Tackling consumer confusion and giving retirees what they want. How can the wishes of consumers be supported by the pension reforms? Wednesday 14 th January 2015 This research has been supported by Just Retirement, LV, Partnership, Key Retirement and EY #pensionfreedoms

Transcript

Tackling consumer confusion and

giving retirees what they want.

How can the wishes of consumers be

supported by the pension reforms?

Wednesday 14th January 2015

This research has been supported by Just Retirement, LV, Partnership, Key Retirement and EY

#pensionfreedoms

Welcome

Lawrence ChurchillTrustee

ILC-UK

#pensionfreedoms

This research has been supported by Just Retirement, LV, Partnership, Key Retirement and EY

Ben FranklinSenior Research Fellow

ILC-UK

#pensionfreedoms

This research has been supported by Just Retirement, LV, Partnership, Key Retirement and EY

Making the system fit for purpose

How consumer appetite for secure income could be supported by the pension reforms

Ben Franklin, Senior Research Fellow, International Longevity Centre@ilcuk @bjafranklin

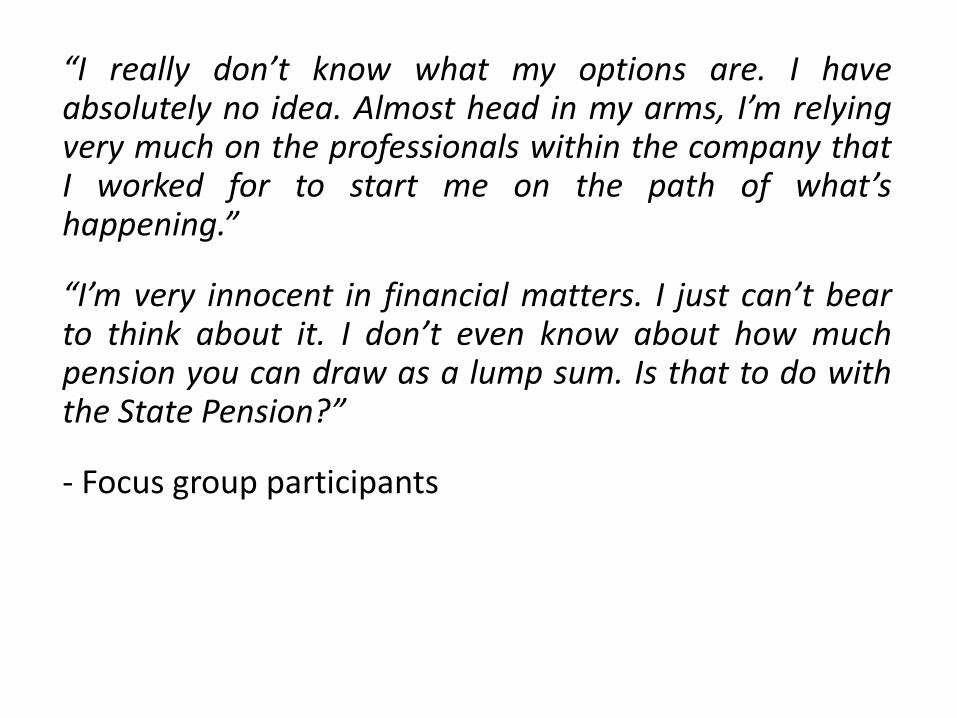

“I really don’t know what my options are. I haveabsolutely no idea. Almost head in my arms, I’m relyingvery much on the professionals within the company thatI worked for to start me on the path of what’shappening.”

“I’m very innocent in financial matters. I just can’t bearto think about it. I don’t even know about how muchpension you can draw as a lump sum. Is that to do withthe State Pension?”

- Focus group participants

Building an evidence base

The problem

• Lack of consumer research tapping into consumerpreferences in light of new pension freedoms.

What did we do?

• Focus group sessions to identify possible issues facing thoseapproaching retirement.

• Commissioned YouGov survey of over 5,000 people aged55-70 not yet retired and yet to draw on their privatepension wealth. Approx 30 questions.

Towards a profile of those affected by the reforms

Pension seen as way to deliver income

Risk averse

Low level of financial capability

Positive about Guidance

Financial advice seen as key source of support

but many remain wary about accessing it

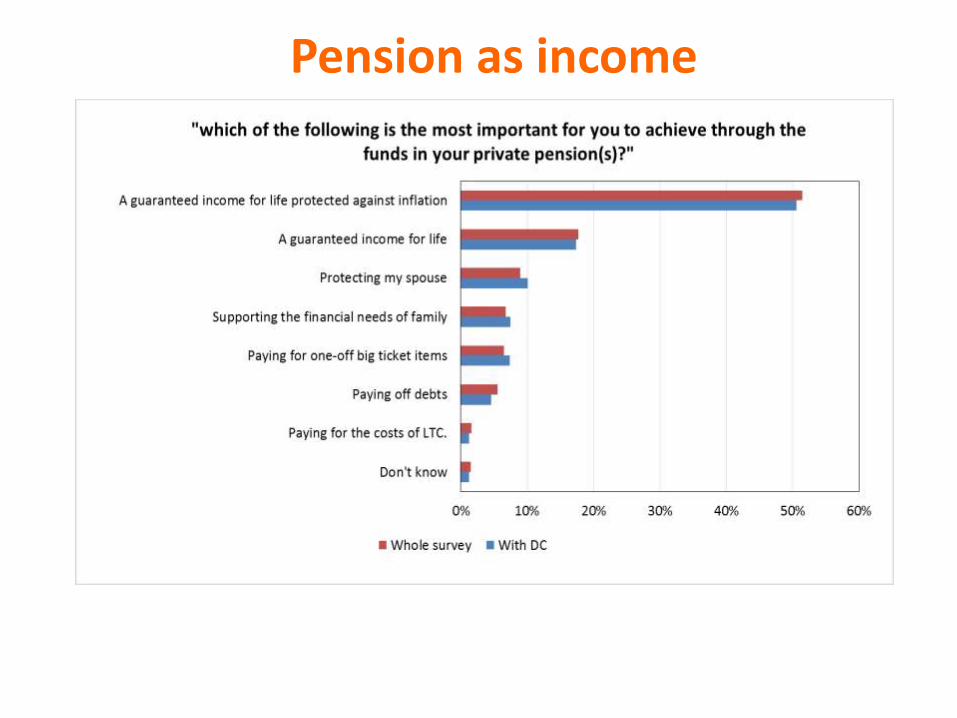

Pension as income

…pension as income (continued)

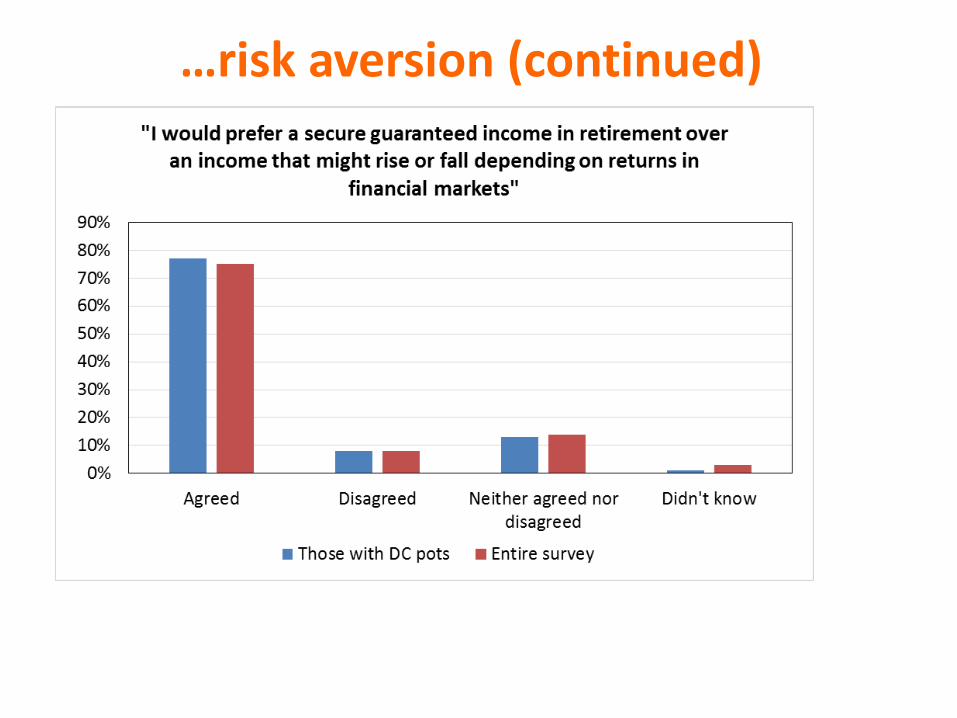

Risk aversion

…risk aversion (continued)

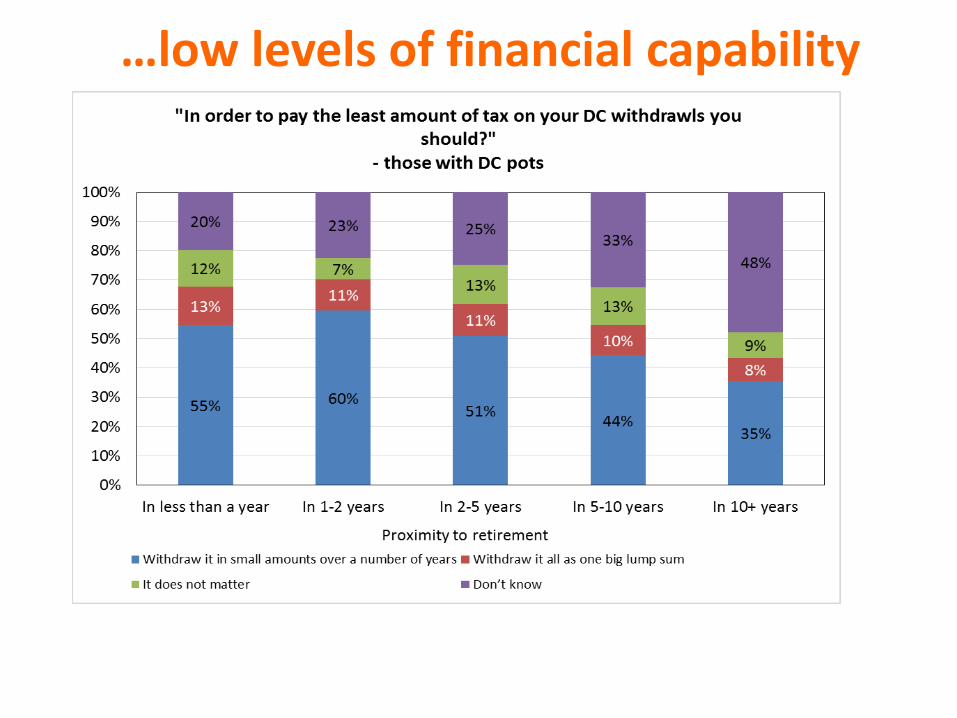

Low levels of financial capability

…low levels of financial capability

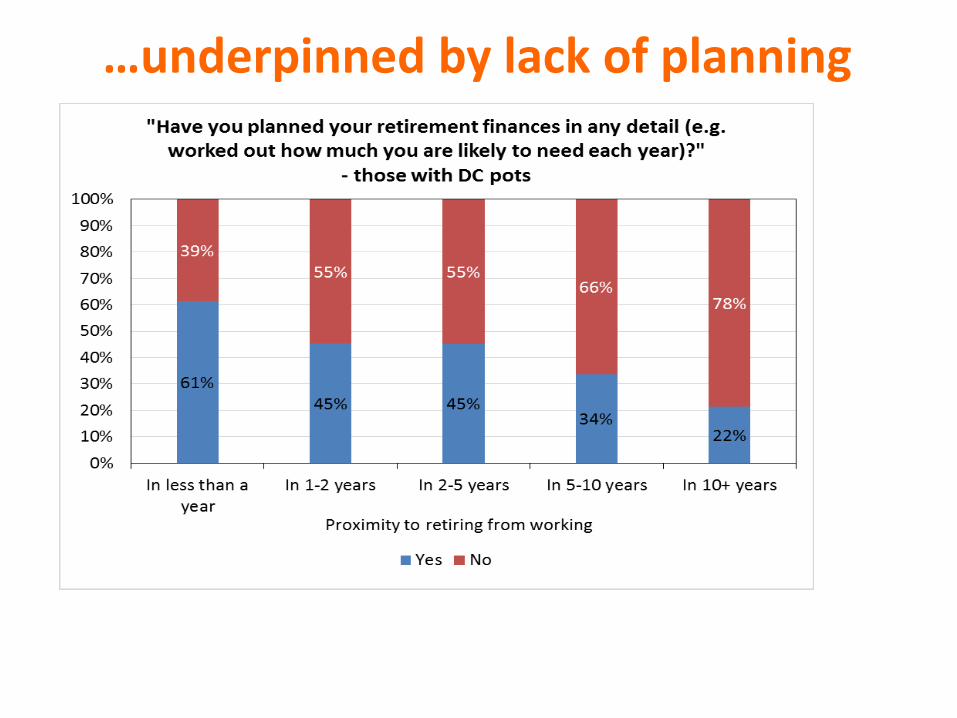

…underpinned by lack of planning

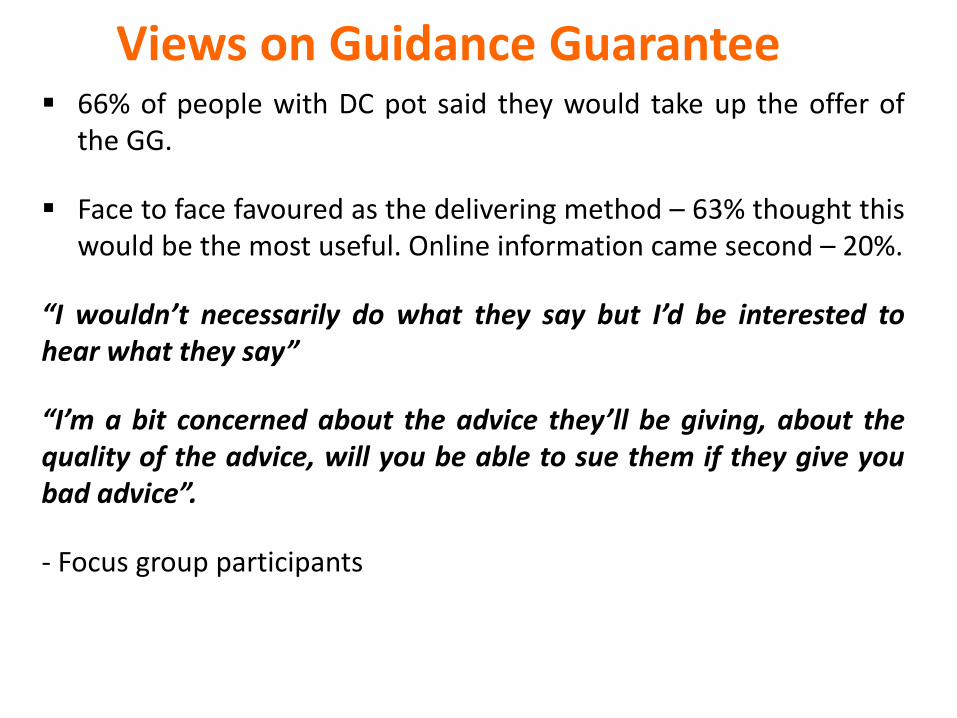

Views on Guidance Guarantee 66% of people with DC pot said they would take up the offer of

the GG.

Face to face favoured as the delivering method – 63% thought thiswould be the most useful. Online information came second – 20%.

“I wouldn’t necessarily do what they say but I’d be interested tohear what they say”

“I’m a bit concerned about the advice they’ll be giving, about thequality of the advice, will you be able to sue them if they give youbad advice”.

- Focus group participants

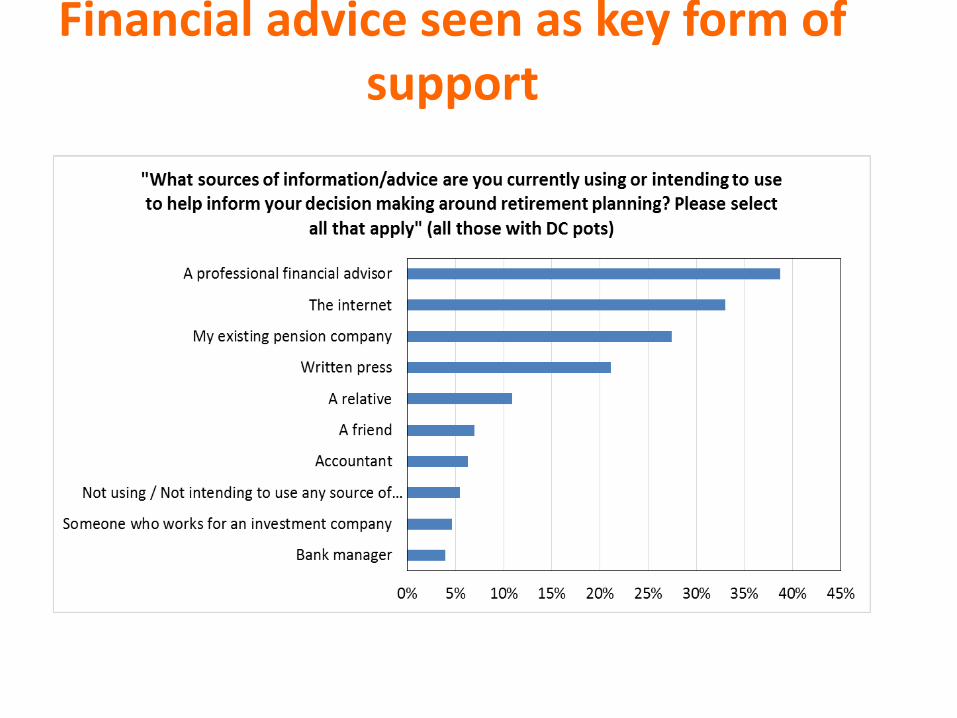

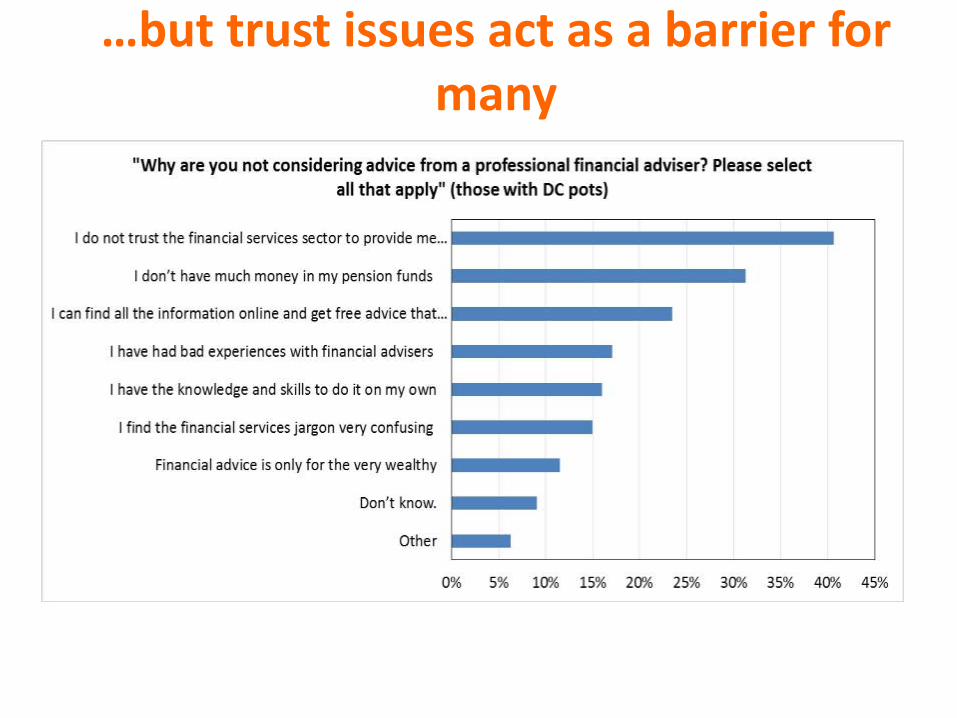

Financial advice seen as key form of support

…but trust issues act as a barrier for many

What are the implications?• Risk of mismatch between consumer preferences and the

choices they finally make.

• Driven by low financial capability, lack of planning and failure to seek professional financial advice.

• Guidance will be critical but will be far from sufficient given this consumer profile.

• Contingency plans urgently needed to support those who do not take up guidance and those who do but may still make poor decisions.

Many thanks

Ben FranklinSenior Research FellowInternational Longevity Centre - [email protected]: @ilcuk