of total fleet Alphaliner Charter Rate Index

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

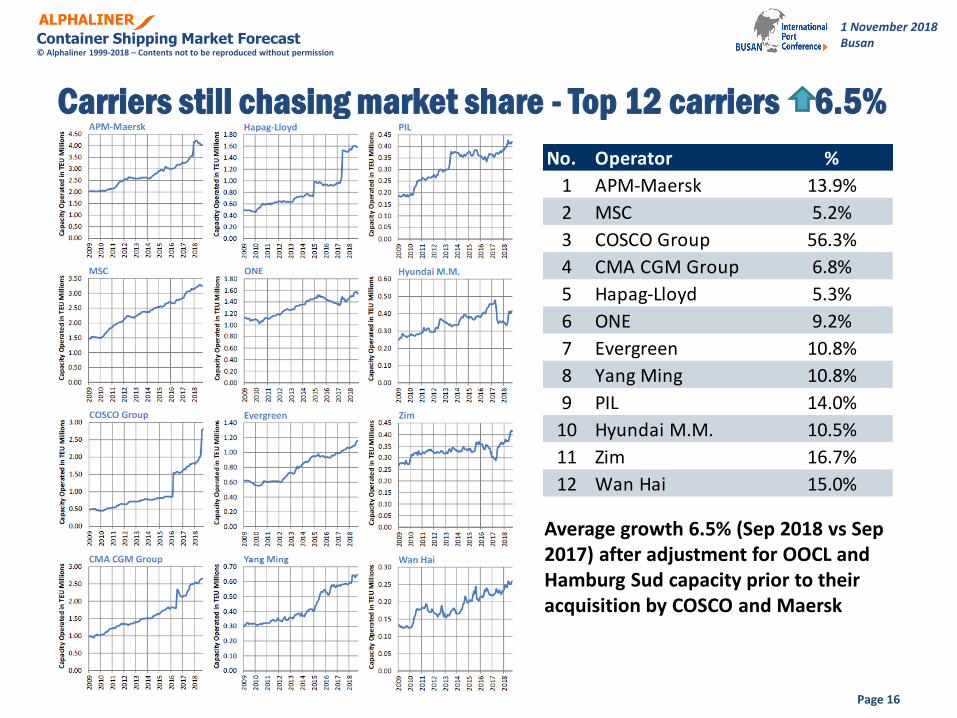

Carriers still chasing market share - Top 12 carriers 6.5%

Page 16

No. Operator %

1 APM-Maersk 13.9%

2 MSC 5.2%

3 COSCO Group 56.3%

4 CMA CGM Group 6.8%

5 Hapag-Lloyd 5.3%

6 ONE 9.2%

7 Evergreen 10.8%

8 Yang Ming 10.8%

9 PIL 14.0%

10 Hyundai M.M. 10.5%

11 Zim 16.7%

12 Wan Hai 15.0%

Average growth 6.5% (Sep 2018 vs Sep 2017) after adjustment for OOCL and Hamburg Sud capacity prior to their acquisition by COSCO and Maersk

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Cap

acit

y O

per

ated

in T

EU M

illio

ns

Maersk : Capacity Operated 2009-2018

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Cap

acit

y O

per

ated

in T

EU M

illio

ns

MSC : Capacity Operated 2009-2018

0.00

0.50

1.00

1.50

2.00

2.50

3.00

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Cap

acit

y O

per

ated

in T

EU M

illio

ns

COSCO : Capacity Operated 2009-2018

0.00

0.50

1.00

1.50

2.00

2.50

3.00

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Cap

acit

y O

per

ated

in T

EU M

illio

ns

CMA CGM : Capacity Operated 2009-2018

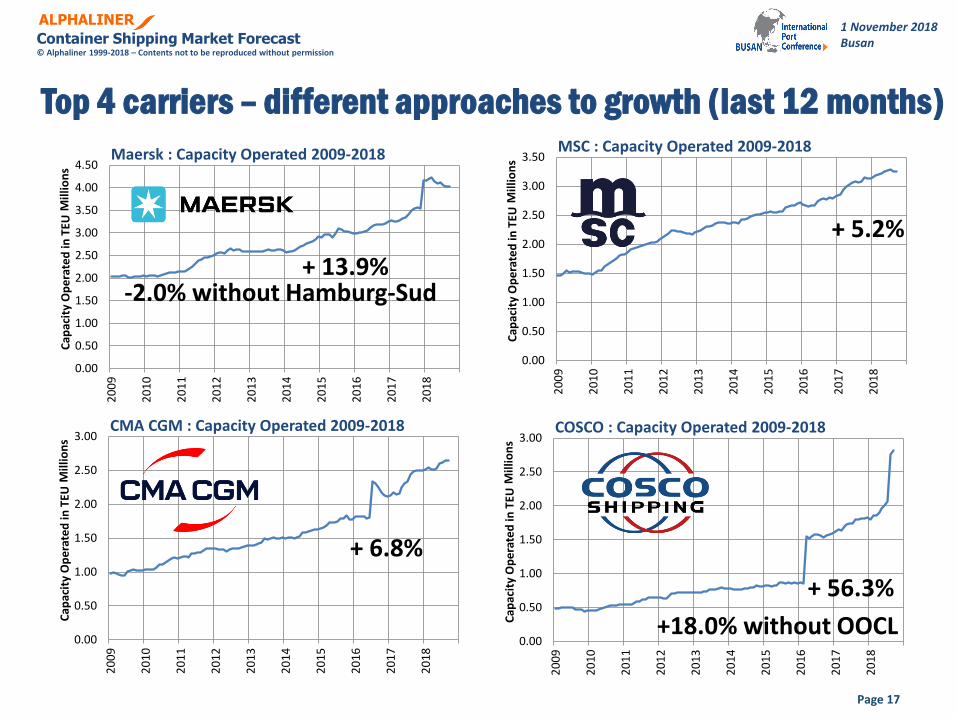

Top 4 carriers – different approaches to growth (last 12 months)

Page 17

-2.0% without Hamburg-Sud+ 13.9%

+ 5.2%

+ 6.8%

+ 56.3%

+18.0% without OOCL

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

COSCO - most aggressive growth

Page 18

COSCO SHIPPING

Deliveries in 2018

20K class – 11 ships (9 delivered)

14k class – 7 ships (5 delivered)

Deliveries in 2019

20K class – 6 ships

14k class – 4 ships

ALPHALINER

Container Shipping Market Forecast © Alphaliner 1999-2018 – Contents not to be reproduced without permission

1 November 2018Busan

End Please send any queries to [email protected]