35

14 April 2016 BCM Anthony Woolley Proposed tax legislation revision

| Date post: | 18-Feb-2017 |

| Category: |

Business |

| Upload: | the-business-council-of-mongolia |

| View: | 135 times |

| Download: | 3 times |

14 April 2016

BCM

Anthony Woolley

Proposed tax legislation revision

Hogan Lovells | 2

• The need for tax reform

• Tax reform – Phase I (2007)

• Tax reform – Phase II (2015 - onwards)

• Phase II - proposed legislation for revision

– General Tax Law

– Corporate Income Tax Law

– Personal Income Tax Law

• Revision to VAT Law and Customs Duty and Tariffs Law

• Law on Customs Duty Exemptions

Table of contents

| 3 Hogan Lovells

• Since 1990, over 100 laws were adopted with regard to taxation

• 46 of these laws have repealed

• 55 laws are currently in effect

• Amendments to tax legislation

– 53% related to state stamp duty

– 22% relate to tax exemptions

• Amendments to tax legislation

– Creation of business-friendly environment

– Simplicity, equality and sustainability

Evolution of the current tax regime

| 4 Hogan Lovells

• Introduced "4 x 10%"

– Value added tax rate – 10% (reduction from 15%)

– Personal income tax rate – 10% (flat rate from 3 staged progressive taxation)

– Corporate income tax rate – 10% (from 15%)

– Social insurance premium rate – 10% (reduced from 29% and 19%)

Tax reform Phase I - 2007

Need for the tax reform

| 5 Hogan Lovells

• 2012 - 2016 Government Action Plan

– "All Mongolians employed and having a proper source of income"

– "To bring the public private partnership to a new level and create a business friendly

environment"

• Phase II Tax reform objectives included

– Risk management system to be introduced in respect of inspections

Tax reform

| 6 Hogan Lovells

• VAT Law recently revised

• Proposed revisions to tax legislation

– General Taxation Law

– Corporate Income Tax Law ("CIT")

– Personal Income Tax Law ("PIT")

• Revision to the Customs Duty and Tariffs Law, VAT Law and

Budget Law

• Law on Customs Duty Exemption

Tax reform Phase II

Hogan Lovells | 7

• Current regime no longer meet social needs

• Tax disputes: 2008 - 2012

– tax disputes involving MNT 726.135.2 million relating to 274 taxpayers

– 66.8% of the disputes were decided in taxpayer's favour

• World Bank - Doing Business "Paying taxes" ranking

– 2012: 57th

– 2013: 70th

Tax Reform

Hogan Lovells | 8

• Revised law

– Listed for agenda for 11 April 2016

– 10 chapters

– 60 articles

• Current law

– Adopted 20 May 2006

– 9 chapters

– 76 articles

General Tax Law ("GTL")

Hogan Lovells | 9

• Reflects the merging of former General Tax Authority and

Customs General Authority

• Revised, consolidated and introduced new terminology:

– taxpayer, tax re-imposition, tax re-imposition act, authorised representative (of

taxpayer), affiliated entities (Company Law)

– "actions without a definite business purpose" (tax evasion)

– tax evasion within the framework of the law (manipulation of tax exemption and partial

relief policies etc.)

– Principle of actual price determination (affiliated entities transaction)

– Detailed sample pricing method

Draft General Tax Law

Hogan Lovells | 10

• Tax to include inter alia:

– Asset taxes (immovable property, firearms, vehicles)

– Waste management services

– Fees for utilisation of natural resources other than minerals

• Tax support

– Tax stabilisation of tax as per relevant laws (Investment Law)

– Reimbursement of tax payments in certain circumstances (student dependents, VAT)

– Tax holiday of exemption or discount for certain purposes and definite period

• Taxpayer registration/updating of details – 21 days (now 14 / 20)

Draft General Tax Law

Hogan Lovells | 11

• Taxpayer rights

– Right to file a complaint with Tax Dispute Committee

– Right to provide relevant evidence and grounds in defence of an allegatgion

– Benefit from a simplified tax registration regime

• Taxpayer obligations

– Clarifies sales terminal requirement for all taxpayers under the VAT Law

– Obligation to inform the relevant tax authority in the event the owner/shareholder of the

legal entity "directly" or "indirectly" changes (Article 14.1.15)

Draft General Tax Law

Hogan Lovells | 12

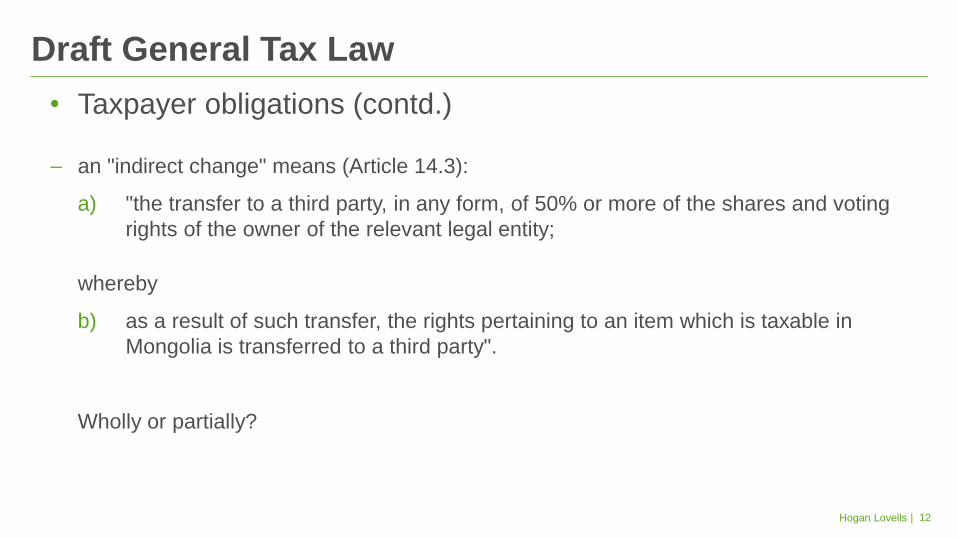

• Taxpayer obligations (contd.)

– an "indirect change" means (Article 14.3):

a) "the transfer to a third party, in any form, of 50% or more of the shares and voting

rights of the owner of the relevant legal entity;

whereby

b) as a result of such transfer, the rights pertaining to an item which is taxable in

Mongolia is transferred to a third party".

Wholly or partially?

Draft General Tax Law

Hogan Lovells | 13

• Clarification of tax inspectors' rights

– Right of entry into premises

requires the permission of the "management officer" of the relevant tax authority

must be in the presence of:

o eyewitnesses; and

o the taxpayer or his/her/their authorised representative

– Summon the taxpayer and his "client/customer" (харилцагч)

– Demand that other taxpayers who have had interactions with the taxpayer provide information relating to the income, expenses and assets of the relevant taxpayer being audited

Draft General Tax Law

Hogan Lovells | 14

• Tax inspectors – prohibitions

– Disclose confidential information

– Disclose to the taxpayer any acts which have not yet been approved

– Over/undercharge those taxpayers who benefit from an Investment Agreement with the GoM

– undertake representation roles, within 2 years of leaving the employment with tax authority

– contact and/or pressure taxpayers re. matters not related to tax (such as persuade to purchase

goods/services)

Draft General Tax Law

Hogan Lovells | 15

• Improvements to tax database

– information on decisions of the Tax Dispute Resolution Committee and courts

– information from relevant authorities

– information obtained from third parties

– tax payment history

• Systemisation of tax inspectors' decisions

– printed on pro forma forms as adopted by the central tax authority

– each to contain unique numbers and be registered in the database

Draft General Tax Law

Hogan Lovells | 16

• Tax imposition

– 1 week extension if tax payment and reporting dates fall during public holidays

– taxpayer may amend a tax report already submitted unless tax inspection has started

– Points for review of tax reports have been expanded (from 6 to 10)

– Within 5 working days of such review, discrepancies in the information shall be notified to the taxpayer

– The taxpayer must make necessary changes or provide an explanation within 5 working days

– Within 5 days a receipt of response from the taxpayer, tax authority may:

agree to the taxpayer's response; and

in the event of disagreement, inform the risk officer at the tax authority and inform the taxpayer re. the same

Draft General Tax Law

Hogan Lovells | 17

• Tax inspections/audits

– Must be risk-based (central tax authority is to adopt detailed regulations)

– Potential conflicts of interest must be taken into consideration when assigning tax

inspectors

– Entry into premises must take place during office hours but may be unannounced

– Entry into premises/property includes inspection of computer and similar devices

– Rights of ownership must be "honoured"

– The owner of the property, his/her authorised representative or local governance body

representative must be present; however absence shall not prevent the investigation

General Tax Law

Hogan Lovells | 18

• Revised Law

– Listed on agenda for 11 April 2016

– 10 chapters

– 60 articles

• Current Law

– Adopted 29 June 2006

– 9 chapters

– 76 articles

Corporate Income Tax Law ("CIT Law")

Hogan Lovells | 19

• Not For Profits

– Those entities whose principal activities are not for profit, but who conduct business

activities, are now subject to CIT

• Permanent establishments

– Permanent establishments of foreign entities are subject to CIT under the current law

– Draft law now defines "permanent establishments" as a permanent establishment of a

corporate entity of a country with whom Mongolia has entered into a DTT

Draft Corporate Income Tax Law

Hogan Lovells | 20

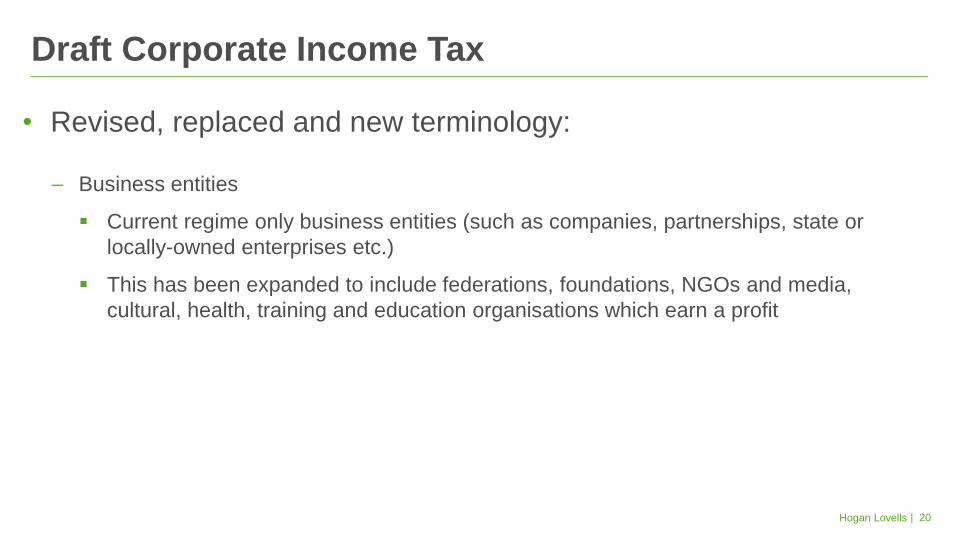

• Revised, replaced and new terminology:

– Business entities

Current regime only business entities (such as companies, partnerships, state or

locally-owned enterprises etc.)

This has been expanded to include federations, foundations, NGOs and media,

cultural, health, training and education organisations which earn a profit

Draft Corporate Income Tax

Hogan Lovells | 21

• Mongolian-sourced income (Article 4.1.8)

– Income from goods and services sold in Mongolia by non-resident taxpayer

– Income from organising of culture, sports and other event in Mongolia by non-resident taxpayer

– Income generated from sale of tangible and nontangible goods in his/her possession, usage, proprietorship in Mongolia by non-resident taxpayer

– Income generated from sales of tangible and intangible goods and rights pertaining to the same non-resident taxpayer

– Income generated from share sales by/of resident taxpayer

– Income generated from dividends paid by resident taxpayer

– Income generated from interest and guarantee paid by state, local government and resident taxpayer

– Income generated from goods and services sold in Mongolia to resident taxpayer by non-resident taxpayer

– Other income similar to the same

Draft Corporate Income Tax Law

Corporate Income Tax – Taxable Income

22

• Operational income - new categories

– Income from similar activities

– environmental restoration fund amounts repaid to the licence holder

• Assets income - new categories:

– Fees for use of experimental equipment in industry, trade and science

– Fee for right to conduct business (Article 10.2.7): MNT 500,000

Draft Corporate Income Tax

• Asset sales income - new categories:

– Current law:

sales of movable property; and

sales of immovable property

– Revised law:

sales of immovable property;

sales of rights; and

sales from tangible property and intangible assets

23

Hogan Lovells | 24

Current law

• For the purposes of the CIT Law, affiliated parties of a business entity

means those persons that:

– hold 20% or more of the issued common shares of such business entity;

– are entitled to receive 20% or more of dividends and profit distributions of such business

entity; or

– are entitled to appoint 20% or more of management personnel of such business entity or

determine policies and directions of its operations.

Affiliated parties

Corporate Income Tax Law

Hogan Lovells | 25

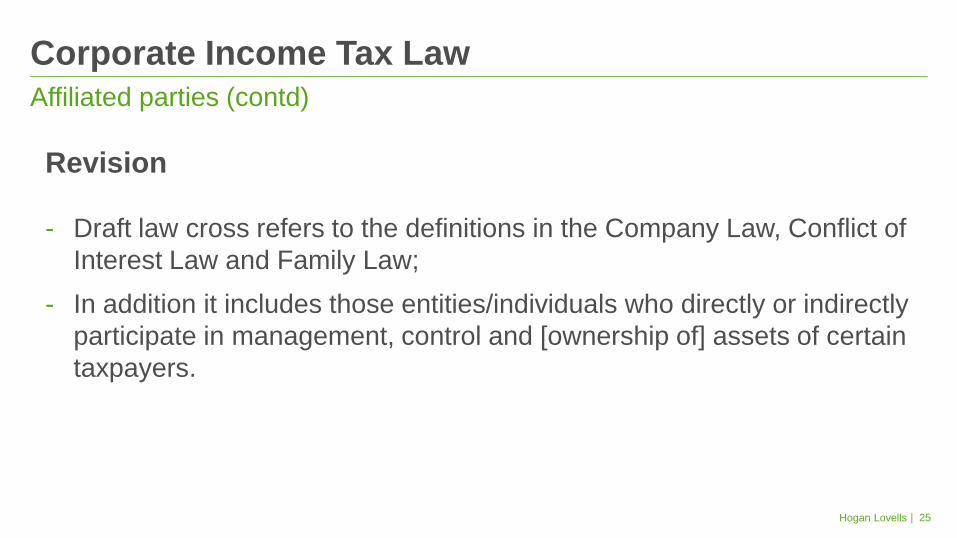

Revision

- Draft law cross refers to the definitions in the Company Law, Conflict of

Interest Law and Family Law;

- In addition it includes those entities/individuals who directly or indirectly

participate in management, control and [ownership of] assets of certain

taxpayers.

Affiliated parties (contd)

Corporate Income Tax Law

Hogan Lovells | 26

• Draft Law

– Income MNT 0 - 10 billion: 10%

– That portion over 10 billion: 25%

• Current Law

– Income MNT 0 - 3 billion: 10%

– That portion over 3 billion: 25%

Changes to standard tax rates

Corporate Income Tax Law

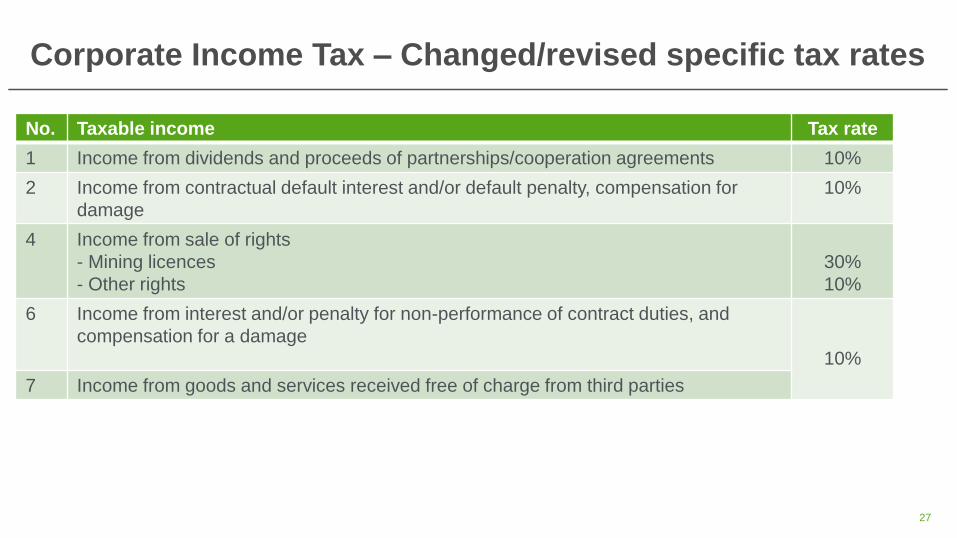

Corporate Income Tax – Changed/revised specific tax rates

No. Taxable income Tax rate

1 Income from dividends and proceeds of partnerships/cooperation agreements 10%

2 Income from contractual default interest and/or default penalty, compensation for

damage

10%

4 Income from sale of rights

- Mining licences

- Other rights

30%

10%

6 Income from interest and/or penalty for non-performance of contract duties, and

compensation for a damage

10%

7 Income from goods and services received free of charge from third parties

27

Corporate Income Tax – Changed/revised specific tax rates

No. Taxable income Tax rate

9 Business entities that are resident in Mongolia*

10% & 2%

10 Withholding tax on income earned within Mongolia or Mongolian-sourced income of

tax payers without permanent establishment

20%

28

Corporate Income Tax – Withholding tax regime

• 20% withholding tax for tax payers without a permanent establishment:

– income earned within Mongolia or

– certain Mongolian-sourced income:

– Income from goods and services sold in Mongolia by non-resident taxpayer

– Income from organising of culture, sports and other event in Mongolia by non-resident taxpayer

– Income generated from sale of tangible and nontangible goods in his/her possession, usage,

proprietorship in Mongolia by non-resident taxpayer

– Income generated from sales of tangible and intangible goods and rights pertaining to the same

non-resident taxpayer

– Income generated from goods and services sold in Mongolia to resident taxpayer by non-

resident taxpayer

– Similar incomes

29

Losses carried forward

• Current law:

– Infrastructure and mining: 4 – 8 years

– Other sectors: 2 years

- Revised law: 5 years

- Exclusion: does not apply to foreign permanent establishments of

Mongolia-incorporated entities.

30

Hogan Lovells | 31

• Exclusion: Article 27.9 - payment of fee (MNT 500,000) for dormant entities – Reporting for shall start the year following the year of incorporation

– Reporting by 10 February

– Simplified tax report shall be submitted once a year (Article 27.10)

• Tax payments – threshold-based – Income of MNT 1.5 billion or more – quarterly reporting to be submitted within 20

days of the next quarter

– Income of MNT 50 million - 1.5 billion semi-annual reporting by 10 February and 20 July (Article 27.5)

Reporting

Corporate Income Tax Law

Hogan Lovells | 32

• Tax payments – threshold-based (contd)

– Income MNT 50 million or less (Article 27.6)

now may report semi-annually by 10 February and 20 July (Article 27.5)

Reporting

Corporate Income Tax Law

Draft Corporate Income Tax Law

Tax exemptions

• Current CIT Law contains multiple tax exemptions

• Revised law exemptions reduced to:

– interest accrued on bonds issued by the government or Development Bank;

– income of legal entity with more than 25 employees of whom at least 2/3 are

handicapped;

– income from sales of technique and equipment that are environmentally friendly, efficient

in terms of natural resources usage, reduces environmental pollution and waste; and

– income from sale of products allocated to the taxpayer as per the relevant product

sharing agreement in the petroleum sector (GoM to determine)

33

Draft Corporate Income Tax Law

Tax credits

• For those legal entities whose resident in Mongolia and whose income is below MNT 1.5 billion, 90% of the tax shall be credited

• The relevant taxpayer shall benefit from the credit in the following year

• New/revised exclusions:

– Minerals extraction, import, export

– Petroleum extraction, import, export

– Mobile communications operations

– Banking and finance

– Alcohol producers and sellers

• Such 90% shall not apply to dormant entities who pay MNT 500,000

34

| 35 Hogan Lovells

• Tax regime is undergoing major changes

• Political circumstances are affecting the legal development

• Tax reform Phase II, first part - VAT Law

- Amendment to PIT Law

• Tax reform Phase II, second part

- General Tax Law – more clarity provided

- CIT Law – amendments and clarifications

• Overall message is business-friendly tax regime

• Real implications to be tested once proposed laws and adopted and implemented

Conclusion

![Fisheries Management (General) Regulations 2017extwprlegs1.fao.org/docs/pdf/sa180032.pdfVersion: 15.1.2018 [17.1.2018] This version is not published under the Legislation Revision](https://static.documents.pub/doc/80x56/5fe894511e840f021962251f/fisheries-management-general-regulations-version-1512018-1712018-this-version.jpg)