3

Holland FinTech Meet Up 13 March 2015 Martijn Berghuijs Robert van Altena

| Date post: | 17-Jul-2015 |

| Category: |

Economy & Finance |

| Upload: | holland-fintech |

| View: | 81 times |

| Download: | 4 times |

Holland FinTech Meet Up 13 March 2015

Martijn Berghuijs Robert van Altena

2 © [year] [legal member firm name], registered with the trade register in [country] under number [number], is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved. Printed in [country]. The KPMG name, logo and ‘cutting through complexity’ are registered trademarks of KPMG International.

Understanding the Regulatory Life Cycle

Phase

■ Identify developments (through external and internal networks)

■ Lobby actively

■ Assess impact of (new) regulation in terms of business, processes, systems, people, reporting & monitoring.

■ Cluster regulation into Compliance Themes

■ Set up implementation project ■ If applicable, obtain regulatory approval or licenses ■ Update processes, systems and procedures

Public debate Promulgation of rules Implementation Maintenance

■ Monitor & review compliance with regulation

UN

CER

TAIN

TY

Time

Activity

Compliance costs

Strategic (“game changing”)

EMIR

DGS

Solvency ll

Wft (Bankers’ oath/ suitability test)

Telco Law BRRD

Wbfo

EU Privacy Regulation (data leackages)/ Wbp

Dodd-Frank incl Volcker rule

FATCA

Pension Law (Witteveen)/ FTK

Basel lll

FSB: Insurer Recovery and Resolution Plans (incl bail-in)

FSB: Industry funded policy holder protection schemes

IAIS: Basic Capital Requirements (incl HLA)

IASB: IFRS 9, IFRS 4 Phase II FS European Rulebook/

Group Supervision

US: Social Media Regulations

US: Cloud Security & Risk Standards

PRIPs

IMD2

BGFO

MiFID2

UCITS VI

EU Privacy Regulation

Mass claims

IAIS: ComFrame

PSD2

AML IV

EMD

Kredietunie

3 © [year] [legal member firm name], registered with the trade register in [country] under number [number], is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved. Printed in [country]. The KPMG name, logo and ‘cutting through complexity’ are registered trademarks of KPMG International.

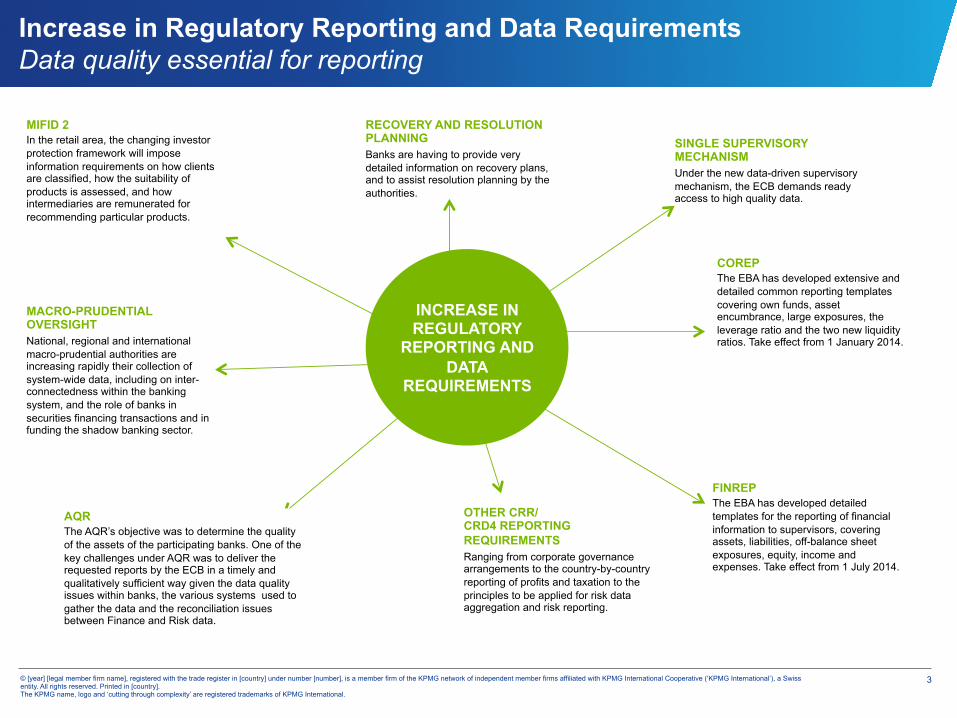

Increase in Regulatory Reporting and Data Requirements Data quality essential for reporting

MIFID 2 In the retail area, the changing investor protection framework will impose information requirements on how clients are classified, how the suitability of products is assessed, and how intermediaries are remunerated for recommending particular products.

MACRO-PRUDENTIAL OVERSIGHT National, regional and international macro-prudential authorities are increasing rapidly their collection of system-wide data, including on inter-connectedness within the banking system, and the role of banks in securities financing transactions and in funding the shadow banking sector.

OTHER CRR/ CRD4 REPORTING REQUIREMENTS Ranging from corporate governance arrangements to the country-by-country reporting of profits and taxation to the principles to be applied for risk data aggregation and risk reporting.

FINREP The EBA has developed detailed templates for the reporting of financial information to supervisors, covering assets, liabilities, off-balance sheet exposures, equity, income and expenses. Take effect from 1 July 2014.

COREP The EBA has developed extensive and detailed common reporting templates covering own funds, asset encumbrance, large exposures, the leverage ratio and the two new liquidity ratios. Take effect from 1 January 2014.

SINGLE SUPERVISORY MECHANISM Under the new data-driven supervisory mechanism, the ECB demands ready access to high quality data.

RECOVERY AND RESOLUTION PLANNING Banks are having to provide very detailed information on recovery plans, and to assist resolution planning by the authorities.

INCREASE IN REGULATORY

REPORTING AND DATA

REQUIREMENTS

AQR The AQR’s objective was to determine the quality of the assets of the participating banks. One of the key challenges under AQR was to deliver the requested reports by the ECB in a timely and qualitatively sufficient way given the data quality issues within banks, the various systems used to gather the data and the reconciliation issues between Finance and Risk data.