ADB SME DEVELOPMENT TA BACKGROUND REPORT SME CONSTRAINTS IN TAXATION SYSTEM (SYNOPSIS, FINDINGS, RECOMMENDATIONS) KAI HAUERSTEIN, FRANK NIEMANN MAY 2002 Published by: ADB Technical Assistance SME Development State Ministry for Cooperatives & SME Jalan H.R. Rasuna Said Kav.3 Jakarta 12940 Tel: ++62 21 520 15 40 Fax: ++62 21 527 94 82 e-mail: [email protected]

Transcript

ADB SME DEVELOPMENT TA

BACKGROUND REPORT

SME CONSTRAINTS IN TAXATION SYSTEM (SYNOPSIS, FINDINGS, RECOMMENDATIONS)

3.2 GENERAL OBSERVATIONS ON THE INCOME TAX LAW .................................41

3.3 SPECIFIC OBSERVATION ON INCOME TAX: SME´S OPERATING AS SOLE TRADERS PAY LESS INCOME TAX THAN CORPORATIONS ...............43

3.4 GENERAL OBSERVATION ON THE VAT AND SALES TAX ON LUXURY GOODS LAW ........................................................................................................44

3.6 LOW TAX COMPLIANCE AND KNOWLEDGE.....................................................45

3.7 OBSERVATIONS ON GENERAL RULES AND PROCEDURES..........................47

4 AGENDA FOR RECOMMENDATIONS ................................................................48

4.1 RECOMMENDATIONS TO PREPARE THE GROUND FOR TAX POLICY IMPROVEMENTS..................................................................................................48

4.2 RECOMMENDATIONS TO IMPROVE THE IMPACT AND AWARENESS OF INCOME TAX ........................................................................................................48

4.3 RECOMMENDATIONS TO INCLUDE SME IN THE VAT SYSTEM......................49

ADB SME DEVELOPMENTTA

IV

II. TABLE OF ABBREVIATIONS

ADB Asian Development Bank

BPKP State Audit Authority

CV Commanditair vennotschap = Limited partnership

DGT Directorate General for Taxes

GR Government Regulation

IPEDA Iuran Pembangunan Daerah = Local Wealth Tax

JDP Jenderal Directorate Pajak

PND Perusahan Non Directori

PPh Pajak Perhasilan = Income Tax Law

PPN Pajak Pertambahan Nilai Barang

PPnBM Pajak Penjualan atas Barang Mewah

PT PerseroanTerbatas = Limited liability company

SME Small and Medium Enterprise

TA Technical Assistance

TKUdTCP Tentang Kententuan Umum Dan Tata Cara Perpajakan = Law on General Rules and Procedures of Taxation

URT Usaha Rumah Tangga

UU Undang Undang = Law

VAT Value Added Tax

ADB SME DEVELOPMENTTA

V

III. TABLE OF FIGURES

Figure 1: Depreciation methods and rates according to Article 11 PPh......................10 Figure 2: Tax Tariffs Before and After the 2000 Tax Reform ......................................13 Figure 3: Income Tax Payable by Individual Tax Payers, Before and After the Tax Reform 2000.................................................................................................14 Figure 4: Income Tax Payable by Corporate Tax Payers, Before and After the Tax Reform 2000................................................................................................15 Figure 5: Overview Withholding Taxes........................................................................18 Figure 6: Other services subject to PPH 23 Withholding Tax and their respective Tax Rates ....................................................................................................20 Figure 7: Examples of VAT exempted goods/services................................................22 Figure 8: Luxury Tax on Goods...................................................................................28 Figure 9: Exemptions / Incentives ...............................................................................38 Figure 10: Comparison income tax tariffs between Sole Trader and corporations ......43 Figure 11: Tax Compliance according to ADB TA Survey ............................................45 Figure 12: Income Tax Forms received between 1995-1997 ......................................46

ADB SME DEVELOPMENTTA

VI

IV. TABLE OF REFERENCES

Author Title

Anonymous Home page Directorate Genderal for Taxes (DGT) in the Ministry of Finance, http://www.pajak.go.id/profil/grafik_statistik

Anonymous 1996 Economic Census, Profile of Establishment with Legal En-tity, Badan Pusat Statistic, Jakarta, 1996

Anonymous Profil Usaha Kecil dan Menengah Tidak Berbadan Hukum, Badan Pusat Statisitk, Jakarta, 1999

Anonymous Tax Flash Vol. 04/2002, Vol.03/2002, Vol.02/2002, Vol. 08/2001, Vol. 07/2001, Vol 06/2001, Vol. 04/200, Vol. 13/2000, Price Waterhouse Coopers, Dr. Hadi Sutanto & Rekan, Jakarta, 2000, 2001, 2002.

Harvey Galper and Geoffry Walton, Bar-ents Group

Investment Tax Incentives: Recent Indonesian Experience and Options for Reform http://www.barents fiscal.or.id.

J.S. Uppal Taxation in Indonesia, Gadjah Mada University Press, 2000

ADB SME DEVELOPMENTTA

VII

V. EXECUTIVE SUMMARY ENGLISH

The specific impact of Taxation Laws on SME requires Policy Makers to take different view. Therefore, a review of SME relevant (national) Tax Laws and Regulations as well as the findings and recommendations to improve the SME friendliness of the taxation system are set out in this report.

Taxation System (Legislation and Administration) often hampers SME growth or forces them into the informal sector. Laws an regulations (legislation) effects on the cash flow through tax payments but also cause high compliance costs through formal and ad-ministrative standards like book-keeping requirements, tax self assessment, and pe-nalities. Often do those constraints not only relate to tax laws but also to bureaucratic behavior (administration). The interaction with bureaucracy is often encountered with bribes, lengthy procedures and in-transparency.

Focus of the report is the National Taxation System, covering Income Tax, Value Added Tax, Sales Tax on Luxury Goods, Tax on Transfer of Land and Building, and the Law on General Rules and Procedures of Taxation. Even though becoming in-creasingly important province and district taxes are not part of this report as well as custom taxes, retributions, and contributions.

National Tax Policy in Indonesia has undergone radical changes with three major tax reforms in the last eighteen years. The latest, in the year 2000, significantly stream-lined tax regulations and has reduced the average income tax burden for most SMEs Considering numerous exemptions for SMEs, indirect incentives, and the general availability of facilities creation of (additional) SME specific tax incentives is not re-quired.

Even though promising attempts have been undertaken to reduce formal requirements as well as administrative burden the overall tax environment is still SME unfriendly last but not least due to legal uncertainty and corrupt tax authorities.

Income Tax

In material terms the 2000 Income Tax Reform introduced a new tax rate structure reducing the tax burden for most SME. The main features of the new structure are (i) introducing separate tax tariffs for individual and corporate taxpayers, (ii) reducing tax rates for lower income brackets, (iii) increasing the top tax rate for individual taxpayers from 30% to 35%. In combination with the increase in tax free allowances for individual taxpayers, the reform has significantly reduced the tax burden of low and middle-income taxpayers.

ADB SME DEVELOPMENTTA

VIII

Tax Rate Until 2000 Tax Rate from 2001 Progression Zone (Taxable

Income in Million Rp.) Individual and Corpo-

rate Taxpayers Individual Taxpayer

Corporate Taxpayer

0-25 5% 5% 25-50 15% 10% 10%

50-100 15% 15% 100-200 25% over 200

30%

35% 30%

Tax free allowances Taxpayer Rp. 1,728,000 Rp. 2,880,000 Spouse with own income Rp. 1,728,000 Rp. 2,880,000 Spouse without own income Rp 864,000 Rp. 1,440,000 Each other dependant (max. 3) Rp 864,000 Rp. 1,440,000 Maximum Tax Free Allowance (2 earners, 3 dependants) Rp. 6,048,000

Rp. 10,080,000

The 2000 Tax Reform did not substantially alter the legal base for tax withholding and external collection. However, some withholding tax rates were increased, most relevant for SME increasing the final withholding tax rate on interest income from deposits and savings from 15% to 20%; increasing the final withholding tax rate on Rentals of Land and/or Buildings from 6% to 10%, withdrawing/ limiting the final tax of 4% on consulting income and increasing the effective withholding tax rate ( now creditable) on fees for professional services, including legal, tax, technical and management consultancy, from 6% to 7,5% of gross income; introducing a new with-holding tax for construction services.

Value Added Tax/ Sales Tax on Luxury Goods

The 2000 Tax Reform increased the threshold for those small sized companies, which can opt to be exempted from Value Added Tax from Rp 24.000.000,00 to 360,000,000.00 (goods) and 180,000,000.00 (services) and reduced the scope of VAT exempted goods and services. However numerous exemptions remain with regards to tax objects and tariffs and tax liability.

Major improvements of the formal requirements have been encountered. Under the new law all taxable enterprises can claim monthly refunds whenever (creditable inputs for a month exceed outputs). If the taxpayer satisfies certain criteria, the refund proc-ess may be even granted within seven days by making advance refund payments, i.e. prior to tax audit. Tax Reform 2000 newly provides that Commercial invoice can be used as a standard tax invoice provided sufficient detail is provided:

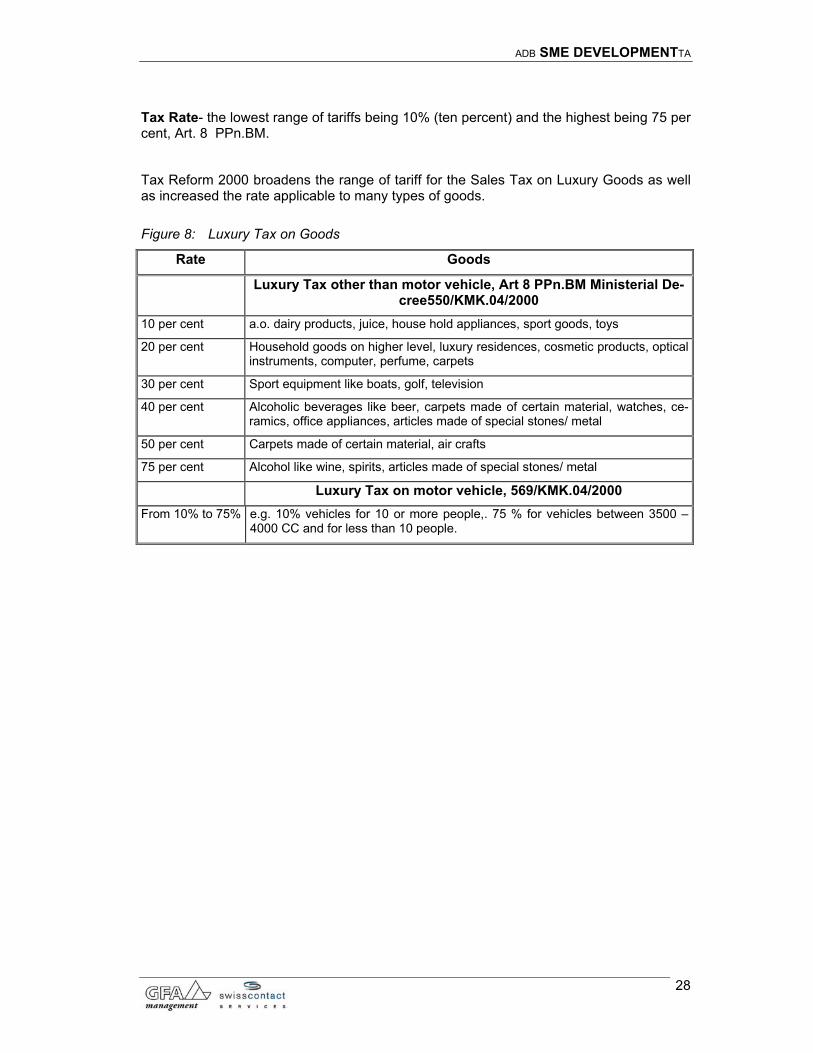

Tax Reform 2000 broadens the range of tariff for the Sales Tax on Luxury Goods as well as increased the rate applicable to many types of goods.

Tax of Transfer of Land and Building

Tax of Transfer of Land and Building was introduced in 1997. Before, only the income from the transfer of land and building was taxed (5% final withholding tax on the trans-fer value). Now, both Income Tax and Transfer of Land and Building Tax are cumula-tively due. The “new “ Law on Tax of Transfer of Land and Building (Law No. 20/2000) imposes an additional tax only on transfer of the title. To reduce the tax burden for lower income class the law provides exemptions, discounts, and reduction from tax li-ability

ADB SME DEVELOPMENTTA

IX

General Rules and Procedures of Taxation

Formal requirements set out in the General Rules and Procedures of Taxation (often specified in the respective tax laws) are often overly complicated and business un-friendly. These obligations range from requirements to (i) register, (ii) keep proper documentation (books and records, (iii) to self-assess the tax liability. The self-assessments of tax liability include requirements to file a tax returns, compute own tax liability, perform down payments.

Tax Reform 2000 eased on the one hand the administrative burden by introducing the possibility of simplified tax forms, exemptions to perform monthly instalment payments, and advance refund payments, i.e. without an obligatory audit. On the other hand im-poses heavy administrative fines or criminal charges on those, who do not comply, especially for those who fail to register. As a rule the reclaim of tax is only possible af-ter a mandatory audit has been conducted (exception see above), thus torpedoing the self-assessment scheme and increasing the interference with tax authorities.

ADB SME DEVELOPMENTTA

X

Findings

The SME Sector can draw on numerous exemptions/ indirect incentives. After the re-view of the Taxation System it seems that small/ medium sector .is part of an overall tax policy, which aims to reduce their burden through indirect incentives and exemp-tions. An overview of these exemptions/incentives is illustrated in the table below.

Exemptions/ Incen-tives

Regulation Requirement SME Eligibility

Simplification calculat-ing Net Income by us-ing Net Calculation Norm

Art 5 (1)a PPH, Art 28 (2), KUdTCP

Annual gross turnover less than Rp.600,000,000

SME Classification

Exemptions from keep-ing books and accounts

Art, 14 (2), PPH, Art 28 (2) KUdTCP

Annual gross turnover less than Rp.600,000,000

SME Classification

Exemption from filing Tax Returns

Decree Minister of Finance 535/KMK.04/2000

If net-income is not more than non-taxable income set forth in Art. 7 PPH

SMEs with losses in start-up phase

Exemptions from VAT liability

Art 1, Decree Minister of Finance, No 552/KMK.04/2000

Have to opt

Goods: gross turnover not ex-ceeding 360,000,000

Services: gross turnover not ex-ceeding 180,000,000

SME Classification

Reduced Income Tax Rate from Income re-ceived from the sale of participation/ shares in SMEs

Art 4 (2)k PPH De-cree of Minister of Finance 250/KMK.04/1995)

Venture Capital Company

Joint Venture with SME in specific sectors Not traded in stock ex-change

Net sales not more than Rp. 5 million

SME Classification

Final Tax Regime for construction remains for “Small Construction Companies”

GR No 140/2000 Contract of not more than Rp. 1 billion + certi-fies as SME

(SME entrepreneur cer-tificat)

SME Classification

Reduced tax burden through higher tax free allowance

Art 7 PPH Individual Tax Payer SME as Sole Trader

Reduced tax burden through new Progres-sion

Art 17 PPH Individual Tax Payer SME as Sole Trader

ADB SME DEVELOPMENTTA

XI

Exemptions/ Incen-tives

Regulation Requirement SME Eligibility

Reduced Income (Withholding) Tax Tariff for the income received from the transfer of capital participation

GR 4, 1995 Venture Capital Com-pany

Joint Venture with SME in specific sectors

Not traded in stock ex-change

Net sales not more than Rp. 5 million, Decree of Minister of Finance 250/KMK.04/1995)

No Income Tax due for income from dividends

Art 4 (3) PPH Dividends received from investment in joint ven-ture with SME

Net sales not more than Rp. 5 million, Decree of Minister of Finance 250/KMK.04/1995)

Non Existence of SME Definition- The table above shows that the varying definitions create confusion who should benefit from the simplifications, exemptions, and incen-tives. As a consequence SME policy may not reach the desired target group.

Foreseen direct tax incentives in the Tax System are often irrelevant for SMEs as their focus are certain business sectors and/or promoted areas.

Withholding Taxes and obligatory audits are torpedoing the (best practice) self-assessment scheme, thus increasing interaction with government and tax collectors causing bureaucratic hassle, official harassment and corruption.

SME operating as sole traders are paying less Income Tax than corporations and less than before Tax Reform 2000.

VAT exemptions may cause disadvantages for sub-contractors (linkages) and are an disincentive to conduct proper books.

VAT Law discourages SME to opt for VAT liability as no further SME tailored simplifi-cations for entering the VAT system are provided.

Lengthy and burdensome refund procedures are discouraging SME to enter the VAT System.

The Sales Tax on Luxury Goods discriminates specific sectors without considering ex-emptions for small and medium sized enterprises.

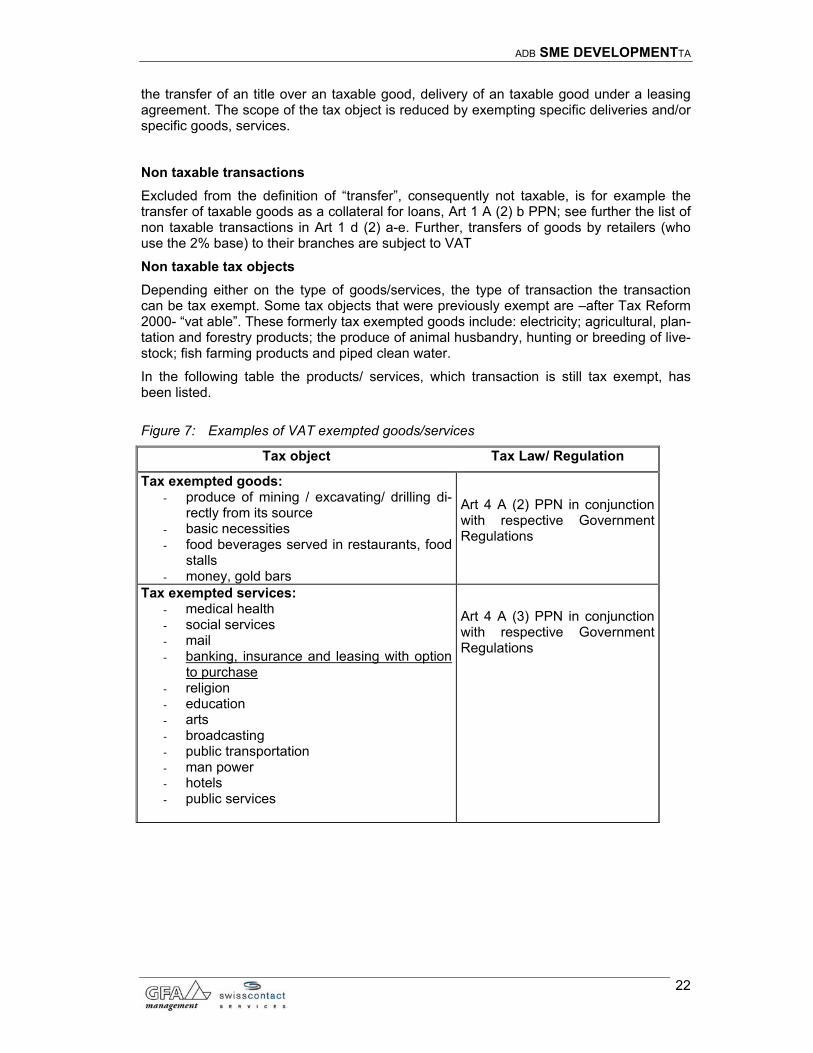

SME have to comply with complex and complicated requirements set out in various tax laws, which include: registration requirements, documentation requirements, and self-assessments requirements. These requirements are often coupled with high criminal charges making SME vulnerable for predatory tax officials.

Indonesia strives to enhance tax compliance among SME. However, in this process adequate balances have to be found between public interest to reduce tax evasion and the need for simple formal requirements in order not to place undue administrative and economic requirements on SME.

According to a quantitative survey, conducted by the ADB TA SME Development, tax compliance and knowledge among SME is relatively low.

ADB SME DEVELOPMENTTA

XII

Recommendations

Tax procedures as well as the overall administrative climate still require a thorough review. Establish a working group to review the tax regulations and procedures on SME with specific attention towards further simplification of administrative & formal re-quirements. Under participation of private stakeholders ( small and medium busi-nesses, pressure groups, tax consultants) initiate further studies with regards to the specific tax perception of SMEs e.g. corruption, tax compliance, tax knowledge, and further hampering tax regulations.

Regional autonomy has increased the taxation rights of local Governments. Therefore, the impact of local taxes requires a in depth review/ assessment. Attention should be further given to the potential to harmonize, as far as possible, administrative proce-dures, judicial supervision, and formal requirements (e.g. recording duties, calculation of tax base).

Indonesia strives to enhance tax compliance among SME. In order to improve tax compliance and bring SME back into the formal sector initiate an awareness campaign among SME to provide information on the taxation system. A user-friendly information package published in Indonesian could inform about business taxation and thus raise the understanding about the taxation system and procedures.

Indonesia still lacks a SME definition, not only in the taxation system. A unified SME definition is essential to achieve a focused SME tax policy for all taxes.

The withholding schemes, obligatory audits for tax refunds, and lengthy tax refund procedures have a negative impact on a –in principle- well balanced tax system. In general withholding schemes should be reduced and the obligatory audit be replaced by a modified verification and reconsidered as an exemption rather than a rule. As a first step small corporations should be exempted from withholding requirements and those withholding schemes, which have a negative impact on sub-contracting are to be replaced by the self-assessment scheme.

The awareness of the positive effects triggered by the Income Tax Reform has not been sufficiently enhanced. Government should make use of this positive image and send out the message that SME are the winners of the Income Tax Reform by signifi-cantly reducing their tax burden, granting them new indirect tax incentives, as well as exemptions and simplifications. It is therefore recommended to advocate this positive impact on SME.

Reconsider the general view on the practice to install monthly down payments even though tax payers are materially not liable to pay Income Tax. A shift in this practice would help to reduce the negative impact on the cash flow, especially for SME.

Currently, the majority or SME are heavily criminalized merely they do not register. To build a golden bridge to the formal sector amnesty rules for those, which did not com-ply with registration requirements because of lack of information or knowledge should be provided. Further, it is recommended to generally exclude those in the low income strata (yearly gross income of not more than Rp. 50.000.000) from all tax require-ments, also the requirement to register.

Transactions of a VAT exempted company could be generally rated zero per cent (in-stead of being tax exempt). As another option the non-collection of VAT is recom-mended. As a consequence VAT is not imposed on the transaction, while small com-panies are still allowed to credit the input tax. This in turn would create an incentive to comply with tax regulations, conducting books etc., as well as creating an incentive for a higher request for tax consulting services.

ADB SME DEVELOPMENTTA

XIII

Small enterprises could be exempted from Sales Tax purchasing one computer for business purposes.

ADB SME DEVELOPMENTTA

XIV

VI. EXECUTIVE SUMMARY BAHASA INDONESIA

Dampak khusus Undang-undang Perpajakan bagi UKM mendorong para Pembuat Kebi-jakan untuk merubah sudut pandang. Oleh karena itu laporan ini menjabarkan pengkajian Undang-undang dan Peraturan Perpajakan (nasional) yang relevan dengan UKM maupun temuan dan me-rekomendasi suatu sistim perpajakan untuk meningkatkan ke-akraban perpajakan kepada UKM.

Sistim Perpajakan (Legislasi dan Administrasi) seringkali menghambat pertumbuhan UKM atau memaksa mereka ke sektor informal. Undang-undang dan peraturan (legis-lasi) mempunyai dampak terhadap alur kas akibat pembayaran pajak akan tetapi juga menyebabkan biaya tinggi untuk memenuhi persyaratan (high compliance costs) me-lalui standardidasi administrasi yang resmi seperti kewajiban memelihara pembukuan yang rapi, menilai-sendiri pajak (tax self assessment) dan denda. Seringkali ham-batan-hambatan tersebut bukan saja terkait dengan undang-undang perpajakan tetapi juga akibat perilaku birokrasi. Interaksi dengan birokrasi seringkali berbentuk penyua-pan, prosedur berbelit dan proses yang tidak transparen.

Fokus laporan ini ialah pada Sistem Perpajakan Nasional, meliputi Pajak Pendapatan, Pajak Pertambahan Nilai, Pajak Penjualan Barang Mewah, Pajak Penjualan Bumi dan Bangunan, dan Undang-undang tentang Peraturan Umum dan Prosedur Perpajakan. Walaupun merupakan hal yang makin penting, pajak provinsi dan kabupaten maupun bea-cukai, retribusi dan kontribusi tidak merupakan bagian dari laporan ini.

Dalam delapanbelas tahun terakhir Kebijakan Perpajakan Nasional di Indonesia telah mengalami perubahan radikal dengan tiga reformasi besar. Kebijakan terakhir, dalam tahun 2000, ialah membuat penyempurnaan peraturan pajak yang signifikan sehingga pada umumnya mengurangi beban pajak pendapatan UKM rata-rata. Dengan mem-pertimbangkan sejumlah besar pembebasan bagi UKM, insentif tidak-langsung, dan fasilitas umum yang sudah tersedia maka tidak diperlukan lagi menciptakan (tamba-han) insentif perpajakan bagi UKM.

Walaupun telah di-upayakan keras untuk mengurangi persyaratan resmi maupun be-ban administratif, lingkungan umum perpajakan masih saja kurang-akrab terhadap UKM dan yang tidak kalah penting, ialah akibat ketidak-pastian hukum dan perilaku pejabat-pejabat yang korup.

Pajak Pendapatan

Dari segi materi, Reformasi Pajak Pendapatan tahun 2000 memperkenalkan suatu struktur tarip pajak baru yang mengurangi beban pajak bagi sejumlah besar UKM. Ciri utama struktur baru ialah (i) memilah tarip pajak antara wajib pajak perorangan dan badan; (ii) mengurangi beban pajak bagi golongan berpenghasilan rendah, (iii) menaikkan tingkat pajak bagi wajib pajak golongan atas dari 30% hingga 35%. Den-gan kombinasi kenaikan pembebasan pajak bagi wajib pajak perorangan, maka re-formasi telah mengurangi secara signifikan beban pajak golongan wajib pajak ber-penghasilan rendah dan menengah.

ADB SME DEVELOPMENTTA

XV

Tarip Pajak hingga 2000

Tarip Pajak mulai 2001 Pajak Progresif (Pendapatan

Kena Pajak – Rp.juta.) Wajib Pajak Peroran-gan dan Badan

Wajib Pajak Perorangan

Wajib Pajak Badan

0-25 5% 5% 25-50 15% 10% 10%

50-100 15% 15% 100-200 25%

Diatas 200

30%

35% 30%

Pembebasan Pajak Wajib Pajak Rp. 1,728,000 Rp. 2,880,000 Isteri dengan penghasilan Rp. 1,728,000 Rp. 2,880,000 Isteri tanpa penghasilan Rp 864,000 Rp. 1,440,000 Tanggungan (max. 3) Rp 864,000 Rp. 1,440,000 Pembebasan Pajak max. (2 bekerja, 3 tanggungan) Rp. 6,048,000

Rp. 10,080,000

Secara substansial Reformasi Pajak tahun 2000 tidak merubah dasar hukum pajak pemotongan/pemungutan (withholding tax) dan pemungutan external. Namun demikian, beberapa tarip pajak pemotongan/pemungutan dinaikkan, yang paling rele-van dengan UKM ialah kenaikan tarip pajak pemotongan/pemungutan final penda-patan bunga dari deposit dan tabungan dari 15% hingga 20%; kenaikan tarip pajak pemotongan final dari Penyewaan Tanah dan/atau Gedung dari 6% hingga 10%; pencabutan / pembatasan pajak final 4% dari pendapatan konsultan dan kenaikan tarip pajak pemotongan efektif (sekarang dapat di-kredit kembali) terhadap penghasi-lan jasa-jasa professional, termasuk konsultansi hukum, pajak, teknis dan mana-jemen, dari 6% hingga 7,5% dari pendapatan kotor; dan pajak pemotongan baru jasa-jasa konstruksi.

Pajak Pertambahan Nilai / Pajak Penjualan Barang Mewah

Reformasi Pajak tahun 2000 menaikkan ambang batas bagi perusahaan kecil se-hingga dapat memilih pembebasan dari Pajak Pertambahan Nilai mulai Rp 24.000.000 hingga Rp.360,000,000 (barang) dan Rp.180,000,000 (jasa-jasa) dan mengurangi cakupan PPN barang dan jasa-jasa. Namun demikian masih terdapat sejumlah besar pembebasan yang berkaitan dengan obyek pajak, tarip pajak serta kewajiban pajak.

Terdapat sejumlah besar perbaikan dalam persyaratan resmi perpajakan. Dalam un-dang-undang pajak yang baru semua wajib pajak badan dapat klaim pengembalian setiap bulan apabila pemasukan kredit melampaui pengeluaran dalam sebulan. Apa-bila wajib pajak memenuhi beberapa criteria tertentu, proses pengembalian mungkin dapat disetujui dalam waktu tujuh hari dengan pembayaran dimuka, yaitu sebelum audit pajak. Reformasi Pajak tahun 2000 menyebutkan bahwa Invoice komersial dapat dipakai sebagai standard invoice pajak apabila memuat cukup perincian.

Reformasi Pajak tahun 2000 memperlebar jenjang tarip bagi Pajak Penjualan Barang Mewah maupun meningkatkan tarip yang berlaku bagi banyak ragam barang.

Pajak Penjualan Bumi dan Bangunan

Pajak Penjualan Bumi dan Bangunan dimulai dalam tahun 1997. Sebelumnya, hanya pendapatan atas penjualan bumi dan bangunan dibebankan pajak (pajak pemotongan final 5% atas nilai jual). Saat ini, baik Pajak Pendapatan maupun Pajak Penjualan Bumi dan Bangunan secara kumulatif harus dibayar. Undang-undang Pajak Penjualan Bumi dan Bangunan “baru” (UU No. 20/2000) hanya menambahkan pajak atas balik

ADB SME DEVELOPMENTTA

XVI

nama. Untuk mengurangi beban pajak bagi golongan berpenghasilan rendah undang-undang memberikan pembebasan, diskon, dan pengurangan kewajiban pajak.

Peraturan Umum dan Prosedur Perpajakan

Persyaratan formal yang ditetapkan dalam Peraturan Umum dan Prosedur Perpajakan (diperinci dalam undang-undang pajak yang bersangkutan) seringkali terlalu rumit dan kurang akrab bagi bisnis. Kewajiban ini terentang dari persyaratan untuk (i) mendaftar, (ii) membuat dokumentasi yang wajar (pembukuan dan catatan), (iii) untuk membuat penilaian sendiri atas kewajiban membayar pajak. Penilaian sendiri kewajiban mem-bayar pajak termasuk kewajiban mengisi surat pernyataan pajak, menghitung sendiri kewajiban membayar pajak, dan membayar pajak.

Reformasi Pajak tahun 2000 disatu fihak mengurangi beban administratif dengan memberi kemungkinan penyederhanaan format pajak, pembebasan membayar cicilan pajak bulanan, dan pembayaran pengembalian dimuka, yaitu tanpa wajib-audit. Difi-hak lain, menerbitkan denda administratif berat atau tuntutan pidana terhadap mereka yang tidak memenuhi kewajibannya, terutama bagi mereka yang tidak mendaftarkan diri. Secara umum, klaim pajak hanya mungkin dilakukan setelah dilakukan audit-wajib (lihat pengecualian diatas), dan dengan demikian meniadakan skema penilaian sendiri dan meningkatkan intervensi otoritas perpajakan.

ADB SME DEVELOPMENTTA

XVII

Temuan

Bagi sector UKM terdapat sejumlah besar pembebasan / insetif tidak-langsung. Sete-lah pengkajian-ulang Sistim Perpajakan, tampak bahwa sektor kecil-menengah meru-pakan bagian dari suatu kebijakan perpajakan umum yang bermaksud mengurangi beban mereka melalui insetif tidak-langsung dan pembebasan. Suatu risalah pembe-basan / insentif dijabarkan dibawah ini.

Pembebasan/ Insen-tif

Peraturan Persyaratan Perysaratan UKM

Penyederhanaan perhi-tungan Pendapatan Net dengan Norma Perhi-tungan Net

Ayat 5 (1)a PPH, Ayat 28 (2), KUdTCP

Omzet tahunan kurang dari Rp.600,000,000

Klasifikasi UKM

Pembebasan membuat pembukuan dan cata-tan

Ayat 14 (2), PPH, Ayat 28 (2) KUdTCP

Omzet tahunan kurang dari Rp.600,000,000

Klasifikasi UKM

Pembebasan mengisi SPT

Keputusan Menkeu 535/KMK.04/2000

Bila penghasilan net tidak melampaui penghasilan tidak-kena pajak sesuai Art. 7 PPH

UKM dengan kerugian saat mu-lai bisnis

Pembebasan dari ke-wajiban PPN

Ayat 1, Keputusan Menkeu No. 552/KMK.04/2000

Dapat memilih

Barang: omzet gross tidak melampaui 360,000,000

Jasa-jasa: omzet gross tidak melampaui 180,000,000

Klasifikasi UKM

Pengurangan Tarip Pa-jak Pendapatan yang diterima dari penjualan partisipasi / saham di UKM

Ayat 4 (2)k PPH Keputusan Menkeu 250/KMK.04/1995)

Perusahaan Modal Ven-tura

Joint Ven-ture dengan UKM di sek-tor spesifik Tidak diperda-gangkan di bursa effek

Penjualan Net tidak melam-paui Rp. 5 juta

Klasifikasi UKM

Perhitungajn Pajak Fi-nal untuk konstruksi bagi “Usaha Kecil Kon-struksi”

PP No 140/2000 Kontrak kurang dari Rp. 1 milyar + kwalifikasi sebagai UKM

(Sertifikasi UKM)

Klasifikasi UKM

Pengurangan beban pajak melalui peningka-tan pembebasan pajak

Ayat 7 PPH Wajib Pajak Perorangan UKM sebagai Pedagang

Pengurangan beban pajak melalui tarip Pa-jak Progres baru

Ayat 17 PPH Wajib Pajak Perorangan UKM sebagai Pedagang

ADB SME DEVELOPMENTTA

XVIII

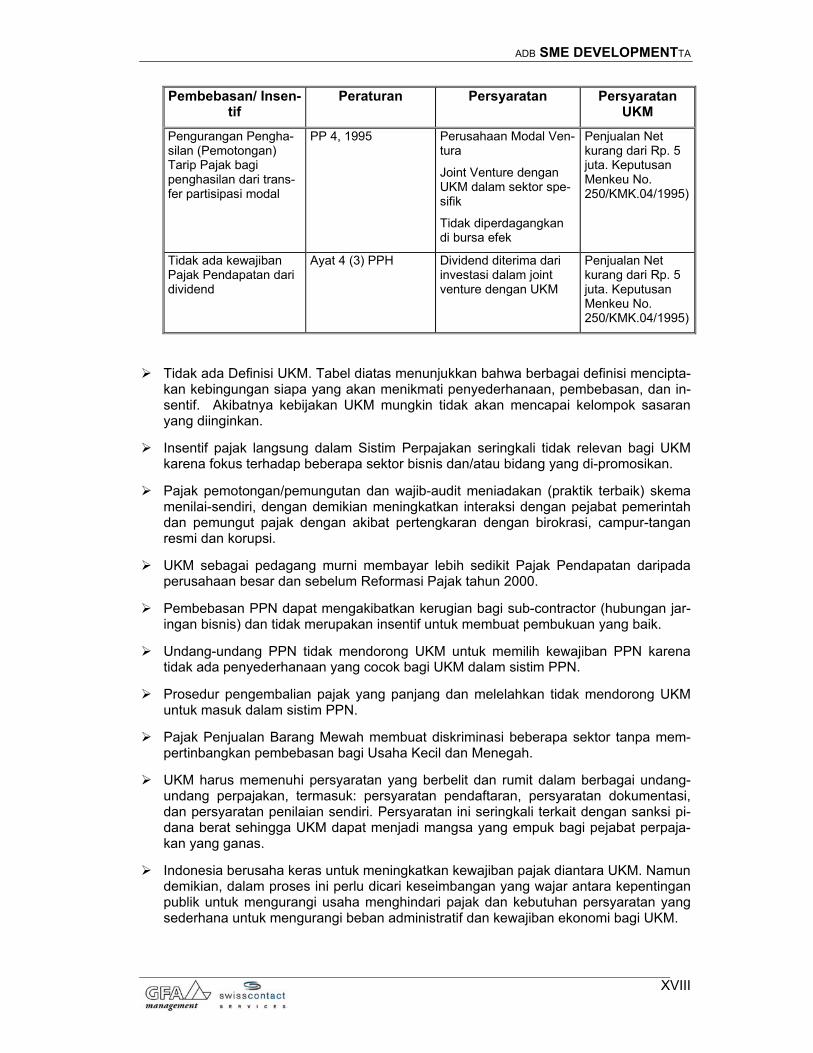

Pembebasan/ Insen-tif

Peraturan Persyaratan Persyaratan UKM

Pengurangan Pengha-silan (Pemotongan) Tarip Pajak bagi penghasilan dari trans-fer partisipasi modal

PP 4, 1995 Perusahaan Modal Ven-tura

Joint Venture dengan UKM dalam sektor spe-sifik

Tidak diperdagangkan di bursa efek

Penjualan Net kurang dari Rp. 5 juta. Keputusan Menkeu No. 250/KMK.04/1995)

Tidak ada kewajiban Pajak Pendapatan dari dividend

Ayat 4 (3) PPH Dividend diterima dari investasi dalam joint venture dengan UKM

Penjualan Net kurang dari Rp. 5 juta. Keputusan Menkeu No. 250/KMK.04/1995)

Tidak ada Definisi UKM. Tabel diatas menunjukkan bahwa berbagai definisi mencipta-kan kebingungan siapa yang akan menikmati penyederhanaan, pembebasan, dan in-sentif. Akibatnya kebijakan UKM mungkin tidak akan mencapai kelompok sasaran yang diinginkan.

Insentif pajak langsung dalam Sistim Perpajakan seringkali tidak relevan bagi UKM karena fokus terhadap beberapa sektor bisnis dan/atau bidang yang di-promosikan.

Pajak pemotongan/pemungutan dan wajib-audit meniadakan (praktik terbaik) skema menilai-sendiri, dengan demikian meningkatkan interaksi dengan pejabat pemerintah dan pemungut pajak dengan akibat pertengkaran dengan birokrasi, campur-tangan resmi dan korupsi.

UKM sebagai pedagang murni membayar lebih sedikit Pajak Pendapatan daripada perusahaan besar dan sebelum Reformasi Pajak tahun 2000.

Pembebasan PPN dapat mengakibatkan kerugian bagi sub-contractor (hubungan jar-ingan bisnis) dan tidak merupakan insentif untuk membuat pembukuan yang baik.

Undang-undang PPN tidak mendorong UKM untuk memilih kewajiban PPN karena tidak ada penyederhanaan yang cocok bagi UKM dalam sistim PPN.

Prosedur pengembalian pajak yang panjang dan melelahkan tidak mendorong UKM untuk masuk dalam sistim PPN.

Pajak Penjualan Barang Mewah membuat diskriminasi beberapa sektor tanpa mem-pertinbangkan pembebasan bagi Usaha Kecil dan Menegah.

UKM harus memenuhi persyaratan yang berbelit dan rumit dalam berbagai undang-undang perpajakan, termasuk: persyaratan pendaftaran, persyaratan dokumentasi, dan persyaratan penilaian sendiri. Persyaratan ini seringkali terkait dengan sanksi pi-dana berat sehingga UKM dapat menjadi mangsa yang empuk bagi pejabat perpaja-kan yang ganas.

Indonesia berusaha keras untuk meningkatkan kewajiban pajak diantara UKM. Namun demikian, dalam proses ini perlu dicari keseimbangan yang wajar antara kepentingan publik untuk mengurangi usaha menghindari pajak dan kebutuhan persyaratan yang sederhana untuk mengurangi beban administratif dan kewajiban ekonomi bagi UKM.

ADB SME DEVELOPMENTTA

XIX

Menurut hasil suatu survey kuantitatif yang dibuat oleh ADB TA SME Development, pengetahuan dan kewajiban pajak diantara UKM relatif rendah.

Rekomendasi

Prosedur perpajakan maupun iklim umum administratif masih memerlukan pengkajian yang mendalam. Disarankan untuk membuat suatu kelompok-kerja untuk mengkaji-ulang peraturan dan prosedur perpajakan bagi UKM dengan perhatian khusus terha-dap penyederhanaan persyaratan administratif & formal yang berlanjut. Dengan par-tisipasi stakeholders swasta (bisnis kecil dan menengah, pressure groups, konsultan pajak) dimulai membuat studi lebih lanjut tentang persepsi pajak khusus bagi UKM, misalnya korupsi, kewajiban pajak, pengetahuan perpajakan, dan hambatan-hambatan peraturan perpajakan.

Otonomi regional telah meningkatkan hak perpajakan pemerintah daerah. Oleh karena itu dampak pajak lokal memerlukan pengkajian mendalam / penilaian. Selan-jutnya perlu memperhatikan potensi harmonisasi, sejauh mungkin, prosedur adminis-tratif, supervisi peradilan, dan persyaratan formal (mis., kewajiban pencatatan, men-ghitung dasar pajak, dsbnya).

Indonesia berusaha keras untuk meningkatkan ketaatan pajak diantara UKM. Untuk meningkatkan keataatan pajak dan membawa UKM kembali ke sector formal seyogy-anya dimulai dengan suatu kampanye kesadaran untuk menyediakann informasi ten-tang sistim perpajakan diantara UKM. Seyogyanya dibuat suatu perangkat informasi yang akrab UKM yang memuat informasi perpajakan bisnis dan dengan demikian da-pat meningkatkan pemahaman tentang sistim dan prosedur perpajakan.

Indonesia belum memiliki suatu definisi UKM, bukan hanya dalam sistim perpajakan. Suatu kesatuan pemahaman definisi UKM sangat penting untuk membuat suatu kebi-jakan UKM yang focus dalam semua hal perpajakan.

Skema pajak pemotongan/pemungutan, wajib-audit untuk pengembalian pajak, dan prosedur pengembalian pajak yang berbelit mempunyai dampak negatif – secara prin-sipiil – terhadap sistim perpajakan yang berimbang. Secara umum skema pemoton-gan/pemungutan seyogyanya dikurangi dan wajib-audit diganti dengan suatu modifi-kasi verifikasi dan dipertimbangkan kembali sebagai suatu pembebasan ketimbang suatu peraturan tetap. Sebagai suatu langkah awal, usaha kecil seyogyanya dibebas-kan dari persyaratan pemotongan/pemungutan dan skema pemotongan yang mem-punyai dampak negatif terhadap sub-kontrakting sebaiknya diganti dengan skema penilaian sendiri.

Kesadaran dampak positif yang diperoleh dari Reformasi Pajak Pendapatan belum cukup ditingkatkan. Pemerintah seyogyanya memanfaatkan citra positif ini dan men-yebar berita bahwa UKM mendapatkan manfaat dari Reformasi Pajak Pendapatan se-cara signifikan dengan mengurangi beban pajak mereka, memberikan insentif pajak tidak-langsung yang baru, maupun pembebasan dan penyederhanaan. Oleh karena itu disarankan untuk membuat advokasi dampak positif tersebut bagi UKM.

Mempertimbangkan kembali pandangan umum mengenai praktik pembayaran cicilan pajak bulanan walaupun wajib-pajak secara material tidak wajib membayar Pajak Pendapatan. Suatu perubahan dalam praktik ini akan membantu mengurangi dampak negatif pada alur kas, utamanya bagi UKM.

ADB SME DEVELOPMENTTA

XX

Saat ini, sebagian besar UKM didenda berat hanya karena tidak mendaftarkan diri. Untuk membangun sebuah jembatan emas menuju sector formal, seyogyanya dibuat peraturan pengampunan bagi mereka yang tidak memenuhi persyaratan pendaftaran karena tidak ada informasi atau pengetahuan tentang perpajakan. Selanjutnya dis-arankan untuk mengecualikan golongan strata berpenghasilan rendah (penghasilan kotor setahun kurang dari Rp. 50.000.000) dari semua persyaratan perpajakan terma-suk kewajiban mendaftarkan diri.

Perusahaan yang dibebaskan dari PPN seyogyanya diberi klasifikasi nol percent (ketimbang dibebaskan dari pajak). Sebagai alternatif lain maka disarankan untuk ti-dak memungut PPN. Akibatnya PPN tidak dibebankan pada transaksi sedangkan usaha kecil masih di-izinkan untuk membuat kredit atas pajak masukan. Dengan demikian hal ini akan menciptakan insentif agar memenuhi kewajiban perpajakan, membuat pembukuan, dsbnya, maupun penciptaan insentif untuk meningkatkan per-mintaan terhadap jasa konsultansi perpajakan.

Usaha kecil dapat dibebaskan dari Pajak Penjualan apabila membeli sebuah kom-puter untuk penggunaan dalam bisnis.

ADB SME DEVELOPMENTTA

XXI

ADB SME DEVELOPMENTTA

1

1 WHY THIS REPORT IS WRITTEN / SCOPE OF WORK

This report as one output of the ADB SME Development Project aims at supporting the Indonesian inter-ministerial SME development task force in formulating a medium-term SME development strategy that is in line with the country's overall reform program and stabilization efforts. One focus of attention is creating a conducive taxation environment for SME and SME development policies. In more detail, the purpose of the report is to propose an agenda to the Indonesian Government for enhancing a business friendly taxation system. Its recommendations will be reflected in a revised Medium-Term Action Plan for the Development of SMEs as it merges Objective 1 in Annex D with Annex A of the Medium Term Action Plan.

As a Final Report it further meets the requirements of Output 1.6 to be delivered by the TA (Working Group SME Environment) “Existing tax system is assessed with regard to SME relevant taxation and strategies for SME friendly taxation are developed”.

The actual scope of work reflected in this report is the result of two refinements, which have been agreed upon with the Task Force.

1st Refinement: As Annex D of the Mid Term Action Plan still focuses on actions introduc-ing new tax incentives it was agreed to translate and merge tax related actions into the SME Environment Action Plan under Objective 2- Improve, simplify and streamline laws and regulations and here under Action 2.5: Review of Tax Laws and their Enforce-ments with regards to their impact on SME.

2nd Refinement: The ADB-TA together with the Taskforce decided to give the taxation issue a lower priority taking into consideration the intensive and well-founded reform work currently carried out by the Ministry of Finance with USAID assistance. As a result this re-port will include three outputs, namely (i) information on SMEs perception of taxation laws and practice as a result from the TA's conducted quantitative survey, (ii) preparation of a synopsis of SME-specific tax regulations in Indonesia, (iii) elaboration of specific SME constraints/ incentives with regards to general impact of tax laws, the Income Tax Law, the Value Added Tax and the enforcements of those laws. The results with main aspects for consideration will be submitted to the Task Force and the USAID project, which is working on the revision of the taxation system. This project, located in the Ministry of Fi-nance, aims at supporting Indonesian tax reform and simplification and has, a/o, already compiled an extensive tax expenditure report listing most tax exemptions in main national taxes, as well as commenced work on regional taxation issues.

To meet the before mentioned requirements this report supplies a synopsis of Indonesian Taxation System (national) taking into account the Tax Reform 2000 (Chapter 2) as well as the relevance for SMEs. Based on an assessment findings are developed for further discussion (Chapter 3). The findings will than be then translated in recommendations, which are reflected in Chapter 4.

ADB SME DEVELOPMENTTA

2

Taxation System often hampers SME growth or forces them into the informal sector Taxation can effect a business on various levels, i.e. it can have effects on (i) cash flow (through tax payments), (ii) business decisions (evaluation which decision is most benefi-cial to save taxes, and (iii) on the accounting system of a business (bookkeeping require-ments).1 Constraints within in this structure often relate to issues that taxes are too high, discriminate SMEs against other businesses or burden them with extensive and compli-cated tax filing and bookkeeping requirements.

Often constraints do not only relate to tax laws but also to bureaucratic behavior, i.e. how those laws and regulations are executed by the tax authorities. With regards to SMEs the impact of all taxes has an associated high level of interaction with government. This often is a source of considerable hassle and thus has direct result on the productivity of the business. On top, considerable constraints are encountered like (i) informal fees, bribes; (ii) lengthy procedures, (iii) accountability, and transparency.

With numerous taxes, and a high interface with Government, which is often perceived to have corruption costs associated with it, the SME sector on many occasions prefers to stay in the undocumented informal sector or prefers to remain small. It is therefore impor-tant to examine the impact of the Tax System on SMEs, because tax laws and regulations (legislation) as well as the execution of those regulations can hamper the productivity and thus the growth of the small business sector.

Strategies to remove constraints In order to remove the before mentioned constraints Governments developed various strategies. One approach is to directly intervene on business level by granting tax incen-tives. The other approach is to intervene on macro-level improving the tax environment.

The rationale of tax incentives is to compensate a specific target group for identified defi-ciencies. There are commonly four kind direct tax incentives found in income tax systems around the world: Various shortcomings of providing incentives caused a shift of para-digm. Today policies focuses on a cleaner income tax system with few preferences of any kind, broad tax bases, moderate tax rates. Between 1987 and 1999 almost every OECD country had reformed its income tax system following major changes to the income tax structures. If policy makers want to create a conducive tax environment they should have the following objectives in mind: simple procedures; low tax rates; low official charges, and fair and impartial treatment of all taxpayers.

1 Lothar Haberstock, Introduction in the Business Economics of Taxation, 6. Auflg., S + W Steuer und Wirtschaftsverlag,

Hamburg, p. 19, 20

ADB SME DEVELOPMENTTA

3

2 SYNOPSIS OF BUSINESS RELEVANT TAX LAWS IN INDONESIA

2.1 Overview and Focus

The Indonesian tax system and legislation dates back to the Dutch colonial period. It fol-lows the continental European legal tradition, which is primarily based on codified norms in the form of laws, Presidential Regulations and Ministerial Decrees. Court decisions play a much less prominent role than in countries following the Anglo-Saxon legal tradition.

In postcolonial times, several major tax reforms have been undertaken:

The 1983 Tax reform consolidated numerous individual laws and decrees into a sin-gle, comprehensive Law on Income Tax (Undang Undang No 7, 1983 tentang Pajak Perhasilan- in future referred to as UU PPh). In addition, the Sales Tax was replaced with Value Added Tax, albeit a so-called Sales Tax on Luxury Goods has been main-tained. Finally, the reform introduced a Law on General Rules and Procedures of Taxation in order to harmonise assessment and collection of various taxes.

During the 1993 tax reform, the Income Tax Law was revised and complemented by a number of Presidential Decrees. Revisions in particular related to calculation of tax-able profits, the introduction of tax facilities for capital investment in certain business fields and areas, and taxation of income from sale of land and buildings, stock shares, venture capital investment and interest on deposits and savings. In addition, proce-dural regulations for VAT and Sales Tax on Luxury Goods where consolidated with procedures for other taxes and integrated into the Law on General Rules and Proce-dures of Taxation.

The 2000 tax reform, entering into force by January 1st, 2001, finally, introduced new income tax tariffs, and extended the coverage of income tax and VAT by removing a number of sector-specific and enterprise-specific tax exemptions.

Structure of the Tax System After the 2000 tax reform, the Indonesian tax system consists of the following taxes:

Income tax is levied on the taxable income of resident individuals, corporations and non-residents with taxable income from Indonesia. Indonesia does not have a sepa-rate Corporate Tax Law. The Income Tax Law applies to individuals and corporations alike, although applying different income tax tariffs on both groups of taxpayers.

Value Added Tax (VAT) is levied on commercial transactions in Indonesia, excluding those of the financial sector.

Sales Tax on Luxury Goods is levied on the import or manufacture of certain goods. Although being referred to as 'Sales Tax' and regulated together with VAT, it in fact constitutes an excise, as it is only levied once at the source of product origin, and not on each sale of the respective good.

As most excises are levied as 'Sales Tax on Luxury Goods', Excise Tax plays a less prominent role. The national government only levies excise tax on tobacco products and alcoholic beverages. In addition, Indonesia has a moderate motor vehicle fuel tax, the revenue from which is distributed between provincial (10%) and district/city governments (90%).

ADB SME DEVELOPMENTTA

4

Tax of Transfer of Land and Building was introduced in 1997. 5% transfer tax is lev-ied on the purchasing price or market value of the transferred object. With the 2000 tax reform, transfers resulting from inheritance and from company mergers, previously excluded from this tax, became also taxable.

Wealth tax (IPEDA) is levied locally on property (land and buildings) and the wealth of citizens. It is distributed between districts/cities (90%) and provinces (10%).

Province and district taxes: A number of taxes are raised on the level of the prov-inces and districts. The provinces raise Motor Vehicle Tax and Tax on Transfer of Ownership of Motor Vehicles. District taxes regulated by national law include (i) Hotel and Restaurant Tax, (ii) Advertisement Tax, (iii) Street lighting tax, (iv) Mineral removal and processing tax and (vi) Water exploitation tax.

Hotel and Restaurant Tax - The highest tax rate for the hotel and restaurant tax is 10% of the amount paid to

the hotel and/or restaurant. Entertainment Tax (Pajak Hiburan)

- The highest tax rate for the entertainment tax is 35% of the amount paid or which should have been paid to watch and/or enjoy entertainment.

Advertisement Tax (Pajak Reklame) - The highest tax rate for the advertisement tax is 25% of the lease value of the

advertisement. Tax on Street Lighting (Pajak Penerangan Jalan)

- The highest tax rate for the street lighting tax is 10% of the sales value of the electrical power and will be collected by PLN (the National Electrical Company) from the electric bill every month.

Tax on Collecting and Exploiting Group C Mining Products. - The highest tax is 20% on the sales value of the exploiting proceeds from Group

C Mining Products. The regulation also stipulates the types of Group C mining products.

Tax on Motor Vehicles (Pajak Kendaraan Bermotor) - The tax rates for motor vehicles are set at 1.5% for private vehicles, 1% for public

vehicles, and 0.5% for heavy equipment as calculated from the sales value (the standard market price) or other value which can be used to assess the tax.

Duty on Transfer of Title to Motor Vehicles - The rates for the duty on the first delivery are 3% and 10%. - The rates for the duty on the second and subsequent deliveries are 0.3% and

1%. - The rates for the duty on delivery due to an inheritance are 0.03% and 0.1% (de-

pending on the type of vehicle) calculated from the sales value (the standard market price) or other value that can be used to assess the tax.

Tax on Water Vehicles (yachts, cruise ships, sports boats, and certain other vessels)

- The tax rate is set at 1.5% for water vehicles calculated from the sales value (the standard market price) or other value that can be used to assess the tax.

Duty on Transfer of Title to Water Vehicles - The duty on the first delivery is set at 5%. - The duty on the second and subsequent deliveries is set at 1%. - The duty on deliveries due to an inheritance is set at 0.1% (depending on the

type of vehicle) calculated from the sales value (the standard market price) or other value that can be used to assess the tax.

Besides the above regional taxes, the regulation also covers taxes on fuel and parking.

ADB SME DEVELOPMENTTA

5

Fiscal decentralization introduced the right for provinces and districts to introduce new taxes and retributions. Examples of locally introduced taxes include tourist tax, radio tax, dog-owner licenses, billiard tax and, most controversially, road usage tax.

Withholding Taxes In general, Indonesia has adopted a self-assessment system. Taxpayers have to register with the tax offices, and present a periodic or annual Tax Return on relevant taxes. This system implies that taxpayers have the obligation of computing their own tax liability. It also implies that in general no official assessment is necessary.

A distinct feature of the Indonesian Tax Law is the widespread use of tax withholding schemes, which replace self-assessment. Tax withholding extends far beyond tax objects usually governed by such schemes worldwide such as income from employment or divi-dends, and also covers a number of business transactions such as professional services, or subcontracts for certain industries, and even travel abroad by individuals. Moreover, tax withholding is not restricted to income tax, but also applied to VAT. Withholding mecha-nisms ar e not regulated in the Law on General Rules and Procedures of Taxation, but in individual laws and decrees.

Some withholding taxes, such as withholding tax on income from employment, are cred-ited against actual tax due as per Tax Return or Tax Assessment Notice. Others, how-ever, are considered as final. Such Final Withholding Taxes replace transaction taxes common in many other countries. An example is the Withholding Tax on Income from Sales Transactions (Government Regulation 41/1994), which, as being final, is materially a sales tax on stock exchange transactions.

Other public charges In addition to taxes, public charges (levies) also include

Custom Taxes- Governmental charges imposed on goods at the time they are im-ported into a state; and

Retributions- Usage fees for specific purposes and services, such as parking or mar-ket fees, or airport tax.

Contributions for Social Security and the Foundation for the Mitigation of Poverty.

Report Focus This Background Report focuses its synopsis on national taxation laws and regulations including those on withholding taxes.. Time and resource constraints did not allow analyz-ing local taxes and other public charges in detail. Special consideration is given to the elements and impacts of the 2000 tax reform.

2.2 Income Tax (revised according to Law No.17 of 2000)

2.2.1 General The Taxation of individuals and enterprises- independent of the legal form- is stipulated in a single statute, Undang Undang No 7, 1983 tentang Pajak Perhasilan- UU PPh-, which was for the third time completely revised by Law No 17, 2000 of 2nd August 2000.

ADB SME DEVELOPMENTTA

6

In order to enhance justice with regards to the imposition of tax, revisions were particularly made with respect to the coverage of tax subjects, tax objects and deductible expenses. In order to distribute more proportionate tax burdens among the respective group of tax-payers, the new law distinguishes between individual and corporate taxpayers. The new law also amends the tax rate structure and introduces a new concept in relation to transfer pricing issues. Some of the changes made to the old (existing) law are set out below.

2.2.2 Tax subjects Individuals and undivided estates, legal bodies and permanent establishments are, ac-cording to Article 2(1) PPh, subject to income tax:

An undivided estate is defined as a unit in lieu of the beneficiaries.

A body is defined as including the following legal forms (usaha berbadan) according to Indonesian business law:

• Limited liability company or Perseroan Terbatas-PT- (Naamlose Vennotschap),

• Other partnerships, namely the basic partnership (maatschap) and open part-nership (firma);

• Cooperatives;

• Legal entities established and owned by the government, including those in le-gal forms as defined by Law No. 12/1967 on co-operatives, including Perusa-haan Perseroan or Persero (state owned limited liability company), Perusahaan Umum or Perum (public enterprise), Perusahaan Jawatan or Perjan (govern-ment agency), and Perusahaan Daerah or Perusda (local state owned com-pany);

In addition, bodies according to Article 2 PPh include affiliations, associations, foundations or similar organizations, institutes, pension funds "and other forms of business".

The only business form without legal incorporation is the sole trader (perorangan). Sole traders are regarded as individuals, not as bodies under the income law. The sole trader is the by far most common legal form among SMEs. According to a 1999 survey of the Indonesian Statistical Office (BPS), more than 98% SMEs operate as sole traders1.

Resident and non-resident tax subjects The law distinguishes between resident and non-resident tax subjects. Resident tax sub-jects are individuals residing in Indonesia or present there for more than 183 days in any twelve-month period, and bodies established or domiciled in Indonesia. Non-resident tax subjects are individuals residing in Indonesia for less than 183 days, and bodies not es-tablished or domiciled in Indonesia, which receive income from Indonesia and/or carry out activities through a permanent establishment in Indonesia.

Unlike in several other countries, origin does not influence tax status. An Indonesian citi-zen residing abroad and not visiting Indonesia is not subject to Indonesian income tax. A foreign citizen residing for more than 183 years in Indonesia, on the other hand, is, as a 1 Profil Usaha Kecil dan Menengah Tidak Berbadan Hukum, Badan Pusat Statisitk, Jakarta, 1999, counts 14.520.041

Indonesian SMEs operating without legal incorporation, compared to 239.408 businesses incorporated as legal entities. SME in this survey are those with less than 20 employees.

ADB SME DEVELOPMENTTA

7

resident tax subject, liable for income tax in Indonesia with his worldwide income, includ-ing income derived from his country of origin.

A permanent establishment is defined as establishment used by a non-resident tax sub-ject to conduct business or engage in activities in Indonesia. Permanent establishments listed in Article 2 Paragraph 5 PPh include places of management, representative offices and agents, factories and workshops, construction, installation and assembly projects, and any furnishing of services conducted for more than sixty days in any twelve-month period.

Most income tax regulations do not distinguish between the aforementioned types of tax subjects. However, the 2000 tax reform introduced different tax tariffs for individual tax subjects and for bodies. For permanent establishments, the list of tax objects is restricted, as is the list of deductible expenses. Taxation of non-resident taxpayers shall primarily be effected through final, non-reimbursable withholding of income tax. As this synopsis fo-cuses on SME-relevant aspects of taxation, no further reference will be given to specific regulation for permanent establishments and non-resident taxpayers.

2.2.3 Tax Objects

Taxable sources of income According to Article 4 Paragraph 1 PPh, object of income tax is any increase in eco-nomic capability received or accrued by a Taxpayer, originating from within or without Indonesia, which can be used for consumption or to increase the wealth of the taxpayer. The list of taxable income sources includes, among others,

Income from employment and services,

Lottery prices and awards,

Business profit,

Gains from the sale or transfer of property,

Income from rent, dividends, interest and royalties,

Gains from property revaluation, foreign exchange fluctuation and debt cancellation, and

insurance payments received.

Non- taxable sources of income Not taxable according to Article 4 Paragraph 3 PPh are

Aid and donations, including those received in kind for services, e.g. from 'food for work' projects, and gifts received by small businesses

Gifts received from direct blood relatives, and inheritances,

Payments received from life, health, accident, or education insurance, and

Profit shares received from a limited partnership without shares (C.V.), affiliation, as-sociation, firma or kongsi, i.e. enterprise forms with full shareholder liability where the profit has already been taxed on the enterprise level.

In addition, Article 4 Paragraph 3 k PPH excludes income received or accrued by a ven-ture-capital company as share of the profit of a joint venture with a small or medium-

ADB SME DEVELOPMENTTA

8

sized firm from taxation, provided the joint venture engages in certain business activities to be determined by the Minister of Finance, and its shares are not traded on the stock exchange. This regulation is to encourage venture capital investment in SMEs.

Changes introduced by the 2000 tax reform The 2000 tax reform has extended the scope of the following taxable objects:

Dividends received by foundations and legal bodies with limited shareholder liability (Limited liability company –P.T., cooperatives and State Enterprises) were previously not categorized as tax objects. Under the new law, these types of dividends are treated as tax objects. Dividends received from equity participation in business corporations established and domiciled in Indonesia only continue to be tax exempted according to Art. 4 (3) PPh if

• the dividends are paid out from reserved retained earnings, and the recipient is a cooperative, or a limited liability company or State/Regional owned enterprise that owns at least 25% of the paid-in capital of the company paying the divi-dends and has a core business activity other than owning shares in the com-pany paying the dividends; or

• the dividends are received by a venture capital from investment in or joint ven-tures with small and medium enterprises (SME). SME in this respect are de-fined as a company that has annual net sales not more than Rp 5 billion (Minis-try of Finance Decree 250/KMK.04/1995)

Interest on Bonds received or obtained by an Investment Fund Company will be treated as tax objects as of the fifth year of its establishment or the date of its business license (Article 4 paragraph 3 (j) PPh). Previously, such income was not categorized as tax object.

The 2000 tax reform has introduced one new tax exemption. According to Article 31B PPh, gains related to debt restructuring organized through a special institution estab-lished by the government, namely the Jakarta Initiative Task Force, are now tax exempt. The tax exemption covers gains from:

forgiveness of debt;

transfer of property to the creditor for the settlement of debts; and/or

debt-equity swaps.

ADB SME DEVELOPMENTTA

9

2.2.4 Calculation of Net Income The net income shall be calculated by deducting income-related expenses from the gross income (Art. 6 PPh). In general, all expenses to earn, recover and secure the income are deductible according to Article 5 Paragraph 1 Subpara a.) PPh. This includes costs of ma-terials, wages and wage-related expenses, interest, rent, royalties, travel costs, waste processing costs, administrative costs and taxes other than income tax. Deductible are as well contributions to an approved pension funds, insurance premiums, foreign exchange losses and costs of scholarships, apprenticeships and training.

Non-deductible expenses Non-deductible expenses according to Article 9 PPh include

Profit distribution, including dividends;

Costs incurred for the personal benefit of shareholders, partners or members, as well as excessive compensation for work paid to shareholders or other parties having a special relationship; and costs incurred for the personal benefit of a Taxpayer or his dependents;

Formation or accumulation of reserves, except for bad debts of a bank or a finance leasing business, reserves in insurance business, and reclamation costs for a mining business;

Expenses on non-taxable objects such as gift, aid, donations, inheritances, and pre-miums for personal insurance (with the exception of insurance premiums paid by an employer as part of the income an employee), as well as expenses incurred in relation with income subject to final withholding tax (see below for details);

Salaries paid to members of an association, firma or limited partnership, as profit dis-tribution from such bodies is tax-exempt on the level of the shareholders;

Income Tax;

Administrative and criminal penalties in the form of interest, fines and surcharges.

The tax law is unclear on certain promotion expenses: Are expenses for promotional dis-tribution of product samples deductible as expenses to earn and secure income, or non-deductible, because such samples are gifts and donations? What about business lunches and receptions? No Government Regulation or Ministerial Decree clarifying these ques-tions could be found.

Activation, valuation and depreciation

Article 10 Paragraph 6 PPh stipulates that inventories and the use of inventories for the calculation of production costs shall be valued according to the purchase price by using either the average cost of inventory or the first-in first-out method. This means that inven-tory revaluations carried out according to commercial accounting standards, e.g. revaluat-ing raw material stocks according to a change in world market prices, are not accepted in income calculation for income tax purposes. No reference is given in the Income Tax Law to the deductibility or non-deductibility of inventory losses.

ADB SME DEVELOPMENTTA

10

Expenses for assets having a useful life of more than one year may not be deducted in the year of purchase, but have to be activated and depreciated over the assets' useful life period (Art. 9(2) PPh). The duty for activation covers expenditures to purchase, erect, ex-pand, improve or alter such assets. There is no indication in the law and corresponding regulations and decrees that, as in many other countries, major repairs have to be acti-vated. Similarly, shipping costs for durable assets appear to be directly deductible and do not have to be activated and depreciated.

The income tax law or corresponding regulation and decrees do not include any regulation on assets of minor value. In many countries, durable assets with acquisition costs below a certain level, e.g. DM 800 in Germany, do not have to be activated in order to simplify ac-counting.

Besides tangible assets, businesses also have to activate expenditure to acquire intangi-ble assets and other expenditure with a useful life of more than one year. The catalogue of respective expenditure in Article 11a PPh is rather limited. It only names expenditures incurred before the commencement of commercial operations, extraction rights, forestry concessions, and, optionally, expenditures for the formation and expansion of capital. No reference is given to intangible assets such as licenses, patents, software, brand names and goodwill. Article 6 Paragraph 1 PPh stipulates that costs related to research and de-velopment carried out in Indonesia do not have to be activated, but can be fully deducted from gross income in the year when they have arisen. Whether this implies, that costs re-lated to research and development carried out outside Indonesia have to be activated as intangible assets, remains unclear.

Annual depreciation depends on the expected useful life and the depreciation method chosen by the taxpayer. Under Indonesian Income Tax Law there are two different depre-ciation methods available, the use of which depends on whether the asset in question is movable, immovable, tangible or intangible. For tangible movable assets the taxpayer may choose between:

Straight-line depreciation, where a fixed percentage is applied annually to the as-set’s acquisition cost, or

Reducing-balance (degressive) depreciation, where a fixed percentage is each year applied to the opening book value.

Figure 1: Depreciation methods and rates according to Article 11 PPh

Depreciation/Amortization Rates Type of As-set

Useful Life in years Straight Line (percent of his-

Movable and Intangible Assets Category I 4 25% 50% Category II 8 12,5% 25% Category III 16 6,25% 12,5% Category IV 20 5% 10% Buildings Permanent 20 5% - Non Perma-nent

10 10% --

ADB SME DEVELOPMENTTA

11

Categories 1-4 are further specified in the attachments of the ministerial decree, 520/KMK.04/2000. Depreciation periods for many assets are rather long compared to in-ternational standards. Category I, for example, only includes assets such as small office equipment and motorcycles, while limousines and trucks are classified in category II, i.e. eight years usual life. In industrialized countries, road vehicles are usually assigned a use-ful life of four years, while computers are often even only assigned a useful life of three years. Similarly, most processing equipment, e.g. for wood processing, is classified in category III (16 years useful life). The standard in most industrialized countries is depre-ciation over eight to ten years.

Under a new decree (MoF Decree No. 138/KMK.03/2002), issued April 2002, computers, printers and scanners are categorized under Category 1 fixed assets. This will accelerate the monthly depreciation of such assets.

Indonesian tax law does not allow for extraordinary depreciation due to technical out-datedness or a lower market price for comparable used equipment or buildings. However, in case of sale or withdrawal of assets, the book value is treated as a loss, while the sales price or insurance reimbursement is treated as income.

Net Income Calculation Norm for small enterprises Art. 14 PPh sets out that an individual taxpayer with annual gross turnover of not more than Rp. 600 million may use the Net Income Calculation Norm for income calculation, provided such intention is communicated to the Director General of Taxes within the first three months of the tax year concerned. Under this Norm, the net income is calculated as percentage of gross turnover. The percentage rates to be applied differ by economic activ-ity and region. The respective ordinance of the DG Taxation (Kep – 536/PJ/2000) distin-guishes 183 different economic activities and three regional classes (12 major cities, other district capitals, other regions), which is a total 549 different percentage rates to be ap-plied. If gross turnover stems from several economic activities and/or regions, it has to be broken up in order to have the correct percentage applied to each turnover component.

While in principle meant to simplify net income calculation, it is questionable whether the Net Income Calculation Norm in its current level of sophistication and detail can reach this objective.

Income Tax for Certain Individual Traders From 1 April 2002 on, an individual trader in the consumer goods retail business (exclud-ing restaurants and motor vehicle trading) with outlets in several locations has to pay monthly Income Tax instalments at 2% per month of gross income, MoF Decree No. 84/KMK/ 2002, DGT Decree No. 171/PJ/2002)

2000 Tax Reform The 2000 tax reform introduced a number of new regulations and clarifications with re-spect to tax deductibility:

Bad debt: Previously, non-collectible receivables could be deducted from profit. Under the new law, write-off of non-collectible receivables is only deductible under certain conditions, including corresponding write-off in the commercial balance sheet, and failure to collect the debt by court order, or publicly declared bankruptcy of the debtor.

Benefits in Kind: Deductibility of expenses for food and drinks provided by the em-ployer was not regulated under the old law. Under the new law, food and drinks are treated as deductible expenses as long as they are provided to all employees.

ADB SME DEVELOPMENTTA

12

Installation costs: Under the old law, expenses for installation of tangible assets with a useful life of more than one year had to be activated and depreciated. Under the new law, installation costs are directly deductible and do not require activation and de-preciation anymore.

Review of asset classification: No changes in the basic depreciation tables have been made during the 2000 tax reform. However, some reclassification of assets took place. Category II, e.g., now includes certain equipment in the semiconductor industry. Furthermore, unspecified assets will now be subject to classification by the Ministry of Finance. Previously, unspecified assets were deemed to be included under Category III (16 years useful life).

Depreciation as tax incentive: In order to boost direct investment in Indonesia, Arti-cle 31A PPh of the old law provided a general clause allowing the government grant-ing unspecified tax incentives to taxpayers investing in certain business sectors and/or certain areas. As application of this clause had in some cases raised concern about eventual abuse in the interest of specific investors, the new law now specifies these incentives in more detail. It basically foresees the option for the government to double straight-line and reducing-balance depreciation rates for specific business sec-tors as a means to enhance investment in those sectors.

2.2.5 Tax Base The taxable income (tax base) is derived from the net income by deducting the following positions where applicable:

Losses incurred in previous tax periods:. Such losses can in general be carried forward for a maximum of five consecutive years (Art. 6 (2) PPh). Article 31A PPh of the new law provides the possibility to extend by Government Regulation the loss compensation period to a maximum of 10 years for taxpayers investing in specific business sectors and/or locations

Tax Free Allowances for individual tax payers (Article 7 PPh) as follows:

• Rp. 2,880,000 (Rp. 1,728,000 before the 2000 tax reform) for each taxpayer. If both partners of a married couple earn taxable income, each of them is entitled to this allowance.

• an additional amount of Rp.1,400,000 (before Rp. 864,000) for a married tax-payer whose spouse does not have own income.

• an additional amount of Rp.1, 440,000 (before Rp. 864,000) for any blood-related members of the family and relatives by marriage in direct line and adopted children, who are full dependents of the taxpayer, for up to three (3) dependents.

Investment Allowance: In order to boost direct investment in Indonesia, Article 31A PPh allows for reducing the taxable net income from investment in specific business sectors and/or locations to a maximum of 30% of the invested amount. Details have to be defined by respective Government Regulation.

ADB SME DEVELOPMENTTA

13

2.2.6 Tax Calculation (Tax rates) Indonesia operates with a progressive income tax tariff, i.e. tax rates increase with taxable net income. Payable income tax is calculated by multiplying the taxable net income with the income tax rate applicable to each respective income bracket (progression zone).

The 2000 Tax Reform introduced a new tax rate structure. The main purpose was to dis-tribute more proportionate tax burdens among different groups of taxpayers. The main features of the new structure are:

Introducing separate tax tariffs for individual and corporate taxpayers;

Reducing tax rates for lower income brackets;

Increasing the top tax rate for individual taxpayers from 30% to 35%.

In combination with the increase in tax free allowances for individual taxpayers, the reform has significantly reduced the tax burden of low and middle-income taxpayers.

Figure 2: Tax Tariffs Before and After the 2000 Tax Reform

Tax Rate Until 2000 Tax Rate from 2001 Progression Zone (Taxable In-

come in Million Rp.) Individual and Corpo-

rate Taxpayers Individual Taxpayer

Corporate Taxpayer

0-25 5% 5% 25-50 15% 10% 10%

50-100 15% 15% 100-200 25% over 200

30%

35% 30%

Tax free allowances Taxpayer Rp. 1,728,000 Rp. 2,880,000 Spouse with own income Rp. 1,728,000 Rp. 2,880,000 Spouse without own income Rp 864,000 Rp. 1,440,000 Each other dependant (max. 3) Rp 864,000 Rp. 1,440,000 Maximum Tax Free Allowance (2 earners, 3 dependants) Rp. 6,048,000

Rp. 10,080,000

ADB SME DEVELOPMENTTA

14

Individual taxpayers A before-after comparison yields that the increase in the top tax rate for individual taxpay-ers from 30% to 35% leads to higher total tax payable if the net income exceeds Rp. 540 million. For taxpayers with a net income below this level, total income tax payable is re-duced by tax rate reduction in the Rp. 25-50 million income bracket and introduction of two new progression zones for the income brackets from Rp. 50-100 million and Rp. 100-200 million. In absolute figures, the relief is most pronounced for net incomes between Rp. 150-250 million. Tax payable in this income range is reduced by some Rp. 15 million. In relative terms, taxpayers with a net income below Rp. 100 million benefit most. Their total tax payable is reduced by 50% or more. Figure 1 on the following page illustrates these effects of the 2000 tax reform in more detail.1

Figure 3: Income Tax Payable by Individual Tax Payers, Before and After the Tax Re-form 2000

The vast majority of SME operate as sole trader and are therefore taxed as individual tax payers, Less than 4% of the respondents to the TA's survey indicated a turnover of more than Rp. 1,5 billion. It is therefore fair to assume that most SME generate net incomes be-low Rp. 250 million and benefit significantly from the 2000 tax reform.

1 In order to simplify tabulation, Rp. 5 million total tax free allowance before and Rp. 10 million total tax free allowance

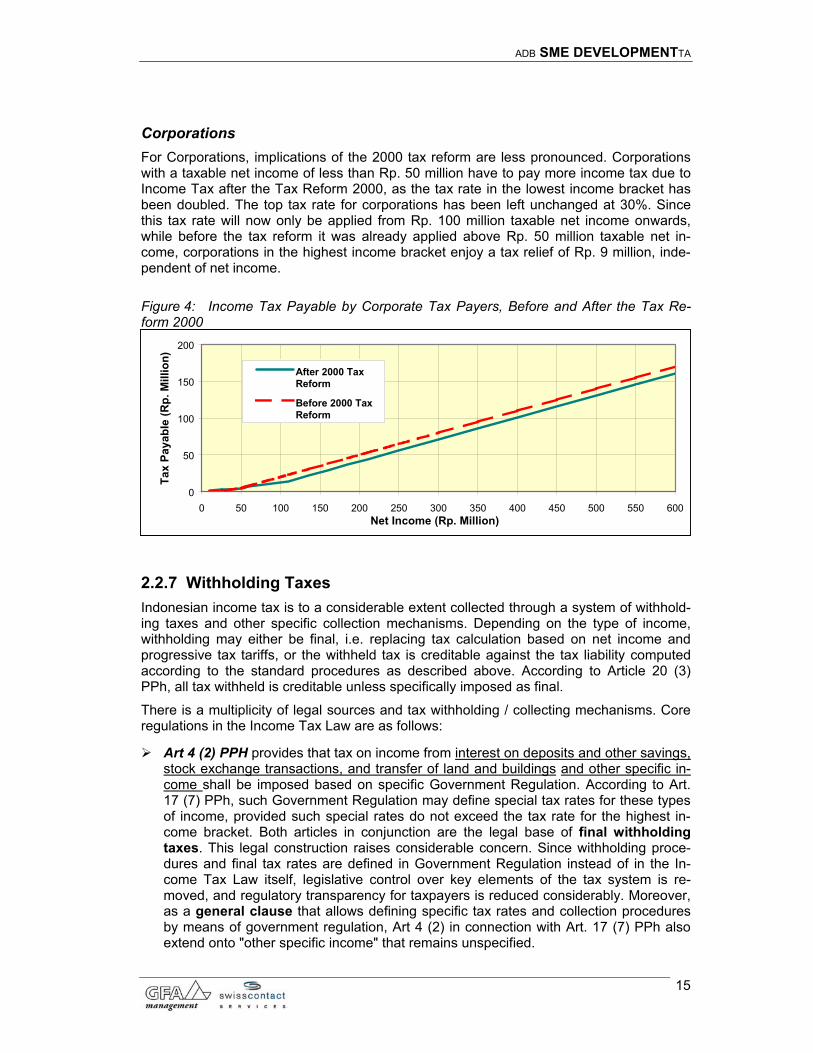

Corporations For Corporations, implications of the 2000 tax reform are less pronounced. Corporations with a taxable net income of less than Rp. 50 million have to pay more income tax due to Income Tax after the Tax Reform 2000, as the tax rate in the lowest income bracket has been doubled. The top tax rate for corporations has been left unchanged at 30%. Since this tax rate will now only be applied from Rp. 100 million taxable net income onwards, while before the tax reform it was already applied above Rp. 50 million taxable net in-come, corporations in the highest income bracket enjoy a tax relief of Rp. 9 million, inde-pendent of net income.

Figure 4: Income Tax Payable by Corporate Tax Payers, Before and After the Tax Re-form 2000

2.2.7 Withholding Taxes Indonesian income tax is to a considerable extent collected through a system of withhold-ing taxes and other specific collection mechanisms. Depending on the type of income, withholding may either be final, i.e. replacing tax calculation based on net income and progressive tax tariffs, or the withheld tax is creditable against the tax liability computed according to the standard procedures as described above. According to Article 20 (3) PPh, all tax withheld is creditable unless specifically imposed as final.

There is a multiplicity of legal sources and tax withholding / collecting mechanisms. Core regulations in the Income Tax Law are as follows:

Art 4 (2) PPH provides that tax on income from interest on deposits and other savings, stock exchange transactions, and transfer of land and buildings and other specific in-come shall be imposed based on specific Government Regulation. According to Art. 17 (7) PPh, such Government Regulation may define special tax rates for these types of income, provided such special rates do not exceed the tax rate for the highest in-come bracket. Both articles in conjunction are the legal base of final withholding taxes. This legal construction raises considerable concern. Since withholding proce-dures and final tax rates are defined in Government Regulation instead of in the In-come Tax Law itself, legislative control over key elements of the tax system is re-moved, and regulatory transparency for taxpayers is reduced considerably. Moreover, as a general clause that allows defining specific tax rates and collection procedures by means of government regulation, Art 4 (2) in connection with Art. 17 (7) PPh also extend onto "other specific income" that remains unspecified.

Art 21 PPh stipulates that "Income Tax in connection with work, services or activities … (of) a resident individual Taxpayer" shall be withheld by the employer, or, as far as pensions are concerned, the pension fund or comparable body. Tax withholding under this article also extends towards employment of professionals performing independent work for corporate taxpayers, other legal bodies or the government.

Art 22 PPh entitles the Minister of Finance to "designate government treasurers to collect taxes in connection with payment for delivery of goods", and to "designate cer-tain bodies to collect tax from a tax payer conducting activities in the import sector or business activities in other sectors". From a systematic perspective, this article is of major concern, since it allows tax collection based on tax-deductible expenditure, irre-spectively of whether this expenditure will result in taxable income or not. Moreover, the law does not stipulate any formal requirements (e.g. a government or ministerial decree) for such 'designation', which implies that respective regulation also does not have to be published. Tax withholding and collection established in relation to this arti-cle is reported to include tax collection from importers based on the CIF import value, as well as tax collection by manufacturers of certain commodities (cigarettes, sugar, flour, cement, steel, automotives, petrol) on behalf of their products' distributors and users1. Whether the tax withheld / collected in relation to this article is final or credit-able could not be established.