82

0 Investor Day November 6, 2013

0

Investor Day November 6, 2013

1

Forward-Looking Statements The following information contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of

1995, including statements about the Company’s plans, strategies and prospects as well as future volume and earnings trends and

expectations. These forward-looking statements are based on management’s current expectations and beliefs, as well as a number of

assumptions concerning future events. These forward-looking statements are subject to risks, uncertainties, assumptions and other

important factors. You are cautioned not to put undue reliance on such forward-looking statements because actual results may vary

materially from those expressed or implied. The reports filed by the Company pursuant to United States securities laws contain

discussions of these risks and uncertainties, which include, but are not limited to, competition from other weight management industry

participants or the development of more effective or more favorably perceived weight management methods; the Company’s ability to

continue to develop innovative new services and products and enhance its existing services and products, or the failure of its services

and products to continue to appeal to the market; the effectiveness of the Company’s marketing and advertising programs; the impact

on the Weight Watchers brand of actions taken by the Company’s franchisees, licensees and suppliers; risks and uncertainties

associated with the Company’s international operations, including economic, political and social risks and foreign currency risks; the

Company’s ability to successfully make acquisitions or enter into joint ventures, including its ability to successfully integrate, operate or

realize the projected benefits of such businesses; uncertainties related to a downturn in general economic conditions or consumer

confidence; the seasonal nature of the Company’s business; the impact of events that discourage or impede people from gathering

with others or accessing resources; the Company’s ability to enforce its intellectual property rights both domestically and internationally,

as well as the impact of its involvement in any claims related to intellectual property rights; uncertainties regarding the satisfactory

operation of the Company’s information technology or systems; the impact of security breaches or privacy concerns; the impact of

disputes with the Company’s franchise operators; the impact of existing and future laws and regulations; the impact of the Company’s

debt service obligations and restrictive debt covenants; the possibility that the interests of the Company’s majority owner will conflict

with other holders of its common stock; and other risks and uncertainties, including those detailed from time to time in the Company’s

periodic reports filed with the Securities and Exchange Commission. The Company assumes no obligation to, and expressly disclaims

any obligation to, update or revise any forward-looking statements, whether as a result of new information, future events or otherwise,

except as required by law.

Non-GAAP Financial Statements In this presentation, we may refer to some non-GAAP financial measures, including, among others, EBITDAS. Please see Appendix

for reconciliation to appropriate GAAP financial measures.

2

Objectives (Agenda)

• Share our situation assessment

• Outline our strategic agenda

Pillar 1: Drive immediate performance improvements

Pillar 2: Re-imagine the core offering

Pillar 3: Grow the healthcare business

Pillar 4: Strengthen the organization

• Discuss financial aspirations and business model

3

Business Overview

• Who we serve

Globally, 3.5M+ active members

Age skews 50+; household income slightly higher than average; ethnically under-developed

• Who we are

Global leader in commercial weight management

50 years of history

Revenue by geography: 63% US / 37% international

Presence in 23 countries

• What we offer

Meetings

• Multi-modal behavior modification with service providers playing key role

• $42.95 per month (Monthly Pass in the US)

• 70% of revenue

Weight Watchers Online

• Pure self-help delivered digitally

• $18.95 per month (in the US)

• 30% of revenue

Source: Internal satisfaction studies

4

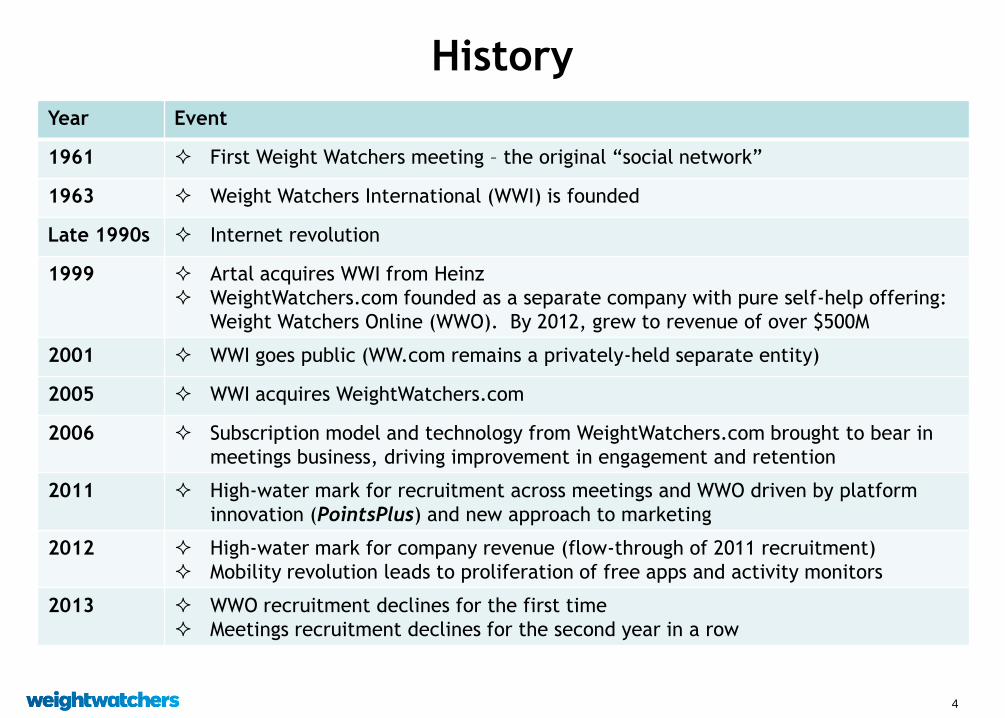

History

Year Event

1961 First Weight Watchers meeting – the original “social network”

1963 Weight Watchers International (WWI) is founded

Late 1990s Internet revolution

1999 Artal acquires WWI from Heinz

WeightWatchers.com founded as a separate company with pure self-help offering:

Weight Watchers Online (WWO). By 2012, grew to revenue of over $500M

2001 WWI goes public (WW.com remains a privately-held separate entity)

2005 WWI acquires WeightWatchers.com

2006 Subscription model and technology from WeightWatchers.com brought to bear in

meetings business, driving improvement in engagement and retention

2011 High-water mark for recruitment across meetings and WWO driven by platform

innovation (PointsPlus) and new approach to marketing

2012 High-water mark for company revenue (flow-through of 2011 recruitment)

Mobility revolution leads to proliferation of free apps and activity monitors

2013 WWO recruitment declines for the first time

Meetings recruitment declines for the second year in a row

5

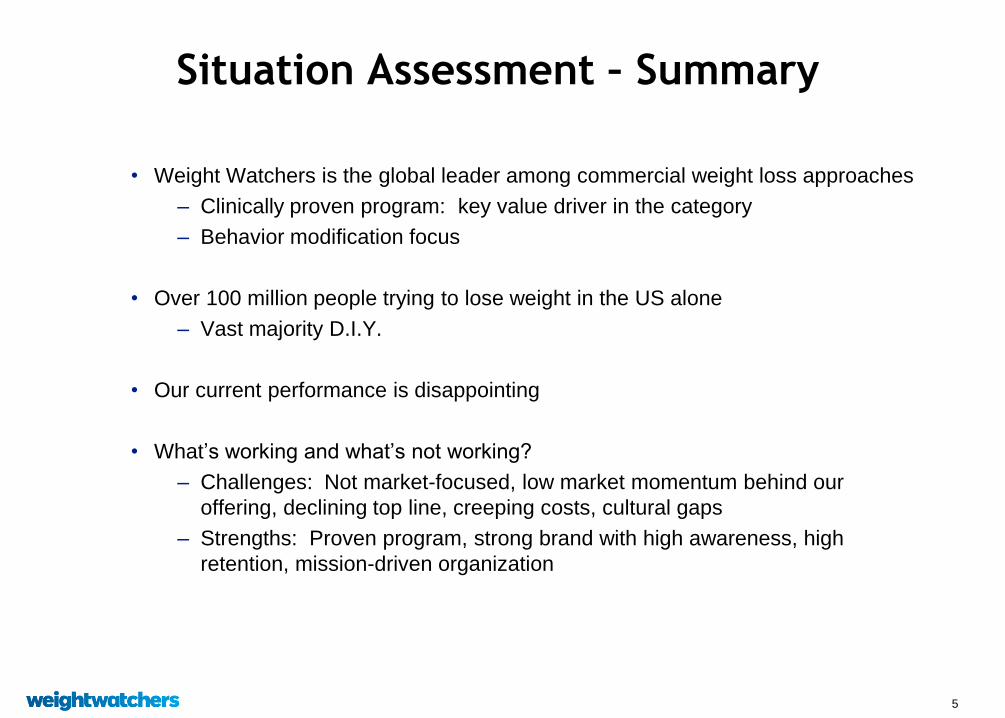

Situation Assessment – Summary

• Weight Watchers is the global leader among commercial weight loss approaches

– Clinically proven program: key value driver in the category

– Behavior modification focus

• Over 100 million people trying to lose weight in the US alone

– Vast majority D.I.Y.

• Our current performance is disappointing

• What’s working and what’s not working?

– Challenges: Not market-focused, low market momentum behind our

offering, declining top line, creeping costs, cultural gaps

– Strengths: Proven program, strong brand with high awareness, high

retention, mission-driven organization

6

Large and growing market $60B+ spent on weight-related products and services in the US alone

US Market Size, 2008 through 2013E

Market Size

($B)

Source: MarketData Enterprises, “The U.S. Weight Loss & Diet Control Market” (12th Edition, March 2013).

Note: Includes diet beverages, artificial sweeteners, health clubs, commercial weight loss approaches, OTC and prescription

drugs, diet foods and meal replacements, surgery, books and videos.

56.5

58.0 58.4

60.6 61.6

63.6

52.0

54.0

56.0

58.0

60.0

62.0

64.0

66.0

2008 2009 2010 2011 2012 2013E

Traditional View of Commercial Weight

Management Market

Dieting (alone or combined with exercise)

Exercise alone

Apps

44%

13% 87%

12%

Own Plan

71%

Book/Mag Plan

4%

Pills

2%

Commercial Plans

5%

Other

7%

Total US adults trying to lose weight (August 2013)

7 Source: Internal research

8

Support-seeking 22%

Shortcutters11%

Empowered 15%

Complacent18%

Depleted 18%

Systematic 17%

Broader market opportunity revealed with attitudinal

segmentation: 68% of US women in primary target segments

• Seeking structured, proven

plans

• Focus on long-term goals

• Expects tools/accountability for

healthy disciplined approach

• Often burdened by multiple

health conditions

• Requires more active

intervention often healthcare

professional

• Privacy critical

• Seeking clear

direction/frequent touch

points

• Many have also gotten

professional support

• Has tried multiple weight

loss plans

• Time-pressed

• Seeking short-term, quick

fix

Source: Internal research; women who want to lose 11+ pounds

9

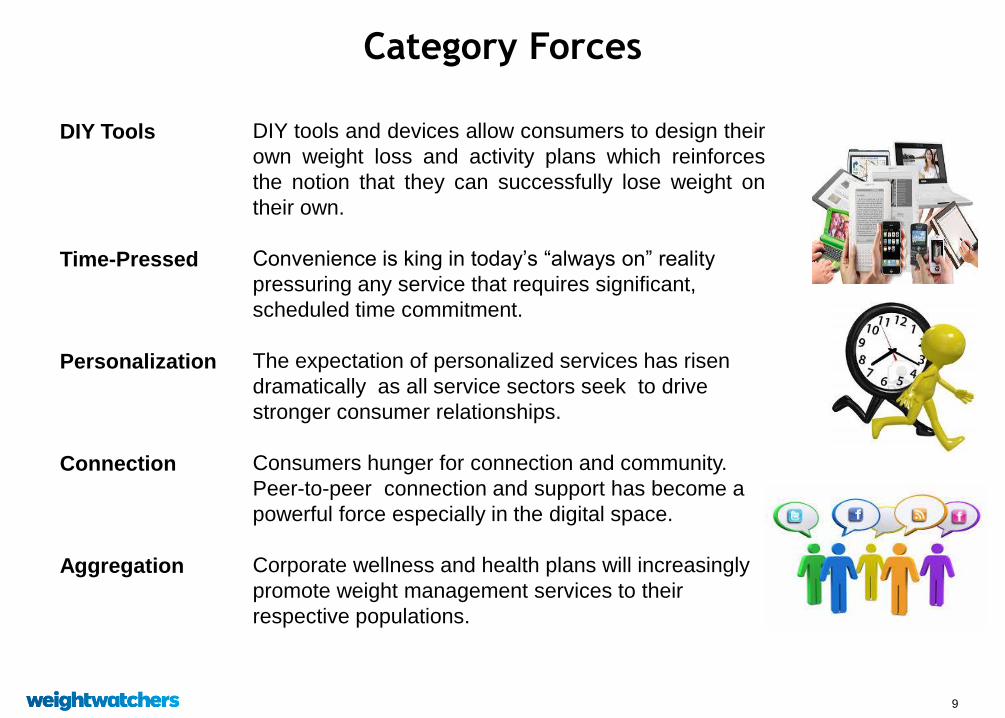

Category Forces

DIY Tools

Time-Pressed

Personalization

Connection

Aggregation

DIY tools and devices allow consumers to design their

own weight loss and activity plans which reinforces

the notion that they can successfully lose weight on

their own.

Convenience is king in today’s “always on” reality

pressuring any service that requires significant,

scheduled time commitment.

The expectation of personalized services has risen

dramatically as all service sectors seek to drive

stronger consumer relationships.

Consumers hunger for connection and community.

Peer-to-peer connection and support has become a

powerful force especially in the digital space.

Corporate wellness and health plans will increasingly

promote weight management services to their

respective populations.

10

Science: What drives weight loss

• Tracking of intake, activity and weight

• Engagement

Attendance at group support sessions

Use of digital tools

• Weight loss in the first month

• Higher initial weight

11

Unpacking 2013 revenue performance Flow-through of worsening WWO recruitment trend to negative double digits

results in paid weeks decline vs. prior in Q3

2013 vs. 2012 (%)

Q1 Q2 Q3

Weight Watchers Online (Global)

Paid Weeks 10% 4% -3%

Revenue 11% 7% 1%

Weakening WWO paid weeks drives weakening

revenue: expectation of mid-single-digit revenue

decline in Q4

12

Key revenue driver: paid weeks In 2013, meetings paid weeks continue to decline, while WWO paid

weeks turned negative for the first time in Q3

Global Paid Weeks by Year, 2007 through 2013E (M)

0

20

40

60

80

100

120

2007 2008 2009 2010 2011 2012 2013

Meetings

WWO

E*

*Based on expectations that meetings paid weeks down low double digits and WWO paid weeks down mid-single digits in Q4 2013 vs. the prior year period.

13

Marketing: 2013 spend levels roughly right

• This category is very responsive to marketing

• Uneven investment levels over the last few years driven by

strategic shifts

• Latest internal analysis suggests that 2013 spend levels are

about right and provide key learnings related to mix

• We will continue to evaluate

Source: Internal tracking study Q3 2013

14

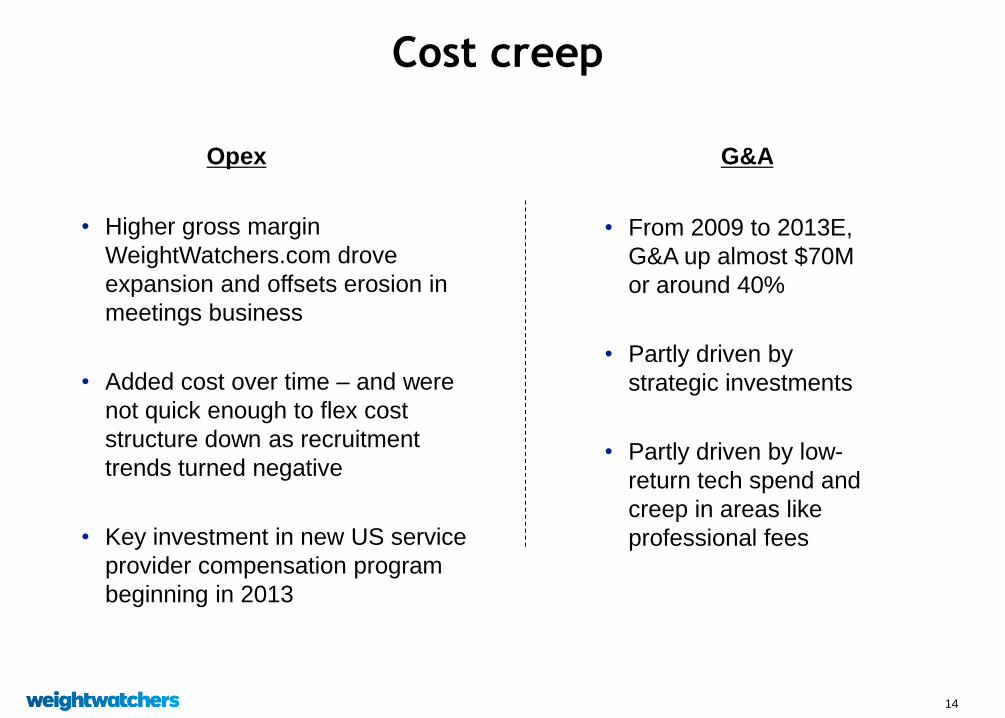

Cost creep

• Higher gross margin

WeightWatchers.com drove

expansion and offsets erosion in

meetings business

• Added cost over time – and were

not quick enough to flex cost

structure down as recruitment

trends turned negative

• Key investment in new US service

provider compensation program

beginning in 2013

• From 2009 to 2013E,

G&A up almost $70M

or around 40%

• Partly driven by

strategic investments

• Partly driven by low-

return tech spend and

creep in areas like

professional fees

Opex G&A

15

Profit reflects revenue volatility and cost creep Operating Income, 2008 through 2012

Operating

Income

($M’s)

444

395 388

546

496

-

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013E*

*Based on expectation of full year 2013 EPS of $3.85-$3.95.

Notes:

See Appendix for a reconciliation of non-GAAP financial measures to the most comparable GAAP measures.

-2008 Operating Income excludes negative impact of UK VAT ruling of $18.7M related to prior years.

-2009 Operating Income excludes impact of UK Self-employment ruling of $32.5M (pretax) related to prior years and also excludes restructuring charges of $5.5M .

-2010 Operating Income excludes the benefit of a $2.0M increase in revenues for the reversal of an over-accrual related to the UK VAT ruling .

-2012 Operating Income excludes the benefit of a $14.5 million over-accrual reversal associated with the UK Self-employment ruling.

~460

16

• Our online offer is under pressure

Missed mobility revolution

Over-estimated technology-based competitive insulation

Lower level of support

Low level of differentiation / declining value proposition

• Low level of innovation on meetings business

Added digital tools, but…

Low level of personalization

• Strong brand, but seen as judgmental, tied to perfection

• Complexity… “like a maze”

• Under-leveraged community

Key challenges flow from the bifurcation of our

offerings and our organization

17

• Clear global market leader in commercial weight loss

Scale

Scope

Profitability

• Powerful brand

High awareness

Trust

Efficacy

• Proven program

Scientifically supported

Multi-modal… in person, online, mobile

Leaders

• Large multi-tiered community

Active members

Lapsed

Favorables

Strengths to build on

18

1. Drive immediate performance improvement

2. Re-imagine the core offering

3. Grow the healthcare business

4. Strengthen the organization

The Four Strategic Pillars

19

Objectives (Agenda)

• Share our situation assessment

• Outline our strategic agenda

Pillar 1: Drive immediate performance improvement

Pillar 2: Re-imagine the core offering

Pillar 3: Grow the healthcare business

Pillar 4: Strengthen the organization

• Discuss financial aspirations and business model

20

Driving immediate performance improvement Cost, also part of Pillar 1, will be discussed later in presentation

Initiative Description

Product

Enhancements

Increase differentiation of the Online product

21

Driving immediate performance improvement Cost, also part of Pillar 1, will be discussed later in presentation

Initiative Description

Product

Enhancements

Increase differentiation of the online product

January

Enrollment

Insight-driven program news:

• Created specifically to resonate with the January consumer

mindset

• Anxious, overwhelmed, fear of failing

• New beginning as the point of inspiration

• Innovative on-ramp to the Weight Watchers experience

22

Driving immediate performance improvement Cost, also part of Pillar 1, will be discussed later in presentation

Initiative Description

Product

Enhancements

Increase differentiation of the online product

January

Enrollment

Insight-driven program news:

• Created specifically to resonate with the January consumer

mindset

• Anxious, overwhelmed, fear of failing

• New beginning as the point of inspiration

• Innovative on-ramp to the Weight Watchers experience

First Four

Weeks

Driving engagement by focusing on early tenures - insights:

• Our leaders are more comfortable providing support to

members several months into their journeys, while…

• …our members want more help early on than we give them

• At the end of the first month, the propensity of a meeting

enrollment attending in any given week is in the mid 60’s. At

the end of the second month, it is in the mid 40’s.

23

Driving immediate performance improvement Cost, also part of Pillar 1, will be discussed later in presentation

Initiative Description

Product

Enhancements

Increase differentiation of the online product

January

Enrollment

Insight-driven program news:

• Created specifically to resonate with the January consumer

mindset

• Anxious, overwhelmed, fear of failing

• New beginning as the point of inspiration

• Innovative on-ramp to the Weight Watchers experience

First Four

Weeks

Driving engagement by focusing on early tenures - insights:

• Our leaders are more comfortable providing support to

members several months into their journeys, while…

• …our members want more help early on than we give them

• At the end of the first month, the propensity of a meeting

enrollment attending in any given week is in the mid 60’s. At

the end of the second month, it is in the mid 40’s.

Consumer

Activation

Compelling advertising – strong investment, optimized mix

Leverage large community for brand advocacy to drive recruitment

24

Objectives (Agenda)

• Share our situation assessment

• Outline our strategic agenda

Pillar 1: Drive immediate performance improvement

Pillar 2: Re-imagine the core offering

Pillar 3: Grow the healthcare business

Pillar 4: Strengthen the organization

• Discuss financial aspirations and business model

25

Re-imagine the core offering

• Create a new portfolio of consumer offerings

• Break free from divide between online and meetings

• Leverage a deeper understanding of consumer needs…

• What drives value in the category

• Solve for the consumer’s weight management needs on the

consumer’s terms

• Build a leading-edge test-and-learn model

• Better read, faster entry

• Evolve brand positioning in concert with offering

26

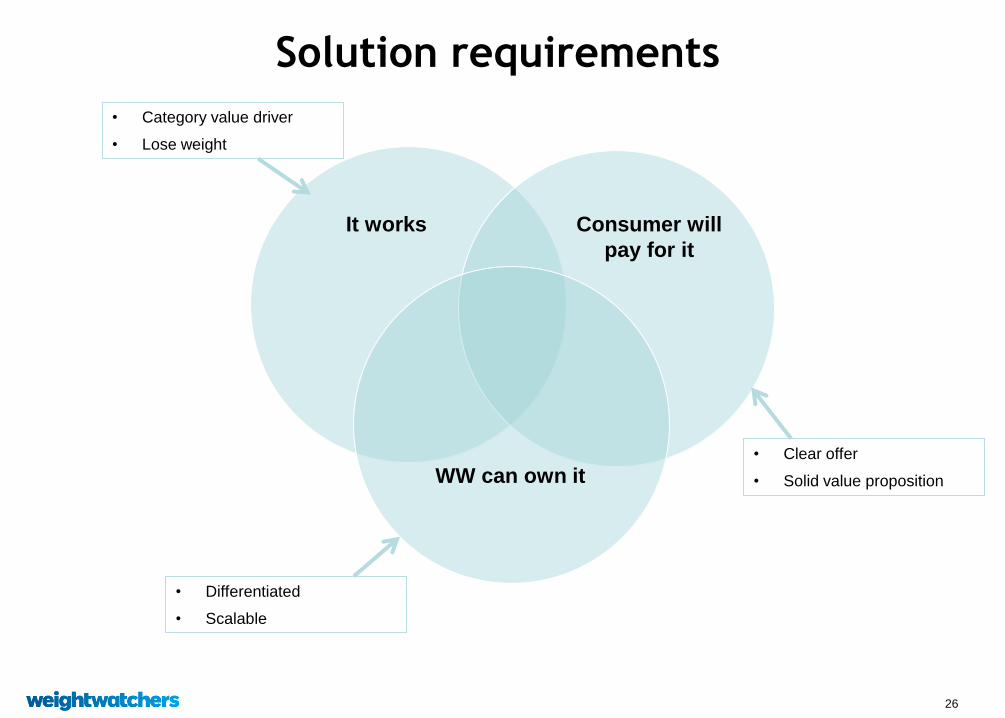

Solution requirements

It works Consumer will

pay for it

WW can own it

• Category value driver

• Lose weight

• Differentiated

• Scalable

• Clear offer

• Solid value proposition

27

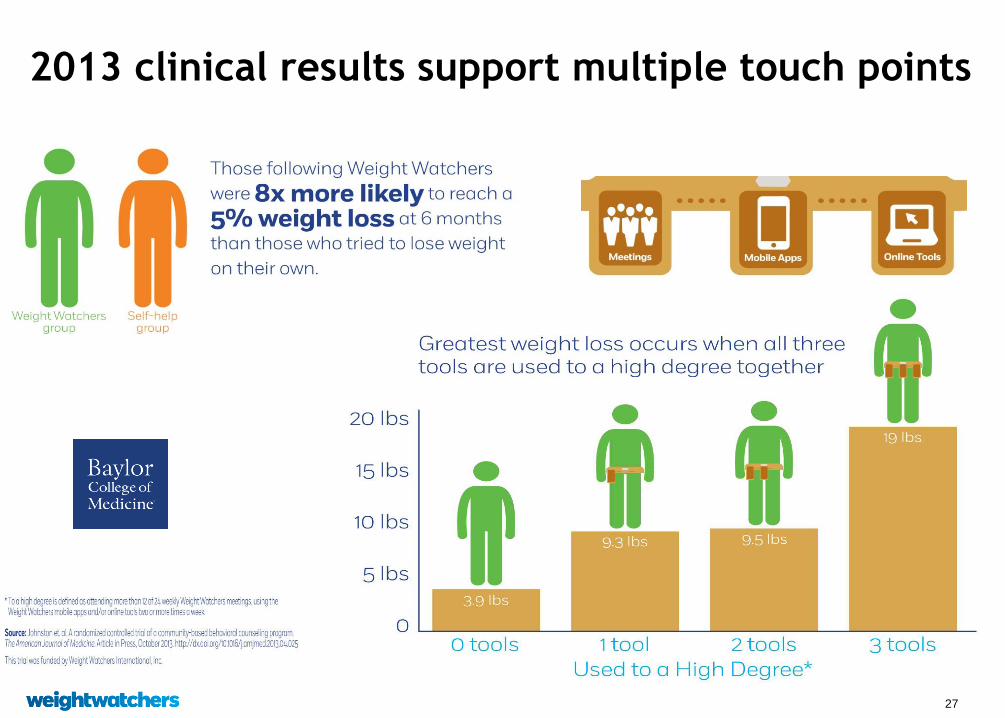

2013 clinical results support multiple touch points

28

Insights drive exploration

Example insight Exploration

• Consumers actively seeking less judgmental support

for their journey

• Support

• Popularity of D-I-Y is evidence that consumers seek a

program that ‘fits my goals & preferences’ • Personalization

• Time scarcity demands a more flexible experience

that allows users to follow WW on their terms

• On demand

• Gameful engagement is a powerful currency for

creating stickier experiences

• Immersion

• Weight-conscious consumers have varied goals

• Success

29

• Face-to-face group meetings

• Access to a leader

• WW-driven conversations

Areas of exploration

SUPPORT

• Peer to peer, on-demand community

• Access to team of experts

• 1:1 coaching on demand

• Consumer-driven conversations /

topics

Potential

additions

30

• Choose Meetings or Online

• Eat your favorite foods

• Browse to find the right advice

for you

Areas of exploration

PERSONALIZATION

• Matched to a group of others like you

• Dietary suggestions based on your

nutrition preferences

• Recommendations tailored to your

goals & preferences

• A program defined by your own goals

Potential

additions

31

• Built one-size-fits-all

• Attend a meeting at a specific time

• Delivery channels dictated service

(Meetings vs. Online)

• Use digital tools for on-the-go situations

• Monthly subscription

Areas of exploration

ON DEMAND

• Tailored to your desired level of intensity

• Flexible schedules for accessing experts and

support

• Flexible access to service across all touch

points

• Flexible pricing / payment options

• Build your own package or program

Potential

additions

32

• Tracking tokens

• New topics each week

• Weight goal milestones

• Community and access to a leader

• Closed WW platform

Areas of exploration

IMMERSION

• Compelling incentives and rewards

• Crowd-sourced topics / format

• Game-like experiences

• Social / Community Challenges

• Relevant 3rd party partnerships

Potential

additions

33

• Losing weight

Areas of exploration

SUCCESS

• Gaining a healthy lifestyle

• Getting active / fit

Potential

additions

34

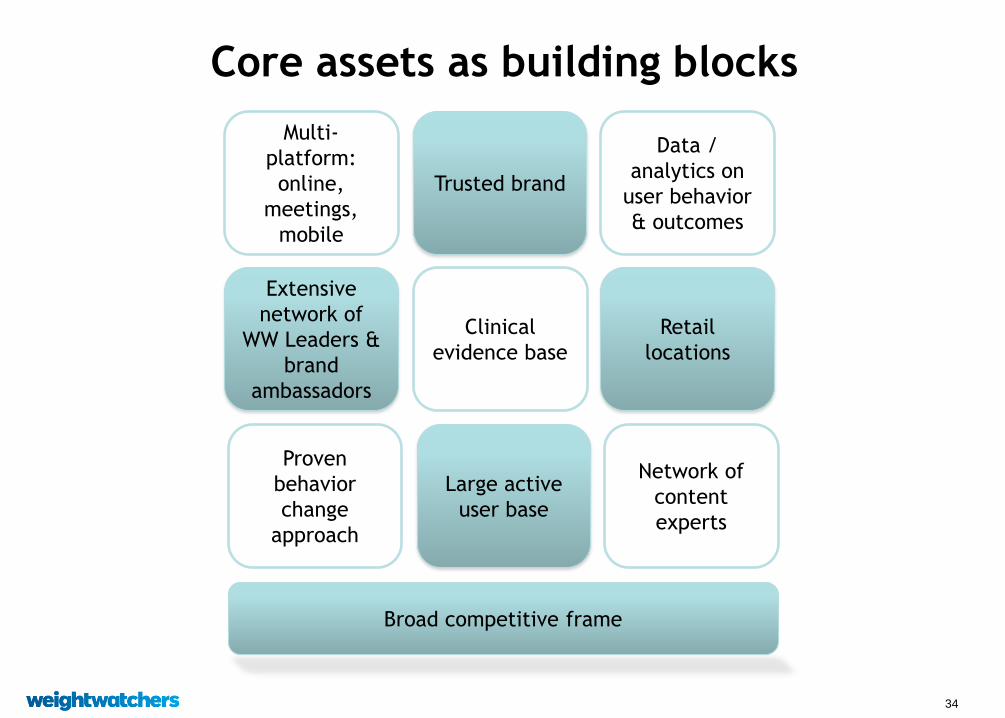

Core assets as building blocks

Extensive

network of

WW Leaders &

brand

ambassadors

Clinical

evidence base

Retail

locations

Multi-

platform:

online,

meetings,

mobile

Trusted brand

Data /

analytics on

user behavior

& outcomes

Proven

behavior

change

approach

Large active

user base

Network of

content

experts

Broad competitive frame

35

Consumer validation engine

Ideas / Insights

Concept optimization

Product Development

CONCEPT

1

CONCEPT

2

• Shortens cycle time

• Improves validity

• Leverages richness of asset base and community

• Integrated with product development

36

Building discipline and filling the pipeline

Timing

• Definition

• Ability to implement

Ideas / Insights

Concept optimization

Product Development

CONCEPT

1

CONCEPT

2

37

Evolve the brand positioning in concert with

offering

Current

Strengths Inclusiveness

“Support”

38

Objectives (Agenda)

• Share our situation assessment

• Outline our strategic agenda

Pillar 1: Drive immediate performance improvement

Pillar 2: Re-imagine the core offering

Pillar 3: Grow the healthcare business

Pillar 4: Strengthen the organization

• Discuss financial aspirations and business model

39

Weight Watchers Health Solutions Agenda

I. Overview

II. The B2B/Healthcare Market – Recent Trends

III. Sizing the Opportunity

IV. Our Strategy to Compete

V. Requirements to Compete

40

Weight Watchers Health Solutions Overview / Investment Thesis

• Clear market opportunity

Obesity drives significant cost for employers, health plans, providers and employees

• Growing emphasis on prevention driven by regulatory changes and focus on corporate

wellness

Mitigate exploding cost of chronic disease treatment

• WWHS is well-positioned to serve this market based on our assets

Strong Science and clinical proof, face-to-face, brand, market presence

Existing foothold in 200+ blue chip clients

$75M business today, split between small and large employers

• Identified what has been missing – in the process of putting those capabilities in place

HIPAA, Systems, Data capture, Dedicated team with healthcare experience

• Financially: significant, incremental and profitable (margins similar to traditional B2C)

• Option value beyond ‘base’ opportunity

41

We are mapping our plan against the US

healthcare ecosystem

Payor

Intermediary

Provider

Patient /

Consumer

Employers Government

Health

Plans

Benefit

Consultants TPAs PBMs

Health Systems

Physician

Networks

(PPOs)

Wellness

Vendors

Consumers

Consumers

Where we play today

Consumers

42

Obesity is the largest preventable condition

driving healthcare systems costs (US)

Excess weight drives 10% of healthcare costs (Harvard)

Obesity raises annual medical costs by $2,741/adult (Jnl Health Economics)

http://www.hsph.harvard.edu/obesity-prevention-source/obesity-consequences/economic/

Finkelstein EA, Trogdon JG, Cohen JW, Dietz W. Annual medical spending attributable to obesity:

Medical Care Costs of Obesity – Cawley, Jnl Health Economics 2012

payer- and service-specific estimates. Health Aff (Millwood). 2009;28(5):w822–w831.

http://www.teachade.com/resources/support/5035b250c0cd6.pdf

Increased cost to private insurers

$443 per

inpatient

stay

$398 per

outpatient

stay $284

in

prescription

benefits

$160B cost to payers

$140B cost to

individuals

$130B cost to

employers

$20B other

80% of diabetes cases

attributable to obesity

Heart disease is the

cause of death in 68%

of adults with

diabetes; stroke,16%

Diabetes accounts for 45%

of kidney disease

cases

70% of hypertension cases are attributable to

obesity

79M Americans suffer

from pre-Diabetes for

which the CDC recommended

treatment is intensive

behavioral therapy for obesity

43

Healthcare reform has dramatically

increased focus on prevention services

Access and

Reimbursement of

Counseling for

Obesity and Obesity-

Related conditions

will increase over the

next several years

ACA - required essential health benefits include all

USPSTF A and B-rated preventive care - Obesity

Allows Health Plans to use “reasonable management techniques”

to determine coverage and institute alternative IBT approaches

Weight Watchers has been clinically proven to meet the

Intensive Behavioral Therapy requirements and is the only

program available on a national basis

Change in orientation toward consumerism

Increase in demand for consumer choice and creating relationships with

members as consumers

Benefit design shift toward consumer accountability

is further encouraged in health care reform

Incentive designs and variable premiums to encourage personal

responsibility for health and wellness

44

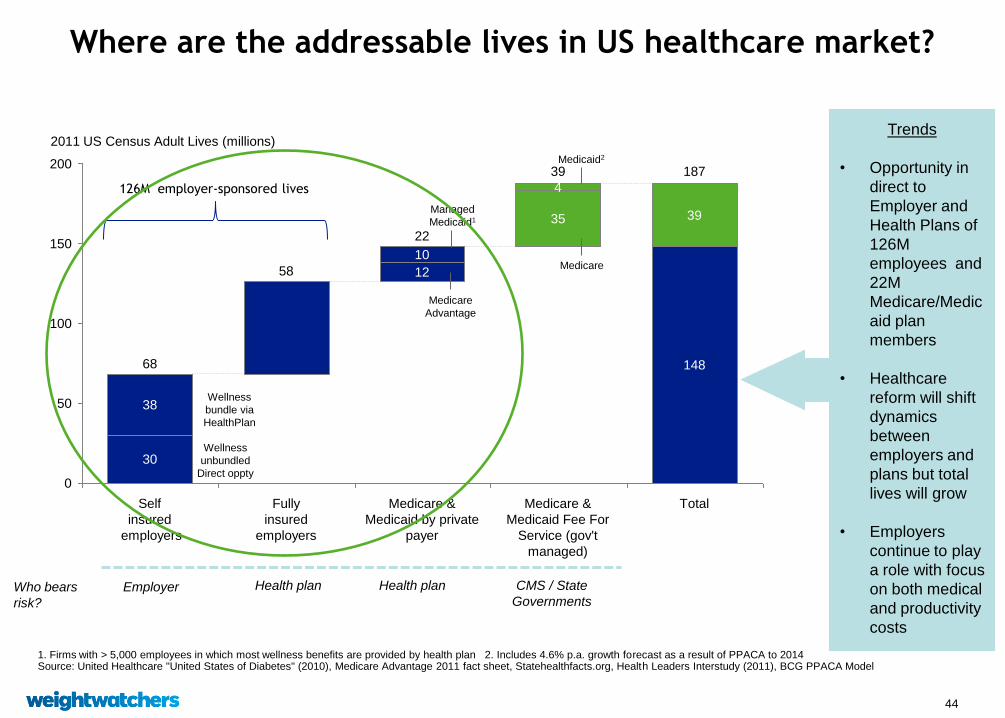

Where are the addressable lives in US healthcare market?

Trends

• Opportunity in

direct to

Employer and

Health Plans of

126M

employees and

22M

Medicare/Medic

aid plan

members

• Healthcare

reform will shift

dynamics

between

employers and

plans but total

lives will grow

• Employers

continue to play

a role with focus

on both medical

and productivity

costs

2011 US Census Adult Lives (millions)

200

150

100

50

0

Total

187

148

39

Medicare &

Medicaid Fee For

Service (gov't

managed)

39

12

10

Fully

insured

employers

58

Self

insured

employers

68

30

38

35

22

Medicare &

Medicaid by private

payer

4 126M employer-sponsored lives

Wellness

bundle via

HealthPlan

Wellness

unbundled

Direct oppty

Medicare

Advantage

Managed

Medicaid1

Medicare

Medicaid2

1. Firms with > 5,000 employees in which most wellness benefits are provided by health plan 2. Includes 4.6% p.a. growth forecast as a result of PPACA to 2014 Source: United Healthcare "United States of Diabetes" (2010), Medicare Advantage 2011 fact sheet, Statehealthfacts.org, Health Leaders Interstudy (2011), BCG PPACA Model

Who bears

risk?

Employer Health plan Health plan CMS / State

Governments

45

How our Weight Watchers Health Solutions Model Works

Today + Tomorrow

• Product/Service Scope

• Client Customization

• Client Subsidy/

Reimbursement

• Pricing

Employer Direct Sales

Health Plan

Benefit Consultant Via Intermediary Client Sales Call

Client – Sell-in

Member - Pull-through

• Enrollment

• Subsidy/

Reimbursement level

• Employee Co-Pay

• Engagement

Employee direct marketing

Health Plan Wellness Via Other Direct to member

WWHS

Sales Team

WWHS

Marketing/Acct Mgmt

Team

46

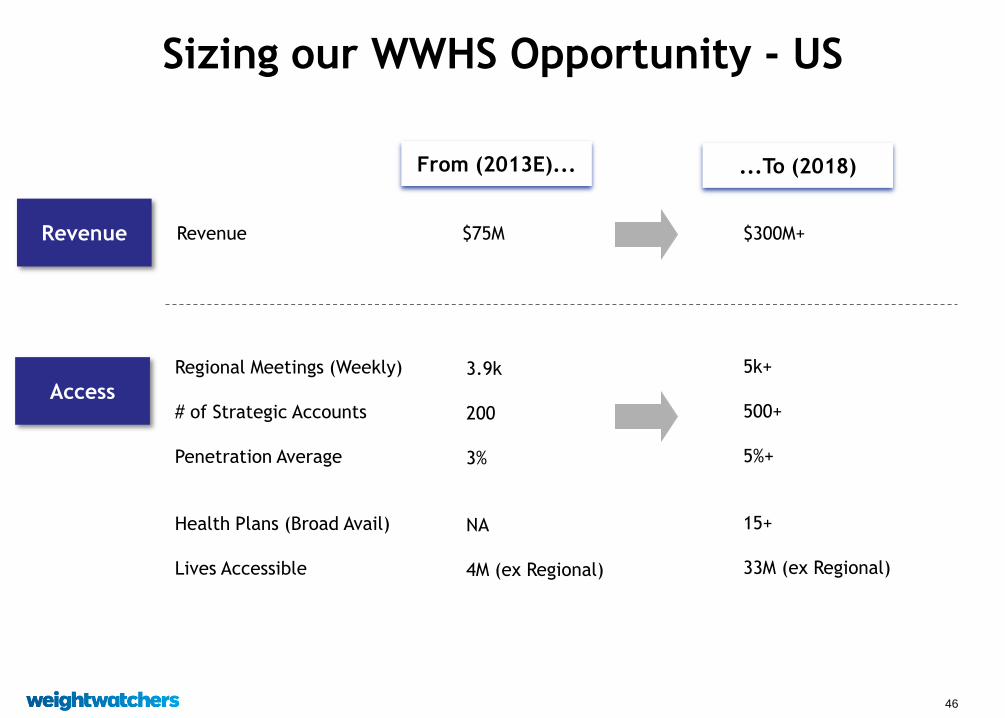

Sizing our WWHS Opportunity - US

From (2013E)... ...To (2018)

Access

Regional Meetings (Weekly)

# of Strategic Accounts

Penetration Average

Health Plans (Broad Avail)

Lives Accessible

Revenue Revenue $75M

3.9k

200

3%

NA

4M (ex Regional)

5k+

500+

5%+

15+

33M (ex Regional)

$300M+

47

US Market Opportunity Market share based approach

Obesity and Weight

Management

Potential Weight

Watchers Share

Accessible Market

Share

Revenue

Total Preventive

Health & Wellness

Market Size

(1) Analysis of preventive health and wellness services market and segments (KFF 2013, US census 2012,Towers Watson 2012, Willis Survey 2011). Employer

incentives for wellness related behavior change have doubled to $561M since 2009 (Fidelity Investments and NBGH Report 2013)

(2) Analysis of obesity and weight management services market. 30-60% of employers offer weight management programs (KFF 2013, Towers Watson 2012,

SHRM 2012).

$6 – 10 Billion

20 - 25%

$300 – 500 Million

• Large and growing size of

Preventive Health and Wellness

market (1)

• Obesity and weight

management programs are

growing focus of preventive

health (2)

• Market leaders in other

healthcare services have

achieved 20% - 30% share

$1.2 – 2 Billion

48

✔

✔

✔

✔

✔

✔

✔

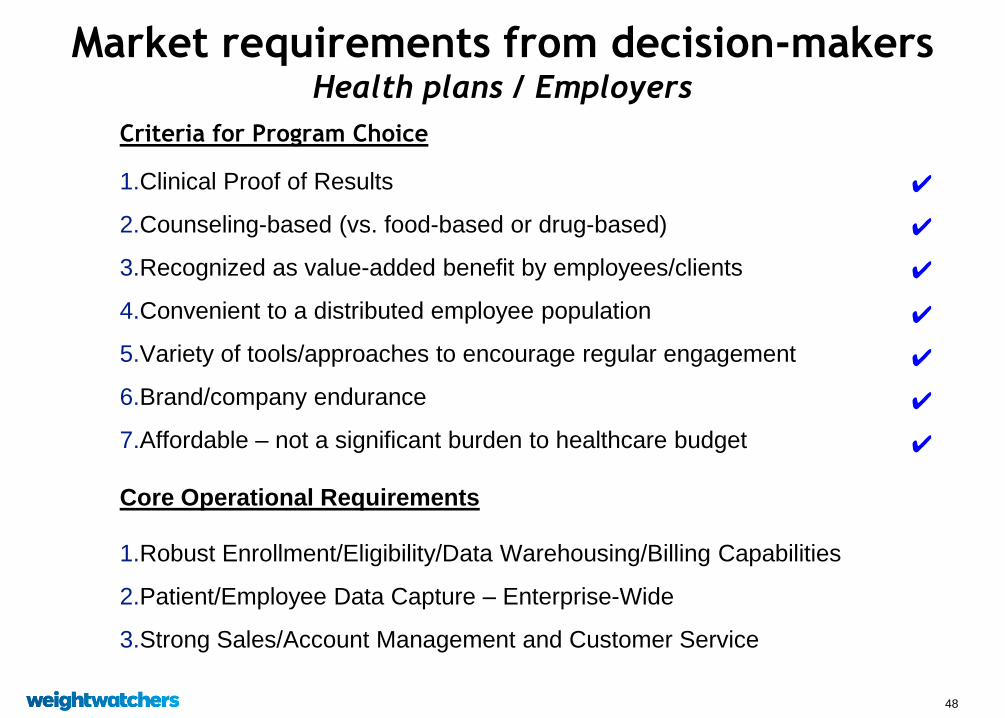

Market requirements from decision-makers Health plans / Employers

Criteria for Program Choice

1.Clinical Proof of Results

2.Counseling-based (vs. food-based or drug-based)

3.Recognized as value-added benefit by employees/clients

4.Convenient to a distributed employee population

5.Variety of tools/approaches to encourage regular engagement

6.Brand/company endurance

7.Affordable – not a significant burden to healthcare budget

Core Operational Requirements

1.Robust Enrollment/Eligibility/Data Warehousing/Billing Capabilities

2.Patient/Employee Data Capture – Enterprise-Wide

3.Strong Sales/Account Management and Customer Service

49

Survey of Corporate Wellness Decision Makers

WEIGHT WATCHERS SURVEY AMONG CORPORATE HR & BENEFITS DECISION MAKERS Q32. If you could only offer one of these programs at your place of work, which one would it be? *Not asked if not aware of any of the programs listed Q33. Why this program? (open end – not coded)

Preference Among Workplace Obesity Programs

58% NET

7% NET

2% NET

5% NET

Open Ended Response - Why Weight Watchers?

• Popular among employees

• Teaches lifestyle change

• Best reputation and gimmick-free

• Employees want it

• I think it is more practical and easy to follow

• It works and is cost-effective

• The support system is better and more user-friendly

50

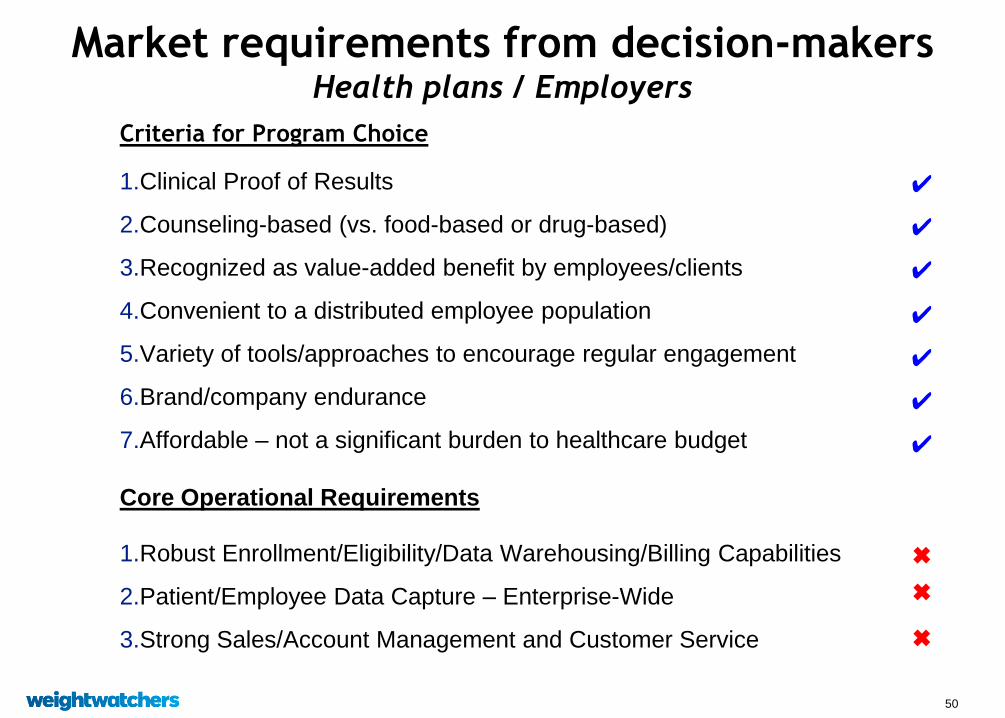

✔

✔

✔

✔

✔

✔

✔

✖

✖

✖

Market requirements from decision-makers Health plans / Employers

Criteria for Program Choice

1.Clinical Proof of Results

2.Counseling-based (vs. food-based or drug-based)

3.Recognized as value-added benefit by employees/clients

4.Convenient to a distributed employee population

5.Variety of tools/approaches to encourage regular engagement

6.Brand/company endurance

7.Affordable – not a significant burden to healthcare budget

Core Operational Requirements

1.Robust Enrollment/Eligibility/Data Warehousing/Billing Capabilities

2.Patient/Employee Data Capture – Enterprise-Wide

3.Strong Sales/Account Management and Customer Service

51

Weight Watchers Health Solutions: The Team

Executive Role Background Start Date

Colin Watts President Johnson & Johnson, Walgreens, Campbells,

Nabisco

1/2012

Heidi Bowman VP, Operations &

Healthcare Strategy

Medco (Express Scripts), Schering-Plough

(Merck)

9/2012

Peter Dunphy VP,

Commercialization

ActiveHealth, Aetna, Quest Diagnostic,

Best Doctors

9/2013

Susan

Fanciullo

National Sales

Director

Wellpoint, Anthem BCBS, UHC 4/2013

Cecile Johnson Senior Director,

Client Operations

Medco, US Homecare, WellChoice 1/2013

Key dedicated WWHS executives:

Complemented by strong cross-functional members in key areas

52

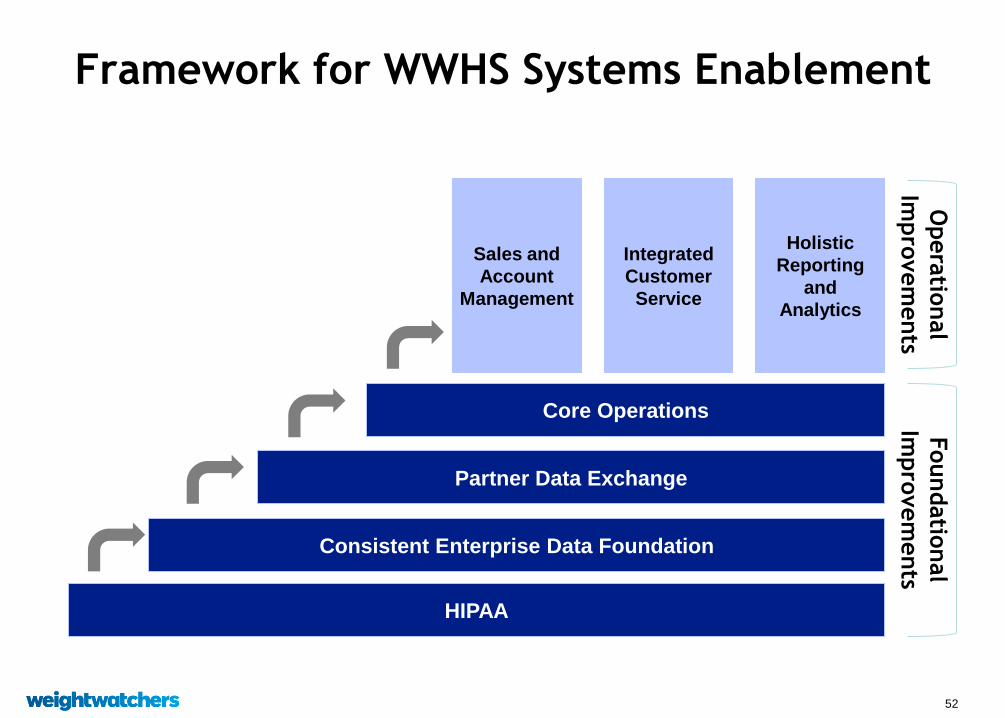

Framework for WWHS Systems Enablement

HIPAA

Foundatio

nal

Impro

vem

ents

Consistent Enterprise Data Foundation

Partner Data Exchange

Core Operations

Holistic

Reporting

and

Analytics

Integrated

Customer

Service

Sales and

Account

Management

Opera

tional

Impro

vem

ents

53

Strengthen HIPAA Compliance Key Areas of Focus

People

Process

Privacy Capabilities

&

HIPAA Controls

People Stream

Responsible for remediation efforts

related to training and awareness,

communication, policy development,

governance

Process Stream

Responsible for standard operating

procedures, vendor management, surveys,

monitoring, retention, and hardcopy PHI

Technology

Technology Stream

Responsible for information security,

websites, applications and systems,

tools, and electronic PHI

54

Bringing together the meeting & digital experiences into the hands of our service providers

– A technology platform for meeting room automation: healthcare data capture, better member experience

– Ensure “single-member view” across all key Weight Watchers channels with HIPAA compliance

– Deploy hardware solution that can be used in all types of meetings (traveler, @work, stores)

500 Champ-units deployed at @work locations in 2013 to capture key requirements

Preparing for Phase II pilot of new units and begin deployment in our US meeting rooms in 2014/2015

Data capture: next generation of meeting room technology

2013 2014

Q4 Q1 Q2 Q3 Q4

Tech architecture

definition

Prototype

Pilot

Product Discovery

Delivery POC

Begin national deployment

Product Discovery

Delivery

55

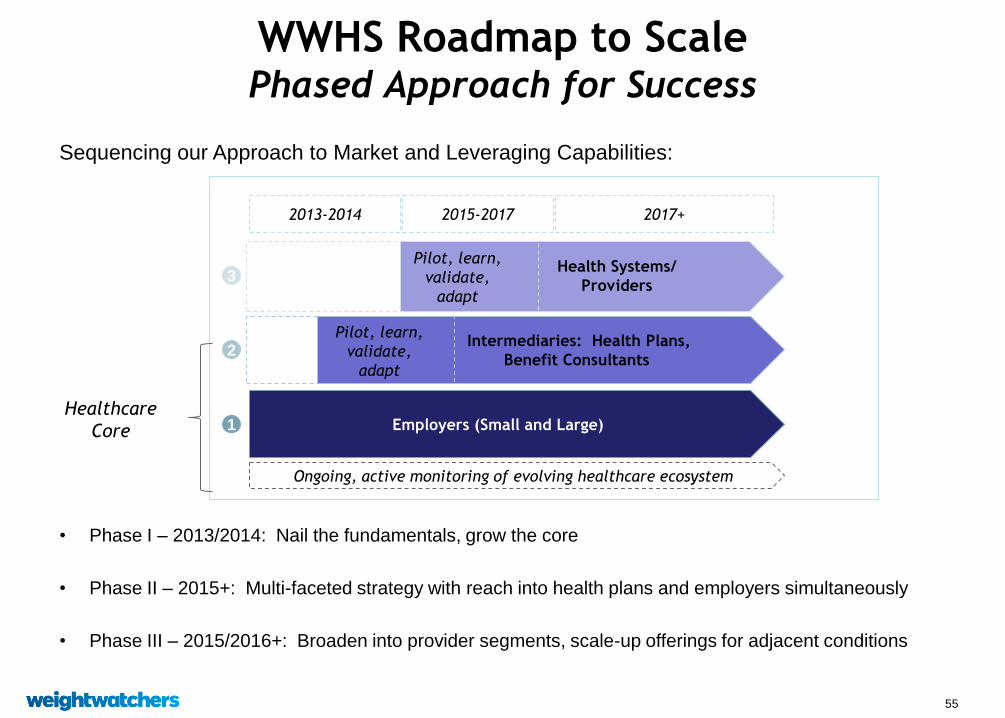

WWHS Roadmap to Scale Phased Approach for Success

Sequencing our Approach to Market and Leveraging Capabilities:

• Phase I – 2013/2014: Nail the fundamentals, grow the core

• Phase II – 2015+: Multi-faceted strategy with reach into health plans and employers simultaneously

• Phase III – 2015/2016+: Broaden into provider segments, scale-up offerings for adjacent conditions

Ongoing, active monitoring of evolving healthcare ecosystem

Employers (Small and Large) 1

Intermediaries: Health Plans,

Benefit Consultants 2

Health Systems/

Providers

Pilot, learn,

validate,

adapt

3

2013-2014 2015-2017 2017+

Healthcare

Core

Pilot, learn,

validate,

adapt

56

Select WWHS Relationships

Employers Health Plans Providers

57

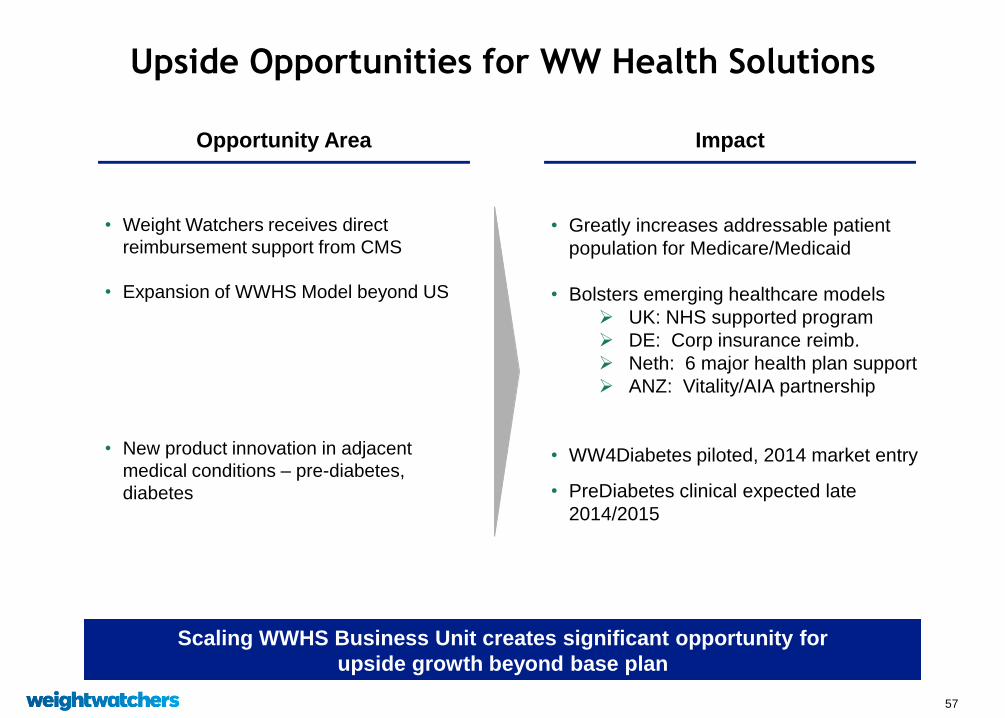

Upside Opportunities for WW Health Solutions

Opportunity Area

• Weight Watchers receives direct

reimbursement support from CMS

• Expansion of WWHS Model beyond US

• New product innovation in adjacent

medical conditions – pre-diabetes,

diabetes

Impact

• Greatly increases addressable patient

population for Medicare/Medicaid

• Bolsters emerging healthcare models

UK: NHS supported program

DE: Corp insurance reimb.

Neth: 6 major health plan support

ANZ: Vitality/AIA partnership

• WW4Diabetes piloted, 2014 market entry

• PreDiabetes clinical expected late

2014/2015

Scaling WWHS Business Unit creates significant opportunity for

upside growth beyond base plan

58

Objectives (Agenda)

• Share our situation assessment

• Outline our strategic agenda

Pillar 1: Drive immediate performance improvement

Pillar 2: Re-imagine the core offering

Pillar 3: Grow the healthcare business

Pillar 4: Strengthen the organization

• Discuss financial aspirations and business model

59

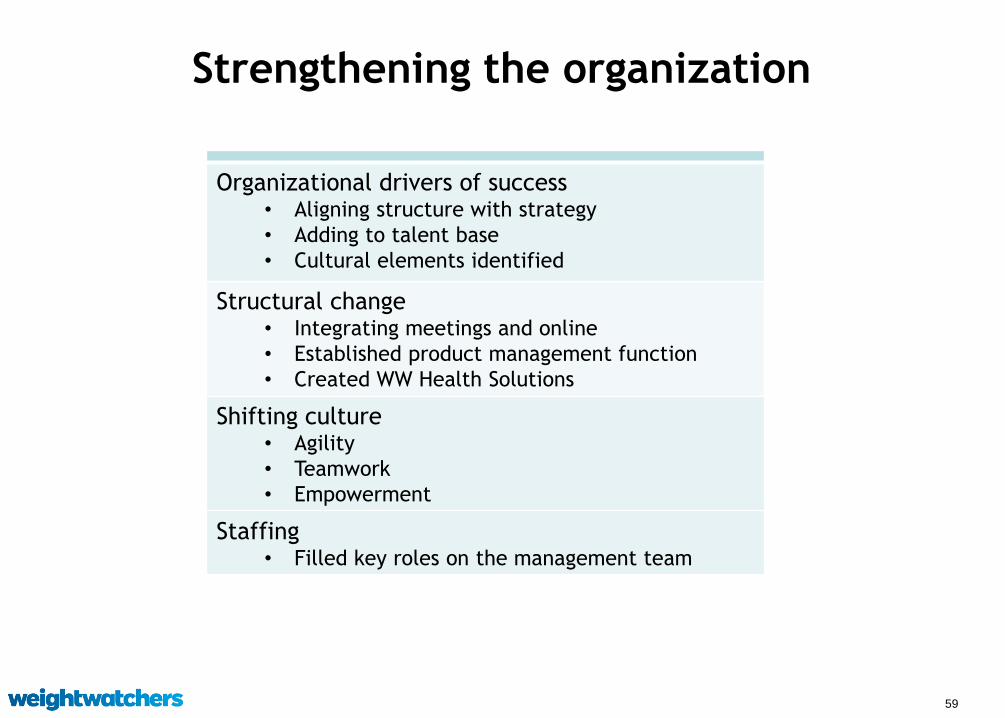

Organizational drivers of success • Aligning structure with strategy

• Adding to talent base

• Cultural elements identified

Structural change • Integrating meetings and online

• Established product management function

• Created WW Health Solutions

Shifting culture • Agility

• Teamwork

• Empowerment

Staffing • Filled key roles on the management team

Strengthening the organization

60

Objectives (Agenda)

• Share our situation assessment

• Outline our strategic agenda

Pillar 1: Drive immediate performance improvement

Pillar 2: Re-imagine the core offering

Pillar 3: Grow the healthcare business

Pillar 4: Strengthen the organization

• Discuss financial aspirations and business model

61

Financial aspirations

• Multi-year transformation

Path to recovery likely not linear

– 2014 challenging year

• Five-year aspiration: $2B+ in revenues by 2018

Revenue growth not expected in 2014

Expect to see positive recruitment trends in 2015 benefitting from strategic initiatives, but

revenue growth may not be until FY2016 and beyond

• Transformation will reinvent B2C which will remain biggest part of business for foreseeable

future, though B2B increasingly important

B2C returns to growth after reinvigorating core initiatives implemented

B2B expected to represent 15-25% or $300-500M by 2018

• Targeting 2013-2015 annualized gross cost savings of $150M

$90M achieved to date

• Manage margins so earnings grow faster than sales

• Clear capital priorities: Fund the business and reduce debt towards approximately 3X

leverage

62

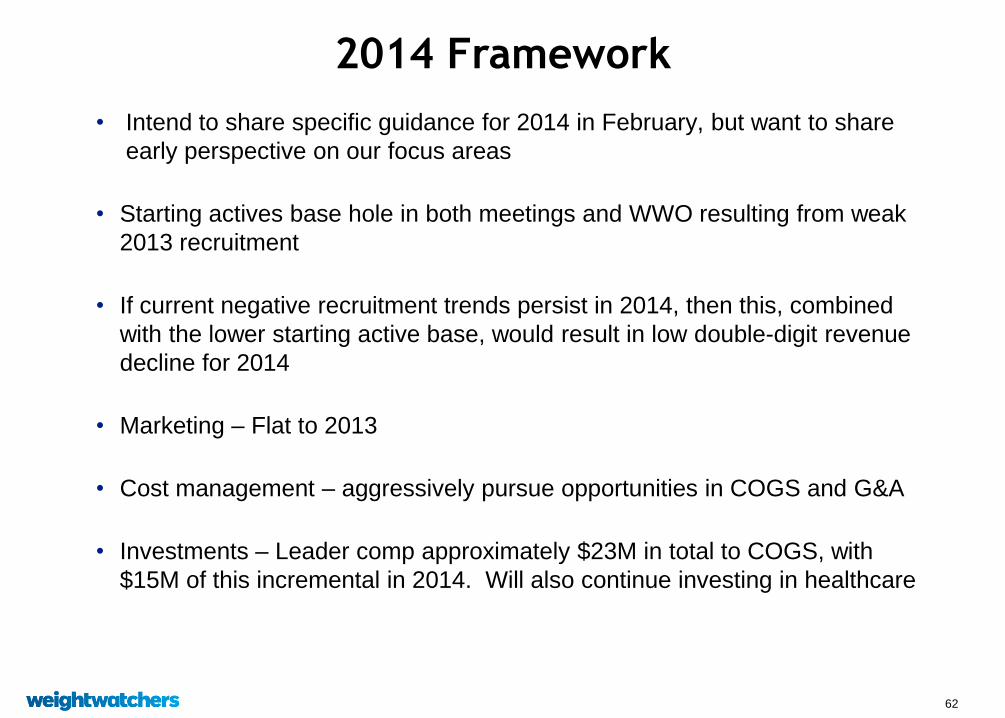

2014 Framework

• Intend to share specific guidance for 2014 in February, but want to share

early perspective on our focus areas

• Starting actives base hole in both meetings and WWO resulting from weak

2013 recruitment

• If current negative recruitment trends persist in 2014, then this, combined

with the lower starting active base, would result in low double-digit revenue

decline for 2014

• Marketing – Flat to 2013

• Cost management – aggressively pursue opportunities in COGS and G&A

• Investments – Leader comp approximately $23M in total to COGS, with

$15M of this incremental in 2014. Will also continue investing in healthcare

63

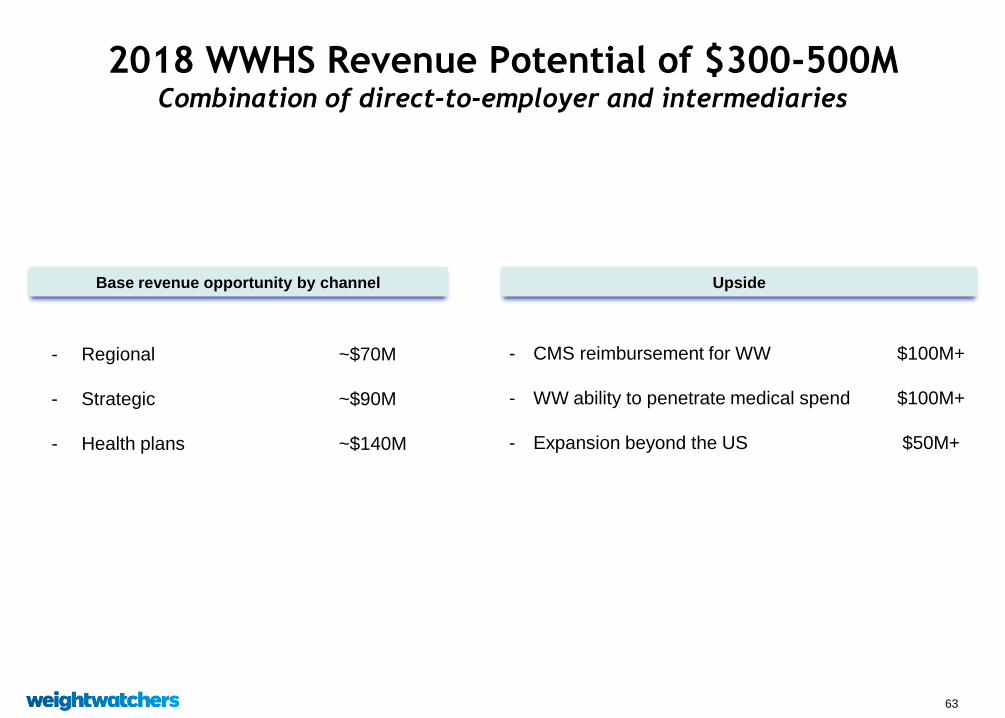

2018 WWHS Revenue Potential of $300-500M Combination of direct-to-employer and intermediaries

Base revenue opportunity by channel

- CMS reimbursement for WW $100M+

- WW ability to penetrate medical spend $100M+

- Expansion beyond the US $50M+

Upside

- Regional ~$70M

- Strategic ~$90M

- Health plans ~$140M

64

Targeting $150M gross annualized savings run rate

over 2013-15

• On track to deliver ~$90M gross annualized savings from FY13 initiatives ~$60M Marketing

~$30M G&A and COGS

• Targeting incremental $60M beyond wave 1

• Further marketing cuts not expected in 2014; expected to be flat on $ basis Will continue to evaluate mix and productivity

• Savings will come from G&A and COGS; committed to right-sizing

business and improving meetings margin

• Cost savings will more than fund investments

65

Notes:

See Appendix for a reconciliation of non-GAAP financial measures to the most comparable GAAP measures.

-2008 Revenue & Gross Profit M argin exclude negative impact of UK VAT ruling of $18.7M related to prior years.

-2009 Gross Profit M argin excludes impact of UK Self-employment ruling of $32.5M (pretax) related to prior years.

-2010 Revenue & Gross Profit M argin exclude the benefit of a $2.0M increase in revenues for the reversal of an over-accrual related to the UK VAT ruling .

-2012 Gross Profit M argin excludes the benefit of a $14.5 million over-accrual reversal associated with the UK Self-employment ruling.

Consolidated Revenue + Gross Profit Margin

1,555

1,399

1,819 1,827

1,450

54.9%

57.6%

57.5%

54.4%

58.5%

54.4%

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2008 2009 2010 2011 2012 2013E

52.0%

53.0%

54.0%

55.0%

56.0%

57.0%

58.0%

59.0%

Global Revenue

GM %

Overall Gross Margin Trend

in $Ms

*

*Based on expectations that Q4 2013 global revenue down low double digits versus the prior year period and 2013 full-year total-company gross margin will be down 100bps versus the prior year.

66

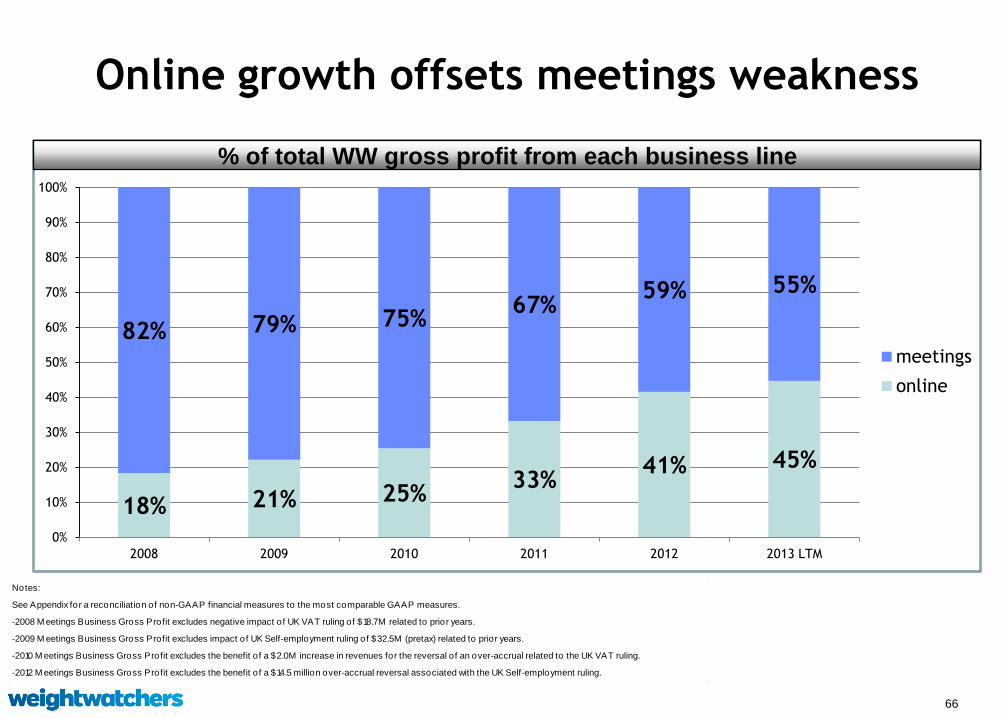

Online growth offsets meetings weakness

18% 21% 25% 33%

41% 45%

82% 79% 75% 67%

59% 55%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 LTM

meetings

online

% of total WW gross profit from each business line

Notes:

See Appendix for a reconciliation of non-GAAP financial measures to the most comparable GAAP measures.

-2008 M eetings Business Gross Profit excludes negative impact of UK VAT ruling of $18.7M related to prior years.

-2009 M eetings Business Gross Profit excludes impact of UK Self-employment ruling of $32.5M (pretax) related to prior years.

-2010 M eetings Business Gross Profit excludes the benefit of a $2.0M increase in revenues for the reversal of an over-accrual related to the UK VAT ruling.

-2012 M eetings Business Gross Profit excludes the benefit of a $14.5 million over-accrual reversal associated with the UK Self-employment ruling.

67

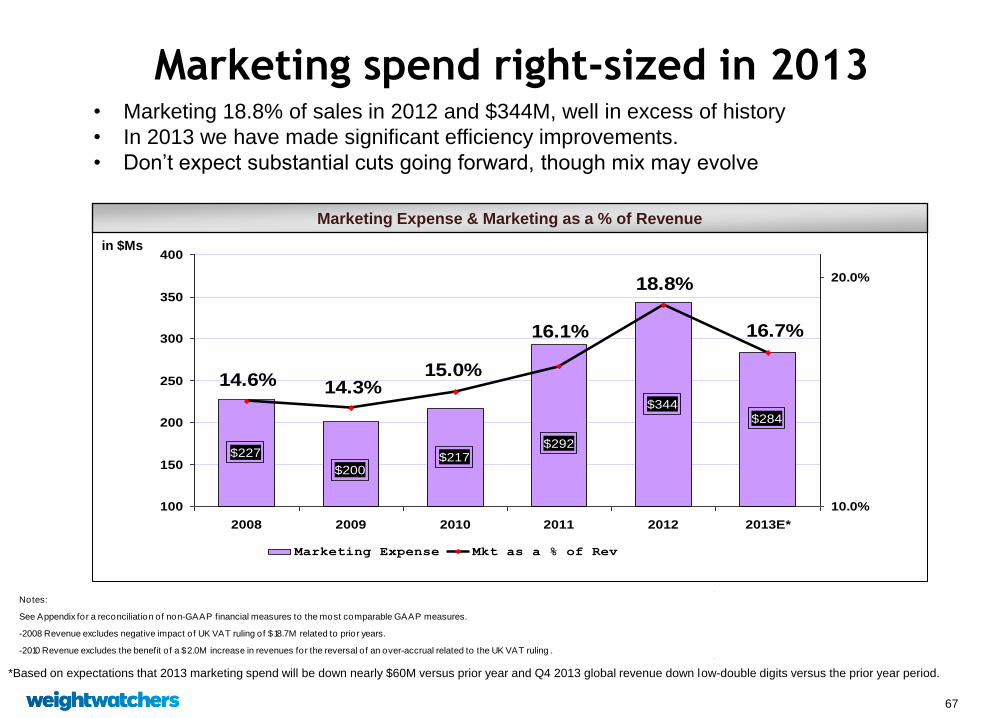

Marketing spend right-sized in 2013

$227 $217

$344

$284

$200

$292

14.6%

16.1%

15.0%14.3%

16.7%

18.8%

100

150

200

250

300

350

400

2008 2009 2010 2011 2012 2013E*

10.0%

20.0%

Marketing Expense Mkt as a % of Rev

in $Ms

Marketing Expense & Marketing as a % of Revenue

• Marketing 18.8% of sales in 2012 and $344M, well in excess of history

• In 2013 we have made significant efficiency improvements.

• Don’t expect substantial cuts going forward, though mix may evolve

*Based on expectations that 2013 marketing spend will be down nearly $60M versus prior year and Q4 2013 global revenue down low-double digits versus the prior year period.

Notes:

See Appendix for a reconciliation of non-GAAP financial measures to the most comparable GAAP measures.

-2008 Revenue excludes negative impact of UK VAT ruling of $18.7M related to prior years.

-2010 Revenue excludes the benefit of a $2.0M increase in revenues for the reversal of an over-accrual related to the UK VAT ruling .

68

Notes:

See Appendix for a reconciliation of non-GAAP financial measures to the most comparable GAAP measures.

-2008 Revenue excludes negative impact of UK VAT ruling of $18.7M related to prior years.

-2010 Revenue excludes the benefit of a $2.0M increase in revenues for the reversal of an over-accrual related to the UK VAT ruling .

$182 $183

$228

$238

$171$208

11.7% 11.5%

12.6%12.2%

14.0%

12.5%

100

120

140

160

180

200

220

240

260

280

2008 2009 2010 2011 2012 2013E*

10.0%

G&A Expense G&A as a % of Rev

G&A has increased

in $Ms G&A Expense & G&A as a % of Revenue

• G&A has ballooned relative to sales over the past several years

• Some warranted for growth investments, e.g., healthcare

• Some initial success and several opportunities for further cost action

in $M’s

*Based on expectations that 2013 G&A spend will be up no more than $10M versus the prior year and Q4 2013 global revenue down low-double digits versus the prior year period.

15.0%

69

6%

20%

13%

10% 4%

46%

2013E

B2B

Other Tech

Tech Prof Fees

Non-Tech Prof Fees

Other G&A

Salaries & Benefits

2013 mix shift in G&A driven by investments

in tech and Healthcare

0.5%

19%

6%

7%

16%

52%

2009

Note: % based on unallocated G&A; portion of technology costs are allocated to online COS

Healthcare

70

Professional Fees ~$100M

Big opportunity as they are not only in G&A

Professional fee mix % total

53%

20%

26%

G&A

COGS

Marketing

Note: Total is not 100% due to rounding

71

Cash flow priorities

• Fund the business

• Pay down debt

• Make selective acquisitions

72

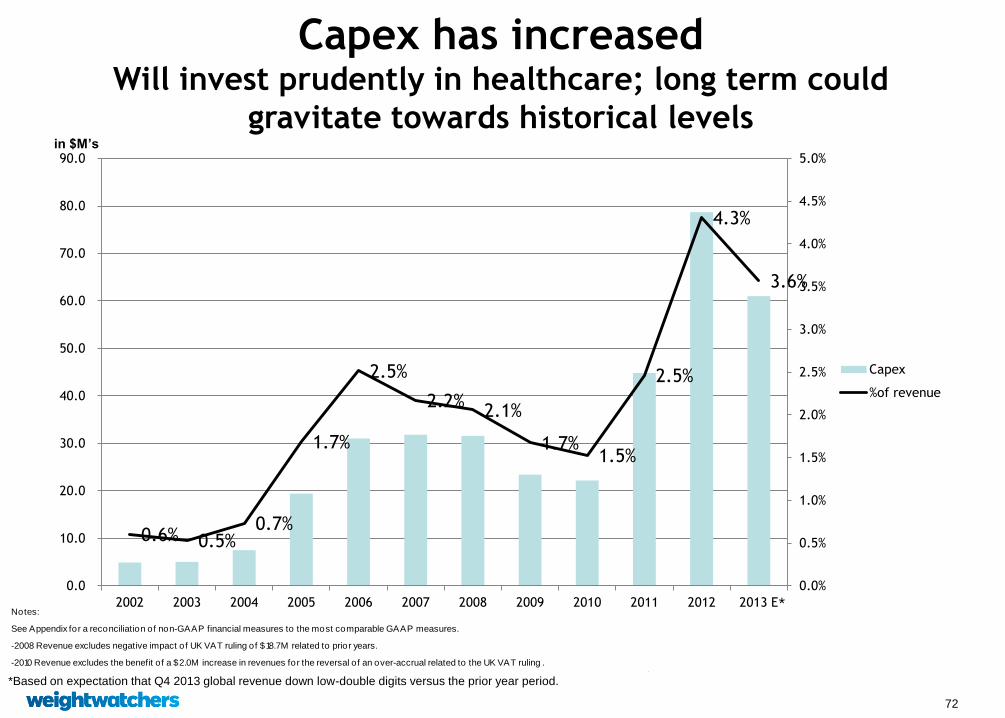

Capex has increased Will invest prudently in healthcare; long term could

gravitate towards historical levels in $M’s

Notes:

See Appendix for a reconciliation of non-GAAP financial measures to the most comparable GAAP measures.

-2008 Revenue excludes negative impact of UK VAT ruling of $18.7M related to prior years.

-2010 Revenue excludes the benefit of a $2.0M increase in revenues for the reversal of an over-accrual related to the UK VAT ruling .

0.6% 0.5% 0.7%

1.7%

2.5%

2.2% 2.1%

1.7% 1.5%

2.5%

4.3%

3.6%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 E

Capex

%of revenue

*

*Based on expectation that Q4 2013 global revenue down low-double digits versus the prior year period.

73

Debt reduction is a clear priority

2.0x

3.4x 3.3x 3.2x

3.1x

1.7x

4.3x 4.2x

~3x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

5.0x

0

500

1000

1500

2000

2500

2006 2007 2008 2009 2010 2011 2012 3Q13 2018E

Net Debt

Net Debt/EBITDAS

in $Ms

See Appendix for a reconciliation of non-GAAP financial measures to the most comparable GAAP measures.

-2008 EBITDAS excludes negative impact of UK VAT ruling of $18.7M related to prior years.

-2009 EBITDAS excludes impact of UK Self-employment ruling of $32.5M (pretax) related to prior years. EBITDAS also excludes restructuring charges of $5.5M.

-2010 EBITDAS excludes the benefit of a $2.0M increase in revenues for the reversal of an over-accrual related to the UK VAT ruling.

-2012 EBITDAS excludes the benefit of a $14.5 million over-accrual reversal associated with the UK Self-employment ruling.

EBITDAS = earnings before interest, taxes, depreciation, amortization, and stock-based compensation expense.

Target

74

Effective Q1 2014, revising operating structure Full P&L accountability is being rolled into the geographies: our WW.com

business will no longer be a separate business unit

Implications for reporting:

• No change in income statement in earnings press release financials

• Commitment to sharing volume and revenue for Online

May re-evaluate when hybrid model is fully in place

• Will still report meetings COGS and cost of Internet revenues on a

consolidated basis

• Will report segment profitability for regions

Intend to provide revised historical segment geographic

data before reporting Q1 2014

75

We are committed to an open dialogue and

sharing of milestones

• In addition to continued reporting of paid weeks (our best volume

metric), we’re introducing the total active member base (Monthly Pass

+ WWO) quarterly

In combination, they provide good visibility into our progress

• On a periodic basis, we will update other metrics that we shared today

• We will also share WWHS progress

76

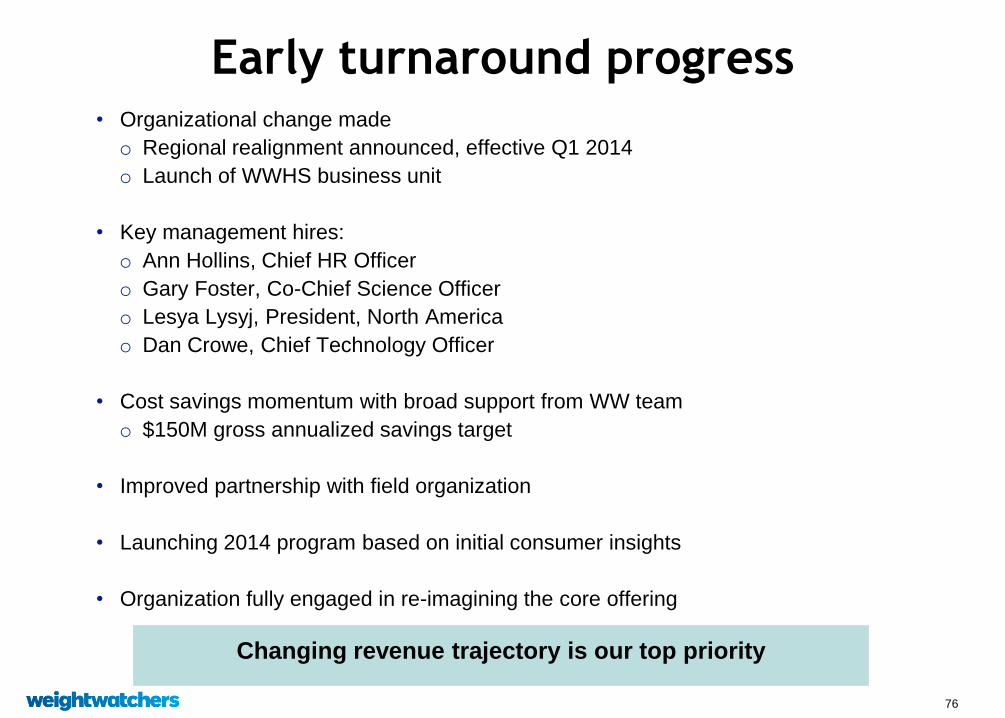

Early turnaround progress • Organizational change made

o Regional realignment announced, effective Q1 2014

o Launch of WWHS business unit

• Key management hires:

o Ann Hollins, Chief HR Officer

o Gary Foster, Co-Chief Science Officer

o Lesya Lysyj, President, North America

o Dan Crowe, Chief Technology Officer

• Cost savings momentum with broad support from WW team

o $150M gross annualized savings target

• Improved partnership with field organization

• Launching 2014 program based on initial consumer insights

• Organization fully engaged in re-imagining the core offering

Changing revenue trajectory is our top priority

77

Investment thesis

• Seasoned management team driving a multi-year transformation

o Realistic about the environment

o Sense of urgency

• Clear pathway to rejuvenated B2C business

• Mobilizing resources to accelerate healthcare growth

• Aggressive cost structure management

• Debt pay-down is a priority

Successful execution yields $2B+ revenue by

2018 with earnings growing faster than sales

78

Appendix – Non-GAAP Reconciliations

79

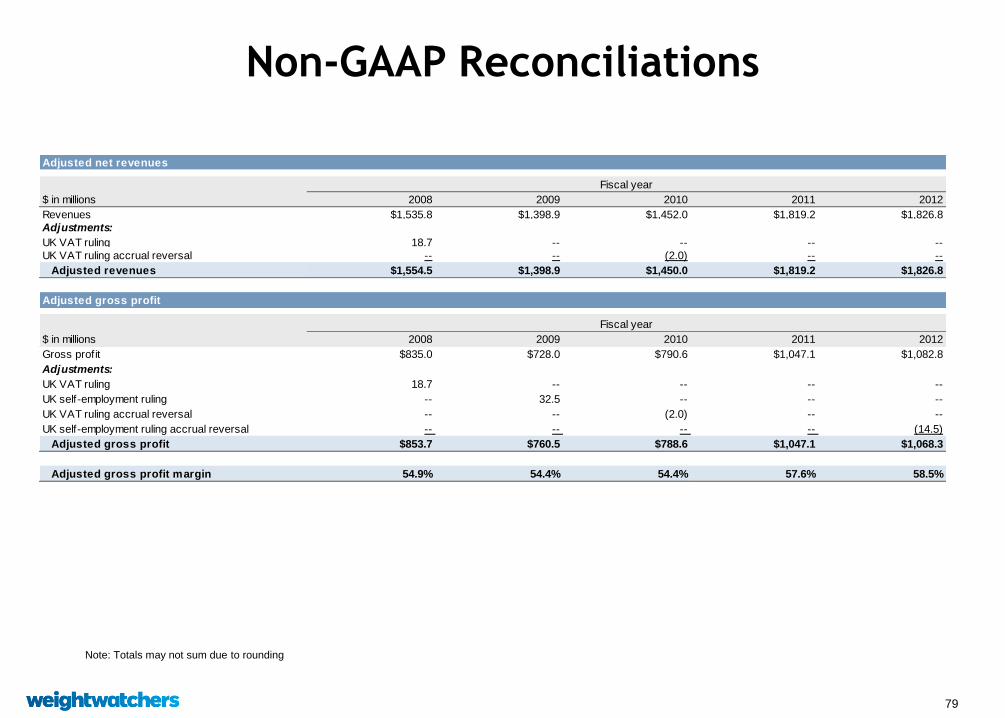

Non-GAAP Reconciliations

Note: Totals may not sum due to rounding

Adjusted net revenues

Fiscal year

$ in millions 2008 2009 2010 2011 2012

Revenues $1,535.8 $1,398.9 $1,452.0 $1,819.2 $1,826.8

Adjustments:

UK VAT ruling 18.7 -- -- -- --

UK VAT ruling accrual reversal -- -- (2.0) -- --

Adjusted revenues $1,554.5 $1,398.9 $1,450.0 $1,819.2 $1,826.8

Adjusted gross profit

Fiscal year

$ in millions 2008 2009 2010 2011 2012

Gross profit $835.0 $728.0 $790.6 $1,047.1 $1,082.8

Adjustments:

UK VAT ruling 18.7 -- -- -- --

UK self-employment ruling -- 32.5 -- -- --

UK VAT ruling accrual reversal -- -- (2.0) -- --

UK self-employment ruling accrual reversal -- -- -- -- (14.5)

Adjusted gross profit $853.7 $760.5 $788.6 $1,047.1 $1,068.3

Adjusted gross profit margin 54.9% 54.4% 54.4% 57.6% 58.5%

80

Non-GAAP Reconciliations (continued)

Note: Totals may not sum due to rounding

Adjusted operating income

Fiscal year

$ in millions 2008 2009 2010 2011 2012

Operating income $425.0 $356.7 $390.3 $546.3 $510.8

Adjustments:

UK VAT ruling 18.7 -- -- -- --

Restructuring -- 5.5 -- -- --

UK self-employment ruling -- 32.5 -- -- --

UK VAT ruling accrual reversal -- -- (2.0) -- --

UK self-employment ruling accrual reversal -- -- -- -- (14.5)

Adjusted operating income $443.7 $394.7 $388.3 $546.3 $496.3

Adjusted EBITDAS

$ in millions 2006 2007 2008 2009 2010 2011 2012 3Q 2013

Net Income $209.8 $201.2 $204.3 $177.3 $194.2 $304.9 $257.4 $231.9

Interest 49.5 109.3 92.7 66.7 76.2 59.9 90.5 106.7

Taxes 120.8 125.3 132.0 115.6 120.7 178.7 159.5 143.6

EBIT $380.1 $435.8 $429.0 $359.6 $391.1 $543.5 $507.4 $482.2

Depreciation and amortization 13.4 19.0 24.5 27.9 29.0 31.0 36.6 43.1

Stock-based compensation 11.8 11.8 11.3 8.8 8.6 9.1 8.8 5.5

EBITDAS $405.3 $466.6 $464.8 $396.3 $428.7 $583.6 $552.8 $530.7

Adjustments:

UK VAT ruling -- -- 18.7 -- -- -- -- --

Restructuring -- -- -- 5.5 -- -- -- --

UK self-employment ruling -- -- -- 32.5 -- -- -- --

UK VAT ruling accrual reversal -- -- -- -- (2.0) -- -- --

UK self-employment ruling accrual reversal -- -- -- -- -- -- (14.5) 0.0

Adjusted EBITDAS $405.3 $466.6 $483.5 $434.3 $426.7 $583.6 $538.3 $530.7

Cash and cash equivalents $37.5 $39.8 $47.3 $48.7 $43.3 $53.2 $70.2 $181.3

Total debt 849.2 1,648.1 1,647.5 1,453.0 1,365.1 1,051.8 2,406.4 2,394.0

Net debt / Adjusted EBITDAS 2.0 X 3.4 X 3.3 X 3.2 X 3.1 X 1.7 X 4.3 X 4.2 X

Fiscal year

81

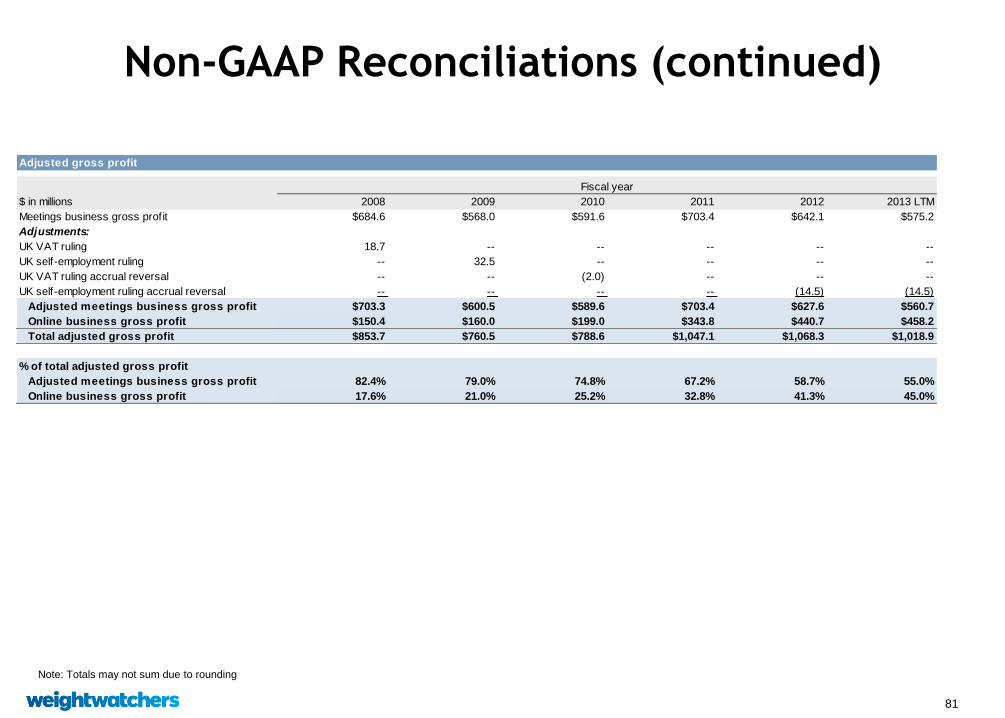

Non-GAAP Reconciliations (continued)

Note: Totals may not sum due to rounding

Adjusted gross profit

Fiscal year

$ in millions 2008 2009 2010 2011 2012 2013 LTM

Meetings business gross profit $684.6 $568.0 $591.6 $703.4 $642.1 $575.2

Adjustments:

UK VAT ruling 18.7 -- -- -- -- --

UK self-employment ruling -- 32.5 -- -- -- --

UK VAT ruling accrual reversal -- -- (2.0) -- -- --

UK self-employment ruling accrual reversal -- -- -- -- (14.5) (14.5)

Adjusted meetings business gross profit $703.3 $600.5 $589.6 $703.4 $627.6 $560.7

Online business gross profit $150.4 $160.0 $199.0 $343.8 $440.7 $458.2

Total adjusted gross profit $853.7 $760.5 $788.6 $1,047.1 $1,068.3 $1,018.9

% of total adjusted gross profit

Adjusted meetings business gross profit 82.4% 79.0% 74.8% 67.2% 58.7% 55.0%

Online business gross profit 17.6% 21.0% 25.2% 32.8% 41.3% 45.0%